MTF Squeeze Analyzer - [tradeviZion]MTF Squeeze Analyzer

Multi-Timeframe Squeeze Pro Analyzer Tool

Overview:

The MTF Squeeze Analyzer is a comprehensive tool designed to help traders monitor the TTM Squeeze indicator across multiple timeframes in a streamlined and efficient manner. Built with Pine Script™ version 5, this indicator enhances your market analysis by providing detailed insights into squeeze conditions and momentum shifts, enabling you to make more informed trading decisions.

Key Features:

1. Multi-Timeframe Monitoring:

Comprehensive Coverage: Track squeeze conditions across multiple timeframes, including 1-minute, 5-minute, 15-minute, 30-minute, 1-hour, 2-hour, 4-hour, and daily charts.

Squeeze Counts: Keep count of the number of consecutive bars the price has been within each squeeze level (low, mid, high), helping you assess the strength and duration of consolidation periods.

2. Dynamic Table Display:

Customizable Appearance: Adjust table position, text size, and colors to suit your preferences.

Color-Coded Indicators: Easily identify squeeze levels and momentum shifts with intuitive color schemes.

Message Integration: Features rotating messages to keep you engaged and informed.

3. Alerts for Key Market Events:

Squeeze Start and Fire Alerts: Receive notifications when a squeeze starts or fires on your selected timeframes.

Custom Squeeze Count Alerts: Set thresholds for squeeze counts and get alerted when these levels are reached, allowing you to anticipate potential breakouts.

Fully Customizable: Choose which alerts you want to receive and tailor them to your trading strategy.

4. Momentum Analysis:

Momentum Oscillator: Visualize momentum using a histogram that changes color based on momentum shifts.

Detailed Insights: Determine whether momentum is increasing or decreasing to make more strategic trading decisions.

How It Works:

The indicator is based on the TTM Squeeze concept, which identifies periods of low volatility where the market is "squeezing" before a potential breakout. It analyzes the relationship between Bollinger Bands and Keltner Channels to determine squeeze conditions and uses linear regression to calculate momentum.

1. Squeeze Levels:

No Squeeze (Green): Market is not in a squeeze.

Low Compression Squeeze (Gray): Mild consolidation, potential for a breakout.

Mid Compression Squeeze (Red): Moderate consolidation, higher breakout potential.

High Compression Squeeze (Orange): Strong consolidation, significant breakout potential.

2. Squeeze Counts:

Tracks the number of consecutive bars in each squeeze condition.

Helps identify how long the market has been consolidating, providing clues about potential breakout timing.

3. Momentum Histogram:

Upward Momentum: Shown in aqua or blue, indicating increasing or decreasing upward momentum.

Downward Momentum: Displayed in red or yellow, representing increasing or decreasing downward momentum.

Using Alerts:

Stay ahead of market movements with customizable alerts:

1. Enable Alerts in Settings:

Squeeze Start Alert: Get notified when a new squeeze begins.

Squeeze Fire Alert: Be alerted when a squeeze ends, signaling a potential breakout.

Squeeze Count Alert: Set a specific number of bars for a squeeze condition, and receive an alert when this count is reached.

2. Set Up Alerts on Your Chart:

Click on the indicator name and select " Add Alert on MTF Squeeze Analyzer ".

Choose your desired alert conditions and customize the notification settings.

Click " Create " to activate the alerts.

How to Set It Up:

1. Add the Indicator to Your Chart:

Search for " MTF Squeeze Analyzer " in the TradingView Indicators library.

Add it to your chart.

2. Customize Your Settings:

Table Display:

Choose whether to show the table and select its position on the chart.

Adjust text size and colors to enhance readability.

Timeframe Selection:

Select the timeframes you want to monitor.

Enable or disable specific timeframes based on your trading strategy.

Colors & Styles:

Customize colors for different squeeze levels and momentum shifts.

Adjust header and text colors to match your chart theme.

Alert Settings:

Enable alerts for squeeze start, squeeze fire, and squeeze counts.

Set your preferred squeeze type and count threshold for alerts.

3. Interpret the Data:

Table Information:

The table displays the squeeze status and counts for each selected timeframe.

Colors indicate the type of squeeze, making it easy to assess market conditions at a glance.

Momentum Histogram:

Use the histogram to gauge the strength and direction of market momentum.

Observe color changes to identify shifts in momentum.

Why Use MTF Squeeze Analyzer ?

Enhanced Market Insight:

Gain a deeper understanding of market dynamics by monitoring multiple timeframes simultaneously.

Identify potential breakout opportunities by analyzing squeeze durations and momentum shifts.

Customizable and User-Friendly:

Tailor the indicator to fit your trading style and preferences.

Easily adjust settings without needing to delve into the code.

Time-Efficient:

Save time by viewing all relevant squeeze information in one place.

Reduce the need to switch between different charts and timeframes.

Stay Informed with Alerts:

Never miss a critical market movement with fully customizable alerts.

Focus on other tasks while the indicator monitors the market for you.

Acknowledgment:

This tool builds upon the foundational work of John Carter , who developed the TTM Squeeze concept. It also incorporates enhancements from LazyBear and Makit0 , providing a more versatile and powerful indicator. MTF Squeeze Analyzer extends these concepts by adding multi-timeframe analysis, squeeze counting, and advanced alerting features, offering traders a comprehensive solution for market analysis.

Note: Always practice proper risk management and test the indicator thoroughly to ensure it aligns with your trading strategy. Past performance is not indicative of future results.

Trade smarter with TradeVizion—unlock your trading potential today!

Oscillators

CANSLIM IBD Relative Strength NIFTYSMLCAP250 (Daily & Weekly)This Pine Script (written in version 5) is designed to calculate the IBD Relative Strength for both daily and weekly timeframes, comparing the current chart's security to the NIFTY SMLCAP 250 index. Here's a breakdown of the code:

1. Indicator Initialization: This line sets up the indicator with both a short and full title. The overlay=true means the plot will be drawn on top of the price chart.

2. Fetching Data: This fetches the daily ("D") and weekly ("W") close prices for the NIFTY SMLCAP 250 index.

3. Relative Strength Calculation: Relative strength is calculated as the ratio of the security's current close price to the close price of the NIFTY SMLCAP 250, multiplied by 100 for both daily and weekly timeframes.

4. Timeframe-Based Selection: Here, the script checks whether the chart is in daily or weekly mode and selects the corresponding relative strength value.

5. Scaling with Multiplier: This section ensures there are at least 60 bars of data and scales the relative strength by using a multiplier derived from the 60th previous bar's close price.

6. Plotting: Finally, the scaled relative strength is plotted on the chart in black.

Improvements :

Dynamic Timeframe Handling: You might want to extend this for other timeframes, e.g., monthly.

Customization: You can add user input parameters to adjust the timeframe, scale factor, or period dynamically.

Color Enhancements: You can add color variation to indicate strength/weakness more clearly.

Trend CCITrend CCI (TCCI) Indicator

Description:

The Trend CCI (TCCI) indicator is a unique combination of the Commodity Channel Index (CCI) and the Average True Range (ATR), designed to identify trends and market reversals with a refined sensitivity to price volatility. The indicator plots the CCI, adjusted by an ATR filter, and color-codes the trendline to signal uptrends and downtrends.

How It Works:

This indicator uses the CCI to measure price momentum and an ATR-based filter to smooth out market noise, making it easier to detect significant shifts in the market trend. Key parameters such as the ATR Period, ATR Multiplier, and CCI Period have been carefully chosen to optimize the indicator's performance:

1. ATR Period (default: 18)

The ATR Period determines the number of periods used to calculate the **Average True Range**, which reflects market volatility. In this case, an **ATR Period of 18** has been selected for several reasons:

Balance between responsiveness and noise reduction : A period of 18 strikes a balance between being responsive to recent price movements and filtering out minor fluctuations. Shorter ATR periods might be too reactive, creating false signals, while longer periods might miss shorter-term trends.

Adaptable to various market conditions : An 18-period ATR is suitable for both intraday and swing trading strategies, making it versatile across different time frames.

Standard industry practice : Many traders use ATR settings between 14 and 20 periods as a convention for detecting reliable volatility levels.

