F&O Time Zones – Final Fixed📌 This indicator highlights high-probability intraday time zones used in Indian F&O (Futures & Options) strategies. Ideal for scalping, breakout setups, and trap avoidance.

🕒 Covered Time Zones:

• 9:15 – 9:21 AM → Flash Trades (first 1-minute volatility)

• 9:21 – 9:30 AM → Smart Money Trap (VWAP fakeouts)

• 9:30 – 9:50 AM → Fake Breakout Zone

• 9:50 – 10:15 AM → Institutional Entry Timing

• 10:15 – 10:45 AM → VWAP Range Scalps

• 10:45 – 11:15 AM → Second Trap Zone

• 11:15 – 1:00 PM → Trend Continuation Window

• 1:00 – 1:45 PM → Volatility Compression

• 1:45 – 2:15 PM → Institutional Exit Phase 1

• 2:15 – 2:45 PM → Trend Acceleration / Reversals

• 2:45 – 3:15 PM → Expiry Scalping Zone

• 3:15 – 3:30 PM → Dead Zone (square-off time)

🔧 Features:

✓ Clean vertical lines per zone

✓ Optional label positions (top or bottom)

✓ Adjustable line style, width, and color

🧠 Best used on: NIFTY, BANKNIFTY, FINNIFTY (5-min or lower)

---

🔒 **Disclaimer**:

This script is for **educational purposes only**. It is not financial advice. Trading involves risk. Please consult a professional or do your own research before taking any positions.

—

👤 Script by: **JoanJagan**

🛠️ Built in Pine Script v5

Option

IV Rank Oscillator by dinvestorqShort Title: IVR OscSlg

Description:

The IV Rank Oscillator is a custom indicator designed to measure and visualize the Implied Volatility (IV) Rank using Historical Volatility (HV) as a proxy. This indicator helps traders determine whether the current volatility level is relatively high or low compared to its historical levels over a specified period.

Key Features :

Historical Volatility (HV) Calculation: Computes the historical volatility based on the standard deviation of logarithmic returns over a user-defined period.

IV Rank Calculation: Normalizes the current HV within the range of the highest and lowest HV values over the past 252 periods (approximately one year) to generate the IV Rank.

IV Rank Visualization: Plots the IV Rank, along with reference lines at 50 (midline), 80 (overbought), and 20 (oversold), making it easy to interpret the relative volatility levels.

Historical Volatility Plot: Optionally plots the Historical Volatility for additional reference.

Usage:

IV Rank : Use the IV Rank to assess the relative level of volatility. High IV Rank values (close to 100) indicate that the current volatility is high relative to its historical range, while low IV Rank values (close to 0) indicate low relative volatility.

Reference Lines: The overbought (80) and oversold (20) lines help identify extreme volatility conditions, aiding in trading decisions.

Example Use Case:

A trader can use the IV Rank Oscillator to identify potential entry and exit points based on the volatility conditions. For instance, a high IV Rank may suggest a period of high market uncertainty, which could be a signal for options traders to consider strategies like selling premium. Conversely, a low IV Rank might indicate a more stable market condition.

Parameters:

HV Calculation Length: Adjustable period length for the historical volatility calculation (default: 20 periods).

This indicator is a powerful tool for options traders, volatility analysts, and any market participant looking to gauge market conditions based on historical volatility patterns.

NSE Option Chain

This Indicator show Options Data on signal dashboard , that help trader to analyse the market.

Options data consist of two things , Call and Put.

Every Strike has its Call and Put price.

So if user Opens any chart which is traded in options , dashboard will show total 16 Call and 16 Put strikes

8 Above from ATM and 8 Below from ATM.

On left hand side of dashboard there is Call data and on right side there is Put data.

Call side datas are , Call LTP which is latest price of that call strike , Call Chg which is change in points from previous day close and third is Call % which is % change from previous day close.

Same is on put side.

