Bullrun Profit Maximizer [QuantraSystems]Bullrun Profit Maximizer

Quantra Systems guarantees that the information created and published within this document and on the Tradingview platform is fully compliant with applicable regulations, does not constitute investment advice, and is not exclusively intended for qualified investors.

Important Note!

The system equity curve presented here has been generated as part of the process of testing and verifying the methodology behind this script.

Crucially, it was developed after the system was conceptualized, designed, and created, which helps to mitigate the risk of overfitting to historical data. In other words, the system was built for robustness, not for simply optimizing past performance.

This ensures that the system is less likely to degrade in performance over time, compared to hyper optimized systems that are tailored to past data. No tweaks or optimizations were made to this system post backtest.

Even More Important Note!!

The nature of markets is that they change quickly and unpredictably. Past performance does not guarantee future results - this is a fundamental rule in trading and investing.

While this system is designed with broad, flexible conditions to adapt quickly to a range of market environments, it is essential to understand that no assumptions should be made about future returns based on historical data. Markets are inherently uncertain, and this system - like all trading systems - cannot predict future outcomes.

Introduction

The "Adaptive Pairwise Momentum System" is not a prototype to the Bullrun Profit Maximizer (BPM) . The Bullrun Profit Maximizer is a fully re-engineered, higher frequency momentum system.

The Bullrun Profit Maximizer (BPM) uses a completely different filter logic and refines momentum calculations, specifically to support higher frequency trading on Crypto's Blue Chip assets. It correctly calculates fees and slippage by compounding them against System Profit before plotting the equity curve.

Unlike prior systems, this script utilizes a completely new filter logic and refined momentum calculation, specifically built to support higher frequency trading on blue-chip assets, while minimizing the impact of fees and slippage.

While the APMS focuses on Macro Trend Alignment, the BPM instead applies an equity curve based filter, allowing for targeted precision on the current asset’s trend without relying on broader market conditions. This approach delivers more responsive and asset specific signals, enhancing agility in today’s fast paced crypto markets.

The BPM dynamically optimizes capital allocation across up to four high performing assets, ensuring that the portfolio adapts swiftly to changing market conditions. The system logic consists of sophisticated quantitative methods, rapid momentum analysis and alpha cyclicality/seasonality optimizations. The overarching goal is to ensure that the portfolio is always invested in the highest performing asset based on dynamic market conditions, while at the same time managing risk through rapid asset filters and internal mechanisms like alpha cyclicality, volatility and beta analysis.

In addition to these core functionalities, the BPM comes with the typical Quantra Systems UI design, structured to reduce data clutter and provide users with only the most essential, impactful information. The BPM UI format delivers clear and easy to read signals. It enables rapid decision making in a high frequency environment without compromising on depth or accuracy.

Bespoke Logic Filtering with Equity Curve Precision

The BPM script utilizes a completely new methodology and focuses on intraday rotations of blue-chip crypto assets, while previously built systems were designed with a longer term focus in mind.

In response to the need for more precise signal generation, the BPM replaces the previous macro trend filter with a new, highly specific equity curve activation filter. This unique logic filter is driven solely by the performance trends of the asset currently held by the system. By analyzing the equity curve directly, this system can make more targeted, timely allocations based on asset specific momentum, allowing for quick adjustments that are more relevant to the held asset rather than general market conditions.

The benefits of this new, unique approach are twofold: first, it avoids premature allocation shifts based on broader macro movements, and second, it enables the system to adapt dynamically to the performance of each asset individually. This asset specific filtering allows traders to capitalize on localized strength within individual blue-chip cryptoassets without being affected by lags in the overall market trend.

High Frequency Momentum Calculation for Enhanced Flexibility

The BPM incorporates a newly designed momentum calculation that increases its suitability across lower timeframes. This new momentum indicator captures and processes more data points within a shorter window than ever before, rather than extending bar intervals and potentially losing high frequency detail. This creates a smooth, data rich featureset that is especially suited for blue-chip assets, where liquidity reduces slippage and fees, making higher frequency trading viable.

