Combo 2/20 EMA & Bandpass Filter by TamarokDescription:

This strategy combines a 2/20 exponential moving average (EMA) crossover with a custom bandpass filter to generate buy and sell signals.

Use the Fast EMA and Slow EMA inputs to adjust trend sensitivity, and the Bandpass Filter Length, Delta, and Zones to fine-tune momentum turns.

Signals occur when both EMA and BPF agree in direction, with optional reversal and time filters.

How to use:

1. Add the script to your chart in TradingView.

2. Adjust the EMA and BP Filter parameters to match your asset’s volatility.

3. Enable ‘Reverse Signals’ to trade counter-trend, or use the time filter to limit sessions.

4. Set alerts on Long Alert and Short Alert for automated notifications.

Inspiration:

Based on HPotter’s original combo strategy (Stocks & Commodities Mar 2010).

Updated to Pine Script v6 with streamlined code and alerts.

WARNING:

For purpose educate only

Filter

Kent Directional Filter🧭 Kent Directional Filter

Author: GabrielAmadeusLau

Type: Filter

📖 What It Is

The Kent Directional Filter is a directionality-sensitive smoothing tool inspired by the Kent distribution, a probability model used to describe directional and elliptical shapes on a sphere. In this context, it's repurposed for analyzing the angular trajectory of price movements and smoothing them for actionable insights.

It’s ideal for:

Detecting directional bias with probabilistic weighting

Enhancing momentum or trend-following systems

Filtering non-linear price action

🔬 How It Works

Price Angle Estimation:

Computes a rough angular shift in price using atan(src - src ) to estimate direction.

Kent Distribution Weighting:

κ (kappa) controls concentration strength (how sharply it prefers a direction).

β (beta) controls ellipticity (bias toward curved vs. linear moves).

These parameters influence how strongly the indicator favors movements at ~45° angles, simulating a directional “lens.”

Smoothing:

A Simple Moving Average (SMA) is applied over the raw directional probabilities to reduce noise and highlight the underlying trend signal.

⚙️ Inputs

Source: Price series used for angle calculation (default: close)

Smoothing Length: Window size for the moving average

Pi Divisor: Pi / 4 would be 45 degrees, you can change the 4 to 3, 2, etc.

Kappa (κ): Controls how focused the directionality is (higher = sharper filter)

Beta (β): Adds curvature sensitivity; higher values accentuate asymmetrical moves

🧠 Tips for Best Results

Use κ = 1–2 for moderate directional filtering, and β = 0.3–0.7 for smooth elliptical bias.

Combine with volume-based indicators to confirm breakout strength.

Works best in higher timeframes (1h–1D) to capture macro directional structure.

I might revisit this.

TASC 2025.07 Laguerre Filters█ OVERVIEW

This script implements the Laguerre filter and oscillator described by John F. Ehlers in the article "A Tool For Trend Trading, Laguerre Filters" from the July 2025 edition of TASC's Traders' Tips . The new Laguerre filter utilizes the UltimateSmoother filter in place of an exponential moving average (EMA) in its calculation, offering improved responsiveness and reduced lag.

█ CONCEPTS

As Ehlers explains in his article, the Laguerre filter is a form of transversal filter . A transversal filter calculates an output signal using a tapped delay line . It creates multiple delayed versions of an input signal, applies weight to each delay, and then calculates their sum to generate the filtered result.

The Laguerre filter's structure relies on Laguerre polynomials — solutions to a differential equation solved by Edmond Laguerre in the 1800s. When Ehlers analyzed the formula for these polynomials on discrete systems (e.g., financial time series), he found that the first term's expression corresponds to an EMA response, and all subsequent terms correspond to an all-pass response. In contrast to other filter types, an all-pass filter produces phase shift (i.e., delay) in an input signal's components without affecting its amplitude.

Ehlers observed that these characteristics of Laguerre polynomials make them suitable for use in a transversal filter structure, and thus the Laguerre filter was born. However, he notes that EMAs are not great filters in general. As such, to improve on the Laguerre filter's design, Ehlers modified it by replacing the EMA term with his UltimateSmoother filter. The resulting Laguerre filter has significantly reduced lag, achieving a tighter response to market fluctuations while maintaining smoothness. Ehlers suggests that traders can analyze crossings between the UltimateSmoother and this Laguerre filter, or those between two Laguerre filters of different order, for helpful buy and sell signals.

In addition to the Laguerre filter, Ehlers derived a smooth, low-lag oscillator based on the difference between the first and second terms in the modified filter structure, scaled by the root mean square (RMS). The resulting oscillator provides an alternative filtered representation of market data, which can help traders identify swing and mean-reversion signals.

█ USAGE

This indicator calculates both the Laguerre filter and the Laguerre oscillator described in Ehlers' article. It displays the Laguerre filter on the main chart pane and the oscillator in a separate pane.

Users can control the behavior of the filter and oscillator with the inputs in the "Settings/Inputs" tab:

The "Period" input defines the critical period of the UltimateSmoother used in the Laguerre filter and oscillator calculations. Its default value is 30.

The "Gamma" input determines the weighting behavior of the Laguerre filter and oscillator. It accepts a positive value between 0 and 1. Use a lower value for quicker responsiveness to market changes, and a higher value for trends. The default value is 0.5.

The "RMS length" input determines the length of the RMS calculation for oscillator normalization. The default value is 100 bars.

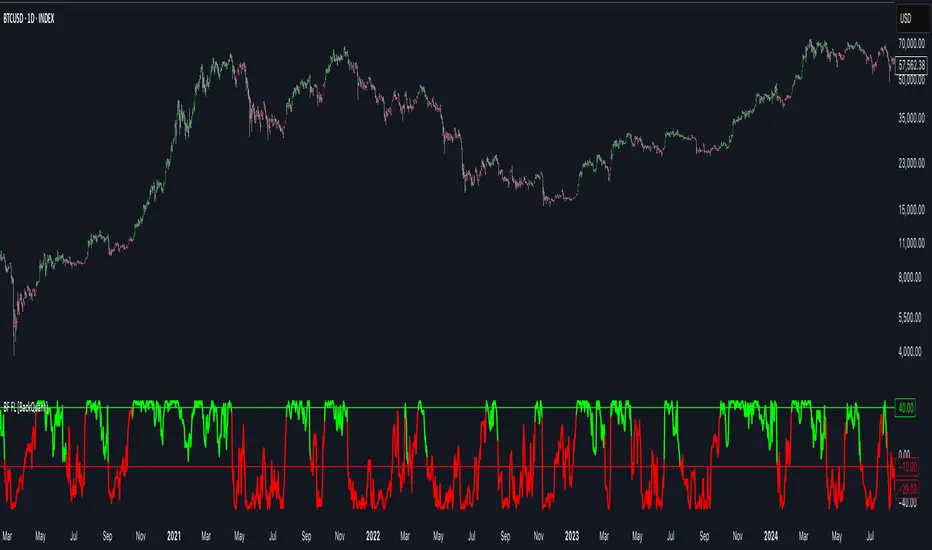

Bilateral Filter For Loop [BackQuant]Bilateral Filter For Loop

The Bilateral Filter For Loop is an advanced technical indicator designed to filter out market noise and smooth out price data, thus improving the identification of underlying market trends. It employs a bilateral filter, which is a sophisticated non-linear filter commonly used in image processing and price time series analysis. By considering both spatial and range differences between price points, this filter is highly effective at preserving significant trends while reducing random fluctuations, ultimately making it suitable for dynamic trend-following strategies.

Please take the time to read the following:

Key Features

1. Bilateral Filter Calculation:

The bilateral filter is the core of this indicator and works by applying a weight to each data point based on two factors: spatial distance and price range difference. This dual weighting process allows the filter to preserve important price movements while reducing the impact of less relevant fluctuations. The filter uses two primary parameters:

Spatial Sigma (σ_d): This parameter adjusts the weight applied based on the distance of each price point from the current price. A larger spatial sigma means more smoothing, as further away values will contribute more heavily to the result.

Range Sigma (σ_r): This parameter controls how much weight is applied based on the difference in price values. Larger price differences result in smaller weights, while similar price values result in larger weights, thereby preserving the trend while filtering out noise.

The output of this filter is a smoothed version of the original price series, which eliminates short-term fluctuations, helping traders focus on longer-term trends. The bilateral filter is applied over a rolling window, adjusting the level of smoothing dynamically based on both the distance between values and their relative price movements.

2. For Loop Calculation for Trend Scoring:

A for-loop is used to calculate the trend score based on the filtered price data. The loop compares the current value to previous values within the specified window, scoring the trend as follows:

+1 for upward movement (when the filtered value is greater than the previous value).

