Color Library: Rainbow Index & Simplest Return ColorLibrary "Color Library!"

To help with large projects that need colors!

If you guys make the library bigger, share it so we can all have tons of colors!

2 Functions

Uppercase and Lowercase, because why not?

import library as color

1.) color.this("Brown") // or color.this("brown") both work

2.) color.rainbow(1) //Returns first index of Rainbow

this(x)

TODO: color.this(Brown)

Parameters:

x : TODO: String Color Name

Returns: TODO: Color

rainbow(x)

TODO: Return Rainbow Index

Parameters:

x : TODO: Number is index of Rainbow :)

Returns: TODO: Color

Library

Binance_Min_Limit_Order_amount_libraryLibrary "Binance_Min_Limit_Order_amount_library"

TODO: This library give us the minimum Limit Order amount for the contract in Binance.

m_qty(n_v, m_fee, t_fee, cost, m_t)

TODO: it give us the Minimum Qty for the trading in Binance

Parameters:

n_v : TODO: min_notional_value. 5 dollar is the minimum notional amount in Binance at the moment.

m_fee : TODO: maker_fee %

t_fee : TODO: taker_fee %

cost : TODO: your investing money

m_t : TODO: if you want Limit_Order, put the "T", if you want Market_Order, put the "M" defval="M"

Returns: TODO: for the coin of binance on your chart,

Reference: www.binance.com

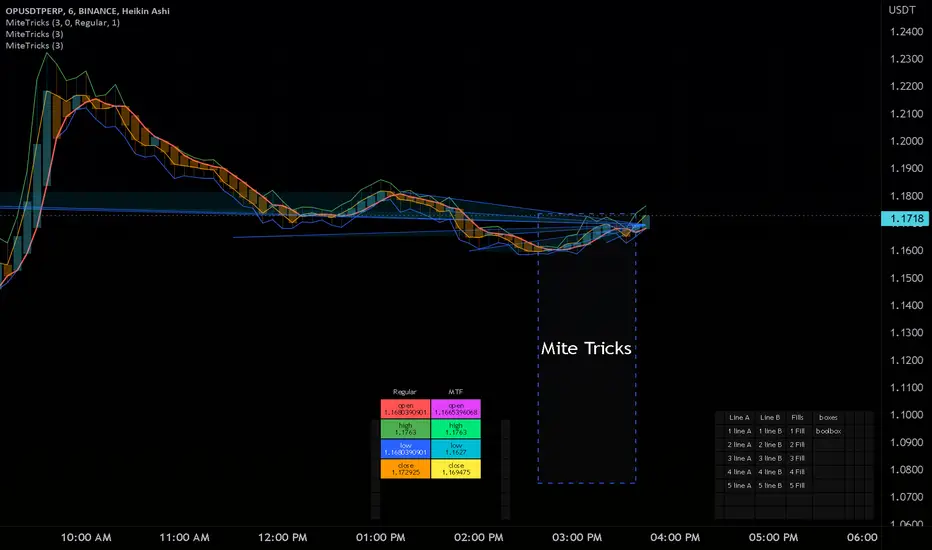

MiteTricksLibrary "MiteTricks"

Matrix Global Registry.

Get, Set, automatic growing, universal get/set,

multi-matrix dictionaries, multi-dictionary matrixes..

add slice matrixes of any type, share one common global key registry

pull up an item from a category, and item name ie a table of info.

same cell needs a color, a size, a string, a value, etc..

all of which can be pulled up with the same group id, and key id.

just swap which matrix you pull the value from.

this has a side benefit of non-repainting and recalculating

when pulling values, changing inputs..

makes for very fast/clean usage..

benefit :

floats = value

strings = names

lines = drawn items

table =table of data items for this key

colors = color for line/table/fill,label..

all of those can be pulled with "get(_VALUES,_groupIDX,_keyIDX)" where only the values matrix needs be swapped, and the same item/coordinates remains for all the possible matrixes that item appears in.

also useful as a dictionary/registry for any given type of item,,

and goes very handy with floats/strings/colors/bools with my matrixautotable

very helpful when prototyping or doing development work as a shortcut.

initRegistry()

Registry inititalizer

Returns: registry of string matrix type

newbool(optional, optional, optional)

create bool type new matrix presized 2x2 for reg

Parameters:

optional: row size

optional: column size

optional: fill value(default is bool (na)

Returns: bool matrix of specified size and fill, or blank 2x2 for registry use

newbox(optional, optional, optional)

create box type new matrix presized 2x2 for reg

Parameters:

optional: row size

optional: column size

optional: fill value(default is box (na)

Returns: box matrix of specified size and fill, or blank 2x2 for registry use

newcolor(optional, optional, optional)

create color type new matrix presized 2x2 for reg

Parameters:

optional: row size

optional: column size

optional: fill value(default is color (na)

Returns: color matrix of specified size and fill, or blank 2x2 for registry use

newfloat(optional, optional, optional)

create float type new matrix presized 2x2 for reg

Parameters:

optional: row size

optional: column size

optional: fill value(default is float (na)

Returns: float matrix of specified size and fill, or blank 2x2 for registry use

newint(optional, optional, optional)

create int type new matrix presized 2x2 for reg

Parameters:

optional: row size

optional: column size

optional: fill value(default is int (na)

Returns: int matrix of specified size and fill, or blank 2x2 for registry use

newlabel(optional, optional, optional)

create label type new matrix presized 2x2 for reg

Parameters:

optional: row size

optional: column size

optional: fill value(default is label (na)

Returns: label matrix of specified size and fill, or blank 2x2 for registry use

newline(optional, optional, optional)

create line type new matrix presized 2x2 for reg

Parameters:

optional: row size

optional: column size

optional: fill value(default is line (na)

Returns: line matrix of specified size and fill, or blank 2x2 for registry use

newlinefill(optional, optional, optional)

create linefill type new matrix presized 2x2 for reg

Parameters:

optional: row size

optional: column size

optional: fill value(default is linefill(na)

Returns: linefill matrix of specified size and fill, or blank 2x2 for registry use

newstring(optional, optional, optional)

create string type new matrix presized 2x2 for reg

Parameters:

optional: row size

optional: column size

optional: fill value(default is string (na)

Returns: string matrix of specified size and fill, or blank 2x2 for registry use

newtable(optional, optional, optional)

create table type new matrix presized 2x2 for reg

Parameters:

optional: row size

optional: column size

optional: fill value(default is table (na)

Returns: table matrix of specified size and fill, or blank 2x2 for registry use

newfrom(INIT_FILL)

newfrom Matrix full of item input

Parameters:

INIT_FILL: item to fill (2x2) the matri and set type. a type(na) works

addrow(m, v)

addrow Add new row to matrix

Parameters:

m: matrix of type being added to

v: value of type being added to ( best leave NA on string for registry purposes)

addcolumn(matrix, value)

addcolumn

Parameters:

matrix: of type being added to

value: of type being added to ( best leave NA on string for registry purposes)

get(_VALS, _KEYREG, _GROUP, _KEY)

get Grabs value and returns single item

Parameters:

_VALS: Matrix Values slice

_KEYREG: Registry values matrix (strings)

_GROUP: name of group/category or int group key

_KEY: name of item to fetch from value registry or int key id

Returns: item

get(_VALS, _GROUP, _KEY)

get Grabs value and returns single item

Parameters:

_VALS: Matrix Values slice

_GROUP: name of group/category

_KEY: name of item to fetch from value registry

getgid(_KEYREG, _GROUP)

getgid

Parameters:

_KEYREG: Reg to pull group id from

_GROUP: group index int, or string name to get the other missing type

getkid(_KEYREG, _GROUP, _KEY)

getkid

Parameters:

_KEYREG: Reg to pull Key id from

_GROUP: group index int, or string name

_KEY: index of string key id to get it's ID int

getkey(_KEYREG, _GROUP, _KEY)

getkey

Parameters:

_KEYREG: Reg to pull Key id from

_GROUP: group index int, or string name for getting key string

_KEY: index of string key id to get it's match of other type

set(_VALS, _KEYREG, _GROUP, _KEY, _value)

set items to reg and matrix container

Parameters:

_VALS: Values matrix container

_KEYREG: Key registry

_GROUP: (string) Group/Category name

_KEY: (string) Key for item

_value: item

Returns: void

del(_VALS, _KEYREG, _GROUP, _KEY)

del grroup id

Parameters:

_VALS: Matrix Values slice

_KEYREG: Registry values matrix (strings)

_GROUP: name of group/category

_KEY: name of item to Delete from values and key

detached(_GROUP, _KEY, _VALUE)

detached make detached registry/val matrix

Parameters:

_GROUP: Name of first group

_KEY: Name of first item

_VALUE: Item of any type, sets the output type too.

threengine_global_automation_libraryLibrary "threengine_global_automation_library"

A collection of functions used for trade automation

getBaseCurrency()

Gets the base currency for the chart's ticker. Supported trade pairs are USD, USDT, USDC, BTC, and PERP.

