Metatron Lines (Highs & Lows Geometry)Metatron Lines

Hey TradingView community! 👋

I wanted to share something I've been working on that might help you see market structure from a different angle. This indicator connects pivot highs and lows using geometric patterns, creating what I call "Metatron Lines."

What it does (simply put):

- Finds significant highs and lows on your chart

- Draws lines connecting these points to reveal hidden geometric relationships

- Shows you the underlying structure that price tends to respect

Why I built this:

I noticed that markets often move in patterns that aren't immediately obvious. Sometimes the most important levels aren't the obvious support and resistance lines, but the intersections and angles created by connecting multiple pivot points. This tool helps visualize those relationships.

How it might help you:

- Pattern Recognition : Spot geometric formations that traditional analysis might miss

- Support/Resistance : See where multiple geometric lines converge to create strong levels

- Market Structure : Better understand how price flows and where it might find obstacles

- Confluence Areas : Identify zones where multiple geometric elements align

A few honest thoughts:

This isn't a magic bullet or a guaranteed profit maker (nothing is!). It's simply another lens through which to view price action. Some traders find geometric analysis helpful, others prefer different approaches - and that's perfectly fine.

I've tried to make it customizable so you can adjust it to fit your trading style and timeframe. The default settings work well for most instruments, but feel free to experiment.

Settings you can adjust:

- Pivot detection sensitivity

- Number of connection points

- Line colors and styles

- Which connections to show (highs, lows, or both)

I hope some of you find this useful! I'm always learning from this community, so if you have suggestions for improvements or different ways to use it, I'd love to hear them.

Trade safe and trust your process! 📈

---

This indicator is provided as-is for educational and analysis purposes. Please practice proper risk management and never risk more than you can afford to lose.

GEOMETRIC

Itakura-Saito Autoregressive Extrapolation of Price [Loxx]Itakura-Saito Autoregressive Extrapolation of Price is an indicator that uses an autoregressive analysis to predict future prices. This is a linear technique that was originally derived or speech analysis algorithms.

What is Itakura-Saito Autoregressive Analysis?

The technique of linear prediction has been available for speech analysis since the late 1960s (Itakura & Saito, 1973a, 1970; Atal & Hanauer, 1971), although the basic principles were established long before this by Wiener (1947). Linear predictive coding, which is also known as autoregressive analysis, is a time-series algorithm that has applications in many fields other than speech analysis (see, e.g., Chatfield, 1989).

Itakura and Saito developed a formulation for linear prediction analysis using a lattice form for the inverse filter. The Itakura–Saito distance (or Itakura–Saito divergence) is a measure of the difference between an original spectrum and an approximation of that spectrum. Although it is not a perceptual measure it is intended to reflect perceptual (dis)similarity. It was proposed by Fumitada Itakura and Shuzo Saito in the 1960s while they were with NTT. The distance is defined as: The Itakura–Saito distance is a Bregman divergence, but is not a true metric since it is not symmetric and it does not fulfil triangle inequality.

read more: Selected Methods for Improving Synthesis Speech Quality Using Linear Predictive Coding: System Description, Coefficient Smoothing and Streak

Data inputs

Source Settings: -Loxx's Expanded Source Types. You typically use "open" since open has already closed on the current active bar

LastBar - bar where to start the prediction

PastBars - how many bars back to model

LPOrder - order of linear prediction model; 0 to 1

FutBars - how many bars you want to forward predict

Things to know

Normally, a simple moving average is calculated on source data. I've expanded this to 38 different averaging methods using Loxx's Moving Avreages.

This indicator repaints

Related Indicators (linear extrapolation of price)

