MetaWorldEngineFilterLibrary3Library "MetaWorldEngineFilterLibrary3"

GetCandleStickSize(Rule, Rule)

returns size of the candle

Parameters:

Rule : 1: (float) _src_high

Rule : 2: (float) _src_low

Returns: candlestick size

GetCandleStickBodySize(Rule, Rule)

returns size of the candle body

Parameters:

Rule : 1: (float) _src_open

Rule : 2: (float) _src_close

Returns: candlestick body size

FilterLongerLowerWickCandles(Rule, Rule, Rule)

Alters Candlestick Value to Magnify Candles with Long Wicks

Parameters:

Rule : 1: (float) open

Rule : 2: (float) close

Rule : 2: (float) low

Returns: Midpoint of the candle body less the lower wick. If value returned has a large delta from midpoint of the body, then it is short wick

IsBullish(Rule, Rule)

Determine if Candle is Bullish or Bearish

Parameters:

Rule : 1: (float) open

Rule : 2: (float) close

Returns: True is Bullish

IsDoji(Rule, Rule)

Determine if Candle is a Doji

Parameters:

Rule : 1: (int) Candle Index

Rule : 2: (float) Percentage of candle size. Larger the Number the less stringent the doji criterion

Returns: True if a Doji

MACD(Rule, Rule, Rule, Rule)

Computes MACD

Parameters:

Rule : 1: (float) _src

Rule : 2: (int) _fastLength input fast ema length

Rule : 2: (int) _slowLength input slow ema length

Rule : 3: (int) _signalLength input length of signal line (sma of MACD line)

Returns: Returns MACD and Signal Line

isFastSlowCrossed(Rule, Rule)

Computes if SeriesA crosses SeriesB

Parameters:

Rule : 1: (float) Series Input

Rule : 2: (float) Series Input

Returns: if SeriesA crosses SeriesB then true else false

isReversalUpTrend(Rule, Rule)

Computes if SeriesA crosses over SeriesB to determine reversal uptrend

Parameters:

Rule : 1: (float) Series Input

Rule : 2: (float) Series Input

Returns: if SeriesA crosses over SeriesB then true else false

isReversalDownTrend(Rule, Rule)

Computes if SeriesA crosses over SeriesB to determine reversal uptrend

Parameters:

Rule : 1: (float) Series Input

Rule : 2: (float) Series Input

Returns: if SeriesA crosses over SeriesB then true else false

SSMA(Rule, Rule)

Computes smoothed SMA

Parameters:

Rule : 1: (float) source

Rule : 2: (float) sma length

Returns: a single concatenated string for evaluation

GetTimeFrame()

Get Current timeframe in minutes

Returns: an integer value in minutes

getMA(float, int, string, float)

Gets a Moving Average based on type

Parameters:

float : _src The source data

int : length The MA period

string : maType The type of MA

float : sigma / smoothness of ALMA, else NA

Returns: A moving average with the given parameters

Indicators and strategies

TradersCustomLibraryLibrary "TradersCustomLibrary"

TODO: add library description here

SelectOptimalTimeframeTrendlineSettings()

calculateShortStopLoss()

calculateLongStopLoss()

werdygerTrend()

trendLines()

stoch()

timeToString()

obvFilterThis library comes with everything you need to add an On Balance Volume (OBV) filter to your strategy.

getOnBalanceVolumeFilter(source, maType, fastMaLength, fastMaLength)

Get the fast and slow moving average for on balance volume

Parameters:

source : hook this up to an 'input.source' input

maType : Choose from EMA, SMA, RMA, or WMA

fastMaLength : int smoothing length for fast moving average

fastMaLength : int smoothing length for fast moving average int smoothing length for slow moving average

Returns: Tuple with fast obv moving average and slow obv moving average

Add this to your strategy

▾ ▾ ▾ ▾ ▾ ▾ ▾ ▾ ▾ ▾ ▾ ▾ ▾ ▾ ▾ ▾ ▾ ▾ ▾ ▾ ▾ ▾ ▾ ▾

import jordanfray/obvFilter/1 as obv

obvSource = input.source(defval=close, title="OBV Source", group="On Balance Volume Filter")

obvMaType = input.string(defval="EMA", title="OBV Smoothing Type", options = , group="On Balance Volume Filter")

fastMaLength = input.int(title = "Fast OBV MA Length", defval = 9, minval = 2, maxval = 200, group="On Balance Volume Filter")

slowMaLength = input.int(title = "Slow OBV MA Length", defval = 21, minval = 1, maxval = 200, group="On Balance Volume Filter")

