Tomas' Financial Conditions Z Score"The indicator is a composite z-score comprised of the following four components (equally-weighted):

Credit spreads - ICE BofA High Yield Option Adjusted Spread (BAMLH0A0HYM2) and ICE BofA Corporate Index Option Adjusted Spread (BAMLC0A0CM)

Volatility indexes - VIX (S&P 500 implied volatility) and MOVE (US Treasury bond implied volatility)

I've got it set to a 160-day lookback period, which I think is roughly the best setting after some tinkering.

When the z-score is above zero, it throws a red signal - and when the z-score is below zero, it throws a green signal.

This indicator is a follow-on from the "traffic light financial conditions indicator" that I wrote a thread about a couple of months ago.

I moved on from that previous indicator because it is based on the Federal Reserve's NFCI, which is regularly revised, but I didn't take that into account at the time.

So not a great real-time indicator, if the signal can be subsequently revised in the opposite direction weeks later.

This new indicator is based on real-time market data, so there's no revisions, and it also updates daily, as opposed to weekly for the NFCI"

Fundamental Analysis

US Recessions OverlayThe US Recessions Overlay indicator highlights the periods of US economic recessions directly on your TradingView chart. Using historical data from the Great Depression to the present, it provides a visual representation of recessions as transparent red backgrounds. This can help traders and analysts correlate market movements with historical economic downturns.

Features:

- Displays US recessions since the Great Depression (1929) as shaded areas.

- Automatically adjusts the background shading to match the date ranges of historical recessions.

- A simple and effective way to observe market behavior during recessionary periods.

- Fully customizable to include new recession periods or modify transparency levels.

How to Use:

Apply the indicator to any chart. Recession periods will appear as red-shaded backgrounds, providing a clear visual cue for market behavior during those times.

Use Case:

Ideal for traders, economists, and market historians who wish to study the impact of recessions on financial markets.

Crypto Sectors Performance [Daveatt]IMPORTANT

⚠️ This script must be used on the Daily timeframe only.

OVERVIEW

This indicator brings the powerful sector analysis capabilities from velo.xyz/market's

Sector Performance chart to TradingView.

It enables traders to track and compare performance across the crypto market's major sectors, providing essential insights for sector rotation strategies and market analysis.

CALCULATION METHOD

The indicator calculates performance across six key crypto sectors: DeFi, Gaming, Layer 1s, Layer 2s, AI, and Memecoins.

For each sector, it computes a rolling percentage performance by averaging the performance of multiple representative tokens.

All sector performances are rebased to 0% at the start of each period, making relative comparisons clear and intuitive.

VISUALIZATION MODES

The script features two distinct visualization methods:

Plots Mode:

Displays continuous performance lines for each sector over time, ideal for tracking relative strength trends and sector momentum. Each sector has its own color-coded line with performance values clearly marked.

Bars Mode:

Presents current sector performance as vertical bars, offering an immediate visual comparison of sector gains and losses.

The bars are color-coded and labeled with exact percentage values for precise analysis.

For the "Bars Mode", I used the box.new() function

SECTOR COMPOSITION

Each sector comprises carefully selected representative tokens:

- DeFi: AAVE, 1INCH, JUP, MKR, UNI

- Gaming: GALA, AXS, RONIN, SAND

- Layer 1: BTC, ETH, AVAX, APT, SOL, BNB, SUI

- Layer 2: ARB, OP, ZK, POL, STRK, MNT

- AI: FET, NEAR, RENDER, TAO

- Memecoins: PEPE, BONK, SHIB, DOGE, WIFU, POPCAT

PERFORMANCE TRACKING

The indicator implements a rolling window approach for performance calculations.

Starting from 0% at the beginning of each period, it tracks relative performance with positive values indicating outperformance and negative values showing underperformance.

Multiple timeframe options (1W, 1M, 3M, 6M, and 1Y) allow for both short-term and long-term analysis.

APPLICATIONS

This tool proves invaluable for:

- Sector rotation analysis

- Identifying trending sectors

- Comparing relative strength

- Gauging market sentiment

- Understanding market structure through sector performance

Thanks for reading and for the support

Daveatt

Stablecoin Delta [SAKANE]Overview

Stablecoin Delta is an indicator designed to provide a detailed analysis of the market trends of major stablecoins (USDT and USDC). Stablecoins play a crucial role in supporting the liquidity of the cryptocurrency market, and fluctuations in their supply significantly impact the prices of Bitcoin and other cryptocurrencies.

This indicator leverages data from CryptoCap to visualize the daily changes in the market capitalization of stablecoins. Traders can use this tool to understand the effects of stablecoin supply fluctuations on the market in a timely manner, enabling more strategic investment decisions.

The key benefits include the ability to quickly monitor stablecoin supply changes, utilize this data as a supplementary tool for predicting Bitcoin price movements, and identify both short-term market movements and long-term trends. This indicator is valuable for traders of all levels, from beginners to seasoned professionals.

Features

- Support for USDT and USDC Market Cap

Monitor the market trends of these two major stablecoins using data from CryptoCap. Users can also choose to analyze only one of them.

- Daily Net Change Calculation

Calculates the daily change in market capitalization compared to the previous day, providing a clear view of trends.

- Flexible Smoothing Options

Apply either SMA or EMA smoothing for both the histogram and the line chart, based on user preference.

- Customizable Colors

Customize the colors for the histogram (positive/negative) and line chart for better visualization.

Visualization

- Histogram

Displays daily net changes as a histogram, with positive changes (green) and negative changes (red) clearly differentiated.

- Smoothed Line Chart

Provides a smoothed line chart to make trend identification easier.

Use Cases

- In-depth Analysis of the Cryptocurrency Market

The supply of stablecoins is a critical factor influencing the price of Bitcoin and other cryptocurrencies. This indicator helps traders understand overall market liquidity, enabling more effective investment decisions.

- Short-Term and Long-Term Strategy Development

Trends derived from stablecoin supply fluctuations are essential for traders to gauge short-term price movements and long-term market flows.

- Real-Time Market Adjustment

In times of sudden market shifts, this tool enables traders to quickly assess changes in stablecoin supply and adjust their positions accordingly.

Future Plans

- Additional stablecoins will be considered for inclusion if their market share grows significantly.

Disclaimer

- This indicator relies on data from CryptoCap. The results are subject to the accuracy and timeliness of the data and should be used as reference information only.

Combined Zero Lag EMA with Crosses | ASHGCombined Zero Lag EMA with Crosses

This indicator combines the power of Zero Lag Exponential Moving Averages (EMAs) with the widely used Golden Cross and Death Cross signals. It provides an efficient and precise trend-following tool for traders.

