Consecutive Candle Detector Consecutive Candle Detector , can be used to highlight impulsive moves . 3 or more candles with the same colour in the same direction .

Set an alert notification to let you know price has moved in an impulsive way and is forming a pattern to sell or buy

Forecasting

[Becak] - Swing Point Retracement & Prediction" - Swing Point Retracement & Prediction," is designed to identify swing points in price action, calculate retracement levels, and predict potential future price levels. It's a technical analysis tool that can help traders identify potential support and resistance levels, as well as possible reversal points.

HOW IT WORK

Swing Point Detection:

The indicator uses the ta.pivothigh() and ta.pivotlow() functions to identify swing highs and lows within a specified lookback period.

Retracement Levels:

When a new swing point is detected, the indicator calculates a retracement level based on the user-defined retracement percentage. It draws a dashed blue line at the retracement level, along with a yellow circle and a label showing the price.

Swing Point Labeling:

Swing highs are marked with a green "H" label and the price, and Swing lows are marked with a red "L" label and the price.

Price Prediction:

Based on the most recent swing point, the indicator attempts to predict the next potential high or low. It draws a purple dashed line extending into the future, indicating the predicted price level.

HOW TO USE THIS INDICATOR:

adjust the input parameters:

"Swing Point Lookback": Determines how far back the indicator looks to identify swing points. A larger value will result in fewer, more significant swing points.

"Retracement %": Sets the percentage for calculating retracement levels. 50% is a common Fibonacci retracement level, but you can adjust this based on your trading strategy.

"Prediction Length": Determines how far into the future the prediction line extends.

Interpret the results:

Use the swing point labels (H and L) to quickly identify recent highs and lows. The blue dashed lines and yellow circles indicate potential support or resistance levels based on the retracement percentage. The purple dashed line shows a potential future price target. This can be used to set profit targets or identify potential reversal zones.

Combine with other analysis:

This indicator works best when combined with other forms of analysis, such as trend lines, moving averages, or candlestick patterns.

Use the retracement levels and predictions as potential entry or exit points, but always confirm with other indicators or price action signals.

2024 - Seasonality - Open to CloseScript Description:

This Pine Script is designed to visualise **seasonality** in the financial markets by calculating the **open-to-close percentage change** for each month of a selected asset. It creates a **heatmap** table to display the monthly performance over multiple years. The script provides detailed statistical summaries, including:

- **Average monthly percentage changes**

- **Standard deviation** of the changes

- **Percentage of months with positive returns**

The script also allows users to adjust colour intensities for positive and negative values, specify which year to start from, and skip specific months. Key metrics such as averages, standard deviations, and percentages of positive months can be toggled on or off based on user preferences. The result is a clear, visual representation of how an asset typically performs month by month, aiding in seasonality analysis.

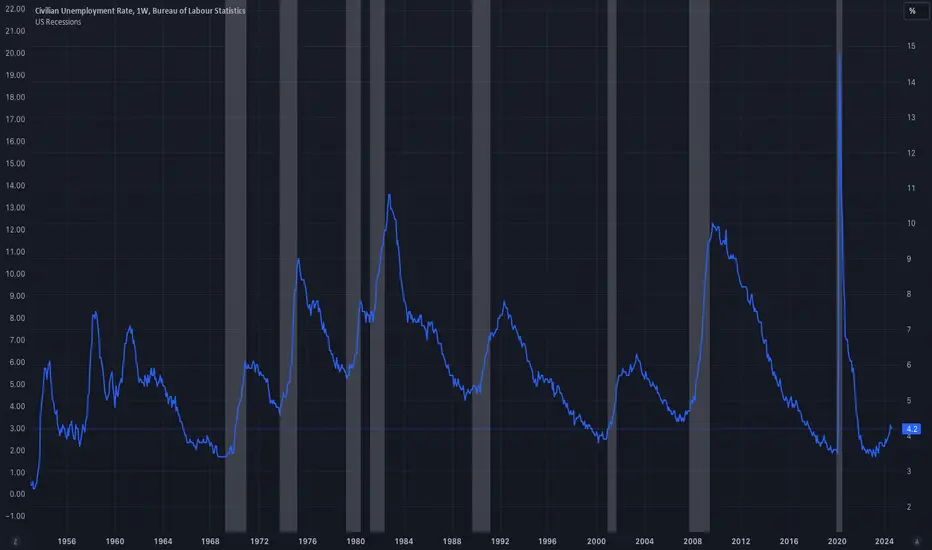

US Recessions based on James Hamilton's JHDUSRGDPBRThis simple script uses James Hamilton's JHDUSRGDPBR indicator to colour areas representing recession periods in the US. Best used in conjunction with other macroeconomics indicators, like –as in the example– unemployment rates

Forex - Lot size calculatorThis indicator is specifically designed for Forex traders who need a convenient lot size calculator directly on their charts. It allows users to input their account balance, risk percentage, and stop-loss distance in pips to easily determine the appropriate lot size for a given trade, ensuring effective risk management.

Key Features:

Lot Size Calculation: Automatically calculates the lot size based on user-defined inputs: account balance, risk percentage, and stop-loss distance.

Error Handling: The indicator only works with Forex pairs. If applied to non-Forex assets, a clear and prominent red error message will appear in the bottom-right corner of the chart, reminding the user that this script is intended exclusively for Forex trading.

Simple Visualization: The calculated lot size is displayed in an easy-to-read table directly on the chart.

How to Use:

Add the indicator to a Forex chart.

Enter your account balance, risk percentage, and stop-loss pips in the input fields.

The indicator will display the calculated lot size for the chosen Forex pair.

Important Notes:

This script is intended only for Forex assets. If used on other instruments (e.g., stocks, crypto, indices), an error message will be shown.

Always validate lot sizes with your broker, as there can be slight variations depending on broker specifications and leverage settings.

Magic Touch Line DetectorSummary of the Magic Touch Line Detector Script:

Purpose:

The Magic Touch Line Detector script is designed to identify significant price points in the market by analyzing candlestick wicks and bodies. It plots lines based on the detected wicks, classifying them as either ascending or descending. The script tracks how frequently price touches these lines and highlights the "most touched" lines for both ascending and descending categories. This script is particularly useful for traders looking to identify key price levels and trends over time.

How It Works:

Wick and Body Detection:

The script starts by analyzing the highs and lows of candlestick wicks relative to their bodies over a user-defined lookback period. A significant wick is identified based on a specified wick-to-body ratio and a deviation threshold measured against the Average True Range (ATR).

Line Creation:

Once a significant upper or lower wick is detected, the script calculates unconventional highs and lows (i.e., points that differ from the absolute highs and lows of the lookback period). Lines are then drawn from these unconventional price points using the slope between the detected wick and the current bar, ensuring a smooth extension.

Line Refinement and Touch Tracking:

As new bars are added, the script tracks how often the price touches the previously drawn lines. The number of touches each line receives is counted and updated in real-time, and the script ensures that only the most touched line is highlighted.

Highlighting and Labeling:

For each category (ascending and descending), the most touched line is identified and given special highlighting with thicker lines and different colors. Labels are also generated to show the number of touches that the most touched line has received. Old labels are cleared to avoid clutter.

Explanation of the Settings:

Lookback Period for Highs and Lows:

This sets the number of bars the script will use to detect the highest highs and lowest lows. A larger lookback period gives the script a broader context to work with, potentially identifying more significant price points.

Minimum Wick-to-Body Ratio:

This ratio determines what qualifies as a "significant" wick. It compares the length of the wick to the body of the candle. A higher ratio means that only wicks that are much longer than the candle body will be considered significant.

Price Deviation Threshold (in ATR multiples):

This setting controls how much price deviation from the ATR is required for a wick to be deemed significant. It acts as a filter to reduce noise by ignoring smaller wicks that are within normal price movements.

Line Touch Tolerance Factor (ATR multiple):

When checking if a price touches a line, the script uses this setting to define how close the price must be to the line to count as a "touch." This tolerance is a multiplier of the ATR, allowing for some flexibility in what is considered a touch.

Price Difference Threshold:

This defines the minimum price difference required to plot a line. If the price difference between the high and low of a detected wick is too small, the script can avoid plotting a line for insignificant moves.

