[ BETA ][ IND ][ LIB ] Dynamic LookBack RSI RangeGet visual confirmation with this indicator if the current range selected had been oversold or overbough in the latest n bars

Historical

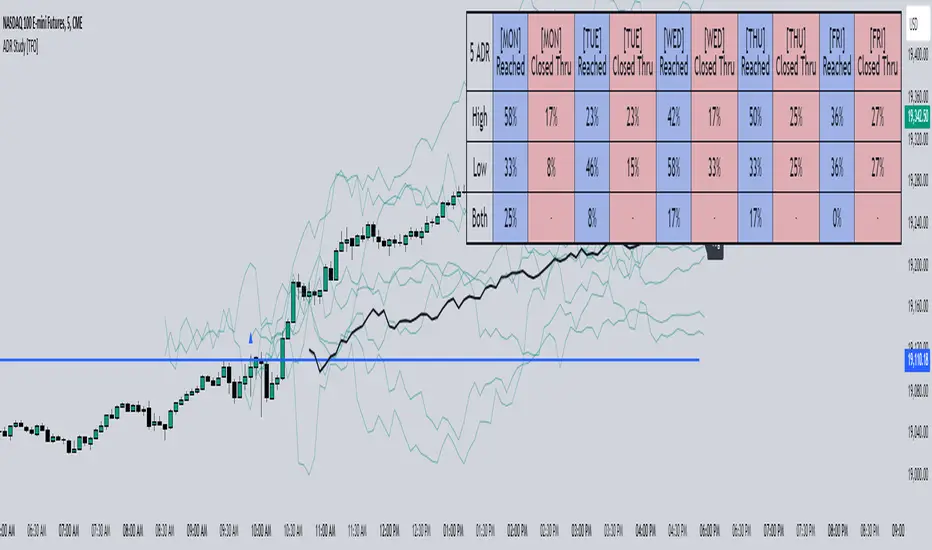

ADR Study [TFO]This indicator is focused on the Average Daily Range (ADR), with the goal of collecting data to show how often price reaches/closes through these levels, as well as a look at historical moves that reached ADR and at similar times of day to study how price moved for the remainder of the session.

The ADR here (blue line) is calculated using the difference between a day's highest and lowest points. If our ADR length is 5, then we are taking this difference from the last 5 days and averaging them together. At the following day's open, we take half of this average and plot it above and below the daily opening price to place theoretical limits on how far price may move according to the lookback period. The triangles indicate when price has reached ADR (either +ADR or -ADR), and alerts can be created for these events.

The Scale Factor is an optional parameter to scale the ADR by a certain amount. If set to 2 for example, then the ADR would be 2x the average daily range. This value will be reflected in the statistics options so that users can see how different values affect the outcomes.

Show Table will display data collected on how often price reaches these levels, and how often price closes through them, for each day of the week. By default, these are colored as blue and red, respectively. From the following chart of NQ1!, we can see for example that on Mondays, price reached +ADR 38% of the time and closed through it 23% of the time. Note that the statistics for closing through the ADR levels are derived from all instances, not just those that reached ADR.

Show Sample Sizes will display how many instances were collected for all given sets of data. Referring to the same example of NQ1!, we can see that this particular chart has collected data from 109 Mondays. From those Mondays, 41 reached +ADR (38%, verifying our initial claim) and 25 closed through it (23%). This is important to understand the scope of the data that we're working with, as percentages can be misleading for smaller sample sizes.

Show Histogram will plot the same exact data as the table, just in a histogram form to visually emphasize the differences on a day-by-day basis. On this chart of RTY1!, we can see for example from the top histogram that on Wednesdays, 40% reached +ADR and only 22% closed through it. Similarly if we look at the bottom histogram, we can see that Wednesdays reached -ADR 46% of the time and closed through it only 28% of the time.

We can also use Show Sample Sizes to display the same information that would be in the table, showing how many instances were collected for each event. In this case we can see that we observed 175 Fridays, where 76 reached +ADR (43%) and 44 closed above it (25%).

Show Historical Moves is an interesting feature of this script. When enabled, if price has reached +/- ADR in the current session, the indicator will plot the evolution of the close prices from all past sessions that reached +/- ADR to see how they traded for the remainder of the session. These calculations are made with respect to the ADR range at the time that price traded through these levels.