Key Features:

Short and Long Zero Lag EMAs: The indicator uses two Zero Lag EMAs with customizable periods (Short and Long). The short EMA is typically more responsive to price changes, while the long EMA smooths out price data, providing a broader trend perspective.

Golden Cross and Death Cross signals: The Golden Cross occurs when the short EMA crosses above the long EMA, indicating a potential bullish trend. The Death Cross occurs when the short EMA crosses below the long EMA, signaling a possible bearish trend.

Combined Zero Lag EMA: The average of the Short and Long Zero Lag EMAs gives a balanced view of the market's overall direction.

Plotting and Alerts: The indicator plots both the short and long Zero Lag EMAs, as well as the combined EMA, with visual cues for Golden and Death Crosses. Alerts can be set for when these crosses occur.

Use this indicator for clearer entry and exit points, helping you stay ahead of market movements.

This indicator is based on Kıvanç ÖZBİLGİÇ's "Zero Lag EMA v2" indicator.

tr.tradingview.com

Birleştirilmiş Zero Lag EMA ve Cross (Kesişim) Sinyalleri

Bu gösterge, Zero Lag (Sıfır Gecikmeli) Üssel Hareketli Ortalamaların (EMA) gücünü, yaygın olarak kullanılan Golden Cross (Altın Kesişim) ve Death Cross (Ölüm Kesişimi) sinyalleriyle birleştirir. Yatırımcılar için verimli ve hassas bir trend takip aracıdır.

Öne Çıkan Özellikler:

Kısa ve Uzun Zero Lag EMA: Gösterge, özelleştirilebilir periyotlarla iki Zero Lag EMA kullanır (Kısa ve Uzun). Kısa EMA, fiyat değişimlerine daha hızlı tepki verirken, uzun EMA fiyat verilerini düzleştirerek daha geniş bir trend perspektifi sunar.

Golden Cross ve Death Cross sinyalleri: Golden Cross, kısa EMA'nın uzun EMA'yı yukarı doğru kesmesiyle oluşur ve potansiyel bir yükseliş trendine işaret eder. Death Cross ise, kısa EMA'nın uzun EMA'yı aşağı doğru kesmesiyle oluşur ve düşüş trendi sinyali verir.

Birleştirilmiş Zero Lag EMA: Kısa ve uzun Zero Lag EMA'larının ortalaması, piyasanın genel yönünü dengeli bir şekilde gösterir.

Grafik ve Uyarılar: Gösterge, kısa ve uzun Zero Lag EMA'ları ile birleştirilmiş EMA'yı çizerek Golden Cross ve Death Cross sinyalleri için görsel uyarılar sağlar. Bu kesişimler gerçekleştiğinde alarm kurabilirsiniz.

Bu göstergeleri kullanarak, piyasa hareketlerinden önce net giriş ve çıkış noktaları belirleyebilir, böylece daha bilinçli kararlar alabilirsiniz.

Bu indikatör Kıvanç ÖZBİLGİÇ'in "Zero Lag EMA v2" indikatörünü temel alarak hazırlanmıştır.

tr.tradingview.com

FuTech : Earnings (All 269 Fundamental Metrics of Tradingview)FuTech : Earnings Indicator

The FuTech : Earnings Indicator is a revolutionary tool, offering the most comprehensive integration of all 269 fundamental financial metrics available from the TradingView platform.

This groundbreaking indicator is designed to empower financial researchers, traders, investors, and analysts with an unmatched depth of data, enabling superior analysis and decision-making.

Overview

"FuTech : Earnings Indicator" is the first-ever indicator to provide a holistic comparison of fundamental financial metrics for any stock, covering quarterly, yearly, and trailing twelve months (TTM) periods.

This tool brings together key financial data from income statements, balance sheets, cash flows, and other critical metrics found in company annual reports.

It also incorporates additional unique features like per-employee data, R&D expenses, and capital expenditures (CapEx), which are typically hidden within dense financial statements of Annual Reports.

---

Key Features and Capabilities

1. Comprehensive Financial Metrics

- "FuTech : Earnings Indicator" offers access to all 269 fundamental metrics available on TradingView platform. This includes widely used data such as revenue, profit margins, and EPS, alongside more niche metrics like R&D expenditure, employee efficiency, and financial scores developed by renowned analysts.

- Users can explore income statement data (e.g., net income, gross profit), balance sheet items (e.g., total assets, liabilities), cash flow metrics, and other financial statistics such as Altman Score, per employee expenses etc. in unparalleled detail.

2. Comparison Across Time Periods

- "FuTech : Earnings Indicator" allows users to analyze data for:

- Quarterly periods (e.g., Q1, Q2, Q3, Q4).

- Yearly comparisons for a broad historical view.

- TTM analysis to observe the most recent trends and developments.

- Users can select a minimum of 4 periods up to an unlimited range for detailed comparisons in both quarter.

3. Dynamic Data Display

- Users can select up to 5 key metrics alongside the stock price column to focus their analysis on the most relevant data points.

- Highlighting with green and red symbols offers an intuitive and visual representation:

- Green : Positive trends or improvements.

- Red : Negative trends or deteriorations.

4. Automated Averages

- "FuTech : Earnings Indicator" automatically calculates averages of selected metrics across the chosen periods. This feature helps users quickly identify performance trends and smooth out anomalies, enabling faster and more reliable research.

5. Designed for Research Excellence

- FuTech serves a wide audience, including:

- Corporate finance professionals who need a deep dive into financial metrics.

- Individual investors seeking robust tools for investment analysis.

- Broking companies and equity research analysts performing stock analysis.

- Traders looking to incorporate fundamental metrics into their strategies.

- Technical analysts seeking a better understanding of price behavior in relation to fundamentals.

- Fundamental research aspirants who want an edge in their learning process.

6. Unmatched Detail for Deeper Insights

- By pulling all 269 Financial metrics from the TradingView, "FuTech : Earnings Indicator" enables:

- Cross-comparison of a stock’s performance with its historical benchmarks.

- Evaluation of rare data like R&D expenses, CapEx trends, and employee efficiency ratios for enhanced investment insights.

- This ensures users can study stocks in greater depth than ever before.

7. Enhanced Usability

- Simple to use and visually appealing, "FuTech : Earnings Indicator" is designed with researchers in mind.

- Its intuitive interface ensures even novice users can navigate the wealth of data without feeling overwhelmed.