-1 for downward movement (when the filtered value is less than the previous value).

The cumulative result of this loop gives a continuous trend score, which serves as a directional indicator for the market's momentum. By summing the scores over the window period, the loop provides an aggregate value that reflects the overall trend strength. This score helps determine whether the market is experiencing a strong uptrend, downtrend, or sideways movement.

3. Long and Short Conditions:

Once the trend score has been calculated, it is compared against predefined threshold levels:

A long signal is generated when the trend score exceeds the upper threshold, indicating that the market is in a strong uptrend.

A short signal is generated when the trend score crosses below the lower threshold, signaling a potential downtrend or trend reversal.

These conditions provide clear signals for potential entry points, and the color-coding helps traders quickly identify market direction:

Long signals are displayed in green.

Short signals are displayed in red.

These signals are designed to provide high-confidence entries for trend-following strategies, helping traders capture profitable movements in the market.

4. Trend Background and Bar Coloring:

The script offers customizable visual settings to enhance the clarity of the trend signals. Traders can choose to:

Color the bars based on the trend direction: Bars are colored green for long signals and red for short signals.

Change the background color to provide additional context: The background will be shaded green for a bullish trend and red for a bearish trend. This visual feedback helps traders to stay aligned with the prevailing market sentiment.

These features offer a quick visual reference for understanding the market's direction, making it easier for traders to identify when to enter or exit positions.

5. Threshold Lines for Visual Feedback:

Threshold lines are plotted on the chart to represent the predefined long and short levels. These lines act as clear markers for when the market reaches a critical threshold, triggering a potential buy (long) or sell (short) signal. By showing these threshold lines on the chart, traders can quickly gauge the strength of the market and assess whether the trend is strong enough to warrant action.

These thresholds can be adjusted based on the trader's preferences, allowing them to fine-tune the indicator for different market conditions or asset behaviors.

6. Customizable Parameters for Flexibility:

The indicator offers several parameters that can be adjusted to suit individual trading preferences:

Window Period (Bilateral Filter): The window size determines how many past price values are used to calculate the bilateral filter. A larger window increases smoothing, while a smaller window results in more responsive, but noisier, data.

Spatial Sigma (σ_d) and Range Sigma (σ_r): These values control how sensitive the filter is to price changes and the distance between data points. Fine-tuning these parameters allows traders to adjust the degree of noise reduction applied to the price series.

Threshold Levels: The upper and lower thresholds determine when the trend score crosses into long or short territory. These levels can be customized to better match the trader's risk tolerance or asset characteristics.

Visual Settings: Traders can customize the appearance of the chart, including the line width of trend signals, bar colors, and background shading, to make the indicator more readable and aligned with their charting style.

7. Alerts for Trend Reversals:

The indicator includes alert conditions for real-time notifications when the market crosses the defined thresholds. Traders can set alerts to be notified when:

The trend score crosses the long threshold, signaling an uptrend.

The trend score crosses the short threshold, signaling a downtrend.

These alerts provide timely information, allowing traders to take immediate action when the market shows a significant change in direction.

Final Thoughts

The Bilateral Filter For Loop indicator is a robust tool for trend-following traders who wish to reduce market noise and focus on the underlying trend. By applying the bilateral filter and calculating trend scores, this indicator helps traders identify strong uptrends and downtrends, providing reliable entry signals with minimal market noise. The customizable parameters, visual feedback, and alerting system make it a versatile tool for traders seeking to improve their timing and capture profitable market movements.

Thus following all of the key points here are some sample backtests on the 1D Chart

Disclaimer: Backtests are based off past results, and are not indicative of the future.

INDEX:BTCUSD

INDEX:ETHUSD

CRYPTO:SOLUSD

Wavelet Filter with Adaptive Upsampling [BackQuant]Wavelet Filter with Adaptive Upsampling

The Wavelet Filter with Adaptive Upsampling is an advanced filtering and signal reconstruction tool designed to enhance the analysis of financial time series data. It combines wavelet transforms with adaptive upsampling techniques to filter and reconstruct price data, making it ideal for capturing subtle market movements and enhancing trend detection. This system uses high-pass and low-pass filters to decompose the price series into different frequency components, applying adaptive thresholding to eliminate noise and preserve relevant signal information.

Shout out to Loxx for the Least Squares fitting of trigonometric series and Quinn and Fernandes algorithm for finding frequency

www.tradingview.com

Key Features

1. Frequency Decomposition with High-Pass and Low-Pass Filters:

The indicator decomposes the input time series using high-pass and low-pass filters to separate the high-frequency (detail) and low-frequency (trend) components of the data. This decomposition allows for a more accurate analysis of underlying trends, while mitigating the impact of noise.

2. Soft Thresholding for Noise Reduction:

A soft thresholding function is applied to the high-frequency component, allowing for the reduction of noise while retaining significant market signals. This function adjusts the coefficients of the high-frequency data, removing small fluctuations and leaving only the essential price movements.

3. Adaptive Upsampling Process:

The upsampling process in this script can be customized using different methods: sinusoidal upsampling, advanced upsampling, and simple upsampling. Each method serves a unique purpose:

Sinusoidal Upsample uses a sine wave to interpolate between data points, providing a smooth transition.

Advanced Upsample utilizes a Quinn-Fernandes algorithm to estimate frequency and apply more sophisticated interpolation techniques, adapting to the market’s cyclical behavior.

Simple Upsample linearly interpolates between data points, providing a basic upsampling technique for less complex analysis.

4. Reconstruction of Filtered Signal:

The indicator reconstructs the filtered signal by summing the high and low-frequency components after upsampling. This allows for a detailed yet smooth representation of the original time series, which can be used for analyzing underlying trends in the market.

5. Visualization of Reconstructed Data:

The reconstructed series is plotted, showing how the upsampling and filtering process enhances the clarity of the price movements. Additionally, the script provides the option to visualize the log returns of the reconstructed series as a histogram, with positive returns shown in green and negative returns in red.

6. Cumulative Series and Trend Detection:

A cumulative series is plotted to visualize the compounded effect of the filtered and reconstructed data. This feature helps traders track the overall performance of the asset over time, identifying whether the asset is following a sustained upward or downward trend.

7. Adaptive Thresholding and Noise Estimation:

The system estimates the noise level in the high-frequency component and applies an adaptive thresholding process based on the standard deviation of the downsampled data. This ensures that only significant price movements are retained, further refining the trend analysis.

8. Customizable Parameters for Flexibility:

Users can customize the following parameters to adjust the behavior of the indicator:

Frequency and Phase Shift: Control the periodicity of the wavelet transformation and the phase of the upsampling function.

Upsample Factor: Adjust the level of interpolation applied during the upsampling process.

Smoothing Period: Determine the length of time used to smooth the signal, helping to filter out short-term fluctuations.

References

Enhancing Cross-Sectional Currency Strategies with Context-Aware Learning to Rank

arxiv.org

Daubechies Wavelet - Wikipedia

en.wikipedia.org

Quinn Fernandes Fourier Transform of Filtered Price by Loxx

Note on Usage for Mean-Reversion Strategy

This indicator is primarily designed for trend-following strategies. However, by taking the inverse of the signals, it can be adapted for mean-reversion strategies. This involves buying underperforming assets and selling outperforming ones. Caution: This method may not work effectively with highly correlated assets, as the price movements between correlated assets tend to mirror each other, limiting the effectiveness of mean-reversion strategies.

Final Thoughts

The Wavelet Filter with Adaptive Upsampling is a powerful tool for traders seeking to improve their understanding of market trends and noise. By using advanced wavelet decomposition and adaptive upsampling, this system offers a clearer, more refined picture of price movements, enhancing trend-following strategies. It’s particularly useful for detecting subtle shifts in market momentum and reconstructing price data in a way that removes noise, providing more accurate insights into market conditions.

WLSMA: fast approximation🙏🏻 Sup TV & @alexgrover

O(N) algocomplexity, just one loop inside. No, you can't do O(1) @ updates in moving window mode, only expanding window will allow that.

Now I have time series & stats models of my own creation, nowhere else available, just TV and my github for now, ain’t no legacy academic industry I always have fun about, but back in 2k20 when I consciously ain’t known much about quant, I remember seeing post by @alexgrover recreating Moving Regression Endpoint dropped on price chart (called LSMA here) as a linear filter combination of filters (yea yeah DSP terms) as 3WMA - 2SMA. Now it’s my time to do smth alike aye?

...

This script is remake of my 1st degree WLSMA via linear filter combo. It’s much faster, we aint calculate moving regression per se, we just match its freq response. You can see it on the screen (WLSMAfa) almost perfectly matching the original one (WLSMA).