Slope Adjustment Multiplier:

This multiplier adjusts the slope of the lines that are drawn from detected price points. It affects the length and angle of the lines, allowing users to control how far and at what angle the lines should extend across the chart.

Customization Options:

Show Ascending/Descending Lines:

These toggles allow users to decide whether ascending (bullish) or descending (bearish) lines should be shown on the chart.

Line Color, Style, and Width (for Ascending and Descending Lines):

These settings give users control over how the lines appear visually. You can customize the color, style (solid, dashed, dotted), and width of both ascending and descending lines.

Most Touched Line Color:

Users can define a different color for the "most touched" line, which is automatically identified by the script. This setting helps highlight the line that has been interacted with the most by the price.

How to Use the Script:

Setup the Lookback Period and Deviation Filters:

Start by setting the lookback period and the filters for wick-to-body ratio and deviation threshold. These settings help control the script's sensitivity to market movements.

Refine the Tolerance and Slope:

Adjust the line touch tolerance and slope adjustment multiplier to control how closely the script tracks price touches and how the lines are extended on the chart.

Customize Visuals:

Once the lines are being drawn, customize the colors, styles, and widths to ensure the lines are easy to read on your chart. You can also decide if you want to display both ascending and descending lines or focus on just one.

By setting up the script based on these inputs and parameters, you can get a real-time view of significant price levels and how often the price interacts with them, helping you make more informed trading decisions.

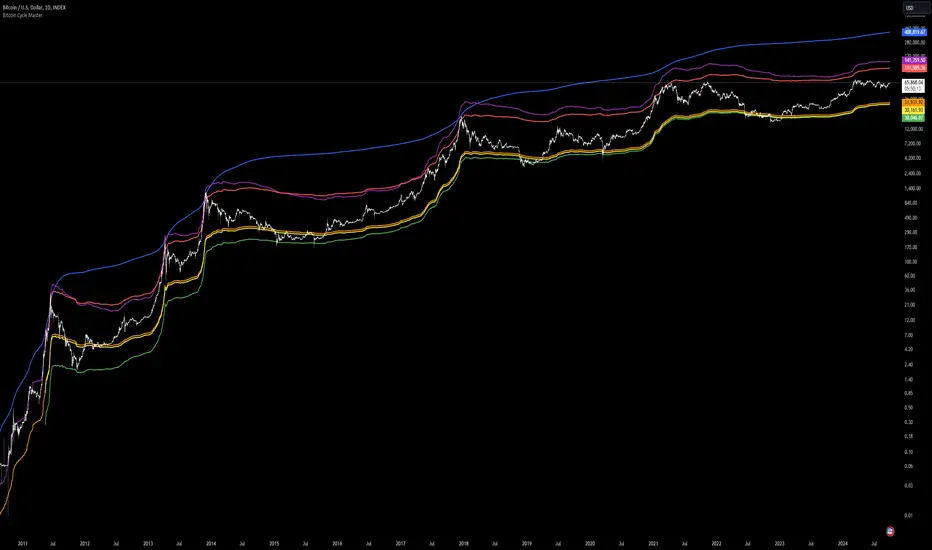

Bitcoin Cycle Master [InvestorUnknown]The "Bitcoin Cycle Master" indicator is designed for in-depth, long-term analysis of Bitcoin's price cycles, using several key metrics to track market behavior and forecast potential price tops and bottoms. The indicator integrates multiple moving averages and on-chain metrics, offering a comprehensive view of Bitcoin’s historical and projected performance. Each of its components plays a crucial role in identifying critical cycle points:

Top Cap: This is a multiple of the Average Cap, which is calculated as the cumulative sum of Bitcoin’s price (price has a longer history than Market Cap) divided by its age in days. Top Cap serves as an upper boundary for speculative price peaks, multiplied by a factor of 35.

Time_dif() =>

date = ta.valuewhen(bar_index == 0, time, 0)

sec_r = math.floor(date / 1000)

min_r = math.floor(sec_r / 60)

h_r = math.floor(min_r / 60)

d_r = math.floor(h_r / 24)

// Launch of BTC

start = timestamp(2009, 1, 3, 00, 00)

sec_rb = math.floor(start / 1000)

min_rb = math.floor(sec_rb / 60)

h_rb = math.floor(min_rb / 60)

d_rb = math.floor(h_rb / 24)

difference = d_r - d_rb

AverageCap() =>

ta.cum(btc_price) / (Time_dif() + btc_age)

TopCap() =>

// To calculate Top Cap, it is first necessary to calculate Average Cap, which is the cumulative sum of Market Cap divided by the age of the market in days.

// This creates a constant time-based moving average of market cap.

// Once Average cap is calculated, those values are multiplied by 35. The result is Top Cap.

// For AverageCap the BTC price was used instead of the MC because it has more history

// (the result should have minimal if any deviation since MC would have to be divided by Supply)

AverageCap() * 35

Delta Top: Defined as the difference between the Realized Cap and the Average Cap, this metric is further multiplied by a factor of 7. Delta Top provides a historically reliable signal for Bitcoin market cycle tops.

DeltaTop() =>

// Delta Cap = Realized Cap - Average Cap

// Average Cap is explained in the Top Cap section above.

// Once Delta Cap is calculated, its values over time are then multiplied by 7. The result is Delta Top.

(RealizedPrice() - AverageCap()) * 7

Terminal Price: Derived from Coin Days Destroyed, Terminal Price normalizes Bitcoin’s historical price behavior by its finite supply (21 million bitcoins), offering an adjusted price forecast as all bitcoins approach being mined. The original formula for Terminal Price didn’t produce expected results, hence the calculation was adjusted slightly.

CVDD() =>

// CVDD stands for Cumulative Value Coin Days Destroyed.

// Coin Days Destroyed is a term used for bitcoin to identify a value of sorts to UTXO’s (unspent transaction outputs). They can be thought of as coins moving between wallets.

(MCR - TV) / 21000000

TerminalPrice() =>

// Theory:

// Before Terminal price is calculated, it is first necessary to calculate Transferred Price.

// Transferred price takes the sum of > Coin Days Destroyed and divides it by the existing supply of bitcoin and the time it has been in circulation.

// The value of Transferred Price is then multiplied by 21. Remember that there can only ever be 21 million bitcoin mined.

// This creates a 'terminal' value as the supply is all mined, a kind of reverse supply adjustment.

// Instead of heavily weighting later behavior, it normalizes historical behavior to today. By normalizing by 21, a terminal value is created

// Unfortunately the theoretical calculation didn't produce results it should, in pinescript.

// Therefore the calculation was slightly adjusted/improvised

TransferredPrice = CVDD() / (Supply * math.log(btc_age))

tp = TransferredPrice * 210000000 * 3

Realized Price: Calculated as the Market Cap Realized divided by the current supply of Bitcoin, this metric shows the average value of Bitcoin based on the price at which coins last moved, giving a market consensus price for long-term holders.

CVDD (Cumulative Value Coin Days Destroyed): This on-chain metric analyzes Bitcoin’s UTXOs (unspent transaction outputs) and the velocity of coins moving between wallets. It highlights key market dynamics during prolonged accumulation or distribution phases.

Balanced Price: The Balanced Price is the difference between the Realized Price and the Terminal Price, adjusted by Bitcoin's supply constraints. This metric provides a useful signal for identifying oversold market conditions during bear markets.

BalancedPrice() =>

// It is calculated by subtracting Transferred Price from Realized Price

RealizedPrice() - (TerminalPrice() / (21 * 3))

Each component can be toggled individually, allowing users to focus on specific aspects of Bitcoin’s price cycle and derive meaningful insights from its long-term behavior. The combination of these models provides a well-rounded view of both speculative peaks and long-term value trends.

Important consideration:

Top Cap did historically provide reliable signals for cycle peaks, however it may not be a relevant indication of peaks in the future.

Indicator Test with Conditions TableOverview: The "Indicator Test with Conditions Table" is a customizable trading strategy developed using Pine Script™ for the TradingView platform. It allows users to define complex entry conditions for both long and short positions based on various technical indicators and price levels.

Key Features:

Customizable Input Conditions:

Users can configure up to three input conditions for both long and short entries, each with its own logical operator (AND/OR) for combining conditions.