2. ATR Multiplier (default: 1.5)

The ATR Multiplier is applied to the ATR value to define how sensitive the indicator is to volatility. In this case, a multiplier of 1.5 has been chosen:

Avoiding whipsaws in low volatility markets: By setting the multiplier to 1.5, the indicator filters out smaller, less significant price movements, reducing the likelihood of whipsaw signals (i.e., false trend reversals during periods of low volatility).

Optimizing signal accuracy: A moderate multiplier like 1.5 ensures that the indicator only generates signals when the price moves a significant distance from the average range. Higher multipliers (e.g., 2.0) may ignore valid opportunities, while lower multipliers (e.g., 1.0) might create too many signals.

Enhancing trend clarity : The multiplier’s role in widening the range allows the indicator to respond more clearly during periods of strong trends, reducing signal noise and false positives.

3. CCI Period (default: 63)

The CCI Period defines the number of periods used to calculate the Commodity Channel Index. A 63-period CCI is selected based on the following considerations:

Smoothing the momentum calculation: A longer period, such as 63, is used to smooth out the CCI and reduce the effects of short-term price fluctuations. This period captures longer-term momentum, making it ideal for identifying more significant market trends.

-Filtering out short-term noise: While shorter CCI periods (e.g., 14 or 20) may be more reactive, they tend to produce more signals, some of which may be false. A 63-period CCI focuses on stronger and more sustained price movements, providing fewer but higher-quality signals.

Adapted to intermediate trading: A 63-period CCI aligns well with traders looking for medium-term trend-following strategies, striking a balance between long-term trend identification and responsiveness to significant price shifts.

How to Use:

Green Area: When the trendline turns green, it signals that the CCI is positive, reflecting upward momentum. This can be interpreted as a buy signal, indicating the potential for long positions or continuing bullish trades.

Red Area: When the trendline turns red, it signals that the CCI is negative, reflecting downward momentum. This can be interpreted as a sell signal, indicating potential short positions or bearish trades.

ATR Filter: The ATR helps reduce false signals by ignoring minor price movements. Traders can adjust the ATR Multiplier to make the indicator more or less sensitive based on market conditions. A lower multiplier (e.g., 1.2) may increase signal frequency, while a higher multiplier (e.g., 2.0) reduces it.

Originality:

The Trend CCI (TCCI) stands out due to its combination of the CCI and ATR. While many indicators simply plot raw CCI values, this script enhances the CCI’s effectiveness by incorporating an ATR-based volatility filter. This ensures that only significant trends trigger signals, making it a more reliable tool in volatile markets. The choice of the ATR period, multiplier, and CCI period ensures a refined balance between trend detection and noise reduction, distinguishing it as a powerful trend-following indicator.

Additionally, the visual aspect—using color-coded trendlines that dynamically shift between green and red—simplifies the interpretation of market trends, offering traders a clear and immediate understanding of trend direction and momentum strength.

Final Recommendations:

Use in Trending Markets The TCCI is most effective in trending markets, where its signals align with broader market momentum. In sideways or low-volatility markets, consider adjusting the ATR multiplier or using other complementary indicators to confirm the signals.

Risk Management: Always integrate robust risk management practices, such as using stop-loss orders and position sizing, to protect against sudden market reversals or periods of heightened volatility.

Adjust for Volatility: Consider the volatility of the asset being traded. In highly volatile assets, a higher ATR multiplier (e.g., 2.0) may be necessary to filter out noise, while in more stable assets, a lower multiplier (e.g., 1.2) might generate earlier signals.

By using the Trend CCI (TCCI) indicator with a deeper understanding of its key parameters, traders can better identify trends, reduce noise, and improve their overall decision-making in the markets.

Good Profits!

Uptrick: Market MoodsThe "Uptrick: Market Moods" indicator is an advanced technical analysis tool designed for the TradingView platform. It combines three powerful indicators—Relative Strength Index (RSI), Average True Range (ATR), and Bollinger Bands—into one cohesive framework, aimed at helping traders better understand and interpret market sentiment. By capturing shifts in the emotional climate of the market, it provides a holistic view of market conditions, which can range from calm to stressed or even highly excited. This multi-dimensional analysis tool stands apart from traditional single-indicator approaches by offering a more complete picture of market dynamics, making it a valuable resource for traders looking to anticipate and react to changes in market behavior.

The RSI in the "Uptrick: Market Moods" indicator is used to measure momentum. RSI is an essential component of many technical analysis strategies, and in this tool, it is used to identify potential market extremes. When RSI values are high, they indicate an overbought condition, meaning the market may be approaching a peak. Conversely, low RSI values suggest an oversold condition, signaling that the market could be nearing a bottom. These extremes provide crucial clues about shifts in market sentiment, helping traders gauge whether the current emotional state of the market is likely to result in a reversal. This understanding is pivotal in predicting whether the market is transitioning from calm to stressed or from excited to overbought.

The Average True Range adds another layer to this analysis by offering insights into market volatility. Volatility is a key factor in understanding the mood of the market, as periods of high volatility often reflect high levels of excitement or stress, while low volatility typically indicates a calm, steady market. ATR is calculated based on the range of price movements over a given period, and the higher the value, the more volatile the market is. The "Uptrick: Market Moods" indicator uses ATR to dynamically gauge volatility levels, helping traders understand whether the market is currently moving in a way that aligns with its emotional mood. For example, an increase in ATR accompanied by an RSI value that indicates overbought conditions could suggest that the market is in a highly excited state, with the potential for either strong momentum continuation or a sharp reversal.

Bollinger Bands complement these tools by providing visual cues about price volatility and the range within which the market is likely to move. Bollinger Bands plot two standard deviations away from a simple moving average of the price. This banding technique helps traders visualize how far the price is likely to deviate from its average over a certain period. The "Uptrick: Market Moods" indicator uses Bollinger Bands to establish price boundaries and identify breakout conditions. When prices break above the upper band or below the lower band, it often signals that the market is either highly stressed or excited. This breakout condition serves as a visual representation of the market mood, alerting traders to moments when prices are moving beyond typical ranges and when significant emotional shifts are occurring in the market.

Technically, the "Uptrick: Market Moods" indicator has been developed using TradingView’s Pine Script language, a highly efficient language for building custom indicators. It employs functions like ta.rsi, ta.atr, and ta.sma to perform the necessary calculations. The use of these built-in functions ensures that the calculations are both accurate and efficient, allowing the indicator to operate in real-time without lagging, even in volatile market conditions. The ta.rsi function is used to compute the Relative Strength Index, while ta.atr calculates the Average True Range, and ta.sma is used to smooth out price data for the Bollinger Bands. These functions are applied dynamically within the script, allowing the "Uptrick: Market Moods" indicator to respond to changes in market conditions in real time.

The user interface of the "Uptrick: Market Moods" indicator is designed to provide a visually intuitive experience. The market mood is color-coded on the chart, making it easy for traders to identify whether the market is calm, stressed, or excited at a glance. This feature is especially useful for traders who need to make quick decisions in fast-moving markets. Additionally, the indicator includes an interactive table that updates in real-time, showing the most recent mood state and its frequency. This provides valuable statistical insights into market behavior over specific time frames, helping traders track the dominant emotional state of the market. Whether the market is in a prolonged calm state or rapidly transitioning through moods, this real-time feedback offers actionable data that can help traders adjust their strategies accordingly.

The RSI component of the "Uptrick: Market Moods" indicator helps detect the speed and direction of price movements, offering insight into whether the market is approaching extreme conditions. By providing signals based on overbought and oversold levels, the RSI helps traders decide whether to enter or exit positions. The ATR element acts as a volatility gauge, dynamically adjusting traders’ expectations in response to changes in market volatility. Meanwhile, the Bollinger Bands help identify trends and potential breakout conditions, serving as an additional confirmation tool that highlights when the price has moved beyond normal boundaries, indicating heightened market excitement or stress.