Levinson-Durbin Autocorrelation Extrapolation of Price

Weighted Burg AR Spectral Estimate Extrapolation of Price

Helme-Nikias Weighted Burg AR-SE Extra. of Price

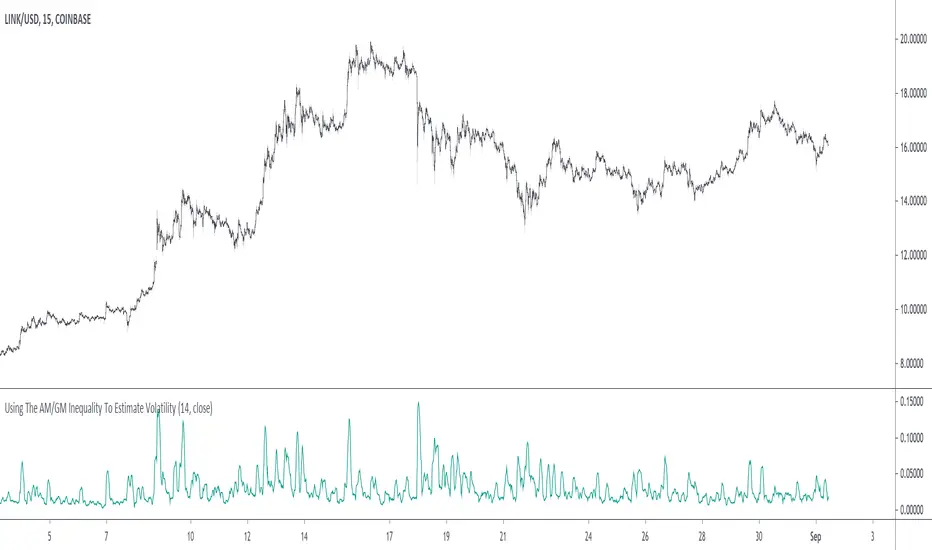

Using The AM/GM Inequality To Estimate VolatilityA volatility indicator derived from the AM/GM inequality. I don't think it will be necessary to describe the usage and interpretation of such indicator, and I don't think it is super useful, however, this is not the case of the script, which contains three ways to compute the geometric mean, with a classic, a simple, and an efficient way. The AM/GM inequality is also a really interesting concept, and I'll try to"prove" it in this post by using DSP. I also added more comments in the script in order to highlight some stuff.

The AM/GM Inequality

When we talk about the mean, we are referring to the "arithmetic" one by default, but there exist more types of means. Two other ones include the "geometric" and "harmonic" means, both are part of the Pythagorean means with the arithmetic mean.

Each one of them as several properties, but the most interesting aspect is their inequality, that is:

HM <= GM <= AM

The arithmetic mean is the one with the highest value, while the harmonic mean is the one with the lowest value. In the case each data point is equal to each other, all the means have the same value.

In our case, the inequality of interest is the inequality between the geometric and arithmetic mean, where the geometric mean is lower or equal than the arithmetic one. Many proofs/explanations exist, I'll try my version using DSP, where instead of thinking about means, we think about rolling means, which allows us to interpret them as low-pass filters. So we end up having the geometric moving average (GMA) and arithmetic moving average (SMA).

We know that GMA <= SMA , the SMA has a unity passband, this implies that the GMA has a passband lower than 1 (for non-equal input values), this explains why the GMA is smaller than the SMA. In order for a FIR filter to have a passband lower than 1, the sum of the filter coefficients must be lower than 1. In order to further proves this consider the following equation:

sqrt(a×b) = k×a + k×b

Here sqrt(a×b) is the geometric mean of a and b , the right-hand side of the equation is a weighted sum between a and b and coefficient k , we want to solve the equation with respect to k , if k×2 < 1 then we have the proof that GMA < SMA . The solution with respect to k is:

k = sqrt(a×b)/(a+b)

which always gives a number lower than 0.5, as such k×2 < 1 and thus the passband is lower than 1. If our input values are equal to each other, we end up with the following solution for k :

k = sqrt(a×a)/(a+a) = a/(2×a) = 0.5

as such the GMA has the coefficients of an SMA as long as the input values are equal to each other.

Because of this inequality, we can subtract the SMA to a GMA and take the square root of the result in order to have a volatility indicator, however, both moving averages are still pretty close to each other, which gives a very small result for the indicator.

Uwu I am a bit tired, better indicators coming up

Portfolio: alpha, beta, stdev, variance, mean, max drawdown...Portfolio Metrics **New**

'returns'

'log returns'

'geometric returns'

portfolio alpha

portfolio beta

portfolio,market correlation

portfolio standard deviation

portfolio variance

mean portfolio returns

maximum drawdown

maximum gain

Spread by//Every spread & central tendency measure in 1 script with comfortable visualization, including scrips's status line.

Spread measures:

- Standard deviation (for most cases);

- Average deviation (if there are extreme values);

- GstDev - Geometric Standard Deviation (exclusively for Geometric Mean);

- HstDev - Harmonic Deviation (exclusively for Harmonic Mean).