Color code is done based on positive or negative of data. If change or % is negative then color is red else green.

ATM strike data is plotted in bold

Inputs :

Spot Symbol Input for Option dashboard

Expiry date of that option contract

Strike interval between 2 strikes

Reference ATM strike ( user should keep this input as current ATM strike )

How to Use :

If dashboard shows call side is negative and put side is positive then that means market Bearish , because falling market leads to falling price of call and increase in price of Put.

Similarly if put is negative and call is positive then market is bullish.

This dashboard give trend conformation , trader should take other conformation also before taking trade.

SPX IB Intraday Real TimeThis indicator was designed for traders doing Iron Butterflies intradays with the SPX.

Draw and assemble the picture of an IB with the call and put wings chosen according to the selected configuration. Additionally, it shows both breakevens according to the credit obtained.

The indicator shows the distance, in real time, between the current price of the SPX and the breakevens (calls and puts) that have been selected. This result is shown in percentages and points. In the upper right corner (for calls) and lower right (for puts). The label will change color as the price moves closer or further away from the breakevens.

Setting:

Open Time (Hour): IB opening time.

Open Time (Minute): IB opening minutes.

Open Price: Strike to which the center or body of the IB was opened.

Auto Price Open: If enabled, it will take the strike at the price closest to the SPX.

Wings Width: width of the IB wings.

Credit: Refers to the credit obtained according to the IB that was opened.

Shows Breakeven: Shows breakeven points at expiration based on credit earned.

Add SMAs: Adds the SMAs 8, 20 and 50 to the chart.

Note 1: It is recommended to use TradingView's Dark Theme Color.

Note 2: this indicator will only work in intraday times of less than 30 minutes (1m,2m,5m,10m,15m,30m) and will only show results while the market is open, that is, in real time.

************************************

Spanish Version:

Este indicador fue diseñado para los traders que hacen intradías de Iron Butterflies con el SPX.

Dibuja y arma el cuadro de un IB con las alas call y puts elegidas de acuerdo a la configuración seleccionada. Además, muestra ambos breakevens según el crédito obtenido.

El indicador muestra la distancia, en tiempo real, entre el actual precio del SPX y los breakevens (calls y puts) que se hayan seleccionado. Este resultado se muestra en porcentajes y en puntos. En la esquina superior derecha (para los calls) e inferior derecha (para los puts). El label cambiará de color a medida que el precio se acerque o aleje de los breakevens.

Configuración:

Open Time (Hour): Hora de apertura del IB.

Open Time (Minute): Minutos de apertura del IB.

Open Price: Strike al que se abrió el centro o cuerpo del IB.

Auto Price Open: Si se encuentra habilitado tomará el strike al precio más cercano al SPX.

Wings Width: ancho de las alas del IB.

Credit: Se refiere al crédito obtenido según el IB que se abrió.

Shows Breakeven: Muestra los puntos de breakeven en la expiración según el crédito obtenido.

Add SMAs: Agrega al cuadro las SMA 8, 20 y 50.

Nota 1: se recomienda usar el Dark Theme Color de TradingView.

Nota 2: este indicador solo funcionará en temporalidades intradías menores a 30 minutos (1m,2m,5m,10m,15m,30m) y solo mostrará resultados mientras el mercado esté abierto, o sea en tiempo real.

Supertrend x4 w/ Cloud FillSuperTrend is one of the most common ATR based trailing stop indicators.

The average true range (ATR) plays an important role in 'Supertrend' as the indicator uses ATR to calculate its value. The ATR indicator signals the degree of price volatility. In this version you can change the ATR calculation method from the settings. Default method is RMA, when the alternative method is SMA.

The indicator is easy to use and gives an accurate reading about an ongoing trend. It is constructed with two parameters, namely period and multiplier.

The implementation of 4 supertrends and cloud fills allows for a better overall picture of the higher and lower timeframe trend one is trading a particular security in.

