Liquidity Finder Library🔵 Introduction

You may intend to utilize the "Liquidity" detection capability in your indicators. Instead of writing it, you can import the "Liquidity Finder" library into your code. One of the advantages of this approach is time-saving and reduction in scripting errors.

🔵 Key Features

Identification of "Statics Liquidity"

Identification of "Dynamics Liquidity"

🔵 How to Use

Firstly, you can add the library to your code as shown in the example below :

import TFlab/LiquidityFinderLibrary/1 as Liq

The parameters of the "LLF" function are as follows :

sPP : A float variable ranging from 0 to 0.4. Increasing this number decreases the sensitivity of the "Statics Liquidity Line Detection" function and increases the number of detected lines. The default value is 0.3.

dPP : A float variable ranging from 0.4 to 1.95. Increasing this number increases the sensitivity of the "Dynamics Liquidity Line Detection" function and decreases the number of detected lines. The default value is 1.

SRs : An int variable. By default, it's set to 8. You can change this number to specify the periodicity of static liquidity pivot lines.

SRd : An int variable. By default, it's set to 3. You can change this number to specify the periodicity of dynamic liquidity pivot lines.

ShowHLLs : A bool variable. You can enable or disable the display of "High Statics Liquidity Line".

ShowLLLs : A bool variable. You can enable or disable the display of "Low Statics Liquidity Line".

ShowHLLd : A bool variable. You can enable or disable the display of "High Dynamics Liquidity Line".

ShowLLd : A bool variable. You can enable or disable the display of "High Dynamics Liquidity Line".

🟣Recommendation

You can use the following code snippet to import Liquidity Finder into your code for time-saving.

//import Library

import TFlab/LiquidityFinderLibrary/1 as Liq

//input

SLLS = input.float(0.30 , 'Statics Liquidity Line Sensitivity', maxval = 0.4 ,minval = 0.0, step = 0.01) // Statics Liquidity Line Sensitivity

DLLS = input.float(1.00 , 'Dynamics Liquidity Line Sensitivity', maxval = 1.95 ,minval = 0.4, step = 0.01) // Dynamics Liquidity Line Sensitivity

SPP = input.int(8 , 'Statics Period Pivot') // Statics Period Pivot

DPP = input.int(3 , 'Dynamics Period Pivot') // Dynamics Period Pivot

ShowSHLL = input.bool(true , 'Show Statics High Liquidity Line')

ShowSLLL = input.bool(true , 'Show Statics Low Liquidity Line')

ShowDHLL = input.bool(true , 'Show Dynamics High Liquidity Line')

ShowDLLL = input.bool(true , 'Show Dynamics Low Liquidity Line')

//call function

Liq.LLF(SPP,DPP,SLLS,DLLS,ShowSHLL,ShowSLLL,ShowDHLL,ShowDLLL)

Liquiditymethod

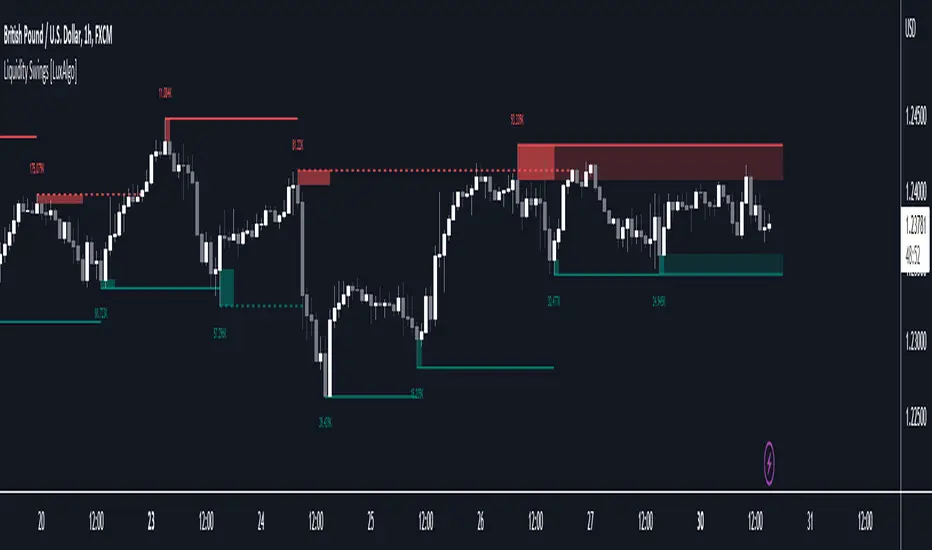

Liquidity Swings [LuxAlgo]The liquidity swings indicator highlights swing areas with existent trading activity. The number of times price revisited a swing area is highlighted by a zone delimiting the swing areas. Additionally, the accumulated volume within swing areas is highlighted by labels on the chart. An option to filter out swing areas with volume/counts not reaching a user-set threshold is also included.

This indicator by its very nature is not real-time and is meant for descriptive analysis alongside other components of the script. This is normal behavior for scripts detecting pivots as a part of a system and it is important you are aware the pivot labels are not designed to be traded in real-time themselves.

🔶 USAGE

The indicator can be used to highlight significant swing areas, these can be accumulation/distribution zones on lower timeframes and might play a role as future support or resistance.

Swing levels are also highlighted, when a swing level is broken it is displayed as a dashed line. A broken swing high is a bullish indication, while a broken swing low is a bearish indication.

Filtering swing areas by volume allows to only show significant swing areas with an higher degree of liquidity. These swing areas can be wider, highlighting higher volatility, or might have been visited by the price more frequently.

🔶 SETTINGS

Pivot Lookback : Lookback period used for the calculation of pivot points.

Swing Area : Determine how the swing area is calculated, "Wick Extremity" will use the range from price high to the maximum between price close/open in case of a swing high, and the range from price low to the minimum between price close/open in case of a swing low. "Full Range" will use the full candle range as swing area.

Intrabar Precision : Use intrabar data to calculate the accumulated volume within a swing area, this allows obtaining more precise results.

Filter Areas By : Determine how swing areas are filtered out, "Count" will filter out swing areas where price visited the area a number of time inferior to the user set threshold. "Volume" will filter out swing areas where the accumulated volume within the area is inferior to the user set threshold.

🔹 Style

Swing High : Show swing highs.

Swing Low : Show swing lows.

Label Size : Size of the labels on the chart.

Note that swing points are confirmed after Pivot Lookback bars, as such all elements are displayed retrospectively.