These modified functions will calculate everything right, they will take source, length, AND basis of your choice, unlike the ones from TW.

Central tendency measures:

- Mean (if everything's cool & equal);

- Median (values clustering towards low/high part of the rolling window);

- Trimean (3/more distinguishable clusters of data);

- Midhinhe (2 distinguishable clusters of data);

- Geometric Mean ( |low.. ... ... .. .... ... . . . . . . . . . . . .high| this kinda data); <- Exp law

- Harmonic Mean { |low. . . . . . . . . . . . . . .. . . .high| kinda data). <- Reciprocal law

Listen:

1) Don't hesitate using Standard Deviation with non-mean, like "Midhinge Standard Devition", despite what ol' stats gurus gonna say, it works when it's appropriate;

2) Don't check log space while using Geometric Mean & Geometric Standard Deviation, these 2 implement log stuff by design, I mean unless u wanna make it double xd

3) You can use this script, modify it how you want, ask me questions whatever, just make money using it;

4) Use Midrange & Midpoints in tandem when data follows ~addition law (like this . . . . . . . . . . . . . . . . . . . . .). <- just addition law

Look at the data, choose spread measure first, then choose central tendency measure, not vice versa.

!!!

Ain't gonna place ® sign on standard deviations like one B guy did in 1980s lmao, but if your wanna use Harmonic Deviations in science/write about/cite it/whatever, pls give me a lil credit at least, I've never seen it anywhere and unfortunately had to develop it by myself. it's useful when your data develops by reciprocals law (opposite to exponential).

Peace TW

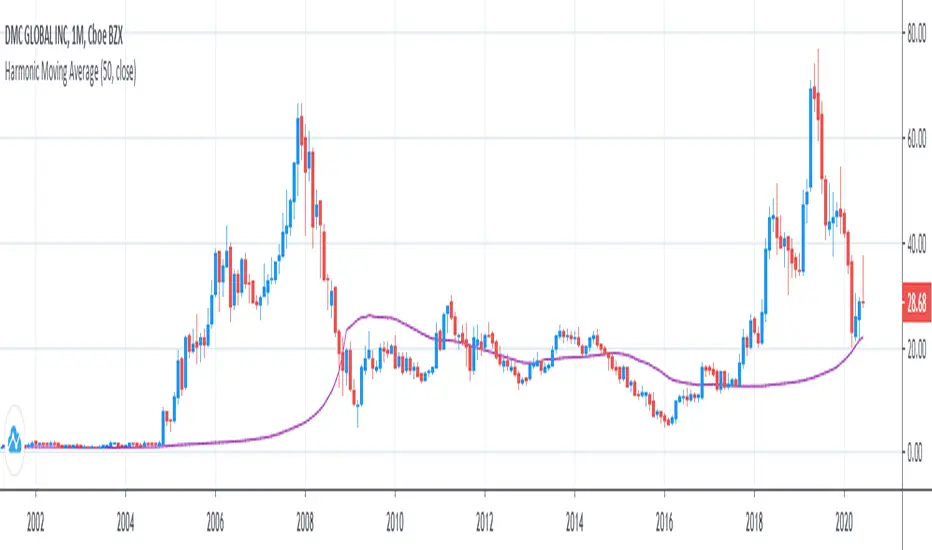

Harmonic Moving AverageI was legitimately surprised no1 has already coded it out on TradingView, but you guys can copypaste & include it in Pine 5 if your see this xd

Here is it.

I've checked and double checked everything, the calculations are right, it can be proved by plotting mean, geometric mean & harmonic mean together and noticing that geometric mean will be always between Harmonic mean, which is always below, and Mean, which is always above.

...

Other central tendency measures are also here as well for usability.