The default values used while constructing a supertrend indicator is 10 for average true range or trading period.

The key aspect what differentiates this indicator is the Multiplier. The multiplier is based on how much bigger of a range you want to capture. In our case by default, it starts with 2.636 and 3.336 for Set 1 & Set 2 respectively giving a narrow band range or Short Term (ST) timeframe visual. On the other hand, the multipliers for Set 3 & Set 4 goes up to 9.736 and 8.536 for the multiplier respectively giving a large band range or Long Term (LT) timeframe visual.

A ‘Supertrend’ indicator can be used on equities, futures or forex, or even crypto markets and also on minutes, hourly, daily, and weekly charts as well, but generally, it fails in a sideways-moving market. That's why with this implementation it enables one to stay out of the market if they choose to do so when the market is ranging.

This Supertrend indicator is modelled around trends and areas of interest versus buy and sell signals. Therefore, to better understand this indicator, one must calibrate it to one's need first, which means day trader (shorter timeframe) vs swing trader (longer time frame), and then understand how it can be utilized to improve your entries, exits, risk and position sizing.

Example:

In this chart shown above using SPX500:OANDA, 15R Time Frame, we can see that there is at any give time 1 to 4 clouds/bands of Supertrends. These four are called Set 1, Set 2, Set 3 and Set 4 in the indicator. Set's 1 & 2 are considered short term, whereas Set's 3 & 4 are considered long term. The term short and long are subjective based on one's trading style. For instance, if a person is a 1min chart trader, which would be short term, to get an idea of the trend you would have to look at a longer time frame like a 5min for instance. Similarly, in this cases the timeframes = Multiplier value that you set.

Optional Ideas:

+ Apply some basic EMA/SMA indicator script of your choice for easier understanding of the trend or to allow smooth transition to using this indicator.

+ Split the chart into two vertical layouts and applying this same script coupled with xdecow's 2 WWV candle painting script on both the layouts. Now you can use the left side of the chart to show all bearish move candles only (make the bullish candles transparent) and do the opposite for the right side of the chart. This way you enhance focus to just stick to one side at a given time.

Credits:

This indicator is a derivative of the fine work done originally by KivancOzbilgic

Here is the source to his original indicator: ).

Disclaimer:

This indicator and tip is for educational and entertainment purposes only. This not does constitute to financial advice of any sort.

Options Price CalculatorIn the team, we continue to explore and expand the boundaries of TradingView.

For now, there is not much an options trader can do with options in TradingView.

We wanted to change that and created a simple option pricer.

You can set up in parameters a set of strikes, implied volatility, and days to expiry.

The indicators will take a risk-free rate from US01Y and the underlying price from your current chart.

It will compute prices and greeks for both put and call options.

Thanks to @MUQWISHI for helping code it.

Disclaimer

Please remember that past performance may not indicate future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

Cox-Ross-Rubinstein Binomial Tree Options Pricing Model [Loxx]Cox-Ross-Rubinstein Binomial Tree Options Pricing Model is an options pricing panel calculated using an N-iteration (limited to 300 in Pine Script due to matrices size limits) "discrete-time" (lattice based) method to approximate the closed-form Black–Scholes formula. Joshi (2008) outlined varying binomial options pricing model furnishes a numerical approach for the valuation of options. Significantly, the American analogue can be estimated using the binomial tree. This indicator is the complex calculation for Binomial option pricing. Most folks take a shortcut and only calculate 2 iterations. I've coded this to allow for up to 300 iterations. This can be used to price American Puts/Calls and European Puts/Calls. I'll be updating this indicator will be updated with additional features over time. If you would like to learn more about options, I suggest you check out the book textbook Options, Futures and other Derivative by John C Hull.

***This indicator only works on the daily timeframe!***

A quick graphic of what this all means:

In the graphic, "n" are the steps, in this case we can do up to 300, in production we'd need to do 5-15K. That's a lot of steps! You can see here how the binomial tree fans out. As I said previously, most folks only calculate 2 steps, here we are calculating up to 300.