By retaining more data, this system captures subtle shifts in momentum more effectively than traditional approaches, offering higher resolution insights. These modifications result in a system capable of generating highly responsive signals on faster timeframes, empowering traders to act quickly in volatile markets.

User Interface and Enhanced Readability

The BPM also features a reimagined, streamlined user interface, making it easier than ever to monitor essential signals at a glance. The new layout minimizes extraneous data points in the tables, leaving only the most actionable information for traders. This cleaner presentation is purpose built to help traders identify the strongest asset in real time, with clear, color coded signals to facilitate swift decision making in fast moving markets.

Equity Stats Table : Designed for clarity, the stats table focuses on the current allocation’s performance metrics, emphasizing the most critical metrics without unnecessary clutter.

Color Coded Highlights : The interface includes the option to highlight both the current top performing asset, and historical allocations - with indicators of momentum shifts and performance metrics readily accessible.

Clear Signals : Visual cues are presented in an enhanced way to improve readability, including simplified line coloring, and improve visualization of the outperforming assets in the allocation table.

Dynamic Asset Reallocation

The BPM dynamically allocates capital to the strongest performing asset in a selected pool. This system incorporates a re-engineered, pairwise momentum measurement designed to operate at higher frequencies. The system evaluates each asset against others in real time, ensuring only the highest momentum asset receives allocation. This approach keeps the portfolio positioned for maximum efficiency, with an updated weighting logic that favors assets showing both strength and sustainability.

Position Changes and Slippage Calculation

Position changes are optimized for faster reallocation, with realistic slippage and fee calculations factored into each trade. The system’s structure minimizes the impact of these costs on blue-chip assets, allowing for more active management on short timeframes without incurring significant drag on performance.

A Special Note on Fees + Slippage

In the image above, the system has been applied to four different timeframes - 12h, 8h, 4h and 1h - using identical settings and a selected slippage and fees amount of 0.2%. In this stress test, we isolate the choppy downwards period from the previous Bitcoin all time high - set in March 2024, to the current date where Bitcoin is currently sitting at around the same level.

This illustrates an important concept: starting at the 12h, the system performed better as the timeframes decreased. In fact, only on the 4hr chart did the system equity curve make a new all time high alongside Bitcoin. It is worth noting that market phases that are “non-trending” are generally the least profitable periods to use a momentum/trend system - as most systems will get caught by false momentum and will “buy the top,” and then proceed to “sell the bottom.”

Lower timeframes typically offer more data points for the algorithm to compute over, and enable quicker entries and exits within a robust system, often reducing downside risk and compounding gains more effectively - in all market environments.

However, slippage, fees, and execution constraints are still limiting factors. Although blue-chip cryptocurrencies are more liquid and can be traded with lower fees compared to low cap assets, frequent trading on lower timeframes incurs cumulative slippage costs. With the BPM system set to a realistic slippage rate of 0.2% per trade, this example emphasizes how even lower fees impact performance as trade frequency increases.

Finding the optimal balance between timeframe and slippage impact requires careful consideration of factors such as portfolio size, liquidity of selected tokens, execution speed, and the fee rate of the exchange you execute trades on.

Number of Position Changes

Understanding the number of position changes in a strategy is critical to assessing its feasibility in real world trading. Frequent position changes can lead to increased costs due to slippage and fees. Monitoring the number of position changes provides insight into the system’s behavior - helping to evaluate how active the strategy is and whether it aligns with the trader's desired time input for position management.

Equity Curve and Performance Calculations

To provide a benchmark, the script also generates a Buy-and-Hold (or "HODL") equity curve that represents a 100% allocation to Bitcoin, the highest market cap cryptoasset. This allows users to easily compare the performance of the dynamic rotation system with that of a more traditional investment strategy.