Returns: Base currency as a string

getChartSymbol()

Get the current chart's symbol without the base currency appended to it. Supported trade paris are USD, USDT, USDC, BTC, and PERP.

Returns: Ssymbol and base currency

getDecimals()

Calculates how many decimals are on the quote price of the current market

Returns: The current deimal places on the market quote price

checkVar()

Plot a string as a label on the chart to test variable value. Use str.tostring() for any variable that isn't a string.

Returns: Label with stringified variable

getStrategyAlertMessage()

Generates stringified JSON for a limit order that can be passed to the strategy alert_message for a long entry.

Returns: Stringifed JSON for a long entry

taGetAdx()

Calculates the Average Directional Index

Returns: The value of ADX as a float

taGetEma()

Calculates the EMA based on a type, source, and length. Supported types are EMA, SMA, RMA, and WMA.

Returns: The value of the selected EMA

isBetweenTwoTimes()

Checks to see if within a rage based on two times

@retunrs true/false boolean

getAllTradeIDs()

This gets all closed trades and open trades

@retunrs an array of all open and closed trade ID's

getOpenTradeIDs()

This gets all open trades

@retunrs an array of all open trade ID's

orderAlreadyExists()

This checks to see if a provided order id uses the getAllTradeIDs() function to check

@retunrs an array of all open and closed trade ID's

orderCurrentlyExists()

This checks to see if a provided order id uses the getAllTradeIDs() function to check

Returns: an array of all open and closed trade ID's

getContractCount()

calulates the number of contracts you can buy with a set amount of capital and a limit price

Returns: number of contracts you can buy based on amount of capital you want to use and a price

getLadderSteps()

Returns: array of ladder entry prices and amounts based on total amount you want to invest across all ladder rungs and either a range between ladderStart and LadderStop based on specificed number of ladderRungs OR ladderStart, ladderRungs, and LadderSpacingPercent

"Swap" - Bool/Position/Value : Array / Matrix / Var AutoswapLibrary "swap"

Side / Boundary Based All Types Swapper

- three automagical types for Arrays, Matrixes, and Variables

-- no signal : Long/ Short position autoswap

-- true / false : Boolean based side choice

-- Src / Thresh : if source is above or below the threshold

- two operating modes for variables, Holding mode only for arrays/matrixes

-- with two items, will automatically change between the two caveat is it does not delete table/box/line(fill VAR items automatically)

-- with three items, a neutral is available for NA input or neutral

- one function name for all of them. One import name that's easy to type/remember

-- make life easy for your conditional items.

side(source, thresh, _a, _b, _c)

side Change outputs based on position or a crossing level

Parameters:

source : (float) OPTIONAL value input

thresh : (float) OPTIONAL boundary line to cross

_a : (any) if Long/True/Above

_b : (any) if Short/False/Below

_c : (any) OPTIONAL NOT FOR MTX OR ARR... Neutral Item, if var/varip on a/b it will leave behind, ie, a table or box or line will not erase , if it's a varip you're sending in.

Returns: first, second, or third items based on input conditions

Please notify if bugs found.

Thanks.

fontilabLibrary "fontilab"

Provides function's indicators for pivot - trend - resistance.

pivots(src, lenght, isHigh) Detecting pivot points (and returning price + bar index.

Parameters:

src : The chart we analyse.

lenght : Used for the calcul.

isHigh : lookging for high if true, low otherwise.

Returns: The bar index and the price of the pivot.

calcDevThreshold(tresholdMultiplier, closePrice) Calculate deviation threshold for identifying major swings.

Parameters:

tresholdMultiplier : Usefull to equilibrate the calculate.

closePrice : Close price of the chart wanted.

Returns: The deviation threshold.

calcDev(basePrice, price) Custom function for calculating price deviation for validating large moves.

Parameters:

basePrice : The reference price.

price : The price tested.

Returns: The deviation.

pivotFoundWithLines(dev, isHigh, index, price, dev_threshold, isHighLast, pLast, iLast, lineLast) Detecting pivots that meet our deviation criteria.

Parameters:

dev : The deviation wanted.

isHigh : The type of pivot tested (high or low).

index : The Index of the pivot tested.

price : The chart price wanted.

dev_threshold : The deviation treshold.

isHighLast : The type of last pivot.

pLast : The pivot price last.

iLast : Index of the last pivot.

lineLast : The lst line.

Returns: The Line and bool is pivot High.

getDeviationPivots(thresholdMultiplier, depth, lineLast, isHighLast, iLast, pLast, deleteLines, closePrice, highPrice, lowPrice) Get pivot that meet our deviation criteria.

Parameters:

thresholdMultiplier : The treshold multiplier.

depth : The depth to calculate pivot.

lineLast : The last line.

isHighLast : The type of last pivot

iLast : Index of the last pivot.

pLast : The pivot price last.

deleteLines : If the line are draw or not.

closePrice : The chart close price.

highPrice : The chart high price.

lowPrice : The chart low price.

Returns: All pivot the informations.

getElIntArrayFromEnd() Get the last element of an int array.

getElFloatArrayFromEnd() Get the last element of an float array.

getElBoolArrayFromEnd() Get the last element of a bool array.

isTrendContinuation(isTrendUp, arrayBounds, lastPrice, precision) Check if last price is between bounds array.

Parameters:

isTrendUp : Is actual trend up.

arrayBounds : The trend array.

lastPrice : The pivot Price that just be found.

precision : The percent we add to actual bounds to validate a move.

Returns: na if price is between bounds, true if continuation, false if not.

getTrendPivots(trendBarIndexes, trendPrices, trendPricesIsHigh, interBarIndexes, interPrices, interPricesIsHigh, isTrendHesitate, isTrendUp, trendPrecision, pLast, iLast, isHighLast) Function to update array and trend related to pivot trend interpretation.

Parameters:

trendBarIndexes : The array trend bar index.

trendPrices : The array trend price.

trendPricesIsHigh : The array trend is high.

interBarIndexes : The array inter bar index.

interPrices : The array inter price.

interPricesIsHigh : The array inter ishigh.

isTrendHesitate : The actual status of is trend hesitate.

isTrendUp : The actual status of is trend up.

trendPrecision : The var precision to add in "iscontinuation" function.

pLast : The last pivot price.

iLast : The last pivot bar index.

isHighLast : The last pivot "isHigh".

Returns: trend & inter arrays, is trend hesitate, is trend up.

drawBoundLines(startIndex, startPrice, endIndex, endPrice, breakingPivotIndex, breakingPivotPrice, isTrendUp) Draw bounds and breaking line of the trend.

Parameters:

startIndex : Index of the first bound line.

startPrice : Price of first bound line.

endIndex : Index of second bound line.

endPrice : price of second bound line.

breakingPivotIndex : The breaking line index.

breakingPivotPrice : The breaking line price.

isTrendUp : The actual status of the trend.

Returns: The lines bounds and breaking line.

merge_pinbarLibrary "merge_pinbar"

merge_pinbar: merge bars and check whether the bar is a pinbar

merge_pinbar(simple, simple) merge_pinbar: merge bars and check whether the bar is a pinbar

Parameters:

simple : int period: the statistic bar period

simple : int max_bars: the max bars to be merged

Returns: array:

Timed_exit_alert_for_webhookLibrary "Timed_exit_alert_for_webhook"

TODO: add library description here

fun(x) TODO: add function description here

Parameters:

x : TODO: add parameter x description here

Returns: TODO: add what function returns

for exiting FCM like Tradovate and AMP using API and python MT5 and Webhooks

the writer take no responsibility for trades made using this script its written for informational purposes only

adx: Configurable ADX (library) Library "adx"

Calculate ADX (and its constituent parts +DI, -DI, ATR),

using different moving averages and periods.

adx(atrMA, diMA, adxMA, atrLen, diLen, adxLen, h, l, c)

Parameters:

atrMA : Moving Average used for calculating the Average True Range.

Traditionally RMA, but using SMA here and in adxMA gives good results too.

diMA : Moving Average used for calculating the Directional Index.

Traditionally, RMA.

adxMA : Moving Average used for calculating the Average Directional

Index. Traditionally RMA, but using SMA here and in atrMA gives good results

too.

atrLen : Length of the Average True Range.

diLen : Length of the Directional Index.

adxLen : Length (smoothing) of the Average Directional Index.

h : Candle's high.

l : Candle's low.

c : Candle's close.