Applications of FuTech : Earnings Indicator

FuTech : Earnings Indicator is incredibly versatile and has applications in diverse fields of financial research and trading:

1. Corporate Finance

- Professionals in corporate finance can leverage "FuTech : Earnings Indicator" to benchmark company performance, study efficiency ratios, and evaluate financial health across various metrics.

2. Investors and Traders

- Long-term investors can use the tool to study the fundamental strengths of a stock before making buy-and-hold decisions.

- Traders can incorporate "FuTech : Earnings Indicator" into their analysis to align comprehensive fundamental trends with their targeted technical signals.

3. Equity Research Analysts

- Analysts can streamline their workflows by quickly identifying trends, outliers, and averages across large datasets.

4. Education and Research

- "FuTech : Earnings Indicator" is ideal for students and aspiring financial analysts who want a practical tool for understanding real-world data.

How FuTech : Earnings Indicator Stands Out

1. First-Ever Integration of All Financial Metrics

- It's an exclusive tool which offers the ability to explore all 269 financial metrics available on TradingView for a single stock research in-depth for quarters, years or TTM periods.

2. Period Customization

- Users have complete flexibility to select and analyze data across any range of time periods, allowing for customized insights tailored to specific research goals.

3. Data Visualization

- The intuitive use of color-coded symbols (green for positive trends, red for negative) makes complex data easy to interpret at a glance.

4. Actionable Insights

- The automated average calculations provide actionable insights for making informed decisions without manual computations.

5. Unique Metrics

- Metrics such as research and development costs, CapEx, and per-employee efficiency data offer unique angles that aren’t typically available in traditional analysis tools.

Why to Use FuTech : Earnings Indicator ?

1. Boost Your Research Power

- With FuTech, you can unlock a world of data that gives you the edge in analyzing stocks. Whether you’re a seasoned analyst or a beginner, this tool offers something for everyone.

2. Save Time and Effort

- The automated features and intuitive interface eliminate the need for time-consuming manual calculations and formatting.

3. Make Better Decisions

- "FuTech : Earnings Indicator's" detailed comparison capabilities and insightful visual aids allow for more accurate assessments of a stock’s performance and potential.

4. Broad Appeal

- From individual investors to financial institutions, FuTech is a valuable tool for anyone in the world of finance.

---

Conclusion

- The FuTech : Earnings Indicator is a must-have for anyone serious about financial analysis.

- It combines the depth of all 269 fundamental metrics with intuitive tools for comparison, visualization, and calculation.

- Designed for ease of use and powerful insights, FuTech : Earnings Indicator is set to transform the way financial data is analyzed and understood.

Thank you !

Jai Swaminarayan Dasna Das !

He Hari ! Bas Ek Tu Raji Tha !

Bitcoin Events HistoryWith this tool, you can travel back to Bitcoin’s very first price quote and retrace its entire history directly on your chart. Major events are plotted as labels or markers, providing context for how significant moments shaped Bitcoin’s journey.

Key Features

Comprehensive Event Coverage: From Bitcoin’s inception to the most recent updates.

Custom View: Change label colors, styles, sizes, and fonts using the script’s settings.

Regular Updates: New events are added regularly to keep the history current.

Replay History

Use Bar Replay Mode to step through Bitcoin’s price history and see events unfold in sequence.

Follow the on-screen instructions for a more immersive experience.

Community Contributions

If you notice a significant event missing or misplaced on a particular date, feel free to leave a comment! Your suggestions will be considered for the next update.

To all Bitcoin enthusiasts, traders, and anyone eager to explore the history of cryptocurrency from its inception, I hope you enjoy this indicator :)

Global Market Strength IndicatorThe Global Market Strength Indicator is a powerful tool for traders and investors. It helps compare the strength of various global markets and indices. This indicator uses the True Strength Index (TSI) to measure market strength.

The indicator retrieves price data for different markets and calculates their TSI values. These values are then plotted on a chart. Each market is represented by a different colored line, making it easy to distinguish between them.

One of the main benefits of this indicator is its comprehensive global view. It covers major indices and country-specific ETFs, giving users a broad perspective on global market trends. This wide coverage allows for easy comparison between different markets and regions.

The indicator is highly customizable. Users can adjust the TSI smoothing period to suit their preferences. They can also toggle the visibility of individual markets. This feature helps reduce chart clutter and allows for more focused analysis.

To use the indicator, apply it to your chart in TradingView. Adjust the settings as needed, and observe the relative positions and movements of the TSI lines. Lines moving higher indicate increasing strength in that market, while lines moving lower suggest weakening markets.

The chart includes reference lines at 0.5 and -0.5. These help identify potential overbought and oversold conditions. Markets with TSI values above 0.5 may be considered strong or potentially overbought. Those below -0.5 may be weak or potentially oversold.

By comparing the movements of different markets, users can identify which markets are leading or lagging. They can also spot potential divergences between related markets. This information can be valuable for identifying sector rotations or shifts in global market sentiment.

A dynamic legend automatically updates to show only the visible markets. This feature improves chart readability and makes it easier to interpret the data.

The Global Market Strength Indicator is a versatile tool that provides valuable insights into global market performance. It helps traders and investors identify trends, compare market performances, and make more informed decisions. Whether you're looking to spot emerging global trends or identify potential trading opportunities, this indicator offers a comprehensive solution for global market analysis.

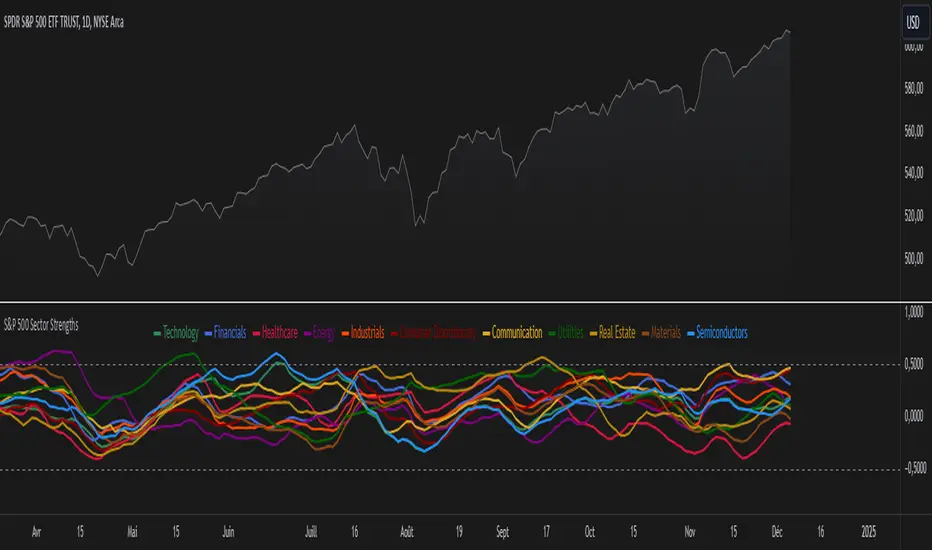

S&P 500 Sector StrengthsThe "S&P 500 Sector Strengths" indicator is a sophisticated tool designed to provide traders and investors with a comprehensive view of the relative performance of various sectors within the S&P 500 index. This indicator utilizes the True Strength Index (TSI) to measure and compare the strength of different sectors, offering valuable insights into market trends and sector rotations.

