Pivot Range - Fisher's Methodology(1D & 3D & W & M)Pivot Range - Fisher's Methodology(1D & 3D & W & M)

Version 2.00

Created by TWA_TradeWithAmir(TWA_PriceActionTips)

Updated 10/29/2020

Based On Mark B. Fisher's ACD Methodology

* 1D Pivot Range, 3D Pivot Range, Weekly Pivot Range & Monthly Pivot Range

Fisher

Daily Risk RangesThis indictor creates daily Risk Ranges using historical volatility, volatility skew and vol-of-vol.

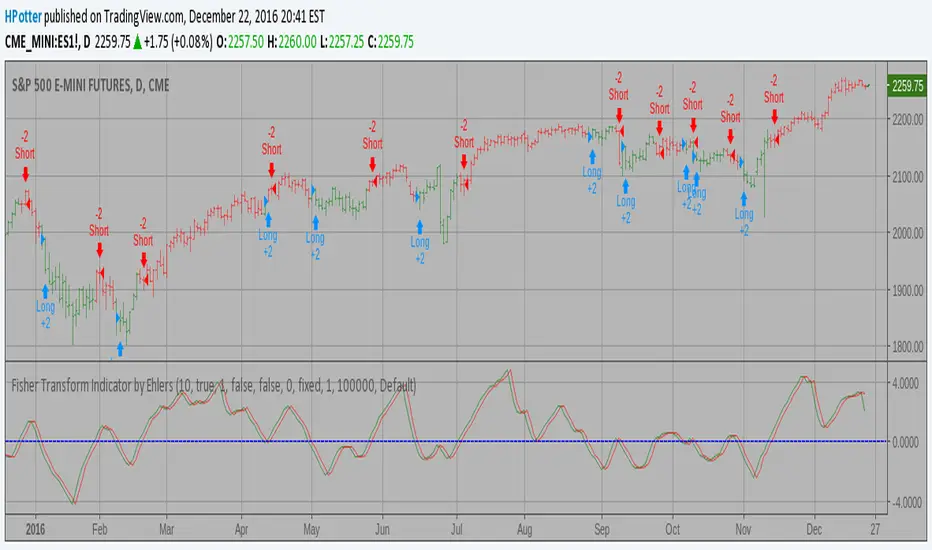

Combo Backtest 123 Reversal & Fisher Transform Indicator This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Market prices do not have a Gaussian probability density function

as many traders think. Their probability curve is not bell-shaped.

But trader can create a nearly Gaussian PDF for prices by normalizing

them or creating a normalized indicator such as the relative strength

index and applying the Fisher transform. Such a transformed output

creates the peak swings as relatively rare events.

Fisher transform formula is: y = 0.5 * ln ((1+x)/(1-x))

The sharp turning points of these peak swings clearly and unambiguously

identify price reversals in a timely manner.

WARNING:

- For purpose educate only

- This script to change bars colors.

Combo Strategy 123 Reversal & Fisher Transform Indicator This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

Market prices do not have a Gaussian probability density function

as many traders think. Their probability curve is not bell-shaped.

But trader can create a nearly Gaussian PDF for prices by normalizing

them or creating a normalized indicator such as the relative strength

index and applying the Fisher transform. Such a transformed output

creates the peak swings as relatively rare events.

Fisher transform formula is: y = 0.5 * ln ((1+x)/(1-x))

The sharp turning points of these peak swings clearly and unambiguously

identify price reversals in a timely manner.

WARNING:

- For purpose educate only

- This script to change bars colors.

Ehlers Fisher Transform Indicator [CC]The Fisher Transform Indicator was created by John Ehlers and the beauty of this indicator is that it provides sharp and clear turning points that are also very early. Buy when the indicator line is green and sell when it is red.

This was a special request so let me know if you would like me to publish other scripts or if you want something custom done!

