Line Chart ShiftedThis indicator is designed to assist traders who rely on both line charts and candlestick patterns in their technical analysis. By plotting the closing price from previous bars and shifting it left by a customizable amount, this indicator overlays a line chart directly onto a candlestick chart, giving traders a clearer view of trends and key levels.

Key Features:

Shifted Close Price: The line is plotted based on the closing prices of the previous 3 candles, providing an advanced view of the market's price movements.

Customizable Line Width and Color: Traders can easily modify the thickness and color of the line to match their charting style or improve visibility when analyzing price action.

How It Helps:

Combines Line and Candlestick Charts: For traders who analyze both line and candlestick charts, this indicator provides an effective way to see how price has been evolving, helping to identify support, resistance, and trend lines more easily.

Enhanced Visualization: By shifting the line slightly to the left, the overlay offers a clean separation between the current candlestick and the historical line, improving clarity and making it easier to spot trends.

Options

US Market Support & ResistanceUS Market Support & Resistance Indicator (For 5-30 Minute Timeframes)

This indicator plots key support and resistance levels for the US market based on the high and low of the first candle at the market open. It also shades the area between these levels with a color that dynamically changes to indicate the current trend:

* Green: Price is above the resistance level, suggesting a potential uptrend.

* Red: Price is below the support level, suggesting a potential downtrend.

* Gray: Price is trading between the support and resistance levels, suggesting a sideways trend.

Additionally, the indicator displays a small dashboard in the top right corner of the chart showing the current trend ("Upward", "Downward", or "Sideways") in the corresponding color.

Key Features:

* US Market Time Identification: Accurately identifies US market open and close times in UTC and colors candles red during these times.

* Support & Resistance Plotting: Plots support and resistance lines at the high and low of the first candle at the market open and extends them infinitely on the chart.

* Shaded Area Between Levels: Shades the area between the support and resistance lines with a color that dynamically changes based on the current price location relative to these levels.

* Trend Display: Displays a dashboard showing the current trend based on the shaded area's color.

* Open Alert: Issues an alert when the US market opens.

* Supported Timeframes: Works on timeframes less than 30 minutes and greater than 5 minutes.

* Economic News: Not recommended for use during periods of sporadic economic news releases, as sudden price fluctuations may cause false signals.

How to Use:

* Add the indicator to your chart, ensuring the timeframe is between 5 and 30 minutes.

* Wait for the US market to open.

* Observe the shaded area's color and the dashboard to identify the current trend.

* Use the support and resistance levels to make trading decisions, keeping in mind not to rely solely on it during news releases.

Caution: This indicator relies on support and resistance levels drawn at the US market open and may not always be accurate, especially during periods of high volatility. It should be used in conjunction with other technical analysis tools to confirm the trend and make informed trading decisions.

Note: This description is designed to be compliant with TradingView's policies on indicator publishing.

Tomorrow Floor Pivots with CPR By Nifty ZThe colors for resistance and support levels have been updated to gradient reds and greens for clearer distinction.

The CPR band uses light blue and purple to stand out more effectively.

Here's a detailed explanation of the user inputs and the typical use of **Floor Pivots for Tomorrow’s Market Range** in a trading context, focusing on support, resistance, and breakout scenarios:

The script allows traders to customize key parameters for their analysis:

1. Pivot Timeframe:

- Users can select different timeframes for calculating floor pivots, such as 1 hour, 4 hours, daily, weekly, monthly, etc.

- This is crucial because the timeframe selection influences the granularity of the support and resistance levels for the next trading day.

- For instance, selecting a **Daily** timeframe will calculate floor pivots for the next trading day, while selecting **Weekly** will give levels for the upcoming week.

2. Show Floor Pivots:

- Users can toggle the visibility of the calculated **Floor Pivots**, which include resistance levels (R1, R2, R3, R4) and support levels (S1, S2, S3, S4).

3. Show CPR (Central Pivot Range):

- CPR (Central Pivot Range) is a key area where the price tends to consolidate.

- The script allows users to enable or disable the visibility of CPR, which consists of the BC (Bottom Central Pivot) and TC (Top Central Pivot).

4. Show Labels:

- Users can choose whether or not to display labels indicating the **Pivot**, **Support**, and Resistance levels on the chart. This can be helpful for visual analysis when day trading.

Understanding Floor Pivots

The Floor Pivots (Pivot, Resistance, and Support levels) for tomorrow's market range are calculated based on today’s high, low, and close. These levels help traders anticipate how the market may behave in the upcoming session.

1. Pivot:

- The Pivot Point is a central level, calculated as the average of the high, low, and close. It’s considered a reference point that determines the market’s overall bias.

- If the price is trading **above the pivot**, it generally suggests a **bullish** sentiment for the day.

- If the price is trading **below the pivot**, it suggests a **bearish** sentiment.

2. Resistance Levels (R1, R2, R3, R4):

- R1 is often the first area where price may stall in an uptrend. It represents the first major resistance level.

- **R2**, **R3**, and **R4** mark additional levels of resistance, progressively further away from the current price. These are used to project potential upward targets.

- These resistance levels are areas where the price might encounter selling pressure, especially during day trading.

3. **Support Levels (S1, S2, S3, S4):**

- Similarly, **S1** is the first area where the price might find support in a downtrend.

- **S2**, **S3**, and **S4** provide deeper support levels where the price may bounce from.

- These support zones are used by day traders to anticipate where the price might reverse upward.

### **Role of Resistance and Support in Day Trading**

- **Resistance Levels (R1, R2, R3, R4)** indicate potential areas where price could **stall** during an uptrend. These levels are useful for **short-term traders** looking to set exit points or identify reversal zones.

- **Support Levels (S1, S2, S3, S4)** highlight areas where the price could **find support** and potentially **bounce** higher. These levels are particularly helpful for identifying buy zones in a downtrend.

- If a price **breaks out** above the resistance levels or **breaks down** below the support levels, it often signals a strong trend continuation.

