Kalman SmootherA derivation of the Kalman Filter.

Lower Gain values create smoother results.The ratio Smoothing/Lag is similar to any Low Lagging Filters.

The Gain parameter can be decimal numbers.

Kalman Smoothing With Gain = 20

For any questions/suggestions feel free to contact me

Filter

One Dimensional Parametric Kalman FilterA One Dimensional Kalman Filter, the particularity of Kalman Filtering is the constant recalculation of the Error between the measurements and the estimate.This version is modified to allow more/less filtering using an alternative calculation of the error measurement.

Camparison of the Kalman filter Red with a moving average Black of both period 50

Can be used as source for others indicators such as stochastic/rsi/moving averages...etc

For any questions/suggestions feel free to contact me

Auto-Line With DriftA variation on the Auto-Line indicator, we allow it to get closer to the price thanks to a drift , this also allow the line to be more directional .

This indicator can be used with moving averages using crosses as signals or as a band indicator by ploting a + dev as the upper band and a - dev as the lower one.

For any help or suggestions feel free to send a message :)

Range Filter [DW]This is an experimental study designed to filter out minor price action for a clearer view of trends.

Inspired by the QQE's volatility filter, this filter applies the process directly to price rather than to a smoothed RSI.

First, a smooth average price range is calculated for the basis of the filter and multiplied by a specified amount.

Next, the filter is calculated by gating price movements that do not exceed the specified range.

Lastly the target ranges are plotted to display the prices that will trigger filter movement.

Custom bar colors are included. The color scheme is based on the filtered price trend.

Jurik Moving AverageThis indicator was originally developed by Mark Jurik.

NOTE: If Mr. Jurik ask me to remove this indicator from public access then I will do it.

Butterworth FilterButterworth Filter script.

This indicator was described by John F. Ehlers in his book "Rocket Science for Traders" (2001, Chapter 15: Infinite Impulse Response Filters).

Gaussian FilterGaussian Filter script.

This indicator was described by John F. Ehlers in his book "Rocket Science for Traders" (2001, Chapter 15: Infinite Impulse Response Filters).

Hampel FilterHampel Filter script.

This indicator was originally developed by Frank Rudolf Hampel (Journal of the American Statistical Association, 69, 382–393, 1974: The influence curve and its role in robust estimation).

The Hampel filter is a simple but effective filter to find outliers and to remove them from data. It performs better than a median filter.

Ehlers FilterThis is the Adaptive Ehlers Filter.

I had to unroll the for loops and array because TV is missing crucial data structures and data conversions (Arrays and series to integer conversion for values).

I'm in the process of releasing some scripts. This is a very old script I had. This contains volatility ranges and can be used as trading signals. You can also see how the EF moves up or down, the direction, when price is sideways, and use price breaks up and down as signals from the line.

Have fun, because I didn't making this script hahaha

NOTE : There is an issue with the script where at certain time frames it positions itself below or above. I think its due to calculations. If anyone knows the fix before I get the chance to take a look at it, please let me know.

books.google.com

Ehlers Super Passband FilterEhlers Super Passband Filter script.

This indicator was originally developed by John F. Ehlers (Stocks & Commodities V. 34:8: The Super Passband Filter).

Ehlers StochasticEhlers Stochastic script.

This indicator was originally developed by John F. Ehlers (Stocks & Commodities V. 32:1: Predictive And Successful Indicators).

Ehlers Roofing FilterEhlers Roofing Filter script.

This indicator was originally developed by John F. Ehlers (Stocks & Commodities V. 32:1: Predictive And Successful Indicators).