Despite the robust capabilities of the "Uptrick: Market Moods" indicator, it does have limitations. In markets affected by sudden shifts, such as those driven by major news events or external economic factors, the indicator’s performance may not always be reliable. These external factors can cause rapid mood swings that are difficult for any technical analysis tool to fully anticipate. Additionally, the indicator’s complexity may pose a learning curve for novice traders, particularly those who are unfamiliar with the concepts of RSI, ATR, and Bollinger Bands. However, with practice, traders can become proficient in using the tool to its full potential, leveraging the insights it provides to better navigate market shifts.

For traders seeking a deeper understanding of market sentiment, the "Uptrick: Market Moods" indicator is an invaluable resource. It is recommended for those dealing with medium to high volatility instruments, where understanding emotional shifts can offer a strategic advantage. While it can be used on its own, integrating it with other forms of analysis, such as fundamental analysis and additional technical indicators, can enhance its effectiveness. By confirming signals with other tools, traders can reduce the likelihood of false signals and improve their overall trading strategy.

To further enhance the accuracy of the "Uptrick: Market Moods" indicator, it can be integrated with volume-based tools like Volume Profile or On-Balance Volume (OBV). This combination allows traders to confirm the moods identified by the indicator with volume data, providing additional confirmation of market sentiment. For example, when the market is in an excited mood, an increase in trading volume could reinforce the reliability of that signal. Conversely, if the market is stressed but volume remains low, traders may want to proceed with caution. Using multiple indicators together creates a more comprehensive trading approach, helping traders better manage risk and make informed decisions based on multiple data points.

In conclusion, the "Uptrick: Market Moods" indicator is a powerful and unique addition to the suite of technical analysis tools available on TradingView. It provides traders with a multi-dimensional view of market sentiment by combining the analytical strengths of RSI, ATR, and Bollinger Bands into a single tool. Its ability to capture and interpret the emotional mood of the market makes it an essential tool for traders seeking to gain an edge in understanding market behavior. While the indicator has certain limitations, particularly in rapidly shifting markets, its ability to provide real-time insights into market sentiment is a valuable asset for traders of all experience levels. Used in conjunction with other tools and sound trading practices, the "Uptrick: Market Moods" indicator offers a comprehensive solution for navigating the complexities of financial markets.

RSI (Kernel Optimized) | Flux Charts💎 GENERAL OVERVIEW

Introducing our new KDE Optimized RSI Indicator! This indicator adds a new aspect to the well-known RSI indicator, with the help of the KDE (Kernel Density Estimation) algorithm, estimates the probability of a candlestick will be a pivot or not. For more information about the process, please check the "HOW DOES IT WORK ?" section.

Features of the new KDE Optimized RSI Indicator :

A New Approach To Pivot Detection

Customizable KDE Algorithm

Realtime RSI & KDE Dashboard

Alerts For Possible Pivots

Customizable Visuals

❓ HOW TO INTERPRET THE KDE %

The KDE % is a critical metric that reflects how closely the current RSI aligns with the KDE (Kernel Density Estimation) array. In simple terms, it represents the likelihood that the current candlestick is forming a pivot point based on historical data patterns. a low percentage suggests a lower probability of the current candlestick being a pivot point. In these cases, price action is less likely to reverse, and existing trends may continue. At moderate levels, the possibility of a pivot increases, indicating potential trend shifts or consolidations.Traders should start monitoring closely for confirmation signals. An even higher KDE % suggests a strong likelihood that the current candlestick could form a pivot point, which could lead to a reversal or significant price movement. These points often align with overbought or oversold conditions in traditional RSI analysis, making them key moments for potential trade entry or exit.

📌 HOW DOES IT WORK ?

The RSI (Relative Strength Index) is a widely used oscillator among traders. It outputs a value between 0 - 100 and gives a glimpse about the current momentum of the price action. This indicator then calculates the RSI for each candlesticks, and saves them into an array if the candlestick is a pivot. The low & high pivot RSIs' are inserted into two different arrays. Then the a KDE array is calculated for both of the low & high pivot RSI arrays. Explaining the KDE might be too much for this write-up, but for a brief explanation, here are the steps :

1. Define the necessary options for the KDE function. These are : Bandwidth & Nº Steps, Array Range (Array Max - Array Min)

2. After that, create a density range array. The array has (steps * 2 - 1) elements and they are calculated by (arrMin + i * stepCount), i being the index.

3. Then, define a kernel function. This indicator has 3 different kernel distribution modes : Uniform, Gaussian and Sigmoid

4. Then, define a temporary value for the current element of KDE array.

5. For each element E in the pivot RSI array, add "kernel(densityRange.get(i) - E, 1.0 / bandwidth)" to the temporary value.

6. Add 1.0 / arrSize * to the KDE array.

Then the prefix sum array of the KDE array is calculated. For each candlestick, the index closest to it's RSI value in the KDE array is found using binary search. Then for the low pivot KDE calculation, the sum of KDE values from found index to max index is calculated. For the high pivot KDE, the sum of 0 to found index is used. Then if high or low KDE value is greater than the activation threshold determined in the settings, a bearish or bullish arrow is plotted after bar confirmation respectively. The arrows are drawn as long as the KDE value of current candlestick is greater than the threshold. When the KDE value is out of the threshold, a less transparent arrow is drawn, indicating a possible pivot point.

🚩 UNIQUENESS

This indicator combines RSI & KDE Algorithm to get a foresight of possible pivot points. Pivot points are important entry, confirmation and exit points for traders. But to their nature, they can be only detected after more candlesticks are rendered after them. The purpose of this indicator is to alert the traders of possible pivot points using KDE algorithm right away when they are confirmed. The indicator also has a dashboard for realtime view of the current RSI & Bullish or Bearish KDE value. You can fully customize the KDE algorithm and set up alerts for pivot detection.

⚙️ SETTINGS

1. RSI Settings

RSI Length -> The amount of bars taken into account for RSI calculation.

Source -> The source value for RSI calculation.

2. Pivots

Pivot Lengths -> Pivot lengths for both high & low pivots. For example, if this value is set to 21; 21 bars before AND 21 bars after a candlestick must be higher for a candlestick to be a low pivot.

3. KDE

Activation Threshold -> This setting determines the amount of arrows shown. Higher options will result in more arrows being rendered.

Kernel -> The kernel function as explained in the upper section.

Bandwidth -> The bandwidth variable as explained in the upper section. The smoothness of the KDE function is tied to this setting.

Nº Bins -> The Nº Steps variable as explained in the upper section. It determines the precision of the KDE algorithm.

Optimized Comprehensive Analysis Table# Enhanced Comprehensive Analysis Table

This advanced indicator provides a holistic view of market sentiment by analyzing multiple technical indicators simultaneously. It's designed to give traders a quick, at-a-glance summary of market conditions across various timeframes and analysis methods.

## Key Features:

- Analyzes 9 popular technical indicators

- Weighted voting system for overall market sentiment

- Customizable indicator weights

- Clear, color-coded table display

## Indicators Analyzed:

1. MACD (Moving Average Convergence Divergence)

2. RSI (Relative Strength Index)

3. Moving Averages (50, 100, 200-period)

4. Stochastic Oscillator

5. Parabolic SAR

6. MFI (Money Flow Index)

7. CCI (Commodity Channel Index)

8. OBV (On Balance Volume)

9. ADX (Average Directional Index)

## How It Works:

Each indicator's signal is calculated and classified as bullish, bearish, or neutral. These signals are then weighted according to user-defined inputs. The weighted votes are summed to determine an overall market sentiment.

## Interpretation:

- The table displays the state of each indicator and the overall market sentiment.

- Green indicates bullish conditions, red bearish, and yellow neutral.

- The "Overall State" row at the bottom provides a quick summary of the combined analysis.

## Customization:

Users can adjust the weight of each indicator to fine-tune the analysis according to their trading strategy or market conditions.

This indicator is ideal for traders who want a comprehensive overview of market conditions without having to monitor multiple indicators separately. It's particularly useful for confirming trade setups, identifying potential trend reversals, and managing risk.

Note: This indicator is meant to be used as part of a broader trading strategy. Always combine with other forms of analysis and proper risk management.