= obv.getOnBalanceVolumeFilter(obvSource, obvMaType, fastMaLength, slowMaLength)

TrigLibrary "Trig"

Trigonometric functions

rt_get_angleAlpha(a, b, c, deg)

Get angle α of a right triangle, given the lengths of its sides

Parameters:

a : length of leg a (float)

b : length of leg b (float)

c : length of hypotenuse (float)

deg : flag to return angle in degrees (bool - default = false)

Returns: angle α in radians (or degrees if deg == true)

rt_get_angleAlphaFromLine(x1, y1, x2, y2, l, deg)

Get angle α of a right triangle formed by the given line

Parameters:

x1 : x coordinate 1 (int - optional, required if argument l is not specified)

y1 : y coordinate 1 (float - optional, required if argument l is not specified)

x2 : x coordinate 2 (int - optional, required if argument l is not specified)

y2 : y coordinate 2 (float - optional, required if argument l is not specified)

l : line object (line - optional, required if x1, y1, x2, and y2 agruments are not specified)

deg : flag to return angle in degrees (bool - default = false)

Returns: angle α in radians (or degrees if deg == true)

rt_get_angleBeta(a, b, c, deg)

Get angle β of a right triangle, given the lengths of its sides

Parameters:

a : length of leg a (float)

b : length of leg b (float)

c : length of hypotenuse (float)

deg : flag to return angle in degrees (bool - default = false)

Returns: angle β in radians (or degrees if deg == true)

rt_get_angleBetaFromLine(x1, y1, x2, y2, l, deg)

Get angle β of a right triangle formed by the given line

Parameters:

x1 : x coordinate 1 (int - optional, required if argument l is not specified)

y1 : y coordinate 1 (float - optional, required if argument l is not specified)

x2 : x coordinate 2 (int - optional, required if argument l is not specified)

y2 : y coordinate 2 (float - optional, required if argument l is not specified)

l : line object (line - optional, required if x1, y1, x2, and y2 agruments are not specified)

deg : flag to return angle in degrees (bool - default = false)

Returns: angle β in radians (or degrees if deg == true)

PlurexSignalLibrary "PlurexSignal"

Provides functions that wrap the built in TradingView strategy functions so you can seemlessly integrate with Plurex Signal automation.

NOTE: Be sure to set your strategy close_entries_rule="ANY" and pyramiding=20 or some other amount appropriate to your strategy in order to have multiple entries.

plurexMarket()

Build a Plurex market string from a base and quote asset symbol.

Returns: A market string that can be used in Plurex Signal messages.

tickerToPlurexMarket()

Builds Plurex market string from the syminfo

Returns: A market string that can be used in Plurex Signal messages.

simpleMessage(secret, action, marketOverride)

Builds Plurex Signal Message json to be sent to a Signal webhook

Parameters:

secret : The secret for your Signal on plurex

action : The action of the message. One of .

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

Returns: A json string message that can be used in alerts to send messages to Plurex.

long(secret, marketOverride, qty)

Open a new long entry. Wraps strategy function and sends plurex message as an alert.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

qty : Corresponds to strategy.entry qty

short(secret, marketOverride, qty)

Open a new short entry. Wraps strategy function and sends plurex message as an alert.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

qty : Corresponds to strategy.entry qty

closeAll(secret, marketOverride)

Close all positions. Wraps strategy function and sends plurex message as an alert.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

closeLongs(secret, marketOverride)

Close all longs. Wraps strategy function and sends plurex message as an alert.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

closeShorts(secret, marketOverride)

Close all shorts. Wraps strategy function and sends plurex message as an alert.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

closeLastLong(secret, marketOverride)

Close last long entry. Wraps strategy function and sends plurex message as an alert.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

closeFirstLong(secret, marketOverride)

Close first long entry. Wraps strategy function and sends plurex message as an alert.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

closeLastShort(secret, marketOverride)

Close last short entry. Wraps strategy function and sends plurex message as an alert.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

closeFirstShort(secret, marketOverride)

Close first short entry. Wraps strategy function and sends plurex message as an alert.

