Simple way to BEAT the market [STRATEGY]This script has been created to demonstrate the effectiveness of using market regime filters in your trading strategy, and how they can improve your returns and lower your drawdowns

This strategy adds a simple filter (A historical volatility percentile filter, an implementation of which can be found on my trading profile) to a traditional buy and hold strategy of the index SPY.

Note, There are other filters that could also be added including a long-term moving average/percentile rank filter/ADX filter etc, to improve the returns further.

The filter closes our long position during periods of volatility that exceed the 95th percentile (or in the top 5% of volatile days) and buys back when the volatility is below 95% rank of the past 100 days

Have included the backtest results since 1993 which is 28 years of data at the time of writing. Comparison of traditional buy and hold with this modified strategy can be found below:

Traditional buy and hold:

Return per year: 7.95 % (ex Dividends)

Total return: 851.1 %

Max drawdown: 50.79 %

'Modified' buy and hold (this script):

Return per year: 9.92 % (ex Dividends)

Total return: 1412.2 %

Max drawdown: 31.57 %

Feel free to use some of the market filters in my trading profile to improve and refine your strategies further, or make a copy and play around with the code yourself. This is just a simple example for demo purposes.

Long-term

GBP/JPY Daily time FX Strategy ATR W% BaselineThis is a preety good strategy suited for long term trading.

It has been adapted and optimized in this case for GBP/JPY 1D time frame.

Its made of Kiojun baseline, together with ATR for stop loss and size calculation and Williams % R

For the purpose of this example we simulate that we have a leverage of 100x in order to be able to buy the ammount of lots required for our stop loss to be in same page with the risk % of our capital.

For entry we have for long, ascending R in the last 2 candles and crossover of close with KIOJUN baseline. For short the same but in reverse.

We exit if we reach the TP -100 points in this example, or SL , which is based on ATR of the last x days.

If you have any questions feel free to write me in private !

Low volatility Buy w/ TP & SL (Coinrule)The compression of volatility usually leads to expansion. When the breakout comes, it can ignite strong trends. One way to catch a coin trading in an accumulation area is to spot three moving averages with values close to each other. The strategy uses a combination of Moving Averages to spot the best time to buy a coin before its breakout.

Buy Condition

The MA200 is greater than the MA100

The MA50 is greater than the MA100

According to backtesting results, the 1-hour time frame is the best to run this strategy.

Sell Condition

Take Profit: the price increases 8% from the entry price

Stop Loss: the price drops 4% from the entry price

The strategy has a profitability of 40-60% (depending on the market conditions). Having a ratio of two between Take profit and Stop Loss helps keeping the strategy profitable in the long term.

Wilder's Volatility Trailing Stop Strategy with various MA'sFor Educational Purposes. Results can differ on different markets and can fail at any time. Profit is not guaranteed.

This only works in a few markets and in certain situations. Changing the settings can give better or worse results for other markets. This strategy is based on Wilder's Volatility System. It is an ATR trailing stop that is used for long term trends. This strategy focuses on the trailing stop alone and goes long and short only when it goes above or below the trailing line. It is similar to Donchian channels except it does not include the certain period channel breakout, only the trailing signal. This is only the trailing stop and an attempt to show how well it works standalone as Wilder described.

In his book, Wilder recommends a multiplier of 2.8-3.1 and an ATR lookback of 7 periods along with a running moving average or otherwise known as Wilder's moving average. The calculation and programming part for the trailing stop varies everywhere. I opted to keep it as simple and accurate as I could think of and interpret from the book. The variations to these types of indicators are numerous unfortunately, but Wilder seems to be the original author of ATR and this ATR-based trailing stop. In his book he says to use the significant closing price or highest/lowest closing price for the calculation part but I also included the option of choosing the highest high and lowest low, and the option to choose various moving averages in case anyone wants to experiment.

Comparing this and Donchian channels, it seems that a 2.5 multiplier is somewhat similar to the middle band of DCs and a 3.0 multiplier is somewhat similar to a double length middle band of DCs. It's hard to say which is the better trailing stop for a long term strategy. It's hard to beat the simplicity of DCs but maybe some might find a need for more inputs in a trailing stop or maybe an ATR based one like Wilder's can work better depending on what setting or strategy it's used in.

Global Indices Weekly Investment StrategyThis strategy aims to provide the optimal times to buy/sell assets on a long term basis. From my testing it works best on a weekly or monthly time frame. The default values are currently set to work best on Global Indices such as the S&P 500. It is very simple in its core, it uses price historical price action to estimate where in a market cycle the asset is. Then combined with a basic Moving-Average-like baseline and long term trend oscillator to gauge direction, it attempts to find the best time to buy/sell an asset to reduce capital draw-down and maximise future profits.

Returns here are based on an account balance and trade sizes of £100,000 with no compounding. Does not take into account exchange fees - 0% commission.

Please let me know if you have found any optimal settings for a given market using this strategy; such as all commodities. Or if you have any suggestions on how the strategy could be improved in general.

ElanStrategy v2.0A trend-following strategy with a twist.

I worked on the premise that Bitcoin price swings can not be predicted properly, since it's such a heavily manipulated market. Therefore, I chose to work with following the trend instead of predicting reversals.

It uses a weighted average of short, medium, and long range MA's.

