Multi-Asset Ratio (20 vs 5) - LuchapThis indicator calculates and displays the ratio between the sum of the prices of several base assets and the sum of the prices of several quote assets. You can select up to 20 base assets and 5 quote assets, and enable or disable each asset individually to refine your analysis. This ratio allows you to quickly evaluate the relative performance of different groups of assets.

Forecasting

Reversal Probability Zone & Levels [LuxAlgo]The Reversal Probability Zone & Levels tool allows traders to identify a zone starting from the last detected reversal to highlight the probability of where the next reversal would be from a price and time perspective.

Price and time levels within the zone are displayed for up to 4 percentiles defined by the user.

🔶 USAGE

By default, the tool displays a zone with the 25th, 50th, 75th and 90th percentiles on both the price and time axis, indicating where, when and how many of the past reversals have occurred.

Traders can select the length for swing detection and the maximum number of reversals for probability calculations. The tool considers both bullish and bearish reversals separately, which means that if the last reversal was a swing high, the zone would show the probabilities for the last defined Maximum reversals

The Maximum reversals value has a direct impact on the probabilities, the more data traders use the more significant the result, probabilities over 10 occurrences are far weak compared to probabilities over 1000 occurrences.

🔹 Percentiles

Traders can fine-tune the percentile parameters in the settings panel.

A given percentile means that the number of occurrences in the data set is less than or equal to the percentile.

In English, this means

Percentile 20th: 20% of the occurrences are less than or equal to this value, so 80% of the occurrences are greater than this value.

Percentile 50th: 50% of the occurrences are below and 50% are above this value.

Percentile 80th: 80% of occurrences are lower than or equal to this value, so 20% of occurrences are greater than this value.

🔹 Normalize data

The Normalize Data feature allows traders to make an apples to apples comparison when we have a lot of historical data on high timeframe charts, using returns between swings instead of raw price.

🔹 Display Style

By default, the tool has the No overlapping feature enabled to display a clean chart, traders can turn it off, but this can fill the chart with too much information and barely see the price.

Traders can enable/disable settings to show only the last zone and the swing markers on the chart.

🔶 SETTINGS

Swing Length: The maximum length in bars used to identify a swing

Maximum Reversals: Maximum number of reversals included in calculations

Normalize Data: Use returns between swings instead of raw price

Percentiles: Enable/disable each of the four percentiles and select the percentile number, line style, colors, and size

🔹 Style

No Overlapping Zones: Enable or disable the No overlap between zones feature

Show Only Last Zone: Enable/disable display of last zone only

Show Marks: Enable/disable reversal markers

Kalman Filter Trend BreakersThe Kalman filter is a recursive algorithm developed in 1960 by Rudolf E. Kálmán, a Hungarian-American engineer and mathematician, that provides optimal estimates of a system's state by combining noisy measurements with a predictive model. It is widely used in control systems, signal processing, and finance for tracking and forecasting.

In trading, KF might be a good replacement for a moving average, as it reacts to price changes in a different way. Not only it follows price direction, but can also track the velocity of price change. This specific behaviour of KF is used in this indicator to track changes in trends.

Trend is characterized by price moving directionally, however, any trend comes to pause or complete stop and reversal, as the price changes more slowly (a trend fades into a sideways movement for a while) or the price movement changes direction, thus making a reversal.

This indicator detects the points where such changes occur (trend breaker points), and produces signals, which serve as points of current trend pausing or reversing. By applying different settings for KF calculation, you can produce less or more signals that indicate change in trend character, and either detect only significant trends changes, or less and shorter trends changes as well.

The signals do not differentiate the exact type of a trend change (it can be a brief trend pause followed by a continuation, as well as a complete reversal). However, once you are in a trend, the significant velocity change indicates a change in trend structure. In this sense, trend breaker signals should not be followed blindly, and can be used only as trend (and subsequently, position) exit confirmations, but not the entry contrarian confirmations.

For better visual representation, you can use chart signals attached to bars, and additionally paint a vertical gradient at each signal which shows significant trend deceleration.

Kalman filter calculations used in this indicator are partially based on an open-source code from @loxx which was published in 2022 as Kalman filter overlay .

Bollinger Bands with Narrow ConsolidationThe indicator is based on the standard Bollinger Bands indicator in TradingView. Its main difference is the ability to display narrow consolidation zones (with an adjustable percentage) and generate signals in these zones.

Narrow consolidation zones can be considered as a signal before the start of a strong trend, whether upward or downward.

Индикатор построен на стандартном индикаторе полос боллинджера в трейдинг вью. Его отличие заключается в том, что здесь есть возможность отображения зон узкой консолидации (процент настраивается) и генерации сигналов на этих зонах.

Зоны узкой консолидации можно рассматривать как сигнал перед началом сильного треда как восходящего, так и нисходящего.

Markov + Monte Carlo Simulation with EVMarkov Monte Carlo Projection (MMCP) – A Probabilistic Approach to Price Forecasting

Introduction: A New Approach to Price Projection

The Markov Monte Carlo Projection (MMCP) is an advanced stochastic forecasting tool that models potential future price paths using a combination of Markov Chain transition probabilities and Monte Carlo simulations. Unlike traditional technical indicators that rely on fixed formulas, MMCP employs probability distributions and simulated price movement paths to estimate future price behavior dynamically.

This indicator is designed to adapt to changing market conditions and provides traders with a probabilistic framework rather than a fixed forecast. By incorporating volatility modeling, MMCP enables traders to size projections proportionally to recent price action, making it an adaptive and flexible forecasting tool.

Mathematical Foundations

Markov Chains: Modeling Probability of Price Movements

A Markov Chain is a stochastic process where the probability of transitioning to the next state depends only on the current state and not on past states (i.e., it is memoryless).

