3SMA +30 Stan Weinstein +200WMA +alert-crossingIndicator Description: Stan Weinstein Strategy + Key Moving Averages

🔹 Introduction

This indicator combines the Classic Stan Weinstein Strategy with a modern update based on the author’s latest recommendations. It includes key moving averages that help identify trends and potential entry or exit points in the market.

📊 Included Moving Averages (Fully Customizable)

All moving averages in this indicator have modifiable parameters, allowing users to adjust values in the input settings.

1️⃣ 30-Week SMA (Stan Weinstein): A long-term trend indicator defining the asset’s main trend.

2️⃣ 40-Week SMA (Weinstein Update): An adjusted version recommended by the author in his recent updates.

3️⃣ 10-Day SMA: Displays short-term price action and helps confirm trend changes.

4️⃣ 100-Day SMA: A medium-term trend measure used by traders to assess trend strength.

5️⃣ 200-Day WMA (Weighted Moving Average): A very long-term indicator that filters market noise and confirms solid trends.

🔍 How to Interpret It

✔️ 30/40-Week SMA in an uptrend → Confirms an accumulation phase or an upward price trend.

✔️ Price above the 200-WMA → Indicates a strong and healthy long-term trend.

✔️ 10-SMA crossing other moving averages → Can signal an early entry or exit opportunity.

✔️ 100-SMA vs. 200-WMA → A breakout of the 100-SMA above the 200-WMA may signal a new bullish phase.

🚨 Built-in Alerts (Key Crossovers)

The indicator includes automatic alerts to notify traders when key moving averages cross, allowing timely reactions:

🔔 10-SMA crossing the 40-SMA → Possible medium-term trend shift.

🔔 10-SMA crossing the 200-WMA → Confirmation of a stronger trend.

🔔 40-SMA crossing the 200-WMA → Long-term trend reversal signal.

💡 Customization: All moving average periods can be adjusted in the input settings, making the indicator flexible for different trading strategies.

Forecasting

Open Vertical Lines [TradeWithRon]This indicator allows traders to draw vertical lines manually or automatically based on the current or specified higher timeframes. It is a versatile tool designed to help users identify and mark significant changes in the market, such as new candle formations, based on a selected or auto-adjusted timeframe.

Open Source

Features:

Timeframe Customization: Users can either manually specify a desired timeframe (e.g., 1-hour, 1-day, etc.) or enable the "Auto" feature, which automatically adjusts the timeframe based on the current chart's timeframe for better alignment with different trading strategies.

Customizable Line Style: The vertical line can be drawn in three different styles: Solid, Dashed, or Dotted, giving users the flexibility to choose their preferred appearance for better chart readability.

Line Color: Users can select the color of the vertical line with transparency options to match their chart's visual preferences.

Auto Timeframe Adjustments: The "Auto Align" option dynamically adjusts the timeframe used for vertical lines depending on the chart's current timeframe. For example, if you’re using a lower timeframe (e.g., 5 minutes), the indicator will automatically switch to a higher timeframe (e.g., 1 hour or daily) to mark vertical lines, ensuring the lines correspond to higher timeframe price action.

Vertical Line Placement:

A vertical line is placed each time a new candle appears on the chart, marking key moments for the user to analyze market movements. This can be helpful for marking the start of new trading sessions or significant events in the market.

How to Use:

1. Apply the indicator to your chart.

2. Configure the preferred timeframe settings (either fixed or auto-align).

3. Customize the line style and color according to your visual preference.

4. The indicator will automatically place vertical lines on the chart when a new candle is formed, based on your selected timeframe.

AltSeasonality - MTFAltSeason is more than a brief macro market cycle — it's a condition. This indicator helps traders identify when altcoins are gaining strength relative to Bitcoin dominance, allowing for more precise entries, exits, and trade selection across any timeframe.

The key for altcoin traders is that the lower the timeframe, the higher the alpha.

By tracking the TOTAL3/BTC.D ratio — a real-time measure of altcoin strength versus Bitcoin — this tool highlights when capital is rotating into or out of altcoins. It works as a bias filter, helping traders avoid low-conviction setups, especially in chop or during BTC-led conditions.

________________________________________________________________________

It works well on the 1D chart to validate swing entries during strong altcoin expansion phases — especially when TOTAL3/BTC.D breaks out while BTCUSD consolidates.

On the 4H or 1D chart, rising TOTAL3/BTC.D + a breakout on your altcoin = high-conviction setup. If BTC is leading, fade the move or reduce size. Consider pairing with the Accumulation - Distribution Candles, optimized for the 1D (not shown).

🔍 Where this indicator really excels, however, is on the 1H and 15M charts, where short-term traders need fast bias confirmation before committing to a move. Designed for scalpers, intraday momentum traders, and tactical swing setups.

Use this indicator to confirm whether an altcoin breakout is supported by broad market flow — or likely to fail due to hidden BTC dominance pressure.

________________________________________________________________________

🧠 How it works:

- TOTAL3 = market cap of altcoins (excl. BTC + ETH)

- BTC.D = Bitcoin dominance as % of total market cap

- TOTAL3 / BTC.D = a normalized measure of altcoin capital strength vs Bitcoin

- BTCUSD = trend baseline and comparison anchor

The indicator compares these forces side-by-side, using a normalized dual-line ribbon. There is intentionally no "smoothing".

When TOTAL3/BTC.D is leading, the ribbon shifts to an “altseason active” phase. When BTCUSD regains control, the ribbon flips back into BTC dominance — signaling defensive posture.

________________________________________________________________________

💡 Strategy Example:

On the 1H chart, a crossover into altseason → check the 15M chart for confirmation. Consider adding the SUPeR TReND 2.718 for confirmation (not shown). If both align, you have trend + flow confluence. If BTCUSD is leading or ribbon is mixed, reduce exposure or wait for confirmation. Further confirmation via Volume breakouts in your specific coin.

⚙️ Features:

• MTF source selection (D, 1H, 15M)

• Normalized ribbon (TOTAL3/BTC.D vs BTCUSD)

• Cross-aware fill shading

• Custom color and transparency controls

• Optional crossover markers

• Midline + zone guides (0.2 / 0.5 / 0.8)

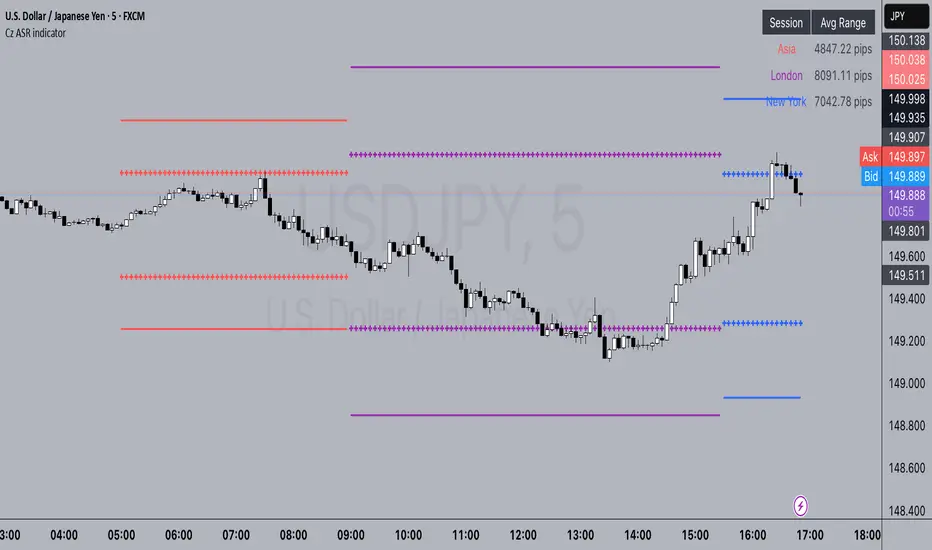

Cz ASR indicatorAverage session range indicator built by me. Great tool to gauge volatility and intraday reversal zones. Great for FX as there is an included table that shows range in pips; however, this can be applied across all assets as a volatility measure.