Input conditions can be based on:

Price Sources: Users can select any price data (e.g., close, open, high, low) for each condition.

Comparison Operators: Users can choose from a variety of operators, including:

Greater than (>)

Greater than or equal to (>=)

Less than (<)

Less than or equal to (<=)

Equal to (=)

Not equal to (!=)

Crossover (crossover)

Crossunder (crossunder)

Logical Operators:

The strategy provides options for combining conditions using logical operators (AND/OR) for greater flexibility in defining entry criteria.

Dynamic Condition Evaluation:

The strategy evaluates the defined conditions dynamically, checking whether they are enabled before proceeding with the comparison.

Users can toggle conditions on and off using boolean inputs, allowing for quick adjustments without modifying the code.

Visual Feedback:

A table is displayed on the chart, providing real-time status updates on the conditions and whether they are enabled. This enhances user experience by allowing easy monitoring of the strategy's logic.

Order Execution:

The strategy enters long or short positions based on the combined conditions' evaluations, automatically executing trades when the criteria are met.

How to Use:

Set Up Input Conditions:

Navigate to the strategy’s input settings to configure your desired price sources, operators, and logical combinations for long and short conditions.

Monitor Conditions:

Observe the condition table displayed at the bottom right of the chart to see which conditions are enabled and their current evaluations.

Adjust Strategy Parameters:

Modify the conditions, logical operators, and input sources as needed to optimize the strategy for different market scenarios or trading styles.

Execution:

Once the conditions are met, the strategy will automatically enter trades based on the defined logic.

Conclusion: The "Indicator Test with Conditions Table" strategy is a robust tool for traders looking to implement customized trading logic based on various market conditions. Its flexibility and real-time monitoring capabilities make it suitable for both novice and experienced traders.

COT INDEX v2The **Commitment of Traders (COT)** report is a valuable tool for analyzing market sentiment, providing insight into the positions of futures traders at the close of the Tuesday trading session. Prepared by the Commodity Futures Trading Commission (CFTC), the report is published every Friday at 3:30 p.m. Eastern Time, and the data is freely available on the CFTC website.

Traders are categorized into three groups: **Commercial Traders**, **Non-Commercial Traders** (large speculators), and **Nonreportable** (small speculators). This information can be applied to charts to visualize the direction of the positions held by major market participants and to receive key COT signals.

The **COT index** ranges from 0% to 100%, reflecting market sentiment over the past 26 weeks. Extreme values, below 25% or above 75%, represent bearish or bullish sentiment, respectively. However, it is important to note that the COT index is not a timing tool but rather an indicator of the overall sentiment of major market players.

For a more tailored analysis, you can adjust the period for index calculation, customize chart styles, and highlight extreme areas.

Custom Text BoxThis is an indicator to have text anchored in any symbol or chart, keep your ules at sight so is easy for you to follow, have your Bias too.

Flat Market Range Pro [CHE]Flat Market Range Pro Indicator

Introduction

Hey there! 👋

Welcome to our overview of the Flat Market Range Pro indicator. Whether you're new to trading or a seasoned pro, this tool is designed to help you spot those flat market conditions where prices are chilling within a certain range. By highlighting these consolidation zones and potential breakout points, it offers some pretty neat insights to boost your trading strategies. Let’s dive in and explore how this indicator can make your trading journey smoother and more informed!

How It Works

The Flat Market Range Pro indicator is all about understanding the ebb and flow of the market. Here's a simple breakdown:

Range Detection:

Range Period (range_period): This sets the number of bars (think of them as time slices) the indicator looks back to find the highest highs and lowest lows. It’s like setting the scope for your search.

Minimum Candles in Range (min_candles_in_range): Ensures that there are enough candles (price bars) within the range to make the detection meaningful. No point in highlighting a range if it’s too short, right?

Adaptive Moving Average (AMA):

Think of AMA as the indicator’s way of staying flexible. It smooths out the price data to better spot trends within those flat ranges. Don’t worry, it’s working behind the scenes and won’t clutter your chart.

Breakout Detection:

When the price decides to break free from its cozy range, the indicator flags it. It waits for confirmation to make sure it’s not just a fleeting move, adding a layer of reliability to your signals.

Visualization:

Flat Market Zones: These are shaded areas that highlight where the price has been consolidating.

Support and Resistance Lines: Automatically drawn lines that mark key price levels, helping you see where the price might bounce or break through.

Trade Signals: Arrows popping up to show potential buy or sell opportunities when breakouts occur.

Breaking It Down

1. Detecting the Range

The indicator scans through the past range_period bars to find the highest and lowest prices. This creates a dynamic range that adjusts as new data comes in. It’s like having a smart assistant keeping an eye on where the action is happening.

2. The Role of AMA

Even though you won’t see AMA on your chart, it plays a crucial role. It helps the indicator adapt to changing market conditions by smoothing out the data, making sure the breakout signals are spot-on and not just random noise.

3. Spotting Breakouts

A breakout happens when the price moves beyond the established range. The indicator marks these moments with clear arrows, so you know when it might be a good time to jump in or out of a trade. Plus, it waits for confirmation to ensure these signals are solid.

4. Visualizing Flat Markets

Shaded boxes highlight the areas where the price has been consolidating, making it easy to see when the market is flat. Support and resistance lines are drawn automatically, and you can even customize how they look to match your personal style.

Customize It Your Way

One of the best things about the Flat Market Range Pro indicator is how customizable it is. Here’s what you can tweak:

Range Settings:

Adjust the range_period to fit different timeframes.

Set the min_candles_in_range to ensure the ranges you see are meaningful.

Moving Average Settings:

Change the ma_length and ma_lookback to fine-tune how the AMA responds to price movements.

Visual Tweaks:

Pick your favorite colors and transparency levels for the shaded zones.

Choose whether to display support and resistance lines and extend them indefinitely if you like.

Toggle trade arrows and labels on or off based on what you find most helpful.

Organizing these settings into logical groups makes it super easy to customize the indicator just the way you like it.

Real-World Examples

1. Spotting Consolidation: Imagine you’re watching a stock that’s been moving sideways for a while. The indicator highlights this consolidation with shaded boxes and support/resistance lines, giving you a clear picture of where the price is hanging out.

2. Trading Breakouts: When the price finally decides to break free from the range, the indicator pops up buy or sell arrows. This helps you catch the move early, whether you’re looking to enter a new trade or exit an existing one.

3. Making Informed Decisions: With clear visual cues and reliable signals, you can make smarter trading decisions without getting overwhelmed by too much information.

Behind the Scenes: Technical Insights

For those curious about the nuts and bolts, here’s a peek into how the Flat Market Range Pro indicator is built:

Efficient Range Calculation:

Uses loops to scan through the specified range_period, ensuring accurate detection of high and low points.

Adaptive Logic with AMA:

Incorporates the Simple Moving Average (SMA) to create a threshold coefficient, making the indicator responsive to market changes.

Clear Visualization:

Utilizes box.new and label.new for intuitive visual representations of flat markets.

Employs plotshape and plot to display breakout signals clearly on your chart.

Optimized Performance:

Avoids plotting unnecessary elements like AMA, keeping your chart clean and focused on what matters.

Why You’ll Love It

The Flat Market Range Pro indicator brings a lot to the table:

Accurate Range Detection:

Pinpoints consolidation zones by analyzing historical highs and lows.

Flexible and Adaptive:

AMA ensures the indicator stays responsive to different market conditions.

User-Friendly Visuals:

Shaded zones, support/resistance lines, and clear trade signals make your chart easy to understand at a glance.

Highly Customizable:

Tailor the settings to match your trading style and preferences.

Reliable Signals:

Confirmation mechanisms help reduce false signals, giving you more confidence in your trades.

Wrapping It Up

The Flat Market Range Pro indicator is a fantastic tool for anyone looking to navigate flat or consolidating markets with ease. By combining precise range detection, adaptive logic, and clear visual cues, it helps you identify consolidation phases and seize breakout opportunities effectively. Its customizable features ensure that it fits seamlessly into your trading strategy, whether you’re just starting out or have years of experience under your belt.