Returns:

statisticsLibrary "statistics"

General statistics library.

erf(x) The "error function" encountered in integrating the normal

distribution (which is a normalized form of the Gaussian function).

Parameters:

x : The input series.

Returns: The Error Function evaluated for each element of x.

erfc(x)

Parameters:

x : The input series

Returns: The Complementary Error Function evaluated for each alement of x.

sumOfReciprocals(src, len) Calculates the sum of the reciprocals of the series.

For each element 'elem' in the series:

sum += 1/elem

Should the element be 0, the reciprocal value of 0 is used instead

of NA.

Parameters:

src : The input series.

len : The length for the sum.

Returns: The sum of the resciprocals of 'src' for 'len' bars back.

mean(src, len) The mean of the series.

(wrapper around ta.sma).

Parameters:

src : The input series.

len : The length for the mean.

Returns: The mean of 'src' for 'len' bars back.

average(src, len) The mean of the series.

(wrapper around ta.sma).

Parameters:

src : The input series.

len : The length for the average.

Returns: The average of 'src' for 'len' bars back.

geometricMean(src, len) The Geometric Mean of the series.

The geometric mean is most important when using data representing

percentages, ratios, or rates of change. It cannot be used for

negative numbers

Since the pure mathematical implementation generates a very large

intermediate result, we performed the calculation in log space.

Parameters:

src : The input series.

len : The length for the geometricMean.

Returns: The geometric mean of 'src' for 'len' bars back.

harmonicMean(src, len) The Harmonic Mean of the series.

The harmonic mean is most applicable to time changes and, along

with the geometric mean, has been used in economics for price

analysis. It is more difficult to calculate; therefore, it is less

popular than eiter of the other averages.

0 values are ignored in the calculation.

Parameters:

src : The input series.

len : The length for the harmonicMean.

Returns: The harmonic mean of 'src' for 'len' bars back.

median(src, len) The median of the series.

(a wrapper around ta.median)

Parameters:

src : The input series.

len : The length for the median.

Returns: The median of 'src' for 'len' bars back.

variance(src, len, biased) The variance of the series.

Parameters:

src : The input series.

len : The length for the variance.

biased : Wether to use the biased calculation (for a population), or the

unbiased calculation (for a sample set). .

Returns: The variance of 'src' for 'len' bars back.

stdev(src, len, biased) The standard deviation of the series.

Parameters:

src : The input series.

len : The length for the stdev.

biased : Wether to use the biased calculation (for a population), or the

unbiased calculation (for a sample set). .

Returns: The standard deviation of 'src' for 'len' bars back.

skewness(src, len) The skew of the series.

Skewness measures the amount of distortion from a symmetric

distribution, making the curve appear to be short on the left

(lower prices) and extended to the right (higher prices). The

extended side, either left or right is called the tail, and a

longer tail to the right is called positive skewness. Negative

skewness has the tail extending towards the left.

Parameters:

src : The input series.

len : The length for the skewness.

Returns: The skewness of 'src' for 'len' bars back.

kurtosis(src, len) The kurtosis of the series.

Kurtosis describes the peakedness or flatness of a distribution.

This can be used as an unbiased assessment of whether prices are

trending or moving sideways. Trending prices will ocver a wider

range and thus a flatter distribution (kurtosis < 3; negative

kurtosis). If prices are range-bound, there will be a clustering

around the mean and we have positive kurtosis (kurtosis > 3)

Parameters:

src : The input series.

len : The length for the kurtosis.

Returns: The kurtosis of 'src' for 'len' bars back.

excessKurtosis(src, len) The normalized kurtosis of the series.

kurtosis > 0 --> positive kurtosis --> trending

kurtosis < 0 --> negative krutosis --> range-bound

Parameters:

src : The input series.

len : The length for the excessKurtosis.

Returns: The excessKurtosis of 'src' for 'len' bars back.

normDist(src, len, value) Calculates the probability mass for the value according to the

src and length. It calculates the probability for value to be

present in the normal distribution calculated for src and length.

Parameters:

src : The input series.

len : The length for the normDist.

value : The series of values to calculate the normal distance for

Returns: The normal distance of 'value' to 'src' for 'len' bars back.

normDistCumulative(src, len, value) Calculates the cumulative probability mass for the value according

to the src and length. It calculates the cumulative probability for

value to be present in the normal distribution calculated for src

and length.

Parameters:

src : The input series.

len : The length for the normDistCumulative.

value : The series of values to calculate the cumulative normal distance

for

Returns: The cumulative normal distance of 'value' to 'src' for 'len' bars

back.

zScore(src, len, value) Returns then z-score of objective to the series src.

It returns the number of stdev's the objective is away from the

mean(src, len)

Parameters:

src : The input series.

len : The length for the zScore.

value : The series of values to calculate the cumulative normal distance

for

Returns: The z-score of objectiv with respect to src and len.

er(src, len) Calculates the efficiency ratio of the series.

It measures the noise of the series. The lower the number, the

higher the noise.

Parameters:

src : The input series.

len : The length for the efficiency ratio.

Returns: The efficiency ratio of 'src' for 'len' bars back.

efficiencyRatio(src, len) Calculates the efficiency ratio of the series.

It measures the noise of the series. The lower the number, the

higher the noise.

Parameters:

src : The input series.

len : The length for the efficiency ratio.

Returns: The efficiency ratio of 'src' for 'len' bars back.

fractalEfficiency(src, len) Calculates the efficiency ratio of the series.

It measures the noise of the series. The lower the number, the

higher the noise.

Parameters:

src : The input series.

len : The length for the efficiency ratio.

Returns: The efficiency ratio of 'src' for 'len' bars back.

mse(src, len) Calculates the Mean Squared Error of the series.

Parameters:

src : The input series.

len : The length for the mean squared error.

Returns: The mean squared error of 'src' for 'len' bars back.

meanSquaredError(src, len) Calculates the Mean Squared Error of the series.

Parameters:

src : The input series.

len : The length for the mean squared error.

Returns: The mean squared error of 'src' for 'len' bars back.

rmse(src, len) Calculates the Root Mean Squared Error of the series.

Parameters:

src : The input series.

len : The length for the root mean squared error.

Returns: The root mean squared error of 'src' for 'len' bars back.

rootMeanSquaredError(src, len) Calculates the Root Mean Squared Error of the series.

Parameters:

src : The input series.

len : The length for the root mean squared error.

Returns: The root mean squared error of 'src' for 'len' bars back.

mae(src, len) Calculates the Mean Absolute Error of the series.

Parameters:

src : The input series.

len : The length for the mean absolute error.

Returns: The mean absolute error of 'src' for 'len' bars back.

meanAbsoluteError(src, len) Calculates the Mean Absolute Error of the series.

Parameters:

src : The input series.

len : The length for the mean absolute error.

Returns: The mean absolute error of 'src' for 'len' bars back.

CRCHud - HUD Library (Heads Up Display)Library "CRCHud"

Library of functions which will contain functions that allow reusable HUD (Heads up Display) components to used from within other scripts

add_cell_change() - Adds a new cell to designated table which displays the data source value, the line color, data title, and automatically calculated %percent change stats based on lookback value supplied (default - previous bar)

Punchline_LibLibrary "Punchline_Lib"

roundSmart(float) Truncates decimal points of a float value based on the amount of digits before the decimal point

Parameters:

float : _value any number

Returns: float

tostring_smart(float) converts a float to a string, intelligently cutting off decimal points

Parameters:

float : _value any number

Returns: string

The Divergent LibraryLibrary "TheDivergentLibrary"

The Divergent Library is only useful when combined with the Pro version of The Divergent - Advanced divergence indicator . This is because the Basic (free) version of The Divergent does not expose the "Divergence Signal" value.

Usage instructions:

1. Create a new chart

2. Add The Divergent (Pro) indicator to your chart

3. Create a new strategy, import this library, add a "source" input, link it to "The Divergent: Divergence Signal", and use the library to decode the divergence signals from The Divergent (You can find example strategy code published in our profile)

4. Act on the divergences signalled by The Divergent

---

isRegularBullishEnabled(context) Returns a boolean value indicating whether Regular Bullish divergence detection is enabled in The Divergent.

Parameters:

context : The context of The Divergent Library.

Returns: A boolean value indicating whether Regular Bullish divergence detection is enabled in The Divergent.

isHiddenBullishEnabled(context) Returns a boolean value indicating whether Hidden Bullish divergence detection is enabled in The Divergent.

Parameters:

context : The context of The Divergent Library.

Returns: A boolean value indicating whether Hidden Bullish divergence detection is enabled in The Divergent.

isRegularBearishEnabled(context) Returns a boolean value indicating whether Regular Bearish divergence detection is enabled in The Divergent.