How it works:

The script measures the range of sessions, including Asia, London, and New York. The lookback period could be adjusted so you can find what length works best and is most accurate. This is then averaged out to provide the ASR. This provides us with an upper and lower bound of which the price could potentially fluctuate in based on the past session ranges. I have also added the 50% ASR, which is also a super useful metric for reversals or continuations.

There is also a configurable UTC so that you can adjust the indicator so it can accurately measure the range within certain sessions.

Note - different session start and stop times vary from market to market. I have set the code to the standard forex market opens however, if you wish to change the time ,you are able to do so by editing the variables in the script

Enjoy :)

Vertical Line at Specified HoursThis script helps you easily separate time.

This indicator can be used for many different purposes. For example, I use it to separate different days and sessions.

Features :

1- Ability to use 10 vertical lines simultaneously

2- The Possibility to change the color of lines

3- The Possibility to change the line type

Tip : The times you enter in the input section must be in the New York time zone.

ATR - Asymmetric Turbulence Ribbon🧭 Asymmetric Turbulence Ribbon (ATR)

The Asymmetric Turbulence Ribbon (ATR) is an enhanced and reimagined version of the standard Average True Range (ATR) indicator. It visualizes not just raw volatility, but the structure, momentum, and efficiency of volatility through a multi-layered visual approach.

It contains two distinct visual systems:

1. A zero-centered histogram that expresses how current volatility compares to its historical average, with intensity and color showing speed and conviction

2. A braided ribbon made of dual ATR-based moving averages that highlight transitions in volatility behavior—whether volatility is expanding or contracting

The name reflects its purpose: to capture asymmetric, evolving turbulence in market behavior, through structure-aware volatility tracking.

_______________________________________________________________

🔧 Inputs (Fibonacci defaults)

ATR Length

Lookback period for ATR calculation (default: 13)

ATR Base Avg. Length

Moving average period used as the zero baseline for histogram (default: 55)

ATR ROC Lookback

Number of bars to measure rate of change for histogram color mapping (default: 8)

Timeframe Override

Optionally calculate ATR values from a higher or fixed timeframe (e.g., 1D) for macro-volatility overlay

Show Ribbon Fill

Toggles colored fill between ATR EMA and HMA lines

Show ATR MAs

Toggles visibility of ATR EMA and HMA lines

Show Crossover Markers

Shows directional triangle markers where ATR EMA and HMA cross

Show Histogram

Toggles the entire histogram display

_______________________________________________________________

📊 Histogram Component: Volatility Energy Profile

The histogram shows how far the current ATR is from its moving average baseline, centered around zero. This lets you interpret volatility pressure—whether it's expanding, contracting, or preparing to reverse.

To complement this, the indicator also plots the raw ATR line in aqua. This is the actual average true range value—used internally in both the histogram and ribbon calculations. By default, it appears as a slightly thicker line, providing a clear reference point for comparing historical volatility trends and absolute levels.

Use the baseline ATR to:

- Compare real-time volatility to previous peaks or troughs

- Monitor how ATR behaves near histogram flips or ribbon crossovers

- Evaluate volatility phases in absolute terms alongside relative momentum

The ATR line is particularly helpful for users who want to keep tabs on raw volatility values while still benefiting from the enhanced visual storytelling of the histogram and ribbon systems.

Each histogram bar is colored based on the rate of change (ROC) in ATR: The faster ATR rises or falls, the more intense the color. Meanwhile, the opacity of each bar is adjusted by the effort/result ratio of the price candle (body vs. range), showing how much price movement was achieved with conviction.

Color Interpretation:

🔴 Red

Strong volatility expansion

Market entering or deepening into a volatility burst

Seen during breakouts, panic moves, or macro shock events

Often accompanied by large real candle bodies

🟠 Orange

Moderate volatility expansion

Heating up phase, often precedes breakouts

Common in strong trending environments

Signals tightening before acceleration

🟡 Yellow

Mild volatility increase

Transitional state—energy building, not yet exploding

Appears in early trend development or pullbacks

🟢 Green

Mild volatility contraction

ATR cooling off

Seen during consolidation, reversion, or range balance

Good time to assess upcoming directional setups

🔵 Aqua

Moderate compression

Volatility is clearly declining

Signals consolidation within larger structure

Pre-breakout zones often form here

🔵 Deep Blue

Strong volatility compression

Market is coiling or dormant

Can signal upcoming squeeze or fade environment

Often followed by sharp expansion

Opacity scaling:

Brighter bars = efficient, directional price action (strong bodies)

Faded bars = indecision, chop, absorption, or wick-heavy structure

Together, color and opacity give a 2D view of market volatility: Hue = the type and direction of volatility

Opacity = the quality and structure behind it

Use this to gauge whether volatility is rising with conviction, fading into neutrality, or compressing toward breakout potential.

_______________________________________________________________

🪡 Ribbon Component: Volatility Rhythm Structure

The ribbon overlays two moving averages of ATR:

EMA (yellow) – faster, more reactive

HMA (orange) – smoother, more rhythmic

Their relationship creates the ribbon logic:

Yellow fill (EMA > HMA)

Short-term volatility is increasing faster than the longer-term rhythm

Signals active expansion and engagement

Orange fill (HMA > EMA)

Volatility is decaying or leveling off

Suggests possible exhaustion, pullback, or range

Crossover triangle markers (optional, off by default to avoid clutter) identify the moment of shift in volatility phase.

The ribbon reflects the shape of volatility over time—ideal for mapping cyclical energy shifts, transitional states, and alignment between current and average volatility.

_______________________________________________________________

📐 Strategy Application

Use the Asymmetric Turbulence Ribbon to:

- Detect volatility expansions before breakouts or directional runs

- Spot compression zones that precede structural ruptures

- Visually separate efficient moves from noisy market activity

- Confirm or fade trade setups based on underlying energy state

- Track the volatility environment across multiple timeframes using the override

_______________________________________________________________

🎯 Ideal Timeframes

Designed to function across all timeframes, but particularly powerful on intraday to daily ranges (1H to 1D)

Use the timeframe override to anchor your chart in higher-timeframe volatility context, like daily ATR behavior influencing a 1H setup.

_______________________________________________________________

🧬 Customization Tips

- Increase ATR ROC Lookback for smoother color transitions

- Extend ATR Base Avg Length for more macro-driven histogram centering

- Disable the histogram for ribbon-only rhythm view

- Use opacity and color shifts in the histogram to detect stealth energy builds

- Align ATR phases with structure or order flow tools for high-quality setups

ATR and Moving AverageUsing ATR and Moving Average: A Technical Analysis Strategy

The Average True Range (ATR) and the Moving Average are two important technical analysis tools that can be used together to identify trading opportunities in the market. In this article, we will explore how to use these two tools and how the crossover between them can indicate changes in the market.

What is ATR?

The Average True Range (ATR) is a measure of the volatility of an asset, which calculates the average true range of an asset over a period of time. The true range is the difference between the closing price and the opening price of an asset, or the difference between the closing price and the highest or lowest price of the day. ATR is an important measure of volatility, as it helps to identify the magnitude of price fluctuations of an asset.

What is Moving Average?

The Moving Average is a technical analysis tool that calculates the average price of an asset over a period of time. The Moving Average can be used to identify trends and price patterns, and is an important tool for traders. There are different types of Moving Averages, including the Simple Moving Average (SMA), the Exponential Moving Average (EMA), and the Weighted Moving Average (WMA).

Crossover between ATR and Moving Average

The crossover between ATR and Moving Average can be an important indicator of changes in the market. When ATR crosses above the Moving Average, it may indicate that the volatility of the asset is increasing and that the price may be about to rise. This occurs because ATR is increasing, which means that the true range of the asset is increasing, and the Moving Average is being surpassed, which means that the price is rising.