Historical Proximity (Bars) allows the user to observe historical moves where price reached ADR within this many bars of the current session (assuming price has reached an ADR level in the current session). In the above chart, this is set to 1000 so that we can observe each and every instance where price reached an ADR level. However, we can refine this a bit more.

By limiting the Historical Proximity to something like 20, we are only considering historical moves that reached ADR within 20 bars of todays +ADR reach (9:50 am EST, noted by the blue triangle up). We can enable Show Average Move to display the average move by the filtered dataset, and Match +/-ADR to only observe moves inline with the current day's price action (in this case, only moves that reached +ADR, since price has not reached -ADR).

We can add one more filter to this data with the setting Only Show Days That: closed through ADR; closed within ADR; or either. The option either is what you see above, as we are considering both days that closed through ADR and days that closed within it (note that in this case, closing within ADR simply means that price reached +ADR and closed the day below it, and vice versa for -ADR; this does not mean that price must have closed in between +ADR and -ADR). If we set this to only show instances that closed within ADR, we see the following data.

Alternatively, we can choose to Only Show Days That closed through ADR, where we would see the following data. In this case, the average move very much resembles the price action that occurred on this particular day. This is in no way guaranteed, but it makes an interesting case for how we could use this data in our analysis by observing similar, historical price action.

Please note that this data will change over time on a rolling basis due to TradingView's bar lookback, and that for this same reason, lower timeframes will yield less data than larger timeframes.

Historical Price Projection [LuxAlgo]The Historical Price Projection tool aims to project future price behavior based on historical price behavior plus a user defined growth factor.

The main feature of this tool is to plot a future price forecast with a surrounding area that exactly matches the price behavior of the selected period, with or without added drift.

Other features of the tool include:

User-selected period up to 500 bars anywhere on the chart within 5000 bars

User selected growth factor from 0 (no growth) to 100, this is the percentage of drift to be used in the forecast.

User selected area wide

Show/hide forecast area

🔶 USAGE

This tool generates a price projection with exactly the same price behavior over the period selected by the user, plus a growth factor .

The user must confirm the selection of the anchor point in order for the tool to be executed; this can be done directly on the chart by clicking on any bar, or via the date field in the settings panel.

As we can see on this chart, the four phases of the market cycle are clearly defined and marked, so we choose the distribution phase as our anchor point because in our analysis, we want to see how the market would behave if we were currently at the same point in the cycle.

In the image above, the growth factor parameter is set to 0 so that the projection matches the selection. The tool will use up to 500 bars after the selection point.

The growth factor is defined as the percentage of drift that the tool will use.

Drift is defined as follows:

For periods with a positive return: average negative return within the period

For negative return periods: average positive return within the period

On the chart above, we have selected the same period but added a growth factor of 10, so that the tool uses a 10% drift in its calculations of future prices.

As the return in the selected period is negative, the added drift will make the projection more bearish than the prices from the selection.

On this chart we have changed the selected period, we have chosen the accumulation phase of the last cycle as the anchor point, again with a growth factor of 10%.

As we can see, prices explode higher, making the projection very bullish, as the added effect of both the bullish selected period and the 10% drift is taken into account.

This last chart is a long-term chart, a quarterly chart of the Dow, and it will serve as a review exercise.

What if... everything goes south and the crash of '29 is repeated?

The answer is in the chart, and it is not for the faint of heart

In this case we have chosen a growth factor of 0 to see exactly the same price behaviour projected into the future.

🔶 SETTINGS

🔹 Data Gathering

Anchor point: Starting point for data collection, up to 500 bars will be used.

🔹 Data Transformation

Growth Factor: Values from 0 to 100, is the amount of drift used to calculate the next price in the series.

Area Width: Values from 0 to 100, controls the width of the area around the forecast as an increment/decrement of the growth factor.

🔹 Style

Price line width: Size of the price line.

Bullish color

Bearish color

Show Area: Show forecast area.

Area color

ADR % RangesThis indicator is designed to visually represent percentage lines from the open of the day. The % amount is determined by X amount of the last days to create an average...or Average Daily Range (ADR).

