Essa - Multi-Timeframe LevelsEnhanced Multi‐Timeframe Levels

This indicator plots yearly, quarterly and monthly highs, lows and midpoints on your chart. Each level is drawn as a horizontal line with an optional label showing “ – ” (for example “Apr 2025 High – 1.2345”). If two or more timeframes share the same price (within two ticks), they are merged into a single line and the label lists each timeframe.

A distance table can be shown in any corner of the chart. It lists up to five active levels closest to the current closing price and shows for each level:

level name (e.g. “May 2025 Low”)

exact price

distance in pips or points (calculated according to the instrument’s tick size)

percentage difference relative to the close

Alerts can be enabled so that whenever price comes within a user-specified percentage of any level (for example 0.1 %), an alert fires. Once price decisively crosses a level, that level is marked as “broken” so it does not trigger again. Built-in alertcondition hooks are also provided for definite breaks of the current monthly, quarterly and yearly highs and lows.

Monthly lookback is configurable (default 6 months), and once the number of levels exceeds a cap (calculated as 20 + monthlyLookback × 3), the oldest levels are automatically removed to avoid clutter. Line widths and colours (with adjustable opacity for quarterly and monthly) can be set separately for each timeframe. Touches of each level are counted internally to allow future extension (for example visually emphasising levels with multiple touches).

Monthly Charts

JL - DWM OHLCThis indicator plots the following price levels on your chart automatically AND will not show up if you are using a timeframe bigger than 60 minutes, 1 day, or 1 week.

Here are the price levels that are automatically plotted for you, and so you know the styling is different for Daily, Weekly, Monthly levels so you can easily distinguish between them:

- Prior Day: High / Low / Close

- Current Day: Open

- Prior Week: High / Low / Close

- Current Week: Open

- Prior Month: High / Low / Close

- Current Month: Open

These plots are timeframe dependent and will not plot on subsequently higher timeframes, here is how they work:

Daily Price Levels are only shown on timeframes that are smaller than 60 minutes.

Weekly Price Levels are only shown on timeframes smaller than 1 Day.

Monthly Price Levels are only shown on timeframes smaller than 1 Week.

This way, you can turn on the indicator and not have to think about turning off certain price levels if you switch to a larger / longer timeframe than what you typically use.

For example, Daily OHLC price levels will quickly clutter the 60 minute chart, and likely you don't need to know the HLC of the Prior Day if you are looking at the 60 minute chart. Therefor it may be helpful to automatically hide the Daily price level plots, and only show the Weekly and Monthly plots on the 60 minute timeframe.

I hope you find this indicator helpful, thanks for reading.

day of Month | xilixMonthly Marker (1D Only)

The Monthly Marker indicator automatically highlights a specific day of the month on a daily (1D) chart by drawing a vertical line. Users can select their desired day of the month and customize the line color.

Features:

✅ Marks the chosen day of each month with a vertical line.

✅ Customizable line color (set in the indicator settings).

✅ Helps traders quickly identify key monthly dates.

Note: This indicator will not work on lower timeframes (e.g., 4H, 1H) and will show an error if applied outside the 1D timeframe.

Best Use Cases: Monthly trend tracking, economic event alignment, and custom date-based analysis. 🚀

VWAP Balance Zones - SessionsVWAP Balance Zones Sessions Version is an alternate take on the Original VWAP Balance Zones indicator. The Sessions version allows users to select a specific session to view the VWAP Balance Zones at while still utilizing the full ETH Data.

The Session version provides a better focused display while still maintaining the core functions of the original script with mindful optimizations.

Author's Note: "VBZ Sessions was made with logistics in mind, for the users who only trade within certain times of the day. While it displays the same core concepts, it is not as "Raw" of a display as the Original. For this reason, some users may prefer the Original VWAP Balance Zones, which is why I have opted to release this alternate version instead of updating the original."

> What are VWAP Balance Zones?

"VWAP Balance Zones" is an original concept aimed at identifying the equilibrium area between market participants within the current trend by averaging the Daily Extremes and the Daily VWAP.

Refer to the illustration below for a better understanding of exactly how VWAP Balance Zones are formed:

These zones are displayed for the Daily, Weekly, and Monthly VWAPs, with the most interactive timeframe being the Daily.

> Features

1. The Session Version uses ETH data at all times, and does not solely rely on the chart's data to create the VWAPs or Zones.

This allows the user to focus on a specific trading session, while not losing out on the full VBZ Calculation, with the notable benefit of a cleaner display.

The Original VBZ starts drawing at the beginning of the chart's "Day", and would produce different results when using an RTH chart vs an ETH chart. Along with creating a bird's nest of unusable data at the beginning of the day.

2. Session Start and End lines are displayed for easier identification of the designated trading session.

3. The extreme "Close" Lines are no longer displayed to reduce noise and redundancy.

4. Additionally, the interior VWAP lines are no longer displayed. Ultimately, this was to reduce noise and focus the script on the 50% zones.

5. Weekly and Monthly Zones are now displayed due to the reduced noise!

6. As with the original, the weekly display will yield to the daily, and the monthly display will yield to the weekly.

In the screenshot below, you can observe this behavior.

Enjoy!

D|W|M|Y Breaks with NY TimezoneThis indicator plots breaks for multiple timeframes: Daily, Weekly, Monthly, Quarterly, Half Yearly, Yearly.

I also added the option to change timezone to New York to see the week the ICT way ;)

Daily/Weekly/Monthly LevelsDaily/Weekly/Monthly Levels

TLDR

Shows Daily/Weekly/Monthly reversal levels. These can act as support/resistance levels.

Can only see what's in your candle history. I.e. It won't see old monthlies on your 1m chart! Use Daily to see everything with the most history.

Can only see levels higher than or equal to your current time frame. I.e. it will not see daily levels if you're looking at a weekly chart.

Doesn't keep levels that have been closed through. Does keep levels that have been only wicked.

This indicator shows you daily, weekly and monthly horizontal reversal levels to save you the hassle of doing it yourself. It's a little aid to speed up your TA routine.

Usage Details and Limitations

All daily, weekly, and monthly levels will be marked with lines on the chart automatically. Levels will only be visible from that level's TF or lower, i.e. you can't see the daily levels from the weekly chart, but you can see all levels from daily or lower charts. No levels will be displayed if you select a time frame higher than 1 month.

New levels will not be drawn if they are very close to existing levels. You can change the 'closeness' threshold in settings. It is specified as a percentage move from the existing level.

However, higher TF levels will REPLACE lower TF levels if they are too close. If you set the 'closeness' setting to 0, all levels will be drawn.

Levels will only be drawn if they are in your displayed candle range! I.e. the lower you go in timeframe, the less history you can see, and so levels originating from further back might be missed!

One technique you might have is to load up the daily timeframe and use that to mark any nearby levels of interest.

How does it work?

Basically, it looks for reversal candles on the D/W/M Timeframes, and draws a line for you from the open of the reversal candle (of that TF), so long as you are on a TF equal or lower than that level.

New bars on that TF that close through that TF's old levels will clear that level. Wicks do not clear.

Each newly found level will not be drawn if it's within the percentage distance of an existing level of equal or higher time frame.