For price movement, MMCP analyzes the past N bars (set by the lookback window) to determine the transition probabilities of price moving up, down, or remaining the same based on past behavior:

Pup=Number of Up MovesTotal Moves

Pup=Total MovesNumber of Up Moves

Pdown=Number of Down MovesTotal Moves

Pdown=Total MovesNumber of Down Moves

Psame=1−(Pup+Pdown)

Psame=1−(Pup+Pdown)

These probabilities guide how future price movements are simulated, ensuring that projections reflect historical price behavior tendencies.

Monte Carlo Simulations: Generating Possible Futures

Monte Carlo simulations involve running many random trials to estimate possible outcomes. Each trial simulates a future price path by:

Randomly selecting a direction based on the Markov probabilities Pup,Pdown,PsamePup,Pdown,Psame.

Determining the magnitude of the price movement using a normally distributed volatility model.

Iterating this process across multiple forecast bars to simulate a range of potential price paths.

This process does not predict a single outcome, but rather generates a probability-weighted range of future price possibilities.

Volatility Modeling: Scaling Movements Proportionally

Why We Use Standard Deviation (σσ)

Price movement is inherently volatile, and the magnitude of price shifts must be scaled relative to recent volatility. MMCP calculates rolling price returns and then derives the standard deviation of those returns:

σ=stdev(price returns,lookback)

σ=stdev(price returns,lookback)

The Volatility Multiplier allows users to adjust the impact of this volatility on projected movements. This makes the indicator adaptive to different asset price ranges.

Key User Adjustments

1. Volatility Multiplier – Tuning Projections for Different Assets

The scale of the Volatility Multiplier must be tuned for each asset because it is relative to the magnitude of price action. For example:

Low-priced assets (e.g., $2.50 stocks) → A multiplier of 0.1 works best.

Mid-priced assets (e.g., $250 stocks) → A multiplier of 3 works best.

High-priced assets (e.g., Bitcoin) → A multiplier of 1000 works best.

🔹 If projections seem too extreme, decrease the multiplier.

🔹 If projections seem too flat, increase the multiplier.

The Volatility Multiplier can also be fine-tuned to make the projected signal proportionate to the immediately preceding price action.

2. Expected Value (EV) Path – Analyzing Aggregate Future Probabilities

The EV Line is a computed average of all simulated paths, giving traders an expected mean trajectory.

If you find that the EV Line is not visible, try increasing the volatility multiplier to make it more pronounced.

3. Projection Inversion – Enhancing Analysis with Paired Indicators

A unique feature of MMCP is the projection inversion toggle, designed to allow traders to run multiple instances of the indicator in tandem.

When one instance is set to normal projection and another to inverted projection, traders can pair them together using identical settings (except inversion). This setup allows for a mirrored probability perspective and enhances visualizing volatility dynamics.

Additionally, traders can use multiple sets of paired indicators, each with a different lookback window, to build a multi-layered, probability-driven market visualization. This dynamic approach provides an evolving structure of probable price movement in different time frames, offering deeper insights into potential market conditions.

How MMCP Works in Real-Time

Each new bar triggers a fresh Monte Carlo simulation, meaning that projections organically evolve with the market. This ensures that MMCP is always responding to current conditions, rather than applying static assumptions.

How to Use MMCP in Trading

✔ Identifying Potential Reversal & Continuation Zones

If most Monte Carlo paths project upward, bullish momentum is likely.

If most Monte Carlo paths project downward, bearish momentum is likely.

The Expected Value (EV) Line can help confirm the most probable trajectory.

✔ Analyzing Market Sentiment in Real Time

Use multiple instances of MMCP with different lookback windows to capture short-term vs. long-term sentiment.

Enable projection inversion to analyze potential mirrored moves.

✔ Fine-Tuning MMCP for Your Strategy

Adjust the Volatility Multiplier to match the price scale of your asset.

Increase the number of simulations to improve statistical robustness.

Use shorter lookback windows for more responsive predictions, or longer windows for more stable forecasts.

Why MMCP is a Game-Changer

✅ Dynamic & Probabilistic – Unlike fixed indicators, MMCP adapts in real-time.

✅ Fully Stochastic – MMCP embraces uncertainty using Markov models & Monte Carlo simulations.

✅ Customizable for Any Asset – Adjust the Volatility Multiplier for small or large price movements.

✅ Live Updates – The projection organically evolves with every new price bar.

✅ Multi-Perspective Analysis – Traders can run paired normal and inverted projections for deeper insights.

By tuning Volatility Multiplier, Lookback Window, and Projection Inversion, traders can customize MMCP to fit their strategy.

Final Thoughts

The Markov Monte Carlo Projection (MMCP) is not about making absolute predictions—it is about understanding probability distributions in price action.

By leveraging Monte Carlo simulations, Markov transition probabilities, and dynamic volatility modeling, MMCP gives traders a powerful probability-based edge in forecasting potential price movement.

Cognitive Echo IndexCognitive Echo Index – User Guide

Overview

The Cognitive Echo Index is a composite indicator that combines several technical aspects—including price deviation from a moving average, normalized volatility (via ATR), and volume variations—to create a single numeric value. The output is scaled between -100 and +100, offering insights into market momentum and potential trend reversals.

How It Works

Price Component:

The indicator calculates the percentage change between the current price and its 14-period simple moving average (SMA). This helps identify how far the price deviates from its recent trend.

Volatility Component:

Using the Average True Range (ATR) over a 14-period, the script normalizes current ATR against its 14-period SMA. This shows relative volatility, highlighting unusual market activity.