1. ADR Percentage Lines: The core function of the script is to apply lines to the chart that represent specific percentage changes from the daily open. It first calculates the average over X amount of days and then displays two lines that are 1/3rd of that average. One line goes above the other line goes below. The other two lines are the full "range" of the average. These lines can act as boundaries or targets to know how an asset has moved recently. *Past performance is not indicative of current or future results.

The calculation for ADR is:

Step 1. Calculate Today's Range = DailyHigh - DailyLow

Step 2. Store this average after the day has completed

Step 3. Sum all day's ranges

Step 4. Divide by total number of days

Step 5. Draw on chart

2. Customizable Inputs: Users have the flexibility to customize the script through various inputs. This includes the option to display lines only for the current trading day (`todayonly`), and to select which lines are displayed. The user can also opt to show a table the displays the total range of previous days and the average range of those previous days.

3. No Secondary Timeframe: The ADR is computed based on whatever timeframe the chart is and does not reference secondary periods. Therefore the script cannot be used on charts greater than daily.

This script is can be used by all traders for any market. The trader might have to adjust the "X" number of days back to compute a historical average. Maybe they only want to know the average over the past week (5 days) or maybe the past month (20 days).

Historic Volume/Market ProfilesHistoric Volume/Market Profile is a Periodic Volume Profile with all of the improvements known in the original Volume/Market Profile.

VMP is a 2 in 1 Volume and Market Profile Indicator.

HVMP uses the base of VMP to offer a quick and simple view at multiple historic profiles at the same time.

This includes:

Cluster Identification for High Volume and Low Volume Areas.

Maximizing granularity by utilizing boxes and lines to get up to 1000 rows.

New Inclusions in HVMP vs VMP:

HVMP granularity is determined by the # of profiles on display. By doing this, each profile will get an even amount of allocated rows to use and granularity is scaled per-profile, to fit within the row allowance.

For Example: 1000/(# of profiles) = Maximum # of rows per profile.

HVMP introduces the "Auto-Scale" Option (on by Default), this automatically fits each profile within the defined timeframe period to provide a consistent display when switching timeframes.

Even with "Auto-Scale" enabled, "Display Size" dictates which direction the profile is displayed.

Below is a Negative Display Size (Displays from right to left, starting at the end of the period)

Below is a Positive Display Size (Displays from left to right, starting at the beginning of the period)

HVMP is only for historical data, you can get a live profile with the same Node Identification using VMP (Volume Market/Profile). The indicator that this one is based on.

Find it Here: Volume/Market Profile

Enjoy!

Seasonal Performance for Stocks & CryptoThe Seasonal Performance indicator quickly allows you to see if you are in a bullish or bearish time of year for an underlying security and where the current performance stacks up compared to the same time of year historically. Table is fully customizable from colors to what data to see.

Table Displays

Average Performance

Best Performance

Worst Performance

Last Performance

Current Performance

Note this indicator will only work with Stocks, ETF's, Index's or Crypto.

Statistics: High & Low timings of custom session; 1yr historyGet statistics of the Session High and Session Low timings for any custom session; based on around 1yr of data.

//Purpose:

-To get data on the 'time of day' tendencies of an asset.

-Narrow in on a custom defined session and get statistics on that session.

//Notes:

-Input times are always in New York time (but changing the timezone after setting WILL adust both table stats and background highlight correctly.

-For particularly long sessions, make sure text size is set to 'tiny' (very long vertical table), or adjust table to display horizontally.

-You'll notice most assets show higher readings around NY equities open (9:30am NY time). Other assets will have 'hot-spots' at other times too.

-Timings represent the beginning of a 15m candle. i.e. reading for 15:45 represents a high occurring between 15:45 and 1600.

-Premium users should get 20k bars => around 1year's worth of data on a 15minute chart. Days of history is displayed in the top left corner of the table.

//Limitations

-only designed and working on 15minute timeframe (to gather a full year of meaningful/comparable % stats, need 15minute 'buckets' of time.

-sessions cannot cross through midnight, or start at midnight (00:15 is ok). 00:15 >> 23:45 is the max session length. On BTC, same applies but 01:00 instead of midnight (all in NY time).

