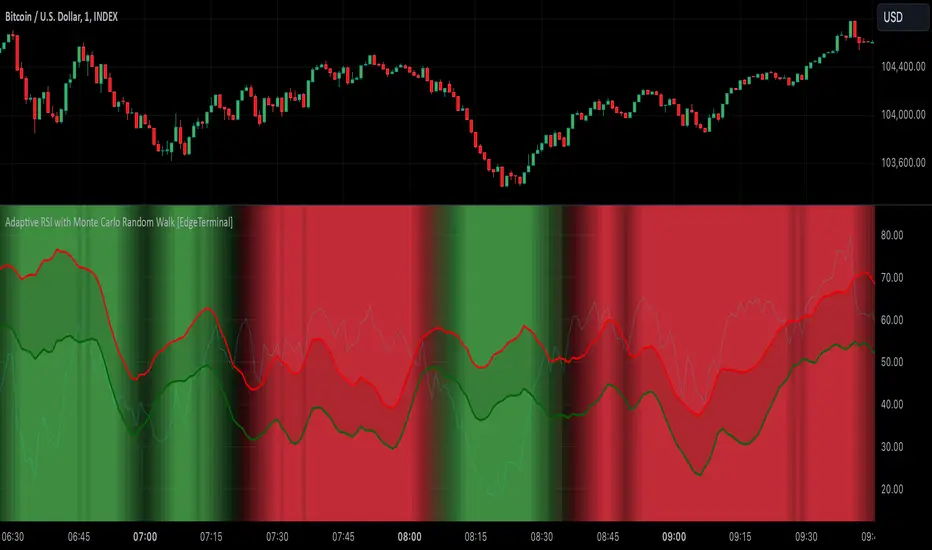

Adaptive RSI with Monte Carlo Random Walk [EdgeTerminal]The Monte Carlo Random Walk RSI indicator revolutionizes the traditional RSI by replacing static overbought/oversold levels with dynamic, statistically-driven bands that adapt to market conditions. Enhanced with smooth transitions, visual cues, and advanced filtering, this indicator provides a sophisticated approach to market analysis.

How it works:

In this indicator, the machine learning simulation works by combining multiple market signals in a weighted system that adapts to market conditions. Instead of just using simple RSI overbought/oversold levels, it analyzes the relationships between RSI, price momentum, and volatility to generate a comprehensive score.

The RSI component contributes 40% to the final signal, while momentum and volatility each contribute 30%. These signals are normalized and combined to create a score between 0-100, similar to how a machine learning model would generate probability predictions.

When this score is very high (above 80) along with traditional RSI signals, it suggests a stronger likelihood of a price reversal than using RSI alone.

The indicator doesn't use actual Monte Carlo simulations, but it does incorporate the concept of probability through its scoring system. Rather than giving simple buy/sell signals, it provides different levels of conviction (strong vs weak signals) based on how multiple factors align.

For example, a strong buy signal only occurs when both the ML score is above 80 AND the RSI is in oversold territory, indicating that multiple market conditions are favorable. This multi-factor approach helps reduce false signals that might occur with traditional RSI and provides traders with more nuanced information about potential trade opportunities.

Key Innovations:

Dynamic Bands vs Static Levels: Traditional RSI uses fixed 70/30 or 80/20 levels, this adaptive RSI creates adaptive bands based on market behavior and automatically adjusts to volatility and trend changes to reduce false signals in trending markets.

1. Calculate price volatility: σ = stdDev(returns)

2. Generate random walks: R(t) = R(t-1) + N(0,σ)

3. Transform to RSI space

4. Create probability distribution

5. Extract confidence intervals

Statistical Analysis: We use Monte Carlo simulations to generate probability bands. This allows the indicator levels to automatically adapt to current market conditions, generating more accurate overbought and oversold levels.

1. Measure deviation: D = |RSI - nearestBand|

2. Normalize by volatility: N = D/ATR

3. Calculate strength multiplier: max(1, N)

The indicator uses Monte Carlo simulations to model potential RSI paths. For each simulation, we generate random returns using market volatility, then calculate RSI components, calculate RSI, and finally, repeat N times (default 200 simulations)

Settings:

RSI Length: Controls the lookback period for the RSI calculation. Higher values result in smoother RSI, and slower signals. It affects exponential smoothing factor, impacts volatility measurement and influences random walk generation.

Number of Simulations: Controls Monte Carlo simulation count. Higher values result in more accurate bands, but lower calculation. More simulation means you get a better normal distribution, reducing random variation in bands.

Confidence Level: this controls statistical significance of bands. Higher values result in wider bands, meaning fewer trading signals are generated.

- 0.95 = 95% confidence interval

- Captures 2 standard deviations

- Controls false signal probability

Band Smoothing: Applies SMA to raw band values. Higher values mean smoother brands but result in more lag.

Minimum Signal Strength: Normalizes RSI deviation by ATR. The higher the value, it requires stronger moves. It uses ATR for volatility normalization and creates standard deviation equivalent.

Trend Sensitivity: Measures trend strength relative to volatility. Higher values filter more trending conditions

Volume Threshold: Compares current volume to average. Higher values require stronger volume confirmation. It validates price movement and confirms institutional participation.

How to Use:

Background gradually turns red in overbought and turns green in oversold conditions. Based on your trade direction, you want to pay attention when overbought or oversold levels start shifting.