E9 MACD

The E9 MACD (Moving Average Convergence Divergence) indicator is a powerful tool used in technical analysis to help traders identify potential buy and sell signals based on price action. It is designed to provide clear visual cues and alerts for trading decisions. Here’s how it applies to price action and its key functionalities:

Key Features and Functionality

MACD Line and Signal Line:

MACD Line: Represents the difference between a fast and a slow moving average of the price. It helps in identifying the momentum of the price movement.

Signal Line: A smoothed average of the MACD Line, used to generate trading signals when the MACD Line crosses above or below it.

Histogram: The histogram shows the difference between the MACD Line and the Signal Line. It visually represents the strength of the trend, with positive values indicating bullish momentum and negative values indicating bearish momentum.

Trend Coloring:

Uptrend: When the MACD Line is above the Signal Line, the bars can be colored green to indicate a potential buying opportunity.

Downtrend: When the MACD Line is below the Signal Line, the bars can be colored red to signal a potential selling opportunity.

Timeframe Flexibility:

The E9 MACD can be adjusted to different timeframes, allowing traders to analyze short-term or long-term trends based on their trading strategy. This flexibility helps in tailoring the indicator’s analysis to different market conditions.

Visual Alerts and Highlights:

The indicator includes options to highlight price bars and background colors when significant crossovers occur, making it easier to spot key trading signals.

Circles can be plotted on the MACD Line to indicate cross events, enhancing visual clarity.

Customizable Appearance:

Traders can customize the appearance of the MACD Line, Signal Line, and Histogram, including color and line width, to suit their personal preferences and improve readability.

Alerts for Trading Signals:

The E9 MACD can generate alerts for crossovers of the MACD Line and Signal Line, helping traders stay informed of potential trading opportunities even when they are not actively monitoring the charts.

Application in Trading

The E9 MACD is particularly useful for:

Identifying potential entry and exit points based on the crossing of the MACD Line and Signal Line.

Gauging the strength of the current trend through the histogram.

Adjusting to different timeframes to align the indicator with various trading strategies, from day trading to long-term investing.

By providing clear visual indicators and alerts, the E9 MACD helps traders make more informed decisions and better understand the momentum and direction of price movements.

RSI Multi-Timeframe PINESCRIPTLABS📈 Use the Relative Strength Index (RSI) calculated across multiple time frames to generate signals

🔹 Intraday: Displays a table with real-time RSI values for the time frames of 5 minutes, 15 minutes, 30 minutes, 1 hour, 4 hours, and 1 day.

🔹 Standard: Displays a table with real-time RSI values for the time frames of 30 minutes, 1 hour, 4 hours, 1 day, 1 week, and 1 month.

The indicator allows you to customize overbought and oversold thresholds, as well as choose between viewing RSI values for intraday or standard time frames, tailoring the analysis to your specific needs. 🔧📊

🔔 Signals are generated when in 4 of the 6 time frames we define below:

Overbought Signal (When RSI indicates overbought conditions):

• Intraday: Activated when the RSI in the time frames of 5 minutes, 15 minutes, 30 minutes, and 1 hour is above the 70 threshold. 📈

• Standard: Activated when the RSI in the time frames of 30 minutes, 1 hour, 4 hours, and 1 day is above the 70 threshold. 📈

Oversold Signal (When RSI indicates oversold conditions):

• Intraday: Activated when the RSI in the time frames of 5 minutes, 15 minutes, 30 minutes, and 1 hour is below the 30 threshold. 📉

• Standard: Activated when the RSI in the time frames of 30 minutes, 1 hour, 4 hours, and 1 day is below the 30 threshold. 📉

Español:

📈 Utiliza el Índice de Fuerza Relativa (RSI) calculado en varios marcos de tiempo para generar señales

🔹 Intraday: Muestra una tabla con los valores del RSI en tiempo real para los marcos de tiempo de 5 minutos, 15 minutos, 30 minutos, 1 hora, 4 horas y 1 día.

🔹 Standard: Muestra una tabla con los valores del RSI en tiempo real para los marcos de tiempo de 30 minutos, 1 hora, 4 horas, 1 día, 1 semana y 1 mes.

El indicador te permite personalizar los umbrales de sobrecompra y sobreventa, así como elegir entre ver los valores RSI para marcos de tiempo intradía o estándar, adaptando el análisis a tus necesidades específicas. 🔧📊

🔔 Las señales se generan cuando en 4 de los 6 marcos de tiempo que definimos a continuación:

Señal de Sobrecompra (Cuando el RSI indica sobrecompra):

• Intraday: Se activa cuando el RSI en los marcos de tiempo de 5 minutos, 15 minutos, 30 minutos y 1 hora está por encima del umbral de 70. 📈

• Standard: Se activa cuando el RSI en los marcos de tiempo de 30 minutos, 1 hora, 4 horas y 1 día están por encima del umbral de 70. 📈

Señal de Sobreventa (Cuando el RSI indica sobreventa):

• Intraday: Se activa cuando el RSI en los marcos de tiempo de 5 minutos, 15 minutos, 30 minutos y 1 hora está por debajo del umbral de 30. 📉

• Standard: Se activa cuando el RSI en los marcos de tiempo de 30 minutos, 1 hora, 4 horas y 1 día están por debajo del umbral de 30. 📉

TASC 2024.10 Adaptive Oscillator Threshold█ OVERVIEW

This script introduces a more dynamic approach to generating trading signals using the RSI indicator and a threshold that adapts to price trends and dispersion. This methodology comes from Francesco Bufi's article "Overbought/Oversold Oscillators: Useless Or Just Misused" from the October 2024 edition of TASC's Traders' Tips .

█ CONCEPTS

According to Francesco Bufi's observations, an oscillator-based buy signal should have a threshold that varies with the trend direction: higher during uptrends and lower during downtrends. Additionally, the level should decrease as the distance from the price to its mean increases to reduce signals in volatile conditions. Accordingly, Bufi proposes a formula for an adaptive buy level whose value is proportional to the trend (linear regression slope) and inversely proportional to the typical distance between price and its mean (standard deviation). Traders can apply this method to any oscillator to add adaptivity without modifying the oscillator's calculations, as it's simply an adaptive technique for interpreting the calculated values.

This script demonstrates the application of Bufi's Adaptive Threshold (BAT) in a simple RSI-based strategy and allows users to compare its performance to the traditional fixed-threshold approach. Bufi's observations suggest that using the BAT instead of a static threshold can help improve the backtest performance of oscillator-based systems.

█ DISCLAIMER

This strategy script educates users on the trading systems outlined by the TASC article. By default, it uses 10% of equity as the order size and a slippage amount of 5 ticks. Traders should adjust these settings and the commission amount when using this script.

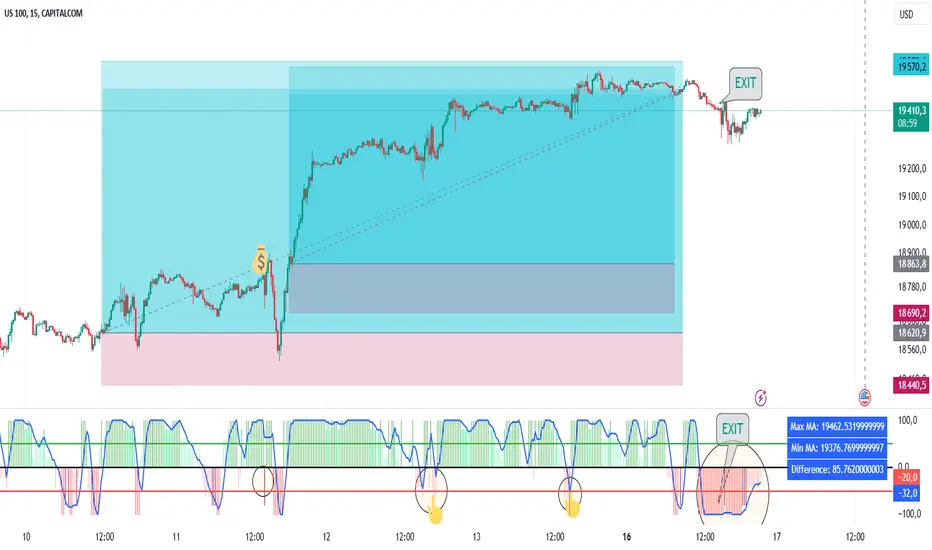

Power MarketPower Market Indicator

Description: The Power Market Indicator is designed to help traders assess market strength and make informed decisions for entering and exiting positions. This innovative indicator provides a comprehensive view of the evolution of Simple Moving Averages (SMA) over different periods and offers a clear measure of market strength through a total score.