Parameters:

context : The context of The Divergent Library.

Returns: A boolean value indicating whether Regular Bearish divergence detection is enabled in The Divergent.

isHiddenBearishEnabled(context) Returns a boolean value indicating whether Hidden Bearish divergence detection is enabled in The Divergent.

Parameters:

context : The context of The Divergent Library.

Returns: A boolean value indicating whether Hidden Bearish divergence detection is enabled in The Divergent.

getPivotDetectionSource(context) Returns the 'Pivot Detection Source' setting of The Divergent. The returned value can be either "Oscillator" or "Price".

Parameters:

context : The context of The Divergent Library.

Returns: One of the following string values: "Oscillator" or "Price".

getPivotDetectionMode(context) Returns the 'Pivot Detection Mode' setting of The Divergent. The returned value can be either "Bodies" or "Wicks".

Parameters:

context : The context of The Divergent Library.

Returns: One of the following string values: "Bodies" or "Wicks".

isLinked(context) Returns a boolean value indicating the link status to The Divergent indicator.

Parameters:

context : The context of The Divergent Library.

Returns: A boolean value indicating the link status to The Divergent indicator.

init(firstBarSignal, displayLinkStatus, debug) Initialises The Divergent Library's context with the signal produced by The Divergent on the first bar. The value returned from this function is called the "context of The Divergent Library". Some of the other functions of this library requires you to pass in this context.

Parameters:

firstBarSignal : The signal from The Divergent indicator on the first bar.

displayLinkStatus : A boolean value indicating whether the Link Status window should be displayed in the bottom left corner of the chart. Defaults to true.

debug : A boolean value indicating whether the Link Status window should display debug information. Defaults to false.

Returns: A bool array containing the context of The Divergent Library.

processSignal(signal) Processes a signal from The Divergent and returns a 5-tuple with the decoded signal: [ int divergenceType, int priceBarIndexStart, int priceBarIndexEnd, int oscillatorBarIndexStart, int oscillatorBarIndexEnd]. `divergenceType` can be one of the following values: na → No divergence was detected, 1 → Regular Bullish, 2 → Regular Bullish early, 3 → Hidden Bullish, 4 → Hidden Bullish early, 5 → Regular Bearish, 6 → Regular Bearish early, 7 → Hidden Bearish, 8 → Hidden Bearish early.

Parameters:

signal : The signal from The Divergent indicator.

Returns: A 5-tuple with the following values: [ int divergenceType, int priceBarIndexStart, int priceBarIndexEnd, int oscillatorBarIndexStart, int oscillatorBarIndexEnd].

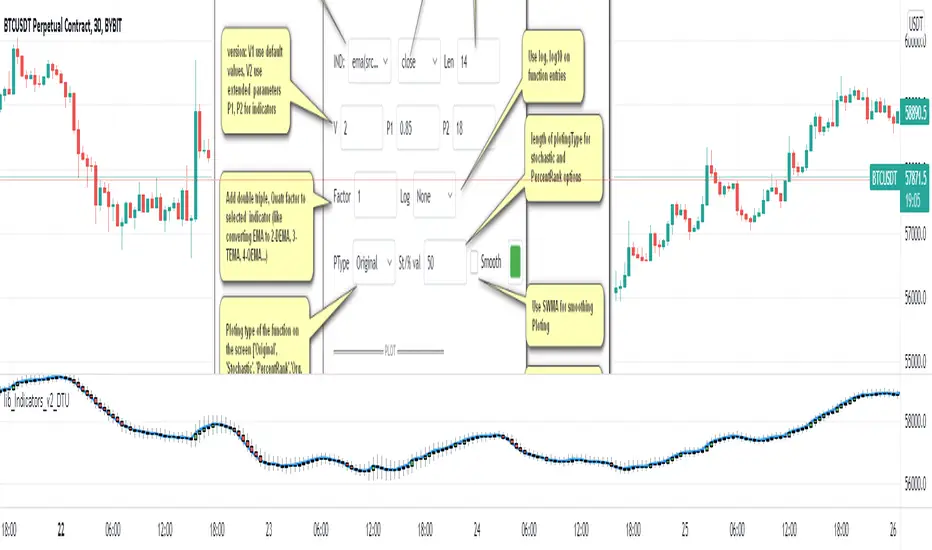

lib_Indicators_v2_DTULibrary "lib_Indicators_v2_DTU"

This library functions returns included Moving averages, indicators with factorization, functions candles, function heikinashi and more.

Created it to feed as backend of my indicator/strategy "Indicators & Combinations Framework Advanced v2 " that will be released ASAP.

This is replacement of my previous indicator (lib_indicators_DT)

I will add an indicator example which will use this indicator named as "lib_indicators_v2_DTU example" to help the usage of this library

Additionally library will be updated with more indicators in the future

NOTES:

Indicator functions returns only one series :-(

plotcandle function returns candle series

INDICATOR LIST:

hide = 'DONT DISPLAY', //Dont display & calculate the indicator. (For my framework usage)

alma = 'alma(src,len,offset=0.85,sigma=6)', //Arnaud Legoux Moving Average

ama = 'ama(src,len,fast=14,slow=100)', //Adjusted Moving Average

acdst = 'accdist()', //Accumulation/distribution index.

cma = 'cma(src,len)', //Corrective Moving average

dema = 'dema(src,len)', //Double EMA (Same as EMA with 2 factor)

ema = 'ema(src,len)', //Exponential Moving Average

gmma = 'gmma(src,len)', //Geometric Mean Moving Average

hghst = 'highest(src,len)', //Highest value for a given number of bars back.

hl2ma = 'hl2ma(src,len)', //higest lowest moving average

hma = 'hma(src,len)', //Hull Moving Average.

lgAdt = 'lagAdapt(src,len,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter

lgAdV = 'lagAdaptV(src,len,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter variation

lguer = 'laguerre(src,len)', //Ehler's Laguerre filter

lsrcp = 'lesrcp(src,len)', //lowest exponential esrcpanding moving line

lexp = 'lexp(src,len)', //lowest exponential expanding moving line

linrg = 'linreg(src,len,loffset=1)', //Linear regression

lowst = 'lowest(src,len)', //Lovest value for a given number of bars back.

pcnl = 'percntl(src,len)', //percentile nearest rank. Calculates percentile using method of Nearest Rank.

pcnli = 'percntli(src,len)', //percentile linear interpolation. Calculates percentile using method of linear interpolation between the two nearest ranks.

rema = 'rema(src,len)', //Range EMA (REMA)

rma = 'rma(src,len)', //Moving average used in RSI. It is the exponentially weighted moving average with alpha = 1 / length.

sma = 'sma(src,len)', //Smoothed Moving Average

smma = 'smma(src,len)', //Smoothed Moving Average

supr2 = 'super2(src,len)', //Ehler's super smoother, 2 pole

supr3 = 'super3(src,len)', //Ehler's super smoother, 3 pole

strnd = 'supertrend(src,len,period=3)', //Supertrend indicator

swma = 'swma(src,len)', //Sine-Weighted Moving Average

tema = 'tema(src,len)', //Triple EMA (Same as EMA with 3 factor)

tma = 'tma(src,len)', //Triangular Moving Average

vida = 'vida(src,len)', //Variable Index Dynamic Average

vwma = 'vwma(src,len)', //Volume Weigted Moving Average

wma = 'wma(src,len)', //Weigted Moving Average

angle = 'angle(src,len)', //angle of the series (Use its Input as another indicator output)

atr = 'atr(src,len)', //average true range. RMA of true range.

bbr = 'bbr(src,len,mult=1)', //bollinger %%

bbw = 'bbw(src,len,mult=2)', //Bollinger Bands Width. The Bollinger Band Width is the difference between the upper and the lower Bollinger Bands divided by the middle band.

cci = 'cci(src,len)', //commodity channel index

cctbb = 'cctbbo(src,len)', //CCT Bollinger Band Oscilator

chng = 'change(src,len)', //Difference between current value and previous, source - source .

cmo = 'cmo(src,len)', //Chande Momentum Oscillator. Calculates the difference between the sum of recent gains and the sum of recent losses and then divides the result by the sum of all price movement over the same period.

cog = 'cog(src,len)', //The cog (center of gravity) is an indicator based on statistics and the Fibonacci golden ratio.

cpcrv = 'copcurve(src,len)', //Coppock Curve. was originally developed by Edwin "Sedge" Coppock (Barron's Magazine, October 1962).

corrl = 'correl(src,len)', //Correlation coefficient. Describes the degree to which two series tend to deviate from their ta.sma values.