The script tracks key performance metrics for both the dynamic portfolio and the HODL strategy, including:

Sharpe Ratio

The Sharpe Ratio is a key metric that evaluates a portfolio’s risk adjusted return by comparing its ‘excess’ return to its volatility. Traditionally, the Sharpe Ratio measures returns relative to a risk-free rate. However, in our system’s calculation, we omit the risk-free rate and instead measure returns above a benchmark of 0%. This adjustment provides a more universal comparison, especially in the context of highly volatile assets like cryptocurrencies, where a traditional risk-free benchmark, such as the usual 3-month T-bills, is often irrelevant or too distant from the realities of the crypto market.

By using 0% as the baseline, we focus purely on the strategy's ability to generate raw returns in the face of market risk, which makes it easier to compare performance across different strategies or asset classes. In an environment like cryptocurrency, where volatility can be extreme, the importance of relative return against a highly volatile backdrop outweighs comparisons to a risk-free rate that bears little resemblance to the risk profile of digital assets.

Sortino Ratio

The Sortino Ratio improves upon the Sharpe Ratio by specifically targeting downside risk and leaves the upside potential untouched. In contrast to the Sharpe Ratio (which penalizes both upside and downside volatility), the Sortino Ratio focuses only on negative return deviations. This makes it a more suitable metric for evaluating strategies like the Bullrun Profit Maximizer - that aim to minimize drawdowns without restricting upside capture. By measuring returns relative to a 0% baseline, the Sortino ratio provides a clearer assessment of how well the system generates gains while avoiding substantial losses in highly volatile markets like crypto.

Omega Ratio

The Omega Ratio is calculated as the ratio of gains to losses across all return thresholds, providing a more complete view of how the system balances upside and downside risk even compared to the Sortino Ratio. While it achieves a similar outcome to the Sortino Ratio by emphasizing the system's ability to capture gains while limiting losses, it is technically a mathematically superior method. However, we include both the Omega and Sortino ratios in our metric table, as the Sortino Ratio remains more widely recognized and commonly understood by traders and investors of all levels.

Usage Summary:

While the backtests in this description are generated as if a trader held a portfolio of just the strongest tokens, this was mainly designed as a method of logical verification and not a recommended investment strategy. In practice, this system can be used in multiple ways.

It can be used as above, or as a factor in forming part of a broader asset selection tool, or even a method of filtering tokens by strength in order to inform a day trader which tokens might be optimal to look at, for long-only trading setups on an intrabar timeframe.

Summary

The Bullrun Profit Maximizer is an advanced tool tailored for traders, offering the precision and agility required in today’s markets. With its asset specific equity curve filter, reworked momentum analysis, and streamlined user interface, this system is engineered to maximize gains and minimize risk during bullmarkets, with a strong focus on risk adjusted performance.

Its refined approach, focused on high resolution data processing and adaptive reallocation, makes it a powerful choice for traders looking to capture high quality trends on clue-chip assets, no matter the market’s pace.

Outperformance

Stock vs Custom Symbol OutperformanceStock vs Custom Symbol Outperformance" is a powerful technical analysis indicator designed to help traders and investors gauge the relative performance of a stock against a selected benchmark symbol. This tool enables users to easily visualize how a stock is performing in comparison to another asset, such as an index or another stock.

Key Features:

Custom Symbol Comparison: Input any symbol to compare against the stock of interest, allowing for flexible analysis tailored to specific market conditions.

Outperformance Calculation: The indicator calculates the percentage change in price for both the stock and the selected benchmark, providing a clear view of relative performance.

Moving Average Smoothing: A customizable moving average smooths the outperformance data, helping to identify trends and reduce noise in the signals.

Threshold Lines: Set upper and lower threshold lines to visualize significant levels of outperformance or underperformance, aiding in decision-making.

Dynamic Color Coding: The outperformance bars are color-coded—green indicates that the stock is outperforming the benchmark, while red indicates underperformance.

How to Use:

Select a Benchmark: Use the input field to choose the symbol against which you want to compare the stock.