Each new level also checks for existing levels on lower TFs that it can replace. E.g. if a monthly bar closes and produces a monthly level equal to an existing daily or weekly level, that daily or weekly level will be replaced. Use the settings to specify your 'closeness' allowance.

Please remember, it can only see as far back as your candle history, so you won't see old monthlies on a 1 minute chart! Use the daily TF to see all three levels at once with maximum history.

Multi-Timeframe Liquidity LevelsMulti-Timeframe Liquidity Levels – Overview

The Multi-Timeframe Liquidity Levels indicator automatically displays significant highs and lows from various timeframes (Daily, Weekly, Monthly, and Quarterly) on your current chart. This allows traders to quickly identify potential support and resistance zones without frequently switching between different timeframe charts. Additionally, the script offers extra lines for special reference points (e.g., the “Midnight” midpoint of the current day and the previous day’s open/close) to highlight potential liquidity zones even more clearly.

1. Core Idea and Benefits

Time-Saving: Instead of manually reviewing charts in different timeframes, the indicator fetches relevant high/low levels automatically and shows them on your active timeframe.

Clear Layout: Traders instantly see where the Daily, Weekly, Monthly, and Quarterly highs and lows lie—areas often associated with institutional orders or liquidity hunts.

Customizable: You can tailor the color scheme, line style (Solid, Dashed, Dotted), and line width, ensuring the displayed levels fit your personal charting style.

2. How It Works

Multi-Timeframe High/Low

For each timeframe (Day, Week, Month, Quarter), the indicator references the previous candle’s high and low (high , low ).

Using request.security(...), these values are plotted on the chart you’re currently viewing.

Flexible Display

You can individually enable or disable the Daily, Weekly, Monthly, and Quarterly lines, depending on which levels are most relevant to your trading.

With Line Style (Solid, Dashed, Dotted) and Line Width, you can easily emphasize certain lines you consider more important.

Additional Lines

“Midnight” Line: A theoretical midpoint between today’s high and low, which can be useful for gauging daily pivot areas.

Previous Day’s Open/Close: Many traders track these reference points to anticipate market reactions. You can show or hide these lines as desired.

Automatic Line Removal & Creation

When a particular timeframe (e.g., “Show Monthly Levels”) is disabled, the script automatically removes the existing monthly lines.

Enabling it again recreates those lines without hassle.

3. Usage and Interpretation

Identifying Support and Resistance

Highs and lows from higher timeframes are often key zones for entries, exits, or major market reactions.

A Daily level may be crucial for short-term traders, whereas Monthly or Quarterly levels can indicate long-term liquidity areas.

Spotting Market Shifts

If price decisively moves above a Higher-Timeframe line, it could signal strong momentum.

Conversely, a failed breakout (where price quickly returns under or above a level) might warn of a potential reversal.

Extra Lines as Filters

The “Midnight” Line helps visualize a rough central price for the current day, aiding in intraday directional bias.

Previous Day’s Open/Close: Common reference points for day traders, where swift approaches and rejections can indicate potential entries or partial take-profit zones.

4. Practical Tips

Use Color-Coding Wisely: Assign distinct colors (e.g., Blue for Daily, Green for Weekly, Orange for Monthly, Purple for Quarterly) so you can easily discern which timeframe you’re looking at.

Toggle On/Off As Needed: Day traders might focus on Daily and Weekly, while long-term traders may pay closer attention to Monthly and Quarterly.

Combine with Price Action: Lines alone don’t constitute a trading strategy. Use them alongside candlestick patterns, volume analysis, or other indicators for a more complete market perspective.

5. Important Notes & Recommendations

Not Financial Advice: This indicator simply reflects historical high/low data across multiple timeframes and does not constitute a buy or sell recommendation.

Trader Responsibility: Observe how the market actually behaves around these lines and adapt your risk management accordingly.

Unlock the Power of Seasonality: Monthly Performance StrategyThe Monthly Performance Strategy leverages the power of seasonality—those cyclical patterns that emerge in financial markets at specific times of the year. From tax deadlines to industry-specific events and global holidays, historical data shows that certain months can offer strong opportunities for trading. This strategy was designed to help traders capture those opportunities and take advantage of recurring market patterns through an automated and highly customizable approach.

The Inspiration Behind the Strategy:

This strategy began with the idea that market performance is often influenced by seasonal factors. Historically, certain months outperform others due to a variety of reasons, like earnings reports, holiday shopping, or fiscal year-end events. By identifying these periods, traders can better time their market entries and exits, giving them an advantage over those who solely rely on technical indicators or news events.

The Monthly Performance Strategy was built to take this concept and automate it. Instead of manually analyzing market data for each month, this strategy enables you to select which months you want to focus on and then executes trades based on predefined rules, saving you time and optimizing the performance of your trades.

Key Features:

Customizable Month Selection: The strategy allows traders to choose specific months to test or trade on. You can select any combination of months—for example, January, July, and December—to focus on based on historical trends. Whether you’re targeting the historically strong months like December (often driven by the 'Santa Rally') or analyzing quieter months for low volatility trades, this strategy gives you full control.

Automated Monthly Entries and Exits: The strategy automatically enters a long position on the first day of your selected month(s) and exits the trade at the beginning of the next month. This makes it perfect for traders who want to benefit from seasonal patterns without manually monitoring the market. It ensures precision in entering and exiting trades based on pre-set timeframes.

Re-entry on Stop Loss or Take Profit: One of the standout features of this strategy is its ability to re-enter a trade if a position hits the stop loss (SL) or take profit (TP) level during the selected month. If your trade reaches either a SL or TP before the month ends, the strategy will automatically re-enter a new trade the next trading day. This feature ensures that you capture multiple trading opportunities within the same month, instead of exiting entirely after a successful or unsuccessful trade. Essentially, it keeps your capital working for you throughout the entire month, not just when conditions align perfectly at the beginning.

Built-in Risk Management: Risk management is a vital part of this strategy. It incorporates an Average True Range (ATR)-based stop loss and take profit system. The ATR helps set dynamic levels based on the market’s volatility, ensuring that your stops and targets adjust to changing market conditions. This not only helps limit potential losses but also maximizes profit potential by adapting to market behavior.

Historical Performance Testing: You can backtest this strategy on any period by setting the start year. This allows traders to analyze past market data and optimize their strategy based on historical performance. You can fine-tune which months to trade based on years of data, helping you identify trends and patterns that provide the best trading results.

Versatility Across Asset Classes: While this strategy can be particularly effective for stock market indices and sector rotation, it’s versatile enough to apply to other asset classes like forex, commodities, and even cryptocurrencies. Each asset class may exhibit different seasonal behaviors, allowing you to explore opportunities across various markets with this strategy.

How It Works:

The trader selects which months to test or trade, for example, January, April, and October.

The strategy will automatically open a long position on the first trading day of each selected month.

If the trade hits either the take profit or stop loss within the month, the strategy will close the current position and re-enter a new trade on the next trading day, provided the month has not yet ended. This ensures that the strategy continues to capture any potential gains throughout the month, rather than stopping after one successful trade.

At the start of the next month, the position is closed, and if the next month is also selected, a new trade is initiated following the same process.