### **Understanding the Central Pivot Range (CPR)**

The **CPR** is formed by two key levels:

- **BC (Bottom Central Pivot):** The midpoint of the day’s high and low.

- **TC (Top Central Pivot):** The difference between the pivot and BC.

The CPR acts as a region of **consolidation** or **indecision** where the market is likely to stay within a narrow range. The width of the CPR gives traders a sense of volatility:

- A **narrow CPR** often signals that a **breakout** is imminent.

- A **wider CPR** suggests that the market could remain range-bound.

### **Market Sentiment Based on Floor Pivots**

The relationship between **today’s** and **tomorrow’s pivots** is crucial in determining the market sentiment for the next day.

1. **Bullish Case (Higher Highs):**

- If **tomorrow's pivot** is higher than **today's pivot**, it indicates a **bullish sentiment**. This suggests that the market is likely to trend upward in the next session.

- In a **bullish overlapping pivot range**, if **Day 1 (today)** is higher than **Day 2 (tomorrow)**, traders expect continued upward momentum.

2. **Bearish Case (Lower Lows):**

- Conversely, if **tomorrow's pivot** is lower than **today's pivot**, it suggests a **bearish sentiment** and that the market could trend downward in the next session.

- In a **bearish overlapping pivot range**, if **Day 1 (today)** is lower than **Day 2 (tomorrow)**, traders expect continued downward pressure.

### **Breakout Scenarios**

A breakout occurs when the price **violates either the support or resistance levels** significantly, indicating that the price is moving in the direction of the breakout.

1. **Bullish Breakout:**

- If the price consistently stays **above the CPR** and **resistance levels (R1, R2)**, it indicates a strong **bullish breakout**.

- This is especially true when the **CPR is narrow** for both days, signaling a buildup in price action and a potential breakout to the upside.

2. **Bearish Breakout:**

- If the price breaks **below the CPR** and **support levels (S1, S2)**, it indicates a **bearish breakout**.

- A narrow CPR on **both days** suggests that a breakout to the downside could be imminent.

3. **Neutral or Ranging Days:**

- Sometimes, the CPR stays **unchanged** for 4-5 days, indicating a period of **consolidation** where the price is moving within a tight range. This often leads to a significant breakout once the consolidation ends.

Strategic Application of Floor Pivots for Tomorrow

Traders use floor pivots to plan their next-day trades by:

- **Aligning with Market Sentiment:** Based on whether tomorrow’s pivot is higher or lower than today’s, traders can align their trades in the direction of the market’s overall bias.

- **Identifying Entry and Exit Points:** Resistance and support levels provide well-defined areas to enter or exit trades, making pivots essential for day trading strategies.

- **Anticipating Breakouts:** Monitoring the width of the CPR and the relation between pivots helps traders anticipate potential breakouts, allowing them to react quickly to sudden price movements.

By effectively using these pivots and understanding their significance, traders can improve their decision-making for short-term trades in the stock or futures markets.

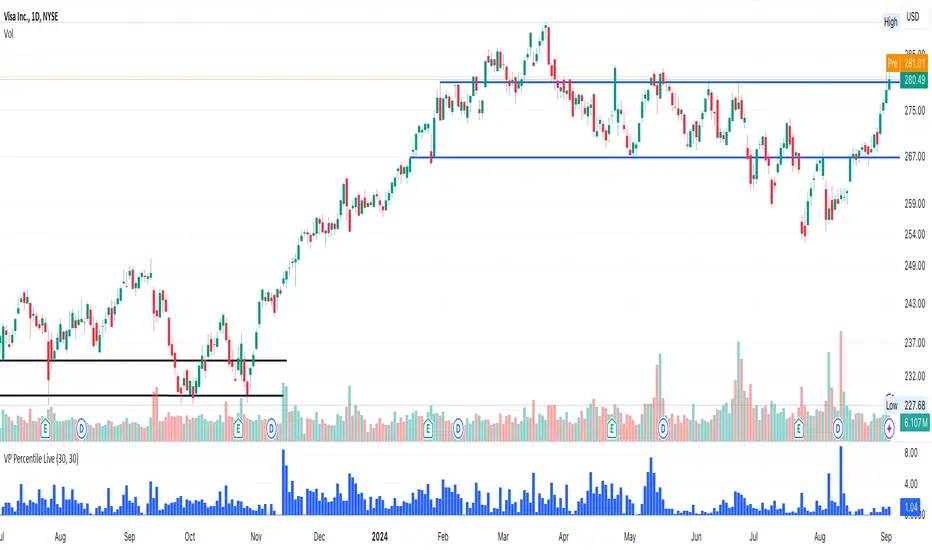

Volume-Price PercentileDescription:

The "Volume-Price Percentile Live" indicator is designed to provide real-time analysis of the relationship between volume percentiles and price percentiles on any given timeframe. This tool helps traders assess market activity by comparing how current volume levels rank relative to historical volume data and how current price movements (specifically high-low ranges) rank relative to historical price data. The indicator visualizes the ratio of volume percentile to price percentile as a histogram, allowing traders to gauge the relative strength of volume against price movements in real time.

Functionality:

Volume Percentile: Calculates the percentile rank of the current volume within a user-defined rolling period (default is 30 bars). This percentile indicates where the current volume stands in comparison to historical volumes over the specified period.

Price Percentile: Calculates the percentile rank of the current candle's high-low difference within a user-defined rolling period (default is 30 bars). This percentile reflects the current price movement's strength relative to past movements over the specified period.

Percentile Ratio (VP Ratio): The indicator plots the ratio of the volume percentile to the price percentile. This ratio helps identify periods when volume is significantly higher or lower relative to price movement, providing insights into potential market imbalances or strength.

Real-Time Data: By fetching data from a lower timeframe (e.g., 1-minute), the indicator updates continuously within the current timeframe, offering live, intra-candle updates. This ensures that traders can see the histogram change in real-time as new data becomes available, without waiting for the current candle to close.