Volume Component:

It computes the percentage change between the current volume and its 14-period SMA to detect spikes or drops in trading activity.

Composite Calculation:

The three components are summed together to produce the final index value, which is then clipped to remain between -100 and +100.

Interpreting the Indicator

Indicator Value Scale:

Positive Values (0 to +100):

Suggest that bullish forces are stronger. Higher values (e.g., above +50) could indicate a strong bullish sentiment.

Negative Values (0 to -100):

Indicate bearish pressures. Lower values (e.g., below -50) may signal strong bearish conditions.

Zero Level:

The midline indicates a balanced market condition with no dominant trend.

Key Horizontal Levels:

+50 Level:

When the indicator crosses above +50, it can be interpreted as a strong bullish signal.

-50 Level:

When the indicator crosses below -50, it can be considered a strong bearish signal.

Usage Tips

Confirmation Tool:

Use the Cognitive Echo Index as an additional confirmation tool in conjunction with other technical indicators or chart patterns to make more informed trading decisions.

Parameter Adjustments:

The script uses a 14-period setting for the moving average, ATR, and volume SMA by default. Depending on your trading timeframe or asset, consider tweaking these periods for better sensitivity.

Trend Analysis:

Watch how the indicator behaves during major price moves. A divergence between the index and the price trend (e.g., price rises while the index falls) may suggest a potential reversal or a false breakout.

Risk Management:

Always incorporate sound risk management practices. Use stop losses and position sizing rules, and consider the indicator as one part of your overall trading strategy.

Customization

Adjusting the Weights:

Although the current version gives equal weight to all three components, advanced users can modify the script to apply different weights to the price, volatility, and volume components based on historical performance or specific market conditions.

Adding Additional Inputs:

Future versions could incorporate external sentiment data or other technical factors if accessible. For now, the indicator focuses on technical inputs available directly within TradingView.

By following this guide, traders can integrate the Cognitive Echo Index into their TradingView platform to gain a unique perspective on market momentum and potential turning points. Enjoy testing and refining the indicator to better suit your trading style!

Gap Detection Indicator V.1This indicator is designed to detect gaps between candles on the chart. It detects all gaps that are higher than the specified percentage setting, draws a line passing through only the starting and ending points of the last gap, and paints between these lines.

If any candle closes above the gap starting level, the lines between the lines are colored green; If any candle closes below the gap starting level, the lines between the lines are colored red.

UPDATE1:

In addition, two more gap levels were added. A date range was added to enable control within the specified date range.

Fib Speed Resistance Fan"Fib Speed Resistance Fan," automatically draws Fibonacci Speed Resistance Fan lines based on the first and third candles of the trading session. Here’s a breakdown of its functionality:

Functionality

Session Start Time Identification

The script identifies the first candle at 9:15 AM using timestamp(), which ensures it captures the market's opening candle.

Candle Indexing

It determines the index of the first candle (firstCandleIndex) using ta.barssince(time >= sessionStart).

The third candle is found by adding two bars to the first candle's index (thirdCandleIndex = firstCandleIndex + 2).

Ensuring Single Execution

A boolean flag hasDrawn ensures that the lines are drawn only once and do not update on future candles.

Validating Data

It checks if the firstCandleIndex and thirdCandleIndex are valid (validSession).

If conditions are met, it extracts the highs and lows of the first and third candles.

Fibonacci Calculation

The script calculates a 0.75 level price between the first candle high/low and third candle low/high.

This level helps in drawing intermediate Fibonacci fan lines.

Drawing the Fibonacci Speed Resistance Fan

If conditions are valid and hasDrawn is false, the script draws:

Main fan lines from:

First candle high → Third candle low (Blue line)

First candle low → Third candle high (Blue line)

Shifted Buy PressureDifferentiated Buy Pressure Indicator Documentation

Overview: The Differentiated Buy Pressure indicator is a custom Pine Script™ indicator designed to measure and visualize buy and sell pressure in the market. It calculates buy pressure based on a combination of volume, range, and gap, and provides a differentiated buy pressure which is shifted by 90°, offering predictive insights.

Inputs:

Window Size: The window size for average calculation (default: 20).

Show Overlay: Option to show the price overlay (default: false).

Overlay Boost Factor: Boosting factor for overlaying the price (default: 0.01).

Calculations:

Relative Range: Calculated as (high - low) / close.

Average Range: Simple moving average of the relative range over the specified window.

Average Volume: Simple moving average of the volume over the specified window.

Relative Gap: Calculated as open / close .

Average Gap: Simple moving average of the relative gap over the specified window.

Buy Pressure: Calculated using the formula: buy_pressure = -math.log(relative_range / avg_range * volume / avg_volume * relative_gap / avg_gap)

Differentiated Buy Pressure: Calculated as the difference between the current and previous buy pressure: diff_buy_pressure = buy_pressure - buy_pressure

Plots:

Zero Line: A horizontal line at zero for reference.

Buy Pressure: Plotted in blue, representing the calculated buy pressure.

Differentiated Buy Pressure: Plotted in red, representing the differentiated buy pressure.

Overlay: Optionally plots the price overlay boosted by the differentiated buy pressure.

Labels:

Labels are created to display the buy pressure and differentiated buy pressure values on the chart.

Usage: This indicator helps traders visualize the buy and sell pressure in the market. Positive values indicate buy pressure, while negative values indicate sell pressure. The differentiated buy pressure, shifted by 90°, provides predictive insights into future market movements.

This documentation provides a comprehensive overview of the Differentiated Buy Pressure indicator, explaining its purpose, inputs, calculations, and usage.

London Breakout by Edwin KPurpose:

The strategy visualizes breakouts based on price action during the London session. It highlights the candles from 09:59 AM to 01:59 PM UTC+3 with different colors depending on whether the price is above or below the high/low from the 10 AM candle.