...

While humans like to overfit, I fw generalizations. So your lovely WMA is actually just one case of a more general weight pattern: pow(len - i, e), where pow is the power function and e is the exponent itself. So:

- If e = 0, then we have SMA (every number in 0th power is one)

- If e = 1, we get WMA

- If e = 2, we get quadratic weights.

We can recreate WLSMA freq response then by combining 2 filters with e = 1 and e = 2.

This is still an approximation, even tho enormously precise for the tasks you’ve shared with me. Due to the non-linear nature of the thing it’s all we can do, and as window size grows, even this small discrepancy converges with true WLSMA value, so we’re all good. Pls don’t try to model this 0.00xxxx discrepancy, it’s not natural.

...

DSP approach is unnatural for prices, but you can put this thing on volume delta and be happy, or on other metrics of yours, if for some reason u dont wanna estimate thresholds by fitting a distro.

All good TV

∞

P.S.: strangely, the first script made & dropped in the location in Saint P where my actual quant way has started ~5 years ago xD, very thankful

TASC 2025.06 Cybernetic Oscillator█ OVERVIEW

This script implements the Cybernetic Oscillator introduced by John F. Ehlers in his article "The Cybernetic Oscillator For More Flexibility, Making A Better Oscillator" from the June 2025 edition of the TASC Traders' Tips . It cascades two-pole highpass and lowpass filters, then scales the result by its root mean square (RMS) to create a flexible normalized oscillator that responds to a customizable frequency range for different trading styles.

█ CONCEPTS

Oscillators are indicators widely used by technical traders. These indicators swing above and below a center value, emphasizing cyclic movements within a frequency range. In his article, Ehlers explains that all oscillators share a common characteristic: their calculations involve computing differences . The reliance on differences is what causes these indicators to oscillate about a central point.

The difference between two data points in a series acts as a highpass filter — it allows high frequencies (short wavelengths) to pass through while significantly attenuating low frequencies (long wavelengths). Ehlers demonstrates that a simple difference calculation attenuates lower-frequency cycles at a rate of 6 dB per octave. However, the difference also significantly amplifies cycles near the shortest observable wavelength, making the result appear noisier than the original series. To mitigate the effects of noise in a differenced series, oscillators typically smooth the series with a lowpass filter, such as a moving average.

Ehlers highlights an underlying issue with smoothing differenced data to create oscillators. He postulates that market data statistically follows a pink spectrum , where the amplitudes of cyclic components in the data are approximately directly proportional to the underlying periods. Specifically, he suggests that cyclic amplitude increases by 6 dB per octave of wavelength.

Because some conventional oscillators, such as RSI, use differencing calculations that attenuate cycles by only 6 dB per octave, and market cycles increase in amplitude by 6 dB per octave, such calculations do not have a tangible net effect on larger wavelengths in the analyzed data. The influence of larger wavelengths can be especially problematic when using these oscillators for mean reversion or swing signals. For instance, an expected reversion to the mean might be erroneous because oscillator's mean might significantly deviate from its center over time.

To address the issues with conventional oscillator responses, Ehlers created a new indicator dubbed the Cybernetic Oscillator. It uses a simple combination of highpass and lowpass filters to emphasize a specific range of frequencies in the market data, then normalizes the result based on RMS. The process is as follows:

Apply a two-pole highpass filter to the data. This filter's critical period defines the longest wavelength in the oscillator's passband.

Apply a two-pole SuperSmoother (lowpass filter) to the highpass-filtered data. This filter's critical period defines the shortest wavelength in the passband.

Scale the resulting waveform by its RMS. If the filtered waveform follows a normal distribution, the scaled result represents amplitude in standard deviations.

The oscillator's two-pole filters attenuate cycles outside the desired frequency range by 12 dB per octave. This rate outweighs the apparent rate of amplitude increase for successively longer market cycles (6 dB per octave). Therefore, the Cybernetic Oscillator provides a more robust isolation of cyclic content than conventional oscillators. Best of all, traders can set the periods of the highpass and lowpass filters separately, enabling fine-tuning of the frequency range for different trading styles.

█ USAGE

The "Highpass period" input in the "Settings/Inputs" tab specifies the longest wavelength in the oscillator's passband, and the "Lowpass period" input defines the shortest wavelength. The oscillator becomes more responsive to rapid movements with a smaller lowpass period. Conversely, it becomes more sensitive to trends with a larger highpass period. Ehlers recommends setting the smallest period to a value above 8 to avoid aliasing. The highpass period must not be smaller than the lowpass period. Otherwise, it causes a runtime error.

The "RMS length" input determines the number of bars in the RMS calculation that the indicator uses to normalize the filtered result.

This indicator also features two distinct display styles, which users can toggle with the "Display style" input. With the "Trend" style enabled, the indicator plots the oscillator with one of two colors based on whether its value is above or below zero. With the "Threshold" style enabled, it plots the oscillator as a gray line and highlights overbought and oversold areas based on the user-specified threshold.

Below, we show two instances of the script with different settings on an equities chart. The first uses the "Threshold" style with default settings to pass cycles between 20 and 30 bars for mean reversion signals. The second uses a larger highpass period of 250 bars and the "Trend" style to visualize trends based on cycles spanning less than one year:

Enhanced Fuzzy SMA Analyzer (Multi-Output Proxy) [FibonacciFlux]EFzSMA: Decode Trend Quality, Conviction & Risk Beyond Simple Averages

Stop Relying on Lagging Averages Alone. Gain a Multi-Dimensional Edge.

The Challenge: Simple Moving Averages (SMAs) tell you where the price was , but they fail to capture the true quality, conviction, and sustainability of a trend. Relying solely on price crossing an average often leads to chasing weak moves, getting caught in choppy markets, or missing critical signs of trend exhaustion. Advanced traders need a more sophisticated lens to navigate complex market dynamics.

The Solution: Enhanced Fuzzy SMA Analyzer (EFzSMA)

EFzSMA is engineered to address these limitations head-on. It moves beyond simple price-average comparisons by employing a sophisticated Fuzzy Inference System (FIS) that intelligently integrates multiple critical market factors:

Price deviation from the SMA ( adaptively normalized for market volatility)

Momentum (Rate of Change - ROC)

Market Sentiment/Overheat (Relative Strength Index - RSI)

Market Volatility Context (Average True Range - ATR, optional)

Volume Dynamics (Volume relative to its MA, optional)

Instead of just a line on a chart, EFzSMA delivers a multi-dimensional assessment designed to give you deeper insights and a quantifiable edge.

Why EFzSMA? Gain Deeper Market Insights

EFzSMA empowers you to make more informed decisions by providing insights that simple averages cannot:

Assess True Trend Quality, Not Just Location: Is the price above the SMA simply because of a temporary spike, or is it supported by strong momentum, confirming volume, and stable volatility? EFzSMA's core fuzzyTrendScore (-1 to +1) evaluates the health of the trend, helping you distinguish robust moves from noise.

Quantify Signal Conviction: How reliable is the current trend signal? The Conviction Proxy (0 to 1) measures the internal consistency among the different market factors analyzed by the FIS. High conviction suggests factors are aligned, boosting confidence in the trend signal. Low conviction warns of conflicting signals, uncertainty, or potential consolidation – acting as a powerful filter against chasing weak moves.

// Simplified Concept: Conviction reflects agreement vs. conflict among fuzzy inputs

bullStrength = strength_SB + strength_WB

bearStrength = strength_SBe + strength_WBe

dominantStrength = max(bullStrength, bearStrength)

conflictingStrength = min(bullStrength, bearStrength) + strength_N

convictionProxy := (dominantStrength - conflictingStrength) / (dominantStrength + conflictingStrength + 1e-10)

// Modifiers (Volatility/Volume) applied...

Anticipate Potential Reversals: Trends don't last forever. The Reversal Risk Proxy (0 to 1) synthesizes multiple warning signs – like extreme RSI readings, surging volatility, or diverging volume – into a single, actionable metric. High reversal risk flags conditions often associated with trend exhaustion, providing early warnings to protect profits or consider counter-trend opportunities.

Adapt to Changing Market Regimes: Markets shift between high and low volatility. EFzSMA's unique Adaptive Deviation Normalization adjusts how it perceives price deviations based on recent market behavior (percentile rank). This ensures more consistent analysis whether the market is quiet or chaotic.

// Core Idea: Normalize deviation by recent volatility (percentile)

diff_abs_percentile = ta.percentile_linear_interpolation(abs(raw_diff), normLookback, percRank) + 1e-10

normalized_diff := raw_diff / diff_abs_percentile

// Fuzzy sets for 'normalized_diff' are thus adaptive to volatility

Integrate Complexity, Output Clarity: EFzSMA distills complex, multi-factor analysis into clear, interpretable outputs, helping you cut through market noise and focus on what truly matters for your decision-making process.