Parameters:

secret : The secret for your Signal on plurex

marketOverride : Optional, defaults to the syminfo for the ticker. Use the `plurexMarket` function to build your own.

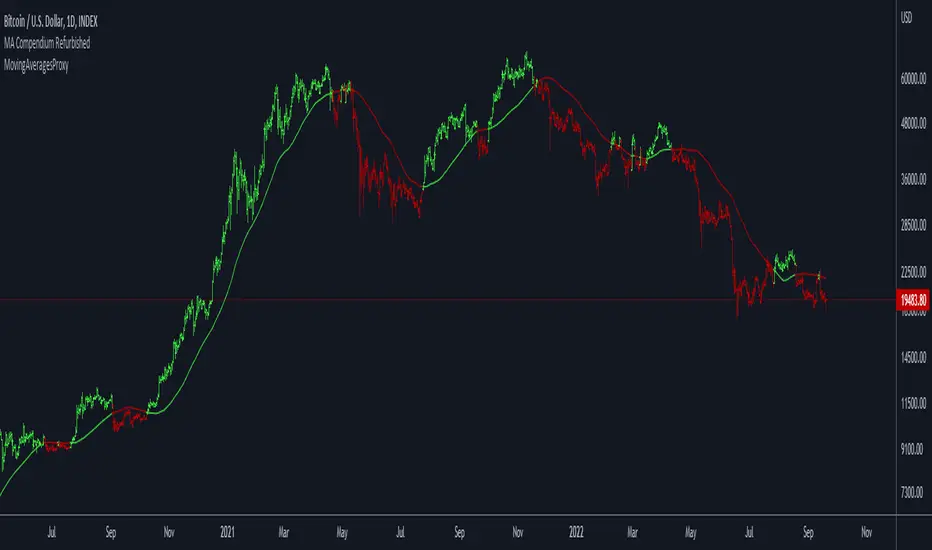

Moving Averages ProxyLibrary "MovingAveragesProxy"

Moving Averages Proxy - Library of all moving averages spread out in different libraries

rvwap(_src, fixedTfInput, minsInput, hoursInput, daysInput, minBarsInput)

Calculates the Rolling VWAP (customized VWAP developed by the team of TradingView)

Parameters:

_src : (float) Source. Default: close

fixedTfInput : (bool) Use a fixed time period. Default: false

minsInput : (int) Minutes. Default: 0

hoursInput : (int) Hours. Default: 0

daysInput : (int) Days. Default: 1

minBarsInput : (int) Bars. Default: 10

Returns: (float) Rolling VWAP

correlationMa(src, len, factor)

Correlation Moving Average

Parameters:

src : (float) Source. Default: close

len : (int) Length

factor : (float) Factor. Default: 1.7

Returns: (float) Correlation Moving Average

regma(src, len, lambda)

Regularized Exponential Moving Average

Parameters:

src : (float) Source. Default: close

len : (int) Length

lambda : (float) Lambda. Default: 0.5

Returns: (float) Regularized Exponential Moving Average

repma(src, len)

Repulsion Moving Average

Parameters:

src : (float) Source. Default: close

len : (int) Length

Returns: (float) Repulsion Moving Average

epma(src, length, offset)

End Point Moving Average

Parameters:

src : (float) Source. Default: close

length : (int) Length

offset : (float) Offset. Default: 4

Returns: (float) End Point Moving Average

lc_lsma(src, length)

1LC-LSMA (1 line code lsma with 3 functions)

Parameters:

src : (float) Source. Default: close

length : (int) Length

Returns: (float) 1LC-LSMA Moving Average

aarma(src, length)

Adaptive Autonomous Recursive Moving Average

Parameters:

src : (float) Source. Default: close

length : (int) Length

Returns: (float) Adaptive Autonomous Recursive Moving Average

alsma(src, length)