Key Parts:

Timestamps:

The code defines specific times for the 09:59 AM candle, 10:00 AM candle, and 01:59 PM UTC+3 times.

The timestamp('UTC+3', ...) function creates the timestamps for those moments.

High and Low of the 10 AM Candle:

The high and low of the 10 AM candle are captured and stored in the ten_am_high and ten_am_low variables.

Bullish and Bearish Conditions:

If the price breaks above (bullish_break) or below (bearish_break) the high or low of the 10 AM candle, respectively.

Bar Coloring:

If the conditions are met (price breaking above or below the 10 AM levels), the script colors the candles during the time frame (09:59 AM to 01:59 PM).

Green color is applied for bullish breakouts.

Red color is applied for bearish breakouts.

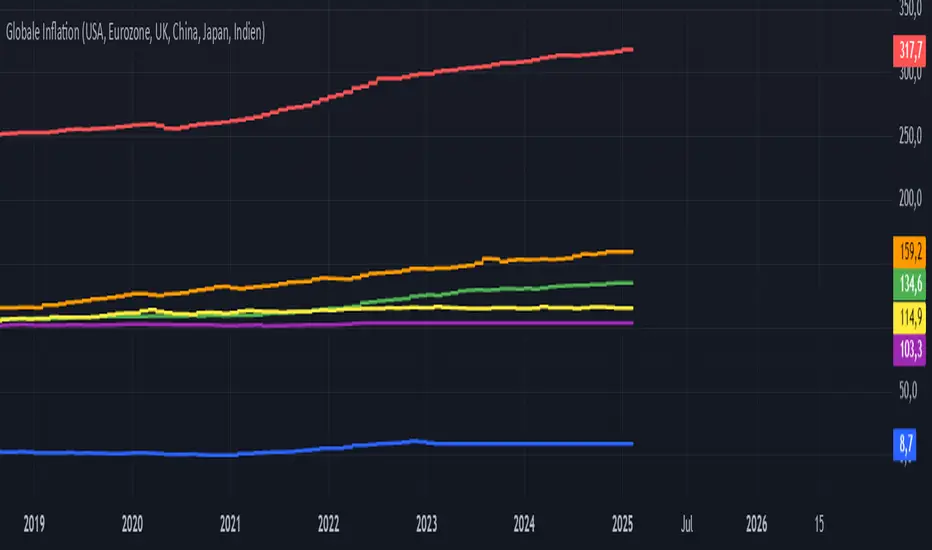

Global Inflation Indicator🔹 Overview:

The Global Inflation Indicator is a macro-analysis tool designed to track and compare inflation trends across major economies. It pulls Consumer Price Index (CPI) data from multiple regions, helping traders and investors analyze how inflation impacts global markets, particularly gold, forex, and commodities.

📊 Key Features:

✅ Tracks inflation in six major economies:

🇺🇸 USA (CPIAUCSL) – Key driver for USD and gold prices

🇪🇺 Eurozone (CPHPTT01EZM659N) – Euro inflation impact

🇬🇧 United Kingdom (GBRCPIALLMINMEI) – GBP & economic trends

🇨🇳 China (CHNCPIALLMINMEI) – Emerging market impact

🇯🇵 Japan (JPNCPIALLMINMEI) – Yen & inflation control policies

🇮🇳 India (INDCPIALLMINMEI) – Key gold-consuming economy

✅ Real-time Inflation Trends:

Provides a visual comparison of inflation levels in different regions.

Helps traders identify inflationary cycles & their effect on global assets.

✅ Macro-Driven Trading Decisions:

Gold & Forex Correlation: High inflation may increase demand for gold.

Interest Rate Expectations: Central banks respond to inflation shifts.

Currency Strength: Inflation impacts USD, EUR, GBP, JPY, CNY, INR.

📉 How to Use It:

Gold traders can assess inflation trends to predict potential price movements.

Forex traders can compare inflation effects on major currency pairs (EUR/USD, USD/JPY, GBP/USD, etc.).

Stock investors can evaluate how inflation affects central bank policies and interest rates.

📌 Conclusion:

The Global Inflation Indicator is a powerful tool for macroeconomic analysis, providing real-time insights into global inflation trends. By integrating this indicator into your gold, forex, and commodity trading strategies, you can make more informed investment decisions in response to economic changes.

Opening ScoreOverview:

The Composite Open Strategy Indicator is designed to provide traders with a unified, early-session directional bias by aggregating multiple non-correlated signals. By combining diverse analytical methods—spanning price action, volume, volatility, and time—the indicator helps you gauge whether the market is leaning bullish or bearish during the critical opening hours.

How It Works:

• Open Range Breakout (ORB) Signal:

The indicator captures the opening range (defined up to a user-specified time, e.g., 9:45 AM ET) and assigns a bullish signal when the price breaks above the high of that range, and a bearish signal when it drops below the low.

• VWAP Signal:

It compares the current price to the Volume Weighted Average Price (VWAP). A price above VWAP suggests buying pressure, while below indicates selling pressure.

• Trend Signal:

Using a simple moving average (with an adjustable period, typically around 20 bars), the indicator determines the prevailing trend. Price above the MA contributes a bullish bias, and price below contributes a bearish bias.

• Volatility Signal:

A volatility filter is applied via the Average True Range (ATR). An increasing ATR relative to the previous bar suggests rising volatility (bullish if combined with upward moves), whereas a decreasing ATR indicates the opposite.

Each of these four signals is assigned an equal weight (modifiable as needed), and their sum forms the composite score.