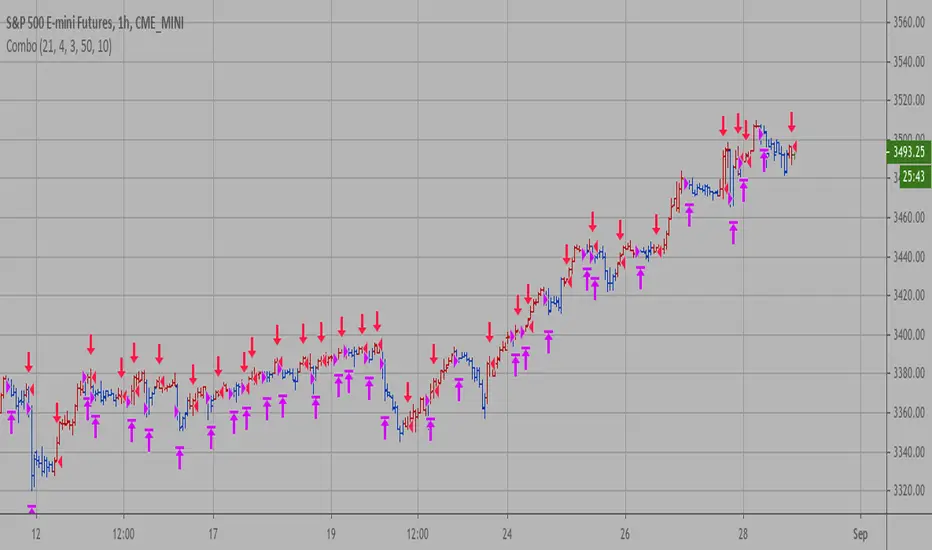

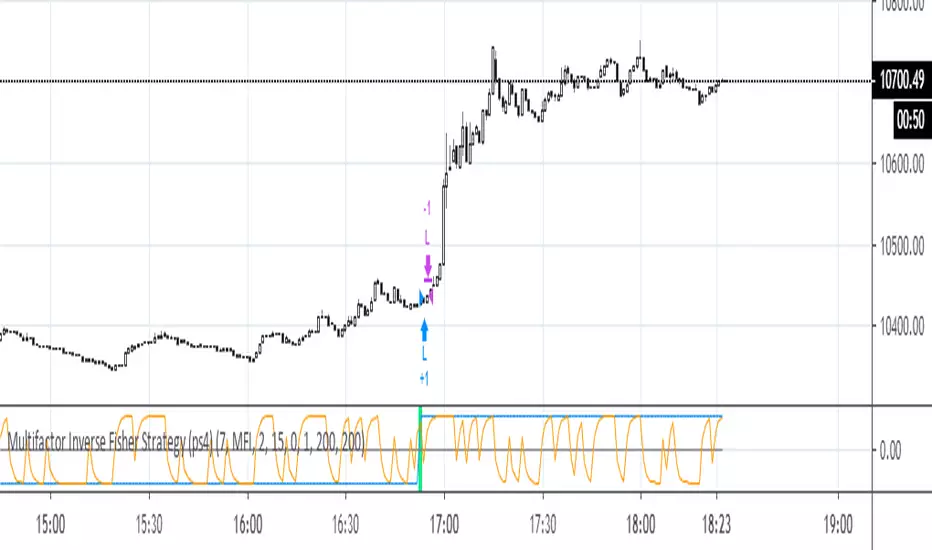

Multifactor Inverse Fisher Strategy (ps4)Best for higher time frames - 30m, 1H, 2H, 3H, 4H, D this strategy uses several factors that are pushed through an Inverse Fisher Transform (IFT). The higher the TF, the better the performance, up to 98%, but the number of deals tends to drop). Middle time frames (5m, 15m) look viable with Scaled Price (Scaled %P) and MFI factors. The factor list can be extended to include cci, stoch, rsi_stoch, emo, macd, cog, dpo, roc, accdist, cctbb, mom, awesome, tva, etc. Some of them need to be rescaled to a 0..100 interval. The IFT produces a value in the -1..1 interval (see: www.mesasoftware.com). This indicator does NOT repaint.

PriceDivergence (ps4)This script implements price divergence module using signals from several factors like:

RSI, RSI Stochastic, MACD, Volume MA, Accumulation/Distribution, Fisher Transform and CCI

Fisher Least Squares Moving AverageIntroduction

I already estimated the least-squares moving average numerous times, one of the most elegant ways was by rescaling a linear function to the price by using the z-score, today i will propose a new smoother (FLSMA) based on the line rescaling approach and the inverse fisher transform of a scaled moving average error with the goal to provide an alternative least-squares smoother, the indicator won't use the correlation coefficient and will try to adresses problems such as overshoots and lag reduction.