Risk Management and Dynamic Adjustments:

Incorporating risk management with this strategy is as easy as turning on the ATR-based system. The strategy will automatically calculate stop loss and take profit levels based on the market’s current volatility, adjusting dynamically to the conditions. This ensures that the risk is controlled while allowing for flexibility in capturing profits during both high and low volatility periods.

Maximizing the Seasonal Edge:

By automating entries and exits based on specific months and combining that with dynamic risk management, the Ultimate Monthly Performance Strategy takes advantage of seasonal patterns without requiring constant monitoring. The added re-entry feature after hitting a stop loss or take profit ensures that you are always in the game, maximizing your chances to capture profitable trades during favorable seasonal periods.

Who Can Benefit from This Strategy?

This strategy is perfect for traders who:

Want to exploit the predictable, recurring patterns that occur during specific months of the year.

Prefer a hands-off, automated trading approach that allows them to focus on other aspects of their portfolio or life.

Seek to manage risk effectively with ATR-based stop losses and take profits that adjust to market conditions.

Appreciate the ability to re-enter trades when a take profit or stop loss is hit within the month, ensuring that they don't miss out on multiple opportunities during a favorable period.

In summary, the Ultimate Monthly Performance Strategy provides traders with a comprehensive tool to capitalize on seasonal trends, optimize their trading opportunities throughout the year, and manage risk effectively. The built-in re-entry system ensures you continue to benefit from the market even after hitting targets within the same month, making it a robust strategy for traders looking to maximize their edge in any market.

Risk Disclaimer:

Trading financial markets involves significant risk and may not be suitable for all investors. The Monthly Performance Strategy is designed to help traders identify seasonal trends, but past performance does not guarantee future results. It is important to carefully consider your risk tolerance, financial situation, and trading goals before using any strategy. Always use appropriate risk management and consult with a professional financial advisor if necessary. The use of this strategy does not eliminate the risk of losses, and traders should be prepared for the possibility of losing their entire investment. Be sure to test the strategy on a demo account before applying it in live markets.

Bull/Bear Ratio By Month Table [MsF]Japanese below / 日本語説明は英文の後にあります。

-------------------------

This is an indicator that shows monthly bull-bear ratio in a table.

By specifying the start year and end year, the ratio will be calculated and showed based on the number of bullish and bearish lines in the monthly bar. It allows you to analyze the trend of each symbol and month (bullish / bearish). Up to 10 symbols can be specified.

You can take monthly bull-bear ratio for the past 10 or 20 years on the web, but with this indicator, you can narrow it down to the period in which you want to see the symbols you want to see. It is very convenient because you can take statistics at will.

Furthermore, if the specified ratio is exceeded, the font color can be changed to any color, making it very easy to read.

=== Parameter description ===

- From … Year of start of aggregation

- To … Year of end of aggregation

- Row Background Color … Row title background color

- Col Background Color … Column title background color

- Base Text Color … Text color

- Background Color … Background Color

- Border Color … Border Color

- Location … Location

- Text Size … Text Size

- Highlight Threshold … Ratio threshold, and color

- Display in counter? … Check if you want to show the number of times instead of the ratio

-------------------------

月別陰陽確率をテーブル表示するインジケータです。

開始年から終了年を指定することで、月足における陽線数および陰線数を元に確率を計算して表示します。

この機能により各シンボルおよび各月の特徴(買われやすい/売られやすい)を認識することができアノマリー分析が可能です。

シンボルは10個まで指定可能です。

過去10年、20年の月別陰陽確率は、Web上でよく見かけますが、このインジケータでは見たいシンボルを見たい期間に絞って、

自由自在に統計を取ることができるため大変便利です。

なお、指定した確率を上回った場合、文字色を任意の色に変更することができるため、大変見やすくなっています。

=== パラメータの説明 ===

- From … 集計開始年

- To … 集計終了年

- Row Background Color … 行タイトルの背景色

- Col Background Color … 列タイトルの背景色

- Base Text Color … テキストカラー

- Background Color … 背景色

- Border Color … 区切り線の色

- Location … 配置

- Text Size … テキストサイズ

- Highlight Threshold … 色変更する確率の閾値、および色

- Display in counter? … 確率ではなく回数表示する場合はチェックする

Adaptive MFT Extremum Pivots [Elysian_Mind]Adaptive MFT Extremum Pivots

Overview:

The Adaptive MFT Extremum Pivots indicator, developed by Elysian_Mind, is a powerful Pine Script tool that dynamically displays key market levels, including Monthly Highs/Lows, Weekly Extremums, Pivot Points, and dynamic Resistances/Supports. The term "dynamic" emphasizes the adaptive nature of the calculated levels, ensuring they reflect real-time market conditions. I thank Zandalin for the excellent table design.

---

Chart Explanation:

The table, a visual output of the script, is conveniently positioned in the bottom right corner of the screen, showcasing the indicator's dynamic results. The configuration block, elucidated in the documentation, empowers users to customize the display position. The default placement is at the bottom right, exemplified in the accompanying chart.

The deliberate design ensures that the table does not obscure the candlesticks, with traders commonly situating it outside the candle area. However, the flexibility exists to overlay the table onto the candles. Thanks to transparent cells, the underlying chart remains visible even with the table displayed atop.

In the initial column of the table, users will find labels for the monthly high and low, accompanied by their respective numerical values. The default precision for these values is set at #.###, yet this can be adjusted within the configuration block to suit markets with varying degrees of volatility.

Mirroring this layout, the last column of the table presents the weekly high and low data. This arrangement is part of the upper half of the table. Transitioning to the lower half, users encounter the resistance levels in the first column and the support levels in the last column.

At the center of the table, prominently displayed, is the monthly pivot point. For a comprehensive understanding of the calculations governing these values, users can refer to the documentation. Importantly, users retain the freedom to modify these mathematical calculations, with the table seamlessly updating to reflect any adjustments made.

Noteworthy is the table's persistence; it continues to display reliably even if users choose to customize the mathematical calculations, providing a consistent and adaptable tool for informed decision-making in trading.

This detailed breakdown offers traders a clear guide to interpreting the information presented by the table, ensuring optimal use and understanding of the Adaptive MFT Extremum Pivots indicator.

---

Usage:

Table Layout:

The table is a crucial component of this indicator, providing a structured representation of various market levels. Color-coded cells enhance readability, with blue indicating key levels and a semi-transparent background to maintain chart visibility.

1. Utilizing a Table for Enhanced Visibility:

In presenting this wealth of information, the indicator employs a table format beneath the chart. The use of a table is deliberate and offers several advantages:

2. Structured Organization:

The table organizes the diverse data into a structured format, enhancing clarity and making it easier for traders to locate specific information.

3. Concise Presentation:

A table allows for the concise presentation of multiple data points without cluttering the main chart. Traders can quickly reference key levels without distraction.

4. Dynamic Visibility:

As the market dynamically evolves, the table seamlessly updates in real-time, ensuring that the most relevant information is readily visible without obstructing the candlestick chart.

5. Color Coding for Readability:

Color-coded cells in the table not only add visual appeal but also serve a functional purpose by improving readability. Key levels are easily distinguishable, contributing to efficient analysis.

Data Values:

Numerical values for each level are displayed in their respective cells, with precision defined by the iPrecision configuration parameter.