Display and Timing:

• Separate Panel:

The composite score is plotted as a histogram in its own indicator panel, ensuring your main price chart remains uncluttered.

• Session Filter:

The indicator is active only during the early session—from 9:30 AM to 12:30 PM Eastern Time—when the initial directional move is most relevant. Outside this time window, the indicator remains inactive.

Trading Insights:

• A positive composite score suggests a bullish bias, indicating that the aggregated signals lean toward an upward trend.

• A negative composite score points to a bearish bias, indicating a downward directional outlook.

Usage:

Ideal for traders looking to capture the market’s early trend direction, this indicator can be used as part of a broader strategy. Its design encourages consistency by combining multiple perspectives (price, volume, volatility, time) into one clear signal, allowing you to focus on setups that align with the dominant early-session move.

Before fully automating your trading approach, you can test and refine this composite method on TradingView using the built-in manual review process. Once confident in its performance, further automation can help integrate this directional bias seamlessly into your overall trading strategy.

Averaged Stochastic RSI by TenozenSimplicity beats everything! Averaged Stochastic RSi is calculated using the 2 points of stochastic of the RSI, where the difference is by 2 (larger), and averaged out the stochastic's values. In result it is less noisy and more responsive towards the market's momentum.

I hope you guys find this indicator useful! So far this is the best indicator I ever had! And I also learned that simplicity is better than complex blurry/abstract problems. Ciao!

Bracket IndicatorThis is an indicator that shows tick target above and below the chart. Allows for visualizing continual bracket target moving with price before getting into trade.

So, for example, if you are watching price and wanting to target 10 points above or below. You can set this bracket indicator on the chart and you will be able to in real time see 10 points above/below the current price.

Share SizeA helpful tool that estimates the amount of times you can trade at your current share size in a small account.

You can adjust the numbers in the settings page!

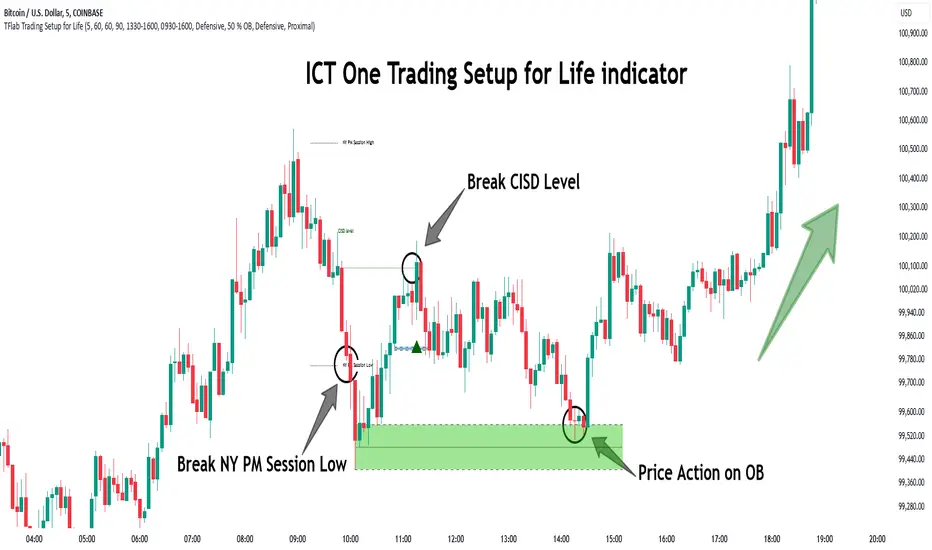

One Trading Setup for Life ICT [TradingFinder] Sweep Session FVG🔵 Introduction

ICT One Trading Setup for Life is a trading strategy based on liquidity and market structure shifts, utilizing the PM Session Sweep to determine price direction. In this strategy, the market first forms a price range during the PM Session (from 13:30 to 16:00 EST), which includes the highest high (PM Session High) and lowest low (PM Session Low).

In the next session, the price first touches one of these levels to trigger a Liquidity Hunt before confirming its trend by breaking the Change in State of Delivery (CISD) Level. After this confirmation, the price retraces toward a Fair Value Gap (FVG) or Order Block (OB), which serve as the best entry points in alignment with liquidity.

In financial markets, liquidity is the primary driver of price movement, and major market participants such as institutional investors and banks are constantly seeking liquidity at key levels. This process, known as Liquidity Hunt or Liquidity Sweep, occurs when the price reaches an area with a high concentration of orders, absorbs liquidity, and then reverses direction.

In this setup, the PM Session range acts as a trading framework, where its highs and lows function as key liquidity zones that influence the next session’s price movement. After the New York market opens at 9:30 EST, the price initially breaks one of these levels to capture liquidity.

However, for a trend shift to be confirmed, the CISD Level must be broken.

Once the CISD Level is breached, the price retraces toward an FVG or OB, which serve as optimal trade entry points.

Bullish Setup :

Bearish Setup :

🔵 How to Use

In this strategy, the PM Session range is first identified, which includes the highest high (PM Session High) and lowest low (PM Session Low) between 13:30 and 16:00 EST. In the following session, the price touches one of these levels for a Liquidity Hunt, followed by a break of the Change in State of Delivery (CISD) Level. The price then retraces toward a Fair Value Gap (FVG) or Order Block (OB), creating a trading opportunity.

This process can occur in two scenarios : bearish and bullish setups.

🟣 Bullish Setup

In a bullish scenario, the PM Session High and PM Session Low are identified. In the following session, the price first breaks the PM Session Low, absorbing liquidity. This process results in a Fake Breakout to the downside, misleading retail traders into taking short positions.

After the Liquidity Hunt, the CISD Level is broken, confirming a trend reversal. The price then retraces toward an FVG or OB, offering an optimal long entry opportunity.