At its core, the indicator calculates the TSI for each sector using price data obtained through the request.security() function. The TSI, a momentum oscillator, is computed using a user-defined smoothing period, allowing for customization based on individual preferences and trading styles. The resulting TSI values for each sector are then plotted on the chart, creating a visual representation of sector strengths.

To use this indicator effectively, traders should focus on comparing the movements of different sector lines. Sectors with lines moving higher are showing increasing strength, while those with descending lines are exhibiting weakness. This comparative analysis can help identify potential investment opportunities and sector rotations. Additionally, when multiple sector lines move in tandem, it may signal a broader market trend.

The indicator includes dashed lines at 0.5 and -0.5, serving as reference points for overbought and oversold conditions. Sectors with TSI values above 0.5 might be considered overbought, suggesting caution, while those below -0.5 could be viewed as oversold, potentially indicating buying opportunities.

One of the key advantages of this indicator is its flexibility. Users can toggle the visibility of individual sectors and customize their colors, allowing for a tailored analysis experience. This feature is particularly useful when focusing on specific sectors or reducing chart clutter for clearer visualization.

The indicator's ability to provide a comprehensive overview of all major S&P 500 sectors in a single chart is a significant benefit. This consolidated view enables quick comparisons and helps in identifying relative strengths and weaknesses across sectors. Such insights can be invaluable for portfolio allocation decisions and in spotting emerging market trends.

Moreover, the dynamic legend feature enhances the indicator's usability. It automatically updates to display only the visible sectors, improving chart readability and interpretation.

By leveraging this indicator, market participants can gain a deeper understanding of sector dynamics within the S&P 500. This enhanced perspective can lead to more informed decision-making in sector allocation strategies and individual stock selection. The indicator's ability to potentially detect early trends by comparing sector strengths adds another layer of value, allowing users to position themselves ahead of broader market movements.

In conclusion, the "S&P 500 Sector Strengths" indicator is a powerful tool that combines technical analysis with sector comparison. Its user-friendly interface, customizable features, and comprehensive sector coverage make it an valuable asset for traders and investors seeking to navigate the complexities of the S&P 500 market with greater confidence and insight.

BTC Price Percentage Difference( Bitfinex - Coinbase)Introduction:

The BTC Price Percentage Difference Histogram Indicator is a powerful tool designed to help traders visualize and capitalize on the price discrepancies of Bitcoin (BTC) between two major exchanges: Bitfinex and Coinbase. By calculating the real-time percentage difference of BTC-USD prices and displaying it as a color-coded histogram, this indicator enables you to quickly spot potential arbitrage opportunities and gain deeper insights into market dynamics.

Features:

• Real-Time Percentage Difference Calculation:

• Computes the percentage difference between BTC-USD prices on Bitfinex and Coinbase.

• Color-Coded Histogram Visualization:

• Green Bars: Indicate that the BTC price on Bitfinex is higher than on Coinbase.

• Red Bars: Indicate that the BTC price on Bitfinex is lower than on Coinbase.

• User-Friendly and Intuitive:

• Simple setup with no additional inputs required.

• Automatically adapts to the chart’s timeframe for seamless integration.

Why Bitfinex Whales Matter:

Bitfinex is renowned for hosting some of the largest Bitcoin traders, often referred to as “whales.” These influential players have the capacity to move the market, and historically, they’ve demonstrated a high success rate in buying at market bottoms and selling at market tops. By tracking the price discrepancies between Bitfinex and other exchanges like Coinbase, you can gain valuable insights into the sentiment and actions of these key market participants.

Correlation Coefficient [Giang]### **Introduction to the "Correlation Coefficient" Indicator**

#### **Idea behind the Indicator**

The "Correlation Coefficient" indicator was developed to analyze the linear relationship between Bitcoin (**BTCUSD**) and other important economic indices or financial assets, such as:

- **SPX** (S&P 500 Index): Represents the U.S. stock market.

- **DXY** (Dollar Index): Reflects the strength of the USD against major currencies.

- **SPY** (ETF representing the S&P 500): A popular trading instrument.

- **GOLD** (Gold price): A traditional safe-haven asset.

The correlation between these assets can help traders understand how Bitcoin reacts to market movements of traditional financial instruments, providing opportunities for more effective trading decisions.

Additionally, the indicator allows users to **customize asset symbols for comparison**, not limited to the default indices (SPX, DXY, SPY, GOLD). This flexibility enables traders to tailor their analysis to specific goals and portfolios.

---

#### **Significance and Use of Correlation in Trading**

**Correlation** is a measure of the linear relationship between two data series. In the context of this indicator:

- **The correlation coefficient ranges from -1 to 1**:

- **1**: Perfect positive relationship (both increase or decrease together).

- **0**: No linear relationship.

- **-1**: Perfect negative relationship (one increases while the other decreases).

- **Use in trading**:

- Identify **strong relationships or unusual divergences** between Bitcoin and other assets.

- Help determine **market sentiment**: For example, if Bitcoin has a negative correlation with DXY, traders might expect Bitcoin to rise when the USD weakens.

- Provide a foundation for hedging strategies or investments based on inter-asset relationships.

---

#### **Components of the Indicator**

The "Correlation Coefficient" indicator consists of the following key components:

1. **Main Data (BTCUSD)**:

- The closing price of Bitcoin is used as the central asset for calculations.

2. **Comparison Data**:

- Users can select different asset symbols for comparison. By default, the indicator supports:

- **SPX**: Stock market index.

- **DXY**: Dollar Index.

- **SPY**: Popular ETF.

- **GOLD**: Gold price.

3. **Correlation Coefficients**:

- Calculated between BTC and each comparison index, based on a Weighted Moving Average (WMA) over a user-defined period.

4. **Graphical Representation**:

- Displays individual correlation coefficients with each comparison index, making it easier for traders to track and analyze.

---

#### **How to Analyze and Use the Indicator**

**1. Identify Key Correlations:**

- Observe the correlation lines between BTC and the indices to determine positive or negative relationships.