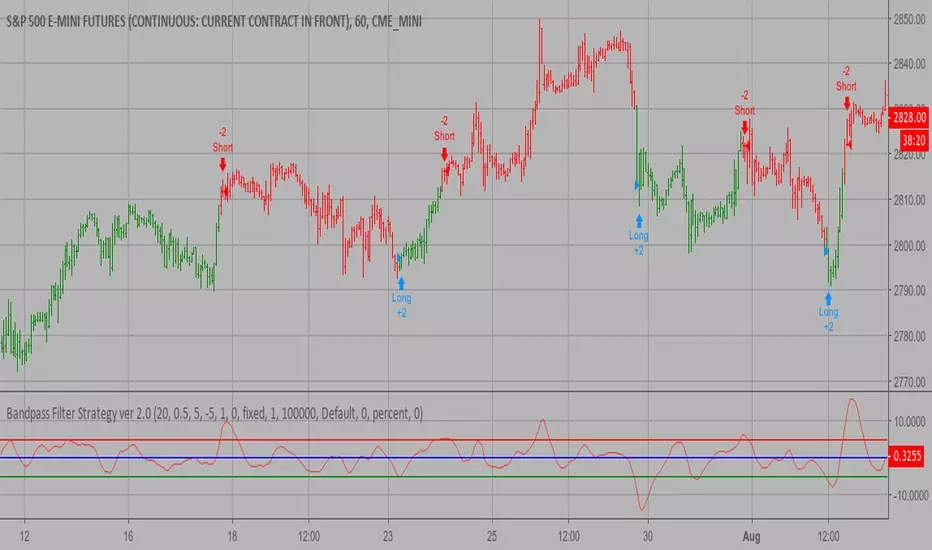

Bandpass Filter Strategy ver 2.0 The related article is copyrighted material from

Stocks & Commodities Mar 2010

You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

You can change long to short in the Input Settings

WARNING:

- For purpose educate only

- This script to change bars colors.

Ehlers Super Smoother FilterEhlers Super Smoother Filter script.

This indicator was originally developed by John F. Ehlers (see his book `Cybernetic Analysis for Stocks and Futures`, Chapter 13: `Super Smoothers`).

Bandpass Filter Strategy ver 2.0 The related article is copyrighted material from

Stocks & Commodities Mar 2010

You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

WARNING:

- This script to change bars colors.

Quadratic RegressionA quadratic regression is the process of finding the equation that best fits a set of data.This form of regression is mainly used for smoothing data shaped like a parabola.

Because we can use short/midterm/longterm periods we can say that we use a Quadratic Least Squares Moving Average or a Moving Quadratic Regression.

Like the Linear Regression (LSMA) a Quadratic regression attempt to minimize the sum of squares (sum of the squared difference between a set of data and an estimator), this is why

those kinds of filters have low lag .

Here the difference between a Least Squared Moving Average ( green ) and a Quadratic Regression ( red ) of both period 500

Here it look like the Quadratic Regression have a best fit than the LSMA

Price FlowFor those who like to trade with the trend instead of against it. This little script shows you what side of the daily/weekly/monthly timeframe open, price is currently trading at so that you dont accidentally trade against the higher timeframe momentum. Timeframes are customizable through the indicator settings panel.

Hamming Windowed Volume Weighted Moving AverageApplying a window to the filter weights provides sometimes extra control over the characteristics of the filter.In this script an hamming window is applied to the volume before being used as a weight.In general this process smooth the frequency response of a filter.

Lets compare the classic vwma with hamming windowed vwma

Something i noticed is that windowed filters depending on their period ( high ones in general ) tend to make less bad crosses with the price ( at least with the hamming window )

Here are some data regarding number of crosses with period 50 with the hamming vwma in orange and the classic vwma in purple

Feel free to use the hamming window when using weighted filter.

Rate of Change w/ Butterworth FilterIt passes the Rate of Change data through a Butterworth filter which creates a smooth line that can allow for easier detection of slope changes in the data over various periods of times.

The butterworth filter line and the rate of change are plotted together by default. The values for the lengths, for both the butterworth filter and the raw ROC data, can be changed from the format menu (through a toggle).

The shorter the Butterworth length, the closer the line is fitted to the raw ROC data, however you trade of with more frequent slope changes.

The longer the Butterworth length, the smoother the line and less frequent the slope changes, but the Butterworth line is farther of center from the raw ROC data.