The initial take-profit target is the PM Session High, but if higher timeframe liquidity levels exist, extended targets can be set.

The stop-loss should be placed below the Fake Breakout low or the first candle of the FVG.

🟣 Bearish Setup

In a bearish scenario, the market first defines its PM Session High and PM Session Low. In the next session, the price initially breaks the PM Session High, triggering a Liquidity Hunt. This movement often causes a Fake Breakout, misleading retail traders into taking incorrect positions.

After absorbing liquidity, the CISD Level breaks, indicating a shift in market structure. The price then retraces toward an FVG or OB, offering the best short entry opportunity.

The initial take-profit target is the PM Session Low, but if additional liquidity exists on higher timeframes, lower targets can be considered.

The stop-loss should be placed above the Fake Breakout high or the first candle of the FVG.

🔵 Setting

CISD Bar Back Check : The Bar Back Check option enables traders to specify the number of past candles checked for identifying the CISD Level, enhancing CISD Level accuracy on the chart.

Order Block Validity : The number of candles that determine the validity of an Order Block.

FVG Validity : The duration for which a Fair Value Gap remains valid.

CISD Level Validity : The duration for which a CISD Level remains valid after being broken.

New York PM Session : Defines the PM Session range from 13:30 to 16:00 EST.

New York AM Session : Defines the AM Session range from 9:30 to 16:00 EST.

Refine Order Block : Enables finer adjustments to Order Block levels for more accurate price responses.

Mitigation Level OB : Allows users to set specific reaction points within an Order Block, including: Proximal: Closest level to the current price. 50% OB: Midpoint of the Order Block. Distal: Farthest level from the current price.

FVG Filter : The Judas Swing indicator includes a filter for Fair Value Gap (FVG), allowing different filtering based on FVG width: FVG Filter Type: Can be set to "Very Aggressive," "Aggressive," "Defensive," or "Very Defensive." Higher defensiveness narrows the FVG width, focusing on narrower gaps.

Mitigation Level FVG : Like the Order Block, you can set price reaction levels for FVG with options such as Proximal, 50% OB, and Distal.

Demand Order Block : Enables or disables bullish Order Block.

Supply Order Block : Enables or disables bearish Order Blocks.

Demand FVG : Enables or disables bullish FVG.

Supply FVG : Enables or disables bearish FVGs.

Show All CISD : Enables or disables the display of all CISD Levels.

Show High CISD : Enables or disables high CISD levels.

Show Low CISD : Enables or disables low CISD levels.

🔵 Conclusion

The ICT One Trading Setup for Life is a liquidity-based strategy that leverages market structure shifts and precise entry points to identify high-probability trade opportunities. By focusing on PM Session High and PM Session Low, this setup first captures liquidity at these levels and then confirms trend shifts with a break of the Change in State of Delivery (CISD) Level.

Entering a trade after a retracement to an FVG or OB allows traders to position themselves at optimal liquidity levels, ensuring high reward-to-risk trades. When used in conjunction with higher timeframe bias, order flow, and liquidity analysis, this strategy can become one of the most effective trading methods within the ICT Concept framework.

Successful execution of this setup requires risk management, patience, and a deep understanding of liquidity dynamics. Traders can enhance their confidence in this strategy by conducting extensive backtesting and analyzing past market data to optimize their approach for different assets.

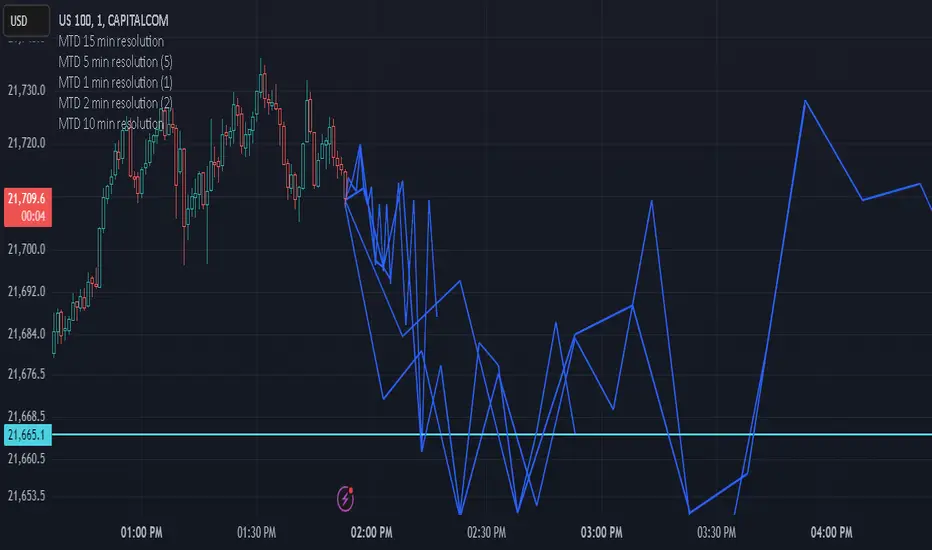

Multi-timeframe Difference Forecast (MTD)Description:

The Multi-timeframe Difference Forecast indicator projects potential future price levels by comparing open prices across multiple timeframe pairs. It uses 12 predefined timeframe pairs where each pair consists of a lower and a higher timeframe. For each pair, the indicator calculates a forecast value by adding the difference between the lower timeframe’s open and the higher timeframe’s open to the current bar’s close. These forecast values are then plotted as points into the future and connected by blue line segments, forming a continuous projection line on your chart.