- Example:

- If the **Correlation Coefficient (BTC-DXY)** sharply declines to -1, this indicates that when USD strengthens, Bitcoin tends to weaken.

**2. Analyze the Strength of Correlations:**

- **Strong Correlations**: If the coefficient is close to 1 or -1, the relationship between the two assets is very clear.

- **Weak Correlations**: If the coefficient is near 0, Bitcoin may be influenced by other factors outside the compared index.

**3. Develop Trading Strategies:**

- Use correlations to predict Bitcoin's price movements:

- If BTC has an inverse relationship with **DXY**, traders might consider selling BTC when the USD strengthens.

- If BTC and **SPX** are strongly correlated, traders can monitor the stock market to predict Bitcoin's trend.

**4. Evaluate Changes Over Time:**

- Use different timeframes (daily, weekly) to track the correlation's fluctuations.

- Look for unusual signals, such as a breakdown or shift from positive to negative relationships.

---

#### **Conclusion**

The "Correlation Coefficient" indicator is a powerful tool that helps traders analyze the relationship between Bitcoin and major financial indices. The ability to customize asset symbols for comparison makes the indicator flexible and suitable for various trading strategies. When used correctly, this indicator not only provides insights into market sentiment but also supports the development of intelligent trading strategies and optimized profits.

Coinbase Premium HeatmapCoinbase Premium Heatmap visualizes spot bitcoin premium (or discount) on Coinbase, relative to other spot markets, visualized as a heatmap overlay.

OPTIMIZED FOR CLARITY

Coinbase Premium can whipsaw quickly, with dramatic state changes over relatively brief periods, unnecessarily complicating its use (for our purposes).

To mitigate whipsaws, the script (a) averages premium/discount on an hourly basis, and (b) introduces lightweight exponential smoothing, to further simplify/clarify state.

WHY IT MATTERS

Spot Coinbase premium is a strong proxy for bullish institutional sentiment and net inflows/accumulation by western financial institutions, ETF providers, and corporations (like MicroStrategy) adding bitcoin to their treasury.

In aggregate, this holder cohort drives trend & sentiment more than any other, so it's important to know their directional bias.

HOW IT'S CALCULATED

Premium / discount calculates the spread between Coinbase spot BTC price, and spot price on Binance + Bybit. Calculation is averaged hourly, with light exponential smoothing.

HOW WE USE THE SCRIPT

When assessing optimal moments to hedge exposure (or sell spot assets) near a presumed impending cycle top, awareness of institutional sentiment is a crucial variable. This script:

(a) Filters out unnecessarily early cycle exit signals (if Coinbase premium is still present)

(b) Confirms other metrics that indicate an impending cycle top (if the neutral to bearish institutional sentiment we'd expect to see is in effect), and

(c) Visualizes state changes (from bearish to bullish & vice versa), that often make for good swing entries & exits on lower timeframes.

Daily Directional Bias Indicator (S&P 500)This indicator is designed to help you be on the right side of the trade.

Most traders who struggle to know which way price may move are only looking at part of the picture. This Directional Bias Indicator uses both the Accumulation/Distribution Line and VIX for directional confirmation.

The Accumulation/Distribution Line

The Accumulation/Distribution (ACC) line helps us gauge market momentum by showing the cumulative flow of money into or out of an asset. When the ACC line is rising, it suggests that buying pressure is dominating, indicating a bullish market. Conversely, when the ACC line is falling, it suggests that selling pressure is stronger, indicating a bearish market. By comparing the ACC line with the VWAP, traders can see if the price is moving in line with the overall market sentiment. If the ACC line is above the VWAP, it suggests the market is in a bullish phase; if it's below, it indicates a bearish phase.

The VIX

The VIX (Volatility Index) is often referred to as the "fear gauge" of the market. When the VIX is rising, it typically signals increased market fear and higher volatility, which can be a sign of bearish market conditions. Conversely, when the VIX is falling, it suggests lower volatility and a more stable, bullish market. Using the VIX with the VWAP helps us confirm market direction, particularly in relation to the S&P 500.

VWAP

For both the ACC Line and VIX, we use a VWAP line to gauge whether the ACC line or the VIX is above or below the average. When the ACC line is above the VWAP, we view it as a sign that price will go up. However, because the VIX has an inverse relationship, when the VIX falls below the VWAP, we take that as a sign to go long.

How to use

The yellow line represents the ACC Line.

The red line represents the VWAP based on the ACC line.

The triangles at the bottom simply show when the ACC line is above or below the VWAP.

The triangles at the top show whether the VIX is bullish or bearish.

If both triangles (top or bottom) are bullish, this confirms that the price of an asset like the S&P 500 will likely go up. If both triangles are pointing down, it suggests that price will fall.

As always, test for yourself.

Happy trading!

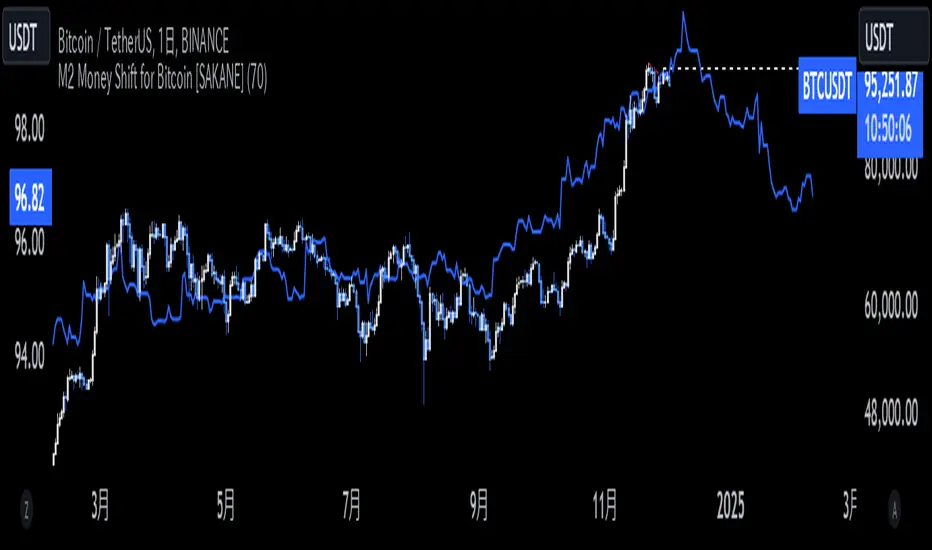

M2 Money Shift for Bitcoin [SAKANE]M2 Money Shift for Bitcoin was developed to visualize the impact of M2 Money, a macroeconomic indicator, on the Bitcoin market and to support trade analysis.