How to Use:

Adding the Indicator: To use this indicator, add it to your chart on TradingView by selecting it from the Indicators list once it is published publicly.

Setting Parameters:

Volume Period Length: This input sets the rolling window length for calculating the volume percentile (default is 30). You can adjust it based on the desired sensitivity or historical period relevance.

Candle Period Length: This input sets the rolling window length for calculating the price percentile based on the high-low difference of candles (default is 30). Adjust this to match your trading style or analysis period.

Interpreting the Histogram:

The histogram represents the volume percentile divided by the price percentile.

Above 1: A value greater than 1 indicates that volume is relatively strong compared to price movement, which may suggest high activity or potential accumulation/distribution phases.

Below 1: A value less than 1 suggests that price movement is relatively stronger than volume, indicating potential weakness in volume relative to price moves.

Near 1: Values close to 1 suggest a balanced relationship between volume and price movement.

Application: Use this indicator to identify potential breakout or breakdown scenarios, assess the strength of price movements, and confirm trends. When volume percentile consistently leads price percentile, it might signal sustained interest and support for the current price trend. Conversely, if volume percentile lags significantly, it might warn of potential trend weakness.

Best Practices:

Multiple Timeframe Analysis: While the indicator provides real-time updates on any timeframe, consider using it alongside higher timeframe analysis to confirm trends and volume behavior across different periods.

Customization: Adjust the period lengths based on the asset’s typical volume and price behavior, as well as your trading strategy (e.g., short-term scalping vs. long-term trend following).

Complement with Other Indicators: Use this indicator in conjunction with other volume-based tools, trend indicators, or momentum oscillators to gain a comprehensive view of market dynamics.

Theta Shield | Flux Charts💎 GENERAL OVERVIEW

Introducing our new Theta Shield indicator! Theta is the options risk factor concerning how fast there is a decline in the value of an option over time. This indicator aims to help the trader avoid sideways market phases in the current ticker, to minimize the risk of theta decay. For more information, please check the "How Does It Work" section.

Features of the new Theta Shield Indicator :

Foresight Of Accumulation Zones

Decrease Risk Of Theta Decay

Clear "Valid" & "Non-Valid" Signals

Validness Trail

Alerts

📌 HOW DOES IT WORK ?

In options trading, theta is defined as the rate of decline in the value of an option due to the passage of time. Traders want to avoid this kind of decay in the value of an option. One of the best ways to avoid it is not holding an option contract when the market is going sideways. This indicator uses a stochastic oscillator to try to get a foresight of sideways markets, warning the trader to not hold an option contract while the price is in a range.

The indicator starts by calculating the stochastic value using close, high & low prices of the candlesticks. Then a stoch threshold & a theta length are determined depending on the option contract type defined by the user in the settings of the indicator. Each candlestick that falls above or below the stoch threshold value is counted, and a "theta valid strength" is calculated using the counted candlesticks, which has a value between -100 & 100. Here is the formula of the "theta valid strength" value :

f_lin_interpolate(float x0, float x1, float y0, float y1, float x) =>

y0 + (x - x0) * (y1 - y0) / (x1 - x0)

thetaValid = Total Candlesticks That Fall Above & Below The Threshold In Last "Theta Length" bars.

thetaValidStrength = f_lin_interpolate(0, thetaLength, -100, 100, thetaValid)

Then a trail is rendered, and "Valid" & "Non-Valid" signals are given using this freshly calculated strength value. Valid means that the indicator currently thinks that no accumulation will happen in the near future, so the option positions in the current ticker are protected from the theta decay. Non-Valid means that the indicator thinks the ticker has entered the accumulation phase, so holding any option position is not recommended, as they may be affected by the theta decay.

🚩 UNIQUENESS

This indicator offers a unique way to avoid theta decay in options trading. It uses a stochastic oscillator and thresholds to calculate a "theta strength" value, which is used for rendering validness signals and a trail. Traders can follow the valid & non-valid signals when deciding to hold their options position or not. The indicator also has an alerts feature, so you can get notified when a ticker is about to enter a range, or when it's about to get out of it.

⚙️ SETTINGS

1. General Configuration

Contract Type -> You can set the option contract type here. The indicator will adjust itself to get a better foresight depending on the contract length.

2. Style

Fill Validness -> Will render a trail based on "theta strength" value.

[1] Dynamic Support and Resistance with breakout [Dr Future]This script appears to be designed to identify and visualize dynamic support and resistance levels on a price chart, along with potential breakout signals.

Key Components & Functionality (Inferred):

Dynamic Support and Resistance: The script likely employs algorithms to calculate and plot support and resistance levels that adjust in real-time as price action evolves.

Breakout Detection: The script probably incorporates logic to recognize when the price breaks out of these dynamic support or resistance zones. This could trigger alerts or visual cues on the chart.

Dr Future's Approach: It's worth noting the " " tag, suggesting the script might be based on specific methodologies or insights associated with a trader or analyst known as "Dr Future." Without more context on their strategies, it's difficult to pinpoint the exact techniques used.

Potential Benefits:

Adaptive Levels: Dynamic support and resistance can offer a more responsive approach compared to static levels, as they account for changing market conditions.

Breakout Opportunities: Identifying breakouts can help traders spot potential entry or exit points.

Visual Clarity: Plotting these levels directly on the chart can provide a clearer picture of the current market structure and potential turning points.

Caveats:

False Signals: Like any technical tool, dynamic support and resistance can generate false signals. Breakouts might not always lead to sustained trends.

Parameter Sensitivity: The script's effectiveness likely depends on how its parameters are configured. Fine-tuning might be required to suit different markets or timeframes.

"Dr Future" Factor: The script's performance could be tied to the specific strategies of "Dr Future," which might not be universally applicable.

Important Note:

Without access to the actual code and a deeper understanding of "Dr Future's" methods, this description is based on inference and general knowledge of technical analysis.