Line Rescaling Method

For those who did not see my least squares moving average estimation using the line rescaling method here is a resume, we want to fit a polynomial function of degree 1 to the price by reducing the sum of squares between the price and the filter, squares is a term meaning the squared difference between the price and its estimation. The line rescaling technique work as follow :

1 - get the z-score of a line.

2 - multiply this z-score with the correlation between the price and a line.

3 - multiply the precedent result with the standard deviation of the price, then sum that to a simple moving average.

This process is shorter than the classical least-squares moving average method.

Z-Score Derivation And The Inverse Fisher Transform

The FLSMA will use a similar approach to the line rescaling technique but instead of using the correlation during step 2 we will use an alternative calculated from the error between the estimate and the price.

In order to do so we must use the inverse fisher transform, the inverse fisher transform can take a z-score and scale it in a range of (1,-1), it is possible to estimate the correlation with it. First lets create our modified z-score in the form of : Z = ma((y - Y)/e) where y is the price, Y our output estimate and e the moving average absolute error between the price and Y and lets call it scaled smoothed error , then apply the inverse fisher transform : r = IFT(Z) = tanh(Z) , we then multiply the z-score of the line with it.

Performance

The FLSMA greatly reduce the overshoots, this mean that the maximas of abs(r) are lower than the maxima's of the absolute correlation, such case is not "bad" but we can see that the filter is not closer to the price than the LSMA during trending periods, we can assume the filter don't reduce least-squares as well as the LSMA.

The image above is the running mean of the absolute error of each the FLSMA (in red) and the LSMA (in blue), we could fix this problem by multiplying the smooth scaled error by p where p can be any number, for example :

z = sma(src - nz(b ,src),length)/e * p where p = 2

In red the FLSMA and in blue the FLSMA with p = 2 , the greater p is the less lag the FLSMA will have.

Conclusion

It could be possible to get better results than the LSMA with such design, the presented indicator use its own correlation replacement but it is possible to use anything in a range of (1,-1) to multiply the line z-score. Although the proposed filter only reduce overshoots without keeping the accuracy of the LSMA i believe the code can be useful for others.

Thanks for reading.

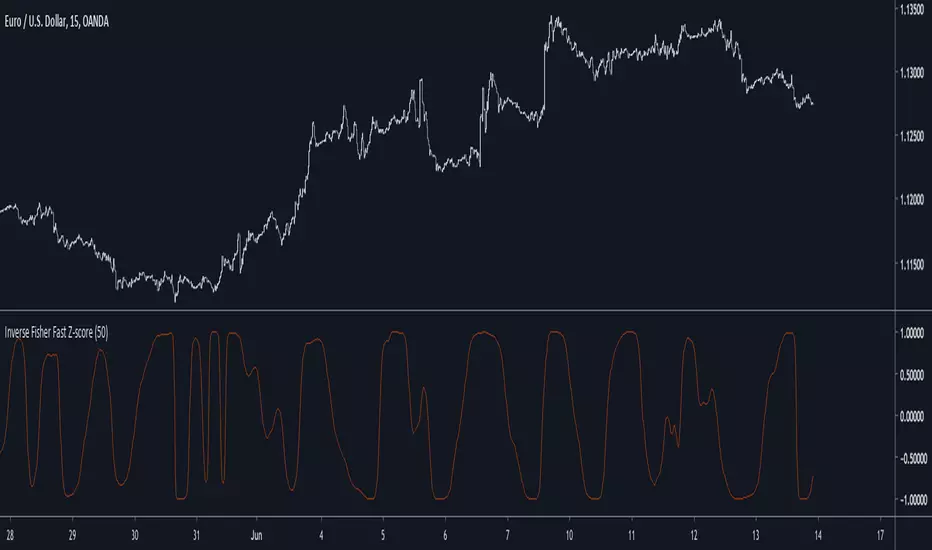

Inverse Fisher Fast Z-scoreIntroduction

The fast z-score is a modification of the classic z-score that allow for smoother and faster results by using two least squares moving averages, however oscillators of this kind can be hard to read and modifying its shape to allow a better interpretation can be an interesting thing to do.

The Indicator

I already talked about the fisher transform, this statistical transform is originally applied to the correlation coefficient, the normal transform allow to get a result similar to a smooth z-score if applied to the correlation coefficient, the inverse transform allow to take the z-score and rescale it in a range of (1,-1), therefore the inverse fisher transform of the fast z-score can rescale it in a range of (1,-1).

inverse = (exp(k*fz) - 1)/(exp(k*fz) + 1)

Here k will control the squareness of the output, an higher k will return heavy side step shapes while a lower k will preserve the smoothness of the output.