Want to learn more about Simple Introduction to Cox, Ross Rubinstein (1979) ?

Watch this short series "Introduction to Basic Cox, Ross and Rubinstein (1979) model."

Limitations of Black Scholes options pricing model

This is a widely used and well-known options pricing model, factors in current stock price, options strike price, time until expiration (denoted as a percent of a year), and risk-free interest rates. The Black-Scholes Model is quick in calculating any number of option prices. But the model cannot accurately calculate American options, since it only considers the price at an option's expiration date. American options are those that the owner may exercise at any time up to and including the expiration day.

What are Binomial Trees in options pricing?

A useful and very popular technique for pricing an option involves constructing a binomial tree. This is a diagram representing different possible paths that might be followed by the stock price over the life of an option. The underlying assumption is that the stock price follows a random walk. In each time step, it has a certain probability of moving up by a certain percentage amount and a certain probability of moving down by a certain percentage amount. In the limit, as the time step becomes smaller, this model is the same as the Black–Scholes–Merton model.

What is the Binomial options pricing model ?

This model uses a tree diagram with volatility factored in at each level to show all possible paths an option's price can take, then works backward to determine one price. The benefit of the Binomial Model is that you can revisit it at any point for the possibility of early exercise. Early exercise is executing the contract's actions at its strike price before the contract's expiration. Early exercise only happens in American-style options. However, the calculations involved in this model take a long time to determine, so this model isn't the best in rushed situations.

What is the Cox-Ross-Rubinstein Model?

The Cox-Ross-Rubinstein binomial model can be used to price European and American options on stocks without dividends, stocks and stock indexes paying a continuous dividend yield, futures, and currency options. Option pricing is done by working backwards, starting at the terminal date. Here we know all the possible values of the underlying price. For each of these, we calculate the payoffs from the derivative, and find what the set of possible derivative prices is one period before. Given these, we can find the option one period before this again, and so on. Working ones way down to the root of the tree, the option price is found as the derivative price in the first node.

Inputs

Spot price: select from 33 different types of price inputs

Calculation Steps: how many iterations to be used in the Binomial model. In practice, this number would be anywhere from 5000 to 15000, for our purposes here, this is limited to 300

Strike Price: the strike price of the option you're wishing to model

% Implied Volatility: here you can manually enter implied volatility

Historical Volatility Period: the input period for historical volatility; historical volatility isn't used in the CRRBT process, this is to serve as a sort of benchmark for the implied volatility,

Historical Volatility Type: choose from various types of implied volatility, search my indicators for details on each of these

Option Base Currency: this is to calculate the risk-free rate, this is used if you wish to automatically calculate the risk-free rate instead of using the manual input. this uses the 10 year bold yield of the corresponding country

% Manual Risk-free Rate: here you can manually enter the risk-free rate

Use manual input for Risk-free Rate? : choose manual or automatic for risk-free rate

% Manual Yearly Dividend Yield: here you can manually enter the yearly dividend yield

Adjust for Dividends?: choose if you even want to use use dividends

Automatically Calculate Yearly Dividend Yield? choose if you want to use automatic vs manual dividend yield calculation

Time Now Type: choose how you want to calculate time right now, see the tool tip

Days in Year: choose how many days in the year, 365 for all days, 252 for trading days, etc

Hours Per Day: how many hours per day? 24, 8 working hours, or 6.5 trading hours

Expiry date settings: here you can specify the exact time the option expires

Take notes:

Futures don't risk free yields. If you are pricing options of futures, then the risk-free rate is zero.

Dividend yields are calculated using TradingView's internal dividend values

This indicator only works on the daily timeframe

Included

Option pricing panel

Loxx's Expanded Source Types

Breakeven rectangle overlay for move contractI'm sharing this little script allowing you to display a breakeven rectangle for the move contract after manually writing your parameters (strike price, contract price). In case you are long your breakeven (at expiration) is when the price expire outside the rectangle. In case you are short your breakeven (again at expiration) is when the price is staying inside the rectangle at expiration. You can change multiple personalisation parameters as you wish.