Interpreting the Multi-Dimensional Output

The true power of EFzSMA lies in analyzing its outputs together:

A high Trend Score (+0.8) is significant, but its reliability is amplified by high Conviction (0.9) and low Reversal Risk (0.2) . This indicates a strong, well-supported trend.

Conversely, the same high Trend Score (+0.8) coupled with low Conviction (0.3) and high Reversal Risk (0.7) signals caution – the trend might look strong superficially, but internal factors suggest weakness or impending exhaustion.

Use these combined insights to:

Filter Entry Signals: Require minimum Trend Score and Conviction levels.

Manage Risk: Consider reducing exposure or tightening stops when Reversal Risk climbs significantly, especially if Conviction drops.

Time Exits: Use rising Reversal Risk and falling Conviction as potential signals to take profits.

Identify Regime Shifts: Monitor how the relationship between the outputs changes over time.

Core Technology (Briefly)

EFzSMA leverages a Mamdani-style Fuzzy Inference System. Crisp inputs (normalized deviation, ROC, RSI, ATR%, Vol Ratio) are mapped to linguistic fuzzy sets ("Low", "High", "Positive", etc.). A rules engine evaluates combinations (e.g., "IF Deviation is LargePositive AND Momentum is StrongPositive THEN Trend is StrongBullish"). Modifiers based on Volatility and Volume context adjust rule strengths. Finally, the system aggregates these and defuzzifies them into the Trend Score, Conviction Proxy, and Reversal Risk Proxy. The key is the system's ability to handle ambiguity and combine multiple, potentially conflicting factors in a nuanced way, much like human expert reasoning.

Customization

While designed with robust defaults, EFzSMA offers granular control:

Adjust SMA, ROC, RSI, ATR, Volume MA lengths.

Fine-tune Normalization parameters (lookback, percentile). Note: Fuzzy set definitions for deviation are tuned for the normalized range.

Configure Volatility and Volume thresholds for fuzzy sets. Tuning these is crucial for specific assets/timeframes.

Toggle visual elements (Proxies, BG Color, Risk Shapes, Volatility-based Transparency).

Recommended Use & Caveats

EFzSMA is a sophisticated analytical tool, not a standalone "buy/sell" signal generator.

Use it to complement your existing strategy and analysis.

Always validate signals with price action, market structure, and other confirming factors.

Thorough backtesting and forward testing are essential to understand its behavior and tune parameters for your specific instruments and timeframes.

Fuzzy logic parameters (membership functions, rules) are based on general heuristics and may require optimization for specific market niches.

Disclaimer

Trading involves substantial risk. EFzSMA is provided for informational and analytical purposes only and does not constitute financial advice. No guarantee of profit is made or implied. Past performance is not indicative of future results. Use rigorous risk management practices.

Fuzzy SMA with DCTI Confirmation[FibonacciFlux]FibonacciFlux: Advanced Fuzzy Logic System with Donchian Trend Confirmation

Institutional-grade trend analysis combining adaptive Fuzzy Logic with Donchian Channel Trend Intensity for superior signal quality

Conceptual Framework & Research Foundation

FibonacciFlux represents a significant advancement in quantitative technical analysis, merging two powerful analytical methodologies: normalized fuzzy logic systems and Donchian Channel Trend Intensity (DCTI). This sophisticated indicator addresses a fundamental challenge in market analysis – the inherent imprecision of trend identification in dynamic, multi-dimensional market environments.

While traditional indicators often produce simplistic binary signals, markets exist in states of continuous, graduated transition. FibonacciFlux embraces this complexity through its implementation of fuzzy set theory, enhanced by DCTI's structural trend confirmation capabilities. The result is an indicator that provides nuanced, probabilistic trend assessment with institutional-grade signal quality.

Core Technological Components

1. Advanced Fuzzy Logic System with Percentile Normalization

At the foundation of FibonacciFlux lies a comprehensive fuzzy logic system that transforms conventional technical metrics into degrees of membership in linguistic variables:

// Fuzzy triangular membership function with robust error handling

fuzzy_triangle(val, left, center, right) =>

if na(val)

0.0

float denominator1 = math.max(1e-10, center - left)

float denominator2 = math.max(1e-10, right - center)

math.max(0.0, math.min(left == center ? val <= center ? 1.0 : 0.0 : (val - left) / denominator1,

center == right ? val >= center ? 1.0 : 0.0 : (right - val) / denominator2))

The system employs percentile-based normalization for SMA deviation – a critical innovation that enables self-calibration across different assets and market regimes:

// Percentile-based normalization for adaptive calibration

raw_diff = price_src - sma_val

diff_abs_percentile = ta.percentile_linear_interpolation(math.abs(raw_diff), normLookback, percRank) + 1e-10

normalized_diff_raw = raw_diff / diff_abs_percentile

normalized_diff = useClamping ? math.max(-clampValue, math.min(clampValue, normalized_diff_raw)) : normalized_diff_raw

This normalization approach represents a significant advancement over fixed-threshold systems, allowing the indicator to automatically adapt to varying volatility environments and maintain consistent signal quality across diverse market conditions.

2. Donchian Channel Trend Intensity (DCTI) Integration

FibonacciFlux significantly enhances fuzzy logic analysis through the integration of Donchian Channel Trend Intensity (DCTI) – a sophisticated measure of trend strength based on the relationship between short-term and long-term price extremes:

// DCTI calculation for structural trend confirmation

f_dcti(src, majorPer, minorPer, sigPer) =>

H = ta.highest(high, majorPer) // Major period high

L = ta.lowest(low, majorPer) // Major period low

h = ta.highest(high, minorPer) // Minor period high

l = ta.lowest(low, minorPer) // Minor period low

float pdiv = not na(L) ? l - L : 0 // Positive divergence (low vs major low)

float ndiv = not na(H) ? H - h : 0 // Negative divergence (major high vs high)

float divisor = pdiv + ndiv

dctiValue = divisor == 0 ? 0 : 100 * ((pdiv - ndiv) / divisor) // Normalized to -100 to +100 range

sigValue = ta.ema(dctiValue, sigPer)

DCTI provides a complementary structural perspective on market trends by quantifying the relationship between short-term and long-term price extremes. This creates a multi-dimensional analysis framework that combines adaptive deviation measurement (fuzzy SMA) with channel-based trend intensity confirmation (DCTI).

Multi-Dimensional Fuzzy Input Variables

FibonacciFlux processes four distinct technical dimensions through its fuzzy system:

Normalized SMA Deviation: Measures price displacement relative to historical volatility context

Rate of Change (ROC): Captures price momentum over configurable timeframes

Relative Strength Index (RSI): Evaluates cyclical overbought/oversold conditions

Donchian Channel Trend Intensity (DCTI): Provides structural trend confirmation through channel analysis

Each dimension is processed through comprehensive fuzzy sets that transform crisp numerical values into linguistic variables:

// Normalized SMA Deviation - Self-calibrating to volatility regimes

ndiff_LP := fuzzy_triangle(normalized_diff, norm_scale * 0.3, norm_scale * 0.7, norm_scale * 1.1)

ndiff_SP := fuzzy_triangle(normalized_diff, norm_scale * 0.05, norm_scale * 0.25, norm_scale * 0.5)

ndiff_NZ := fuzzy_triangle(normalized_diff, -norm_scale * 0.1, 0.0, norm_scale * 0.1)

ndiff_SN := fuzzy_triangle(normalized_diff, -norm_scale * 0.5, -norm_scale * 0.25, -norm_scale * 0.05)

ndiff_LN := fuzzy_triangle(normalized_diff, -norm_scale * 1.1, -norm_scale * 0.7, -norm_scale * 0.3)

// DCTI - Structural trend measurement

dcti_SP := fuzzy_triangle(dcti_val, 60.0, 85.0, 101.0) // Strong Positive Trend (> ~85)

dcti_WP := fuzzy_triangle(dcti_val, 20.0, 45.0, 70.0) // Weak Positive Trend (~30-60)

dcti_Z := fuzzy_triangle(dcti_val, -30.0, 0.0, 30.0) // Near Zero / Trendless (~+/- 20)

dcti_WN := fuzzy_triangle(dcti_val, -70.0, -45.0, -20.0) // Weak Negative Trend (~-30 - -60)

dcti_SN := fuzzy_triangle(dcti_val, -101.0, -85.0, -60.0) // Strong Negative Trend (< ~-85)