Bitcoin price fluctuations have a certain correlation with cycles in M2 money supply.In particular, it has been noted that changes in M2 supply can affect the bitcoin price 70 days in advance.Very high correlations have been observed in recent years in particular, making it useful as a supplemental analytical tool for trading.

Support for M2 data from multiple countries

M2 supply data from the U.S., Europe, China, Japan, the U.K., Canada, Australia, and India are integrated and all are displayed in U.S. dollar equivalents.

Slide function

Using the "Slide Days Forward" setting, M2 data can be slid up to 500 days, allowing for flexible analysis that takes into account the time difference from the bitcoin price.

Plotting Total Liquidity

Plot total liquidity (in trillions of dollars) by summing the M2 supply of multiple countries.

How to use

After applying the indicator to the chart, activate the M2 data for the required country from the settings screen. 2.

2. adjust "Slide Days Forward" to analyze the relationship between changes in M2 supply and bitcoin price

3. refer to the Gross Liquidity plot to build a trading strategy that takes into account macroeconomic influences.

Notes.

This indicator is an auxiliary tool for trade analysis and does not guarantee future price trends.

The relationship between M2 supply and bitcoin price depends on many factors and should be used in conjunction with other analysis methods.

LRSI-TTM Squeeze - AynetThis Pine Script code creates an indicator called LRSI-TTM Squeeze , which combines two key concepts to analyze momentum, squeeze conditions, and price movements in the market:

Laguerre RSI (LaRSI): A modified version of RSI used to identify trend reversals in price movements.

TTM Squeeze: Identifies market compressions (low volatility) and potential breakouts from these squeezes.

Functionality and Workflow of the Code

1. Laguerre RSI (LaRSI)

Purpose:

Provides a smoother and less noisy version of RSI to track price movements.

Calculation:

The script uses a filtering coefficient (alpha) to process price data through four levels (L0, L1, L2, L3).

Movement differences between these levels calculate buying pressure (cu) and selling pressure (cd).

The ratio of these pressures forms the Laguerre RSI:

bash

Kodu kopyala

LaRSI = cu / (cu + cd)

The LaRSI value indicates:

Below 20: Oversold condition (potential buy signal).

Above 80: Overbought condition (potential sell signal).

2. TTM Squeeze

Purpose:

Analyzes the relationship between Bollinger Bands (BB) and Keltner Channels (KC) to determine whether the market is compressed (low volatility) or expanded (high volatility).

Calculation:

Bollinger Bands:

Calculated based on the moving average (SMA) of the price, with an upper and lower band.

Keltner Channels:

Created using the Average True Range (ATR) to calculate an upper and lower band.

Squeeze States:

Squeeze On: BB is within KC.

Squeeze Off: BB is outside KC.

Other States (No Squeeze): Neither of the above applies.

3. Momentum Calculation

Momentum is computed using the linear regression of the difference between the price and its SMA. This helps anticipate the direction and strength of price movements when the squeeze ends.

Visuals on the Chart

Laguerre RSI Line:

An RSI indicator scaled to 0-100 is plotted.

The line's color changes based on its movement:

Green line: RSI is rising.

Red line: RSI is falling.

Key levels:

20 level: Oversold condition (buy signal can be triggered).

80 level: Overbought condition (sell signal can be triggered).

Momentum Histogram:

Displays momentum as histogram bars with colors based on its direction and strength:

Lime (light green): Positive momentum increasing.

Green: Positive momentum decreasing.

Red: Negative momentum decreasing.

Maroon (dark red): Negative momentum increasing.

Squeeze Status Indicator:

A marker is plotted on the zero line to indicate the squeeze state:

Yellow: Squeeze On (compression active).

Blue: Squeeze Off (compression ended, movement expected).

Gray: No Squeeze.

Information Table

A table is displayed in the top-right corner of the chart, showing closing prices for different timeframes (e.g., 1 minute, 5 minutes, 1 hour, etc.). Each timeframe is color-coded.

Alerts

LaRSI Alerts:

Crosses above 20: Exiting oversold condition (buy signal).

Crosses below 80: Exiting overbought condition (sell signal).

Squeeze Alerts:

When the squeeze ends: Indicates a potential price move.

When the squeeze starts: Indicates volatility is decreasing.

Summary

This indicator is a powerful tool for determining market trends, momentum, and squeeze conditions. It helps users identify periods when the market is likely to move or remain stagnant, providing alerts based on these analyses to support trading strategies.

Automatic Fibonacci Levels with EMAAutomatic Fibonacci Levels with EMA

Description:

This script automatically calculates and displays Fibonacci retracement levels based on the highest and lowest prices over a dynamic lookback period. The Fibonacci levels are recalculated on every bar to adapt to price changes, providing an ongoing analysis of key support and resistance areas.

The Fibonacci levels are dynamically colored to reflect the trend direction, determined by the position of the price relative to the Exponential Moving Average (EMA). When the market is in an uptrend (price above EMA), Fibonacci levels are displayed in green, and in a downtrend (price below EMA), they are shown in red. This color coding helps traders quickly identify the current market direction.

Key Features:

Dynamic Fibonacci Levels: Automatically adjusts Fibonacci retracement levels based on recent price action, recalculated with each new bar.

EMA Trend Confirmation: The trend is confirmed by the position of the price relative to the 20-period EMA. Fibonacci levels are color-coded to reflect this trend.

Customizable Lookback Period: Adjust the base lookback period (default 50) and scale it according to your preferred timeframe for more or less sensitivity to recent price action.

Flexible Fibonacci Duration: The Fibonacci levels remain on the chart for a customizable duration (default 2 bars), allowing for visual clarity while adapting to new price action.

Timeframe Scaling: The script automatically adjusts the lookback period based on a scaling factor, making it suitable for different timeframes.

How to Use:

Use the Fibonacci levels to identify potential support and resistance zones based on the market's current price range.

Combine the trend color coding with your own strategy to enhance decision-making, whether for long or short entries.

Adjust the Lookback Period and Fibonacci Duration based on your trading style and timeframe preferences.

This script provides an automatic and customizable way to visualize Fibonacci retracements in a dynamic manner, helping traders make informed decisions based on trend direction and key price levels.

Note: As with any trading tool, always use proper risk management and test the script before using it in live trading.

4-Frame Trend CountThis script tracks the current close vs the close from 4 time frames prior to spot a trend reversal after 9 consecutive up or down moves.