SPY Option returns calculations This script allows you to calculate returns on double butterfly options, specifically for 0 DTE and 1 DTE(days to expiration) for options that have expiration on Monday, Tuesday and Friday(Mostly SPY). The script is bi-directional, meaning it will calculate the returns on a put and call butterfly simultaneously, not just a put or just a call butterfly. The script was developed to calculate how much return could be made on opening a double butterfly option by opening a position right at the open of the day on a 0 DTE option. The script rounds the price up or down to the nearest strike price at open. From there you would need to chose how far to select your options from the opening strike price. You would also need to select how many contracts you would like to open, negative - is selling an option positive + is buying an option. As an example the script is defaulted to a 0,2,4 strike position with buying 1 contract at the 0, selling 3 contracts at the +/- 2 strike and selling 2 contracts at the +/- strike. The default is set to an unbalanced double butterfly as it allows a better credit collection than a standard butterfly. To change to a standard butterfly change the # of contracts to 1 -2 and 1 respectively.

The script defaults a return of 0 on Tuesdays and Thursdays as there are no 0 DTE options available on those days.

If you have questions about script ask ... if you have questions about options ... the answers will likely take too much time to answer.

Doms 0dte/hassan conversion v2 Hello Guys

This is a reupload!

The 0dte is for options trading and is used for the main 1 to 0 odte strategy!

It uses volume, sector and tik analysis in order to give an understanding of looking which way to play.

The next version will look at correlations between the es! Feel free to point out bugs and reach out as I want this to grow into something way stronger!

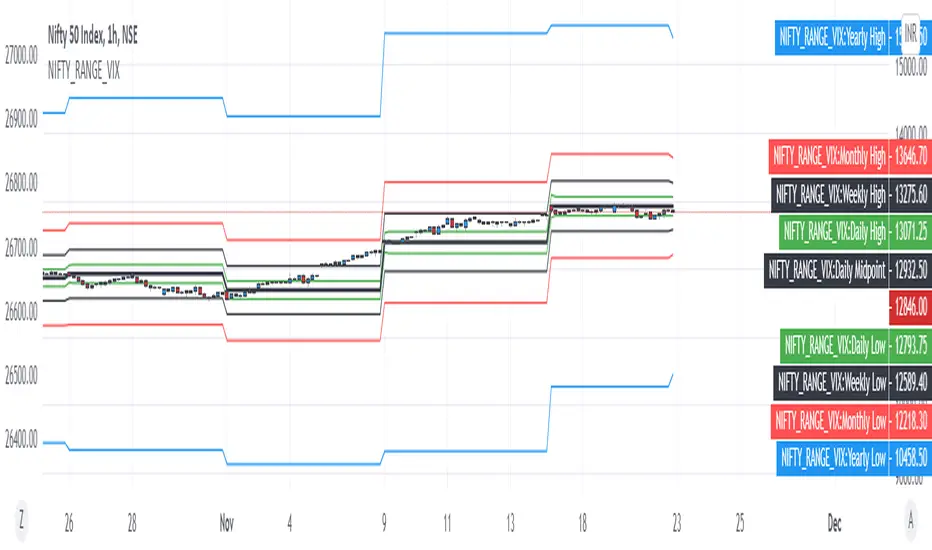

NIFTY VIX BANDSThis script can be used to visually identify the 1 standard deviation range of price movement anticipated by NSE ticker for Volatility Index NSE:INDIAVIX

Ideal to use on NSE:NIFTY ticker only!

The NIFTY range is extended to Yearly, Monthly, Weekly, Daily based on the current value of INDIAVIX.