Key Features:

Multi-Period SMA Analysis:

Calculates Simple Moving Averages (SMA) for 10 different periods ranging from 10 to 100.

Provides detailed analysis by comparing the current closing price with these SMAs.

Market Strength Measurement:

Assesses market strength by calculating a total score based on the relationship between the closing price and the SMAs.

The total score is displayed as a histogram with distinct colors for positive and negative values.

Smoothed Curve for Better View:

A smoothing of the total score is applied using a 5-period Simple Moving Average to represent the overall trend more smoothly.

Dynamic Information Table:

Real-time display of the maximum and minimum values among the SMAs, as well as the difference between these values, providing valuable insights into the variability of moving averages.

Visual Reference Lines:

Horizontal lines at zero, +50, and -50 for easy evaluation of key score levels.

How to Use the Indicator:

Position Entries: Use high positive scores to identify buying opportunities when market strength is strong.

Position Exits: Negative scores may signal market weakness, allowing you to exit positions or wait for a better opportunity.

Data Analysis: The table helps you understand the variability of SMAs, offering additional context for your trading decisions.

This powerful tool provides an in-depth view of market dynamics and helps you navigate your trading strategies with greater confidence. Embrace the Power Market Indicator and optimize your trading decisions today!

Connors RSI with Down GapThe Connors RSI with Down Gap indicator is a technical tool designed to support Larry Connors' Terror Gap Strategy, which is part of his broader framework outlined in the book "Buy the Fear, Sell the Greed: 7 Behavioral Quant Strategies for Traders." This specific indicator integrates the ConnorsRSI calculation with a focus on detecting down gaps in price, providing insights into moments when panic selling may occur.

The ConnorsRSI

ConnorsRSI is a composite indicator developed by Larry Connors that combines three core components:

RSI: A short-term relative strength index measuring the speed and magnitude of price changes.

Streak RSI: Tracks consecutive up or down closes to assess momentum.

Percent Rank: Evaluates how the current close ranks in relation to past prices.

When combined, these three elements provide a nuanced view of short-term overbought or oversold conditions. ConnorsRSI readings below a certain threshold (commonly 30 or lower) suggest that the asset has been heavily sold, indicating potential exhaustion of selling pressure.

Behavioral Finance Insights

The Terror Gap Strategy is grounded in principles from behavioral finance, which studies how psychological factors affect market participants' decision-making. Specifically, the indicator exploits the fear and irrational behavior that often arise when traders face persistent losses, especially after a down gap. According to behavioral finance theories like prospect theory (Kahneman & Tversky, 1979), people tend to overreact to losses, leading to panic selling. This creates opportunities for contrarian traders who understand the psychology behind these market movements.

The ConnorsRSI with Down Gap indicator works because it identifies:

Overextended selling through the ConnorsRSI, where persistent price declines result in low RSI values (indicating panic).

Gap down days, where the opening price is below the previous day’s close, typically amplifying the sense of loss and fear for traders already in losing positions.

Why This Indicator Works

The psychology of losses makes traders more prone to selling during periods of fear, especially when confronted with a gap down after sustained price declines. This indicator, by combining ConnorsRSI with down gaps, offers a quantitative way to spot these moments of panic. Traders can take advantage of these signals to enter positions when the market is in a state of fear, often when there is potential for a reversion to the mean.

Indicator Mechanics

In the current implementation:

The ConnorsRSI is calculated using three components: a short-term RSI, streak RSI, and percent rank.

When the ConnorsRSI drops below a user-defined lower threshold, the indicator highlights oversold conditions.

If there is a down gap (open price lower than the previous close) and the ConnorsRSI is below the threshold, a label is displayed, signaling a potential opportunity to buy.

Practical Use and Application

For traders looking to implement the Terror Gap Strategy, this indicator provides a clear visual cue (via background coloring and labels) when conditions are ripe for a contrarian trade. It can be particularly useful for traders who thrive on taking advantage of fear-driven sell-offs.

However, to fully understand and apply this strategy effectively, it is recommended to purchase Larry Connors' book "Buy the Fear, Sell the Greed." The book provides detailed explanations of how to execute the strategy with precision, including insights into exit conditions, scaling into positions, and managing risk.

Conclusion

The ConnorsRSI with Down Gap indicator combines quantitative analysis with behavioral finance principles to exploit fear-driven market behavior. By utilizing this tool within a disciplined trading strategy, traders can potentially profit from temporary market inefficiencies caused by panic selling.

References

Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263-291.

Connors, L. (2013). Buy the Fear, Sell the Greed: 7 Behavioral Quant Strategies for Traders.

This indicator can be a valuable asset, but understanding its proper use within a broader strategy framework is essential. Purchasing Connors' book is a recommended step toward mastering the approach.

Median Kijun-Sen [InvestorUnknown]The Median Kijun-Sen is a versatile technical indicator designed for both trend-following strategies and long-term market valuation. It incorporates various display modes and includes a backtest mode to simulate its performance on historical price action.

Key Features:

1. Trend-Following and Long-Term Valuation:

The indicator is ideal for trend-following strategies, helping traders identify entry and exit points based on the relationship between price and the Kijun-Sen calculated from median price (customizable price source).

With longer-term settings, it can also serve as a valuation tool (in oscillator display mode), assisting in identifying potential overbought or oversold conditions over extended timeframes.

2. Display Modes:

The indicator can be displayed in three main modes, each serving a different purpose:

Overlay Mode : Plots the Median Kijun-Sen directly over the price chart, useful for visualizing trends relative to price action.

Oscillator Mode : Displays the oscillator that compares the current price to the Median Kijun-Sen, providing a clearer signal of trend strength and direction

Backtest Mode : Simulates the performance of the indicator with different settings on historical data, offering traders a way to evaluate its reliability and effectiveness without needing TradingView's built-in strategy tool

3. Backtest Functionality:

The inbuilt backtest mode enables users to evaluate the indicator's performance across historical data by simulating long and short trades. Users can customize the start and end dates for the backtest, as well as specify whether to allow long & short, long only, or short only signals.

This backtest functionality mimics TradingView's strategy feature, allowing users to test the effectiveness of their chosen settings before applying them to live markets.

equity(series int sig, series float r, startDate, string signals, bool endDate_bool) =>

if time >= startDate and endDate_bool

float a = 0

if signals == "Long & Short"

if sig > 0

a := r

else

a := -r

else if signals == "Long Only"

if sig > 0

a := r

else if signals == "Short Only"

if sig < 0

a := -r

else

runtime.error("No Signal Type found")

var float e = na

if na(e )

e := 1

else

e := e * (1 + a)

float r = 0.0

bool endDate_bool = use_endDate ? (time <= endDate ? true : false) : true

float eq = 1.0

if disp_mode == "Backtest Mode"

r := (close - close ) / close

eq := equity(sig, r, startDate, signals, endDate_bool)

4. Hint Table for Pane Suggestions:

An inbuilt hint table guides users on how to best visualize the indicator in different display modes:

For Overlay Mode, it is recommended to use the same pane as the price action.

For Oscillator and Backtest Modes, it is advised to plot them in a separate pane for better clarity.

This table also provides step-by-step instructions on how to move the indicator to a different pane and adjust scaling, making it user-friendly.

Potential Weakness

One of the key drawbacks is the indicator’s tendency to produce false signals during price consolidations, where price action lacks clear direction and may trigger unnecessary trades. This is particularly noticeable in markets with low volatility.

Alerts

The indicator includes alert conditions for when it crosses above or below key levels, enabling traders to receive notifications of LONG or SHORT signals.

Summary

The Median Kijun-Sen is a highly adaptable tool that serves multiple purposes, from trend-following to long-term valuation. With its customizable settings, backtest functionality, and built-in hints, it provides traders with valuable insights into market trends while allowing them to optimize the indicator to their specific strategy.