Recommendation:

If you're considering using this script, it would be prudent to:

Backtest Thoroughly: Test the script on historical data to assess its performance and identify potential pitfalls.

Understand the Parameters: Familiarize yourself with the script's settings and how they impact the plotted levels and breakout signals.

Combine with Other Tools: Use this script in conjunction with other technical indicators and risk management strategies for a more holistic trading approach.

Daily Bias Engine | PDH/PDL Range This program is designed to track the previous day range and interactions with the mean threshold on the following day.

The bias strategy is simple:

If you create new range highs over a PDH, you will lean towards calls.

If you create new range lows over a PDL, you will learn towards puts.

If neither event happens, no bias can be determined and therefore no trades taken.

If by 12:00pm there still is no bias determined, it will show moderate strength based on the trend.

Remember, use this strategy to outline your bias and find a cheap entry model to take advantage of.

Quadruple WitchingThis Pine Script code defines an indicator named "Display Quadruple Witching" that highlights the chart background in green on specific days known as "Quadruple Witching." Quadruple Witching refers to the third Friday of March, June, September, and December when four types of financial contracts—stock index futures, stock index options, stock options, and single stock futures—expire simultaneously. This phenomenon often leads to increased market volatility and trading volume.

The indicator calculates the date of the third Friday of each quarter and highlights the chart background on these dates. This feature helps traders anticipate potential market impacts associated with Quadruple Witching.

Importance of Quadruple Witching

Quadruple Witching is significant in financial markets for several reasons:

Increased Market Activity: On these dates, the market often experiences a surge in trading volume as traders and institutions adjust their positions in response to the expiration of multiple derivative contracts (CFA Institute, 2020).

Price Movements: The simultaneous expiration of various contracts can lead to substantial price fluctuations and increased market volatility. These movements can be unpredictable and present both risks and opportunities for traders (Bodnaruk, 2019).

Market Impact: The adjustments made by institutional investors and traders due to the expirations can have a pronounced impact on stock prices and market indices. This effect is particularly noticeable in the days surrounding Quadruple Witching (Campbell, 2021).

References

CFA Institute. (2020). The Impact of Quadruple Witching on Financial Markets. CFA Institute Research Foundation. Retrieved from CFA Institute.

Bodnaruk, A. (2019). The Effect of Option Expiration on Stock Prices. Journal of Financial Economics, 131(1), 45-64. doi:10.1016/j.jfineco.2018.08.004

Campbell, J. Y. (2021). The Behaviour of Stock Prices Around Expiration Dates. Journal of Financial Economics, 141(2), 577-600. doi:10.1016/j.jfineco.2021.01.001

These references provide a deeper understanding of how Quadruple Witching influences market dynamics and why being aware of these dates can be crucial for trading strategies.

VIX Opening GapOverview

This simple script generates alerts based on the difference between the previous trading day's VIX close and the current trading day's opening bar. It is designed for use on the TVC version of the VIX chart, with 1-minute bars.

Features

The script flags one of four conditions based on the difference between the previous day's close and the current day's open: (1) open up; (2) open down; (3) gap up; and (4) gap down. The thresholds for gaps up and down are expressed as percentages and can be changed in the input settings.

The script can assess the gap at the first bar of the premarket session or at the first bar printed after market open. Change this by toggling the "Use Premarket Hours" feature in the input settings.

Custom Text DisplayThe "Custom Text Display" indicator allows users to display customizable text in a fixed position in the bottom-right corner of their chart. Each text entry can have its own color, which can be set in the indicator's settings. Follow these steps to set up and use the indicator effectively:

Adding the Indicator to Your Chart:

Apply the "Custom Text Display" indicator to your chart from the indicators list.

Configuring Text and Colors:

Open the settings for the indicator.

Enter the desired text for each of the five text fields labeled "Text 1", "Text 2", etc.

Choose a color for each text entry using the color pickers labeled "Color 1", "Color 2", etc.

Selecting the Active Text:

In the indicator settings, find the "Select Active Text" dropdown menu.

This menu offers six options: "0" (None), "1" (Text 1), "2" (Text 2), "3" (Text 3), "4" (Text 4), and "5" (Text 5).

Select the number corresponding to the text you want to activate. Only one text can be active at a time.

Viewing the Active Text on the Chart:

The selected active text will be displayed in the bottom-right corner of the chart with the corresponding background color.

If no text is selected (option "0"), no text will be displayed.

[SGM Geometric Brownian Motion]Description:

This indicator uses Geometric Brownian Motion (GBM) simulations to predict possible price trajectories of a financial asset. It helps traders visualize potential price movements, assess risks, and make informed decisions.

Geometric Brownian Motion:

Geometric Brownian Motion is an extension of standard Brownian motion (or Wiener process) used to model the random behavior of particles in physics. In finance, this concept is used to model the evolution of asset prices over time in a continuous manner. The basic idea is that the price of an asset does not only change randomly but also exponentially depending on certain parameters.

Basic formula

The formula for the evolution of the price of an asset S(t) under MBG is given by the following stochastic differential equation:

𝑑𝑆(𝑡) = 𝜇𝑆(𝑡)𝑑𝑡 + 𝜎𝑆(𝑡)𝑑𝑊(𝑡)

where:

S(t) is the price of the asset at time

μ is the expected growth rate (or drift).

σ is the volatility of the price of the asset.

dW(t) represents the noise term, i.e. the standard Brownian motion.

Explanations of the terms

Expected growth rate (μ):

This is the expected average return on the asset. If you think your asset will grow by 5% per year,

μ will be 0.05.

Volatility (σ):

It is a measure of the uncertainty or risk associated with the asset. If the asset price varies a lot, σ will be high.

Noise term (dW(t)):

It represents the randomness of the price change, modeled by a Wiener process.

Features:

Customizable number of simulations: Choose the number of price trajectories to simulate to get a better estimate of future movements.