On the other hand, when ATR crosses below the Moving Average, it may indicate that the volatility of the asset is decreasing and that the price may be about to fall. This occurs because ATR is decreasing, which means that the true range of the asset is decreasing, and the Moving Average is being surpassed, which means that the price is falling.

Trading Strategies

There are several trading strategies that can be used with the crossover between ATR and Moving Average. Some of these strategies include:

Buying when ATR crosses above the Moving Average, with the expectation that the price will rise.

Selling when ATR crosses below the Moving Average, with the expectation that the price will fall.

Using the crossover between ATR and Moving Average as a filter for other trading strategies, such as trend analysis or pattern recognition.

In summary, the crossover between ATR and Moving Average can be an important indicator of changes in the market, and can be used as a technical analysis tool to identify trading opportunities. However, it is important to remember that no trading strategy is foolproof, and that it is always important to use a disciplined approach and manage risk adequately.

EURUSD Swing High/Low ProjectionBikini Bottom custom projection tool. Aimed to project tops and bottoms. Don't use unless you understand how it works :)

Professional MSTI+ Trading Indicator"Professional MSTI+ Trading Indicator" is a comprehensive technical analysis tool that combines over 20 indicators to generate high-quality trading signals and assess market sentiment. The script integrates standard indicators (MACD, RSI, Bollinger Bands, Stochastic, Simple Moving Averages, and Volume Analysis) with advanced components (Squeeze Momentum, Fisher Transform, True Strength Index, Heikin-Ashi, Laguerre RSI, Hull MA) and further includes metrics such as ADX, Chaikin Money Flow, Williams %R, VWAP, and EMA for in-depth market analysis.

Key Features:

Multiple Presets for Different Trading Styles:

Choose from optimal configurations like Professional, Swing Trading, Day Trading, Scalping, or Reversal Hunter. Note that the presets may not work perfectly on all pairs, and manual calibration might be required. This flexibility allows you to fine-tune the settings to align with your unique strategies and signals.

Multi-Layered Signal Filtering:

Filters based on trend, volume, and volatility help eliminate false signals, enhancing the accuracy of market entries.

Comprehensive Fear & Greed Index:

The indicator aggregates data from RSI, volatility, momentum, trend, and volume to gauge overall market sentiment, providing an additional layer of market context.

Dynamic Information Panel:

Displays detailed status updates for each component (e.g., MACD, RSI, Laguerre RSI, TSI, Fisher Transform, Squeeze, Hull MA, etc.) along with a visual strength bar that represents the intensity of the trading signal.

Signal Generation:

Buy and sell signals are generated when a predefined number of conditions are met and confirmed over multiple bars. These signals are clearly displayed on the chart with arrows, making it easier to spot potential entry and exit points.

Alert Setup:

Built-in alert conditions allow you to receive real-time notifications when trading signals are generated, helping you stay on top of market movements.

"Professional MSTI+ Trading Indicator" is designed to enhance your trading strategy by providing a multi-faceted market analysis and an intuitive visual interface. While the presets offer a robust starting point, they may require manual calibration on certain pairs, giving you the flexibility to configure your own unique strategies and signals.

Eclipse Dates IndicatorThis TradingView indicator displays vertical lines on eclipse dates from 1980 to 2030, with comprehensive filtering options for different types of eclipses.

Features

Date Range: Covers 221 eclipse events from 1980 to 2030

Eclipse Types: Filter by Solar and/or Lunar eclipses

Eclipse Subtypes: Filter by Total, Partial, Annular, Penumbral, and Hybrid eclipses

Year Range Selection: Focus on specific decades (1980-1990, 1990-2000, etc.)

Visual Customization: Separate styling for Solar and Lunar eclipses

Line Appearance: Customize color, style, and width

Label Options: Show/hide labels with customizable appearance

Eclipse Types

Show Solar Eclipses: Toggle visibility of Solar eclipses

Show Lunar Eclipses: Toggle visibility of Lunar eclipses

Eclipse Subtypes

Show Total Eclipses: Toggle visibility of Total eclipses

Show Partial Eclipses: Toggle visibility of Partial eclipses

Show Annular Eclipses: Toggle visibility of Annular eclipses

Show Penumbral Eclipses: Toggle visibility of Penumbral eclipses

Show Hybrid Eclipses: Toggle visibility of Hybrid eclipses

Visual Settings

Solar/Lunar Eclipse Line Color: Set the color for eclipse lines

Solar/Lunar Eclipse Line Style: Choose between solid, dashed, or dotted lines

Solar/Lunar Eclipse Line Width: Set the width of eclipse lines

Solar/Lunar Label Text Color: Set the color for label text

Solar/Lunar Label Background Color: Set the background color for labels

General Settings

Show Eclipse Labels: Toggle visibility of eclipse labels

Label Size: Choose between tiny, small, normal, or large labels

Extend Lines to Chart Borders: Toggle whether lines extend to chart borders

Year Range: Filter eclipses by decade (1980-1990, 1990-2000, etc.)

Usage Tips

For optimal visualization, use daily or weekly timeframes

When analyzing specific periods, use the Year Range filter

To focus on specific eclipse types, use the type and subtype filters

For cleaner charts, you can hide labels and only show lines

Customize colors to match your chart theme

Data Source

Eclipse data is sourced from NASA's Five Millennium Catalog of Solar Eclipses and includes both solar and lunar eclipses from 1980 to 2030.

Gold Futures vs Spot (Candlestick + Line Overlay)📝 Script Description: Gold Futures vs Spot

This script was developed to compare the price movements between Gold Futures and Spot Gold within a specific time frame. The primary goals of this script are:

To analyze the price spread between Gold Futures and Spot

To identify potential arbitrage opportunities caused by price discrepancies

To assist in decision-making and enhance the accuracy of gold market analysis

🔧 Key Features:

Fetches price data from both Spot and Futures markets (from APIs or chart sources)

Converts and aligns data for direct comparison

Calculates the price spread (Futures - Spot)

Visualizes the spread over time or exports the data for further analysis

📅 Date Created:

🧠 Additional Notes:

This script is ideal for investors, gold traders, or analysts who want to understand the relationship between the Futures and Spot markets—especially during periods of high volatility. Unusual spreads may signal shifts in market sentiment or the actions of institutional players.

Econometrica by [SS]This is Econometrica, an indicator that aims to bridge a big gap between the resources available for analysis of fundamental data and its impact on tickers and price action.

I have noticed a general dearth of available indicators that offer insight into how fundamentals impact a ticker and provide guidance on how they these economic factors influence ticker behaviour.

Enter Econometrica. Econometrica is a math based indicator that aims to co-integrate and model indicator price action in relation to critical economic metrics.

Econometrica supports the following US based economic data:

CPI

Non-Farm Payroll

Core Inflation

US Money Supply

US Central Bank Balance Sheet

GDP

PCE

Let's go over the functions of Econometrica.

Creating a Regression Cointegrated Model

The first thing Econometrica does is creates a co-integrated regression, as you see in the main chart, predicting ticker value ranges from fundamental economic data.

You can visualize this in the main chart above, but here are some other examples:

SPY vs Core Inflation:

BA vs PCE:

QQQ vs US Balance Sheet:

The band represents the anticipated range the ticker should theoretically fall in based on the underlying economic value. The indicator will breakdown the relationship between the economic indicator and the ticker more precisely. In the images above, you can see how there are some metrics provided, including Stationairty, lagged correlation, Integrated Correlation and R2. Let's discuss these very briefly:

Stationarity: checks to ensure that the relationship between the economic indicator and ticker is stationary. Stationary data is important for making unbiased inferences and projections, so having data that is stationary is valuable.

Lagged Correlation: This is a very interesting metric. Lagged correlation means whether there is a delay in the economic indicator and the response of the ticker. Typically, you will observed a lagged correlation between an economic indicator and price of a ticker, as it can take some time for economic changes to reach the market. This lagged correlation will provide you with how long it takes for the economic indicator to catch up with the ticker in months.