For more details, a step-by-step guide on using the indicator, and access to the full Pine Script code, check out the accompanying documentation or reach out for support. Happy trading! 🌟

Questions and Further Information

Got questions or need a hand with the Flat Market Range Pro indicator? Feel free to reach out! Whether you’re curious about how it works or need tips on customizing it for your trading style, we’re here to help. Also, give the indicator a try on different charts to see how it performs in various market conditions. Let’s make your trading experience better together!

Best regards

Chervolino

This script was inspired by: Trend Regularity Adaptive Moving Average

and

Range Detection by HasanRifat

ADX Trend Strength Analyzer█ OVERVIEW

This script implements the Average Directional Index (ADX), a powerful tool used to measure the strength of market trends. It works alongside the Directional Movement Index (DMI), which breaks down the directional market pressure into bullish (+DI) and bearish (-DI) components. The purpose of the ADX is to indicate when the market is in a strong trend, without specifying the direction. This indicator can be especially useful for identifying market trends early and validating trading strategies based on trend-following systems.

The ADX component in this script is based on two key parameters:

ADX Smoothing Length (adxlen), which determines the degree of smoothing for the trend strength.

DI Length (dilen), which defines the look-back period for calculating the directional index values.

Additionally, a horizontal line is plotted at the 30 level, providing a widely used threshold that signifies when a trend is considered strong (above 30).

█ CONCEPTS

Directional Movement (DM): The core idea behind this indicator is the calculation of price movement in terms of bullish and bearish forces. By evaluating the change in highs and lows, the script distinguishes between bullish movement (+DM) and bearish movement (-DM). These values are normalized by dividing them by the True Range (TR), creating the +DI and -DI values.

True Range (TR): The True Range is calculated using the Average True Range (ATR) formula, and it serves to smooth out volatility, ensuring that short-term fluctuations don't distort the long-term trend signal.

ADX Calculation: The ADX is derived from the absolute difference between the +DI and -DI. By smoothing this difference and normalizing it, the ADX is able to measure the overall strength of the trend without regard to whether the market is moving up or down. A rising ADX indicates increasing trend strength, while a falling ADX signals weakening trends.

█ METHODOLOGY

Directional Movement Calculation: The script first determines the upward and downward price movement by comparing changes in the high and low prices. If the upward movement is greater than the downward movement, it registers a bullish signal and vice versa for bearish movement.

True Range Adjustment: The script then applies a smoothing function to normalize these movements by dividing them by the True Range (ATR). This ensures that the trend signal is based on relative, rather than absolute, price movements.

ADX Signal Generation: The final step is to calculate the ADX by applying the Relative Moving Average (RMA) to the difference between +DI and -DI. This produces the ADX value, which is plotted in red, making it easy to visualize shifts in market momentum.

Threshold Line: A blue horizontal line is plotted at 30, which serves as a key reference point. When the ADX is above this line, it indicates a strong trend, whether bullish or bearish.

█ HOW TO USE

Trend Strength: Traders typically use the 30 level as a critical threshold. When the ADX is above 30, it signifies a strong trend, making it a favorable environment for trend-following strategies. Conversely, ADX values below 30 suggest a weak or non-trending market.

+DI and -DI Relationship: The indicator also provides insight into whether the trend is bullish or bearish. When +DI is greater than -DI, the market is considered bullish. When -DI is greater than +DI, the market is considered bearish. While this script focuses on the ADX value itself, the underlying +DI and -DI help interpret the trend direction.

Market Conditions: This indicator is effective in trending markets, but not ideal for choppy or sideways conditions. Traders can use it to determine the best entry and exit points when trends are strong, or to avoid trading in periods of low volatility.

Combining with Other Indicators: The ADX is commonly used in conjunction with oscillators like RSI or moving averages, to confirm the trend strength and avoid false signals.

█ METHOD VARIANTS

This script applies the standard approach for calculating the ADX, but could be adapted with the following variants:

Different Timeframes: The script could be modified to calculate ADX values across higher or lower timeframes, depending on the trader's strategy.

Custom Thresholds: Instead of using the default 30 threshold, traders could adjust the horizontal line to suit their own risk tolerance or market conditions.

Inamdar Wave - Winning Wave

The **"Inamdar Wave"**, also known as the **"Winning Wave"**, is a cutting-edge market indicator designed to help traders ride the waves of momentum and capitalize on high-probability opportunities. With its unique ability to adapt to market shifts, the Inamdar Wave ensures you're always in sync with the market's most profitable moves, making it an indispensable tool for traders looking for consistent success.

### Key Features of the "Inamdar Wave":

1. **Dynamic Market Movement Detection**:

- The **Inamdar Wave** tracks the market’s momentum and identifies clear waves of movement, allowing traders to catch both upswings and downswings with ease.

- This indicator dynamically adjusts based on price action and volatility, ensuring you're always aligned with the market’s natural flow.

- Whether the market is trending or ranging, the **Inamdar Wave** keeps you on the right path, helping you surf the market's waves effortlessly.

2. **Highly Profitable Buy/Sell Signals**:

- The **Inamdar Wave** generates precise buy and sell signals that guide you to the most profitable entry and exit points.

- Its built-in filters ensure you avoid market noise, focusing only on high-probability trades that maximize your potential for profit.

- You’ll confidently enter trades at the start of each new wave, ensuring you ride the momentum for maximum gains.

3. **Visual Wave Highlighting**:

- Color-coded zones help you easily spot bullish (upward) and bearish (downward) waves.

- Green highlights signal upward waves, while red zones indicate downward waves, making it visually simple to recognize the current market direction.

- This feature allows for quick decision-making and a clear understanding of the market's direction at a glance.

4. **Tailored for Any Market Condition**:

- Whether you’re trading a calm or highly volatile market, the **Inamdar Wave** adapts to the changing conditions, ensuring consistent performance across all environments.

- Its flexibility allows it to work seamlessly with any asset class—stocks, forex, crypto, or commodities—making it an all-in-one solution for traders.

- The **Inamdar Wave**'s real-time adjustments keep it relevant regardless of market conditions or timeframes.

5. **Real-Time Alerts**:

- Get instant alerts when a new wave begins, whether it's a buy, sell, or wave reversal.

- You’ll never miss out on a profitable opportunity with real-time notifications that keep you one step ahead of the market.

- These alerts help you act quickly, maximizing the potential of every market movement.

### Inputs:

- **Wave Period**: Customize the sensitivity of the wave detection with adjustable periods to suit your trading style.

- **Signal Source**: Choose from different price sources to fine-tune how the **Inamdar Wave** reacts to market movements.

- **Signal Strength**: Control the sensitivity of wave detection to focus on only the strongest and most profitable moves.

- **Buy/Sell Signals**: Easily toggle buy/sell signals on your chart for enhanced clarity.

- **Wave Highlighting**: Turn visual wave highlights on or off, depending on your preference.

### Use Case:

The **Inamdar Wave** is perfect for traders looking to capture the most profitable waves in any market. Whether you're a short-term scalper or a long-term trend follower, this indicator keeps you in sync with the market’s natural rhythm, ensuring that you're always riding the winning wave. With its powerful buy/sell signals and dynamic wave detection, you'll be better positioned to take advantage of market momentum and secure consistent profits.

In conclusion, the **"Inamdar Wave"** is not just another indicator—it’s your key to riding the market’s most profitable waves with precision and confidence. By following the signals and staying in tune with the market’s natural flow, you’ll be able to maximize your gains and minimize your risks, ensuring a successful trading journey.

US Sentiment Index [CryptoSea]The US Sentiment Index is an advanced analytical tool designed for traders seeking to uncover patterns, correlations, and potential leading signals across key market tickers. This indicator surpasses traditional sentiment measures, providing a data-driven approach that offers deeper insights compared to conventional indices like the Fear and Greed Index.

Key Features

Multi-Ticker Analysis: Integrates data from a diverse set of market indicators, including gold, S&P 500, U.S. Dollar Index, Volatility Index, and more, to create a comprehensive view of market sentiment.

Customisable Sensitivity Settings: Allows users to adjust the moving average period to fine-tune the sensitivity of sentiment calculations, adapting the tool to various market conditions and trading strategies.

Detailed Sentiment Scaling: Utilises a 0-100 scale to quantify sentiment strength, with colour gradients that visually represent bearish, neutral, and bullish conditions, aiding in quick decision-making.