For example, if you're going long on a trade, wait for oversold conditions (green) to start shifting toward red, this can indicate a move into a long direction, helping you catch the trend.

Additionally, the bands represent statistically significant levels where the RSI is likely to reverse, based on recent market behavior. The indicator runs multiple simulations of potential RSI paths. Each simulation uses recent market volatility and characteristics, then creates a statistical distribution of where RSI tends to turn around.

The Upper Band (red line) represents a statistically significant overbought level, when RSI crosses above this band and stays there for a while, the background starts to turn red, indicating it's more extended than normal. This is a lot more reliable than fixed RSI 70 level because it adapts to market conditions. Finally, the probability of reversal increases above this band. You can think of it as a dynamic overbought level.

The Lower Band (green line) is the opposite of the red line, and it represents a statistically significant oversold level. When RSI crosses below this band, it's more oversold than normal. This is a lot more reliable than fixed RSI 30 level because it adapts to market trend and the probability of reversal increases below this band.

Finally, the band width itself represents how volatile the market is. A wider band means the market is more volatile and a narrower band means the market is not as volatile. The width automatically adjusts based on market conditions.

MONTECARLO

Monte Carlo (Polyline Traceback) [Kioseff Trading]Hello!

This script "Monte Carlo (Polyline Traceback) " performs a Monte Carlo simulation using polylines!

By using polylines, and tracing back the initial simulation to its origin point, we can better replicate the ideal output of a Monte Carlo simulation!

Such as:

The image above shows the output of a simulation (image sourced outside TV).

With this script, and polyline capabilities, we can come quite close on TradingView.

The image above shows the indicator in action! Not bad considering the ideal output.

Of course, the script is quite heavy and tries its best to circumvent limitations :D

You might run into load time errors, in which case you might try applying the built-in setting "Force Script Load". This setting will cut-off the visuals for some simulations, but has a higher chance of passing load-time limitations!

As shown in the image above, you can select to only show worst-case and best-case simulations. Using this option will reduce chart lag and improve load times.

Features

Monte Carlo Simulation: Performs Monte Carlo simulation to generate multiple future paths.

Asset Price: Can simulate future asset prices based on historical log returns.

Statistical Methods: Offers two simulation methods—Gaussian (Normal) distribution and Bootstrapping.

Adjustable Parameters: Offers numerous user-adjustable settings like number of simulations, forecast length, and more.

Historical Data Points: Option to specify the amount of historical data to be used in the simulation (price).

Best/Worst Case: Allows you to show only the best case / worst case outcome (range) for all simulations!

Thank you!

Anchored Monte Carlo Shuffled Projection [LuxAlgo]The Anchored Monte Carlo Shuffled Projection tool randomly simulates future price points based on historical bar movements made before a user-anchored point in time.

By anchoring our data and projections to a single point in time, users can better understand and reflect on how the price played out while taking into consideration our random simulations.

🔶 USAGE

After selecting the indicator to apply to the chart, you will be prompted to "Set the Anchor Point". Do so by clicking on the desired location on your chart, only time is used as the anchor point.

Note: To select a new anchor point when applied to the chart, click on the 'More' dropdown next to the indicator status bar (○○○), then select "Reset points...".

Alternate Method: You are also able to click and drag the vertical line that displays on the anchor point bar when the indicator is highlighted.

By randomly simulating bar movements, a range is developed of potential price action which could be utilized to locate future price development as well as potential support/resistance levels.

Performing numerous simulations and taking the average at each step will converge toward the result highlighted by the "Average Line", and can point out where the price might develop, assuming the trend and amount of volatility persist.

Current closing price + Sum of changes in the calculation window

This constraint will cause the simulations always to display an endpoint consistent with the current lookback's slope.

While this may be helpful to some traders, this indicator includes an option to produce a less biased range, as seen below:

🔶 DETAILS

The Anchored Monte Carlo Shuffled Projection tool creates simulations based on prices within a user-set lookback window originating at the specified anchor point. Simulations are done as follows:

Collect each bar's price changes in the user-set window.

Randomize the order of each change in the window.

Project the cumulative sum of the shuffled changes from the current closing price.

Collect data on each point along the way.

This is the process for the Default calculation; for the 'Randomize Direction' calculation, when added onto the front for every other change, the value is inverted, creating the randomized endpoints for each simulation.

The script contains each simulation's data for that bar, with a maximum of 1000 simulations.

To get a glimpse behind the scenes, each simulation (up to 99) can be viewed using the 'Visualize Simulations' Options, as seen below.

Because the script holds the full simulation data, the script can also calculate this data, such as standard deviations.

In this script the Standard deviation lines are the average of all standard deviations across the vertical data groups, this provides a singular value that can be displayed a distance away from the simulation center line.

🔶 SETTINGS

Lookback: Sets the number of Bars to include in calculations.

Simulation Count: Sets the number of randomized simulations to calculate. (Max 1000)

Randomize Direction: See Details Above. Creates a more 'Normalized' Distribution

Visualize Simulations: See Details Above. Turns on Visualizations, and colors are randomly generated. Visualized max does not cap the calculated max. If 1000 simulations are used, the data will be from 1000 simulations, however, only the last 99 simulations will be visualized.

🔹 Standard Deviations

Standard Deviation Multiplier: Sets the multiplier to use for the Standard Deviation distance away from the center line.