Integrated Correlation: This metric tells you how good of a fit the regression bands are in relation to the ticker price. A higher correlation, means the model is better at consistent and accurate information about the anticipated range for the ticker in relation to the economic indicator.

R2: Provides information on the variance and degree of model fit. A high R2 value means that the model is capable of explaining a large amount of variance between the economic indicator and the ticker price action.

Explaining the Relationship

Owning to the fact that the indicator is a bit on the mathy side (it has to be to do this kind of task), I have included ability for the indicator to explain and make suggestions based on the underlying data. It can assess the model's fit and make suggestions for tweaking. It can also explain the implications of the data being presented in the model.

Here is an example with QQQ and the US Balance Sheet:

This helps to simplify and interpret the results you are looking at.

Forecasting the Economic Indicator

In addition to assessing the economic indicator's impact on the ticker, the indicator is also capable of forecasting out the economic indicator over the next 25 releases.

Here is an example of the CPI forecast:

Overall use of the indicator

The indicator is meant to bridge the gap between Technical Analysis and Fundamental Analysis.

Any trader who is attune to fundamentals would benefit from this, as this provides you with objective data on how and to what extent fundamental and economic data impacts tickers.

It can help affirm hypothesis and dispel myths objectively.

It also omits the need from having to perform these types of analyses outside of Tradingview (i.e. in excel, R or Python), as you can get the data in just a few licks of enabling the indicator.

Conclusion

I have tried to make this indicator as user friendly as possible. Though it uses a lot of math, it is fairly straight forward to interpret.

The band plotted can be considered the fair market value or FMV of the ticker based on the underlying economic data, provided the indicator tells you that the relationship is significant (and it will blatantly give you this information verbatim, you don't have to interpret the math stuff).

This is US economic data only. It does not pull economic data from other countries. You can absolutely see how US economic data impacts other markets like the TSX, BANKNIFTY, NIFTY, DAX etc. but the indicator is only pulling US economic data.

That is it!

I hope you enjoy it and find this helpful!

Thanks everyone and safe trades as always 🚀🚀🚀

FiveFactorEdgeUses ATR14, TSI, RSI, Fast Stochastic and Slow Stochastic information to determine potential high and low price, trend strength and direction. The information ia easy to read, self-descriptive and color coded for quick reference. Since it incorporates 5 different elements it could be used by itself but as with any indicator it's highly recommended to use it with other tried and true indicators.

M2 Global Liquidity Index - X Days LeadThis custom indicator overlays the Bitcoin price chart with the Global Liquidity M2 chart, providing a unique perspective on how monetary supply might influence Bitcoin's price movements. The indicator distinguishes between past and future segments of the liquidity data using two distinct colors.

- Past Segment: The portion of the Global Liquidity M2 chart that has already passed is displayed in one color, allowing users to assess historical correlations with Bitcoin's price.

- Future Segment: The upcoming part of the liquidity chart is shown in a different color, offering insights into potential future impacts on Bitcoin's price trajectory.

by walkin

SuperTrader Trend Analysis and Trade Study DashboardSuperTrader Trend Analysis and Trade Study Dashboard

Overview

This script offers a multi-faceted look at market behavior. It combines signals from different momentum indicators, daily cross checks, and a specialized dashboard to reveal trend strength, potential divergences, and how far price has traveled from its recent averages.

Three Musketeers Method

This script uses a special set of three indicators (the “Three Musketeers”) to determine bullish or bearish pressure on the current chart.

Trend Condition – Compares fast vs. slow EMAs (50 and 200) and checks which side of the line price is favoring.

Mean Reversion Condition – Watches RSI crossing typical oversold or overbought thresholds (e.g., crossing above 30 or below 70).

Bollinger Condition – Checks whether price pushes above/below the Bollinger Bands (based on a 20 SMA + standard deviations).

When at least two out of these three conditions align in a bullish way, the script issues a Buy Signal . Conversely, if at least two align in a bearish way, a Sell Signal is triggered. This “Three Musketeers” synergy ensures multiple confirmations before calling a potential market turn.

Mag 8 Daily Performance

The script tracks eight highly influential stocks (AAPL, AMZN, GOOG, NFLX, NVDA, TSLA, META, MSFT) to see which are green (higher) or red (lower) compared to yesterday’s close. It then prints a quick tally – helpful in gauging overall market mood via these major players.

Golden / Death Cross Signals

On a daily time frame, the script notes when the 50-day SMA crosses above or below the 200-day SMA. A “Golden Cross” often signals rising momentum, while a “Death Cross” can hint at oncoming weakness.

RSI & Divergence Checks

RSI helps identify hidden turning points. Whenever a bullish or bearish divergence is spotted, the script updates you via a concise readout.

Hardcoded Settings

EMA lengths for trend checks, Bollinger parameters, etc., are locked in, letting you focus on adjusting only the pivotal study inputs (e.g., RSI length, VIDYA momentum).

VIDYA Trend Line & Fill

Built on an adaptive Variable Index Dynamic Average, it plots a line that quickly reacts to changing momentum. Users can set a “Trend Band Distance” to mark ATR-based thresholds around that line, identifying possible breakouts or breakdowns.

YoYo Distance

This concept measures how far price strays from SMA(10). If it’s too far, the script colors your display to indicate potential snapbacks.

Gap Up/Down Probability

By weighing volume, MACD signals, and whether price sits above/below its midrange, the script estimates probabilities of a gap up or down on the next daily candle.

Table Output & Trend Label

Turning on Show Table Widget reveals a quick dashboard on the chart detailing RSI, CCI, divergences, bull/bear scores, and more. A label on the last bar further summarizes overall trend, gap distance, and the Mag 8 snapshot – perfect for a fast read of current market posture.

Use this script to unify multiple signals in one place, see how far price has ventured from typical patterns, and get daily cross signals plus real-time bullish/bearish calls – all at a glance.

Smart % Levels📈 Smart % Levels – Visualize Significant Percentage Moves

What it does:

This indicator plots horizontal levels based on a percentage change from the previous day's close (or open, if selected). It allows traders to visualize price movements relative to meaningful thresholds like ±1%, ±2%, etc.

What makes it different:

Unlike other level indicators, Smart % Levels only displays the relevant levels based on current price action. This avoids clutter by showing only the levels that are being approached or crossed by the current price. It's a clean and dynamic way to visualize key price zones for intraday analysis.

How it works:

- Select between using the previous day's Close or Open as the reference

- Choose the percentage spacing between levels (e.g., 1%, 0.5%, etc.)

- Enable optional labels to see the exact percentage of each level

- Automatically filters levels to only show those between yesterday's price and today's current price

- Includes customization for colors, line styles, widths, and opacity

Best for:

Day traders and scalpers who want a quick, clean view of how far the current price has moved from yesterday’s reference, without being overwhelmed by unnecessary lines.

Extra notes:

- The levels are recalculated each day at the market open

- All graphics reset at the start of each session to maintain clarity

- This script avoids repainting by only plotting levels relative to available historical data (no lookahead)

This tool is for informational purposes only and should not be considered as financial advice. Always do your own research before making trading decisions.

Daily ProtractorDaily Protractor Indicator

Overview

The Daily Protractor is a visually intuitive tool designed for traders who want to analyze price action through angular measurements on a 5-minute chart. By overlaying a protractor on the chart, this indicator helps identify potential support, resistance, and trend directions based on angular relationships from the first 5-minute candle of each day. It’s particularly useful for intraday traders looking to incorporate geometric analysis into their strategies for spot or strike charts.

Key Features

Dynamic Protractor Overlay: Draws a protractor centered on the low of the first 5-minute candle of each day, with customizable radius in both bars (horizontal) and price units (vertical).

Angular Measurements: Displays angles in 5-degree increments, covering a full 360° circle or a 105° to -105° (91° to 269°) half-circle, depending on user preference.