Configuration:

// User configuration: You can modify this part without code understanding

// Table location configuration

// Position: Table

const string iPosition = position.bottom_right

// Width: Table borders

const int iBorderWidth = 1

// Color configuration

// Color: Borders

const color iBorderColor = color.new(color.white, 75)

// Color: Table background

const color iTableColor = color.new(#2B2A29, 25)

// Color: Title cell background

const color iTitleCellColor = color.new(#171F54, 0)

// Color: Characters

const color iCharColor = color.white

// Color: Data cell background

const color iDataCellColor = color.new(#25456E, 0)

// Precision: Numerical data

const int iPrecision = 3

// End of configuration

The code includes a configuration block where users can customize the following parameters:

Precision of Numerical Table Data (iPrecision):

// Precision: Numerical data

const int iPrecision = 3

This parameter (iPrecision) sets the precision of the numerical values displayed in the table. The default value is 3, displaying numbers in #.### format.

Position of the Table (iPosition):

// Position: Table

const string iPosition = position.bottom_right

This parameter (iPosition) sets the position of the table on the chart. The default is position.bottom_right.

Color preferences

Table borders (iBorderColor):

// Color: Borders

const color iBorderColor = color.new(color.white, 75)

This parameters (iBorderColor) sets the color of the borders everywhere within the window.

Table Background (iTableColor):

// Color: Table background

const color iTableColor = color.new(#2B2A29, 25)

This is the background color of the table. If you've got cells without custom background color, this color will be their background.

Title Cell Background (iTitleCellColor):

// Color: Title cell background

const color iTitleCellColor = color.new(#171F54, 0)

This is the background color the title cells. You can set the background of data cells and text color elsewhere.

Text (iCharColor):

// Color: Characters

const color iCharColor = color.white

This is the color of the text - titles and data - within the table window. If you change any of the background colors, you might want to change this parameter to ensure visibility.

Data Cell Background: (iDataCellColor):

// Color: Data cell background

const color iDataCellColor = color.new(#25456E, 0)

The data cells have a background color to differ from title cells. You can configure this is a different parameter (iDataColor). You might even set the same color for data as for the titles if you will.

---

Mathematical Background:

Monthly and Weekly Extremums:

The indicator calculates the High (H) and Low (L) of the previous month and week, ensuring accurate representation of these key levels.

Standard Monthly Pivot Point:

The standard pivot point is determined based on the previous month's data using the formula:

PivotPoint = (PrevMonthHigh + PrevMonthLow + Close ) / 3

Monthly Pivot Points (R1, R2, R3, S1, S2, S3):

Additional pivot points are calculated for Resistances (R) and Supports (S) using the monthly data:

R1 = 2 * PivotPoint - PrevMonthLow

S1 = 2 * PivotPoint - PrevMonthHigh

R2 = PivotPoint + (PrevMonthHigh - PrevMonthLow)

S2 = PivotPoint - (PrevMonthHigh - PrevMonthLow)

R3 = PrevMonthHigh + 2 * (PivotPoint - PrevMonthLow)

S3 = PrevMonthLow - 2 * (PrevMonthHigh - PivotPoint)

---

Code Explanation and Interpretation:

The table displayed beneath the chart provides the following information:

Monthly Extremums:

(H) High of the previous month

(L) Low of the previous month

// Function to get the high and low of the previous month

getPrevMonthHighLow() =>

var float prevMonthHigh = na

var float prevMonthLow = na

monthChanged = month(time) != month(time )

if (monthChanged)

prevMonthHigh := high

prevMonthLow := low

Weekly Extremums:

(H) High of the previous week

(L) Low of the previous week

// Function to get the high and low of the previous week

getPrevWeekHighLow() =>

var float prevWeekHigh = na

var float prevWeekLow = na

weekChanged = weekofyear(time) != weekofyear(time )

if (weekChanged)

prevWeekHigh := high

prevWeekLow := low

Monthly Pivots:

Pivot: Standard pivot point based on the previous month's data

// Function to calculate the standard pivot point based on the previous month's data

getStandardPivotPoint() =>

= getPrevMonthHighLow()

pivotPoint = (prevMonthHigh + prevMonthLow + close ) / 3

Resistances:

R3, R2, R1: Monthly resistance levels

// Function to calculate additional pivot points based on the monthly data

getMonthlyPivotPoints() =>

= getPrevMonthHighLow()

pivotPoint = (prevMonthHigh + prevMonthLow + close ) / 3

r1 = (2 * pivotPoint) - prevMonthLow

s1 = (2 * pivotPoint) - prevMonthHigh

r2 = pivotPoint + (prevMonthHigh - prevMonthLow)

s2 = pivotPoint - (prevMonthHigh - prevMonthLow)

r3 = prevMonthHigh + 2 * (pivotPoint - prevMonthLow)

s3 = prevMonthLow - 2 * (prevMonthHigh - pivotPoint)

Initializing and Populating the Table:

The myTable variable initializes the table with a blue background, and subsequent table.cell functions populate the table with headers and data.

// Initialize the table with adjusted bgcolor

var myTable = table.new(position = iPosition, columns = 5, rows = 10, bgcolor = color.new(color.blue, 90), border_width = 1, border_color = color.new(color.blue, 70))

Dynamic Data Population:

Data is dynamically populated in the table using the calculated values for Monthly Extremums, Weekly Extremums, Monthly Pivot Points, Resistances, and Supports.

// Add rows dynamically with data

= getPrevMonthHighLow()

= getPrevWeekHighLow()

= getMonthlyPivotPoints()

---

Conclusion:

The Adaptive MFT Extremum Pivots indicator offers traders a detailed and clear representation of critical market levels, empowering them to make informed decisions. However, users should carefully analyze the market and consider their individual risk tolerance before making any trading decisions. The indicator's disclaimer emphasizes that it is not investment advice, and the author and script provider are not responsible for any financial losses incurred.

---

Disclaimer:

This indicator is not investment advice. Trading decisions should be made based on a careful analysis of the market and individual risk tolerance. The author and script provider are not responsible for any financial losses incurred.

Kind regards,

Ely

MA + MACD alert TrendsThis is a strategy/combination of warning indicators using 6MA+MACD.

The strategy details are as follows: This is a simple warning strategy created so that we don't have to monitor the candlestick chart too often.

Note: This isn't an entry strategy; it's a signaling strategy for upcoming trends. For maximum efficiency, we should incorporate more formulas into the command. In the case below, I use Fibonacci to enter the command.

This strategy setting works for a 15-minute time frame, but it can still work for different time frames.

It has been working well with Gold and USOIL for the last two years, as well as with currency pairs like EURUSD and many others.

Components:

EMA100 + EMA200 + MA400 + MA800

MACD (timeframe greater than 1 timeframe)

Fibonacci retreat.

Uptrend alert:

Candles on both EMAs (100-200) + 2 SMAs (400-800)

In the previous 80 candles:

EMA100 cross up to EMA200

At the same time, the MACD cross up 0.

The uptrend warning will trigger when EMA6 cuts down to MA10. That's when the price creates the top and we'll wait for the market to go back to the Fibonacci threshold of 0.618 and start buying (or wait for markets to break up the trendline to buy).