Adjust Parameters: Modify the moving average length and set your desired thresholds for easier identification of performance metrics.

Interpret Results: Analyze the plot for insights into the stock's performance relative to the benchmark, with the moving average providing additional context for trends.

This indicator is ideal for traders looking to refine their strategies by understanding how individual stocks measure up against key benchmarks in the market.

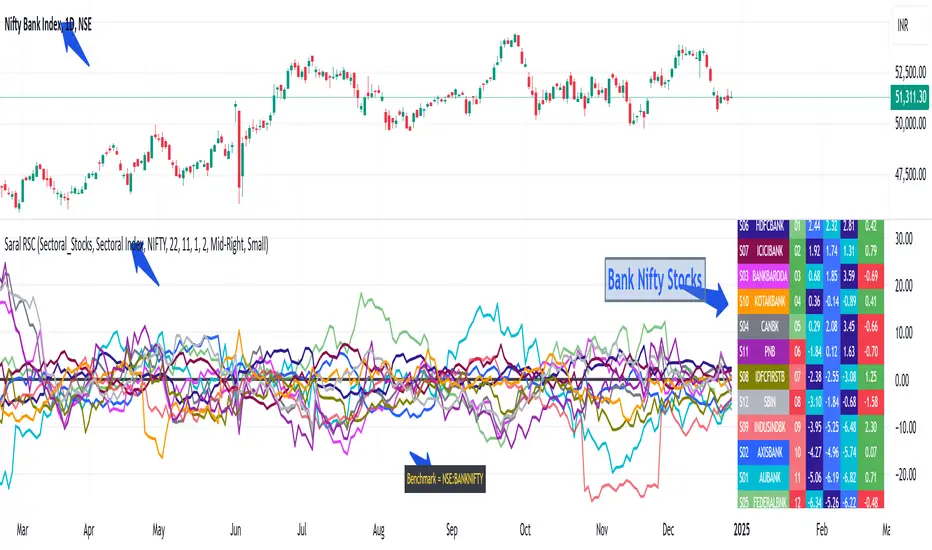

Saral Relative Strength ComparisonRelative Strength Comparison

### Overview

The Relative Strength (RS) Indicator is a robust tool designed to measure the performance of sectors or stocks relative to a benchmark index. This indicator provides a comprehensive way to compare the relative strength of different sectors or stocks, with the default selection being the major sectors of the National Stock Exchange (NSE). It allows traders to analyze which sectors or stocks are outperforming or underperforming the benchmark over a specific period.

The RS compares how much a security's price has changed over a given period relative to the change in price of a benchmark over the same period. The result is expressed as a percentage, showing whether the security has outperformed or underperformed the benchmark. Positive RS values indicate outperformance, while negative values signal underperformance.

This indicator provides a dual representation of the data. RS values are displayed in both line charts and a table. The line charts provide a visual representation of trends, while the table offers a clear numerical comparison of the current, previous, and earlier RS values along with the rank of the sector/stock.

### Key Features

Benchmark & Sectors/Stocks Comparison:

Users can select a benchmark index (default: NIFTY 50) and up to 20 sectors or stocks for comparison. By default, the indicator includes the major sectors of NSE, but users can customize the selection as needed.

Customizable RS Calculation:

Users can set the period for RS calculation, with a default of 22 periods, providing flexibility to match different trading strategies.

Flexible Time Frame:

RS calculations are based on the time frame of the main chart, allowing users to seamlessly switch between different periods, from minutes to hours, days, weeks, or even months depending on their analysis needs.

Customizable Line Chart:

Users can adjust the width and color of the RS lines for each sector, making it easier to distinguish between different sectors on the chart.

Dynamic Table Display:

The indicator includes a toggle to display a table of RS values, with customizable position, toggle for background color coding, and selection for text color & size. This makes it easy to compare the RS values across multiple sectors at a glance.