Quantum Transform - AynetQuantum Transform Trading Indicator: Explanation

This script is called a "Quantum Transform Trading Indicator" and aims to enhance market analysis by applying complex mathematical models. Written in Pine Script, the indicator includes the following elements:

1. General Structure

Quantum Parameters: Inspired by physical and mathematical concepts (Planck constant ℏ, wave function Ψ, time τ, etc.), it uses specific parameters.

Transformation Functions: Applies various mathematical operations to transform price data in different ways.

Signal Generation: Produces signals for long and short positions.

Visualization: Displays different price transformations and signals on the chart.

2. Core Parameters

The parameters allow users to control various transformations:

Planck Constant (ℏ): A scaling factor for wave modulation.

Wave (Ψ): Controls oscillation in price data.

Time (τ): The length of the lookback period for calculations.

Relativity (γ): Power factor in the Lorentz transformation.

Phase Shift (β): Manages phase shift in transformations.

Frequency (ω): Represents the frequency of price movements.

Dimensions (∇): Enables multi-dimensional field analysis.

3. Functions

a) Relativistic Transform

Inspired by the theory of relativity.

Calculates the Lorentz factor using the rate of price change.

Transforms price data to amplify the relativity effect.

b) Phase Transform

Calculates the phase of price data and applies wave modulation.

Creates phase and amplitude modulation based on the bar index.

c) Resonance Transform

Calculates resonance effects using natural frequency and oscillations.

Highlights periodic behaviors of price movements.

d) Field Transform

Applies multi-dimensional field calculations.

Combines strength, wave, and coherence aspects of price data.

e) Chaos Transform

Implements a chaos effect based on sensitivity analysis.

Simulates chaotic behaviors of price movements.

4. Main Calculations

Quantum Price: The average of all transformation functions.

Bands:

Upper Band: The highest level of quantum price.

Lower Band: The lowest level of quantum price.

Mid Band: The average of upper and lower bands.

Momentum: Calculates the rate of change in quantum price.

5. Signal Generation

Long Signal:

Triggered when the phase price crosses above the field price.

Momentum must be positive, and the price above the mid-band.

Short Signal:

Triggered when the phase price crosses below the field price.

Momentum must be negative, and the price below the mid-band.

Signal strength is calculated relative to the momentum moving average.

6. Visualization

Each transformation is displayed in a unique color.

Bands and Momentum: Visualize price behavior.

Signal Icons: Show buy/sell signals using up/down arrows on the chart.

7. Information Panel

A table in the top-right corner of the chart displays:

The current values of each transformation.

Signal strength (as a percentage).

The type of signal (⬆: Long, ⬇: Short).

Applications

Trend Following: Analyze trends with complex transformations.

Resonance and Chaos Analysis: Understand dynamic behaviors of price.

Signal Strategies: Create strong and reliable buy/sell signals.

If you have any additional questions or customization requests regarding this indicator, feel free to ask!

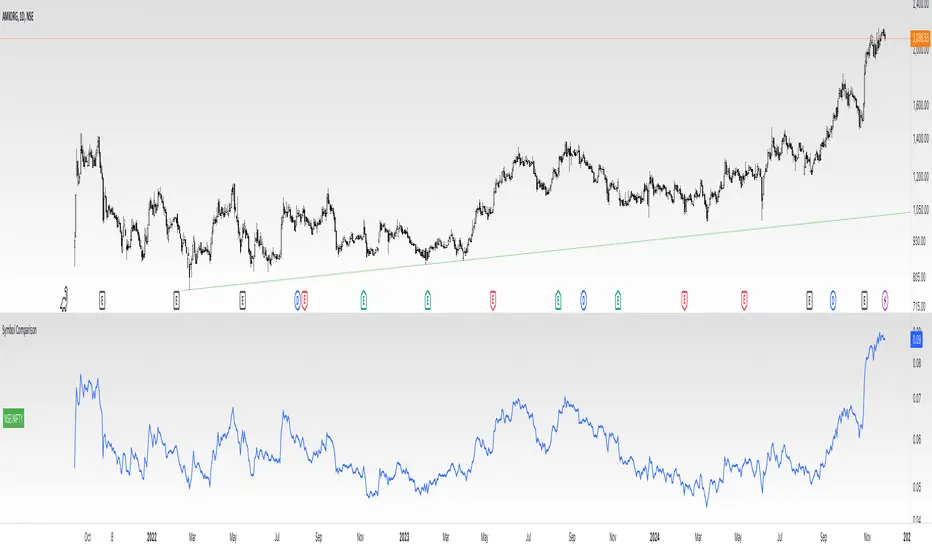

Divides company with IndexOverview:

This indicator simplifies the comparison of a stock's performance against a specified index, such as the Nifty 50. By calculating and plotting the ratio between the two, it provides a clear visual representation of relative strength.

Key Features:

-Direct Comparison: Easily compare any stock against a selected index.

-Customizable Index: Choose from a dropdown menu or input a custom index symbol.

-Visual Clarity: Maximizing the chart provides a clear view of the relative performance.

-SMA Overlay: Add a Simple Moving Average (SMA) to identify trends and potential entry/exit

points.

-Customizable Appearance: Adjust background color, text color, and label size for personalized

visualization.

How to Use:

Add the Indicator: Add the indicator to your chart.

Select the Index: Choose the desired index from the dropdown menu or input a custom symbol.

Analyze the Ratio:

-A rising ratio indicates the stock is outperforming the index.

-A falling ratio suggests underperformance.

-The SMA can help identify potential trends and momentum.

Customize the Appearance: Adjust the background color, text color, and label size to suit your preferences.

Benefits:

-Improved Decision Making: Gain insights into a stock's relative strength.

-Faster Analysis: Quickly compare multiple stocks against a benchmark index.

-Enhanced Visualization: Customize the chart for better understanding.

-By leveraging this indicator, you can make informed trading decisions and gain a deeper

understanding of market dynamics.

Crypto Value RainbowThe best way to value Crypto value is comparing Crypto price against the available money supply circulating in the economy. There are 3 different 4 different type of money supply M0/M1/M2/M3 which denotes the level of money printed by central government to the final credit lend out to the economy via fractional banking system. This rainbow valuation measures the relative Crypto price against the M0/M1/M2/M3 from most popular currency that account for more than 75% of money supply in the world.