Below is an example where the sentiment index can give leading signals. We see a first sign of wekaness in the index as it drops below its moving average. Shortly after we see it dip below our median 50 level, another sign of weakeness. We see the SPX price action to take a hit following the sentiment index decrease.

Tickers Used and Their Impact on Sentiment

The impact of each ticker on sentiment can be bullish or bearish, depending on their behaviour:

Gold (USGD): Typically seen as a safe-haven asset, rising gold prices often indicate increased market fear or bearish sentiment. Conversely, falling gold prices can signal reduced fear and a shift towards bullish sentiment in riskier assets.

S&P 500 (SPX): A rising S&P 500 is usually a sign of bullish sentiment, reflecting confidence in economic growth and market stability. A decline, however, suggests bearish sentiment and a potential move towards risk aversion.

U.S. Dollar Index (DXY): A strengthening U.S. Dollar can be a sign of fear as investors seek safety in the dollar, which is bearish for risk assets. A weakening dollar, on the other hand, can signal bullish sentiment as capital flows into riskier assets.

Volatility Index (VIX): Known as the "fear gauge," a rising VIX indicates increased market fear and bearish sentiment. A falling VIX suggests a calm, bullish market environment.

Junk Bonds (JNK): Rising junk bond prices often reflect bullish sentiment as investors take on more risk for higher returns. Conversely, falling junk bond prices signal increased fear and bearish sentiment.

Long-Term Treasury Bonds (TLT): Higher prices for long-term treasuries usually indicate a flight to safety, reflecting bearish sentiment. Lower prices suggest a shift towards riskier assets, indicating bullish sentiment.

Financial Sector ETF (XLF): Strength in the financial sector is typically bullish, indicating confidence in economic conditions. Weakness in this sector can reflect bearish sentiment and concerns about financial stability.

Unemployment Rate (USUR): A rising unemployment rate is a bearish signal, indicating economic weakness. A declining unemployment rate is bullish, reflecting economic strength and job growth.

U.S. Interest Rates (USINTR, USIRYY): Higher interest rates can be bearish, as they increase borrowing costs and reduce spending. Lower rates are generally bullish, promoting economic growth and risk-taking.

How it Works

Sentiment Calculation: The US Sentiment Index combines data from multiple tickers, calculating sentiment by scaling the distance from their respective moving averages. Each asset's behaviour is interpreted within the context of market fear or greed, providing a refined sentiment reading that adjusts dynamically.

Market Strength Analysis: When the index is above 50 and also above its moving average, it indicates particularly strong or bullish market conditions, driven by greed. Conversely, when the index is below 50 and under its moving average, it signals bearish or weak market conditions, associated with fear.

Correlation and Pattern Detection: The indicator analyses correlations among the included assets to detect patterns that might signal potential market movements, giving traders a leading edge over simpler sentiment measures.

Adaptive Background Colouring: Utilises a colour gradient that dynamically adjusts based on sentiment values, highlighting extreme fear, neutral, and extreme greed levels directly on the chart.

Flexible Display Options: Offers settings to toggle the moving average plot and adjust its period, giving users the ability to tailor the indicator's sensitivity and display to their specific needs.

In this example below, we can see the Sentiment rise above the Moving Average (MA). Price action goes on to follow this, although there is an instance where it dips below the MA, it quickly rises back above again as a sign of strength.

Another way you can use this index is by simply using the MA, if its trending up, we know the macro sentiment is bullish.

Application

Data-Driven Insights: Offers traders a detailed, data-driven approach to sentiment analysis, incorporating a broad spectrum of market indicators to deliver actionable insights.

Pattern Recognition: Helps identify patterns and correlations that may lead to market reversals or continuations, providing a nuanced view that goes beyond simple sentiment gauges.

Enhanced Decision-Making: Equips traders with a robust tool to validate trading strategies and make informed decisions based on comprehensive sentiment analysis.

The US Sentiment Index by is an essential addition to the toolkit of any trader looking to navigate market complexities with precision and confidence. Its advanced features and data-driven approach offer unparalleled insights into market sentiment, setting it apart from conventional sentiment indicators.

Seasonal Tendency (fadi)Seasonal tendency refers to the patterns in stock market performance that tend to repeat at certain times of the year. These patterns can be influenced by various factors such as economic cycles, investor behavior, and historical trends. For example, the stock market often performs better during certain months like November to April, a phenomenon known as the “best six months” strategy. Conversely, months like September are historically weaker.

These tendencies can help investors and traders make more informed decisions by anticipating potential market movements based on historical data. However, it’s important to remember that past performance doesn’t guarantee future results.

This indicator calculates the average daily move patterns over the specified number of years and then removes any outliers.

Settings

Number of years : The number of years to use in the calculation. The number needs to be large enough to create a pattern, but not so large that it may distort the price move.

Seasonality line color : The plotted line color.

Border : Show or hide the border and the color to use.

Grid : Show or hide the grid and the color to use.

Outlier Factor : The Outlier Factor is used to identify unusual price moves that are not typical and neutralize them to avoid skewing the predictions. It is the amount of deviation calculated using the total median price move.

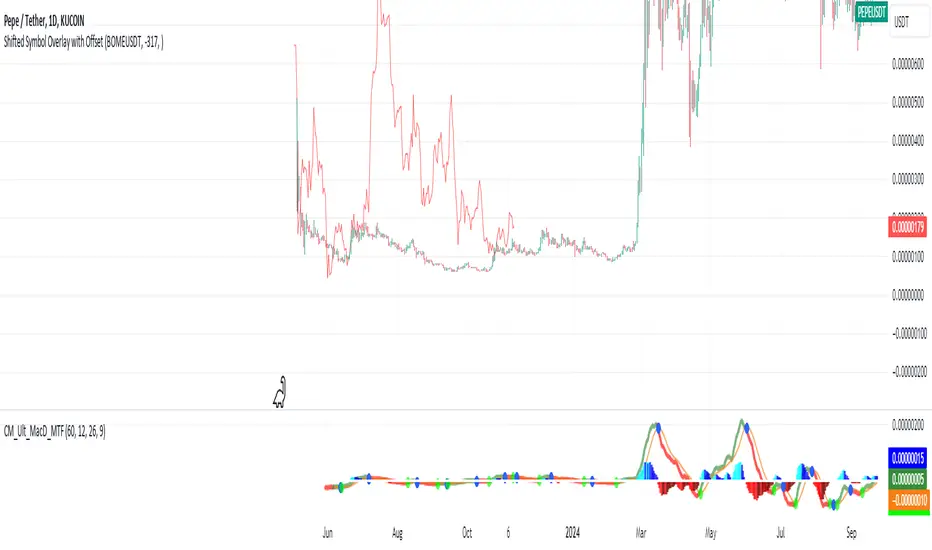

Shifted Symbol Overlay with OffsetThe Shifted Symbol Overlay Indicator is a custom TradingView indicator designed to overlay the price data of one stock or asset over another, allowing for direct visual comparison. This is particularly useful for comparing the performance of two assets over different time periods. The indicator enables you to shift the data from one asset either forward or backward in time, making it easier to compare historical data from one stock with more recent data from another. The indicator supports shifting both to the right (future periods) and to the left (earlier periods), helping traders and analysts explore correlations or divergences between two financial instruments.

The indicator also includes a normalization option that adjusts the scale of the two assets, so you can compare them even if they have vastly different price levels. This is useful when you're interested in relative performance rather than the absolute price values.

Precision Cloud by Dr ABIRAM SIVPRASAD

Precision Cloud by Dr. Abhiram Sivprasad"

The " Precision Cloud" script, created by Dr. Abhiram Sivprasad, is a multi-purpose technical analysis tool designed for Forex, Bitcoin, Commodities, Stocks, and Options trading. It focuses on identifying key levels of support and resistance, combined with moving averages (EMAs) and central pivot ranges (CPR), to help traders make informed trading decisions. The script also provides a visual "light system" to highlight potential long or short positions, aiding traders in entering trades with a clear strategy.

Key Features of the Script:

Central Pivot Range (CPR):

The CPR is calculated as the average of the high, low, and close of the price, while the top and bottom pivots are derived from it. These act as dynamic support and resistance zones.