-if your session crosses through 'dead time' (e.g. 17:00-18:00 S&P NY time); table will correctly omit these non-existent candles, but it will add on the missing hour before the start time.

//Cautionary note:

-Since markets are not uncommonly in a trending state when your defined session starts or ends, the high/low timings % readings for start and end of session may be misleadingly high. Try to look for unusually high readings that are not at the start/end of your session.

Wheat (ZW1!) 15min chart; Table displayed vertically:

Nasdaq (NQ1!) 15m chart; Table displayed horizontally and with smaller text to view a very long custom session:

Price Data LabelThis indicator gives you the ability to see historical data for each bar on the chart by simply hovering over the high of the bar, similar to the functionality of MarketSmith.

Data for each bar includes:

Open

High

Low

Close + Change

Percentage Change

Closing Range

Volume

Volume Percent based on 50 day average

Distance to 4 selectable moving averages

Example of stats on a historical bar:

* Note this only works on the last 500 historical bars. If you use bar replay it will work with 500 historical bars from the last bar.

* If you have multiple indicators on your chart, in order to see the data you will need to use visual order to bring to front. This can be done by clicking the three dots next to the indicator name and selecting visual order.

Volatility Gap TrackerThe Volatility Gap Tracker ( *VGT ) indicator calculates the historical volatility of an asset using the standard deviation of the natural logarithm of the closing price relative to the previous period's closing price. *VGT visualizes the HV with gap lines to highlight when the current HV has increased or decreased significantly compared to the previous period, and adds labels to show the HV value for each of those bars.

Low HV calculated by *VGT can potentially signify a potential move up or down in the price of an asset. When HV is low, it indicates that the price of the asset has been relatively stable or range-bound over the specified period of time. This can sometimes be a precursor to a significant move in either direction, as the price may be building up energy to break out of its range.

*VGT can be used for any market that TradingView supports, including stocks, forex, and cryptocurrencies. It is especially useful for traders who want to identify periods of high volatility or sudden changes in volatility , which can indicate potential trading opportunities or risks. However, it's important to note that HV is a historical measure and may not always accurately predict future volatility .

The indicator can be used under various market conditions, but is especially useful during periods of high volatility , such as market crashes or major news events. It can also be useful for traders who want to monitor the volatility of specific stocks or assets over a longer period of time.

*VGT is provided for informational purposes only and is not a guarantee of future performance or accuracy. Traders should use multiple indicators and analysis methods to make informed trading decisions. Trading involves risks and traders should always conduct their own research and analysis before making any investment decisions.

Multi-Asset Month/Month % change 10yr Averages10 Year Averages of Month-on-Month % change: Shows current asset, and 3x user input assets

-For comparing seasonal tendencies among different assets.

-Choose from a variety of monthly average measures as source: sma(close, length), sma(ohlc4, length); as well as sma's of vwap, vwma, volume, volatility. (sma = simple moving average).

-Averages based on month cf previous month: i.e. Feb % = Feb compared to Jan; Jan % = Jan compared to prev year's Dec. Average of the last 10yrs of these values is the printed value.

-Plot on current year (2023), or previous year (2022). If Plotting on current year, and a month of year has not yet occured, a 9yr average will be printed.

/// notes ///

-daily bars in month is a global setting; so choose assets which have similar trading days per month. i.e. Crypto: length = 30 (days per month); Stocks/FX/Indices: length = 21 (days per month).

-only plots on Daily timeframe.

10yr Avgs; Plotting with Year = 2022; using sma(close, 21) as source for average M/M change

Percent ResearchPercent Research is an indicator that will plot a color / column on the chart in case custom requirements are met.

The requirements are:

- Price : Price requirement (equal or above input).

- Change % Up : Amount the price have moved up in percent (equal or above input).

- Change % Down : Amount the price have moved down in percent (equal or below input).

- Change Interval : Amount of bars the above move happened over.

- Volume : Volume requirement (equal or above input).

- Volume Interval : Amount of bars in a row that each require the above volume.

Example: In case one wants to plot whenever price has made a 20 percent move up or down in a week with minimum 100 000 volume for each of the last 2 days one can use.

Change % Up: 20

Change % Down: -20

Change Interval: 5

Volume: 100 000

Volume Interval: 2

The indicator will plot a color on the chart whenever the requirements are met, which then can be used to look into price action for each colored time period.