Adaptive Least Squares

Parameters:

src : (float) Source. Default: close

length : (int) Length

Returns: (float) Adaptive Least Squares

ahma(src, length)

Ahrens Moving Average

Parameters:

src : (float) Source. Default: close

length : (int) Length

Returns: (float) Ahrens Moving Average

adema(src)

Ahrens Moving Average

Parameters:

src : (float) Source. Default: close

Returns: (float) Moving Average

autol(src, lenDev)

Auto-Line

Parameters:

src : (float) Source. Default: close

lenDev : (int) Length for standard deviation

Returns: (float) Auto-Line

fibowma(src, length)

Fibonacci Weighted Moving Average

Parameters:

src : (float) Source. Default: close

length : (int) Length

Returns: (float) Moving Average

fisherlsma(src, length)

Fisher Least Squares Moving Average

Parameters:

src : (float) Source. Default: close

length : (int) Length

Returns: (float) Moving Average

leoma(src, length)

Leo Moving Average

Parameters:

src : (float) Source. Default: close

length : (int) Length

Returns: (float) Moving Average

linwma(src, period, weight)

Linear Weighted Moving Average

Parameters:

src : (float) Source. Default: close

period : (int) Length

weight : (int) Weight

Returns: (float) Moving Average

mcma(src, length)

McNicholl Moving Average

Parameters:

src : (float) Source. Default: close

length : (int) Length

Returns: (float) Moving Average

srwma(src, length)

Square Root Weighted Moving Average

Parameters:

src : (float) Source. Default: close

length : (int) Length

Returns: (float) Moving Average

EDSMA(src, len)

Ehlers Dynamic Smoothed Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: EDSMA smoothing.

dema(x, t)

Double Exponential Moving Average.

Parameters:

x : Series to use ('close' is used if no argument is supplied).

t : Lookback length to use.

Returns: DEMA smoothing.

tema(src, len)

Triple Exponential Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: TEMA smoothing.

smma(src, len)

Smoothed Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: SMMA smoothing.

hullma(src, len)

Hull Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: Hull smoothing.

frama(x, t)

Fractal Reactive Moving Average.

Parameters:

x : Series to use ('close' is used if no argument is supplied).

t : Lookback length to use.

Returns: FRAMA smoothing.

kama(x, t)

Kaufman's Adaptive Moving Average.

Parameters:

x : Series to use ('close' is used if no argument is supplied).

t : Lookback length to use.

Returns: KAMA smoothing.

vama(src, len)

Volatility Adjusted Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: VAMA smoothing.

donchian(len)

Donchian Calculation.

Parameters:

len : Lookback length to use.

Returns: Average of the highest price and the lowest price for the specified look-back period.

Jurik(src, len)

Jurik Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: JMA smoothing.

xema(src, len)

Optimized Exponential Moving Average.

Parameters:

src : Series to use ('close' is used if no argument is supplied).

len : Lookback length to use.

Returns: XEMA smoothing.

ehma(src, len)

EHMA - Exponential Hull Moving Average

Parameters:

src : Source

len : Period

Returns: Exponential Hull Moving Average (EHMA)

covwema(src, len)

Coefficient of Variation Weighted Exponential Moving Average (COVWEMA)

Parameters:

src : Source

len : Period

Returns: Coefficient of Variation Weighted Exponential Moving Average (COVWEMA)

covwma(src, len)

Coefficient of Variation Weighted Moving Average (COVWMA)

Parameters:

src : Source

len : Period

Returns: Coefficient of Variation Weighted Moving Average (COVWMA)

eframa(src, len, FC, SC)

Ehlrs Modified Fractal Adaptive Moving Average (EFRAMA)

Parameters:

src : Source

len : Period

FC : Lower Shift Limit for Ehlrs Modified Fractal Adaptive Moving Average

SC : Upper Shift Limit for Ehlrs Modified Fractal Adaptive Moving Average

Returns: Ehlrs Modified Fractal Adaptive Moving Average (EFRAMA)

etma(src, len)

Exponential Triangular Moving Average (ETMA)

Parameters:

src : Source

len : Period

Returns: Exponential Triangular Moving Average (ETMA)

rma(src, len)