This versatility, however, comes with the potential weakness of false signals during consolidation phases, so it's most effective in trending markets.

Larry Conners SMTP StrategyThe Spent Market Trading Pattern is a strategy developed by Larry Connors, typically used for short-term mean reversion trading. This strategy takes advantage of the exhaustion in market momentum by entering trades when the market is perceived as "spent" after extended trends or extreme moves, expecting a short-term reversal. Connors uses indicators like RSI (Relative Strength Index) and price action patterns to identify these opportunities.

Key Elements of the Strategy:

Overbought/Oversold Conditions: The strategy looks for extreme overbought or oversold conditions, often indicated by low RSI values (below 30 for oversold and above 70 for overbought).

Mean Reversion: Connors believed that markets, especially in short-term scenarios, tend to revert to the mean after periods of strong momentum. The "spent" market is assumed to have expended its energy, making a reversal likely.

Entry Signals:

In an uptrend, a stock or market index making a significant number of consecutive up days (e.g., 5-7 consecutive days with higher closes) indicates overbought conditions.

In a downtrend, a similar number of consecutive down days indicates oversold conditions.

Reversal Anticipation: Once an extreme in price movement is identified (such as consecutive gains or losses), the strategy places trades anticipating a reversion to the mean, which is usually the 5-day or 10-day moving average.

Exit Points: Trades are exited when prices move back toward their mean or when the extreme conditions dissipate, usually based on RSI or moving average thresholds.

Why the Strategy Works:

Human Psychology: The strategy capitalizes on the fact that markets, in the short term, often behave irrationally due to the emotions of traders—fear and greed lead to overextended moves.

Mean Reversion Tendency: Financial markets often exhibit mean-reverting behavior, where prices temporarily deviate from their historical norms but eventually return. Short-term exhaustion after a strong rally or sell-off offers opportunities for quick profits.

Overextended Moves: Markets that rise or fall too quickly tend to become overextended, as buyers or sellers get exhausted, making reversals more probable. Connors’ approach identifies these moments when the market is "spent" and ripe for a reversal.

Risks of the Spent Market Trading Pattern Strategy:

Trend Continuation: One of the key risks is that the market may not revert as expected and instead continues in the same direction. In trending markets, mean-reversion strategies can suffer because strong trends can last longer than anticipated.

False Signals: The strategy relies heavily on technical indicators like RSI, which can produce false signals in volatile or choppy markets. There can be times when a market appears "spent" but continues in its current direction.

Market Timing: Mean reversion strategies often require precise market timing. If the entry or exit points are mistimed, it can lead to losses, especially in short-term trades where small price movements can significantly impact profitability.

High Transaction Costs: This strategy requires frequent trades, which can lead to higher transaction costs, especially in markets with wide bid-ask spreads or high commissions.

Conclusion:

Larry Connors’ Spent Market Trading Pattern strategy is built on the principle of mean reversion, leveraging the concept that markets tend to revert to a mean after extreme moves. While effective in certain conditions, such as range-bound markets, it carries risks—especially during strong trends—where price momentum may not reverse as quickly as expected.

For a more in-depth explanation, Larry Connors’ books such as "Short-Term Trading Strategies That Work" provide a comprehensive guide to this and other strategies .

Dynamic Volume RSI (DVRSI) [QuantAlgo]Introducing the Dynamic Volume RSI (DVRSI) by QuantAlgo 📈✨

Elevate your trading and investing strategies with the Dynamic Volume RSI (DVRSI) , a powerful tool designed to provide clear insights into market momentum and trend shifts. This indicator is ideal for traders and investors who want to stay ahead of the curve by using volume-responsive calculations and adaptive smoothing techniques to enhance signal clarity and reliability.

🌟 Key Features:

🛠 Customizable RSI Settings: Tailor the indicator to your strategy by adjusting the RSI length and price source. Whether you’re focused on short-term trades or long-term investments, DVRSI adapts to your needs.

🌊 Adaptive Smoothing: Enable adaptive smoothing to filter out market noise and ensure cleaner signals in volatile or choppy market conditions.

🎨 Dynamic Color-Coding: Easily identify bullish and bearish trends with color-coded candles and RSI plots, offering clear visual cues to track market direction.

⚖️ Volume-Responsive Adjustments: The DVRSI reacts to volume changes, giving greater significance to high-volume price moves and improving the accuracy of trend detection.

🔔 Custom Alerts: Stay informed with alerts for key RSI crossovers and trend changes, allowing you to act quickly on emerging opportunities.

📈 How to Use:

✅ Add the Indicator: Set up the DVRSI by adding it to your chart and customizing the RSI length, price source, and smoothing options to fit your specific strategy.

👀 Monitor Visual Cues: Watch for trend shifts through the color-coded plot and candles, signaling changes in momentum as the RSI crosses key levels.

🔔 Set Alerts: Configure alerts for critical RSI crossovers, such as the 50 line, ensuring you stay on top of potential market reversals and opportunities.

🔍 How It Works:

The Dynamic Volume RSI (DVRSI) is a unique indicator designed to provide more accurate and responsive signals by incorporating both price movement and volume sensitivity into the RSI framework. It begins by calculating the traditional RSI values based on a user-defined length and price source, but unlike standard RSI tools, the DVRSI applies volume-weighted adjustments to reflect the strength of market participation.

The indicator dynamically adjusts its sensitivity by factoring in volume to the RSI calculation, which means that price moves backed by higher volumes carry more weight, making the signal more reliable. This method helps identify stronger trends and reduces the risk of false signals in low-volume environments. To further enhance accuracy, the DVRSI offers an adaptive smoothing option that allows users to reduce noise during periods of market volatility. This adaptive smoothing function responds to market conditions, providing a cleaner signal by reducing erratic movements or price spikes that could lead to misleading signals.

Additionally, the DVRSI uses dynamic color-coding to visually represent the strength of bullish or bearish trends. The candles and RSI plots change color based on the RSI values crossing critical thresholds, such as the 50 level, offering an intuitive way to recognize trend shifts. Traders can also configure alerts for specific RSI crossovers (e.g., above 50 or below 40), ensuring that they stay informed of potential trend reversals and significant market shifts in real-time.

The combination of volume sensitivity, adaptive smoothing, and dynamic trend visualization makes the DVRSI a robust and versatile tool for traders and investors looking to fine-tune their market analysis. By incorporating both price and volume data, this indicator delivers more precise signals, helping users make informed decisions with greater confidence.

Disclaimer:

The Dynamic Volume RSI is designed to enhance your market analysis but should not be used as a sole decision-making tool. Always consider multiple factors before making any trading or investment decisions. Past performance is not indicative of future results.

RishiMoney RSIRishiMoney RSI

The "RishiMoney RSI" indicator is designed for traders who want to leverage the power of the Relative Strength Index (RSI) across multiple timeframes.

In addition to regular RSI, this script allows the users to select custom timeframes for two additional RSI calculations, making it easier to identify trends, reversals, and potential entry or exit points.

USAGE

While Returning the same information as a regular RSI the RishiMoney RSI provides two more RSI calculations One for Lagrgest Timeframe and one for middle Timeframe so that the users need not to check for higher timeframes separately Which is very Time consuming. This script solves the problem of time taking process of checking different timeframes RSI calculations.

This script is ideal for traders who want to confirm their analysis across multiple timeframes. By comparing the main RSI with larger and intermediate timeframes, traders can better understand the market's momentum and make more informed decisions.

The RishiMoney RSI crossing above the overbought level can be indicative of a strong uptrend which is highlighted as a green gradient area, while when RishiMoney RSI is crossing under the oversold level can be indicative of a strong downtrend which is highlighted as a red area.

Key Features:

Customizable RSI Period: Set your preferred RSI period for precise calculation and analysis.

Multi-Timeframe RSI:

Largest RSI Timeframe: Choose the largest timeframe for your analysis (Monthly, Weekly, Daily, Hourly, 15 minutes, or 5 minutes).

Middle RSI Timeframe: Select an intermediate timeframe for comparison with the main RSI.

Overbought and Oversold Levels: The indicator includes customizable overbought and oversold levels, which are clearly marked on the chart with dynamic bands.