The values can be customized dependent on preference, example 100% movers over a month or 20% movers over a week etc.

Historical Crypto Conference DatesJust a basic list date script to display various conference dates from the crypto sector. Updates to add more conferences.

Red - BTC Miami

Blue - Consensus

FUNCTION: Limited Historical Data WorkaroundFUNCTION: Limited Historical Data Workaround

If you are working with bitcoin weekly charts, or any other ticker with a low amount of price history this function may help you out. For example you want to apply indicators to some shitcoin that just launched? This can help you.

It can be frustrating to use certain built-ins since they will only give an output once the full lookback length is available. This function allows you to avoid that situation and start plotting things with almost no history whatsoever!

In this example code we do it by utilizing a replacement for the built in pine SMA function. This function allows us to pass a series instead of just a simple int to the length variable of the SMA. This can be achieved with all the pine built ins and I believe @pinecoders has a publication already detailing many of them with full coded examples.

Then we replace the length of the SMA with the custom history function. It checks to see if the current bar index is less than the length of the function. Then if it is, it changes the length to the bar index allowing us to get plots and series earlier than otherwise possible.

10yr, 20yr, 30yr Averages: Month/Month % Change; SeasonalityCalculates 10yr, 20yr and 30yr averages for month/month % change

~shows seasonal tendencies in assets (best in commodities). In above chart: August is a seasonally bullish month for Gold: All the averages agree. And January is the most seasonally bullish month.

~averages represent current month/previous month. i.e. Jan22 average % change represents whole of jan22 / whole of dec21

~designed for daily timeframe only: I found calling monthly data too buggy to work with, and I thought weekly basis may be less precise (though it would certainly reduce calculation time!)

~choose input year, and see the previous 10yrs of monthly % change readings, and previous 10yrs Average, 20yr Average, 30yr Average for the respective month. Labels table is always anchored to input year.

~user inputs: colors | label sizes | decimal places | source expression for averages | year | show/hide various sections

~multi-yr averges always print, i.e if only 10yrs history => 10yr Av = 20yr Av = 30yr Av. 'History Available' label helps here.

Based on my previously publised script: "Month/Month Percentage % Change, Historical; Seasonal Tendency"

Publishing this as seperate indicator because:

~significantly slower to load (around 13 seconds)

~non-premium users may not have the historical bars available to use 20yr or 30yr averages =>> prefer the lite/speedier version

~~tips~~

~after loading, touch the new right scale; then can drag the table as you like and seperate it from price chart

##Debugging/tweaking##

Comment-in the block at the end:

~test/verifify specific array elements elements.

~see the script calculation/load time

~~other ideas ~~

~could tweak the array.slice values in lines 313 - 355 to show the last 3 consecutive 10yr averages instead (i.e. change 0, 10 | 0,20 | 0, 30 to 0, 10 | 10, 20 | 20,30)

~add 40yr average by adding another block to each of the array functions, and tweaking the respective labels after line 313 (though this would likely add another 5 seconds to the load time)

~use alternative method for getting obtaining multi-year values from individual month elements. I used array.avg. You could try array.median, array.mode, array.variance, array.max, array.min (lines 313-355)

Month/Month Percentage % Change, Historical; Seasonal TendencyTable of monthly % changes in Average Price over the last 10 years (or the 10 yrs prior to input year).

Useful for gauging seasonal tendencies of an asset; backtesting monthly volatility and bullish/bearish tendency.

~~User Inputs~~

Choose measure of average: sma(close), sma(ohlc4), vwap(close), vwma(close).

Show last 10yrs, with 10yr average % change, or to just show single year.

Chose input year; with the indicator auto calculating the prior 10 years.

Choose color for labels and size for labels; choose +Ve value color and -Ve value color.

Set 'Daily bars in month': 21 for Forex/Commodities/Indices; 30 for Crypto.

Set precision: decimal places

~~notes~~

-designed for use on Daily timeframe (tradingview is buggy on monthly timeframe calculations, and less precise on weekly timeframe calculations).

-where Current month of year has not occurred yet, will print 9yr average.

-calculates the average change of displayed month compared to the previous month: i.e. Jan22 value represents whole of Jan22 compared to whole of Dec21.