Customizable Display:

Adjust the number of days to display protractors (up to 5 days).

Customize line colors for different angle ranges (0° to 180°, 180° to 360°, and 0° specifically).

Modify line thickness, label size, and label colors for better visibility.

Center Point Highlight: Marks the center of each protractor with a labeled point for easy reference.

Efficient Design:

Optimized with max_lines_count, max_labels_count, and max_bars_back to ensure smooth performance on TradingView.

How It Works

The indicator identifies the first 5-minute candle of each day and uses its low price as the center point for a protractor. It then draws lines at 5-degree intervals, radiating from the center, with each line representing an angle from 0° to 360°. Labels at the end of each line display the angle in degrees, with negative values shown for angles between 195° and 345° (e.g., 270° is displayed as -90°). The protractor’s radius can be adjusted in both time (bars) and price units, allowing traders to scale the tool to their chart’s characteristics.

Usage Instructions

Add to Chart:

Apply the indicator to a 5-minute chart of your chosen instrument (e.g., spot or strike charts).

Interpret the Protractor:

Use the angular lines to identify potential price levels or trend directions.

The 0° line (horizontal) can act as a reference for horizontal support/resistance.

Angles between 0° and 180° (upper half) and 180° and 360° (lower half) are color-coded for quick identification.

Customize Settings:

Toggle the Show 105° to -105° option to display a half-circle (91° to 269°) instead of a full 360° protractor.

Adjust the Radius in Bars and Radius in Price Units to scale the protractor to your chart.

Set the Maximum Days to Display to control how many daily protractors are shown.

Modify line thickness, colors, and label settings to suit your visual preferences.

Customization Options

Protractor Settings:

Show 105° to -105° (91° to 269°): Toggle between a full circle or a half-circle protractor.

Radius in Bars: Set the horizontal span of the protractor (default: 75 bars).

Radius in Price Units: Set the vertical span in price units (default: 1000.0).

Maximum Days to Display: Limit the number of protractors shown (default: 5 days).

Line Settings:

Line Thickness: Adjust the thickness of the protractor lines (1 or 2).

Line Color (0° to 180°): Color for the upper half (default: light blue).

Line Color (180° to 360°): Color for the lower half (default: light red).

Line Color (0°): Color for the 0° line (default: black).

Label Settings:

Label Size: Choose between small, normal, or large labels.

Label Color (0° to 180°): Color for labels in the upper half (default: red).

Label Color (180° to 360°): Color for labels in the lower half (default: green).

Notes

The indicator was designed with the help of Grok3 for use on 5-minute charts only, as it relies on the first 5-minute candle of the day to set the protractor’s center.

For best results, adjust the radius settings to match the volatility and price scale of your instrument. However, where the price is in single digits it is advised to switch off the labels or I would suggest not to use the same.

The protractor can be used alongside other technical tools to confirm trends, reversals, or key price levels.

Limitations: This cannot be used on instruments that trade for more than 75 candles with a timeframe of 5 minutes as the angles would not cover the entire trading window. I am working coming up with a script to address this limitation.

Feedback

I’d love to hear your thoughts! If you find the Daily Protractor helpful or have suggestions for improvements, please leave a comment or reach out. Happy trading!

Composite Reversal IndicatorOverview

The "Composite Reversal Indicator" aggregates five technical signals to produce a composite score that ranges from -5 (strongly bearish) to +5 (strongly bullish). These signals come from:

Relative Strength Index (RSI)

Moving Average Convergence Divergence (MACD)

Accumulation/Distribution (A/D)

Volume relative to its moving average

Price proximity to support and resistance levels

Each signal contributes a value of +1 (bullish), -1 (bearish), or 0 (neutral) to the total score. The raw score is plotted as a histogram, and a smoothed version is plotted as a colored line to highlight trends.

Step-by-Step Explanation

1. Customizable Inputs

The indicator starts with user-defined inputs that allow traders to tweak its settings. These inputs include:

RSI: Length (e.g., 14), oversold level (e.g., 30), and overbought level (e.g., 70).

MACD: Fast length (e.g., 12), slow length (e.g., 26), and signal length (e.g., 9).

Volume: Moving average length (e.g., 20) and multipliers for high (e.g., 1.5) and low (e.g., 0.5) volume thresholds.

Price Levels: Period for support and resistance (e.g., 50) and proximity percentage (e.g., 2%).

Score Smoothing: Length for smoothing the score (e.g., 5).

These inputs make the indicator adaptable to different trading styles, assets, or timeframes.

2. Indicator Calculations

The script calculates five key indicators using the input parameters:

RSI: Measures momentum and identifies overbought or oversold conditions.

Formula: rsi = ta.rsi(close, rsi_length)

Example: With a length of 14, it analyzes the past 14 bars of closing prices.

MACD: Tracks trend and momentum using two exponential moving averages (EMAs).

Formula: = ta.macd(close, macd_fast, macd_slow, macd_signal)

Components: MACD line (fast EMA - slow EMA), signal line (EMA of MACD line).

Accumulation/Distribution (A/D): A volume-based indicator showing buying or selling pressure.

Formula: ad = ta.accdist

Reflects cumulative flow based on price and volume.

Volume Moving Average: A simple moving average (SMA) of trading volume.

Formula: vol_ma = ta.sma(volume, vol_ma_length)

Example: A 20-bar SMA smooths volume data.

Support and Resistance Levels: Key price levels based on historical lows and highs.

Formulas:

support = ta.lowest(low, price_level_period)

resistance = ta.highest(high, price_level_period)

Example: Over 50 bars, it finds the lowest low and highest high.

These calculations provide the raw data for generating signals.

3. Signal Generation

Each indicator produces a signal based on specific conditions:

RSI Signal:

+1: RSI < oversold level (e.g., < 30) → potential bullish reversal.

-1: RSI > overbought level (e.g., > 70) → potential bearish reversal.

0: Otherwise.

Logic: Extreme RSI values suggest price may reverse.

MACD Signal:

+1: MACD line > signal line → bullish momentum.

-1: MACD line < signal line → bearish momentum.

0: Equal.

Logic: Crossovers indicate trend shifts.

A/D Signal:

+1: Current A/D > previous A/D → accumulation (bullish).

-1: Current A/D < previous A/D → distribution (bearish).

0: Unchanged.

Logic: Rising A/D shows buying pressure.

Volume Signal:

+1: Volume > high threshold (e.g., 1.5 × volume MA) → strong activity (bullish).

-1: Volume < low threshold (e.g., 0.5 × volume MA) → weak activity (bearish).

0: Otherwise.

Logic: Volume spikes often confirm reversals.

Price Signal:

+1: Close near support (within proximity %, e.g., 2%) → potential bounce.

-1: Close near resistance (within proximity %) → potential rejection.

0: Otherwise.

Logic: Price near key levels signals reversal zones.

4. Composite Score

The raw composite score is the sum of the five signals:

Formula: score = rsi_signal + macd_signal + ad_signal + vol_signal + price_signal

Range: -5 (all signals bearish) to +5 (all signals bullish).

Purpose: Combines multiple perspectives into one number.

5. Smoothed Score

A smoothed version of the score reduces noise:

Formula: score_ma = ta.sma(score, score_ma_length)

Example: With a length of 5, it averages the score over 5 bars.

Purpose: Highlights the trend rather than short-term fluctuations.

6. Visualization

The indicator plots two elements:

Raw Score: A gray histogram showing the composite score per bar.

Style: plot.style_histogram

Color: Gray.

Smoothed Score: A line that changes color:

Green: Score > 0 (bullish).

Red: Score < 0 (bearish).

Gray: Score = 0 (neutral).

Style: plot.style_line, thicker line (e.g., linewidth=2).

These visuals make it easy to spot potential reversals.

How It Works Together

The indicator combines signals from:

RSI: Momentum extremes.

MACD: Trend shifts.

A/D: Buying/selling pressure.

Volume: Confirmation of moves.

Price Levels: Key reversal zones.