Alerts: Set up alerts for when the RSI crosses into overbought or oversold territory, so you never miss a potential trading opportunity.

Visual Clarity: The script plots the RSI for your selected timeframes with distinct colors, helping you quickly identify trends across different timeframes.

This script is provided for educational purposes only and should not be considered financial advice. Always conduct your own research and consult with a financial advisor before making any trading decisions.

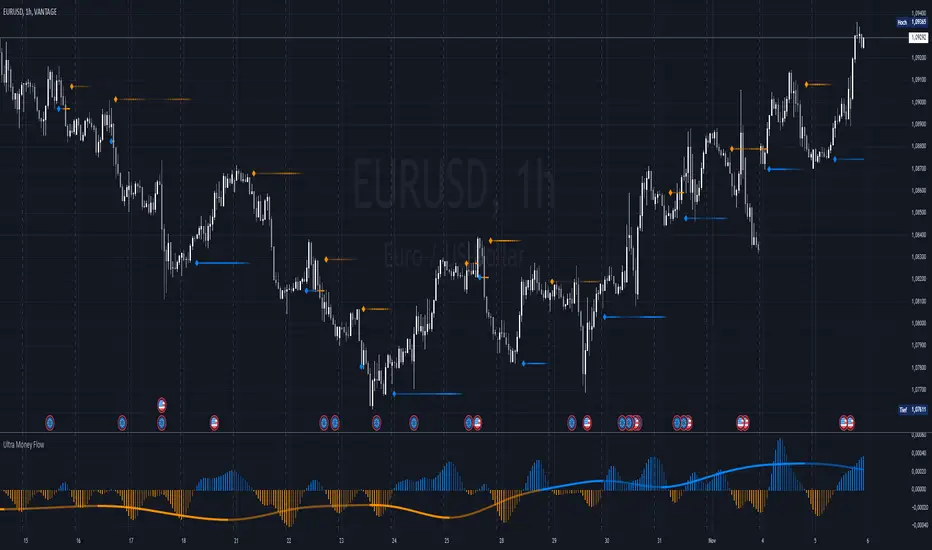

Ultra Money FlowIntroduction

The Ultra Money Flow script is a technical indicator for analyzing stock trends. It highlights buying and selling power, helping you identify bullish (rising) or bearish (falling) market trends.

Detailed Description

The Ultra Money Flow script calculates and visually displays two main components: Fast and Slow money flow. These components represent short-term and long-term trends, respectively.

Here's how it works:

.........

Inputs

You can adjust the speed of analysis (Fast Length and Slow Length) and the type of smoothing applied (e.g., Simple Moving Average, Exponential Moving Average).

Choose colors for visualizing the trends, with blue for bullish (positive) and orange for bearish (negative) movements.

.....

Money Flow Calculation

The script analyzes price changes (delta) over specified periods.

It separates upward price movements (buying power) from downward ones (selling power).

It then calculates the difference between these powers for both Fast and Slow components.

The types of smoothing methods range from traditional ones like the Simple Moving Average (SMA) to advanced ones like the Double Expotential Moving Average (DEMA) or the Triple Exponential Moving Average (TEMA) or the Recursive Moving Average (RMA) or the Weigthend Moving Average (WMA) or the Volume Weigthend Moving Average (VWMA) or Hull Moving Average (HMA).

Very Special ones are the Triple Weigthend Moving Average (TWMA) wich created RedKTrader .

I created the Multi Weigthend Moving Average (MWMA) wich is a simple signal line to the TWMA.

.....

Divergence

This indicator can show divergence by comparing the direction of price movements with the indicator value.

If the price and the indicator move in opposite directions, you can use these signals to help decide when to buy or sell.

.....

Auto Scaling

The script adjusts its calculations based on the time frame you are viewing, whether it's minutes, hours, or days, ensuring accurate representation across different time scales.

.....

Plotting

The script plots the Fast component as a histogram and the Slow component as a line, using the chosen colors to indicate bullish or bearish trends.

The thickness and transparency of these plots give additional clues about the strength of the trend.

.........

By using this indicator, traders can easily spot shifts in buying and selling power, allowing for better-informed decisions in the market.

Special Thanks

I use the TWMA-Function created from RedKTrader to smooth the values.

Special thanks to him for creating and sharing this function!

RSI Buy/Sell SignalsThis Pine Script is designed to plot Buy and Sell signals based on the Relative Strength Index (RSI) for both 15-minute and hourly timeframes. It calculates the RSI values for the current 15-minute chart and requests the hourly RSI data for comparison. Buy signals are generated when the RSI crosses above 60 in either timeframe, while sell signals occur when the RSI crosses below 40. The script also plots visual markers on the chart, indicating buy signals with green labels below the price bars and sell signals with red labels above the price bars. Additionally, it allows for alert conditions, notifying the user when a buy or sell signal is triggered.

RSI 15/60 and ADX PlotIn this script, the buy and sell criteria are based on the Relative Strength Index (RSI) values calculated for two different timeframes: the 15-minute RSI and the hourly RSI. These timeframes are used together to check signals when certain thresholds are crossed, providing confirmation across both short-term and longer-term momentum.

Buy Criteria:

Condition 1:

Hourly RSI > 60: This means the longer-term momentum shows strength.

15-minute RSI crosses above 60: This shows that the shorter-term momentum is catching up and confirms increasing strength.

Condition 2:

15-minute RSI > 60: This indicates that the short-term trend is already strong.

Hourly RSI crosses above 60: This confirms that the longer-term trend is also gaining strength.

Both conditions aim to capture the moments when the market shows increasing strength across both short and long timeframes, signaling a potential buy opportunity.

Sell Criteria:

Condition 1:

Hourly RSI < 40: This indicates that the longer-term trend is weakening.

15-minute RSI crosses below 40: The short-term momentum is also turning down, confirming the weakening trend.

Condition 2:

15-minute RSI < 40: The short-term trend is already weak.

Hourly RSI crosses below 40: The longer-term trend is now confirming the weakness, indicating a potential sell.

These conditions work to identify when the market is showing weakness in both short-term and long-term timeframes, signaling a potential sell opportunity.

ADX Confirmation :

The Average Directional Index (ADX) is a key tool for measuring the strength of a trend. It can be used alongside the RSI to confirm whether a buy or sell signal is occurring in a strong trend or during market consolidation. Here's how ADX can be integrated:

ADX > 25: This indicates a strong trend. Using this threshold, you can confirm buy or sell signals when there is a strong upward or downward movement in the market.

Buy Example: If a buy signal (RSI > 60) is triggered and the ADX is above 25, this confirms that the market is in a strong uptrend, making the buy signal more reliable.

Sell Example: If a sell signal (RSI < 40) is triggered and the ADX is above 25, it confirms a strong downtrend, validating the sell signal.

ADX < 25: This suggests a weak or non-existent trend. In this case, RSI signals might be less reliable since the market could be moving sideways.

Final Approach:

The RSI criteria help identify potential overbought and oversold conditions in both short and long timeframes.

The ADX confirmation ensures that the signals generated are happening during strong trends, increasing the likelihood of successful trades by filtering out weak or choppy market conditions.

This combination of RSI and ADX can help traders make more informed decisions by ensuring both momentum and trend strength align before entering or exiting trades.

Bull Bear Power With EMA FilterDescription of Indicator:

This Pine Script indicator colors price bars based on the open price in relation to custom moving averages (EMA/SMA), Bull/Bear Power (BBPower), and an optional VWAP filter. The bar colors help identify bullish and bearish conditions with added visual cues for price positioning relative to VWAP.

Key Features:

Customizable Moving Averages (EMA/SMA):

The user can select between EMA or SMA for both short-term and long-term moving averages.

Default moving averages are set to 5 (short-term) and 9 (long-term) but can be adjusted by the user.

Bullish Condition (Blue or Purple Bars):

A bar is colored blue if the following conditions are met:

The open price is above both the short-term and long-term moving averages.

The short-term moving average (MA 1) is above the long-term moving average (MA 2).

BBPower (open price minus the 13-period EMA) is positive, indicating bullish strength.

If the VWAP filter is enabled and the price opens below VWAP, the bullish bars will turn purple.