-table displays on the chart over the input year; so for ES, with 2010 selected; shows values from 2001-2010, displaying across 2010-2011 on the chart.

-plots on seperate right hand side scale, so can be shrunk and dragged vertically.

-thanks to @gabx11 for the suggestion which inspired me to write this

Average Daily Pip Ranges by monthShows historical average daily pip ranges for specific months for FOREX pairs

useful for guaging typical seasonal volatility; or rough expected daily pip ranges for different months

works on both DXY and foreign currencies

option to plot 10yrs worth of data; with 10yr average of the average daily range for specific months

cast back to any previous 10yrs of your choosing

@twingall

Last Available Bar InfoLibrary "Last_Available_Bar_Info"

getLastBarTimeStamp()

getAvailableBars()

This simple library is built with an aim of getting the last available bar information for the chart. This returns a constant value that doesn't change on bar change.

For backtesting with accurate results on non standard charts, it will be helpful. (Especially if you are using non standard charts like Renko Chart).

Methods

getLastBarTimeStamp()

: Returns Timestamp of the last available bar (Constant)

getAvailableBars()

:Returns Number of Available Bars on the chart (Constant)

Example

import paragjyoti2012/Last_Available_Bar_Info/v1 as LastBarInfo

last_bar_timestamp=LastBarInfo.getLastBarTimeStamp()

no_of_bars=LastBarInfo.getAvailableBars()

If you are using Renko Charts, for backtesting, it's necesary to filter out the historical bars that are not of this timeframe.

In Renko charts, once the available bars of the current timeframe (based on your Tradingview active plan) are exhausted,

previous bars are filled in with historical bars of higher timeframe. Which is detrimental for backtesting, and it leads to unrealistic results.

To get the actual number of bars available of that timeframe, you should use this security function to get the timestamp for the last (real) bar available.

tf=timeframe.period

real_available_bars = request.security(syminfo.ticker, tf , LastBarInfo.getAvailableBars() , lookahead = barmerge.lookahead_off)

last_available_bar_timestamp = request.security(syminfo.ticker, tf , LastBarInfo.getLastBarTimeStamp() , lookahead = barmerge.lookahead_off)

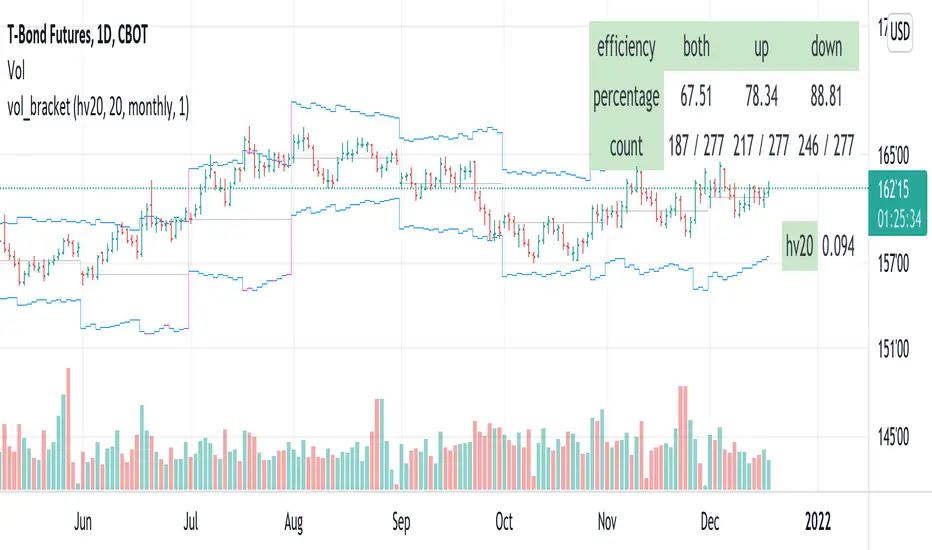

vol_bracketThis simple script shows an "N" standard deviation volatility bracket, anchored at the opening price of the current month, week, or quarter. This anchor is meant to coincide roughly with the expiration of options issued at the same interval. You can choose between a manually-entered IV or the hv30 volatility model.