Advanced Fuzzy Rule System with DCTI Confirmation

The core intelligence of FibonacciFlux lies in its sophisticated fuzzy rule system – a structured knowledge representation that encodes expert understanding of market dynamics:

// Base Trend Rules with DCTI Confirmation

cond1 = math.min(ndiff_LP, roc_HP, rsi_M)

strength_SB := math.max(strength_SB, cond1 * (dcti_SP > 0.5 ? 1.2 : dcti_Z > 0.1 ? 0.5 : 1.0))

// DCTI Override Rules - Structural trend confirmation with momentum alignment

cond14 = math.min(ndiff_NZ, roc_HP, dcti_SP)

strength_SB := math.max(strength_SB, cond14 * 0.5)

The rule system implements 15 distinct fuzzy rules that evaluate various market conditions including:

Established Trends: Strong deviations with confirming momentum and DCTI alignment

Emerging Trends: Early deviation patterns with initial momentum and DCTI confirmation

Weakening Trends: Divergent signals between deviation, momentum, and DCTI

Reversal Conditions: Counter-trend signals with DCTI confirmation

Neutral Consolidations: Minimal deviation with low momentum and neutral DCTI

A key innovation is the weighted influence of DCTI on rule activation. When strong DCTI readings align with other indicators, rule strength is amplified (up to 1.2x). Conversely, when DCTI contradicts other indicators, rule impact is reduced (as low as 0.5x). This creates a dynamic, self-adjusting system that prioritizes high-conviction signals.

Defuzzification & Signal Generation

The final step transforms fuzzy outputs into a precise trend score through center-of-gravity defuzzification:

// Defuzzification with precise floating-point handling

denominator = strength_SB + strength_WB + strength_N + strength_WBe + strength_SBe

if denominator > 1e-10

fuzzyTrendScore := (strength_SB * STRONG_BULL + strength_WB * WEAK_BULL +

strength_N * NEUTRAL + strength_WBe * WEAK_BEAR +

strength_SBe * STRONG_BEAR) / denominator

The resulting FuzzyTrendScore ranges from -1.0 (Strong Bear) to +1.0 (Strong Bull), with critical threshold zones at ±0.3 (Weak trend) and ±0.7 (Strong trend). The histogram visualization employs intuitive color-coding for immediate trend assessment.

Strategic Applications for Institutional Trading

FibonacciFlux provides substantial advantages for sophisticated trading operations:

Multi-Timeframe Signal Confirmation: Institutional-grade signal validation across multiple technical dimensions

Trend Strength Quantification: Precise measurement of trend conviction with noise filtration

Early Trend Identification: Detection of emerging trends before traditional indicators through fuzzy pattern recognition

Adaptive Market Regime Analysis: Self-calibrating analysis across varying volatility environments

Algorithmic Strategy Integration: Well-defined numerical output suitable for systematic trading frameworks

Risk Management Enhancement: Superior signal fidelity for risk exposure optimization

Customization Parameters

FibonacciFlux offers extensive customization to align with specific trading mandates and market conditions:

Fuzzy SMA Settings: Configure baseline trend identification parameters including SMA, ROC, and RSI lengths

Normalization Settings: Fine-tune the self-calibration mechanism with adjustable lookback period, percentile rank, and optional clamping

DCTI Parameters: Optimize trend structure confirmation with adjustable major/minor periods and signal smoothing

Visualization Controls: Customize display transparency for optimal chart integration

These parameters enable precise calibration for different asset classes, timeframes, and market regimes while maintaining the core analytical framework.

Implementation Notes

For optimal implementation, consider the following guidance:

Higher timeframes (4H+) benefit from increased normalization lookback (800+) for stability

Volatile assets may require adjusted clamping values (2.5-4.0) for optimal signal sensitivity

DCTI parameters should be aligned with chart timeframe (higher timeframes require increased major/minor periods)

The indicator performs exceptionally well as a trend filter for systematic trading strategies

Acknowledgments

FibonacciFlux builds upon the pioneering work of Donovan Wall in Donchian Channel Trend Intensity analysis. The normalization approach draws inspiration from percentile-based statistical techniques in quantitative finance. This indicator is shared for educational and analytical purposes under Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0) license.

Past performance does not guarantee future results. All trading involves risk. This indicator should be used as one component of a comprehensive analysis framework.

Shout out @DonovanWall

Fuzzy SMA Trend Analyzer (experimental)[FibonacciFlux]Fuzzy SMA Trend Analyzer (Normalized): Advanced Market Trend Detection Using Fuzzy Logic Theory

Elevate your technical analysis with institutional-grade fuzzy logic implementation

Research Genesis & Conceptual Framework

This indicator represents the culmination of extensive research into applying fuzzy logic theory to financial markets. While traditional technical indicators often produce binary outcomes, market conditions exist on a continuous spectrum. The Fuzzy SMA Trend Analyzer addresses this limitation by implementing a sophisticated fuzzy logic system that captures the nuanced, multi-dimensional nature of market trends.

Core Fuzzy Logic Principles

At the heart of this indicator lies fuzzy logic theory - a mathematical framework designed to handle imprecision and uncertainty:

// Improved fuzzy_triangle function with guard clauses for NA and invalid parameters.

fuzzy_triangle(val, left, center, right) =>

if na(val) or na(left) or na(center) or na(right) or left > center or center > right // Guard checks

0.0

else if left == center and center == right // Crisp set (single point)

val == center ? 1.0 : 0.0

else if left == center // Left-shoulder shape (ramp down from 1 at center to 0 at right)

val >= right ? 0.0 : val <= center ? 1.0 : (right - val) / (right - center)

else if center == right // Right-shoulder shape (ramp up from 0 at left to 1 at center)

val <= left ? 0.0 : val >= center ? 1.0 : (val - left) / (center - left)

else // Standard triangle

math.max(0.0, math.min((val - left) / (center - left), (right - val) / (right - center)))

This implementation of triangular membership functions enables the indicator to transform crisp numerical values into degrees of membership in linguistic variables like "Large Positive" or "Small Negative," creating a more nuanced representation of market conditions.

Dynamic Percentile Normalization

A critical innovation in this indicator is the implementation of percentile-based normalization for SMA deviation:

// ----- Deviation Scale Estimation using Percentile -----

// Calculate the percentile rank of the *absolute* deviation over the lookback period.

// This gives an estimate of the 'typical maximum' deviation magnitude recently.

diff_abs_percentile = ta.percentile_linear_interpolation(math.abs(raw_diff), normLookback, percRank) + 1e-10

// ----- Normalize the Raw Deviation -----

// Divide the raw deviation by the estimated 'typical max' magnitude.

normalized_diff = raw_diff / diff_abs_percentile

// ----- Clamp the Normalized Deviation -----

normalized_diff_clamped = math.max(-3.0, math.min(3.0, normalized_diff))

This percentile normalization approach creates a self-adapting system that automatically calibrates to different assets and market regimes. Rather than using fixed thresholds, the indicator dynamically adjusts based on recent volatility patterns, significantly enhancing signal quality across diverse market environments.

Multi-Factor Fuzzy Rule System

The indicator implements a comprehensive fuzzy rule system that evaluates multiple technical factors:

SMA Deviation (Normalized): Measures price displacement from the Simple Moving Average

Rate of Change (ROC): Captures price momentum over a specified period

Relative Strength Index (RSI): Assesses overbought/oversold conditions

These factors are processed through a sophisticated fuzzy inference system with linguistic variables:

// ----- 3.1 Fuzzy Sets for Normalized Deviation -----

diffN_LP := fuzzy_triangle(normalized_diff_clamped, 0.7, 1.5, 3.0) // Large Positive (around/above percentile)

diffN_SP := fuzzy_triangle(normalized_diff_clamped, 0.1, 0.5, 0.9) // Small Positive

diffN_NZ := fuzzy_triangle(normalized_diff_clamped, -0.2, 0.0, 0.2) // Near Zero

diffN_SN := fuzzy_triangle(normalized_diff_clamped, -0.9, -0.5, -0.1) // Small Negative

diffN_LN := fuzzy_triangle(normalized_diff_clamped, -3.0, -1.5, -0.7) // Large Negative (around/below percentile)

// ----- 3.2 Fuzzy Sets for ROC -----

roc_HN := fuzzy_triangle(roc_val, -8.0, -5.0, -2.0)

roc_WN := fuzzy_triangle(roc_val, -3.0, -1.0, -0.1)

roc_NZ := fuzzy_triangle(roc_val, -0.3, 0.0, 0.3)

roc_WP := fuzzy_triangle(roc_val, 0.1, 1.0, 3.0)

roc_HP := fuzzy_triangle(roc_val, 2.0, 5.0, 8.0)