Downtrend alert:

Candles are below both EMAs ( 100-200 ) + 2 SMAs ( 400-800 )

In the previous 80 candles:

EMA100 cross down to EMA200

At the same time, the MACD cross down zero.

The downtrend warning will trigger when EMA6 cuts to MA10. That's when the price creates a bottom and we'll wait for the market to go back to the Fibonacci threshold of 0.618 and start selling (or wait for the market to break down the trendline to sell).

Recommended RR: 1:1

If you have any questions please let me know!

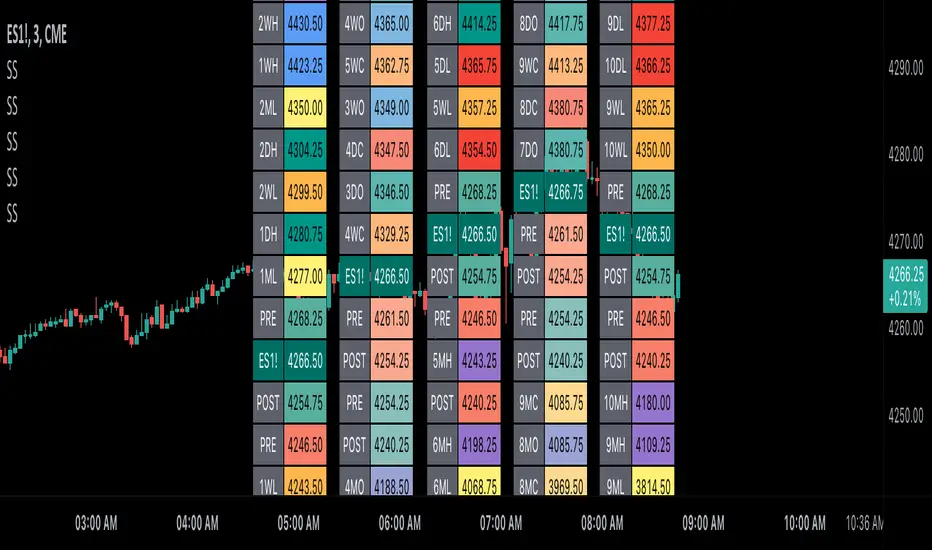

Scoopy StacksWaffle Around Multiple

(Open, High, Low, Close) Stacks On

Pre/Post Market & (Daily, Weekly,

Monthly, Yearly) Sessions With

Meticulous Columns, Rows, Tooltips,

Colors, Custom Ideas, and Alerts.

Sessions Use Two Step Incremental Values

Default Value: (1) Shows Two Previous

(O, H, L, C); Increasing Value Swaps

Sessions With Next Two Stacks.

⬛️ KEY WORDS:

🟢 Crossover | 🔴 Crossunder

📗 High | 📕 Low

📔 Open | 📓 Close

🥇 First Idea | 🥈 Second Idea

🥉 Third Idea | 🎖️ Fourth Idea

🟥 ALERTS:

Default Option: (Per Bar)

Alerts Once Conditions Are Met

(Bar Close) Alerts When Bar Closes

Default Option: (Reg)

Alerts During Regular Market

Trading Hours, (0930-1600)

(Ext) Alerts During Extended

Market Hours, (1600-0930)

(24/7) Alerts All Day

Optional Preferences:

Regular Alerts - Stocks

Extended Alerts - Futures

24/7 Alerts - Crypto

🟧 STACKS:

Default Value: (1)

Incremental Stack Value, Increasing Value

Swaps Sessions With the Next Two Stacks

(✓) Swap Stacks?

Pre/Post Market High/Lows,

1-2 Day High/Lows, 1-2 Week High/Lows,

1-2 Month High/Lows, 1-2 Year High/Lows

( ) Swap Stacks?

Pre/Post Market Open/Close,

1-2 Day Open/Close, 1-2 Week Open/Close,

1-2 Month Open/Close, 1-2 Year Open/Close

🟨 EXAMPLES:

Default Stack:

🟢 | 📗 Pre Market High (PRE) | 4600.00

🔴 | 📕 Post Market Low (POST) | 420.00

Optional: (Open)

🟢 | 📔 Post Market Open (POST) | 4400.00

Optional: (Close)

🔴 | 📓 Pre Market Close (PRE) | 430.00

Default Stack Value: (1)

🔴 | 📗 1 Day High (1DH) | 460.00

Next Stack Value: (3)

🟢 | 📕 4 Day Low (4DL) | 420.00

Optional: (Open)

🔴 | 📔 2 Day Open (2DO) | 440.00

Optional: (Close)

🟢 | 📓 3 Day Close (3DC) | 430.00

Default Stack Value: (5)

🟢 | 📗 5 Week High (5WH) | 460.00

Next Stack Value: (7)

🔴 | 📕 8 Week Low (8WL) | 420.00

Optional: (Open)

🔴 | 📔 7 Week Open (7WO) | 4400.00

Optional: (Close)

🟢 | 📓 6 Week Close (6WC) | 430.00

Default Stack Value: (9)

🔴 | 📗 9 Month High (9MH) | 460.00

Next Stack Value: (11)

🟢 | 📕 12 Month Low (12ML) | 420.00

Optional: (Open)

🟢 | 📔 11 Month Open (11MO) | 4400.00

Optional: (Close)

🔴 | 📓 10 Month Close (10MC) | 430.00

Default Stack Value: (13)

🟢 | 📗 13 Year High (13YH) | 460.00

Next Stack Value: (15)

🟢 | 📕 16 Year Low (16YL) | 420.00

Optional: (Open)

🔴 | 📔 15 Year Open (15YO) | 4400.00

Optional: (Close)

🔴 | 📓 14 Year Close (14YC) | 430.00

🟩 TABLES:

Default Value: (1)

Moves Table Up, Down, Left, or Right

Based on Second Default Value

First Default Value: (Top Right)

Sets Table Placement, Middle Center

Allows Table To Move In All Directions

Second Default Value: (Default)

Fixed Table Position, Switching Values

Moves Direction of the Table

🟦 IDEAS:

(✓) Show Ideas?

Shows Four Ideas With Custom Texts

and Values; Ideas Are Based Around

Post-It Note Reminders with Alerts

Suggestions For Text Ideas:

Take Profit, Stop Loss, Trim, Hold,

Long, Short, Bounce Spot, Retest,

Chop, Support, Resistance, Buy, Sell

🟪 EXAMPLES:

Default Value: (5)

Shows the Custom Table Value For

Sorted Table Positions and Alerts

Default Text: (🥇)

Shown On First Table Cell and

Message Appearing On Alerts

Alert Shows: 🟢 | 🥇 | 5.00

Default Value: (10)

Shows the Custom Table Value For

Sorted Table Positions and Alerts

Default Text: (🥈)

Shown On Second Table Cell and

Message Appearing On Alerts

Alert Shows: 🔴 | 🥈 | 10.00

Default Value: (50)

Shows the Custom Table Value For

Sorted Table Positions and Alerts

Default Text: (🥉)

Shown On Third Table Cell and

Message Appearing On Alerts

Alert Shows: 🟢 | 🥉 | 50.00

Default Value: (100)

Shows the Custom Table Value For

Sorted Table Positions and Alerts

Default Text: (🎖️)

Shown On Fourth Table Cell and

Message Appearing On Alerts

Alert Shows: 🔴 | 🎖️ | 100.00

⬛️ REFERENCES:

Pre-market Highs & Lows on regular

trading hours (RTH) chart

By Twingall

Previous Day Week Highs & Lows

By Sbtnc

Screener for 40+ instruments

By QuantNomad

Daily Weekly Monthly Yearly Opens

By Meliksah55

Ribbit RangesBounce Around Multiple

(Open, High, Low, Close) Ranges

On Pre/Post Market & (Daily, Weekly,

Monthly, Yearly) Sessions With

Meticulous Lines, Labels, Tooltips,

Colors, Custom Ideas, and Alerts.