Unlike my previous scripts, which all show the volatility bracket as a rolling figure, the anchor helps to visualize the volatility estimate in relation to price as it ranges over the (approximate) lifetime of a single, real contract.

vol_rangesThis script shows three measures of volatility:

historical (hv): realized volatility of the recent past

median (mv): a long run average of realized volatility

implied (iv): a user-defined volatility

Historical and median volatility are based on the EWMA, rather than standard deviation, method of calculating volatility. Since Tradingview's built in ema function uses a window, the "window" parameter determines how much historical data is used to calculate these volatility measures. E.g. 30 on a daily chart means the previous 30 days.

The plots above and below historical candles show past projections based on these measures. The "periods to expiration" dictates how far the projection extends. At 30 periods to expiration (default), the plot will indicate the one standard deviation range from 30 periods ago. This is calculated by multiplying the volatility measure by the square root of time. For example, if the historical volatility (hv) was 20% and the window is 30, then the plot is drawn over: close * 1.2 * sqrt(30/252).

At the most recent candle, this same calculation is simply drawn as a line projecting into the future.

This script is intended to be used with a particular options contract in mind. For example, if the option expires in 15 days and has an implied volatility of 25%, choose 15 for the window and 25 for the implied volatility options. The ranges drawn will reflect the two standard deviation range both in the future (lines) and at any point in the past (plots) for HV (blue), MV (red), and IV (grey).

BTC top bottom weekly oscillatorThis indicator is based on the 20 weekly simple moving average and it could be used to help finding potential tops and bottoms on a weekly BTC chart.

This version uses an "oscillator" presentation, it fluctuates around the value zero.

The indicator plots 0 when the close price is near the 20 weekly moving average.

If it's below 0 it reflects the price being below the 20 weekly moving average, and opposite for above.

IT's possible to see how many times the price has hit the 0.5 coef support. In one case it hit 0.6 showing that the 0.5 support can be broken.

The indicator is calculated as Log(close / sma(close))

Instructions:

- Use with the symbol INDEX:BTCUSD so you can see the price since 2010

- Set the timeframe to weekly

Optionals:

- change the coef to 0.6 for a more conservative bottom

- change the coef to 0.4 for a more conservative top

BTC top bottom weekly bandsThis indicator is based on the 20 weekly simple moving average and it could be used to help finding potential tops and bottoms on a weekly BTC chart.

When using the provided "coef" parameter set to the default of 0.5 it shows how most bottoms since 2013 have hit the lower band of this indicator.

The lower band is calculated as exp(coef) * sma(close)

Instructions:

- Use with the symbol INDEX:BTCUSD so you can see the price since 2010

- Set the timeframe to weekly

- Use logarithmic chart (toggle "log" on)

Optionals:

- change the coef to 0.6 for a more conservative bottom

- change the coef to 0.4 for a more conservative top

The Amplifier - Two Day Historical Bitcoin Volatility PlotThe 3rd piece to the other two pieces to our CoT study. This is the Amplifier, which turns select signals into 'Super' Buys/Sells

The other two being the 'Bitcoin Insider CoT Delta', and the on chart Price indicator most will have, if no others the 'Hunt Bitcoin CoT Buy/Sell Signals' that will indicate the key signals, ave 4 a year on the chart as they occur.

Why Bother another CoT signal?

Its different & focused on the Insider's.

Performance -

This Indicator provided a

1. Signal 1 = 26th March 2019 = SUPER LONG at $4,500 that saw a near $14,000 run up

2. Signal 2 = 18th & 24th June 2019 = SHORT at the second & final level $11,700 after repeated attempts & failure in the $13K range, the mini Echo Bitcoin Bull of 2019

3. Signal 3 = 17th December 2019 = LONG $6,900, Bitcoin rallied to Mid $10,500's

4. Signal 4 = 18th Feb 2020 = SUPER SHORT from $9,700's to a final extreme Low of $3,000, calling the CV-19 collapse

5. Signal 5 = 17th March 2020 = LONG from $5,400 no closure point yet

6. Signal 6 = 29th June 2020 = SUPER LONG reiterate from $10,700 no closure sell signal yet

7. Signal 7 = 17th May 2020 = LONG another accumulate LONG with no sell signal yet generated at Post H&S's low of $33,000

Note - This indicator only commences March 2019, as Bitcoin futures were a recent introduction and needed to settle for 6 months in both use and data, no signals were meaningful prior & data was light.