Bearish Condition (Yellow or Orange Bars):

A bar is colored yellow if the following conditions are met:

The open price is below both the short-term and long-term moving averages.

The short-term moving average (MA 1) is below the long-term moving average (MA 2).

BBPower is negative or zero, indicating bearish market conditions.

If the VWAP filter is enabled and the price opens above VWAP, the bearish bars will turn orange.

VWAP Filter (Optional):

An optional filter allows the user to add VWAP (Volume-Weighted Average Price) to the bar coloring logic.

When the VWAP filter is enabled, it provides additional information about price positioning relative to VWAP, turning bullish bars purple and bearish bars orange depending on whether the price opens above or below VWAP.

Usage:

Bullish Trend: Look for blue or purple bars to identify potential bullish momentum.

Bearish Trend: Look for yellow or orange bars to spot bearish conditions in the market.

The indicator allows users to customize the length and type of moving averages (EMA or SMA), as well as decide whether to apply the VWAP filter.

This indicator provides traders with clear visual signals to quickly assess the strength of bullish or bearish conditions based on the price's position relative to custom moving averages, BBPower, and VWAP, helping with trend identification and potential trade setups.

RCYC Bullish Bearish Indicator

Summary: The RCYC Bullish Bearish Indicator is a custom trading tool designed to help traders identify potential bullish and bearish conditions in the market using a combination of KDJ and RSI indicators. This indicator uses color-coded candles to visually represent bullish and bearish signals, making it easy to identify trend changes on the chart. The script is particularly useful for traders who prefer visual signals and want to incorporate both trend momentum (KDJ) and relative strength (RSI) in their analysis.

Description:

The RCYC Bullish Bearish Indicator is a unique mashup of the KDJ and RSI indicators, optimized to provide a clear visual representation of market conditions through color-coded candles. This indicator not only identifies the potential trend shifts but also provides alerts for significant crossover points, enhancing a trader's ability to make informed decisions.

How It Works:

KDJ Calculation:

The KDJ is a variation of the Stochastic Oscillator that includes the %J line, which can go beyond the typical 0-100 range of %K and %D.

The KDJ component of this indicator calculates the highest high and lowest low over a specified period (KDJ Length), using these values to derive the %K line.

The %D line is a smoothed version of %K, and the %J line is derived from %K and %D using the formula: J = 3 * %K - 2 * %D.

This indicator focuses on the behavior of the %J line in relation to a mid-point level (50), identifying crossovers and crossunders that signal potential shifts in market sentiment.

RSI Calculation:

The Relative Strength Index (RSI) is a momentum oscillator that measures the speed and change of price movements. It is widely used to identify overbought or oversold conditions.

In this indicator, RSI values are adjusted and plotted to align visually with the KDJ values, providing a complementary momentum analysis.

Crossover Logic and Candle Coloring:

The indicator tracks two main events:

CrossOver50: When the %J line crosses above the 50 level, indicating potential bullish momentum.

CrossUnder50: When the %J line crosses below the 50 level, indicating potential bearish momentum.

Depending on the crossover events, the script changes the color of the candles on the chart:

Red candles on the initial crossover above 50, followed by dark blue candles to maintain bullish sentiment.

Yellow candles on the initial crossover below 50, followed by light blue candles to maintain bearish sentiment.

Alerts:

The indicator includes alert conditions for both bullish and bearish signals:

Red Candle Alert: Notifies the trader when the %J line crosses above 50.

Yellow Candle Alert: Notifies the trader when the %J line crosses below 50.

These alerts allow traders to react promptly to key market signals without continuously monitoring the chart.

Usage and Benefits:

This indicator is designed for traders looking to combine momentum and trend analysis into a single visual tool. It is particularly useful for those trading in trending markets or looking for entry/exit signals based on momentum shifts.

The color-coded candles provide an intuitive way to assess market conditions at a glance, reducing the complexity associated with analyzing multiple indicators separately.

By integrating both KDJ and RSI, the RCYC Bullish Bearish Indicator offers a balanced approach to trend detection and momentum confirmation, making it versatile for various trading styles, including scalping, swing trading, and position trading.

Originality and Usefulness:

While the indicator builds upon the familiar concepts of KDJ and RSI, it uniquely merges them into a cohesive visual tool with distinct crossover-based alerts and candle coloring.

This approach makes the indicator original, as it simplifies the interpretation of complex signals into straightforward visual cues, enhancing the decision-making process for traders who prefer chart-based analysis.

Color Coded RSI [Phantom]Color Coded RSI

The Color Coded RSI enhances the standard RSI (Relative Strength Index) by applying dynamic color coding to the price bars, making it easier to visualize RSI levels directly on the chart.

Key Feature:

RSI-Based Color Coding: Price bars change color based on RSI values. High RSI values (above 70) show warm colors (red/orange), signaling potential overbought conditions, while low RSI values (below 30) display cool colors (blue), indicating possible oversold levels.

How to Trade with Color Coded RSI:

Overbought (Red/Orange Bars):

When the bars turn red or orange (RSI above 70), the market might be overbought. This could be a signal to sell or exit long positions, expecting a pullback.

Oversold (Blue Bars):

Blue bars (RSI below 30) suggest the market is oversold. Look for buying opportunities or consider exiting short positions, anticipating a rebound.

Neutral (Gray/Green Bars):

Gray or green bars (RSI near 50) indicate neutral conditions. You may want to wait for a clearer trend before taking action.

RSI is best used with other indicators to provide confirmations.

Tian Di Grid Merge Version 6.0

Strategy Introduction:

1. We know that the exchange can only set a maximum of 100 grids. However, our grid strategy can set a maximum of 350 grids.

2. We have added the modes of proportional and differential warehousing.

3. It should be noted that we have not set any filtering conditions, which means that when the price falls below the grid, we will execute a buy action at the closing price, and when the price falls above the grid, we will execute a sell action;

4. We suggest limiting the trading time cycle to 5 meters, as sometimes errors may appear on TV due to the dense grid or the inability to draw so many grids;

5. Please ensure that the minimum spacing between each grid is not less than 0.1%, as this is extremely difficult to profit from, and on the other hand, it may not function due to excessively dense spacing;

6. The maximum number of grids is 350, and the minimum number is currently 3;

matters needing attention:

Don't choose to go long or short together, and don't choose to go even short or short;

Closing position setting: It is recommended to select it to avoid order accumulation;

Unable to trade: If unable to trade normally, switch to a 1m cycle;

Number of cells: Calculate it yourself, 350 is just the maximum number of cells that can be adjusted;

Grid spacing: minimum 0.1%, below which no profit can be made;

Position value: default is 100u, which is the amount already leveraged;

Multiple investment: The order amount for each order is the same, and there is no need for multiple investment;

Open both long and short positions: You can open multiple positions for one account and open one position for one account. Do not open both long and short positions for the same target at the same time

Advanced Stochastic ForLoopAdvanced Stochastic ForLoop

OVERVIEW

Advanced Stochastic ForLoop is an improved version of Stochastic it is designed to calculate an array of values 1 or -1 depending if soruce for calculations is above or below basis.

It takes avereage of values over a range of lengths, providing trend signals smothed based on various moving averages in order to get rid of noise.

It offers flexibility with different signal modes and visual customizations.

TYPE OF SIGNALS

-FAST (MA > MA or MA > 0.99)

-SLOW (MA > 0)

-THRESHOLD CROSSING (set by user treshold for both directions)

-FAST THRESHOLD (when theres an change in signal by set margin e.g 0.4 -> 0.2 means bearsih when FT is set to 0.1, when MA is > 0.99 it will signal bullish, when MA < -0.99 it will signal bearish)

Generaly Lime color of line indicates Bullish, Fuchsia indicates Bearish.

This colors are not set in stone so you can change them in settings.

Alerts included when line color is:

-Bullish Trend, line color is lime

-Bearish Trend, line color is fuchsia

Credit

Idea for this script was from one of indicators created by www.tradingview.com

Warning

This indicator can be really noisy depending on the settings, signal mode so it should be used preferably as a part of an strategy not as a stand alone indicator

Remember the lower the timeframe you use the more noise there is.

No single indicator should be used alone when making investment decisions.