How It Works:

Timeframe Pairs:

The indicator defines 12 pairs. For example:

Pair 1: Lower timeframe = 15 minutes; Higher timeframe = 150 minutes

Pair 2: Lower timeframe = 30 minutes; Higher timeframe = 165 minutes

⋮

Pair 12: Lower timeframe = 180 minutes; Higher timeframe = 720 minutes

Forecast Calculation:

For each pair, the forecast is computed as:

forecast = close + (lower timeframe open - higher timeframe open)

This produces a series of forecast values that are then plotted on the chart.

Time Offset:

Each forecast point is offset into the future by a number of bars calculated as the ratio between the lower timeframe’s duration (in seconds) and the current chart’s timeframe (in seconds). This adjustment helps align the forecast points correctly on the time axis.

Visualization:

The indicator draws blue lines (width = 2) connecting the current price to each forecast point sequentially, forming a polyline that visually represents the projected price trajectory.

How to Use:

Overlay on Chart:

Apply this indicator to any chart, and it will automatically overlay the forecast line on your current price chart.

Timeframe Flexibility:

The calculations adjust to the chart’s timeframe, so you can use it on various timeframes without needing to change the code.

Interpretation:

The forecast line is intended to provide a visual estimate of potential future price movement based on historical open price differences. It is meant to serve as an additional analytical tool rather than a standalone trading signal.

Disclaimer:

This script is provided for educational and informational purposes only and should not be construed as financial or trading advice. Trading involves significant risk, and past performance is not indicative of future results. You should perform your own analysis and consult with a qualified professional before making any trading decisions. Use this indicator at your own risk.

Ultimate T3 Fibonacci for BTC Scalping. Look at backtest report!Hey Everyone!

I created another script to add to my growing library of strategies and indicators that I use for automated crypto trading! This strategy is for BITCOIN on the 30 minute chart since I designed it to be a scalping strategy. I calculated for trading fees, and use a small amount of capital in the backtest report. But feel free to modify the capital and how much per order to see how it changes the results:)

It is called the "Ultimate T3 Fibonacci Indicator by NHBprod" that computes and displays two T3-based moving averages derived from price data. The t3_function calculates the Tilson T3 indicator by applying a series of exponential moving averages to a combined price metric and then blending these results with specific coefficients derived from an input factor.

The script accepts several user inputs that toggle the use of the T3 filter, select the buy signal method, and set parameters like lengths and volume factors for two variations of the T3 calculation. Two T3 lines, T3 and T32, are computed with different parameters, and their colors change dynamically (green/red for T3 and blue/purple for T32) based on whether the lines are trending upward or downward. Depending on the selected signal method, the script generates buy signals either when T32 crosses over T3 or when the closing price is above T3, and similarly, sell signals are generated on the respective conditions for crossing under or closing below. Finally, the indicator plots the T3 lines on the chart, adds visual buy/sell markers, and sets alert conditions to notify users when the respective trading signals occur.

The user has the ability to tune the parameters using TP/SL, date timerames for analyses, and the actual parameters of the T3 function including the buy/sell signal! Lastly, the user has the option of trading this long, short, or both!

Let me know your thoughts and check out the backtest report!

Combined SmartComment & Dynamic S/R LevelsDescription:

The Combined SmartComment & Dynamic S/R Levels script is designed to provide valuable insights for traders using TradingView. It integrates dynamic support and resistance levels with a powerful Intelligent Comment system to enhance decision-making. The Intelligent Comment feature generates market commentary based on key technical indicators, delivering real-time actionable feedback that helps optimize trading strategies.

Intelligent Comment Feature:

The Intelligent Comment function continuously analyzes market conditions and offers relevant insights based on combinations of various technical indicators such as RSI, ATR, MACD, WMA, and others. These comments help traders identify potential price movements, highlighting opportunities to buy, sell, or wait.

Examples of the insights provided by the system include:

RSI in overbought/oversold and price near resistance/support: Indicates potential price reversal points.

Price above VAH and volume increasing: Suggests a strengthening uptrend.

Price near dynamic support/resistance: Alerts when price approaches critical support or resistance zones.

MACD crossovers and RSI movements: Provide signals for potential trend shifts or continuations.

Indicators Used:

RSI (Relative Strength Index)

ATR (Average True Range)

MACD (Moving Average Convergence Divergence)

WMA (Weighted Moving Average)

POC (Point of Control)

Bollinger Bands

SuperSignal

Volume

EMA (Exponential Moving Average)

Dynamic Support/Resistance Levels

How It Works:

The script performs real-time market analysis, assessing multiple technical indicators to generate Intelligent Comments. These comments provide traders with timely guidance on potential market movements, assisting with decision-making in a dynamic market environment. The script also integrates dynamic support and resistance levels to further enhance trading accuracy.

GOLD Volume-Based Entry StrategyShort Description:

This script identifies potential long entries by detecting two consecutive bars with above-average volume and bullish price action. When these conditions are met, a trade is entered, and an optional profit target is set based on user input. This strategy can help highlight momentum-driven breakouts or trend continuations triggered by a surge in buying volume.

How It Works

Volume Moving Average

A simple moving average of volume (vol_ma) is calculated over a user-defined period (default: 20 bars). This helps us distinguish when volume is above or below recent averages.

Consecutive Green Volume Bars

First bar: Must be bullish (close > open) and have volume above the volume MA.

Second bar: Must also be bullish, with volume above the volume MA and higher than the first bar’s volume.

When these two bars appear in sequence, we interpret it as strong buying pressure that could drive price higher.

Entry & Profit Target

Upon detecting these two consecutive bullish bars, the script places a long entry.

A profit target is set at current price plus a user-defined fixed amount (default: 5 USD).

You can adjust this target, or you can add a stop-loss in the script to manage risk further.