// ----- 3.3 Fuzzy Sets for RSI -----

rsi_L := fuzzy_triangle(rsi_val, 0.0, 25.0, 40.0)

rsi_M := fuzzy_triangle(rsi_val, 35.0, 50.0, 65.0)

rsi_H := fuzzy_triangle(rsi_val, 60.0, 75.0, 100.0)

Advanced Fuzzy Inference Rules

The indicator employs a comprehensive set of fuzzy rules that encode expert knowledge about market behavior:

// --- Fuzzy Rules using Normalized Deviation (diffN_*) ---

cond1 = math.min(diffN_LP, roc_HP, math.max(rsi_M, rsi_H)) // Strong Bullish: Large pos dev, strong pos roc, rsi ok

strength_SB := math.max(strength_SB, cond1)

cond2 = math.min(diffN_SP, roc_WP, rsi_M) // Weak Bullish: Small pos dev, weak pos roc, rsi mid

strength_WB := math.max(strength_WB, cond2)

cond3 = math.min(diffN_SP, roc_NZ, rsi_H) // Weakening Bullish: Small pos dev, flat roc, rsi high

strength_N := math.max(strength_N, cond3 * 0.6) // More neutral

strength_WB := math.max(strength_WB, cond3 * 0.2) // Less weak bullish

This rule system evaluates multiple conditions simultaneously, weighting them by their degree of membership to produce a comprehensive trend assessment. The rules are designed to identify various market conditions including strong trends, weakening trends, potential reversals, and neutral consolidations.

Defuzzification Process

The final step transforms the fuzzy result back into a crisp numerical value representing the overall trend strength:

// --- Step 6: Defuzzification ---

denominator = strength_SB + strength_WB + strength_N + strength_WBe + strength_SBe

if denominator > 1e-10 // Use small epsilon instead of != 0.0 for float comparison

fuzzyTrendScore := (strength_SB * STRONG_BULL +

strength_WB * WEAK_BULL +

strength_N * NEUTRAL +

strength_WBe * WEAK_BEAR +

strength_SBe * STRONG_BEAR) / denominator

The resulting FuzzyTrendScore ranges from -1 (strong bearish) to +1 (strong bullish), providing a smooth, continuous evaluation of market conditions that avoids the abrupt signal changes common in traditional indicators.

Advanced Visualization with Rainbow Gradient

The indicator incorporates sophisticated visualization using a rainbow gradient coloring system:

// Normalize score to for gradient function

normalizedScore = na(fuzzyTrendScore) ? 0.5 : math.max(0.0, math.min(1.0, (fuzzyTrendScore + 1) / 2))

// Get the color based on gradient setting and normalized score

final_color = get_gradient(normalizedScore, gradient_type)

This color-coding system provides intuitive visual feedback, with color intensity reflecting trend strength and direction. The gradient can be customized between Red-to-Green or Red-to-Blue configurations based on user preference.

Practical Applications

The Fuzzy SMA Trend Analyzer excels in several key applications:

Trend Identification: Precisely identifies market trend direction and strength with nuanced gradation

Market Regime Detection: Distinguishes between trending markets and consolidation phases

Divergence Analysis: Highlights potential reversals when price action and fuzzy trend score diverge

Filter for Trading Systems: Provides high-quality trend filtering for other trading strategies

Risk Management: Offers early warning of potential trend weakening or reversal

Parameter Customization

The indicator offers extensive customization options:

SMA Length: Adjusts the baseline moving average period

ROC Length: Controls momentum sensitivity

RSI Length: Configures overbought/oversold sensitivity

Normalization Lookback: Determines the adaptive calculation window for percentile normalization

Percentile Rank: Sets the statistical threshold for deviation normalization

Gradient Type: Selects the preferred color scheme for visualization

These parameters enable fine-tuning to specific market conditions, trading styles, and timeframes.

Acknowledgments

The rainbow gradient visualization component draws inspiration from LuxAlgo's "Rainbow Adaptive RSI" (used under CC BY-NC-SA 4.0 license). This implementation of fuzzy logic in technical analysis builds upon Fermi estimation principles to overcome the inherent limitations of crisp binary indicators.

This indicator is shared under Attribution-NonCommercial-ShareAlike 4.0 International (CC BY-NC-SA 4.0) license.

Remember that past performance does not guarantee future results. Always conduct thorough testing before implementing any technical indicator in live trading.

Multi-Fibonacci Trend Average[FibonacciFlux]Multi-Fibonacci Trend Average (MFTA): An Institutional-Grade Trend Confluence Indicator for Discerning Market Participants

My original indicator/Strategy:

Engineered for the sophisticated demands of institutional and advanced traders, the Multi-Fibonacci Trend Average (MFTA) indicator represents a paradigm shift in technical analysis. This meticulously crafted tool is designed to furnish high-definition trend signals within the complexities of modern financial markets. Anchored in the rigorous principles of Fibonacci ratios and augmented by advanced averaging methodologies, MFTA delivers a granular perspective on trend dynamics. Its integration of Multi-Timeframe (MTF) filters provides unparalleled signal robustness, empowering strategic decision-making with a heightened degree of confidence.

MFTA indicator on BTCUSDT 15min chart with 1min RSI and MACD filters enabled. Note the refined signal generation with reduced noise.

MFTA indicator on BTCUSDT 15min chart without MTF filters. While capturing more potential trading opportunities, it also generates a higher frequency of signals, including potential false positives.

Core Innovation: Proprietary Fibonacci-Enhanced Supertrend Averaging Engine

The MFTA indicator’s core innovation lies in its proprietary implementation of Supertrend analysis, strategically fortified by Fibonacci ratios to construct a truly dynamic volatility envelope. Departing from conventional Supertrend methodologies, MFTA autonomously computes not one, but three distinct Supertrend lines. Each of these lines is uniquely parameterized by a specific Fibonacci factor: 0.618 (Weak), 1.618 (Medium/Golden Ratio), and 2.618 (Strong/Extended Fibonacci).

// Fibonacci-based factors for multiple Supertrend calculations

factor1 = input.float(0.618, 'Factor 1 (Weak/Fibonacci)', minval=0.01, step=0.01, tooltip='Factor 1 (Weak/Fibonacci)', group="Fibonacci Supertrend")

factor2 = input.float(1.618, 'Factor 2 (Medium/Golden Ratio)', minval=0.01, step=0.01, tooltip='Factor 2 (Medium/Golden Ratio)', group="Fibonacci Supertrend")

factor3 = input.float(2.618, 'Factor 3 (Strong/Extended Fib)', minval=0.01, step=0.01, tooltip='Factor 3 (Strong/Extended Fib)', group="Fibonacci Supertrend")

This multi-faceted architecture adeptly captures a spectrum of market volatility sensitivities, ensuring a comprehensive assessment of prevailing conditions. Subsequently, the indicator algorithmically synthesizes these disparate Supertrend lines through arithmetic averaging. To achieve optimal signal fidelity and mitigate inherent market noise, this composite average is further refined utilizing an Exponential Moving Average (EMA).

// Calculate average of the three supertends and a smoothed version

superlength = input.int(21, 'Smoothing Length', tooltip='Smoothing Length for Average Supertrend', group="Fibonacci Supertrend")

average_trend = (supertrend1 + supertrend2 + supertrend3) / 3

smoothed_trend = ta.ema(average_trend, superlength)

The resultant ‘Smoothed Trend’ line emerges as a remarkably responsive yet stable trend demarcation, offering demonstrably superior clarity and precision compared to singular Supertrend implementations, particularly within the turbulent dynamics of high-volatility markets.

Elevated Signal Confluence: Integrated Multi-Timeframe (MTF) Validation Suite

MFTA transcends the limitations of conventional trend indicators by incorporating an advanced suite of three independent MTF filters: RSI, MACD, and Volume. These filters function as sophisticated validation protocols, rigorously ensuring that only signals exhibiting a confluence of high-probability factors are brought to the forefront.

1. Granular Lower Timeframe RSI Momentum Filter

The Relative Strength Index (RSI) filter, computed from a user-defined lower timeframe, furnishes critical momentum-based signal validation. By meticulously monitoring RSI dynamics on an accelerated timeframe, traders gain the capacity to evaluate underlying momentum strength with precision, prior to committing to signal execution on the primary chart timeframe.