The script can plot daily CPR, support, and resistance levels (S1/R1, S2/R2, S3/R3) as well as optional weekly and monthly pivot points.

The CPR helps identify whether the price is in a bullish, bearish, or neutral zone.

Support and Resistance Levels:

Three daily support (S1, S2, S3) and resistance (R1, R2, R3) levels are plotted based on the CPR.

These levels act as potential reversal or breakout points, allowing traders to make decisions around key price points.

EMA (Exponential Moving Averages):

The script includes two customizable EMAs (default periods of 9 and 21). You can choose the source for these EMAs (open, high, low, or close).

The crossovers between EMA1 and EMA2 help identify potential trend reversals or momentum shifts.

Lagging Span:

The Lagging Span is plotted with a customizable displacement (default 26), which helps identify overall trend direction by comparing past price with the current price.

Light System:

A color-coded table provides a visual representation of market conditions:

Green indicates bullish signals (e.g., price above CPR, EMAs aligning positively).

Red indicates bearish signals (e.g., price below CPR, EMAs aligning negatively).

Yellow indicates neutral conditions, where there is no clear trend direction.

The system includes lights for CPR, EMA, Long Position, and Short Position, helping traders quickly assess whether the market is in a buying or selling opportunity.

Trading Strategies Using the Script

1. Forex Trading:

Trend-Following with EMAs: Use the EMA crossovers to capture trending markets in Forex. A green light for the EMA combined with a price above the daily or weekly pivot levels suggests a buying opportunity. Conversely, if the EMA light turns red and price falls below the CPR levels, look for shorting opportunities.

Reversal Strategy: Watch for price action near the daily S1/R1 levels. If price holds above S1 and the EMA is green, this could signal a reversal from support. The same applies to resistance levels.

2. Bitcoin Trading:

Momentum Breakouts: Bitcoin is known for its sharp moves. The script helps to identify breakouts from the CPR range. If the price breaks above the TC (Top Central Pivot) with bullish EMA alignment (green light), it could signal a strong uptrend.

Lagging Span Confirmation: Use the Lagging Span to confirm the trend direction. For Bitcoin's volatility, when the lagging span shows consistent alignment with the price and CPR, it often indicates continuation of the trend.

3. Commodities Trading:

Support/Resistance Bounce: Commodities such as gold and oil often react well to pivot levels. Look for price bouncing off S1 or R1 for potential entry points. A green CPR light along with price above the pivot range supports a bullish bias.

EMA Pullback Strategy: If price moves in a strong trend and pulls back to one of the EMAs, a green EMA light suggests re-entry on a pullback. If the EMA light is red and price breaks below the BC (Bottom Central Pivot), short positions could be considered.

4. Stocks Trading:

Long Position Strategy: For stocks, use the combination of the long position light turning green (price above TC and EMA alignment) as a signal to buy. This could be especially useful for riding bullish trends in growth stocks or during earnings seasons when volatility is high.

Short Position Strategy: If the short position light turns green, indicating price below BC and EMAs turning bearish, this could be an ideal setup for shorting overvalued stocks or during market corrections.

5. Options Trading:

Directional Bias for Options: The light system is particularly helpful for options traders. A green long position light provides a clear signal to buy call options, while a green short position light supports buying puts.

Pivot Breakout Strategy: Buy options (calls or puts) when the price breaks above resistance or below support, with confirmation from the CPR and EMA lights. This helps capture the sharp moves required for profitable options trades.

Conclusion

The S&R Precision Cloud script is a versatile tool for traders across markets, including Forex, Bitcoin, Commodities, Stocks, and Options. It combines critical technical elements like pivot ranges, support and resistance levels, EMAs, and the Lagging Span to provide a clear picture of market conditions. The intuitive light system helps traders quickly assess whether to take a long or short position, making it an excellent tool for both new and experienced traders.

The S&R Precision Cloud by Dr. Abhiram Sivprasad script is a technical analysis tool designed to assist traders in making informed decisions. However, it should not be interpreted as financial or investment advice. The signals generated by the script are based on historical price data and technical indicators, which are inherently subject to market fluctuations and do not guarantee future performance.

Trading in Forex, Bitcoin, Commodities, Stocks, and Options carries a high level of risk and may not be suitable for all investors. You should be aware of the risks involved and be willing to accept them before engaging in such activities. Always conduct your own research and consult with a licensed financial advisor or professional before making any trading decisions.

The creators of this script are not responsible for any financial losses that may occur from its use. Past performance is not indicative of future results, and the use of this script is at your own risk.

AHR999 Bitcoin Buy/Sell Signals Indicator - Accurate Trading OppThis Pine Script indicator combines the AHR999 metric with Bitcoin's historical price trends to provide clear buy and sell signals, assisting you in making informed trading decisions at crucial moments. It calculates the AHR999 index based on Bitcoin's 200-day Geometric Moving Average (GMA) and the estimated price, offering customizable buy and sell thresholds for precise entry and exit points. Ideal for traders looking to capture long-term investment trends, this indicator helps you effectively identify Bitcoin market opportunities.

Bitcoin Logarithmic Growth Curve 2024The Bitcoin logarithmic growth curve is a concept used to analyze Bitcoin's price movements over time. The idea is based on the observation that Bitcoin's price tends to grow exponentially, particularly during bull markets. It attempts to give a long-term perspective on the Bitcoin price movements.

The curve includes an upper and lower band. These bands often represent zones where Bitcoin's price is overextended (upper band) or undervalued (lower band) relative to its historical growth trajectory. When the price touches or exceeds the upper band, it may indicate a speculative bubble, while prices near the lower band may suggest a buying opportunity.

Unlike most Bitcoin growth curve indicators, this one includes a logarithmic growth curve optimized using the latest 2024 price data, making it, in our view, superior to previous models. Additionally, it features statistical confidence intervals derived from linear regression, compatible across all timeframes, and extrapolates the data far into the future. Finally, this model allows users the flexibility to manually adjust the function parameters to suit their preferences.

The Bitcoin logarithmic growth curve has the following function:

y = 10^(a * log10(x) - b)

In the context of this formula, the y value represents the Bitcoin price, while the x value corresponds to the time, specifically indicated by the weekly bar number on the chart.

How is it made (You can skip this section if you’re not a fan of math):

To optimize the fit of this function and determine the optimal values of a and b, the previous weekly cycle peak values were analyzed. The corresponding x and y values were recorded as follows:

113, 18.55

240, 1004.42

451, 19128.27

655, 65502.47

The same process was applied to the bear market low values:

103, 2.48

267, 211.03

471, 3192.87

676, 16255.15

Next, these values were converted to their linear form by applying the base-10 logarithm. This transformation allows the function to be expressed in a linear state: y = a * x − b. This step is essential for enabling linear regression on these values.

For the cycle peak (x,y) values:

2.053, 1.268

2.380, 3.002

2.654, 4.282

2.816, 4.816

And for the bear market low (x,y) values:

2.013, 0.394

2.427, 2.324

2.673, 3.504

2.830, 4.211

Next, linear regression was performed on both these datasets. (Numerous tools are available online for linear regression calculations, making manual computations unnecessary).

Linear regression is a method used to find a straight line that best represents the relationship between two variables. It looks at how changes in one variable affect another and tries to predict values based on that relationship.

The goal is to minimize the differences between the actual data points and the points predicted by the line. Essentially, it aims to optimize for the highest R-Square value.

Below are the results:

It is important to note that both the slope (a-value) and the y-intercept (b-value) have associated standard errors. These standard errors can be used to calculate confidence intervals by multiplying them by the t-values (two degrees of freedom) from the linear regression.

These t-values can be found in a t-distribution table. For the top cycle confidence intervals, we used t10% (0.133), t25% (0.323), and t33% (0.414). For the bottom cycle confidence intervals, the t-values used were t10% (0.133), t25% (0.323), t33% (0.414), t50% (0.765), and t67% (1.063).

The final bull cycle function is:

y = 10^(4.058 ± 0.133 * log10(x) – 6.44 ± 0.324)

The final bear cycle function is:

y = 10^(4.684 ± 0.025 * log10(x) – -9.034 ± 0.063)

The main Criticisms of growth curve models:

The Bitcoin logarithmic growth curve model faces several general criticisms that we’d like to highlight briefly. The most significant, in our view, is its heavy reliance on past price data, which may not accurately forecast future trends. For instance, previous growth curve models from 2020 on TradingView were overly optimistic in predicting the last cycle’s peak.