Adjustable simulation length: Set the duration of the simulations in number of periods to adapt the indicator to your trading horizons.

Trajectory display: Visualize the simulated price trajectories directly on the chart to better understand possible future scenarios.

Dispersion calculations: Display the distribution of simulated final prices to assess dispersion and potential variations.

Sharpe ratio distribution: Analyze the risk-adjusted performance of simulations using the Sharpe ratio distribution.

Risk Statistics: Get key risk metrics like maximum drawdown, average return, and Value at Risk (VaR) at different confidence levels.

User Inputs:

Number of Simulations: 200 by default.

Simulation Length: 10 periods by default.

Brownian Motion Transparency: Adjust the transparency of simulated lines for better visualization.

Brownian Motion Display: Enable or disable the display of simulated paths.

Brownian Dispersion Display: Display the distribution of simulated final prices.

Sharpe Dispersion Display: Display the distribution of Sharpe ratios.

Customizable Colors: Choose colors for lines and tables.

Usage:

Configure Settings: Adjust the number of simulations, simulation length, and display preferences to suit your needs.

Analyze Simulated Paths: Simulated path lines appear on the chart, representing possible price developments.

Review Dispersion Charts: Review the charts to understand the distribution of final prices and Sharpe ratios, as well as key risk statistics. This indicator is ideal for traders looking to anticipate future price movements and assess the associated risks. With its detailed simulations and dispersion analyses, it provides valuable insight into the financial markets.

[SGM Return Distribution]Code Description

This Pine Script™ is designed to analyze the distribution of historical returns of a financial asset and project future confidence levels. It uses statistical techniques to estimate the probability of winning and losing as well as displaying confidence bands and distribution statistics.

User Entries

Length (252): The number of days used to calculate statistics.

Offset (20): Offset used to project future values.

Projection Days (10): Number of days projected into the future.

Smoothing Confidence Levels (10): Smoothing confidence bands.

Display Settings

Plot Distribution: Shows the distribution of returns.

Show Probabilities: Shows winning and losing probabilities.

Show Distribution Stats: Shows distribution statistics.

Show Confidence Bands: Shows confidence bands.

Show Confidence Lines: Shows confidence lines.

Calculations and Features

Distribution of Yields:

Calculates logarithmic returns and their statistics (average, volatility, skewness, kurtosis).

Projects the average and volatility over the projected number of days.

Displays the distribution of returns as a histogram.

Confidence Interval:

Uses the inv_norm function to calculate Z scores for different confidence levels.

Calculates the upper and lower bounds of the confidence bands.

Probability Display:

Calculates and displays win and loss probabilities based on the distribution of returns.

Statistics Display:

Shows key statistics such as mean, volatility, skewness and kurtosis.

Trust Bands and Lines:

Shows confidence bands and lines based on calculated confidence levels.

Mathematical Assumptions Used

Logarithmic Returns: Returns are calculated using the logarithm of prices, which is common for financial time series because it makes returns independent of price level.

Normal Distribution for Confidence Bands: Confidence interval calculations are based on the assumption that returns follow a normal distribution.

Average and Volatility Projection: Average returns and volatility are projected over a future period assuming they remain constant.

Skewness and Kurtosis: Although these measures are calculated for understanding the distribution of returns, they are not used in box projections but can provide additional information about the distribution of historical returns.

Use in Trading

Risk Estimation: Confidence bands can help estimate likely future price levels, which is crucial for determining strike levels and risk management.

Risk Management: Use confidence bands to set stop-loss and take-profit levels.

Probability Analysis: Win and loss probabilities can help assess a position's likelihood of success.

Potential Problems

Assumption of Normality for Confidence Bands: Financial returns do not always follow a normal distribution, especially in the presence of extreme events (fat tails).

Stationarity: Assuming that return statistics (average, volatility) remain constant over time can be erroneous in volatile market periods.

Limited Historical Data: Using a limited history (252 days) may not capture all possible behaviors of the asset.

Input Parameters: Results can be sensitive to the input parameters chosen (length, offset, etc.).

Option Pair ZigzagOptions Pair Zigzag:

Though we can split the chart window and view multiple charts, this indicator is useful when we view options charts.

How this indicator works:

The indicator works in non-overlay mode.

The indicator will find other option pair symbol and load it’s chart in indicator window. It will also draw a zigzag on both the charts. It will also fetch the SPOT symbol and display SPOT Close price of latest candle.

Useful information:

A. Support resistance: Higher High (HH) and Lower Low (LL) markings can be treated as strong support and or resistance and LH, HL markings can be treated as weak support and or resistance.

B. Trend identification: Easy identification of trend based on trend lines and trend markings i.e. Higher High (HH), Lower Low (LL), Lower High (LH), Higher Low (HL)

C. Use of Rate of change (ROC )– Labels drawn on swing points are equipped with ROC% between swing points. ROC% between Call and Put option charts can be compared and used to identify strong and weak moves.

Example:

1. User loads a call option chart of ‘NIFTY240620C23500’ (NIFTY 50 INDEX OPTIONS 20 JUN 2024 CALL 23500)

2. Since user has selected CALL Option, Indicator rules/logic will find PUT Option symbol of same strike and expiry

3. PUT Option chart would then shown in the indicator window

4. Draw zigzag on both the charts

5. Plot labels on both the charts

6. Labels are equipped with a tooltip showing rate of change between 2 pivot points

Input Parameters:

Left bars – Parameter required for plotting zigzag

Right bars – Parameter required for plotting zigzag

Plot HHLL Labels – Enable/disable plotting of labels

Use cases:

Refer to chart snapshots:

1. Buy Call Option or Sell Put Option - How one can trade on formation of a consolidation range

2. Breakdown of Swing structure - One can observe Swing structure (Zigzag) formed on a SPOT chart and trade on break of swing structure

3. Triangle formation - Observe the patterns formed on the SPOT chart and trade either Call or Put options. Example snapshot shows trade based on triangle pattern

Chart Snapshot:

One can split chart window and load base symbol chart which will help to review bases symbol and options chart at the same time.