By summing these into a composite score, it filters out noise and provides a unified signal. A high positive score (e.g., +3 to +5) suggests a bullish reversal, while a low negative score (e.g., -3 to -5) suggests a bearish reversal. The smoothed score helps traders focus on the trend.

Practical Use

Bullish Reversal: Smoothed score is green and rising → look for buying opportunities.

Bearish Reversal: Smoothed score is red and falling → consider selling or shorting.

Neutral: Score near 0 → wait for clearer signals.

Traders can adjust inputs to suit their strategy, making it versatile for stocks, forex, or crypto.

Pivot S/R with Volatility Filter## *📌 Indicator Purpose*

This indicator identifies *key support/resistance levels* using pivot points while also:

✅ Detecting *high-volume liquidity traps* (stop hunts)

✅ Filtering insignificant pivots via *ATR (Average True Range) volatility*

✅ Tracking *test counts and breakouts* to measure level strength

---

## *⚙ SETTINGS – Detailed Breakdown*

### *1️⃣ ◆ General Settings*

#### *🔹 Pivot Length*

- *Purpose:* Determines how many bars to analyze when identifying pivots.

- *Usage:*

- *Low values (5-20):* More pivots, better for scalping.

- *High values (50-200):* Fewer but stronger levels for swing trading.

- *Example:*

- Pivot Length = 50 → Only the most significant highs/lows over 50 bars are marked.

#### *🔹 Test Threshold (Max Test Count)*

- *Purpose:* Sets how many times a level can be tested before being invalidated.

- *Example:*

- Test Threshold = 3 → After 3 tests, the level is ignored (likely to break).

#### *🔹 Zone Range*

- *Purpose:* Creates a price buffer around pivots (±0.001 by default).

- *Why?* Markets often respect "zones" rather than exact prices.

---

### *2️⃣ ◆ Volatility Filter (ATR)*

#### *🔹 ATR Period*

- *Purpose:* Smoothing period for Average True Range calculation.

- *Default:* 14 (standard for volatility measurement).

#### *🔹 ATR Multiplier (Min Move)*

- *Purpose:* Requires pivots to show *meaningful price movement*.

- *Formula:* Min Move = ATR × Multiplier

- *Example:*

- ATR = 10 pips, Multiplier = 1.5 → Only pivots with *15+ pip swings* are valid.

#### *🔹 Show ATR Filter Info*

- Displays current ATR and minimum move requirements on the chart.

---

### *3️⃣ ◆ Volume Analysis*

#### *🔹 Volume Change Threshold (%)*

- *Purpose:* Filters for *unusual volume spikes* (institutional activity).

- *Example:*

- Threshold = 1.2 → Requires *120% of average volume* to confirm signals.

#### *🔹 Volume MA Period*

- *Purpose:* Lookback period for "normal" volume calculation.

---

### *4️⃣ ◆ Wick Analysis*

#### *🔹 Wick Length Threshold (Ratio)*

- *Purpose:* Ensures rejection candles have *long wicks* (strong reversals).

- *Formula:* Wick Ratio = (Upper Wick + Lower Wick) / Candle Range

- *Example:*

- Threshold = 0.6 → 60% of the candle must be wicks.

#### *🔹 Min Wick Size (ATR %)*

- *Purpose:* Filters out small wicks in volatile markets.

- *Example:*

- ATR = 20 pips, MinWickSize = 1% → Wicks under *0.2 pips* are ignored.

---

### *5️⃣ ◆ Display Settings*

- *Show Zones:* Toggles support/resistance shaded areas.

- *Show Traps:* Highlights liquidity traps (▲/▼ symbols).

- *Show Tests:* Displays how many times levels were tested.

- *Zone Transparency:* Adjusts opacity of zones.

---

## *🎯 Practical Use Cases*

### *1️⃣ Liquidity Trap Detection*

- *Scenario:* Price spikes *above resistance* then reverses sharply.

- *Requirements:*

- Long wick (Wick Ratio > 0.6)

- High volume (Volume > Threshold)

- *Outcome:* *Short Trap* signal (▼) appears.

### *2️⃣ Strong Support Level*

- *Scenario:* Price bounces *3 times* from the same level.

- *Indicator Action:*

- Labels the level with test count (3/5 = 3 tests out of max 5).

- Turns *red* if broken (Break Count > 0).

Deep Dive: How This Indicator Works*

This indicator combines *four professional trading concepts* into one powerful tool:

1. *Classic Pivot Point Theory*

- Identifies swing highs/lows where price previously reversed

- Unlike basic pivot indicators, ours uses *confirmed pivots only* (filtered by ATR)

2. *Volume-Weighted Validation*

- Requires unusual trading volume to confirm levels

- Filters out "phantom" levels with low participation

3. *ATR Volatility Filtering*

- Eliminates insignificant price swings in choppy markets

- Ensures only meaningful levels are plotted

4. *Liquidity Trap Detection*

- Spots institutional stop hunts where markets fake out traders

- Uses wick analysis + volume spikes for high-probability signals

---

Deep Dive: How This Indicator Works*

This indicator combines *four professional trading concepts* into one powerful tool:

1. *Classic Pivot Point Theory*

- Identifies swing highs/lows where price previously reversed

- Unlike basic pivot indicators, ours uses *confirmed pivots only* (filtered by ATR)

2. *Volume-Weighted Validation*

- Requires unusual trading volume to confirm levels

- Filters out "phantom" levels with low participation

3. *ATR Volatility Filtering*

- Eliminates insignificant price swings in choppy markets

- Ensures only meaningful levels are plotted

4. *Liquidity Trap Detection*

- Spots institutional stop hunts where markets fake out traders

- Uses wick analysis + volume spikes for high-probability signals

---

## *📊 Parameter Encyclopedia (Expanded)*

### *1️⃣ Pivot Engine Settings*

#### *Pivot Length (50)*

- *What It Does:*

Determines how many bars to analyze when searching for swing highs/lows.

- *Professional Adjustment Guide:*

| Trading Style | Recommended Value | Why? |

|--------------|------------------|------|

| Scalping | 10-20 | Captures short-term levels |

| Day Trading | 30-50 | Balanced approach |

| Swing Trading| 50-200 | Focuses on major levels |

- *Real Market Example:*

On NASDAQ 5-minute chart:

- Length=20: Identifies levels holding for ~2 hours

- Length=50: Finds levels respected for entire trading day

#### *Test Threshold (5)*

- *Advanced Insight:*

Institutions often test levels 3-5 times before breaking them. This setting mimics the "probe and push" strategy used by smart money.

- *Psychology Behind It:*

Retail traders typically give up after 2-3 tests, while institutions keep testing until stops are run.

---

### *2️⃣ Volatility Filter System*

#### *ATR Multiplier (1.0)*

- *Professional Formula:*

Minimum Valid Swing = ATR(14) × Multiplier

- *Market-Specific Recommendations:*

| Market Type | Optimal Multiplier |

|------------------|--------------------|

| Forex Majors | 0.8-1.2 |

| Crypto (BTC/ETH) | 1.5-2.5 |

| SP500 Stocks | 1.0-1.5 |

- *Why It Matters:*

In EUR/USD (ATR=10 pips):

- Multiplier=1.0 → Requires 10 pip swings

- Multiplier=1.5 → Requires 15 pip swings (fewer but higher quality levels)