This is why we aimed to present our process for deriving the final functions in a transparent, step-by-step scientific manner, including statistical confidence intervals. It's important to note that the bull cycle function is less reliable than the bear cycle function, as the top band is significantly wider than the bottom band.

Even so, we still believe that the Bitcoin logarithmic growth curve presented in this script is overly optimistic since it goes parly against the concept of diminishing returns which we discussed in this post:

This is why we also propose alternative parameter settings that align more closely with the theory of diminishing returns.

Our recommendations:

Drawing on the concept of diminishing returns, we propose alternative settings for this model that we believe provide a more realistic forecast aligned with this theory. The adjusted parameters apply only to the top band: a-value: 3.637 ± 0.2343 and b-parameter: -5.369 ± 0.6264. However, please note that these values are highly subjective, and you should be aware of the model's limitations.

Conservative bull cycle model:

y = 10^(3.637 ± 0.2343 * log10(x) - 5.369 ± 0.6264)

Birdies [LuxAlgo]The Birdies indicator uses a unique technique to provide support/resistance curves based on a circle connecting the last swing high/low.

A specific, customizable part of this circle acts as a curve of interest, which can trigger visual breakout signals.

🔶 USAGE

The script projects a bird-like pattern when a valid Swing point is found. Multiple customization options are included.

🔹 Trend & Support/Resistance Tool

The color fill patterns and the wing boundaries can give insights into the current trend direction as well as serve as potential support/resistance areas.

In the example above, "Birdies" coincide with pullback and support/resistance zones.

🔹 Swing Length & Buffer

Besides the "Swing Length", with higher values returning longer-term Swing Levels, the script's behavior can be fine-tuned with filters ("Settings" - "Validation").

🔹 Validation

To minimize clutter, three filters are included:

Minimum X-Distance: The minimum amount of bars between subsequent Swings

Minimum Y-Distance: The minimum amount of bars between subsequent Swings

Buffer (Multiple of ATR)

The "Minimum X/Y-Distance" creates a zone where a new Swing is considered invalid. Only when the Swing is out of the zone, can it be considered valid.

In other words, in the example above, a Swing High can only be valid when enough bars/time have passed, and the difference between the last Swing and the previous is more than the ATR multiplied by the "Minimum Y-Distance" factor.

The "Buffer" creates a line above/below the "Birdy", derived from the measured ATR at the conception of the "Birdy" multiplied with a factor ("Buffer").

When the closing price crosses the "Birdy", it must also surpass this buffer line to produce a valid signal, lowering the risk of clutter as a result.

🔶 DETAILS

Birdies are derived from a circle that connects two Swing points. The left-wing curve originates from the most recent "Swing point" to the last value on the circle before crossing its midline. The mirror image of the left wing creates the right wing.

Enabling "Origine" will draw a line from the last Swing to the first.

🔹 Style

The publication includes a style setting with four options.

The first, "Birdy," shows a bird-like shape derived from a circle connecting the last Swing High and Swing Low.

The second option holds everything from the first option but connects both wingtips, providing potential horizontal levels of interest.

When setting "Birdy" to "None", the visual breakout signals will not defer from previous settings, but the focus is shifted towards the fill color, which can help detect potential trend shift.

A fourth setting, "Left Wing", will only show the left part of the "Birdy" pattern, removing the right part from the equation. This will change the visual breakout signals, providing alternative signals.

🔶 SETTINGS

Swing Length: The period used for swing detection, with higher values returning longer-term Swing Levels.

🔹 Validation

Minimum X-Distance: The minimum amount of bars between subsequent Swings

Minimum Y-Distance: The minimum amount of bars between subsequent Swings

Buffer (Multiple of ATR)

🔹 Style

Bullish Patterns: Enable / color

Bearish Patterns: Enable / color

Buffer Zone: Show / Color

Color Fill: Show color fill between two Birdies (if available)

Origine: Show the line between both Swing Points

🔹 Calculation

Calculated Bars: Allows the usage of fewer bars for performance/speed improvement

Standard Deviation based Upper Lower RangeThis script makes use of historical data for finding the standard deviation on daily returns. Based on the mean and standard deviation, the upper and lower range for the stock is shown upto 2x standard deviation. These bounds can be treated as volatility range for the next n trading sessions. This volatility is based on historical data. Users can change the lookback historical period, and can also set the time period (days) for upcoming trading sessions.

This indicator can be useful in determining stoploss and target levels along with the traditional support/resistance levels. It can also be useful in option trading where one needs to determine a range beyond which it is safe to sell an option.

A range of 1 SD has around 65% to 68% probability that it will not be breached. A range of 2 SD has around 95% probability that it will not be breached.

The indicator is based on Normal distribution theory. In future editions, I envision to also calculate the skewness and kurtosis so that we can determine if a stock is properly following Normal Distribution theory. That may further favor the calculated range.

Winning and Losing StreaksThe Pine Script indicator "Winning and Losing Streaks" tracks and visualizes the length of consecutive winning and losing streaks in a financial series, such as stock prices. Here’s a detailed description of the indicator, including the relevance of statistical analysis and streak tracking.

Indicator Description

The "Winning and Losing Streaks" indicator in Pine Script is designed to analyze and display streaks of consecutive winning and losing days in trading data. It helps traders and analysts understand the persistence of trends in price movements.

Here’s how it functions:

Streak Calculation:

Winning Streak: A series of consecutive days where the closing price is higher than the previous day's closing price.

Losing Streak: A series of consecutive days where the closing price is lower than the previous day's closing price.

Doji Candles: The indicator also considers Doji candles, where the difference between the opening and closing prices is minimal relative to the high-low range, and excludes these from being counted as winning or losing days.

Statistical Analysis:

The indicator computes the maximum and average lengths of winning and losing streaks.

It also tracks the current streak lengths and maintains arrays to store the historical streak data.

Visualization:

Histograms: Winning and losing streaks are visualized using histograms, which provide a clear graphical representation of streak lengths over time.

Relevance of Statistical Analysis and Streak Tracking

1. Statistical Significance of Streaks

Tracking winning and losing streaks has significant statistical implications for trading strategies and risk management:

Autocorrelation: Streaks in financial time series can reveal autocorrelation, where past returns influence future returns. Studies have shown that financial time series often exhibit autocorrelation, which can be used to forecast future price movements (Lo, 1991; Jegadeesh & Titman, 1993). Understanding streaks helps in identifying and leveraging these patterns.

Behavioral Finance: Streak analysis aligns with concepts from behavioral finance, such as the "hot-hand fallacy," where investors may perceive trends as more persistent than they are (Gilovich, Vallone, & Tversky, 1985). Statistical streak analysis provides a more objective view of trend persistence, helping to avoid biases.

2. Risk Management and Strategy Development

Risk Assessment: Identifying the length and frequency of losing streaks is crucial for managing risk and adjusting trading strategies. Long losing streaks can indicate potential strategy weaknesses or market regime changes, prompting a reassessment of trading rules and risk management practices (Brock, Lakonishok, & LeBaron, 1992).

Strategy Optimization: Statistical analysis of streaks can aid in optimizing trading strategies. For example, understanding the average length of winning and losing streaks can help in setting more effective stop-loss and take-profit levels, as well as in determining the optimal position sizing (Fama & French, 1993).

Scientific References:

Lo, A. W. (1991). "Long-Term Memory in Stock Market Prices." Econometrica, 59(5), 1279-1313. This paper discusses the presence of long-term memory in stock prices, which is relevant for understanding the persistence of streaks.

Jegadeesh, N., & Titman, S. (1993). "Returns to Buying Winners and Selling Losers: Implications for Stock Market Efficiency." Journal of Finance, 48(1), 65-91. This study explores momentum and reversal strategies, which are related to the concept of streaks.

Gilovich, T., Vallone, R., & Tversky, A. (1985). "The Hot Hand in Basketball: On the Misperception of Random Sequences." Cognitive Psychology, 17(3), 295-314. This paper provides insight into the psychological aspects of streaks and persistence.