🔹 Style

Extend Lines: Extends the Simulated Value Lines into the future for further reference and analysis.

Monte Carlo Shuffled Projection [LuxAlgo]The Monte Carlo Shuffled Projection tool randomly simulates future price points based on historical bar movements made within a user-selected window.

The tool shows potential paths price might take in the future, as well as highlighting potential support/resistance levels.

Note that simulations and their resulting elements are subject to slight changes over time.

🔶 USAGE

By randomly simulating bar movements, a range is developed of potential price action which could be utilized to locate future price development as well as potential support/resistance levels.

Performing a large number of simulations and taking the average at each step will converge toward the result highlighted by the "Average Line", and can point out where the price might develop assuming the trend and amount of volatility persist.

Current closing price + Sum of changes in the calculation window)

This constraint will cause the simulations to always display an endpoint consistent with the current lookback's slope.

While this may be helpful to some traders, this indicator includes an option to produce a less biased range as seen below:

🔶 DETAILS

The Monte Carlo Shuffled Projection tool creates simulations based on the most recent prices within a user-set window. Simulations are done as follows:

Collect each bar's price changes in the user-set window.

Randomize the order of each change in the window.

Project the cumulative sum of the shuffled changes from the current closing price.

Collect data on each point along the way.

This is the process for the Default calculation, for the 'Randomize Direction' calculation, when added onto the front for every other change, the value is inverted, creating the randomized endpoints for each simulation.

The script contains each simulation's data for that bar with a maximum of 1000 simulations.

To get a glimpse behind the scenes each simulation (up to 99) can be viewed using the 'Visualize Simulations' Options as seen below.

Because the script holds the full simulation data, the script can also do calculations on this data, such as calculating standard deviations.

In this script the Standard deviation lines are the average of all standard deviations across the vertical data groups, this provides a singular value that can be displayed a distance away from the simulation center line.

🔶 SETTINGS

Color and Toggle Options are Provided throughout.

Lookback: Sets the number of Bars to include in calculations.

Simulation Count: Sets the number of randomized simulations to calculate. (Max 1000)

Randomize Direction: See Details Above. Creates a more 'Normalized' Distribution

Visualize Simulations: See Details Above. Turns on Visualizations, and colors are randomly generated. Visualized max does not cap the calculated max. If 1000 simulations are used, the data will be from 1000 simulations, however only the last 99 simulations will be visualized.

Standard Deviation Multiplier: Sets the multiplier to use for the Standard Deviation distance away from the center line.

[BCT] Option Pricing via Markov Chain Monte Carlo SimulationOverview:

This script offers a toolkit for quantitative options trading, using Monte Carlo simulations based on actual historical returns to model potential future price paths for underlying assets. A range of metrics related to options trading are also provided.

Monte Carlo Simulations:

The script employs Monte Carlo simulations to model future price paths based on the historical returns of the underlying asset. These simulated paths are represented as parabolas at the 2-sigma, 25th percentile, and median levels for quick reference.

Methodologies:

For calculating options prices at At-the-Money (or any user-selected strike), two methodologies are used:

Simple Averaging: Takes the mean of the simulated asset price paths.

Kernel Density Estimation (KDE): Applied to the simulated asset price paths to produce a smoothed estimate of its probability density function, thereby aiding in a more nuanced option price calculation.

Bootstrap Resampling:

Bootstrap resampling is specifically applied to the simulated asset price paths to generate an estimate of the standard deviation of the options prices. Note that while bootstrap methods are employed, they serve as statistical tools and do not guarantee statistical reliability.

Metrics Displayed:

Model-Estimated At-the-Money (or selected strike) Straddle Price

Model-Estimated At-the-Money (or selected strike) Call Price

Model-Estimated At-the-Money (or selected strike) Put Price

Model-Estimated Standard deviation for Option Prices from simulated price paths

Underlying Monte Carlo Simulation Results (represented as parabolas at the 2 sigma, 25 percentile and median)

This is not financial advice. Use at your own risk.

Disclaimer: Options trading carries a high level of risk and may not be suitable for all investors. This script is intended to serve as an educational tool and should not be considered financial advice. While designed to aid in decision-making, the script's indicators are not guarantees of performance or outcomes. Always conduct your own due diligence before making trading decisions.

Monte Carlo Simulation - Your Strategy [Kioseff Trading]Hello!

This script “Monte Carlo Simulation - Your Strategy” uses Monte Carlo simulations for your inputted strategy returns or the asset on your chart!

Features

Monte Carlo Simulation: Performs Monte Carlo simulation to generate multiple future paths.

Asset Price or Strategy: Can simulate either future asset prices based on historical log returns or a specific trading strategy's future performance.

User-Defined Input: Allows you to input your own historical returns for simulation.

Statistical Methods: Offers two simulation methods—Gaussian (Normal) distribution and Bootstrapping.

Graphical Display: Provides options for graphical representation, including line plots and histograms.

Cumulative Probability Target: Enables setting a user-defined cumulative probability target to quantify simulation results.

Adjustable Parameters: Offers numerous user-adjustable settings like number of simulations, forecast length, and more.

Historical Data Points: Option to specify the amount of historical data to be used in the simulation (price).

Custom Binning: Allows you to select the binning method for histograms, with options like Sturges, Rice, and Square Root.

Best/Worst Case: Allows you to show only the best case / worst case outcome (range) for all simulations!