---

### *3️⃣ Volume Confirmation System*

#### *Volume Threshold (1.2)*

- *Institutional Benchmark:*

- 1.2x = Moderate institutional interest

- 1.5x+ = Strong smart money activity

- *Volume Spike Case Study:*

*Before Apple Earnings:*

- Normal volume: 2M shares

- Spike threshold (1.2): 2.4M shares

- Actual volume: 3.1M shares → STRONG confirmation

---

### *4️⃣ Liquidity Trap Detection*

#### *Wick Analysis System*

- *Two-Filter Verification:*

1. *Wick Ratio (0.6):*

- Ensures majority of candle shows rejection

- Formula: (UpperWick + LowerWick) / Total Range > 0.6

2. *Min Wick Size (1% ATR):*

- Prevents false signals in flat markets

- Example: ATR=20 pips → Min wick=0.2 pips

- *Trap Identification Flowchart:*

Price Enters Zone →

Spikes Beyond Level →

Shows Long Wick →

Volume > Threshold →

TRAP CONFIRMED

---

## *💡 Master-Level Usage Techniques*

### *Institutional Order Flow Analysis*

1. *Step 1:* Identify pivot levels with ≥3 tests

2. *Step 2:* Watch for volume contraction near levels

3. *Step 3:* Enter when trap signal appears with:

- Wick > 2×ATR

- Volume > 1.5× average

### *Multi-Timeframe Confirmation*

1. *Higher TF:* Find weekly/monthly pivots

2. *Lower TF:* Use this indicator for precise entries

3. *Example:*

- Weekly pivot at $180

- 4H shows liquidity trap → High-probability reversal

---

## *⚠ Critical Mistakes to Avoid*

1. *Using Default Settings Everywhere*

- Crude oil needs higher ATR multiplier than bonds

2. *Ignoring Trap Context*

- Traps work best at:

- All-time highs/lows

- Major psychological numbers (00/50 levels)

3. *Overlooking Cumulative Volume*

- Check if volume is building over multiple tests

IU Smart Flow SystemDESCRIPTION

The IU Smart Flow System is a powerful and dynamic order flow-based strategy designed to capture high-probability trades by analyzing bullish and bearish imbalances, trend direction, and RSI strength. It identifies trading opportunities by aligning order flow conditions with the prevailing trend and momentum, making it suitable for trend-following and momentum-based trading.

This system utilizes a unique combination of:

- Order flow score to gauge market imbalance

- Trend filter using SMA and ATR to confirm market direction

- RSI to ensure entry only during strong momentum

USER INPUTS:

- Imbalance Length: Defines the lookback period for calculating bullish and bearish imbalances. (Default: 10)

- Trend Length: Determines the length of the SMA to evaluate the trend direction. (Default: 50)

- RSI Length: Specifies the RSI period to assess momentum strength. (Default: 14)

LONG CONDITIONS:

Long entries are triggered when:

- Order flow score is positive, indicating bullish imbalance

- Price is above the bullish trend level (SMA + ATR), confirming an uptrend

- RSI is above 50, indicating bullish momentum

- No active short position is currently open

SHORT CONDITIONS:

Short entries are triggered when:

- Order flow score is negative, indicating bearish imbalance

- Price is below the bearish trend level (SMA - ATR), confirming a downtrend

- RSI is below 50, indicating bearish momentum

- No active long position is currently open

WHY IT IS UNIQUE:

- Imbalance-Based Approach: Unlike traditional strategies that rely solely on price action, this system evaluates bullish and bearish imbalances to anticipate order flow direction.

- Adaptive Trend Filter: The combination of SMA and ATR dynamically adjusts to market volatility, providing a reliable trend confirmation mechanism.

- Momentum Validation with RSI: Ensures that entries are taken only in the direction of strong momentum, reducing false signals.

HOW USERS CAN BENEFIT FROM IT:

- Enhanced Trade Accuracy: Aligning order flow, trend, and momentum reduces false signals and improves trade success rates.

- Versatile Application: Suitable for various markets and timeframes, making it adaptable to different trading styles.

- Clear Trade Signals: Provides clear entry labels and alerts, ensuring traders never miss a potential opportunity.

- Visual Clarity: The filled region between bullish and bearish trends highlights trend direction, enhancing decision-making.

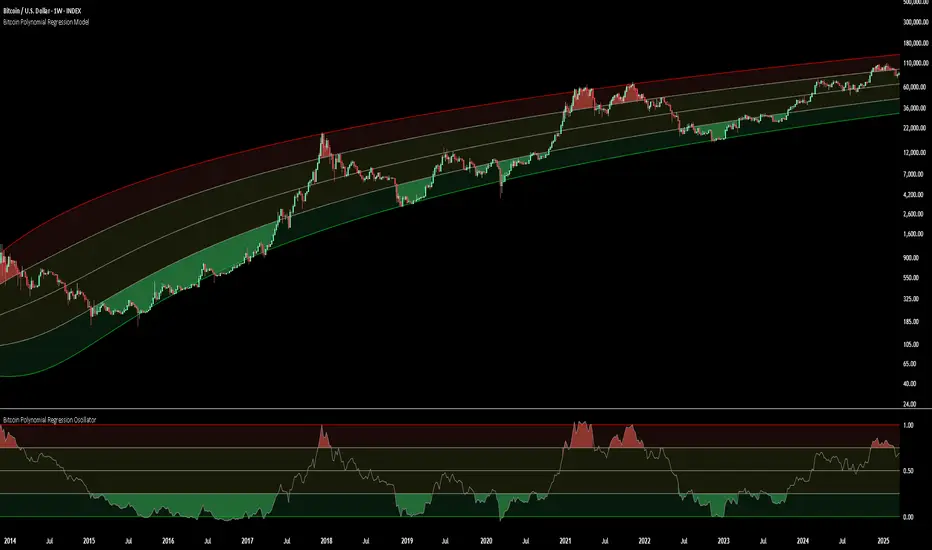

Bitcoin Polynomial Regression ModelThis is the main version of the script. Click here for the Oscillator part of the script.

💡Why this model was created:

One of the key issues with most existing models, including our own Bitcoin Log Growth Curve Model , is that they often fail to realistically account for diminishing returns. As a result, they may present overly optimistic bull cycle targets (hence, we introduced alternative settings in our previous Bitcoin Log Growth Curve Model).

This new model however, has been built from the ground up with a primary focus on incorporating the principle of diminishing returns. It directly responds to this concept, which has been briefly explored here .

📉The theory of diminishing returns:

This theory suggests that as each four-year market cycle unfolds, volatility gradually decreases, leading to more tempered price movements. It also implies that the price increase from one cycle peak to the next will decrease over time as the asset matures. The same pattern applies to cycle lows and the relationship between tops and bottoms. In essence, these price movements are interconnected and should generally follow a consistent pattern. We believe this model provides a more realistic outlook on bull and bear market cycles.

To better understand this theory, the relationships between cycle tops and bottoms are outlined below:https://www.tradingview.com/x/7Hldzsf2/

🔧Creation of the model:

For those interested in how this model was created, the process is explained here. Otherwise, feel free to skip this section.

This model is based on two separate cubic polynomial regression lines. One for the top price trend and another for the bottom. Both follow the general cubic polynomial function:

ax^3 +bx^2 + cx + d.

In this equation, x represents the weekly bar index minus an offset, while a, b, c, and d are determined through polynomial regression analysis. The input (x, y) values used for the polynomial regression analysis are as follows:

Top regression line (x, y) values:

113, 18.6

240, 1004

451, 19128

655, 65502

Bottom regression line (x, y) values:

103, 2.5

267, 211

471, 3193

676, 16255

The values above correspond to historical Bitcoin cycle tops and bottoms, where x is the weekly bar index and y is the weekly closing price of Bitcoin. The best fit is determined using metrics such as R-squared values, residual error analysis, and visual inspection. While the exact details of this evaluation are beyond the scope of this post, the following optimal parameters were found:

Top regression line parameter values:

a: 0.000202798

b: 0.0872922

c: -30.88805

d: 1827.14113

Bottom regression line parameter values:

a: 0.000138314

b: -0.0768236

c: 13.90555

d: -765.8892

📊Polynomial Regression Oscillator:

This publication also includes the oscillator version of the this model which is displayed at the bottom of the screen. The oscillator applies a logarithmic transformation to the price and the regression lines using the formula log10(x) .