Sessions Use Two Step Incremental Values

Default Value: (1) Shows Two Previous

(O, H, L, C); Increasing Value Swaps

Sessions With Next Two Ranges.

⬛️ KEY WORDS:

🟢 Crossover | 🔴 Crossunder

📗 High | 📕 Low

📔 Open | 📓 Close

🥇 First Idea | 🥈 Second Idea

🥉 Third Idea | 🎖️ Fourth Idea

🟥 ALERTS:

Default Option: (Per Bar)

Alerts Once Conditions Are Met

(Bar Close) Alerts When Bar Closes

Default Option: (Reg)

Alerts During Regular Market

Trading Hours, (0930-1600)

(Ext) Alerts During Extended

Market Hours, (1600-0930)

(24/7) Alerts All Day

Optional Preferences:

Regular Alerts - Stocks

Extended Alerts - Futures

24/7 Alerts - Crypto

🟧 RANGES:

Default Value: (1)

Incremental Range Value, Increasing Value

Swaps Sessions With the Next Two Ranges

(✓) Swap Ranges?

Pre/Post Market High/Lows,

1-2 Day High/Lows, 1-2 Week High/Lows,

1-2 Month High/Lows, 1-2 Year High/Lows

( ) Swap Ranges?

Pre/Post Market Open/Close,

1-2 Day Open/Close, 1-2 Week Open/Close,

1-2 Month Open/Close, 1-2 Year Open/Close

🟨 EXAMPLES:

Default Range:

🟢 | 📗 Pre Market High (PRE) | 4600.00

🔴 | 📕 Post Market Low (POST) | 420.00

Optional: (Open)

🟢 | 📔 Post Market Open (POST) | 4400.00

Optional: (Close)

🔴 | 📓 Pre Market Close (PRE) | 430.00

Default Range Value: (1)

🔴 | 📗 1 Day High (1DH) | 460.00

Next Range Value: (3)

🟢 | 📕 4 Day Low (4DL) | 420.00

Optional: (Open)

🔴 | 📔 2 Day Open (2DO) | 440.00

Optional: (Close)

🟢 | 📓 3 Day Close (3DC) | 430.00

Default Range Value: (5)

🟢 | 📗 5 Week High (5WH) | 460.00

Next Range Value: (7)

🔴 | 📕 8 Week Low (8WL) | 420.00

Optional: (Open)

🔴 | 📔 7 Week Open (7WO) | 4400.00

Optional: (Close)

🟢 | 📓 6 Week Close (6WC) | 430.00

Default Range Value: (9)

🔴 | 📗 9 Month High (9MH) | 460.00

Next Range Value: (11)

🟢 | 📕 12 Month Low (12ML) | 420.00

Optional: (Open)

🟢 | 📔 11 Month Open (11MO) | 4400.00

Optional: (Close)

🔴 | 📓 10 Month Close (10MC) | 430.00

Default Range Value: (13)

🟢 | 📗 13 Year High (13YH) | 460.00

Next Range Value: (15)

🟢 | 📕 16 Year Low (16YL) | 420.00

Optional: (Open)

🔴 | 📔 15 Year Open (15YO) | 4400.00

Optional: (Close)

🔴 | 📓 14 Year Close (14YC) | 430.00

🟩 COLORS:

(✓) Swap Colors?

Text Color Is Shown Using

Background Color

( ) Swap Colors?

Background Color Is Shown

Using Text Color

🟦 IDEAS:

(✓) Show Ideas?

Plots Four Ideas With Custom Lines

and Labels; Ideas Are Based Around

Post-It Note Reminders with Alerts

Suggestions For Text Ideas:

Take Profit, Stop Loss, Trim, Hold,

Long, Short, Bounce Spot, Retest,

Chop, Support, Resistance, Buy, Sell

🟪 EXAMPLES:

Default Value: (5)

Shows the Custom Value For

Lines, Labels, and Alerts

Default Text: (🥇)

Shown On First Label and

Message Appearing On Alerts

Alert Shows: 🟢 | 🥇 | 5.00

Default Value: (10)

Shows the Custom Value For

Lines, Labels, and Alerts

Default Text: (🥈)

Shown On Second Label and

Message Appearing On Alerts

Alert Shows: 🔴 | 🥈 | 10.00

Default Value: (50)

Shows the Custom Value For

Lines, Labels, and Alerts

Default Text: (🥉)

Shown On Third Label and

Message Appearing On Alerts

Alert Shows: 🟢 | 🥉 | 50.00

Default Value: (100)

Shows the Custom Value For

Lines, Labels, and Alerts

Default Text: (🎖️)

Shown On Fourth Label and

Message Appearing On Alerts

Alert Shows: 🔴 | 🎖️ | 100.00

⬛️ REFERENCES:

Pre-market Highs & Lows on regular

trading hours (RTH) chart

By Twingall

Previous Day Week Highs & Lows

By Sbtnc

Screener for 40+ instruments

By QuantNomad

Daily Weekly Monthly Yearly Opens

By Meliksah55

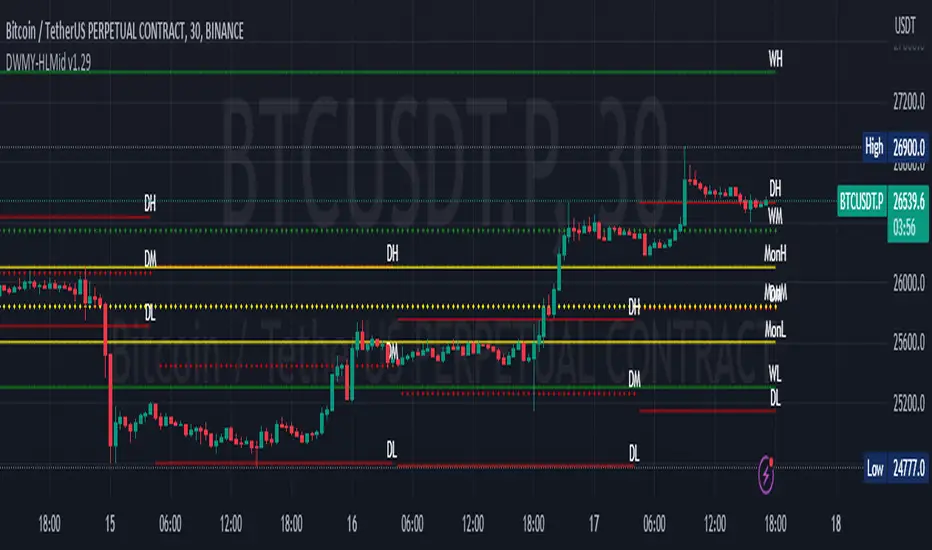

VWAP Balance ZonesVWAP Balance Zones (VBZ) Is based on 3 concepts.