Scatterplot: allows you to show up to 1000 potential outcomes for a specified trade number (or bars forward price endpoint) using a scatter plot.

The image above shows the primary components of the indicator!

The image above shows the best/worst case outcome feature in action!

The image above shows a "fun feature" where 1000 simulated end points for a 15-bar price trajectory are shown as a scatter plot!

How To Perform a Monte Carlo Simulation On Your Strategy

Really, you can input any data into the indicator it will perform a Monte Carlo Simulation on it :D

The following instructions show how to export your strategy results from TradingView to an Excel File, copy the data, and input it into the indicator.

However , you are not limited to following this method!

Wherever your strategy results are stored, simply copy and paste them into the indicator text area in the settings and simulations will begin.

Returns Should Follow This Format

1

3

-3

2

-5

The numbers are presented as a single column. No commas or separators used.

The numbers above are in sequential order. A return of "1" for the first trade and a return of "-5" for the last trade. Your strategy returns will likely be in sequential order already so don't worry too much about this (:

How To Perform a Monte Carlo Simulation On Your TradingView Strategy With Excel Data

Export your strategy returns to an excel file using TradingView

Navigate to your downloads folder to column G "Profit"

Click the column and press CTRL + SPACE to highlight the entire column

Press CTRL + C to copy the entire column

Open this indicator's settings and paste the returns into the text area

The image above illustrates the process!

Notes on Inputting Returns

*Must input your returns without a separate as a vertical list

*The initial text area can only hold so many return values. If your list of trades is large you can input additional returns into two additional text areas at the bottom of the indicator settings.

That should be it; thank you for checking this out!

Drift Study (Inspired by Monte Carlo Simulations with BM) [KL]Inspired by the Brownian Motion ("BM") model that could be applied to conducting Monte Carlo Simulations, this indicator plots out the Drift factor contributing to BM.

Interpretation : If the Drift value is positive, then prices are possibly moving in an uptrend. Vice versa for negative drifts.

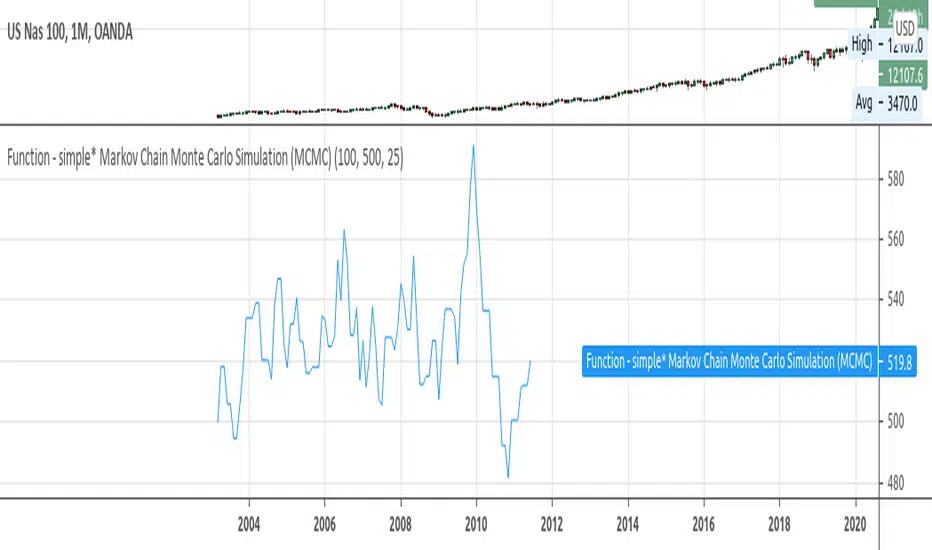

Function - simple* Markov Chain Monte Carlo Simulation (MCMC)Example function of a markov chain monte carlo simulation.

Monte Carlo Range Forecast [DW]This is an experimental study designed to forecast the range of price movement from a specified starting point using a Monte Carlo simulation.

Monte Carlo experiments are a broad class of computational algorithms that utilize random sampling to derive real world numerical results.

These types of algorithms have a number of applications in numerous fields of study including physics, engineering, behavioral sciences, climate forecasting, computer graphics, gaming AI, mathematics, and finance.

Although the applications vary, there is a typical process behind the majority of Monte Carlo methods:

-> First, a distribution of possible inputs is defined.

-> Next, values are generated randomly from the distribution.

-> The values are then fed through some form of deterministic algorithm.

-> And lastly, the results are aggregated over some number of iterations.

In this study, the Monte Carlo process used generates a distribution of aggregate pseudorandom linear price returns summed over a user defined period, then plots standard deviations of the outcomes from the mean outcome generate forecast regions.

The pseudorandom process used in this script relies on a modified Wichmann-Hill pseudorandom number generator (PRNG) algorithm.

Wichmann-Hill is a hybrid generator that uses three linear congruential generators (LCGs) with different prime moduli.

Each LCG within the generator produces an independent, uniformly distributed number between 0 and 1.

The three generated values are then summed and modulo 1 is taken to deliver the final uniformly distributed output.

Because of its long cycle length, Wichmann-Hill is a fantastic generator to use on TV since it's extremely unlikely that you'll ever see a cycle repeat.

The resulting pseudorandom output from this generator has a minimum repetition cycle length of 6,953,607,871,644.