The log-transformed price is then normalized using min-max normalization relative to the log-transformed top and bottom regression line with the formula:

normalized price = log(close) - log(bottom regression line) / log(top regression line) - log(bottom regression line)

This transformation results in a price value between 0 and 1 between both the regression lines. The Oscillator version can be found here.

🔍Interpretation of the Model:

In general, the red area represents a caution zone, as historically, the price has often been near its cycle market top within this range. On the other hand, the green area is considered an area of opportunity, as historically, it has corresponded to the market bottom.

The top regression line serves as a signal for the absolute market cycle peak, while the bottom regression line indicates the absolute market cycle bottom.

Additionally, this model provides a predicted range for Bitcoin's future price movements, which can be used to make extrapolated predictions. We will explore this further below.

🔮Future Predictions:

Finally, let's discuss what this model actually predicts for the potential upcoming market cycle top and the corresponding market cycle bottom. In our previous post here , a cycle interval analysis was performed to predict a likely time window for the next cycle top and bottom:

In the image, it is predicted that the next top-to-top cycle interval will be 208 weeks, which translates to November 3rd, 2025. It is also predicted that the bottom-to-top cycle interval will be 152 weeks, which corresponds to October 13th, 2025. On the macro level, these two dates align quite well. For our prediction, we take the average of these two dates: October 24th 2025. This will be our target date for the bull cycle top.

Now, let's do the same for the upcoming cycle bottom. The bottom-to-bottom cycle interval is predicted to be 205 weeks, which translates to October 19th, 2026, and the top-to-bottom cycle interval is predicted to be 259 weeks, which corresponds to October 26th, 2026. We then take the average of these two dates, predicting a bear cycle bottom date target of October 19th, 2026.

Now that we have our predicted top and bottom cycle date targets, we can simply reference these two dates to our model, giving us the Bitcoin top price prediction in the range of 152,000 in Q4 2025 and a subsequent bottom price prediction in the range of 46,500 in Q4 2026.

For those interested in understanding what this specifically means for the predicted diminishing return top and bottom cycle values, the image below displays these predicted values. The new values are highlighted in yellow:

And of course, keep in mind that these targets are just rough estimates. While we've done our best to estimate these targets through a data-driven approach, markets will always remain unpredictable in nature. What are your targets? Feel free to share them in the comment section below.

Bitcoin Polynomial Regression OscillatorThis is the oscillator version of the script. Click here for the other part of the script.

💡Why this model was created:

One of the key issues with most existing models, including our own Bitcoin Log Growth Curve Model , is that they often fail to realistically account for diminishing returns. As a result, they may present overly optimistic bull cycle targets (hence, we introduced alternative settings in our previous Bitcoin Log Growth Curve Model).

This new model however, has been built from the ground up with a primary focus on incorporating the principle of diminishing returns. It directly responds to this concept, which has been briefly explored here .

📉The theory of diminishing returns:

This theory suggests that as each four-year market cycle unfolds, volatility gradually decreases, leading to more tempered price movements. It also implies that the price increase from one cycle peak to the next will decrease over time as the asset matures. The same pattern applies to cycle lows and the relationship between tops and bottoms. In essence, these price movements are interconnected and should generally follow a consistent pattern. We believe this model provides a more realistic outlook on bull and bear market cycles.

To better understand this theory, the relationships between cycle tops and bottoms are outlined below:https://www.tradingview.com/x/7Hldzsf2/

🔧Creation of the model:

For those interested in how this model was created, the process is explained here. Otherwise, feel free to skip this section.

This model is based on two separate cubic polynomial regression lines. One for the top price trend and another for the bottom. Both follow the general cubic polynomial function:

ax^3 +bx^2 + cx + d.

In this equation, x represents the weekly bar index minus an offset, while a, b, c, and d are determined through polynomial regression analysis. The input (x, y) values used for the polynomial regression analysis are as follows:

Top regression line (x, y) values:

113, 18.6

240, 1004

451, 19128

655, 65502

Bottom regression line (x, y) values:

103, 2.5

267, 211

471, 3193

676, 16255

The values above correspond to historical Bitcoin cycle tops and bottoms, where x is the weekly bar index and y is the weekly closing price of Bitcoin. The best fit is determined using metrics such as R-squared values, residual error analysis, and visual inspection. While the exact details of this evaluation are beyond the scope of this post, the following optimal parameters were found:

Top regression line parameter values:

a: 0.000202798

b: 0.0872922

c: -30.88805

d: 1827.14113

Bottom regression line parameter values:

a: 0.000138314

b: -0.0768236

c: 13.90555

d: -765.8892

📊Polynomial Regression Oscillator:

This publication also includes the oscillator version of the this model which is displayed at the bottom of the screen. The oscillator applies a logarithmic transformation to the price and the regression lines using the formula log10(x) .

The log-transformed price is then normalized using min-max normalization relative to the log-transformed top and bottom regression line with the formula:

normalized price = log(close) - log(bottom regression line) / log(top regression line) - log(bottom regression line)

This transformation results in a price value between 0 and 1 between both the regression lines.

🔍Interpretation of the Model:

In general, the red area represents a caution zone, as historically, the price has often been near its cycle market top within this range. On the other hand, the green area is considered an area of opportunity, as historically, it has corresponded to the market bottom.

The top regression line serves as a signal for the absolute market cycle peak, while the bottom regression line indicates the absolute market cycle bottom.

Additionally, this model provides a predicted range for Bitcoin's future price movements, which can be used to make extrapolated predictions. We will explore this further below.

🔮Future Predictions:

Finally, let's discuss what this model actually predicts for the potential upcoming market cycle top and the corresponding market cycle bottom. In our previous post here , a cycle interval analysis was performed to predict a likely time window for the next cycle top and bottom:

In the image, it is predicted that the next top-to-top cycle interval will be 208 weeks, which translates to November 3rd, 2025. It is also predicted that the bottom-to-top cycle interval will be 152 weeks, which corresponds to October 13th, 2025. On the macro level, these two dates align quite well. For our prediction, we take the average of these two dates: October 24th 2025. This will be our target date for the bull cycle top.

Now, let's do the same for the upcoming cycle bottom. The bottom-to-bottom cycle interval is predicted to be 205 weeks, which translates to October 19th, 2026, and the top-to-bottom cycle interval is predicted to be 259 weeks, which corresponds to October 26th, 2026. We then take the average of these two dates, predicting a bear cycle bottom date target of October 19th, 2026.

Now that we have our predicted top and bottom cycle date targets, we can simply reference these two dates to our model, giving us the Bitcoin top price prediction in the range of 152,000 in Q4 2025 and a subsequent bottom price prediction in the range of 46,500 in Q4 2026.

For those interested in understanding what this specifically means for the predicted diminishing return top and bottom cycle values, the image below displays these predicted values. The new values are highlighted in yellow:

And of course, keep in mind that these targets are just rough estimates. While we've done our best to estimate these targets through a data-driven approach, markets will always remain unpredictable in nature. What are your targets? Feel free to share them in the comment section below.

VIX Implied MovesKey Features:

Three Timeframe Bands:

Daily: Blue bands showing ±1σ expected move

Weekly: Green bands showing ±1σ expected move

30-Day: Red bands showing ±1σ expected move

Calculation Methodology:

Uses VIX's annualized volatility converted to specific timeframes using square root of time rule

Trading day convention (252 days/year)

Band width = Price × (VIX/100) ÷ √(number of periods)

Visual Features:

Colored semi-transparent backgrounds between bands

Progressive line thickness (thinner for shorter timeframes)

Real-time updates as VIX and ES prices change

Example Calculation (VIX=20, ES=5000):

Daily move = 5000 × (20/100)/√252 ≈ ±63 points

Weekly move = 5000 × (20/100)/√50 ≈ ±141 points

Monthly move = 5000 × (20/100)/√21 ≈ ±218 points

This indicator helps visualize expected price ranges based on current volatility conditions, with wider bands indicating higher market uncertainty. The probabilistic ranges represent 68% confidence levels (1 standard deviation) derived from options pricing.