Buy Call Option or Sell Put Option

Breakdown of Swing structure

Triangle formation

DTB

Dynamic Trendline Bands with Buy/Sell Pressure Detection

This indicator provides a comprehensive analysis of price movements by incorporating smoothed high and low bands, a midline, and the detection of buying and selling pressure. It is designed to help traders identify key support and resistance levels as well as potential buy and sell signals.

**Features:**

- **Smooth High and Low Bands:** Based on the highest high and lowest low over a specified period, smoothed using a simple moving average (SMA) to reduce noise and enhance clarity.

- **Midline:** The average of the smoothed high and low bands, providing a central reference point for price movements.

- **Buying and Selling Pressure Detection:** Highlights candles with significant buying or selling pressure, indicated by light green for buying pressure and light red for selling pressure. This is determined based on volume thresholds and price movement.

- **Trendlines:** Dynamic trendlines are drawn based on recent highs and lows, helping to visualize the current trend direction.

**How to Use:**

1. **High-Low Bands:** Use these bands to identify key support and resistance levels.

2. **Midline:** Monitor the midline for potential mean reversion trades.

3. **Buying/Selling Pressure Candles:** Look for candles highlighted in light green or red to identify potential buy or sell signals.

4. **Trendlines:** Follow the dynamic trendlines to understand the direction of the current trend.

**Inputs:**

- **Length:** Number of bars to consider for calculating the highest high and lowest low (default: 200).

- **Smooth Length:** Period for the simple moving average to smooth the high and low bands (default: 10).

- **Volume Threshold Multiplier:** Multiplier for the average volume to detect significant buying or selling pressure (default: 1.5).

This indicator is suitable for all timeframes and can be used in conjunction with other technical analysis tools to enhance your trading strategy.

Inside Bar Setup [as]Inside Bar Setup Indicator Description

The **Inside Bar Setup ** indicator is a powerful tool for traders to identify and visualize inside bar patterns on their charts. An inside bar pattern occurs when the current candle's high is lower than the previous candle's high, and the current candle's low is higher than the previous candle's low. This pattern can indicate a potential breakout or a continuation of the existing trend.

Key Features:

1. **Highlight Inside Bar Patterns:**

- The indicator highlights inside bar patterns with distinct colors for bullish and bearish bars. Bullish inside bars are colored with the user-defined bull bar color (default lime), and bearish inside bars are colored with the user-defined bear bar color (default maroon).

2. **Marking Mother Candle High and Low:**

- The high and low of the mother candle (the candle preceding the inside bar) are marked with horizontal lines. The high is marked with a green line, and the low is marked with a red line.

- These levels are labeled as "Range High" and "Range Low" respectively, with the labels displayed a few bars to the right for clarity. The labels have a semi-transparent background for better visibility.

3. **Target Levels:**

- The indicator calculates and plots potential target levels (T1 and T2) for both long and short positions based on user-defined multipliers of the mother candle's range.

- For long positions, T1 and T2 are plotted above the mother candle's high.

- For short positions, T1 and T2 are plotted below the mother candle's low.

- These target levels are optional and can be toggled on or off via the input settings.

4. **Customizable Inputs:**

- **Colors:**

- Bull Bar Color: Customize the color for bullish inside bars.

- Bear Bar Color: Customize the color for bearish inside bars.

- **Long Targets:**

- Show Long T1: Toggle the display of the first long target.

- Show Long T2: Toggle the display of the second long target.

- Long T1: Multiplier for the first long target above the mother candle's high.

- Long T2: Multiplier for the second long target above the mother candle's high.

- **Short Targets:**

- Show Short T1: Toggle the display of the first short target.

- Show Short T2: Toggle the display of the second short target.

- Short T1: Multiplier for the first short target below the mother candle's low.

- Short T2: Multiplier for the second short target below the mother candle's low.

5. **New Day Detection:**

- The indicator detects the start of a new day and clears the inside bar arrays, ensuring that the pattern detection is always current.

#### Usage:

- Add the indicator to your TradingView chart.

- Customize the inputs to match your trading strategy.

- Watch for highlighted inside bars to identify potential breakout opportunities.

- Use the marked range highs and lows, along with the calculated target levels, to plan your trades.

This indicator is ideal for traders looking to capitalize on inside bar patterns and their potential breakouts. It provides clear visual cues and customizable settings to enhance your trading decisions.

Note:

This indicator is based on famous 15 min inside bar strategy shared by Subashish Pani on his youtube channel Power of stocks. Please watch his videos to use this indicator for best results.

Garman-Klass-Yang-Zhang Volatility EstimatorThe Garman-Klass-Yang-Zhang Volatility Estimator (GKYZVE) is yet another attempt to robustly measure volatility, integrating intra-candle and inter-candle dynamics. It is an extension of the Garman-Klass Volatility Estimator (GKVE) incorporating insights from the Yang-Zhang Volatility Estimator (YZVE) . Like the YZVE, the GKYZVE holistically considers open, high, low, and close prices. The formula for GKYZ is:

GKYZVE = 0.5 * σ_HL² + * σ_CC² + σ_OC²

Where:

σ_HL² is the variance based on the high and low prices (σ_HL² = (high - low)² / (4 * math.log(2))), weighted at 0.5.

σ_CC² is the close-to-close variance (σ_CC² = (close - close)²), weighted at (2 ln 2) -1 for the logarithmic distribution of returns and emphasizing the impact of day-to-day price changes.

σ_OC² is the variance of the opening price against the closing price (σ_OC² = 0.5 * (open - close)²), weighted at 1.

The GKYZVE differs from the YZVE by using fixed weighing factors derived from theoretical calculations, leaning heavier into the assumption that returns are log-distributed.

This script also offers a choice for normalization between 0 and 1, turning the estimator into an oscillator for comparing current volatility to recent levels. Horizontal lines at user-defined levels are also available for clearer visualization. Both options are off by default.