Fun fact: Wichmann-Hill is a widely used PRNG in various software applications. For example, Excel 2003 and later uses this algorithm in its RAND function, and it was the default generator in Python up to v2.2.

The generation algorithm in this script takes the Wichmann-Hill algorithm, and uses a multi-stage transformation process to generate the results.

First, a parent seed is selected. This can either be a fixed value, or a dynamic value.

The dynamic parent value is produced by taking advantage of Pine's timenow variable behavior. It produces a variable parent seed by using a frozen ratio of timenow/time.

Because timenow always reflects the current real time when frozen and the time variable reflects the chart's beginning time when frozen, the ratio of these values produces a new number every time the cache updates.

After a parent seed is selected, its value is then fed through a uniformly distributed seed array generator, which generates multiple arrays of pseudorandom "children" seeds.

The seeds produced in this step are then fed through the main generators to produce arrays of pseudorandom simulated outcomes, and a pseudorandom series to compare with the real series.

The main generators within this script are designed to (at least somewhat) model the stochastic nature of financial time series data.

The first step in this process is to transform the uniform outputs of the Wichmann-Hill into outputs that are normally distributed.

In this script, the transformation is done using an estimate of the normal distribution quantile function.

Quantile functions, otherwise known as percent-point or inverse cumulative distribution functions, specify the value of a random variable such that the probability of the variable being within the value's boundary equals the input probability.

The quantile equation for a normal probability distribution is μ + σ(√2)erf^-1(2(p - 0.5)) where μ is the mean of the distribution, σ is the standard deviation, erf^-1 is the inverse Gauss error function, and p is the probability.

Because erf^-1() does not have a simple, closed form interpretation, it must be approximated.

To keep things lightweight in this approximation, I used a truncated Maclaurin Series expansion for this function with precomputed coefficients and rolled out operations to avoid nested looping.

This method provides a decent approximation of the error function without completely breaking floating point limits or sucking up runtime memory.

Note that there are plenty of more robust techniques to approximate this function, but their memory needs very. I chose this method specifically because of runtime favorability.

To generate a pseudorandom approximately normally distributed variable, the uniformly distributed variable from the Wichmann-Hill algorithm is used as the input probability for the quantile estimator.

Now from here, we get a pretty decent output that could be used itself in the simulation process. Many Monte Carlo simulations and random price generators utilize a normal variable.

However, if you compare the outputs of this normal variable with the actual returns of the real time series, you'll find that the variability in shocks (random changes) doesn't quite behave like it does in real data.

This is because most real financial time series data is more complex. Its distribution may be approximately normal at times, but the variability of its distribution changes over time due to various underlying factors.

In light of this, I believe that returns behave more like a convoluted product distribution rather than just a raw normal.

So the next step to get our procedurally generated returns to more closely emulate the behavior of real returns is to introduce more complexity into our model.

Through experimentation, I've found that a return series more closely emulating real returns can be generated in a three step process:

-> First, generate multiple independent, normally distributed variables simultaneously.

-> Next, apply pseudorandom weighting to each variable ranging from -1 to 1, or some limits within those bounds. This modulates each series to provide more variability in the shocks by producing product distributions.

-> Lastly, add the results together to generate the final pseudorandom output with a convoluted distribution. This adds variable amounts of constructive and destructive interference to produce a more "natural" looking output.

In this script, I use three independent normally distributed variables multiplied by uniform product distributed variables.

The first variable is generated by multiplying a normal variable by one uniformly distributed variable. This produces a bit more tailedness (kurtosis) than a normal distribution, but nothing too extreme.

The second variable is generated by multiplying a normal variable by two uniformly distributed variables. This produces moderately greater tails in the distribution.

The third variable is generated by multiplying a normal variable by three uniformly distributed variables. This produces a distribution with heavier tails.

For additional control of the output distributions, the uniform product distributions are given optional limits.

These limits control the boundaries for the absolute value of the uniform product variables, which affects the tails. In other words, they limit the weighting applied to the normally distributed variables in this transformation.

All three sets are then multiplied by user defined amplitude factors to adjust presence, then added together to produce our final pseudorandom return series with a convoluted product distribution.

Once we have the final, more "natural" looking pseudorandom series, the values are recursively summed over the forecast period to generate a simulated result.

This process of generation, weighting, addition, and summation is repeated over the user defined number of simulations with different seeds generated from the parent to produce our array of initial simulated outcomes.

After the initial simulation array is generated, the max, min, mean and standard deviation of this array are calculated, and the values are stored in holding arrays on each iteration to be called upon later.

Reference difference series and price values are also stored in holding arrays to be used in our comparison plots.

In this script, I use a linear model with simple returns rather than compounding log returns to generate the output.

The reason for this is that in generating outputs this way, we're able to run our simulations recursively from the beginning of the chart, then apply scaling and anchoring post-process.

This allows a greater conservation of runtime memory than the alternative, making it more suitable for doing longer forecasts with heavier amounts of simulations in TV's runtime environment.

From our starting time, the previous bar's price, volatility, and optional drift (expected return) are factored into our holding arrays to generate the final forecast parameters.

After these parameters are computed, the range forecast is produced.

The basis value for the ranges is the mean outcome of the simulations that were run.

Then, quarter standard deviations of the simulated outcomes are added to and subtracted from the basis up to 3σ to generate the forecast ranges.

All of these values are plotted and colorized based on their theoretical probability density. The most likely areas are the warmest colors, and least likely areas are the coolest colors.