// --- Lower Timeframe RSI Filter ---

ltf_rsi_filter_enable = input.bool(false, title="Enable RSI Filter", group="MTF Filters", tooltip="Use RSI from lower timeframe as a filter")

ltf_rsi_timeframe = input.timeframe("1", title="RSI Timeframe", group="MTF Filters", tooltip="Timeframe for RSI calculation")

ltf_rsi_length = input.int(14, title="RSI Length", minval=1, group="MTF Filters", tooltip="Length for RSI calculation")

ltf_rsi_threshold = input.int(30, title="RSI Threshold", minval=0, maxval=100, group="MTF Filters", tooltip="RSI value threshold for filtering signals")

2. Convergent Lower Timeframe MACD Trend-Momentum Filter

The Moving Average Convergence Divergence (MACD) filter, also calculated on a lower timeframe basis, introduces a critical layer of trend-momentum convergence confirmation. The bullish signal configuration rigorously mandates that the MACD line be definitively positioned above the Signal line on the designated lower timeframe. This stringent condition ensures a robust indication of converging momentum that aligns synergistically with the prevailing trend identified on the primary timeframe.

// --- Lower Timeframe MACD Filter ---

ltf_macd_filter_enable = input.bool(false, title="Enable MACD Filter", group="MTF Filters", tooltip="Use MACD from lower timeframe as a filter")

ltf_macd_timeframe = input.timeframe("1", title="MACD Timeframe", group="MTF Filters", tooltip="Timeframe for MACD calculation")

ltf_macd_fast_length = input.int(12, title="MACD Fast Length", minval=1, group="MTF Filters", tooltip="Fast EMA length for MACD")

ltf_macd_slow_length = input.int(26, title="MACD Slow Length", minval=1, group="MTF Filters", tooltip="Slow EMA length for MACD")

ltf_macd_signal_length = input.int(9, title="MACD Signal Length", minval=1, group="MTF Filters", tooltip="Signal SMA length for MACD")

3. Definitive Volume Confirmation Filter

The Volume Filter functions as an indispensable arbiter of trade conviction. By establishing a dynamic volume threshold, defined as a percentage relative to the average volume over a user-specified lookback period, traders can effectively ensure that all generated signals are rigorously validated by demonstrably increased trading activity. This pivotal validation step signifies robust market participation, substantially diminishing the potential for spurious or false breakout signals.

// --- Volume Filter ---

volume_filter_enable = input.bool(false, title="Enable Volume Filter", group="MTF Filters", tooltip="Use volume level as a filter")

volume_threshold_percent = input.int(title="Volume Threshold (%)", defval=150, minval=100, group="MTF Filters", tooltip="Minimum volume percentage compared to average volume to allow signal (100% = average)")

These meticulously engineered filters operate in synergistic confluence, requiring all enabled filters to definitively satisfy their pre-defined conditions before a Buy or Sell signal is generated. This stringent multi-layered validation process drastically minimizes the incidence of false positive signals, thereby significantly enhancing entry precision and overall signal reliability.

Intuitive Visual Architecture & Actionable Intelligence

MFTA provides a demonstrably intuitive and visually rich charting environment, meticulously delineating trend direction and momentum through precisely color-coded plots:

Average Supertrend: Thin line, green/red for uptrend/downtrend, immediate directional bias.

Smoothed Supertrend: Bold line, teal/purple for uptrend/downtrend, cleaner, institutionally robust trend.

Dynamic Trend Fill: Green/red fill between Supertrends quantifies trend strength and momentum.

Adaptive Background Coloring: Light green/red background mirrors Smoothed Supertrend direction, holistic trend perspective.

Precision Buy/Sell Signals: ‘BUY’/‘SELL’ labels appear on chart when trend touch and MTF filter confluence are satisfied, facilitating high-conviction trade action.

MFTA indicator applied to BTCUSDT 4-hour chart, showcasing its effectiveness on higher timeframes. The Smoothed Length parameter is increased to 200 for enhanced smoothness on this timeframe, coupled with 1min RSI and Volume filters for signal refinement. This illustrates the indicator's adaptability across different timeframes and market conditions.

Strategic Applications for Institutional Mandates

MFTA’s sophisticated design provides distinct advantages for advanced trading operations and institutional investment mandates. Key strategic applications include:

High-Probability Trend Identification: Fibonacci-averaged Supertrend with MTF filters robustly identifies high-probability trend continuations and reversals, enhancing alpha generation.

Precision Entry/Exit Signals: Volume and momentum-filtered signals enable institutional-grade precision for optimized risk-adjusted returns.

Algorithmic Trading Integration: Clear signal logic facilitates seamless integration into automated trading systems for scalable strategy deployment.

Multi-Asset/Timeframe Versatility: Adaptable parameters ensure applicability across diverse asset classes and timeframes, catering to varied trading mandates.

Enhanced Risk Management: Superior signal fidelity from MTF filters inherently reduces false signals, supporting robust risk management protocols.

Granular Customization and Parameterized Control

MFTA offers unparalleled customization, empowering users to fine-tune parameters for precise alignment with specific trading styles and market conditions. Key adjustable parameters include:

Fibonacci Factors: Adjust Supertrend sensitivity to volatility regimes.

ATR Length: Control volatility responsiveness in Supertrend calculations.

Smoothing Length: Refine Smoothed Trend line responsiveness and noise reduction.

MTF Filter Parameters: Independently configure timeframes, lookback periods, and thresholds for RSI, MACD, and Volume filters for optimal signal filtering.

Disclaimer

MFTA is meticulously engineered for high-quality trend signals; however, no indicator guarantees profit. Market conditions are unpredictable, and trading involves substantial risk. Rigorous backtesting and forward testing across diverse datasets, alongside a comprehensive understanding of the indicator's logic, are essential before live deployment. Past performance is not indicative of future results. MFTA is for informational and analytical purposes only and is not financial or investment advice.

[GYTS-CE] Market Regime Detector🧊 Market Regime Detector (Community Edition)

🌸 Part of GoemonYae Trading System (GYTS) 🌸

🌸 --------- INTRODUCTION --------- 🌸

💮 What is the Market Regime Detector?

The Market Regime Detector is an advanced, consensus-based indicator that identifies the current market state to increase the probability of profitable trades. By distinguishing between trending (bullish or bearish) and cyclic (range-bound) market conditions, this detector helps you select appropriate tactics for different environments. Instead of forcing a single strategy across all market conditions, our detector allows you to adapt your approach based on real-time market behaviour.

💮 The Importance of Market Regimes

Markets constantly shift between different behavioural states or "regimes":

• Bullish trending markets - characterised by sustained upward price movement

• Bearish trending markets - characterised by sustained downward price movement

• Cyclic markets - characterised by range-bound, oscillating behaviour

Each regime requires fundamentally different trading approaches. Trend-following strategies excel in trending markets but fail in cyclic ones, while mean-reversion strategies shine in cyclic markets but underperform in trending conditions. Detecting these regimes is essential for successful trading, which is why we've developed the Market Regime Detector to accurately identify market states using complementary detection methods.

🌸 --------- KEY FEATURES --------- 🌸

💮 Consensus-Based Detection

Rather than relying on a single method, our detector employs two complementary detection methodologies that analyse different aspects of market behaviour:

• Dominant Cycle Average (DCA) - analyzes price movement relative to its lookback period, a proxy for the dominant cycle

• Volatility Channel - examines price behaviour within adaptive volatility bands

These diverse perspectives are synthesised into a robust consensus that minimises false signals while maintaining responsiveness to genuine regime changes.

💮 Dominant Cycle Framework

The Market Regime Detector uses the concept of dominant cycles to establish a reference framework. You can input the dominant cycle period that best represents the natural rhythm of your market, providing a stable foundation for regime detection across different timeframes.

💮 Intuitive Parameter System

We've distilled complex technical parameters into intuitive controls that traders can easily understand:

• Adaptability - how quickly the detector responds to changing market conditions

• Sensitivity - how readily the detector identifies transitions between regimes

• Consensus requirement - how much agreement is needed among detection methods

This approach makes the detector accessible to traders of all experience levels while preserving the power of the underlying algorithms.

💮 Visual Market Feedback

The detector provides clear visual feedback about the current market regime through:

• Colour-coded chart backgrounds (purple shades for bullish, pink for bearish, yellow for cyclic)

• Colour-coded price bars

• Strength indicators showing the degree of consensus

• Customizable colour schemes to match your preferences or trading system

💮 Integration in the GYTS suite

The Market Regime Detector is compatible with the GYTS Suite , i.e. it passes the regime into the 🎼 Order Orchestrator where you can set how to trade the trending and cyclic regime.

🌸 --------- CONFIGURATION SETTINGS --------- 🌸

💮 Adaptability

Controls how quickly the Market Regime detector adapts to changing market conditions. You can see it as a low-frequency, long-term change parameter:

Very Low: Very slow adaptation, most stable but may miss regime changes

Low: Slower adaptation, more stability but less responsiveness

Normal: Balanced between stability and responsiveness

High: Faster adaptation, more responsive but less stable

Very High: Very fast adaptation, highly responsive but may generate false signals

This setting affects lookback periods and filter parameters across all detection methods.