count = 'count(src,len)', //green avg - red avg

dev = 'dev(src,len)', //ta.dev() Measure of difference between the series and it's ta.sma

fall = 'falling(src,len)', //ta.falling() Test if the `source` series is now falling for `length` bars long. (Use its Input as another indicator output)

kcr = 'kcr(src,len,mult=2)', //Keltner Channels Range

kcw = 'kcw(src,len,mult=2)', //ta.kcw(). Keltner Channels Width. The Keltner Channels Width is the difference between the upper and the lower Keltner Channels divided by the middle channel.

macd = 'macd(src,len)', //macd

mfi = 'mfi(src,len)', //Money Flow Index

nvi = 'nvi()', //Negative Volume Index

obv = 'obv()', //On Balance Volume

pvi = 'pvi()', //Positive Volume Index

pvt = 'pvt()', //Price Volume Trend

rise = 'rising(src,len)', //ta.rising() Test if the `source` series is now rising for `length` bars long. (Use its Input as another indicator output)

roc = 'roc(src,len)', //Rate of Change

rsi = 'rsi(src,len)', //Relative strength Index

smosc = 'smi_osc(src,len,fast=5, slow=34)', //smi Oscillator

smsig = 'smi_sig(src,len,fast=5, slow=34)', //smi Signal

stdev = 'stdev(src,len)', //Standart deviation

trix = 'trix(src,len)' , //the rate of change of a triple exponentially smoothed moving average.

tsi = 'tsi(src,len)', //True Strength Index

vari = 'variance(src,len)', //ta.variance(). Variance is the expectation of the squared deviation of a series from its mean (ta.sma), and it informally measures how far a set of numbers are spread out from their mean.

wilpc = 'willprc(src,len)', //Williams %R

wad = 'wad()', //Williams Accumulation/Distribution.

wvad = 'wvad()' //Williams Variable Accumulation/Distribution.

}

f_func(string, float, simple, float, float, float, simple) f_func Return selected indicator value with different parameters. New version. Use extra parameters for available indicators

Parameters:

string : FuncType_ indicator from the indicator list

float : src_ close, open, high, low,hl2, hlc3, ohlc4 or any

simple : int length_ indicator length

float : p1 extra parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 extra parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 extra parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

Returns: float Return calculated indicator value

fn_heikin(float, float, float, float) fn_heikin Return given src data (open, high,low,close) as heikin ashi candle values

Parameters:

float : o_ open value

float : h_ high value

float : l_ low value

float : c_ close value

Returns: float heikin ashi open, high,low,close vlues that will be used with plotcandle

fn_plotFunction(float, string, simple, bool) fn_plotFunction Return input src data with different plotting options

Parameters:

float : src_ indicator src_data or any other series.....

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

Returns: float

fn_funcPlotV2(string, float, simple, float, float, float, simple, string, simple, bool, bool) fn_funcPlotV2 Return selected indicator value with different parameters. New version. Use extra parameters fora available indicators

Parameters:

string : FuncType_ indicator from the indicator list

float : src_data_ close, open, high, low,hl2, hlc3, ohlc4 or any

simple : int length_ indicator length

float : p1 extra parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 extra parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 extra parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

bool : log_ Use log on function entries

Returns: float Return calculated indicator value

fn_factor(string, float, simple, float, float, float, simple, simple, string, simple, bool, bool) fn_factor Return selected indicator's factorization with given arguments

Parameters:

string : FuncType_ indicator from the indicator list

float : src_data_ close, open, high, low,hl2, hlc3, ohlc4 or any

simple : int length_ indicator length

float : p1 parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

simple : int fact_ Add double triple, Quatr factor to selected indicator (like converting EMA to 2-DEMA, 3-TEMA, 4-QEMA...)

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

bool : log_ Use log on function entries

Returns: float Return result of the function

fn_plotCandles(string, simple, float, float, float, simple, string, simple, bool, bool, bool) fn_plotCandles Return selected indicator's candle values with different parameters also heikinashi is available

Parameters:

string : FuncType_ indicator from the indicator list

simple : int length_ indicator length

float : p1 parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

bool : log_ Use log on function entries

bool : plotheikin_ Use Heikin Ashi on Plot

Returns: float

FunctionZigZagMultipleMethodsLibrary "FunctionZigZagMultipleMethods"

ZigZag Multiple Methods.

method(idx) Helper methods enumeration.

Parameters:

idx : int, index of method, range 0 to 4.

Returns: string

function(method, value_x, value_y) Multiple method ZigZag.

Parameters:

method : string, default='(MANUAL) Percent price move over X * Y', method for zigzag.

value_x : float, x value in method.

value_y : float, y value in method.

Returns: tuple with:

zigzag float

direction

reverse_line float

realtimeofpivot int

GenericTradingLibrary "GenericTrading"

This library aims to collect rare but useful operations for

get_most_recent_long_or_short_position_closed_index() : returns most recent long/short closed bar index.

get_most_recent_long_or_short_position_open_index() : returns most recent long/short closed bar index.

These two functions designed to help to speed up the coding for strategies that contains "re-enter" logic.

These two functions also could applies in the situations where time-count is needed in your condition.

lib_Indicators_DTLibrary "lib_Indicators_DT"

This library functions returns some Moving averages and indicators.

Created it to feed my indicator/strategy "INDICATOR & CONDITIONS COMBINATOR FRAMEWORK v1 " which I will publish it as soon as possible.

Credits: Library includes some public indicators, snippets from tradingview & @03.freeman's ("All MAs displayed") scripts.

(I hope, I dont break Tradingview's House Rules on Script Publishing)

f_plotPrep(src_, src_, src_, src_) Prepare Indicator Plot Type

Parameters:

src_ : Source

src_ : plotingType_ "Original, Stochastic, Percent"

src_ : stochlen_ Stochasting plottingtype length

src_ : plotSWMA_ Use SWMA for the output

Returns: Return the prepared indicator

f_funcPlot(string, float, simple, string, simple, bool) f_funcPlot(string f, float src_, simple int length_, string plotingType_ = "Original", simple int stochlen_=50, bool plotSWMA=false) Return selected indicator value with different parameters

Parameters:

string : f indicator-> options=

float : src_ close,open.....

simple : int length_ indicator length

string : plotingType return param-> options= ['Original', 'Stochastic', 'PercentRank')

simple : int stochlen_ length for return Param

bool : plotSWMA Use SWMA on Plot

Returns: float

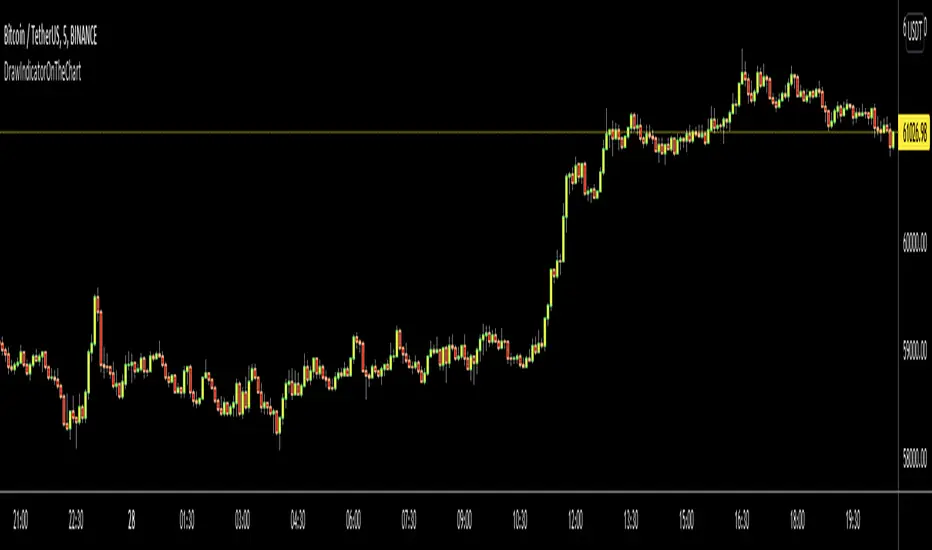

DrawIndicatorOnTheChartLibrary "DrawIndicatorOnTheChart"

this library is used to show an indicator (such RSI, CCI, MOM etc) on the main chart with indicator's horizontal lines in a window. Location of the window is calculated dynamically by last price movemements

drawIndicator(indicatorName, indicator, indicatorcolor, period, indimax_, indimin_, levels, precision, xlocation) draws the related indicator on the chart