An information panel is also displayed at the starting time which shows the starting time and price, forecast type, parent seed value, simulations run, forecast bars, total drift, mean, standard deviation, max outcome, min outcome, and bars remaining.

The interesting thing about simulated outcomes is that although the probability distribution of each simulation is not normal, the distribution of different outcomes converges to a normal one with enough steps.

In light of this, the probability density of outcomes is highest near the initial value + total drift, and decreases the further away from this point you go.

This makes logical sense since the central path is the easiest one to travel.

Given the ever changing state of markets, I find this tool to be best suited for shorter term forecasts.

However, if the movements of price are expected to remain relatively stable, longer term forecasts may be equally as valid.

There are many possible ways for users to apply this tool to their analysis setups. For example, the forecast ranges may be used as a guide to help users set risk targets.

Or, the generated levels could be used in conjunction with other indicators for meaningful confluence signals.

More advanced users could even extrapolate the functions used within this script for various purposes, such as generating pseudorandom data to test systems on, perform integration and approximations, etc.

These are just a few examples of potential uses of this script. How you choose to use it to benefit your trading, analysis, and coding is entirely up to you.

If nothing else, I think this is a pretty neat script simply for the novelty of it.

----------

How To Use:

When you first add the script to your chart, you will be prompted to confirm the starting date and time, number of bars to forecast, number of simulations to run, and whether to include drift assumption.

You will also be prompted to confirm the forecast type. There are two types to choose from:

-> End Result - This uses the values from the end of the simulation throughout the forecast interval.

-> Developing - This uses the values that develop from bar to bar, providing a real-time outlook.

You can always update these settings after confirmation as well.

Once these inputs are confirmed, the script will boot up and automatically generate the forecast in a separate pane.

Note that if there is no bar of data at the time you wish to start the forecast, the script will automatically detect use the next available bar after the specified start time.

From here, you can now control the rest of the settings.

The "Seeding Settings" section controls the initial seed value used to generate the children that produce the simulations.

In this section, you can control whether the seed is a fixed value, or a dynamic one.

Since selecting the dynamic parent option will change the seed value every time you change the settings or refresh your chart, there is a "Regenerate" input built into the script.

This input is a dummy input that isn't connected to any of the calculations. The purpose of this input is to force an update of the dynamic parent without affecting the generator or forecast settings.

Note that because we're running a limited number of simulations, different parent seeds will typically yield slightly different forecast ranges.

When using a small number of simulations, you will likely see a higher amount of variance between differently seeded results because smaller numbers of sampled simulations yield a heavier bias.

The more simulations you run, the smaller this variance will become since the outcomes become more convergent toward the same distribution, so the differences between differently seeded forecasts will become more marginal.

When using a dynamic parent, pay attention to the dispersion of ranges.

When you find a set of ranges that is dispersed how you like with your configuration, set your fixed parent value to the parent seed that shows in the info panel.

This will allow you to replicate that dispersion behavior again in the future.

An important thing to note when settings alerts on the plotted levels, or using them as components for signals in other scripts, is to decide on a fixed value for your parent seed to avoid minor repainting due to seed changes.

When the parent seed is fixed, no repainting occurs.

The "Amplitude Settings" section controls the amplitude coefficients for the three differently tailed generators.

These amplitude factors will change the difference series output for each simulation by controlling how aggressively each series moves.

When "Adjust Amplitude Coefficients" is disabled, all three coefficients are set to 1.

Note that if you expect volatility to significantly diverge from its historical values over the forecast interval, try experimenting with these factors to match your anticipation.

The "Weighting Settings" section controls the weighting boundaries for the three generators.

These weighting limits affect how tailed the distributions in each generator are, which in turn affects the final series outputs.

The maximum absolute value range for the weights is . When "Limit Generator Weights" is disabled, this is the range that is automatically used.

The last set of inputs is the "Display Settings", where you can control the visual outputs.

From here, you can select to display either "Forecast" or "Difference Comparison" via the "Output Display Type" dropdown tab.

"Forecast" is the type displayed by default. This plots the end result or developing forecast ranges.

There is an option with this display type to show the developing extremes of the simulations. This option is enabled by default.

There's also an option with this display type to show one of the simulated price series from the set alongside actual prices.

This allows you to visually compare simulated prices alongside the real prices.

"Difference Comparison" allows you to visually compare a synthetic difference series from the set alongside the actual difference series.

This display method is primarily useful for visually tuning the amplitude and weighting settings of the generators.

There are also info panel settings on the bottom, which allow you to control size, colors, and date format for the panel.

It's all pretty simple to use once you get the hang of it. So play around with the settings and see what kinds of forecasts you can generate!

----------

ADDITIONAL NOTES & DISCLAIMERS

Although I've done a number of things within this script to keep runtime demands as low as possible, the fact remains that this script is fairly computationally heavy.

Because of this, you may get random timeouts when using this script.

This could be due to either random drops in available runtime on the server, using too many simulations, or running the simulations over too many bars.

If it's just a random drop in runtime on the server, hide and unhide the script, re-add it to the chart, or simply refresh the page.

If the timeout persists after trying this, then you'll need to adjust your settings to a less demanding configuration.

Please note that no specific claims are being made in regards to this script's predictive accuracy.

It must be understood that this model is based on randomized price generation with assumed constant drift and dispersion from historical data before the starting point.