RMA - RSI Moving average

Parameters:

src : Source

len : Period

Returns: RSI Moving average (RMA)

thma(src, len)

THMA - Triple Hull Moving Average

Parameters:

src : Source

len : Period

Returns: Triple Hull Moving Average (THMA)

vidya(src, len)

Variable Index Dynamic Average (VIDYA)

Parameters:

src : Source

len : Period

Returns: Variable Index Dynamic Average (VIDYA)

zsma(src, len)

Zero-Lag Simple Moving Average (ZSMA)

Parameters:

src : Source

len : Period

Returns: Zero-Lag Simple Moving Average (ZSMA)

zema(src, len)

Zero-Lag Exponential Moving Average (ZEMA)

Parameters:

src : Source

len : Period

Returns: Zero-Lag Exponential Moving Average (ZEMA)

evwma(src, len)

EVWMA - Elastic Volume Weighted Moving Average

Parameters:

src : Source

len : Period

Returns: Elastic Volume Weighted Moving Average (EVWMA)

tt3(src, len, a1_t3)

Tillson T3

Parameters:

src : Source

len : Period

a1_t3 : Tillson T3 Volume Factor

Returns: Tillson T3

gma(src, len)

GMA - Geometric Moving Average

Parameters:

src : Source

len : Period

Returns: Geometric Moving Average (GMA)

wwma(src, len)

WWMA - Welles Wilder Moving Average

Parameters:

src : Source

len : Period

Returns: Welles Wilder Moving Average (WWMA)

cma(src, len)

Corrective Moving average (CMA)

Parameters:

src : Source

len : Period

Returns: Corrective Moving average (CMA)

edma(src, len)

Exponentially Deviating Moving Average (MZ EDMA)

Parameters:

src : Source

len : Period

Returns: Exponentially Deviating Moving Average (MZ EDMA)

rema(src, len)

Range EMA (REMA)

Parameters:

src : Source

len : Period

Returns: Range EMA (REMA)

sw_ma(src, len)

Sine-Weighted Moving Average (SW-MA)

Parameters:

src : Source

len : Period

Returns: Sine-Weighted Moving Average (SW-MA)

mama(src, len)

MAMA - MESA Adaptive Moving Average

Parameters:

src : Source

len : Period

Returns: MESA Adaptive Moving Average (MAMA)

fama(src, len)

FAMA - Following Adaptive Moving Average

Parameters:

src : Source

len : Period

Returns: Following Adaptive Moving Average (FAMA)

hkama(src, len)

HKAMA - Hilbert based Kaufman's Adaptive Moving Average

Parameters:

src : Source

len : Period

Returns: Hilbert based Kaufman's Adaptive Moving Average (HKAMA)

getMovingAverage(type, src, len, lsmaOffset, inputAlmaOffset, inputAlmaSigma, FC, SC, a1_t3, fixedTfInput, daysInput, hoursInput, minsInput, minBarsInput, lambda, volumeWeighted, gamma_aarma, smooth, linweight, volatility_lookback, jurik_phase, jurik_power)

Abstract proxy function that invokes the calculation of a moving average according to type

Parameters:

type : (string) Type of moving average

src : (float) Source of series (close, high, low, etc.)

len : (int) Period of loopback to calculate the average

lsmaOffset : (int) Offset for Least Squares MA

inputAlmaOffset : (float) Offset for ALMA

inputAlmaSigma : (float) Sigma for ALMA

FC : (int) Lower Shift Limit for Ehlrs Modified Fractal Adaptive Moving Average

SC : (int) Upper Shift Limit for Ehlrs Modified Fractal Adaptive Moving Average

a1_t3 : (float) Tillson T3 Volume Factor

fixedTfInput : (bool) Use a fixed time period in Rolling VWAP

daysInput : (int) Days in Rolling VWAP

hoursInput : (int) Hours in Rolling VWAP

minsInput : (int) Minutrs in Rolling VWAP

minBarsInput : (int) Bars in Rolling VWAP

lambda : (float) Regularization Constant in Regularized EMA

volumeWeighted : (bool) Apply volume weighted calculation in selected moving average

gamma_aarma : (float) Gamma for Adaptive Autonomous Recursive Moving Average

smooth : (float) Smooth for Adaptive Least Squares

linweight : (float) Weight for Volume Weighted Moving Average

volatility_lookback : (int) Loopback for Volatility Adjusted Moving Average

jurik_phase : (int) Phase for Jurik Moving Average

jurik_power : (int) Power for Jurik Moving Average

Returns: (float) Moving average

TALibrary "TA"