This is the second version (see link below for v1.0), The main difference is that this new version uses a less binary position - it will change the position more gradually.

This one will automatically correct for bar duration, and works well from 1 to 4 hour charts. (1 hour chart seems to have data going back to only 2018/01/01 at the moment of writing, so I recommend using the 2H chart or higher)

Previous version:

BadaBing IchimokuUses a combination of entry parameters to define a very strict entry criterion

Uses a simple criteria to close trades

Intended for long-term trending trades

UNKNOWN1Designed for BTC only but with proper settings, I believe it can be used for other markets as well, at the end, it is a trend following strategy. Best TF to use - 1H

ElanStrategy v1.0A trend-following strategy with a twist.

I worked on the premise that Bitcoin price swings can not be predicted properly, since it's such a heavily manipulated market. Therefore, I chose to work with following the trend instead of predicting reversals.

The basis of this strategy is a fairly simple medium-term MA-crossover, but it adds nuance using a long-term MA for deciding on the size of the position.

LONG TERM INVESTMENT TECHNICAL STRATEGY SCRIPT200 - WEEKLY MOVING AVERAGE

GREEN LINE IS 200 WEEKS MOVING AVERAGE OF CLOSE

BLUE LINE IS 200 WEEKS MOVING AVERAGE OF LOW MULTIPLIED BY 0.90

RED LINE IS 100 WEEKS MOVING AVERAGE OF CLOSE

CONDITION: GREEN LINE SHOULD BE ABOVE RED LINE AND PRICE SHOULD BE ABOVE GREEN LINE

BUY ONCE THE PRICE IS ABOVE GREEN LINE AND FULFILLS THE CONDITION.

TARGET 1 FOR TIME FRAME 1 YEAR= 2 X GREEN LINE VALUE WHEN PRICE CROSSED IT

TARGET 2 FOR TIME FRAME 3 YEARS= 3 X GREEN LINE VALUE WHEN PRICE CROSSED IT

TARGET 3 FOR TIME FRAME 5 YEARS= 5 X GREEN LINE VALUE WHEN PRICE CROSSED IT

TARGET 4 FOR TIME FRAME 10 YEARS= 10 X GREEN LINE VALUE WHEN PRICE CROSSED IT

STOP LOSS IS TRAILING TO BLUE LINE

Revistochmanic StrategyRevistochmanic Wave is a stock tracking trends indicator & strategy for medium & long term investing.

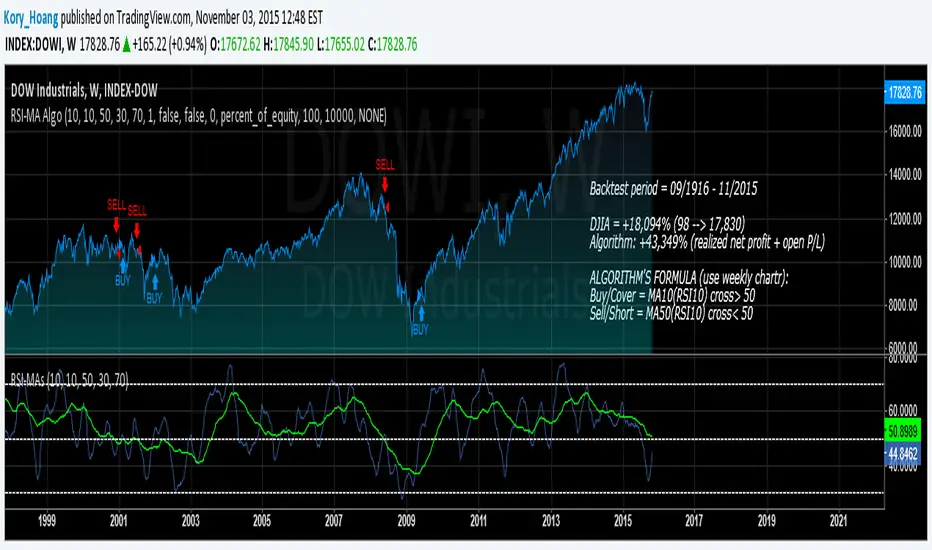

Simple RSI-MA Algo Beats DOW By Huge Margin Over Past 100 Years!This simple RSI-MA long/short algorithm beats the Dow by a FREAKING HUGE margin over the past century (excluding dividends and trading costs).

The algorithm uses a fast SMA of the RSI as a buy/cover signal and a slow SMA of the RSI as a sell/short signal.

Backtest period = 09/17/1916 - 11/02/2015

Dow = 98 --> 17,830 = +18,094% = 5.38% CAGR

Algorithm = net profit + open P/L = +43,349% = 6.31% CAGR

Notice how the algorithm dodged both the 30s' Great Depression and the 2008 Crisis. Pretty cool huh? :)

ALGORITHM'S FORMULA (use weekly chart):

Buy/Cover = MA10(RSI10) cross> 50

Sell/Short = MA50(RSI10) cross< 50

STRATEGY TESTER'S SETTINGS:

- Initial cash = $10,000

- Pyramiding disabled

- Re-investment enabled (order size = 100% of equity )

- Trade re-calculations disabled

DISCLAIMER: None of my ideas and posts are investment advice. Past performance is not an indication of future results. This strategy was constructed with the benefit of hindsight and its future performance cannot be guaranteed.