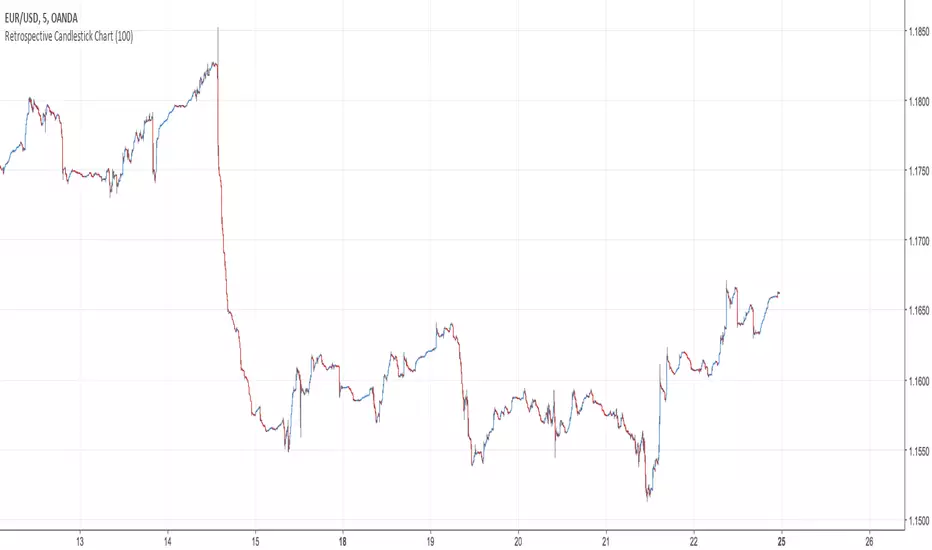

Retrospective Candlestick ChartWhen i was in Japan with some traders colleagues we talked about traditional charting tools from this country and how they changed the way we look at our charts today. Then suddenly one of the japanese traders i have met earlier said "Why not making another charting tool ? Smoother than Heikin-Ashi and including all the information a trader may need but easier to interpret".

So i had the idea of averaging the input and the output of the respective close / open / high and low price using a recursive exponential window functions, each values will be closer to their true value if they are volatile, if they are not then those values will look smoother, the length input represents the reactivity of the candles, high values represents smoother results but less reactive.The goal of those candles is to make all the information easier to interpret by a trader.

500 input length , the price look smoother, supports and resistances are easier to make.

The interpretation of highs and lows are important, the Retrospective Candlestick Chart save you time by showing only huge movements.

Double Exponential SmoothingSingle Exponential Smoothing ( ema ) does not excel in following the data when there is a trend. This situation can be improved by the introduction of a second equation with a second constant gamma .

The gamma constant cant be lower than 0 and cant be greater than 1, higher values of gamma create less lag while preserving smoothness.Higher values of length must be followed by higher values of gamma in order to keep the lag low.

The first smoothing part consist of a classic ema but we add s-s1 to the previous smoothed value, this will help decrease lag.The second smoothing part then updates the trend, which is expressed as the difference between the last two values.

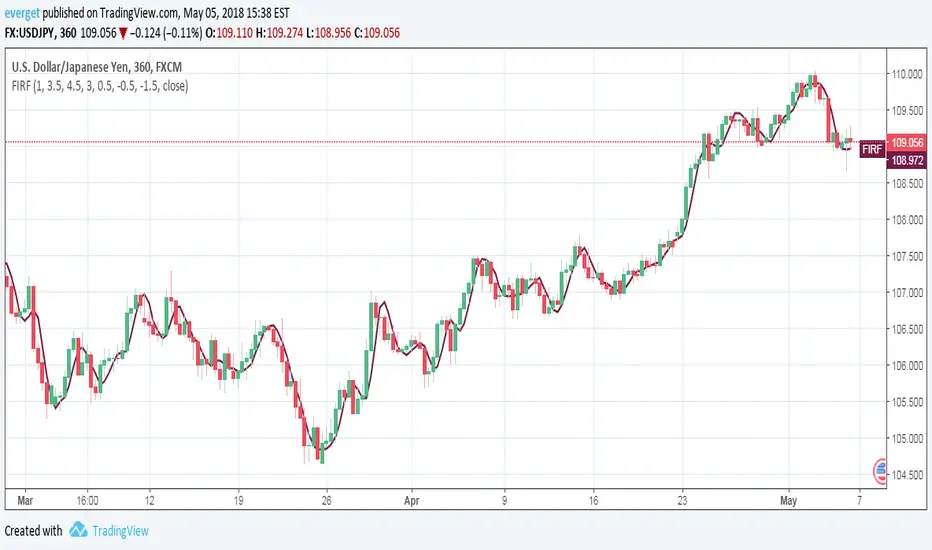

Finite Impulse Response (FIR) FilterFinite Impulse Response (FIR) Filter indicator script.

This indicator was originally developed by John F. Ehlers (Stocks & Commodities V. 20:7 (26-31): Zero-Lag Data Smoothers).

NOTE: Ehlers' favorite FIR filter had 1, 2, 3, 3, 2, 1, 0 coefficients.

Recursive Median FilterRecursive Median Filter indicator script.

This indicator was originally developed by John F. Ehlers (Stocks & Commodities V. 36:03 (8–11): Recursive Median Filters).