Sorting Options:

The table can be sorted either by alphabetical order of sector/stock names or by their rank. The default sorting is by rank, but switching to alphabetical order helps to identify data of specific sector with ease.

Ranking System:

The table includes a column displaying the rank of each sector or stock based on their RS, with the top-performing items listed first by default. This helps users quickly identify market leaders and laggards.

Color-Coded Backgrounds:

The background color of the sector/stock names in the table corresponds to the colors of their RS lines on the chart, making it easy to correlate table data with the visual plots. Also, the table uses a color-coding system which shows ranks of RS Positive sectors with Green background and RS Negative sectors with Red background. Similarly, the maximum RS value of individual sector is highlighted in Navy Blue, the minimum in Aqua and other in Blue background. This visual aid helps users quickly identify the performance trend of individual sector.

Table Positioning:

The table can be positioned at different locations on the chart (Top Right, Middle Right, Bottom Right, Top Left, Middle Left, Bottom Left), ensuring it doesn't obstruct important chart data.

### Input - RS Parameters:

Benchmark: Ticker ID of the comparative security. The default benchmark is the NIFTY 50 index, but users can select any other ticker as the benchmark for comparison.

Period-RS: The period for calculating the RS line. The default period is 22, but users can adjust this to suit their trading strategy and to analyze different time horizons for sector performance.

Line Width: Determines the thickness of the RS line in the chart. The default width is 2, providing a clear visual distinction between different sectors.

### Input - Table Parameters:

Show Table: Toggle to display or hide the table, allowing users to switch between graphical and tabular data representations.

Table Sorting: Users can sort the table alphabetically or by RS rank. The default sorting is by rank.

Table Position: Allows users to select the position of the table on the chart. Options include Top Right, Middle Right, Bottom Right, Top Left, Middle Left, and Bottom Left. The default position is Middle Right.

Color Code for Background: The background of the sector/stock names corresponds to their plot colors for easy mapping between plot and table values. Rank of RS Positive sectors will be highlighted with Green background and RS Negative sectors will be highlighted with Red color. The background color of the RS values in the table will change based on their magnitude. The highest RS value is Navy Blue, the lowest is Aqua, and other is Blue. This visual aid helps users quickly identify the performance of which sectors are improving or deteriorating.

Text Color: Users can select the color of the text displayed in the table. The default text color is White, ensuring readability against various background colors.

Text Size: Allows users to choose the size of the text in the table. Options include Auto, Tiny, Small, Medium, and Large, with the default being Small. This customization ensures that the table remains legible on different chart sizes.

### Input - Sectors/Stocks:

Sector/Stock Selection: Users can select which sectors to include as well as how many sectors to include in the analysis. The default sectors are major sectors of the National Stock Exchange, India. The selected sectors will be plotted as RS lines on the chart and will also appear in the table.

Color: Allows users to choose the color for each sector's RS line, making it easy to distinguish between them on the chart.

### Acknowledgement

This indicator is developed based on the concept discussed by Mr. Subhadip Nandy in Trader's Talk with Mr. Rohit Katwal.

Saral Relative StrengthRelative Strength Indicator

### Overview

The Relative Strength (RS) Indicator is a robust tool designed to measure the performance of a security relative to a benchmark or another security. Unlike traditional indicators, this RS Indicator calculates the outperformance or underperformance in percentage terms, providing a clear and concise comparison.

The equation for calculation can be found in the code itself. This equation compares how much a security's price has changed over a given period (len) relative to the change in price of a benchmark over the same period. The result is expressed as a percentage, showing whether the security has outperformed or underperformed the benchmark. A positive RS value indicates outperformance, while a negative value signals underperformance.

Basically, this indicator is an enhanced version of 'Relative Strength' indicator of 'BharatTrader' Sir with added features like automatic divergence plotting, color-coded filled area and sector names for NSE F&O securities. Default values for some of the parameters are based on discussion by Subhadip Nandy Sir in Trader's Talk with Mr. Rohit Katwal.