CV = US MS + EU MS + CN MS + JP MS + UK MS

CV = Crypto Value

MS = Money Supply

This can only be applied to a few crypto currency:

- BTCUSD Bitcoin

- ETHUSD Ehereum

- BNBUSD BNB

- SOLUSD Solana

- XRPUSD XRP

- TONUSD Toncoin

- DOGEUSD Dogecoin

- TRXUSD Tron

- ADAUSD Cardano

- AVAXUSD Avalanche

The rainbow color is the multiplier for the total Crypto Value by 1x,2x,3x,...,10x

Sri Yantra MTF - AynetSri Yantra MTF - Aynet Script Overview

This Pine Script generates a Sri Yantra-inspired geometric pattern overlay on price charts. The pattern is dynamically updated based on multi-timeframe (MTF) inputs, utilizing high and low price ranges, and adjusting its size relative to a chosen multiplier.

The Sri Yantra is a sacred geometric figure used in various spiritual and mathematical contexts, symbolizing the interconnectedness of the universe. Here, it is applied to visualize structured price levels.

Scientific and Technical Explanation

Multi-Timeframe Integration:

Base Timeframe (baseRes): This is the primary timeframe for the analysis. The opening price and ATR (Average True Range) are calculated from this timeframe.

Pattern Timeframe (patternRes): Defines the granularity of the pattern. It ensures synchronization with price movements on specific time intervals.

Geometric Construction:

ATR-Based Scaling: The script uses ATR as a volatility measure to dynamically size the geometric pattern. The sizeMult input scales the pattern relative to price volatility.

Pattern Width (barOffset): Defines the horizontal extent of the pattern in terms of bars. This ensures the pattern is aligned with price movements and scales appropriately.

Sri Yantra-Like Geometry:

Outer Square: A bounding box is drawn around the price level.

Triangles: Multiple layers of triangles (primary, secondary, and tertiary) are calculated and drawn to mimic the structure of the Sri Yantra. These triangles converge and diverge based on price levels.

Horizontal Lines: Added at key levels to provide additional structure and aesthetic alignment.

Dynamic Updates:

The pattern recalculates and redraws itself on the last bar of the selected timeframe, ensuring it adapts to real-time price data.

A built-in check identifies new bars in the chosen timeframe (patternRes), ensuring accurate updates.

Information Table:

Displays the selected base and pattern timeframes in a table format on the top-right corner of the chart.

Allows traders to see the active settings for quick adjustments.

Key Inputs

Style Settings:

Pattern Color: Customize the color of the geometric patterns.

Size Multiplier (sizeMult): Adjusts the size of the pattern relative to price movements.

Line Width: Controls the thickness of the geometric lines.

Timeframe Settings:

Base Resolution (baseRes): Timeframe for calculating the pattern's anchor (default: daily).

Pattern Resolution (patternRes): Timeframe granularity for the pattern’s formation.

Geometric Adjustments:

Pattern Width (barOffset): Horizontal width in bars.

ATR Multiplier (rangeSize): Vertical size adjustment based on price volatility.

Scientific Concepts

Volatility Representation:

ATR (Average True Range): A standard measure of market volatility, representing the average range of price movements over a defined period. Here, ATR adjusts the vertical height of the geometric figures.

Geometric Symmetry:

The script emulates symmetry similar to the Sri Yantra, aligning with the principles of sacred geometry, which often appear in nature and mathematical constructs. Symmetry in financial data visualizations can aid in intuitive interpretation of price movements.

Multi-Timeframe Fusion:

Synchronizing patterns with multiple timeframes enhances the relevance of overlays for different trading strategies. For example, daily trends combined with hourly patterns can help traders optimize entries and exits.

Visual Features

Outer Square:

Drawn to encapsulate the geometric structure.

Represents the broader context of price levels.

Triangles:

Three layers of interlocking triangles create a fractal pattern, providing a visual alignment to price dynamics.

Horizontal Lines:

Emphasize critical levels within the pattern, offering visual cues for potential support or resistance areas.

Information Table:

Displays the active timeframe settings, helping traders quickly verify configurations.

Applications

Trend Visualization:

Patterns overlay on price movements provide a clearer view of trend direction and potential reversals.

Volatility Mapping:

ATR-based scaling ensures the pattern adjusts to varying market conditions, making it suitable for different asset classes and trading strategies.

Multi-Timeframe Analysis:

Integrates higher and lower timeframes, enabling traders to spot confluences between short-term and long-term price levels.

Potential Enhancements

Add Fibonacci Levels: Overlay Fibonacci retracements within the pattern for deeper price level insights.

Dynamic Alerts: Include alert conditions when price intersects key geometric lines.

Custom Labels: Add text descriptions for critical intersections or triangle centers.

This script is a unique blend of technical analysis and sacred geometry, providing traders with an innovative way to visualize market dynamics.

Pivotal Point Detection

The indicator highlights price gaps (overnight gaps) with significantly increased volume in the daily chart only. These price jumps can occur after earnings reports or other significant news and often point to an important event (e.g., a new product or business model). According to Jesse Livermore, these are called Pivotal Points.

The price jumps displayed by the indicator are not a guarantee that they represent a true Pivotal Point, but they provide a hint of a significant business development - especially when they occur repeatedly alongside revenue growth. This can help identify potentially strong growth stocks and high-performing investments. However, the underlying events and connections must be investigated through additional research.

make posible to find stocks like:

NYSE:PLTR NASDAQ:ROOT NASDAQ:NVDA NYSE:CVNA NYSE:LRN

A "pivotal price line" is drawn at the opening price of the Pivotal Point. This line is considered a support level. If the price falls below this line, the Pivotal Point loses its validity.

Global vs National Index Spread RSIThe Global vs National Index Spread RSI indicator visualizes the relative strength of national stock indices compared to a global benchmark (e.g., AMEX). It calculates the percentage spread between the closing prices of each national index and the global index, applying the Relative Strength Index (RSI) to each spread.

How It Works

Spread Calculation: The spread represents the percentage difference between a national index and the global index.

RSI Application: RSI is applied to these spreads to identify overbought or oversold conditions in the relative performance of the national indices.

Reference Lines: Overbought (70), oversold (30), and neutral (50) levels help guide interpretation.

Insights from Research

The correlation between global and national indices provides insights into market integration and interdependence. Studies such as Forbes & Rigobon (2002) emphasize the importance of understanding these linkages during periods of financial contagion. Observing spread trends with RSI can aid in identifying shifts in investor sentiment and regional performance anomalies.

Use Cases

- Detect divergences between national and global markets.

- Identify overbought or oversold conditions for specific indices.

- Complement portfolio management strategies by monitoring geographic performance.

References

Forbes, K. J., & Rigobon, R. (2002). "No contagion, only interdependence: Measuring stock market co-movements." Journal of Finance.

Eun, C. S., & Shim, S. (1989). "International transmission of stock market movements." Journal of Financial and Quantitative Analysis.