Parameters:

indicatorName : is the indicator name as string such "RSI", "CCI" etc

indicator : is the indicator you want to show, such rsi(close, 14), mom(close, 10) etc

indicatorcolor : is the color of indicator line

period : is the length of the window to show

indimax_ : is the maximum value of the indicator, for example for RSI it's 100.0, if the indicator (such CCI, MOM etc) doesn't have maximum value then use "na"

indimin_ : is the minimum value of the indicator, for example for RSI it's 0.0, if the indicator (such CCI, MOM etc)doesn't have maximum value then use "na"

levels : is the levels of the array for the horizontal lines. for example if you want horizontal lines at 30.0, and 70.0 then use array.from(30.0, 70.0). if no horizontal lines then use array.from(na)

precision : is the precision/number of decimals that is used to show indicator values, for example for RSI set it 2

xlocation : is end location of the indicator window, for example if xlocation = 0 window is created on the index of the last bar/candle

Returns: none

ZenLibraryLibrary "ZenLibrary"

A collection of custom tools & utility functions commonly used with my scripts.

getDecimals() Calculates how many decimals are on the quote price of the current market

Returns: The current decimal places on the market quote price

truncate(float, float) Truncates (cuts) excess decimal places

Parameters:

float : _number The number to truncate

float : _decimalPlaces (default=2) The number of decimal places to truncate to

Returns: The given _number truncated to the given _decimalPlaces

toWhole(float) Converts pips into whole numbers

Parameters:

float : _number The pip number to convert into a whole number

Returns: The converted number

toPips(float) Converts whole numbers back into pips

Parameters:

float : _number The whole number to convert into pips

Returns: The converted number

av_getPositionSize(float, float, float, float) Calculates OANDA forex position size for AutoView based on the given parameters

Parameters:

float : _balance The account balance to use

float : _risk The risk percentage amount (as a whole number - eg. 1 = 1% risk)

float : _stopPoints The stop loss distance in POINTS (not pips)

float : _conversionRate The conversion rate of our account balance currency

Returns: The calculated position size (in units - only compatible with OANDA)

getMA(int, string) Gets a Moving Average based on type

Parameters:

int : _length The MA period

string : _maType The type of MA

Returns: A moving average with the given parameters

getEAP(float) Performs EAP stop loss size calculation (eg. ATR >= 20.0 and ATR < 30, returns 20)

Parameters:

float : _atr The given ATR to base the EAP SL calculation on

Returns: The EAP SL converted ATR size

barsAboveMA(int, float) Counts how many candles are above the MA

Parameters:

int : _lookback The lookback period to look back over

float : _ma The moving average to check

Returns: The bar count of how many recent bars are above the MA

barsBelowMA(int, float) Counts how many candles are below the MA

Parameters:

int : _lookback The lookback period to look back over

float : _ma The moving average to reference

Returns: The bar count of how many recent bars are below the EMA

barsCrossedMA(int, float) Counts how many times the EMA was crossed recently

Parameters:

int : _lookback The lookback period to look back over

float : _ma The moving average to reference

Returns: The bar count of how many times price recently crossed the EMA

getPullbackBarCount(int, int) Counts how many green & red bars have printed recently (ie. pullback count)

Parameters:

int : _lookback The lookback period to look back over

int : _direction The color of the bar to count (1 = Green, -1 = Red)

Returns: The bar count of how many candles have retraced over the given lookback & direction

getBodySize() Gets the current candle's body size (in POINTS, divide by 10 to get pips)

Returns: The current candle's body size in POINTS

getTopWickSize() Gets the current candle's top wick size (in POINTS, divide by 10 to get pips)

Returns: The current candle's top wick size in POINTS

getBottomWickSize() Gets the current candle's bottom wick size (in POINTS, divide by 10 to get pips)

Returns: The current candle's bottom wick size in POINTS

getBodyPercent() Gets the current candle's body size as a percentage of its entire size including its wicks

Returns: The current candle's body size percentage

isHammer(float, bool) Checks if the current bar is a hammer candle based on the given parameters

Parameters:

float : _fib (default=0.382) The fib to base candle body on

bool : _colorMatch (default=false) Does the candle need to be green? (true/false)

Returns: A boolean - true if the current bar matches the requirements of a hammer candle

isStar(float, bool) Checks if the current bar is a shooting star candle based on the given parameters

Parameters:

float : _fib (default=0.382) The fib to base candle body on

bool : _colorMatch (default=false) Does the candle need to be red? (true/false)

Returns: A boolean - true if the current bar matches the requirements of a shooting star candle

isDoji(float, bool) Checks if the current bar is a doji candle based on the given parameters

Parameters:

float : _wickSize (default=2) The maximum top wick size compared to the bottom (and vice versa)

bool : _bodySize (default=0.05) The maximum body size as a percentage compared to the entire candle size

Returns: A boolean - true if the current bar matches the requirements of a doji candle

isBullishEC(float, float, bool) Checks if the current bar is a bullish engulfing candle

Parameters:

float : _allowance (default=0) How many POINTS to allow the open to be off by (useful for markets with micro gaps)

float : _rejectionWickSize (default=disabled) The maximum rejection wick size compared to the body as a percentage

bool : _engulfWick (default=false) Does the engulfing candle require the wick to be engulfed as well?

Returns: A boolean - true if the current bar matches the requirements of a bullish engulfing candle

isBearishEC(float, float, bool) Checks if the current bar is a bearish engulfing candle

Parameters:

float : _allowance (default=0) How many POINTS to allow the open to be off by (useful for markets with micro gaps)

float : _rejectionWickSize (default=disabled) The maximum rejection wick size compared to the body as a percentage

bool : _engulfWick (default=false) Does the engulfing candle require the wick to be engulfed as well?

Returns: A boolean - true if the current bar matches the requirements of a bearish engulfing candle

timeFilter(string, bool) Determines if the current price bar falls inside the specified session

Parameters:

string : _sess The session to check

bool : _useFilter (default=false) Whether or not to actually use this filter

Returns: A boolean - true if the current bar falls within the given time session

dateFilter(int, int) Determines if this bar's time falls within date filter range

Parameters:

int : _startTime The UNIX date timestamp to begin searching from

int : _endTime the UNIX date timestamp to stop searching from

Returns: A boolean - true if the current bar falls within the given dates

dayFilter(bool, bool, bool, bool, bool, bool, bool) Checks if the current bar's day is in the list of given days to analyze

Parameters:

bool : _monday Should the script analyze this day? (true/false)

bool : _tuesday Should the script analyze this day? (true/false)

bool : _wednesday Should the script analyze this day? (true/false)

bool : _thursday Should the script analyze this day? (true/false)

bool : _friday Should the script analyze this day? (true/false)

bool : _saturday Should the script analyze this day? (true/false)

bool : _sunday Should the script analyze this day? (true/false)

Returns: A boolean - true if the current bar's day is one of the given days

atrFilter(float, float) Checks the current bar's size against the given ATR and max size

Parameters:

float : _atr (default=ATR 14 period) The given ATR to check

float : _maxSize The maximum ATR multiplier of the current candle

Returns: A boolean - true if the current bar's size is less than or equal to _atr x _maxSize

fillCell(table, int, int, string, string, color, color) This updates the given table's cell with the given values

Parameters:

table : _table The table ID to update

int : _column The column to update

int : _row The row to update

string : _title The title of this cell

string : _value The value of this cell

color : _bgcolor The background color of this cell

color : _txtcolor The text color of this cell

Returns: A boolean - true if the current bar falls within the given dates

Bursa_SectorLibrary "Bursa_Sector"

: List of stocks classified by sector in Bursa Malaysia (As of Oct 2021)

getSector()

This function will get the sector of current stock that listed in Bursa Malaysia

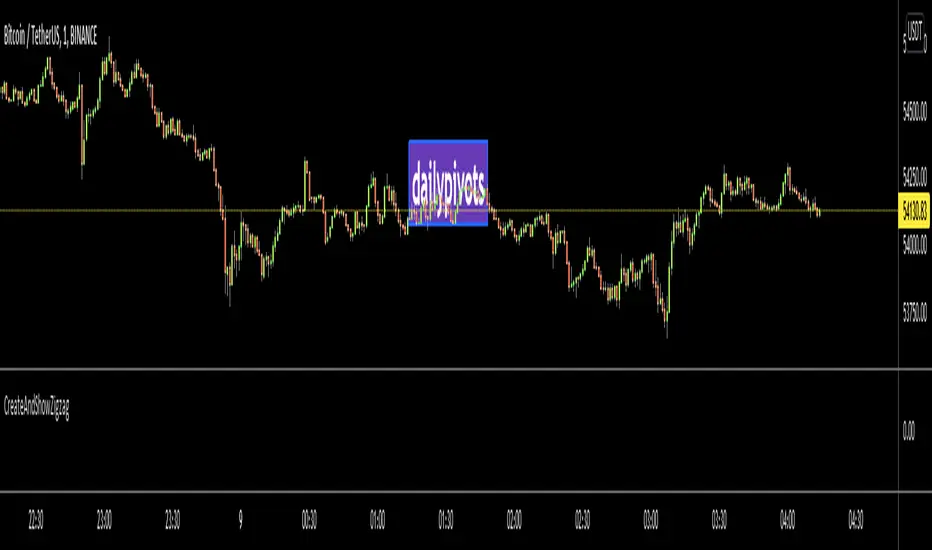

CreateAndShowZigzagLibrary "CreateAndShowZigzag"