### Input Parameters:

Source: The price of a security used in the calculation, with the default being the 'close' price.

Comparative Symbol: Ticker ID of the comparative security, with the default set to NIFTY 50.

Period-RS: The period for calculating the RS line, with a default of 22. The RS line measures the relative performance of the security against the benchmark, helping to identify outperformance or underperformance over time.

Period-MA: The period for calculating the Simple Moving Average (SMA) overlay on the RS line, with a default of 11. The SMA provides a smoothed view of the RS line, helping to identify trends more clearly.

Lookback - Zero Line Trend: Zero Line Trend look-back period, used to determine the angle of the RS line, with a default of 5. This parameter influences the color of the Zero Line based on whether the RS line’s angle is positive or negative.

Lookback - Divergence: Divergence look-back period, with a default of 2, used to detect divergence between the price and the RS line.

Display MA Line: Controls the display of the SMA line. When enabled, the SMA line is plotted over the RS line to indicate trend strength.

Toggle RS Color on MA Crossovers: Controls the color of the RS line. If disabled, the RS line is purple. If enabled, the RS line changes color based on its position relative to the SMA: green for RS > MA, red for RS < MA.

Display Zero Line Trend: Controls the display of the Zero Line. If disabled, the Zero Line is black. If enabled, the Zero Line’s color changes to green or maroon based on the RS line’s angle over time.

Display Divergence: Controls the display of divergence dots on the RS line, indicating potential reversal points.

Display Filled Area: Controls whether the area between the Zero Line and the RS line is filled with color. The fill color changes based on the relationship of the RS line with the SMA & Zero Line as given below.

- Dark Green: RS > 0 and RS > MA, indicating strong outperformance.

- Light Green: RS > 0 and RS < MA, indicating weakening outperformance.

- Dark Red: RS < 0 and RS < MA, indicating strong underperformance.

- Light Red: RS < 0 and RS > MA, indicating weakening underperformance.

Display Sector Name: Controls the display of sector names for NSE F&O securities, helping to plot RS with sectoral indices.

### Key Features:

RS Line:

The RS line represents the relative performance of a security against a benchmark over a specified period (default 22). It helps traders identify whether the security is outperforming or underperforming the benchmark.

SMA Overlay:

A Simple Moving Average (SMA) line is plotted over the RS line, with a default period of 11. The SMA provides a smoothed trend of the RS, making it easier to identify consistent performance trends.

Trend-Sensitive Zero Line:

The Zero Line’s color adapts based on the RS line’s trend:

- Green: Positive angle of the RS line, indicating upward momentum.

- Maroon: Negative angle, indicating downward momentum.

The color can be toggled, with an option to display the Zero Line in black.

Divergence Detection:

Automatically detects and highlights divergences.

- Positive Divergence: RS line rises while the price falls, marked by blue dots.

- Negative Divergence: RS line falls while the price rises, marked by black dots.

Color-Coded Fill Area:

The area between the RS line and the Zero Line is filled with color to visually distinguish different market conditions, with Dark and Light colors providing insight into the strength of the performance:

- Dark Green: Indicates strong outperformance (RS > 0 and RS > MA), suggesting the security is showing significant strength compared to the benchmark.

- Light Green: Indicates weakening outperformance (RS > 0 and RS < MA), signaling that while the security is still outperforming, its strength is diminishing.

- Dark Red: Indicates strong underperformance (RS < 0 and RS < MA), showing the security is significantly weaker than the benchmark.

- Light Red: Indicates weakening underperformance (RS < 0 and RS > MA), suggesting the security is still underperforming but may be regaining some strength.

Sectoral Strength:

Displays sector names for NSE F&O securities, helping users to compare the RS of individual securities with their respective sectoral indices. Comparative Security can be changed easily based on this sector name. Users need not to remember sector names for individual securities.

If any security is not categorized in a specific sector, CNX500 has been considered as a default sector for NSE F&O securities. For other securities, NIFTY50 has been considered as a default sector.