Models like these not consider the real world factors that may influence price movement (economic changes, seasonality, macro-trends, instrument hype, etc.), nor the changes in sample distribution that may occur.

In light of this, it's perfectly possible for price data to exceed even the most extreme simulated outcomes.

The future is uncertain, and becomes increasingly uncertain with each passing point in time.

Predictive models of any type can vary significantly in performance at any point in time, and nobody can guarantee any specific type of future performance.

When using forecasts in making decisions, DO NOT treat them as any form of guarantee that values will fall within the predicted range.

When basing your trading decisions on any trading methodology or utility, predictive or not, you do so at your own risk.

No guarantee is being issued regarding the accuracy of this forecast model.

Forecasting is very far from an exact science, and the results from any forecast are designed to be interpreted as potential outcomes rather than anything concrete.

With that being said, when applied prudently and treated as "general case scenarios", forecast models like these may very well be potentially beneficial tools to have in the arsenal.

Monte Carlo Simulation - Random WalkHello All,

Monte Carlo Simulation is a model used to predict the probability of different outcomes when the intervention of random variables is present. it is used by professionals in such widely disparate fields as finance, project management etc. You can find many articles about Monte Carlo Simulation on the net.

In this script I tried to make Monte Carlo Simulation and "Random Walk". it calculates results over and over, each time using a different set of random values that is created using historical data (500 times by default) and show min-max and some random paths. number of "random walks" is calculated by using number of bars to predict, so if you change "Number of Bars to Predict" then number of random walks may change. Total number of the lines must be less than 500.

"Number of Simulations " is 500 by default, more simulation better results. but if you increase it a lot then you may get "loop takes too long error"

"Number of Bars to Predict" can be between 10-100

"Number of Bars to use as Data Source" is the number of historical bars to use in simulations

Thanks to Ricardo Santos (@RicardoSantos) for letting me use his Random Number Generator Function.

P.S. I am not mathematician and I tried to make it as far as I understood the method. so if you see any issue let me know please.

Some examples:

Number of Bars to Predict = 100:

Number of Bars to Predict = 10:

if you enable "Keep Past Min-Max Levels" option then min-max levels will stay on the chart

Enjoy!

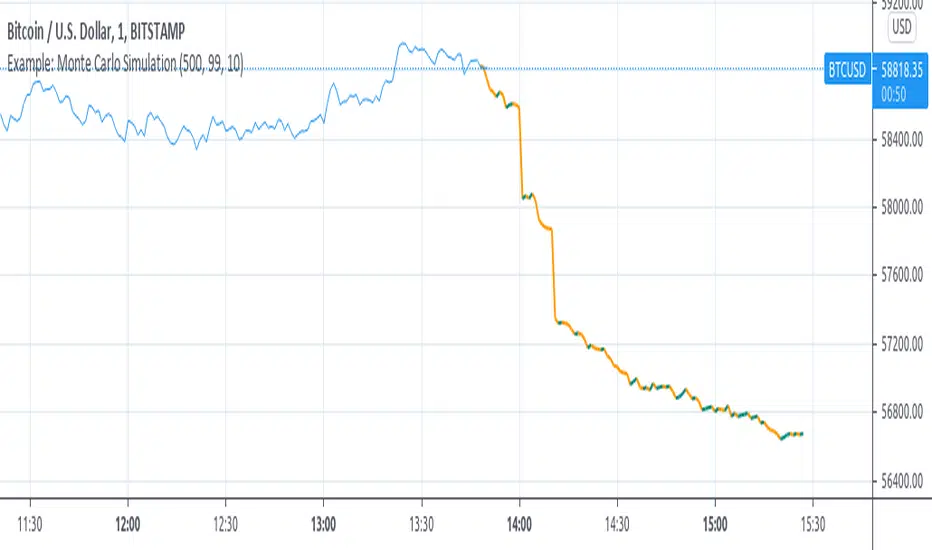

Example: Monte Carlo SimulationExperimental:

Example execution of Monte Carlo Simulation applied to the markets(this is my interpretation of the algo so inconsistencys may appear).

note:

the algorithm is very demanding so performance is limited.

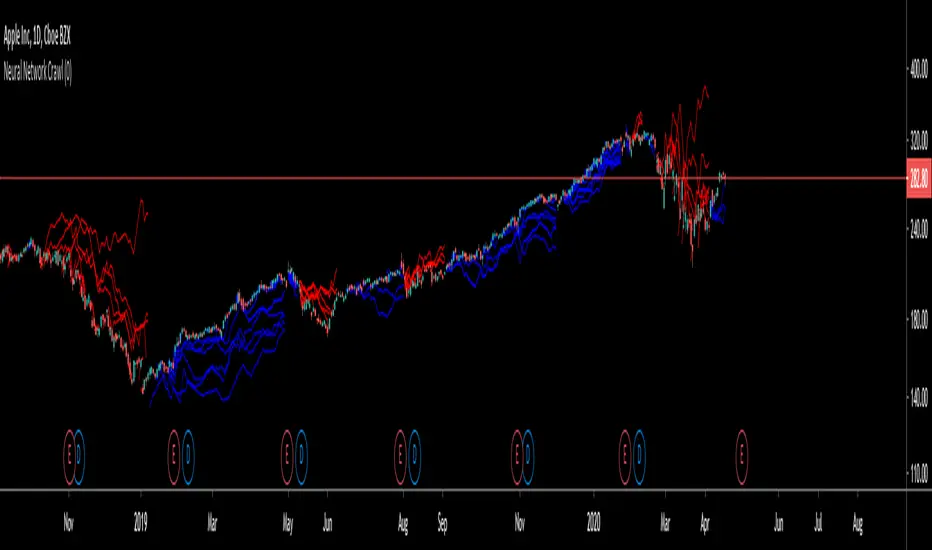

Neural Network CrawlAbout the Indicator

The Crawling Neural Network is a unique algorithm that identifies clusters of random walks that are crossing above or below the market price of the asset.