Many Traders use VWAP to help determine Price Trends.

Trends are typically identified by new Highs or new Lows.

Balanced is found when Supply and Demand are mostly Equal.

VBZ tracks the daily, weekly, and monthly highs and lows; Then plots the average (50%) between the VWAP and the respective extremes.

50% VWAP Zones can be considered significant since they attempt to identify the equilibrium between market participants within the current trend, serving as key reference points to consider for decision making. >While in an uptrend, Buyers may see price falling to the Hi 50% as an attractive value entry for the continuation upwards.

>While ALSO in an uptrend, Sellers may see price falling to the Hi 50% as a change in sentiment with more downwards movement on the way.

Because of these conflicting mindsets, these zones are thought to display areas of balance between buyers and sellers, which can serve as potential decision points throughout the day.

VBZ Draws Zones from the Daily (High/Low/Close) VWAPs and the Day's (High/Low/Close) extremes as seen below.

Technically speaking, an average between vwap and extreme is a single point, to make these into zones I am using multiple sources for vwap and tracking different points of the bar throughout the day (ex. Close VWAP & Daily Highest Close)

Weekly and Monthly are only displaying the Average Price between the VWAP and the (Weekly or Monthly) High/Low.

These hold up as important levels for speculation; however, since most action will be discovered at the daily zones, I am not displaying the zones for the Weekly and Monthly to keep noise to a minimum.

Unique Behaviors:

- Weekly values are hidden on the first day of the week since they are similar to the daily values on the first day of the week.

- Monthly values are hidden in the first week of the month for the same reason.

Monthly Range Support & Resistance [QuantVue]The Monthly Range Support & Resistance Levels is an advanced analytical tool designed to assess monthly price movements and provide potential support and resistance levels.

This tool examines the average monthly price fluctuations over the past 7 months (default), and creates support and resistance levels based on the opening price.

The indicator also considers a standard deviation multiplier.

This enables traders and investors to identify potential price zones.

The support and resistance levels are dynamically updated every month.

Users can also choose to view previous daily levels as well.

Customizable settings for this tool include:

-Averaging Period: Adjust the number of months to calculate the average monthly range.

-Standard Deviation Multiplier: Modify the standard deviation multiplier to fine-tune the sensitivity of the support and resistance levels. A higher multiplier will result in wider levels, accommodating higher price fluctuations.

-Toggle Support & Resistance Prices: Easily switch on or off the display of support and resistance price levels.

-Show Monthly Open Line: Display the monthly opening price as a reference point on the chart.

-Show Previous Levels: Choose whether to display past daily support and resistance levels.

Note: this indicator works on a 1 hour timeframe or higher

Give this indicator a BOOST and COMMENT your thoughts!

We hope you enjoy.

Cheers!

Globex, Extended, Daily, Weekly, Monthly, Yearly Range* Adds Right Side Only Price Line & Labels for Tracking without Extending Both Sides

* Tracks Current, Previous, and Two Previous Globex Sessions/ Futures:

* Tracks Current, Previous, and Two Previous Extended Session/ Stocks:

* Tracks Current, Previous, Two, & Three Previous Day Session/ Equities:

* Tracks Current, Last, Two, Three, Four, & Five Week Session/ Equities:

* Tracks Current, Last, Two, Three, Four, & Five Month Session/ Equities:

* Tracks Current, Last, Two, Three, Four, & Five Year Session/ Equities:

* Allows Custom Range on Globex, Extended, & Daily Sessions

* Allows Custom Range on Weekly, Monthly, & Yearly Sessions

* Lines & Labels Are Not Visible on Chart Scales

* Reversible Text & Background Color

* Lines Extend Accordingly with Range

* Labels show Price & Percent Change

* Background Colors should match Chart Color to avoid Overlapping Text & Labels

* Lines have Offset Extension

* Labels have Offset Extension

* Globex Session is only visible on Futures & if Current Timeframe is Intraday

* Extended Session is only visible on Stocks & if Current Timeframe is Intraday

* Daily, Weekly, Monthly, & Yearly Sessions are visible on All Symbols & All Timeframes

* Globex, Extended, & Regular use their Default Time Sessions but allow Customization

* For Back Testing Default Sessions, switch over on the Menu to Style and Turn On/Off their Background Color; Any Area on the Chart Without Background Color is Regular Session

Daily Monday Weekly Monthly Quarterly Yearly High Low Mid This indicator can be useful for traders who are interested in analyzing price movements over different time periods. By displaying the daily, Monday, weekly, monthly, quarterly, and yearly high and low values along with their mid values on a chart, traders can get a better understanding of how prices have behaved over longer periods of time.

For example, a trader might use this information to identify trends or patterns in the market. They might look for occasions when the daily high and low values move outside of an established range or when the weekly or monthly mid values cross certain key levels. This could signal a potential change in the market trend that the trader could act upon.

Additionally, the code can help traders identify key support and resistance levels based on the high and low values of the candles. By plotting these values on a chart, traders can see where prices tend to find support or resistance over different time periods. This information can be used to place stop loss orders or take profit orders at important levels.

Overall, the benefit of using the code you provided is that it offers traders a comprehensive view of price movements over different time periods, which can aid in making more informed trading decisions.

Each level described above has its own unique label, which is abbreviated for convenience. These abbreviations are listed below for quick reference:

For daily levels: DH (Daily High), DM (Daily Mid), and DL (Daily Low)

For Monday levels: MonH (Monday High), MonM (Monday Mid), and MonL (Monday Low)

For monthly levels: MH (Monthly High), MU50 (Monthly 50 percent of Mid and High), MM (Monthly Mid), MD50 (Monthly 50 percent of Mid and Low), and ML (Monthly Low)

For quarterly levels: 3MH (Quarterly High), 3MU50 (Quarterly 50 percent of Mid and High), 3MM (Quarterly Mid), 3MD50 (Quarterly 50 percent of Mid and Low), and 3ML (Quarterly Low)

For yearly levels: YH (Yearly High), YU50 (Yearly 50 percent of Mid and High), YM (Yearly Mid), YD50 (Yearly 50 percent of Mid and Low), and YL (Yearly Low)

These labels can help you quickly identify the different levels and keep track of important price points.

If the chosen timeframe does not fall under the category of intraday, daily and Monday level will not be displayed.

Please feel free to send your suggestions to @z_mehran.

Seasonal Performance for Stocks & CryptoThe Seasonal Performance indicator quickly allows you to see if you are in a bullish or bearish time of year for an underlying security and where the current performance stacks up compared to the same time of year historically. Table is fully customizable from colors to what data to see.

Table Displays

Average Performance

Best Performance

Worst Performance

Last Performance

Current Performance

Note this indicator will only work with Stocks, ETF's, Index's or Crypto.

Monthly Strategy Performance TableWhat Is This?

This script code adds a Monthly Strategy Performance Table to your Pine Script strategy scripts so you can see a month-by-month and year-by-year breakdown of your P&L as a percentage of your account balance.