Brock, W., Lakonishok, J., & LeBaron, B. (1992). "Simple Technical Trading Rules and the Stochastic Properties of Stock Returns." Journal of Finance, 47(5), 1731-1764. This research examines the effectiveness of technical trading rules, relevant for streak-based strategies.

Fama, E. F., & French, K. R. (1993). "Common Risk Factors in the Returns on Stocks and Bonds." Journal of Financial Economics, 33(1), 3-56. This paper provides a foundation for understanding risk factors and strategy performance.

By analyzing streaks, traders can gain valuable insights into market dynamics and refine their trading strategies based on empirical evidence.

PERFECT PIVOT RANGE DR ABIRAM SIVPRASAD (PPR)PERFECT PIVOT RANGE (PPR) by Dr. Abhiram Sivprasad

The Perfect Pivot Range (PPR) indicator is designed to provide traders with a comprehensive view of key support and resistance levels based on pivot points across different timeframes. This versatile tool allows users to visualize daily, weekly, and monthly pivots along with high and low levels from previous periods, helping traders identify potential areas of price reversals or breakouts.

Features:

Multi-Timeframe Pivots:

Daily, weekly, and monthly pivot levels (Pivot Point, Support 1 & 2, Resistance 1 & 2).

Helps traders understand price levels across various timeframes, from short-term (daily) to long-term (monthly).

Previous High-Low Levels:

Displays the previous week, month, and day high-low levels to highlight key zones of historical support and resistance.

Traders can easily see areas of price action from prior periods, giving context for future price movements.

Customizable Options:

Users can choose which pivot levels and high-lows to display, allowing for flexibility based on trading preferences.

Visual settings can be toggled on and off to suit different trading strategies and timeframes.

Real-Time Data:

All pivot points and levels are dynamically calculated based on real-time price data, ensuring accurate and up-to-date information for decision-making.

How to Use:

Pivot Points: Use daily, weekly, or monthly pivot points to find potential support or resistance levels. Prices above the pivot suggest bullish sentiment, while prices below indicate bearishness.

Previous High-Low: The high-low levels from previous days, weeks, or months can serve as critical zones where price may reverse or break through, indicating potential trade entries or exits.

Confluence: When pivot points or high-low levels overlap across multiple timeframes, they become even stronger levels of support or resistance.

This indicator is suitable for all types of traders (scalpers, swing traders, and long-term investors) looking to enhance their technical analysis and make more informed trading decisions.

Here are three detailed trading strategies for using the Perfect Pivot Range (PPR) indicator for options, stocks, and commodities:

1. Options Buying Strategy with PPR Indicator

Strategy: Buying Call and Put Options Based on Pivot Breakouts

Objective: To capitalize on sharp price movements when key pivot levels are breached, leading to high returns with limited risk in options trading.

Timeframe: 15-minute to 1-hour chart for intraday option trading.

Steps:

Identify the Key Levels:

Use weekly pivots for intraday trading, as they provide more significant levels for options.

Enable the "Previous Week High-Low" to gauge support and resistance from the previous week.

Call Option Setup (Bullish Breakout):

Condition: If the price breaks above the weekly pivot point (PP) with high momentum (indicated by a strong bullish candle), it signifies potential bullishness.

Action: Buy Call Options at the breakout of the weekly pivot.

Confirmation: Check if the price is sustaining above the pivot with a minimum of 1-2 candles (depending on timeframe) and the first resistance (R1) isn’t too far away.

Target: The first resistance (R1) or previous week’s high can be your target for exiting the trade.

Stop-Loss: Set a stop-loss just below the pivot point (PP) to limit risk.

Put Option Setup (Bearish Breakdown):

Condition: If the price breaks below the weekly pivot (PP) with strong bearish momentum, it’s a signal to expect a downward move.

Action: Buy Put Options on a breakdown below the weekly pivot.

Confirmation: Ensure that the price is closing below the pivot, and check for declining volumes or bearish candles.

Target: The first support (S1) or the previous week’s low.

Stop-Loss: Place the stop-loss just above the pivot point (PP).

Example:

Let’s say the weekly pivot point (PP) is at 1500, the price breaks above and sustains at 1510. You buy a Call Option with a strike price near 1500, and the target will be the first resistance (R1) at 1530.

2. Stock Trading Strategy with PPR Indicator

Strategy: Swing Trading Using Pivot Points and Previous High-Low Levels

Objective: To capture mid-term stock price movements using pivot points and historical high-low levels for better trade entries and exits.

Timeframe: 1-day or 4-hour chart for swing trading.

Steps:

Identify the Trend:

Start by determining the overall trend of the stock using the weekly pivots. If the price is consistently above the pivot point (PP), the trend is bullish; if below, the trend is bearish.

Buy Setup (Bullish Trend Reversal):

Condition: When the stock bounces off the weekly pivot point (PP) or previous week’s low, it signals a bullish reversal.

Action: Enter a long position near the pivot or previous week’s low.

Confirmation: Look for a bullish candle pattern or increasing volumes.

Target: Set your first target at the first resistance (R1) or the previous week’s high.

Stop-Loss: Place your stop-loss just below the previous week’s low or support (S1).

Sell Setup (Bearish Trend Reversal):

Condition: When the price hits the weekly resistance (R1) or previous week’s high and starts to reverse downwards, it’s an opportunity to short-sell the stock.

Action: Enter a short position near the resistance.

Confirmation: Watch for bearish candle patterns or decreasing volume at the resistance.

Target: Your first target would be the weekly pivot point (PP), with the second target as the previous week’s low.

Stop-Loss: Set a stop-loss just above the resistance (R1).

Use Previous High-Low Levels:

The previous week’s high and low are key levels where price reversals often occur, so use them as reference points for potential entry and exit.

Example:

Stock XYZ is trading at 200. The previous week’s low is 195, and it bounces off that level. You enter a long position with a target of 210 (previous week’s high) and place a stop-loss at 193.

3. Commodity Trading Strategy with PPR Indicator

Strategy: Trend Continuation and Reversal in Commodities

Objective: To capitalize on the strong trends in commodities by using pivot points as key support and resistance levels for trend continuation and reversal.

Timeframe: 1-hour to 4-hour charts for commodities like Gold, Crude Oil, Silver, etc.

Steps:

Identify the Trend:

Use monthly pivots for long-term commodities trading since commodities often follow macroeconomic trends.

The monthly pivot point (PP) will give an idea of the long-term trend direction.

Trend Continuation Setup (Bullish Commodity):

Condition: If the price is consistently trading above the monthly pivot and pulling back towards the pivot without breaking below it, it indicates a bullish continuation.

Action: Enter a long position when the price tests the monthly pivot (PP) and starts moving up again.

Confirmation: Look for a strong bullish candle or an increase in volume to confirm the continuation.

Target: The first resistance (R1) or previous month’s high.

Stop-Loss: Place the stop-loss below the monthly pivot (PP).

Trend Reversal Setup (Bearish Commodity):

Condition: When the price reverses from the monthly resistance (R1) or previous month’s high, it’s a signal for a bearish reversal.

Action: Enter a short position at the resistance level.

Confirmation: Watch for bearish candle patterns or decreasing volumes at the resistance.

Target: Set your first target as the monthly pivot (PP) or the first support (S1).

Stop-Loss: Stop-loss should be placed just above the resistance level.

Using Previous High-Low for Swing Trades:

The previous month’s high and low are important in commodities. They often act as barriers to price movement, so traders should look for breakouts or reversals near these levels.

Example:

Gold is trading at $1800, with a monthly pivot at $1780 and the previous month’s high at $1830. If the price pulls back to $1780 and starts moving up again, you enter a long trade with a target of $1830, placing your stop-loss below $1770.

Key Points Across All Strategies:

Multiple Timeframes: Always use a combination of timeframes for confirmation. For example, a daily chart may show a bullish setup, but the weekly pivot levels can provide a larger trend context.

Volume: Volume is key in confirming the strength of price movement. Always confirm breakouts or reversals with rising or declining volume.

Risk Management: Set tight stop-loss levels just below support or above resistance to minimize risk and lock in profits at pivot points.

Each of these strategies leverages the powerful pivot and high-low levels provided by the PPR indicator to give traders clear entry, exit, and risk management points across different markets