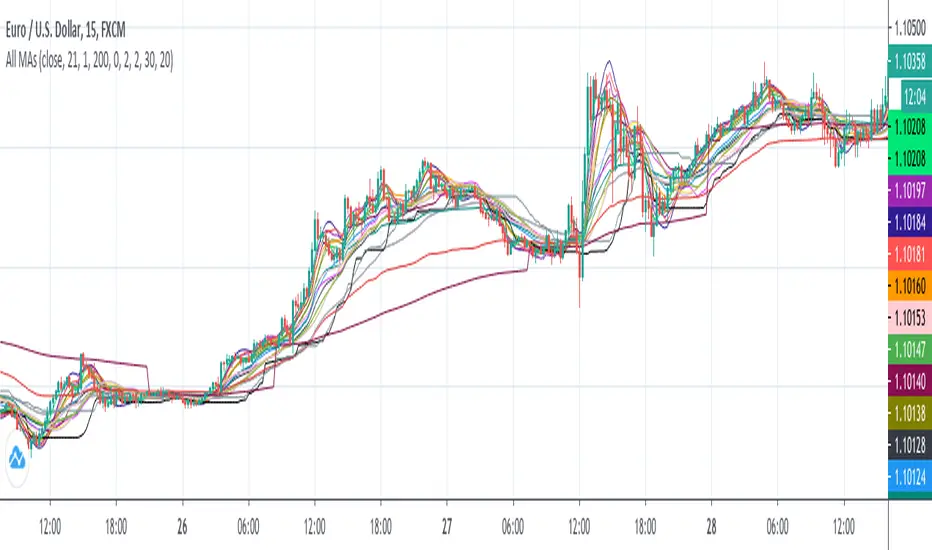

All MAs displayedThis is a collection of moving averages.

Thanks to everget and other pinecoders to pubblish their codes in tradingview.

I just collect a lot of moving averages in one script and transform them in stand alone functions, so you can copy and paste in your script the MA that best fit your needs.

Furthermore, the chart shows which moving average has more smooth and which one has less lag and so on: in this way it is easy to graphically compare moving averages.

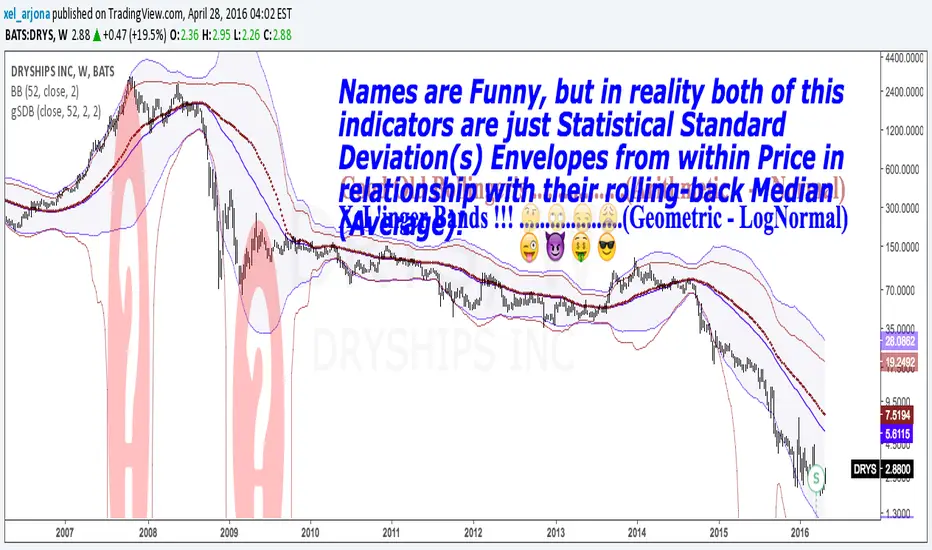

GEOMETRIC STANDARD DEVIATION BANDS v1 by @XeL_ArjonaGEOMETRIC STANDARD DEVIATION BANDS

Ver.1 By Ricardo M Arjona @XeL_Arjona

DISCLAIMER:

The Following indicator/code IS NOT intended to be a formal investment advice or recommendation by the author, nor should be construed as such. Users will be fully responsible by their use regarding their own trading vehicles/assets.

The embedded code and ideas within this work are FREELY AND PUBLICLY available on the Web for NON LUCRATIVE ACTIVITIES and must remain as is.

WHAT'S THIS?

This IS NOT the wheel "Re-Invention"... This is exactly what the name says: A pair of Envelope Bands to measure "volatility", constructed at statistical relation from within price series and their Rolling back MEAN (Simple Moving Average). YES, What Mr. Bollinger did and put it's name to this simple, cleaver and popular formula.

This time, I took the time to make another simple mod, but seems to me to be quite functional in REAL VOLATILE assets like in the example chart: TO USE THEIR GEOMETRIC MODE!!

Cheers!

Any feedback or public modification(s) are quite welcome to the community....!

@XeL_Arjona

Apr 28 2016