General technical analysis functions

div_bull(pS, iS, cp_length_after, cp_length_before, pivot_length, lookback, no_broken, pW, iW, hidW, regW)

Test for bullish divergence

Parameters:

pS : Price series (float)

iS : Indicator series (float)

cp_length_after : Bars after current (divergent) pivot low to be considered a valid pivot (optional int)

cp_length_before : Bars before current (divergent) pivot low to be considered a valid pivot (optional int)

pivot_length : Bars before and after prior pivot low to be considered valid pivot (optional int)

lookback : Bars back to search for prior pivot low (optional int)

no_broken : Flag to only consider divergence valid if the pivot-to-pivot trendline is unbroken (optional bool)

pW : Weight of change in price, used in degree of divergence calculation (optional float)

iW : Weight of change in indicator, used in degree of divergence calculation (optional float)

hidW : Weight of hidden divergence, used in degree of divergence calculation (optional float)

regW : Weight of regular divergence, used in degree of divergence calculation (optional float)

Returns:

flag = true if divergence exists (bool)

degree = degree (strength) of divergence (float)

type = 1 = regular, 2 = hidden (int)

lx1 = x coordinate 1 (int)

ly1 = y coordinate 1 (float)

lx2 = x coordinate 2 (int)

ly2 = y coordinate 2 (float)

div_bear(pS, iS, cp_length_after, cp_length_before, pivot_length, lookback, no_broken, pW, iW, hidW, regW)

Test for bearish divergence

Parameters:

pS : Price series (float)

iS : Indicator series (float)

cp_length_after : Bars after current (divergent) pivot high to be considered a valid pivot (optional int)

cp_length_before : Bars before current (divergent) pivot highto be considered a valid pivot (optional int)

pivot_length : Bars before and after prior pivot high to be considered valid pivot (optional int)

lookback : Bars back to search for prior pivot high (optional int)

no_broken : Flag to only consider divergence valid if the pivot-to-pivot trendline is unbroken (optional bool)

pW : Weight of change in price, used in degree of divergence calculation (optional float)

iW : Weight of change in indicator, used in degree of divergence calculation (optional float)

hidW : Weight of hidden divergence, used in degree of divergence calculation (optional float)

regW : Weight of regular divergence, used in degree of divergence calculation (optional float)

Returns:

flag = true if divergence exists (bool)

degree = degree (strength) of divergence (float)

type = 1 = regular, 2 = hidden (int)

lx1 = x coordinate 1 (int)

ly1 = y coordinate 1 (float)

lx2 = x coordinate 2 (int)

ly2 = y coordinate 2 (float)

AlgebraLibrary "Algebra"

Algebra functions.

line_fromXy(x1, y1, x2, y2)

Get line slope and y-intercept from coordinates

Parameters:

x1 : x coordinate 1 (int - bar index)

y1 : y coordinate 1 (float - price/value)

x2 : x coordinate 2 (int - bar index)

y2 : y coordinate 2 (float - price/value)

Returns: of line

line_getPrice(x, slope, yInt)

Get line slope and y-intercept from coordinates

Parameters:

x : x coordinate to solve for y (int - bar index)

slope : slope of line (float)

yInt : y-intercept of line (float)

Returns: y (price/value)

ConsoleLibrary "Console"

█ OVERVIEW

An easy way to output messages to a console like table using a a simple "print" function that can be called from anywhere in your code including functions.

█ Supports:

- Scrollable console messages

- Customisable number of displayed messages

- More than one "console" for different types of output if required

- The ability to choose which message to start viewing from (useful if the message list is long)

- The ability to place the console table at different positions on the chart to mitigate against

overwriting an existing table.