Functions in this library creates/updates zigzag array and shows the zigzag

getZigzag(zigzag, prd, max_array_size) calculates zigzag using period

Parameters:

zigzag : is the float array for the zigzag (should be defined like "var zigzag = array.new_float(0)"). each zigzag points contains 2 element: 1. price level of the zz point 2. bar_index of the zz point

prd : is the length to calculate zigzag waves by highest(prd)/lowest(prd)

max_array_size : is the maximum number of elements in zigzag, keep in mind each zigzag point contains 2 elements, so for example if it's 10 then zigzag has 10/2 => 5 zigzag points

Returns: dir that is the current direction of the zigzag

showZigzag(zigzag, oldzigzag, dir, upcol, dncol) this function shows zigzag

Parameters:

zigzag : is the float array for the zigzag (should be defined like "var zigzag = array.new_float(0)"). each zigzag points contains 2 element: 1. price level of the zz point 2. bar_index of the zz point

oldzigzag : is the float array for the zigzag, you get copy the zigzag array to oldzigzag by "oldzigzag = array.copy(zigzay)" before calling get_zigzag() function

dir : is the direction of the zigzag wave

upcol : is the color of the line if zigzag direction is up

dncol : is the color of the line if zigzag direction is down

Returns: null

taLibrary "ta"

█ OVERVIEW

This library holds technical analysis functions calculating values for which no Pine built-in exists.

Look first. Then leap.

█ FUNCTIONS

cagr(entryTime, entryPrice, exitTime, exitPrice)

It calculates the "Compound Annual Growth Rate" between two points in time. The CAGR is a notional, annualized growth rate that assumes all profits are reinvested. It only takes into account the prices of the two end points — not drawdowns, so it does not calculate risk. It can be used as a yardstick to compare the performance of two instruments. Because it annualizes values, the function requires a minimum of one day between the two end points (annualizing returns over smaller periods of times doesn't produce very meaningful figures).

Parameters:

entryTime : The starting timestamp.

entryPrice : The starting point's price.

exitTime : The ending timestamp.

exitPrice : The ending point's price.

Returns: CAGR in % (50 is 50%). Returns `na` if there is not >=1D between `entryTime` and `exitTime`, or until the two time points have not been reached by the script.

█ v2, Mar. 8, 2022

Added functions `allTimeHigh()` and `allTimeLow()` to find the highest or lowest value of a source from the first historical bar to the current bar. These functions will not look ahead; they will only return new highs/lows on the bar where they occur.

allTimeHigh(src)

Tracks the highest value of `src` from the first historical bar to the current bar.

Parameters:

src : (series int/float) Series to track. Optional. The default is `high`.

Returns: (float) The highest value tracked.

allTimeLow(src)

Tracks the lowest value of `src` from the first historical bar to the current bar.

Parameters:

src : (series int/float) Series to track. Optional. The default is `low`.

Returns: (float) The lowest value tracked.

█ v3, Sept. 27, 2022

This version includes the following new functions:

aroon(length)

Calculates the values of the Aroon indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

Returns: ( [float, float ]) A tuple of the Aroon-Up and Aroon-Down values.

coppock(source, longLength, shortLength, smoothLength)

Calculates the value of the Coppock Curve indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

longLength (simple int) : (simple int) Number of bars for the fast ROC value (length).

shortLength (simple int) : (simple int) Number of bars for the slow ROC value (length).

smoothLength (simple int) : (simple int) Number of bars for the weigted moving average value (length).

Returns: (float) The oscillator value.

dema(source, length)

Calculates the value of the Double Exponential Moving Average (DEMA).

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The double exponentially weighted moving average of the `source`.

dema2(src, length)

An alternate Double Exponential Moving Average (Dema) function to `dema()`, which allows a "series float" length argument.

Parameters:

src : (series int/float) Series of values to process.

length : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The double exponentially weighted moving average of the `src`.

dm(length)

Calculates the value of the "Demarker" indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

Returns: (float) The oscillator value.

donchian(length)

Calculates the values of a Donchian Channel using `high` and `low` over a given `length`.

Parameters:

length (int) : (series int) Number of bars (length).

Returns: ( [float, float, float ]) A tuple containing the channel high, low, and median, respectively.

ema2(src, length)

An alternate ema function to the `ta.ema()` built-in, which allows a "series float" length argument.

Parameters:

src : (series int/float) Series of values to process.

length : (series int/float) Number of bars (length).

Returns: (float) The exponentially weighted moving average of the `src`.

eom(length, div)

Calculates the value of the Ease of Movement indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

div (simple int) : (simple int) Divisor used for normalzing values. Optional. The default is 10000.

Returns: (float) The oscillator value.

frama(source, length)

The Fractal Adaptive Moving Average (FRAMA), developed by John Ehlers, is an adaptive moving average that dynamically adjusts its lookback period based on fractal geometry.

Parameters:

source (float) : (series int/float) Series of values to process.

length (int) : (series int) Number of bars (length).

Returns: (float) The fractal adaptive moving average of the `source`.

ft(source, length)

Calculates the value of the Fisher Transform indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Number of bars (length).

Returns: (float) The oscillator value.

ht(source)

Calculates the value of the Hilbert Transform indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

Returns: (float) The oscillator value.

ichimoku(conLength, baseLength, senkouLength)

Calculates values of the Ichimoku Cloud indicator, including tenkan, kijun, senkouSpan1, senkouSpan2, and chikou. NOTE: offsets forward or backward can be done using the `offset` argument in `plot()`.

Parameters:

conLength (int) : (series int) Length for the Conversion Line (Tenkan). The default is 9 periods, which returns the mid-point of the 9 period Donchian Channel.

baseLength (int) : (series int) Length for the Base Line (Kijun-sen). The default is 26 periods, which returns the mid-point of the 26 period Donchian Channel.

senkouLength (int) : (series int) Length for the Senkou Span 2 (Leading Span B). The default is 52 periods, which returns the mid-point of the 52 period Donchian Channel.

Returns: ( [float, float, float, float, float ]) A tuple of the Tenkan, Kijun, Senkou Span 1, Senkou Span 2, and Chikou Span values. NOTE: by default, the senkouSpan1 and senkouSpan2 should be plotted 26 periods in the future, and the Chikou Span plotted 26 days in the past.

ift(source)

Calculates the value of the Inverse Fisher Transform indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

Returns: (float) The oscillator value.

kvo(fastLen, slowLen, trigLen)

Calculates the values of the Klinger Volume Oscillator.

Parameters:

fastLen (simple int) : (simple int) Length for the fast moving average smoothing parameter calculation.

slowLen (simple int) : (simple int) Length for the slow moving average smoothing parameter calculation.

trigLen (simple int) : (simple int) Length for the trigger moving average smoothing parameter calculation.

Returns: ( [float, float ]) A tuple of the KVO value, and the trigger value.

pzo(length)

Calculates the value of the Price Zone Oscillator.

Parameters:

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The oscillator value.

rms(source, length)

Calculates the Root Mean Square of the `source` over the `length`.

Parameters:

source (float) : (series int/float) Series of values to process.

length (int) : (series int) Number of bars (length).

Returns: (float) The RMS value.

rwi(length)

Calculates the values of the Random Walk Index.

Parameters:

length (simple int) : (simple int) Lookback and ATR smoothing parameter length.

Returns: ( [float, float ]) A tuple of the `rwiHigh` and `rwiLow` values.

stc(source, fast, slow, cycle, d1, d2)

Calculates the value of the Schaff Trend Cycle indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

fast (simple int) : (simple int) Length for the MACD fast smoothing parameter calculation.

slow (simple int) : (simple int) Length for the MACD slow smoothing parameter calculation.

cycle (simple int) : (simple int) Number of bars for the Stochastic values (length).

d1 (simple int) : (simple int) Length for the initial %D smoothing parameter calculation.

d2 (simple int) : (simple int) Length for the final %D smoothing parameter calculation.

Returns: (float) The oscillator value.

stochFull(periodK, smoothK, periodD)

Calculates the %K and %D values of the Full Stochastic indicator.