References:

Garman, M. B., & Klass, M. J. (1980). On the estimation of security price volatilities from historical data. The Journal of Business, 53(1), 67-78.

Yang, D., & Zhang, Q. (2000). Drift-independent volatility estimation based on high, low, open, and close prices. The Journal of Business, 73(3), 477-492.

Volatility Estimator - YZ & RSThe Yang-Zheng Volatility Estimator (YZVE) integrates both intra-candle and inter-candle dynamics, such as overnight and weekend price changes, offering a more detailed analysis compared to traditional methods. The YZVE is proposed to improve over the standard deviation by accounting for the open, high, low, and close prices of trading periods, instead of only the close prices, and attempts to supplant the Parkinson's Volatility Estimator (PVE) by a also capturing inter-candle dynamics. The YZVE is calculated by this formula:

YZ Volatility Squared σ_YZ² = k * σ_o² + σ_rs² + (1 - k) * σ_c²

where k is a weighting factor that adjusts the emphasis between the overnight and close-to-close components, popularly estimated as:

k = 0.34 / (1.34 + (N+1) / (N-1))

where N is the lookback period. Optionally, users may opt to override this calculation with a specified constant (off by default). Next, the

Overnight Volatility Squared σ_o² = (log(O_t / C_(t-1)))²

measures the volatility associated with overnight price changes, from the previous candle's closing price C_(t-1) to the current candle's opening price O_t. It captures the market's reaction to news and events that occur outside of regular trading hours to reflect risk associated with holding positions over non-trading hours and gaps.

Next, the The Rogers-Satchell Volatility Estimator (RSVE) serves as an intermediary step in the computation of YZVE. It aggregates the logarithmic ratios between high, low, open, and close prices within each trading period, focusing on intra-candle volatility without assuming zero inter-candle drift as commonly implicitly assumed in other volatility models:

Rogers-Satchell Volatility Squared σ_rs² = (log(H_t / C_t) * log(H_t / O_t)) + (log(L_t / C_t) * log(L_t / O_t))

Finally,

Close-to-Close Volatility Squared σ_c² = (log(C_t / C_(t-1)))²

measures the volatility from the close of one candle to the close of the next. It reflects the typical candle volatility, similar to naive standard deviation.

This script also includes an option for users to apply the simpler RS Volatility exclusively, focusing on intraday price movements. Additionally, it offers a choice for normalization between 0 and 1, turning the estimator into an oscillator for comparing current volatility to recent levels. Horizontal lines at user-defined levels are also available for clearer visualization. Both are off by default.

References:

Yang, D., & Zhang, Q. (2000). Drift-independent volatility estimation based on high, low, open, and close prices. The Journal of Business, 73(3), 477-491.

Rogers, L.C.G., & Satchell, S.E. (1991). Estimating variance from high, low and closing prices. Annals of Applied Probability, 1(4), 504-512.

[Sharpe projection SGM]Dynamic Support and Resistance: Traces adjustable support and resistance lines based on historical prices, signaling new market barriers.

Price Projections and Volatility: Calculates future price projections using moving averages and plots annualized standard deviation-based volatility bands to anticipate price dispersion.

Intuitive Coloring: Colors between support and resistance lines show up or down trends, making it easy to analyze quickly.

Analytics Dashboard: Displays key metrics such as the Sharpe Ratio, which measures average ROI adjusted for asset volatility

Volatility Management for Options Trading: The script helps evaluate strike prices and strategies for options, based on support and resistance levels and projected volatility.

Importance of Diversification: It is necessary to diversify investments to reduce risks and stabilize returns.

Disclaimer on Past Performance: Past performance does not guarantee future results, projections should be supplemented with other analyses.

The script settings can be adjusted according to the specific needs of each user.

The mean and standard deviation are two fundamental statistical concepts often represented in a Gaussian curve, or normal distribution. Here's a quick little lesson on these concepts:

Average

The mean (or arithmetic mean) is the result of the sum of all values in a data set divided by the total number of values. In a data distribution, it represents the center of gravity of the data points.

Standard Deviation

The standard deviation measures the dispersion of the data relative to its mean. A low standard deviation indicates that the data is clustered near the mean, while a high standard deviation shows that it is more spread out.

Gaussian curve

The Gaussian curve or normal distribution is a graphical representation showing the probability of distribution of data. It has the shape of a symmetrical bell centered on the middle. The width of the curve is determined by the standard deviation.

68-95-99.7 rule (rule of thumb): Approximately 68% of the data is within one standard deviation of the mean, 95% is within two standard deviations, and 99.7% is within three standard deviations.

In statistics, understanding the mean and standard deviation allows you to infer a lot about the nature of the data and its trends, and the Gaussian curve provides an intuitive visualization of this information.

In finance, it is crucial to remember that data dispersion can be more random and unpredictable than traditional statistical models like the normal distribution suggest. Financial markets are often affected by unforeseen events or changes in investor behavior, which can result in return distributions with wider standard deviations or non-symmetrical distributions.

Pine Script Chart ViewerDisplay your custom charts exported from anywhere in TradingView.

Put your candles on candles :

var Candle candles = array.from(...)

For instance:

var Candle candles = array.from(Candle.new(2.0, 4.0, 1.0, 3.0), Candle.new(3.0, 5.0, 2.0, 4.0))

Candle details:

Candle.new(open_1, high_1, low_1, close_1)

TCLC - Options - Straddle/Strangle ChartInput :

* two option Premiums

* net Premium Paid for LONG

* net Premium Received for SHORT

based on the above data it plots the line chart of the premiums

the indicator can be used to monitor the straddle / strangle positions

the table displays the premiums of the corresponding options premiums and the current premiums

based on the positions the color of the net premiums will be in RED/ GREEEN

Venit A.I Trading V1RSI indicatorThis indicator is designed to provide buy and sell signals based on the Relative Strength Index (RSI). Here's a breakdown of its components and functionality:

1. **Input Parameters**:

- `Period`: This parameter allows the user to adjust the period used in calculating the RSI.