█ Limitations:

The "scrollbar" handle is actually a modified time widget handle. As the handle is grabbed and moved left or right across the chart bars, this script calculates the offset of the bar being pointed to from the last bar in the chart and uses that as the console message offset. However, It isn't possible to position this on the last chart bar with code.

So there are two solutions:

1) Manually change timestamp of the variable scrollStart to the current time (roughly)

eg. scrollStart = "25 Dec 2022 14:30 +0000"

2) Use a higher timeframe (Weeks or Months) and visually find the scroll bar. If it is to the right of the chart bars the console output will read NaN. Grab the handle and move it left and it will snap to the last chart candle position. If it is to the left then find it and move it to the right as needed.

█ Notes On Usage

- Import the library as console (the call will be console.print(...) )

- Assign a console variable name and call the console.initialise function

eg. var con1=console.initialise()

- Use the console.print() function to print a message or messages

This takes two parameters:

_consoleName :this is the console name you are printing to

_message: this is the message that you want to display. It is a string and can be built in the normal way using any pinescript string functions like str.tostring() etc

- Use the console.display function to display the messages.

To work as intended this display function should be placed at the last line with the following code

if i_showMessages

....if i_displayTable == "con1"

........display(con1, i_lineOffset, i_rowsToDisplay, i_gotoMsg, posn)

(More "consoles" can be written to and the example code provided with the library shows this in more detail. Also, the indents don't show in these notes)

Lastly, placement of a console.print() without a qualifying "if" statement will occur for every bar. This may be desired. If not then use under an if statement (example in the supplied code).

Happy debugging :)

-----------------------------------------------------------------------------------------------------------

initialise()

initialise: creates the message array

Parameters:

none :

Returns: message array: this is assigned to the "console" identifier

print(_consoleName, _message)

used to output the desired text string to the console

Parameters:

_consoleName : : the message array

_message : : the console message

Returns: none

display(_consoleName, _lineOffset, _rowsToDisplay, _gotoMsg, _posn)

display: placed in the last section of code. Displays the console messages

Parameters:

_consoleName : : the message array

_lineOffset : : the setting of the scroll bar (time widget)

_rowsToDisplay : : how many rows to show in the console table

_gotoMsg : : which message to display from (default is 0)

_posn : : where the console table will be displayed

Returns: none

KlintLibraryLibrary "KlintLibrary"

GetDecimals()

this is my library, for my own use

thanks for reading

UtilitiesLibrary "Utilities"

General utilities

print_series(s, skip_na, position, show_index, from_index, to_index)

Print series values

Parameters:

s : Series (string)

skip_na : Flag to skip na values (optional bool, dft = false)

position : Position to print the Table (optional string, dft = position.bottom_center)

show_index : Flag to show series indices (optional bool, dft = true)

from_index : First index to print (optional int, dft = 0)

to_index : Last index to print (optional int, dft = last_bar_index)

Returns: Table object, if series was printed

print(v, position, at_index)

Print value

Parameters:

v : Value (string)

position : Position to print the Table (optional string, dft = position.bottom_center)

at_index : Index at which to print (optional int, dft = last_bar_index)

Returns: Table object, if value was printed

lower_tf█ OVERVIEW

This library is a Pine programmer’s tool containing functions to help those who use the request.security_lower_tf() function. Its `ltf()` function helps translate user inputs into a lower timeframe string usable with request.security_lower_tf() . Another function, `ltfStats()`, accumulates statistics on processed chart bars and intrabars.

█ CONCEPTS

Chart bars

Chart bars , as referred to in our publications, are bars that occur at the current chart timeframe, as opposed to those that occur at a timeframe that is higher or lower than that of the chart view.

Intrabars

Intrabars are chart bars at a lower timeframe than the chart's. Each 1H chart bar of a 24x7 market will, for example, usually contain 60 intrabars at the LTF of 1min, provided there was market activity during each minute of the hour. Mining information from intrabars can be useful in that it offers traders visibility on the activity inside a chart bar.

Lower timeframes (LTFs)

A lower timeframe is a timeframe that is smaller than the chart's timeframe. This framework exemplifies how authors can determine which LTF to use by examining the chart's timeframe. The LTF determines how many intrabars are examined for each chart bar; the lower the timeframe, the more intrabars are analyzed.