What is Provided. - Please note the need to also add the Hunt Bitcoin Historical Volatility Indicator for full understanding.

We provide 3 things with the 3 indicators.

'Insider' indications from Largest players in the futures market.

1. Bitcoin Macro Buy Signals.

a) The Bitcoin Commitment of Traders results see us focus solely on Largest 4 Short Open Interest & Largest 4 Long Open Interest aspects of the CoT Release data.

When the difference - is tight, a kind of pinch, these have been great Buy signals in Bitcoin.

We call this difference the Delta & When Delta is 5% or less Bitcoin is a Buy.

2. Bitcoin Macro Sells.

a) A sell signal is Triggered in Bitcoin at any point the Largest 4 short OI > or = to 70

3. AMPLIFIER Trade signals 'Super' Longs or Shorts -

Extreme low volatility events leads to highly impulsive & volatile subsequent moves, if either of 1 or 2 above occur, combined with extreme low volatility

a 'Super Long' or 'SUPER SELL' is generated. In the case of the short side, given Bitcoins general expansive and MACRO Bull trend since inception, we seek an additional component

that is an extreme differential/Delta reading between 4 biggest Longs & Shorts OI.

Namely CoT Delta also must be > 47.5%

We also have a Cautionary level, where it is not necessarily a good idea to accumulate Bitcon, as a better opportunity lower may avail itself, see conditions below.

So the required logic explicitly stated below for all Signals.

1. Long - Hunt Bitcoin CoT Delta < or = 5

2. SUPER Long - Hunt Bitcoin CoT Delta < or = 5; and 2 Day Historical Bitcoin Volatility = or < 20

3. Short - Largest 4 Sellers OI = or > 70

4. SUPER Short - Largest 4 Sellers OI = or > 70; AND..

Hunt Bitcoin CoT Delta = or > 47.5 AND 2 Day Historical BTC Volatility = or < 20

5. Caution - Largest 4 Sellers OI = or > 67.5 AND Hunt Bitcoin CoT Delta = or > 45

WARNING SEE Notes Below

Note 1 - = Largest 4 Open Interest Shorts

Note 2 - = Largest 4 Open Interest Longs

Note 3 - = Hunt Cot Delta = (Largest 4 sellers OI) -( Largest 4 Buyers OI)

Caution = Avoid new Bitcoin Accumulation Right Now, A sell signal might follow Enter on next Long

Note 4 - The Hunt Bitcoin COT Delta signal is a Largest 'Insider' Tracking tool based on a segment of Commitment of Traders data on Bitcoin Futures, released once a week on a Friday.

It is a Macro Timeframe signal , and should not be used for Day trading and Short Timeframe analysis , Entries may be optimised after a Hunt Bitcoin CoT Signal is generated by separate shorter Timeframe analysis.

Note 5 - The Historical Bitcoin Volatility is an additional 'Amplifier' component to the 'Hunt Bitcoin Cot Delta' Insider Signal

Note 6 - The Historical Bitcoin Volatility criteria varies by timeframe, the above levels are those applying on a Two Day TF Chart, select this custom timeframe in Trading View.

if additional criteria are met for LONG & SHORT insider signals, they may become 'Super Longs/Shorts', see conditions box above.

Relative Historical Volatility MCMRelative Historical Volatility

Historical Volatility is relative to it's doubled lookback period of the historical volatility to calculate relative historical volatility.

Including a standard deviation to calculate the volatility value itself is useless. It filters out 32% of the most volatile movements of the asset that you are observing.

Example of RHV:

Period of Volatility Value (POVV) : 10

Relative Historical Volatility : POVV / POVV*2

Historical Volatility of past 10 Bars is compared to the historical volatility of the bast 20 bars to show real growth/decrease of volatility relative to the time of the performing asset.

Comparing historical volatility to the current bar includes much more noise, the relative historical volatility can be perceived as a smoothed historical volatility ind.

Marginal notes:

Added standard deviations adjusted to the relative volatility value to predict probable future volatility of the stock.