Conclusion

The fisher transform sure is useful to kinda filter visual information, it also allow to draw levels since the rescaling is in a specific range, i encourage you to use it.

Notes

During those almost 2 weeks i was even lazier and sadder than ever before, so i think its no use to leave, i also have papers to publish and i need tv for that.

Thanks for reading !

Inverse Fisher Z-Score Introduction

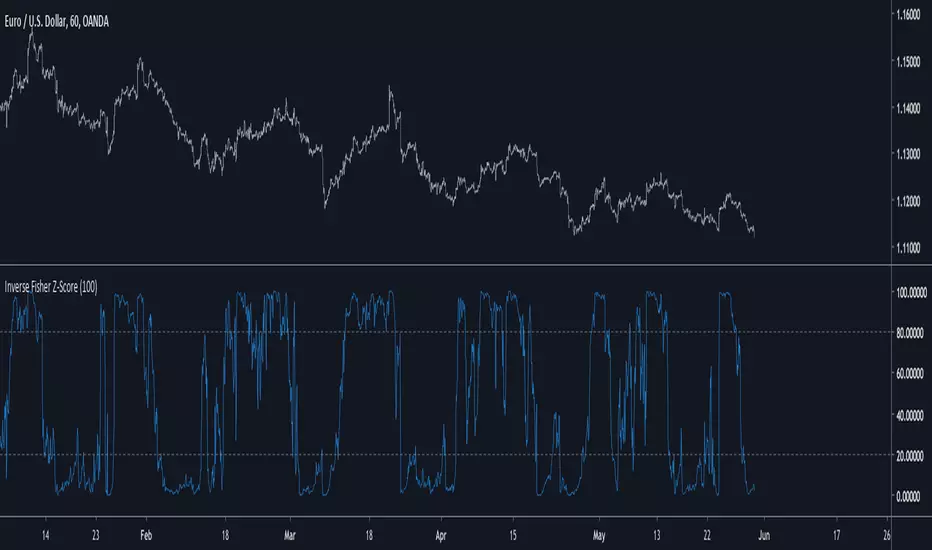

The inverse fisher transform or hyperbolic tangent function is a type os sigmoid function (sometime called squashing function) , those types of functions can rescale a result in a certain range and are widely used in artificial intelligence. More in depth the fisher transform can make the correlation coefficient of a time series normally distributed, in practice if you apply the fisher transform to the correlation coefficient between a time series and a linear function you will end up with an estimate of the z-score of the time series. The inverse transform however can do the contrary, it can take the z-score and transform it into a rough estimate of the correlation coefficient, if your z-score is not smooth then you will have a non-smooth estimate of the correlation coefficient, that's quite nice no ?

The Indicator

The inverse fisher transform of the z-score will produce results in a range of 1/-1, here however i will rescale in a range of 100/0 because its a standard range for oscillators in technical analysis. Values over 80 indicate an overbought market, under 20 an oversold market. The smooth option in the indicator settings will make the indicator use a linearly weighted moving average as input thus resulting in a smoother result.

The indicator with smooth option.

Conclusion

I presented a new oscillator indicator who use the inverse fisher transform of a z-score. Using the fisher transform and its inverse can give a new shape to your indicator, make sure to control the scale of your indicator before applying the fisher transform, the inverse transform should be applied to values in range of 1/-1 but you can use higher limits (2/-2,3/-3...) , however remember that higher limits will approximate an heavy side step function (square shape) . I hope you will find an use to this indicator.

Thanks for reading !

Fisher Stochastic Center of GravityWhat happens when you take the Fisher Transform of a Stochastic Oscillator?

Well, you filter out all the stuff you don't want and are left with super-precise entries!

This indicator works especially well in with a trend-follower in a higher timeframe - iTrend, MAMA, Hull, etc...

How to trade:

Use with another indicator to tell you the current trend.

Take buy and sell signals as you would with the Stoch.

-DasanC

Fisher Transform Multi-Timeframe Backtest (No Trailing)This is the Backtester without Trailing Stops

Credits to mortdiggiddy

Fisher Transform Multi-TimeframePlots the multi-timeframe version of the fisher transform. When the desired interval is less than the chart interval, the intermediate values of the transform will be displayed.