All options are customizable:

Time frame of the VIX Bands

Select / De-select of Plots for Yearly, Monthly Weekly and Daily

Nifty Expiry Day Vikas DhariwalStrategy for Expiry day plan

Here you can find easy expiry day of nifty and bank nifty

mark Thursday with color to find that day for test any expiry strategy plan

thanks call for more updated 8287335651

Commercial Short IndexThis script takes the hedger (commercial short) from the COT report and normalize the chart for configurable time frames (e.g. 26 weeks, 152 weeks and 260 weeks).

Based on the "Commercial Index-Buschi" script by MagicEins.

UCS_3rd FridaySimple script to show you a way to find 3rd Fridays (Monthly Options Expiry)

If that friday is a holiday, then it doesn't generate a signal. Futures & Forex trader need not to worry. I will fix it for the stock traders as well. Time is all I need.

as usual Good Luck for those who believe in it. Practice for those who believe in hard work. Think for those who believe in smart work. ;)

Binary Option Arrows (example) [TheMightyChicken]An example of binary option arrows for candlestick patterns bearish and bullish harami. With results as colored background and an option to choose your expiration (one candle by default). It's just an example for those who has their own strategy and wants to make nice arrows in their chart. All you need to do is rewrite piece of script in lines 9:13 - feel free to ask me for any help, but I believe it's all clear.

Disclaimer: It's just an example how to script arrows for binary option and I am not responsible for any loss of money by using this particular strategy.

I wish happy and successful trading! ;)

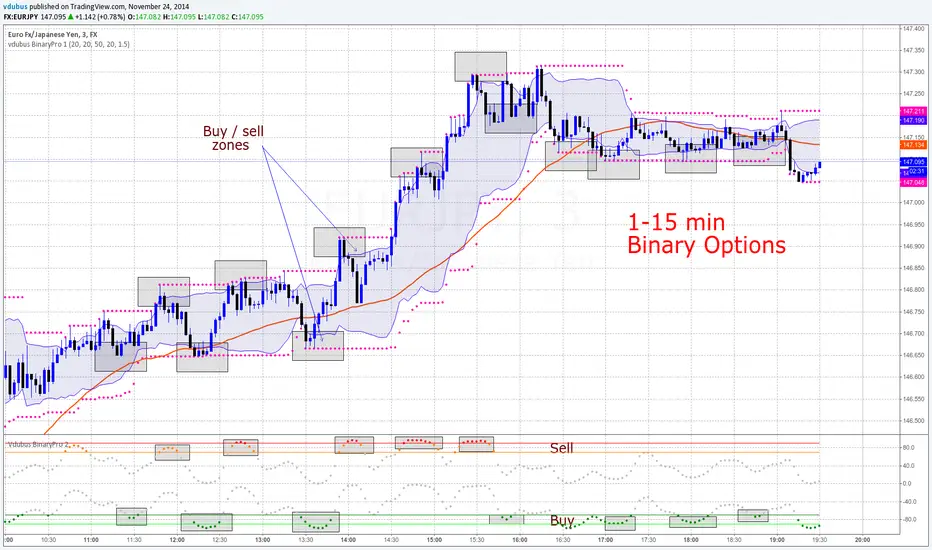

vdubus BinaryPro - Indicators 1 & 2For both scripts - Go to 'MAKE IT MINE'

Modified scripts for Binary trading 1- 3 min charts / 5 -15 min intervals

vdubus BinaryPro 1

Vdubus BinaryPro 2

------------------------------

Vdubus BinaryPro Money Management Strategy: $10 - $50,000 in 15 trades

Tip * break consecutive trades down to lots of 5 compounded / repeat to build up a solid equity foundation., then move on the the next 5 x 3 = 15

if you lose one trade out of the 5, restart the proses. You only ever lose the initial trade size you started with * DOUBLE YOUR WINNINGS NOT YOUR LOSSES !

If you struggle to win 5 compounded trades in a row, compound 2 or 3 trades at a time

drive.google.com