The table is based on realized equity rather than open equity, so it only updates the metrics when a trade is closed.

That's why some numbers will not match the Strategy Tester metrics (such as max drawdown), as the Strategy Tester bases metrics like max drawdown on open trade equity and not realized equity (closed trades).

The script is still a work-in-progress, so make sure to read the disclaimer below. But I think it's ready to release the code for others to play around with.

How To Use It

The script code includes one of my strategies as an example strategy. You need to replace my strategy code with your own. To do that just copy the source code below into a blank script, delete lines 11 -> 60 and paste your strategy code in there instead of mine. The script should work with most systems, but make sure to read the disclaimer below.

It works best with a significant amount of historical data, so it may not work very effectively on intraday timeframes as there is a severe limitation of available bars on TradingView. I recommend using it on 4HR timeframes and above, as anything less will produce very little usable data. Having a premium TradingView plan will also help boost the number of available bars.

You can hover your mouse over a table cell to get more information in the form of tooltips (such as the Long and Short win rate if you hover over your total return cell).

Credit

The code in this script is based on open-source code originally written by QuantNomad, I've made significant changes and additions to the original script but all credit for the idea and especially the display table code goes to them - I just built on top of it:

Why Did I Make This?

None of this is trading or investment advice, just my personal opinion based on my experience as a trader and systems developer these past 6+ years:

The TradingView Strategy Tester is severely limited in some important ways. And unless you use complex Excel formulas on exported test data, you can't see a granular perspective of your system's historical performance.

There is much more to creating profitable and tradeable systems than developing a strategy with a good win rate and a good return with a reasonable drawdown.

Some additional questions we need to ask ourselves are:

What did the system's worst drawdown look like?

How long did it last?

How often do drawdowns occur, and how quickly are they typically recovered?

How often do we have a break-even or losing month or year?

What is our expected compounded annual growth rate, and how does that growth rate compare to our max drawdown?

And many more questions that are too long to list and take a lifetime of trading experience to answer.

Without answering these kinds of questions, we run the risk of developing systems that look good on paper, but when it comes to live trading, we are uncomfortable or incapable of enduring the system's granular characteristics.

This Monthly Performance Table script code is intended to help bridge some of that gap with the Strategy Tester's limited default performance data.

Disclaimer

I've done my best to ensure the numbers this code outputs are accurate, and according to my testing with my personal strategy scripts it appears to work fine. But there is always a good chance I've missed something, or that this code will not work with your particular system.

The majority of my TradingView systems are extremely simple single-target systems that operate on a closed-candle basis to minimize many of the data reliability issues with the Strategy Tester, so I was unable to do much testing with multiple targets and pyramiding etc.

I've included a Debug option in the script that will display important data and information on a label each time a trade is closed. I recommend using the Debug option to confirm that the numbers you see in the table are accurate and match what your strategy is actually doing.

Always do your own due diligence, verify all claims as best you can, and never take anyone's word for anything.

Take care, and best of luck with your trading :)

Kind regards,

Matt.

PS. If you're interested in learning how this script works, I have a free hour-long video lesson breaking down the source code - just check out the links below this script or in my profile.

Weekly and daily separatorsThis script plots vertical line between each trading week (thick, solid) and smaller lines (dotted) between each trading day. This helps kepping a better overview on the aspect of time on the higher timeframes below 1D. The distance of the lines to the top and bottom of the chart is controlled by your chart settings menu under Appearance -> Margins.

Strategy UtilitiesThis library comprises valuable functions for implementing strategies on TradingView, articulated in a professional writing style.

The initial version features a monthly Profit & Loss table with percentage variations, utilizing a modified version of the script by @QuantNomad.

Library "strategy_utilities"

monthly_table(results_prec, results_dark)

monthly_table prints the Monthly Returns table, modified from QuantNomad. Please put calc_on_every_tick = true to plot it.

Parameters:

results_prec (int) : for the precision for decimals

results_dark (bool) : true or false to print the table in dark mode

Returns: nothing (void), but prints the monthly equity table

Sample Usage

import TheSocialCryptoClub/strategy_utilities/1 as su

results_prec = input(2, title = "Precision", group="Results Table")

results_dark = input.bool(defval=true, title="Dark Mode", group="Results Table")

su.monthly_table(results_prec, results_dark)

Multi-Asset Month/Month % change 10yr Averages10 Year Averages of Month-on-Month % change: Shows current asset, and 3x user input assets

-For comparing seasonal tendencies among different assets.

-Choose from a variety of monthly average measures as source: sma(close, length), sma(ohlc4, length); as well as sma's of vwap, vwma, volume, volatility. (sma = simple moving average).

-Averages based on month cf previous month: i.e. Feb % = Feb compared to Jan; Jan % = Jan compared to prev year's Dec. Average of the last 10yrs of these values is the printed value.

-Plot on current year (2023), or previous year (2022). If Plotting on current year, and a month of year has not yet occured, a 9yr average will be printed.

/// notes ///

-daily bars in month is a global setting; so choose assets which have similar trading days per month. i.e. Crypto: length = 30 (days per month); Stocks/FX/Indices: length = 21 (days per month).

-only plots on Daily timeframe.

10yr Avgs; Plotting with Year = 2022; using sma(close, 21) as source for average M/M change

Buy Sell Calendar [LuxAlgo]The Buy Sell Calendar indicator displays a calendar showing the sentiment for the current day/month. Three different methods can be used to determine this sentiment.

The calendar can also highlight the percentage of bullish days/months for a month/year.

🔶 SETTINGS

Frequency: Calendar frequency, options include "Daily" and "Monthly"

Sentiment Method: Method used to determine the sentiment for the day/month, options include: "Linreg", "Accumulated Deltas", and "Max/Min"

Timezone Offset: UTC time zone offset.

Limit Date: Limit date used by the calendar, the sentiment of days/months outside this limit will not be returned.

🔹 Calendar

Show Calendar: Determines whether to display or hide the calendar.

Location: Location of the calendar on the chart.

Size: Calendar size.

🔶 USAGE

The proposed script can allow users to quickly determine if a specific day/month is considered bullish or bearish. A green cell is used for bullish days/months, while a red one is used for bearish days/months.

Additionally vertical lines are displayed on new days/months with a color highlighting the current sentiment for this specific day/month. Note that this is done retrospectively, the color of a line set at time t might differ at time t+n .

🔶 SENTIMENT METHODS

Determining whether a day/month is bullish or bearish can be done using three different methods. Note that each method makes use of the closing price as the input, and as such can eventually return different results depending on the selected timeframe. Each method is described below:

🔹 Linreg

The Linreg method fit lines between each day/month using the method of least squares and determines if that particular day is bullish or bearish based on the line slope sign. For example, a rising line would indicate a bullish day/month.

🔹 Accumulated Deltas

The method of accumulated deltas simply accumulates bullish and bearish price changes for the current day/month, the result with the highest magnitude determines the sentiment for that day/month.

🔹 Max/Min

The max/min method computes a trailing maximum and a trailing minimum for the current day/month. The sentiment is determined by the price position relative to the average between the obtained maximum/minimum, with a bullish sentiment being determined if price is above the average.