The random walks always exist, but the specific series that contribute to the cluster can only be seen during their significant period.

When the price trends strongly in a direction, it is more likely that it will traverse a significant amount of random walks and form a cluster.

The random walks are derived from a random selection of logarithmic movements in the last 200 bars and have been spawned at the beginning of price history.

Additionally, if you add the indicator to your chart multiple times and change the modifier in the settings panel, you can view more random walks that contribute to the clusters as seen in the screenshot below.

This indicator is available to everyone. Enjoy...

Random Walk SimulationUnderstanding the Random Walk Simulation

This indicator randomly generates alternative price outcomes derived from the price movements of the underlying security. Monte Carlo methods rely on repeated random sampling to create a data set that has the same characteristics as the sample source, representing examples of alternate outcomes. The data set created using random sampling is called a “random walk”.

First, every bar in the time stamp is measured and put into a logarithmic population. Then, a sample is drawn at random from the population and is used to determine the next price movement of the random walk. This process is repeated fifteen times to visualise whether the alternative outcomes lie above or beneath the current market price of the security.

Random Walk Utility

The random walk generator allows users of the Monte Carlo to further understand how the Monte Carlo projection is generated by creating a visual representation of individual random walks. Trends that occur on the random walks may correlate to the historical price action of the underlying security.

You can find the Monte Carlo Simulator here:

Input Values

Select the “ Format ”, button located next to the indicator label to adjust the input values and the style.

The Random Walk indicator only has one user-defined input value that can be changed.

The Random_Variable randomises a set of random walks. If this variable is changed, it will run a fresh set of 15 random walks which will result in a slightly different outcome.

Adding the indicator to your chart multiple times using many different random variables will allow you to achieve a more accurate reading. Ideally, the Monte Carlo Simulator takes an average of these to be interpreted.

For more information on this indicator, the full PDF can be found here: www.kenzing.com

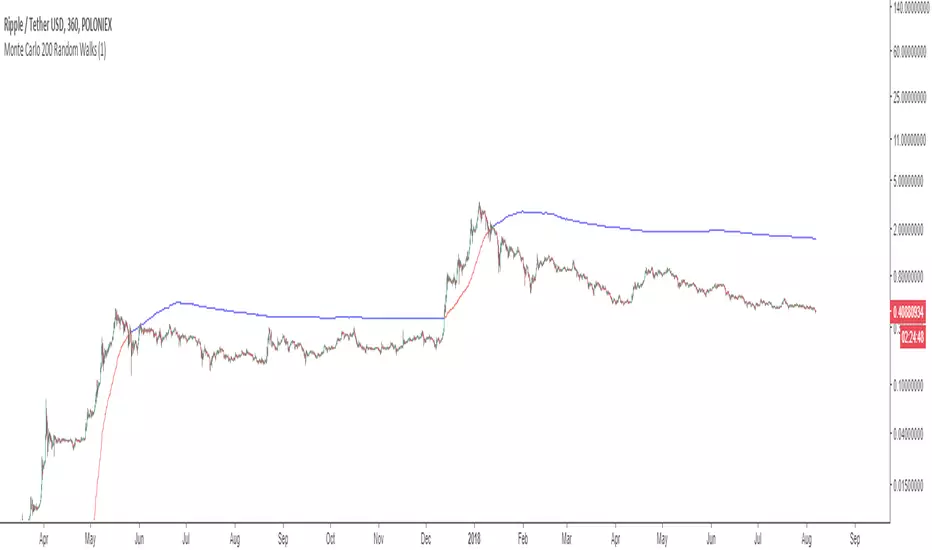

Monte Carlo Simulation (200 Random Walks)Understanding the Monte Carlo Simulation

This indicator uses Monte Carlo methods to predict the future price of a security using 200 random walks.

Monte Carlo methods rely on repeated random sampling to create a data set that has the same characteristics as the sample source, representing examples of alternate possible outcomes. The data set created using random sampling is called a “random walk”. Obtaining a mean from 200 random walks allows us to benchmark the performance of the source against the random walks obtained from the source.

Monte Carlo Utility

This Monte Carlo simulator plots a single line that represents 200 random walks across any security and time stamp. The line is red if most of the random walks are lower than the price of the security, and blue if the walks are higher.

Input Values

Select the “ Format ”, button located next to the indicator label to adjust the input values and the style.

The Monte Carlo indicator has only one user-defined input value that can be changed.

The Random_Variable determines set of random walks. If this variable is changed, it will run a fresh set

of 200 random walks which will result in a slightly different outcome. 200 random walks will load

relatively quick and produce roughly the same outcome as 10,000 random walks.

Adding the indicator to your chart multiple times using many different random variables will allow you

to achieve a more accurate reading.

For more information on this indicator view the PDF here: www.kenzing.com