Recursive Median Oscillator & Fisher Transforms RibbonThis is a composite indicator made up of:

- modifided (rescaled) version of evergets version of recursive median oscillator.

- 1996anoojpatels Futur modification of Ehlers Fisher Transform Ribbons Indicator

I think Ehlers attempts to minimise latency in indicators are extremely valuable and some of my most use trading tools. Thanks to all the authors whose iterations keep moving these indicators toward perfection. Here is my contribution.

Missile RSI (RSI of momentum w/ Dominant Cycle length + Fisher)This is a predictive indicator that looks for explosions in momentum of the cycles in price and large shifts in Momentum (Fisher turns the Bimodal PDF into Guassian like) as statistically unlikely events, showing points to exit or reverse positions.

You can adjust the lowpass frequency cuttoff (Aka what cycles you want to remove from the calculations through the super smoother filter).

To be honest you can monkey trade the direction of the Signal if you'd like but the Divergences and Maxing of the values is whats most useful.

Let me know if you guys want me to add anything else.

Ehlers Fisherized Deviation-Scaled OscillatorEhlers Fisherized Deviation-Scaled Oscillator script.

This indicator was originally developed by John F. Ehlers (Stocks & Commodities V. 36:11: Probability - Probably A Good Thing To Know).

Ehlers Fisher Stochastic Relative Vigor Index StrategyBy John Ehlers from his book "Cybernetic Analysis for Stocks and Futures".

Twiggs Money Flow Fisher Transform// Credits to @LazyBear

// This is an experimental indicator (Originaly coded by Lazybear) modified by @haidinurhasfi by applying the Fisher Transform to Twiggs Money Flow.

// Tune the length according to your trading style and instrument

Rocket RSIRocket RSI indicator script.

This indicator was originally developed by John Ehlers (Stocks & Commodities V.36:6, RocketRSI - A Solid Propellant For Your Rocket Science Trading).

Fisher Multi-Pack [DW]This is an experimental study designed to visualize price activity using John Ehlers Fisher Transform and Inverse Fisher Transform methods.

The Ehlers Fisher Transform is a variation of R. A. Fisher's Z transformation.

In this study, there are five oscillator types to choose from:

-Fisher Transform Indicator - A conversion of price's probability distribution to a Gaussian normal distribution with a smoother output

-Inverse Fisher Relative Strength Index - Converts the RSI's distribution to a bounded distribution between 1 and -1 with a smoother output

-Inverse Fisher Stochastic Oscillator - Converts the Stochastic's distribution to a bounded distribution between 1 and -1 with a smoother output

-Inverse Fisher Commodity Channel Index - Converts the CCI's distribution to a bounded distribution between 1 and -1 with a smoother output

-Inverse Fisher Blast Off Momentum - Converts the BOM's distribution to a bounded distribution between 1 and -1 with a smoother output

The study uses a modified set of Bollinger Bands applied to the chosen oscillator to determine trend and impulse activity, which are highlighted by the color scheme.

Custom bar colors are included.

Fisher Transform Ribbons Indicator V1.0Utilizing the Fisher Transform by Ehlers with different lengths based on multipliers will allow you to notice movements in price and understand whether the shift was a correctional wave, or part of the overall trend.

To learn about Fisher Transform , check out the Fisher Transform documentation: www.mesasoftware.com

Fisher has plenty of functionalities. Ribbons provides you with a view of consistency in price action. If all ribbons flip, generally this is a strong signal that the trend is changing. Fisher is extremely punctual (minimum input lag) and robust (doesn't miss movement). Look for everything, including divergences, trends, and Oversold, Overbought points.

Changing length will further provide you more sensitivity in overselling and buying, while numbing chop.

Enjoy!

And for a single Fisher, check out HPotter's Fisher Transform or LazyBear's implementation of the inverse of the Fisher, which has many other interesting properties

Fisher Transform Indicator by Ehlers Backtest v 2.0 Market prices do not have a Gaussian probability density function

as many traders think. Their probability curve is not bell-shaped.

But trader can create a nearly Gaussian PDF for prices by normalizing

them or creating a normalized indicator such as the relative strength

index and applying the Fisher transform. Such a transformed output

creates the peak swings as relatively rare events.

Fisher transform formula is: y = 0.5 * ln ((1+x)/(1-x))

The sharp turning points of these peak swings clearly and unambiguously

identify price reversals in a timely manner.

For signal used zero.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.