💮 Sensitivity

Controls how sensitive the detector is to market regime transitions. This acts as a high-frequency, short-term change parameter:

Very Low: Requires substantial evidence to identify a regime change

Low: Less sensitive, reduces false signals but may miss some transitions

Normal: Balanced sensitivity suitable for most markets

High: More sensitive, detects subtle regime changes but may have more noise

Very High: Very sensitive, detects minor fluctuations but may produce frequent changes

This setting affects thresholds for regime detection across all methods.

💮 Dominant Cycle Period

This parameter allows you to specify the market's natural rhythm in bars. This represents a complete market cycle (up and down movement). Finding the right value for your specific market and timeframe might require some experimentation, but it's a crucial parameter that helps the detector accurately identify regime changes. Most of the times the cycle is between 20 and 40 bars.

💮 Consensus Mode

Determines how the signals from both detection methods are combined to produce the final market regime:

• Any Method (OR) : Signals bullish/bearish if either method detects that regime. If methods conflict (one bullish, one bearish), the stronger signal wins. More sensitive, catches more regime changes but may produce more false signals.

• All Methods (AND) : Signals only when both methods agree on the regime. More conservative, reduces false signals but might miss some legitimate regime changes.

• Weighted Decision : Balances both methods with equal weighting. Provides a middle ground between sensitivity and stability.

Each mode also calculates a continuous regime strength value that's used for colour intensity in the 'unconstrained' display mode.

💮 Display Mode

Choose how to display the market regime colours:

• Unconstrained regime: Shows the regime strength as a continuous gradient. This provides more nuanced visualisation where the intensity of the colour indicates the strength of the trend.

• Consensus only: Shows only the final consensus regime with fixed colours based on the detected regime type.

The background and bar colours will change to indicate the current market regime:

• Purple shades: Bullish trending market (darker purple indicates stronger bullish trend)

• Pink shades: Bearish trending market (darker pink indicates stronger bearish trend)

• Yellow: Cyclic (range-bound) market

💮 Custom Colour Options

The Market Regime Detector allows you to customize the colour scheme to match your personal preferences or to coordinate with other indicators:

• Use custom colours: Toggle to enable your own colour choices instead of the default scheme

• Transparency: Adjust the transparency level of all regime colours

• Bullish colours: Define custom colours for strong, medium, weak, and very weak bullish trends

• Bearish colours: Define custom colours for strong, medium, weak, and very weak bearish trends

• Cyclic colour: Define a custom colour for cyclic (range-bound) market conditions

🌸 --------- DETECTION METHODS --------- 🌸

💮 Dominant Cycle Average (DCA)

The Dominant Cycle Average method forms a key part of our detection system:

1. Theoretical Foundation :

The DCA method builds on cycle analysis and the observation that in trending markets, price consistently remains on one side of a moving average calculated using the dominant cycle period. In contrast, during cyclic markets, price oscillates around this average.

2. Calculation Process :

• We calculate a Simple Moving Average (SMA) using the specified lookback period - a proxy for the dominant cycle period

• We then analyse the proportion of time that price spends above or below this SMA over a lookback window. The theory is that the price should cross the SMA each half cycle, assuming that the dominant cycle period is correct and price follows a sinusoid.

• This lookback window is adaptive, scaling with the dominant cycle period (controlled by the Adaptability setting)

• The different values are standardised and normalised to possess more resolving power and to be more robust to noise.

3. Regime Classification :

• When the normalised proportion exceeds a positive threshold (determined by Sensitivity setting), the market is classified as bullish trending

• When it falls below a negative threshold, the market is classified as bearish trending

• When the proportion remains between these thresholds, the market is classified as cyclic

💮 Volatility Channel

The Volatility Channel method complements the DCA method by focusing on price movement relative to adaptive volatility bands:

1. Theoretical Foundation :

This method is based on the observation that trending markets tend to sustain movement outside of normal volatility ranges, while cyclic markets tend to remain contained within these ranges. By creating adaptive bands that adjust to current market volatility, we can detect when price behaviour indicates a trending or cyclic regime.

2. Calculation Process :

• We first calculate a smooth base channel center using a low pass filter, creating a noise-reduced centreline for price

• True Range (TR) is used to measure market volatility, which is then smoothed and scaled by the deviation factor (controlled by Sensitivity)

• Upper and lower bands are created by adding and subtracting this scaled volatility from the centreline

• Price is smoothed using an adaptive A2RMA filter, which has a very flat and stable behaviour, to reduce noise while preserving trend characteristics

• The position of this smoothed price relative to the bands is continuously monitored

3. Regime Classification :

• When smoothed price moves above the upper band, the market is classified as bullish trending

• When smoothed price moves below the lower band, the market is classified as bearish trending

• When price remains between the bands, the market is classified as cyclic

• The magnitude of price's excursion beyond the bands is used to determine trend strength

4. Adaptive Behaviour :

• The smoothing periods and deviation calculations automatically adjust based on the Adaptability setting

• The measured volatility is calculated over a period proportional to the dominant cycle, ensuring the detector works across different timeframes

• Both the center line and the bands adapt dynamically to changing market conditions, making the detector responsive yet stable

This method provides a unique perspective that complements the DCA approach, with the consensus mechanism synthesising insights from both methods.

🌸 --------- USAGE GUIDE --------- 🌸

💮 Starting with Default Settings

The default settings (Normal for Adaptability and Sensitivity, Weighted Decision for Consensus Mode) provide a balanced starting point suitable for most markets and timeframes. Begin by observing how these settings identify regimes in your preferred instruments.

💮 Finding the Optimal Dominant Cycle

The dominant cycle period is a critical parameter. Here are some approaches to finding an appropriate value:

• Start with typical values, usually something around 25 works well

• Visually identify the average distance between significant peaks and troughs

• Experiment with different values and observe which provides the most stable regime identification

• Consider using cycle-finding indicators to help identify the natural rhythm of your market

💮 Adjusting Parameters

• If you notice too many regime changes → Decrease Sensitivity or increase Consensus requirement

• If regime changes seem delayed → Increase Adaptability

• If a trending regime is not detected, the market is automatically assigned to be in a cyclic state

• If you want to see more nuanced regime transitions → Try the "unconstrained" display mode (note that this will not affect the output to other indicators)

💮 Trading Applications

Regime-Specific Strategies:

• Bullish Trending Regime - Use trend-following strategies, trail stops wider, focus on breakouts, consider holding positions longer, and emphasize buying dips

• Bearish Trending Regime - Consider shorts, tighter stops, focus on breakdown points, sell rallies, implement downside protection, and reduce position sizes

• Cyclic Regime - Apply mean-reversion strategies, trade range boundaries, apply oscillators, target definable support/resistance levels, and use profit-taking at extremes

Strategy Switching:

Create a set of rules for each market regime and switch between them based on the detector's signal. This approach can significantly improve performance compared to applying a single strategy across all market conditions.

GYTS Suite Integration:

• In the GYTS 🎼 Order Orchestrator, select the '🔗 STREAM-int 🧊 Market Regime' as the market regime source

• Note that the consensus output (i.e. not the "unconstrained" display) will be used in this stream

• Create different strategies for trending (bullish/bearish) and cyclic regimes. The GYTS 🎼 Order Orchestrator is specifically made for this.

• The output stream is actually very simple, and can possibly be used in indicators and strategies as well. It outputs 1 for bullish, -1 for bearish and 0 for cyclic regime.

🌸 --------- FINAL NOTES --------- 🌸

💮 Development Philosophy

The Market Regime Detector has been developed with several key principles in mind:

1. Robustness - The detection methods have been rigorously tested across diverse markets and timeframes to ensure reliable performance.

2. Adaptability - The detector automatically adjusts to changing market conditions, requiring minimal manual intervention.

3. Complementarity - Each detection method provides a unique perspective, with the collective consensus being more reliable than any individual method.

4. Intuitiveness - Complex technical parameters have been abstracted into easily understood controls.

💮 Ongoing Refinement

The Market Regime Detector is under continuous development. We regularly:

• Fine-tune parameters based on expanded market data

• Research and integrate new detection methodologies

• Optimise computational efficiency for real-time analysis

Your feedback and suggestions are very important in this ongoing refinement process!

Dual SuperTrend w VIX Filter - Strategy [presentTrading]Hey everyone! Haven't been here for a long time. Been so busy again in the past 2 months. I recently started working on analyzing the combination of trend strategy and VIX, but didn't get outstanding results after a few tries. Sharing this tool with all of you in case you have better insights.

█ Introduction and How it is Different