Vector ScalerVector Scaler is like Stochastic but it uses a different method to scale the input. The method is very similar to vector normalization but instead of keeping the "vector" we just sum the three points and average them. The blue line is the signal line and the orange line is the smoothed signal line. I have added the "J" line from the KDJ indicator to help spot divergences. Differential mode uses the delta of the input for the calculations. Here are some pictures to help illustrate how this works relative to other popular indicators.

Vector Scaler vs Stochastic

Vector Scaler vs Smooth Stochastic RSI

average set to 100

average set to 200

Normalize

Leavitt Convolution Slope [CC]The Leavitt Convolution Slope indicator was created by Jay Leavitt (Stocks and Commodities Oct 2019, page 11), who is most well known for creating the Volume-Weighted Average Price indicator. This indicator is very similar to the Leavitt Convolution indicator but the big difference is that it is getting the slope instead of predicting the next Convolution value. I changed quite a few things from the original source code so let me know if you like these changes. I added a normalization function using code from a good friend @loxx that I recommend to leave on but feel free to experiment with it. Last but not least, the unsure levels are essentially acting as a buy or sell threshold. I personally recommend to buy or sell for zero crossovers but another option would be to buy or sell for crossovers using the unsure levels. I have color coded the lines to turn light green for a normal buy signal or dark green for a strong buy signal and light red for a normal sell signal, and dark red for a strong sell signal.

This is another indicator in a series that I'm publishing to fulfill a special request from @ashok1961 so let me know if you ever have any special requests for me.

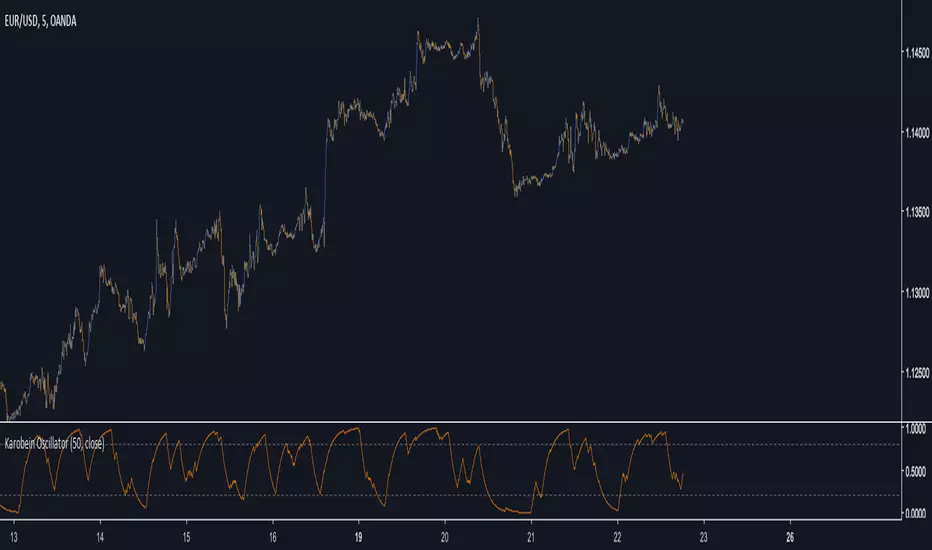

Karobein OscillatorDeveloped by Emily Karobein, the Karobein oscillator is an oscillator that aim to rescale smoothed values with more reactivity in a range of (0,1)

Calculation

The scaling method is similar to the one used in a kalman filter for the kalman gain.

We first average the up/downs x, those calculations are similar to the ones used for calculating the average gain/loss in the relative strength index.

a = ema(src < src ? x : 0,length)

b = ema(src > src ? x : 0,length)

where src is a exponential moving average of length period and x is src/src in the standard calculations, but anything else can be used as long as x > 0 .

Then we rescale the results.

c = x/(x + b)

d = 2*(x/(x + c*a)) - 1

How To Use

It is better to use centerline-cross/breakouts/signal line.

In general when we use something smooth as input in oscillators, breakouts are better than reversals, you can see this with the stochastic and rsi.

So a simple approach could be buying when crossing over 0.8 and selling when crossing under 0.2.

Here is the balance of a strategy using those conditions, length = 50 .

20 trades have been mades since the 29 oct we made 341 pips with eur/usd, of course this backtest was made during good trends period,

this result is not representative of how the strategy work with other conditions/markets.

For any questions/suggestions feel free to contact me

Dollar normalized volumeAn indicator that multiply the closing price with the current volume. (close X volume)

This will show the relative interest in the underlying asset regardless of the price change over time. For the case of FXCM, when the price fell from $16 to $1, its volume spiked 16x at the same time given the fact that 16x more shares can now be purchased with the same amount of dollar.

Enjoy! and remember to give a thumbs up.