Visual Cues

Buy Signal Marker appears on the chart when the second bar confirms the signal.

Green Volume Columns highlight the bars that fulfill the criteria, providing a quick visual confirmation of high-volume bullish bars.

Works fine on 1M-2M-5M-15M-30M. Do not use it on higher TF. Due the lack of historical data on lower TF, the backtest result is limited.

Dynamic 200 EMA with Trend-Based ColoringDescription:

This script plots the 200-period Exponential Moving Average (EMA) and dynamically changes its color based on the trend direction. The script helps traders quickly identify whether the price is above or below the 200 EMA, which is widely used as a long-term trend indicator.

How It Works:

The script calculates the 200 EMA based on the closing price.

If the price is above the EMA, it suggests a bullish trend, and the EMA line turns green.

If the price is below the EMA, it suggests a bearish trend, and the EMA line turns red.

An optional background color is added to enhance visual clarity, highlighting the current trend direction.

Use Cases:

Trend Confirmation: Helps traders determine if the overall trend is bullish or bearish.

Support and Resistance: The 200 EMA is often used as dynamic support/resistance.

Entry & Exit Signals: Traders can use crossovers with the 200 EMA as potential trade signals.

This script is designed for traders looking for a simple yet effective way to incorporate trend visualization into their charts. It is fully open-source and can be customized to fit individual trading strategies.

RSI XTR with selective candle color by Edwin KThis tradingView indicator named "RSI XTR with selective candle color", which modifies the candle colors on the chart based on RSI (Relative Strength Index) conditions. Here's how it works:

- rsiPeriod: Defines the RSI calculation period (default = 5).

- rsiOverbought: RSI level considered overbought (default = 70).

- rsiOversold: RSI level considered oversold (default = 30).

- These values can be modified by the user in the settings.

RSI Calculation

- Computes the RSI value using the ta.rsi() function on the closing price (close).

- The RSI is a momentum indicator that measures the magnitude of recent price changes.

Conditions for Candle Coloring

- when the RSI is above the overbought level.

- when the RSI is below the oversold level.

How It Works in Practice

- When the RSI is above 70 (overbought) → Candles turn red.

- When the RSI is below 30 (oversold) → Candles turn green.

- If the RSI is between 30 and 70, the candle keeps its default color.

This helps traders quickly spot potential reversal zones based on RSI momentum.

EMA & Bollinger BandsThis indicator combines three main functionalities into a single script:

1. Exponential Moving Average (EMA):

- Purpose: Calculates and plots the EMA of a chosen price source.

- Inputs:

- EMA Length: The period for the EMA calculation.

- EMA Source: The price series (such as close) used for the EMA.

- EMA Offset: Allows shifting the EMA line left or right on the chart.

- Output: A blue-colored EMA line plotted on the chart.

2. Smoothing MA on EMA:

- Purpose: Applies a secondary moving average (MA) on the previously calculated EMA. There is also an option to overlay Bollinger Bands on this smoothed MA.

- Inputs:

- Smoothing MA Type: Options include "None", "SMA", "SMA + Bollinger Bands", "EMA", "SMMA (RMA)", "WMA", and "VWMA".

- Selecting "None" disables this feature.

- Choosing "SMA + Bollinger Bands" will additionally plot Bollinger Bands around the smoothed MA.

- Smoothing MA Length: The period used to calculate the smoothing MA.

- BB StdDev for Smoothing MA: The standard deviation multiplier for the Bollinger Bands (applies only when "SMA + Bollinger Bands" is selected).

- Calculation Details:

- The chosen MA type is applied to the EMA value.

- If Bollinger Bands are enabled, the script computes the standard deviation of the EMA over the smoothing period, multiplies it by the specified multiplier, and then plots an upper and lower band around the smoothing MA.

- Output:

- A yellow-colored smoothing MA line.

- Optionally, green-colored upper and lower Bollinger Bands with a filled background if the "SMA + Bollinger Bands" option is selected.

3. Bollinger Bands on Price:

- Purpose: Independently calculates and plots traditional Bollinger Bands based on a moving average of a selected price source.

- Inputs:

- BB Length: The period for calculating the moving average that serves as the basis of the Bollinger Bands.

- BB Basis MA Type: The type of moving average to use (options include SMA, EMA, SMMA (RMA), WMA, and VWMA).

- BB Source: The price series (such as close) used for the Bollinger Bands calculation.

- BB StdDev: The multiplier for the standard deviation used to calculate the upper and lower bands.

- BB Offset: Allows shifting the Bollinger Bands left or right on the chart.

- Calculation Details:

- The script computes a basis line using the selected MA type on the chosen price source.

- The standard deviation of the price over the specified period is then multiplied by the provided multiplier to determine the distance for the upper and lower bands.

- Output:

- A basis line (typically drawn in a blue tone), an upper band (red), and a lower band (teal).

- The area between the upper and lower bands is filled with a semi-transparent blue background for easier visualization.

---

How It Works Together

- Integration:

The script is divided into clearly labeled sections for each functionality. All parts are drawn on the same chart (overlay mode enabled), providing a comprehensive view of market trends.

- Customization:

Users can adjust parameters for the EMA, the smoothing MA (and its optional Bollinger Bands), as well as the traditional Bollinger Bands independently. This allows for flexible customization depending on the trader's strategy or visual preference.

- Utility:

Combining these three analyses into one indicator enables traders to view:

- The immediate trend via the EMA.

- A secondary smoothed trend that might help reduce noise.

- A volatility measure through Bollinger Bands on both the price and the smoothed EMA.

---

This combined indicator is useful for technical analysis by providing both trend-following (EMA and smoothing MA) and volatility indicators (Bollinger Bands) in one streamlined tool.