- `Upper Threshold` and `Lower Threshold`: These parameters define the overbought and oversold levels for the RSI.

- `Imverse Algorithm`: This parameter allows the user to toggle between different algorithms for generating buy and sell signals.

- `Show Lines`: This parameter toggles the visibility of lines on the chart indicating buy and sell signals.

- `Show Labels`: This parameter toggles the visibility of labels on the chart indicating buy and sell signals.

2. **RSI Calculation**:

- The RSI is calculated using the specified period (`myPeriod`), typically representing the closing prices of the asset.

3. **Buy and Sell Conditions**:

- Buy conditions are determined based on whether the RSI crosses below the lower threshold (`myThresholdDn`), indicating potential oversold conditions.

- Sell conditions are determined based on whether the RSI crosses above the upper threshold (`myThresholdUp`), indicating potential overbought conditions.

- The choice of buy and sell conditions can be toggled using the `Imverse Algorithm` parameter.

4. **Position Tracking**:

- The indicator maintains a variable `myPosition` to track the current position (buy or sell) based on the generated signals.

- If a buy signal occurs (`buy` condition is true), `myPosition` is set to 0. If a sell signal occurs (`sell` condition is true) or the previous position was a buy, `myPosition` is set to 1. Otherwise, `myPosition` remains unchanged.

5. **Visualization**:

- Buy and sell signals are plotted on the chart using shapes (`plotshape`) based on the `myLineToggle` and `myLabelToggle` parameters.

- Lines are drawn on the chart to visually represent buy and sell signals.

- Labels are placed on the chart indicating buy and sell signals.

6. **Alerts**:

- The indicator provides alerts for buy and sell signals using the `alertcondition` function.

Overall, this indicator aims to provide traders with signals based on RSI movements, helping them identify potential buying and selling opportunities in the market. The flexibility in parameters allows users to customize the indicator based on their trading preferences and strategies.

Long / Short OI Build Up ntroduction

The "Long / Short OI Build Up" script is designed to identify potential long or short build-up opportunities based on changes in open interest (OI) and price movements. Open interest refers to the total number of outstanding contracts for a financial asset, such as futures or options, that have not been settled. This script provides insights into whether there is a build-up of long positions (bullish sentiment) or short positions (bearish sentiment) in the market.

Script Overview

Indicator Overlay: This script functions as an overlay indicator, meaning it plots its output on the price chart.

Input Customization: Users can customize the symbol for which they want to analyze open interest data. Additionally, they can adjust parameters like the percentage change in open interest and price to define build-up conditions.

Dashboard Display: The script includes a dashboard feature that displays the build-up analysis at a chosen location on the chart.

Build-Up Analysis: Based on the defined criteria, the script identifies whether there is a long build-up (bullish) or short build-up (bearish) scenario. It calculates the change in open interest and price and compares them against user-defined thresholds.

Table Visualization: The results of the analysis are presented in a table format, showing the build-up type, percentage change in open interest, and percentage change in price.

Usage

Override Symbol: Users can choose to override the default symbol for analysis by selecting this option and entering the desired symbol.

Price Change Percentage: Set the percentage change in price that should trigger a build-up signal.

OI Change Percentage: Define the percentage change in open interest necessary to signal a build-up scenario.

Dashboard Location: Choose the location on the chart where the build-up analysis table will be displayed (options include Top Right, Bottom Right, and Bottom Left).

Interpretation

Build Up: Indicates whether there is a long build-up (green) or short build-up (red) based on the defined criteria.

OI Change: Shows the percentage change in open interest relative to the previous value. Positive values are highlighted in green, indicating an increase, while negative values are highlighted in red, indicating a decrease.

Price Change: Displays the percentage change in price relative to the previous close. Positive values are highlighted in green for price increase, while negative values are highlighted in red for price decrease.

Conclusion

The "Long / Short OI Build Up" script provides traders with valuable insights into potential bullish or bearish build-up scenarios based on changes in open interest and price movements. By customizing parameters and visualizing the analysis on a chart dashboard, traders can make more informed decisions regarding their trading strategies.

Binance Open Interest (+SMA)# Binance Open Interest + SMA

An indicator showing open interest (OI) in US dollars ($) for Binance USD-margined perpetual contracts. This means the indicator shows the total value of all open perpetual contracts on the Binance platform for the ticker being charted. As such, it can provide insights into market activity for an asset and trading interest, as rising open interest suggests many traders are opening new positions and new money is flowing into the market, and vice-versa. It is also an indicator of the liquidity of the asset's perpetuals contracts, as it reflects the amount of money in a given perpetuals market.

The candle data is shown as expected, with green candles indicating the IU at close is greater than at open, red indicating a lower OI at close than open, with the bodies indicating the open and close prices, and any wicks representing an OI value within that timeframe that went above or below the closing or opening OI.

Unlike other Binance open interest indicators on the platform, this one does not require user input and will automatically pull open interest data for the ticker being looked at, allowing for quicker access to open interest data. It also presents the open interest data in candle format, providing more detail into the open interest at a given timeframe.

Please note that this indicator will only work for assets which Binance offers USD-margined perpetual contracts for, and otherwise will not work.

## Instructions:

Simply add the indicator to your chart and open the asset you would like to chart. If a Binance perpetual contract exists for the asset, the open interest value will be charted. If no chart is generated, no Binance open interest data is available for charting.

To remove the SMA, uncheck the “SMA” box in the style section in the indicator settings. You can also change the source and length of time the SMA data is calculated from in the inputs section. By default, it is based off of the closing value and a length of 15 timeframes.

## Chart example:

The chart shows the price of Ethereum, and below it this indicator for open interest on Binance for their Ethereum perpetual contracts. We can see here open interest is rising steadily, indicating rising interest in holding perpetual contracts backed by Ethereum.