Parameters:

periodK (simple int) : (simple int) Number of bars for Stochastic calculation. (length).

smoothK (simple int) : (simple int) Number of bars for smoothing of the %K value (length).

periodD (simple int) : (simple int) Number of bars for smoothing of the %D value (length).

Returns: ( [float, float ]) A tuple of the slow %K and the %D moving average values.

stochRsi(lengthRsi, periodK, smoothK, periodD, source)

Calculates the %K and %D values of the Stochastic RSI indicator.

Parameters:

lengthRsi (simple int) : (simple int) Length for the RSI smoothing parameter calculation.

periodK (simple int) : (simple int) Number of bars for Stochastic calculation. (length).

smoothK (simple int) : (simple int) Number of bars for smoothing of the %K value (length).

periodD (simple int) : (simple int) Number of bars for smoothing of the %D value (length).

source (float) : (series int/float) Series of values to process. Optional. The default is `close`.

Returns: ( [float, float ]) A tuple of the slow %K and the %D moving average values.

supertrend(factor, atrLength, wicks)

Calculates the values of the SuperTrend indicator with the ability to take candle wicks into account, rather than only the closing price.

Parameters:

factor (float) : (series int/float) Multiplier for the ATR value.

atrLength (simple int) : (simple int) Length for the ATR smoothing parameter calculation.

wicks (simple bool) : (simple bool) Condition to determine whether to take candle wicks into account when reversing trend, or to use the close price. Optional. Default is false.

Returns: ( [float, int ]) A tuple of the superTrend value and trend direction.

szo(source, length)

Calculates the value of the Sentiment Zone Oscillator.

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The oscillator value.

t3(source, length, vf)

Calculates the value of the Tilson Moving Average (T3).

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

vf (simple float) : (simple float) Volume factor. Affects the responsiveness.

Returns: (float) The Tilson moving average of the `source`.

t3Alt(source, length, vf)

An alternate Tilson Moving Average (T3) function to `t3()`, which allows a "series float" `length` argument.

Parameters:

source (float) : (series int/float) Series of values to process.

length (float) : (series int/float) Length for the smoothing parameter calculation.

vf (simple float) : (simple float) Volume factor. Affects the responsiveness.

Returns: (float) The Tilson moving average of the `source`.

tema(source, length)

Calculates the value of the Triple Exponential Moving Average (TEMA).

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The triple exponentially weighted moving average of the `source`.

tema2(source, length)

An alternate Triple Exponential Moving Average (TEMA) function to `tema()`, which allows a "series float" `length` argument.

Parameters:

source (float) : (series int/float) Series of values to process.

length (float) : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The triple exponentially weighted moving average of the `source`.

trima(source, length)

Calculates the value of the Triangular Moving Average (TRIMA).

Parameters:

source (float) : (series int/float) Series of values to process.

length (int) : (series int) Number of bars (length).

Returns: (float) The triangular moving average of the `source`.

trima2(src, length)

An alternate Triangular Moving Average (TRIMA) function to `trima()`, which allows a "series int" length argument.

Parameters:

src : (series int/float) Series of values to process.

length : (series int) Number of bars (length).

Returns: (float) The triangular moving average of the `src`.

trix(source, length, signalLength, exponential)

Calculates the values of the TRIX indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Length for the smoothing parameter calculation.

signalLength (simple int) : (simple int) Length for smoothing the signal line.

exponential (simple bool) : (simple bool) Condition to determine whether exponential or simple smoothing is used. Optional. The default is `true` (exponential smoothing).

Returns: ( [float, float, float ]) A tuple of the TRIX value, the signal value, and the histogram.

uo(fastLen, midLen, slowLen)

Calculates the value of the Ultimate Oscillator.

Parameters:

fastLen (simple int) : (series int) Number of bars for the fast smoothing average (length).

midLen (simple int) : (series int) Number of bars for the middle smoothing average (length).

slowLen (simple int) : (series int) Number of bars for the slow smoothing average (length).

Returns: (float) The oscillator value.

vhf(source, length)

Calculates the value of the Vertical Horizontal Filter.

Parameters:

source (float) : (series int/float) Series of values to process.

length (simple int) : (simple int) Number of bars (length).

Returns: (float) The oscillator value.

vi(length)

Calculates the values of the Vortex Indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

Returns: ( [float, float ]) A tuple of the viPlus and viMinus values.

vzo(length)

Calculates the value of the Volume Zone Oscillator.

Parameters:

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The oscillator value.

williamsFractal(period)

Detects Williams Fractals.

Parameters:

period (int) : (series int) Number of bars (length).

Returns: ( [bool, bool ]) A tuple of an up fractal and down fractal. Variables are true when detected.

wpo(length)

Calculates the value of the Wave Period Oscillator.

Parameters:

length (simple int) : (simple int) Length for the smoothing parameter calculation.

Returns: (float) The oscillator value.

█ v7, Nov. 2, 2023

This version includes the following new and updated functions:

atr2(length)

An alternate ATR function to the `ta.atr()` built-in, which allows a "series float" `length` argument.

Parameters:

length (float) : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The ATR value.

changePercent(newValue, oldValue)

Calculates the percentage difference between two distinct values.

Parameters:

newValue (float) : (series int/float) The current value.

oldValue (float) : (series int/float) The previous value.

Returns: (float) The percentage change from the `oldValue` to the `newValue`.

donchian(length)

Calculates the values of a Donchian Channel using `high` and `low` over a given `length`.

Parameters:

length (int) : (series int) Number of bars (length).

Returns: ( [float, float, float ]) A tuple containing the channel high, low, and median, respectively.

highestSince(cond, source)

Tracks the highest value of a series since the last occurrence of a condition.

Parameters:

cond (bool) : (series bool) A condition which, when `true`, resets the tracking of the highest `source`.

source (float) : (series int/float) Series of values to process. Optional. The default is `high`.

Returns: (float) The highest `source` value since the last time the `cond` was `true`.

lowestSince(cond, source)

Tracks the lowest value of a series since the last occurrence of a condition.

Parameters:

cond (bool) : (series bool) A condition which, when `true`, resets the tracking of the lowest `source`.

source (float) : (series int/float) Series of values to process. Optional. The default is `low`.

Returns: (float) The lowest `source` value since the last time the `cond` was `true`.

relativeVolume(length, anchorTimeframe, isCumulative, adjustRealtime)

Calculates the volume since the last change in the time value from the `anchorTimeframe`, the historical average volume using bars from past periods that have the same relative time offset as the current bar from the start of its period, and the ratio of these volumes. The volume values are cumulative by default, but can be adjusted to non-accumulated with the `isCumulative` parameter.

Parameters:

length (simple int) : (simple int) The number of periods to use for the historical average calculation.

anchorTimeframe (simple string) : (simple string) The anchor timeframe used in the calculation. Optional. Default is "D".

isCumulative (simple bool) : (simple bool) If `true`, the volume values will be accumulated since the start of the last `anchorTimeframe`. If `false`, values will be used without accumulation. Optional. The default is `true`.

adjustRealtime (simple bool) : (simple bool) If `true`, estimates the cumulative value on unclosed bars based on the data since the last `anchor` condition. Optional. The default is `false`.

Returns: ( [float, float, float ]) A tuple of three float values. The first element is the current volume. The second is the average of volumes at equivalent time offsets from past anchors over the specified number of periods. The third is the ratio of the current volume to the historical average volume.

rma2(source, length)

An alternate RMA function to the `ta.rma()` built-in, which allows a "series float" `length` argument.

Parameters:

source (float) : (series int/float) Series of values to process.

length (float) : (series int/float) Length for the smoothing parameter calculation.

Returns: (float) The rolling moving average of the `source`.

supertrend2(factor, atrLength, wicks)

An alternate SuperTrend function to `supertrend()`, which allows a "series float" `atrLength` argument.

Parameters:

factor (float) : (series int/float) Multiplier for the ATR value.

atrLength (float) : (series int/float) Length for the ATR smoothing parameter calculation.

wicks (simple bool) : (simple bool) Condition to determine whether to take candle wicks into account when reversing trend, or to use the close price. Optional. Default is `false`.

Returns: ( [float, int ]) A tuple of the superTrend value and trend direction.

vStop(source, atrLength, atrFactor)

Calculates an ATR-based stop value that trails behind the `source`. Can serve as a possible stop-loss guide and trend identifier.

Parameters:

source (float) : (series int/float) Series of values that the stop trails behind.

atrLength (simple int) : (simple int) Length for the ATR smoothing parameter calculation.

atrFactor (float) : (series int/float) The multiplier of the ATR value. Affects the maximum distance between the stop and the `source` value. A value of 1 means the maximum distance is 100% of the ATR value. Optional. The default is 1.