Intrabar precision

The precision of calculations increases with the number of intrabars analyzed for each chart bar. As there is a 100K limit to the number of intrabars that can be analyzed by a script, a trade-off occurs between the number of intrabars analyzed per chart bar and the chart bars for which calculations are possible.

█ `ltf()`

This function returns a timeframe string usable with request.security_lower_tf() . It calculates the returned timeframe by taking into account a user selection between eight different calculation modes and the chart's timeframe. You send it the user's selection, along with the text corresponding to the eight choices from which the user has chosen, and the function returns a corresponding LTF string.

Because the function processes strings and doesn't require recalculation on each bar, using var to declare the variable to which its result is assigned will execute the function only once on bar zero and speed up your script:

var string ltfString = ltf(ltfModeInput, LTF1, LTF2, LTF3, LTF4, LTF5, LTF6, LTF7, LTF8)

The eight choices users can select from are of two types: the first four allow a selection from the desired amount of chart bars to be covered, the last four are choices of a fixed number of intrabars to be analyzed per chart bar. Our example code shows how to structure your input call and then make the call to `ltf()`. By changing the text associated with the `LTF1` to `LTF8` constants, you can tailor it to your preferences while preserving the functionality of `ltf()` because you will be sending those string constants as the function's arguments so it can determine the user's selection. The association between each `LTFx` constant and its calculation mode is fixed, so the order of the arguments is important when you call `ltf()`.

These are the first four modes and the `LTFx` constants corresponding to each:

Covering most chart bars (least precise) — LTF1

Covers all chart bars. This is accomplished by dividing the current timeframe in seconds by 4 and converting that number back to a string in timeframe.period format using secondsToTfString() . Due to the fact that, on premium subscriptions, the typical historical bar count is between 20-25k bars, dividing the timeframe by 4 ensures the highest level of intrabar precision possible while achieving complete coverage for the entire dataset with the maximum allowed 100K intrabars.

Covering some chart bars (less precise) — LTF2

Covering less chart bars (more precise) — LTF3

These levels offer a stepped LTF in relation to the chart timeframe with slightly more, or slightly less precision. The stepped lower timeframe tiers are calculated from the chart timeframe as follows:

Chart Timeframe Lower Timeframe

Less Precise More Precise

< 1hr 1min 1min

< 1D 15min 1min

< 1W 2hr 30min

> 1W 1D 60min

Covering the least chart bars (most precise) — LTF4

Analyzes the maximum quantity of intrabars possible by using the 1min LTF, which also allows the least amount of chart bars to be covered.

The last four modes allow the user to specify a fixed number of intrabars to analyze per chart bar. Users can choose from 12, 24, 50 or 100 intrabars, respectively corresponding to the `LTF5`, `LTF6`, `LTF7` and `LTF8` constants. The value is a target; the function will do its best to come up with a LTF producing the required number of intrabars. Because of considerations such as the length of a ticker's session, rounding of the LTF to the closest allowable timeframe, or the lowest allowable timeframe of 1min intrabars, it is often impossible for the function to find a LTF producing the exact number of intrabars. Requesting 100 intrabars on a 60min chart, for example, can only produce 60 1min intrabars. Higher chart timeframes, tickers with high liquidity or 24x7 markets will produce optimal results.

█ `ltfStats()`

`ltfStats()` returns statistics that will be useful to programmers using intrabar inspection. By analyzing the arrays returned by request.security_lower_tf() in can determine:

• intrabarsInChartBar : The number of intrabars analyzed for each chart bar.

• chartBarsCovered : The number of chart bars where intrabar information is available.

• avgIntrabars : The average number of intrabars analyzed per chart bar. Events like holidays, market activity, or reduced hours sessions can cause the number of intrabars to vary, bar to bar.

The function must be called on each bar to produce reliable results.

█ DEMONSTRATION CODE

Our example code shows how to provide users with an input from which they can select a LTF calculation mode. If you use this library's functions, feel free to reuse our input setup code, including the tooltip providing users with explanations on how it works for them.

We make a simple call to request.security_lower_tf() to fetch the close values of intrabars, but we do not use those values. We simply send the returned array to `ltfStats()` and then plot in the indicator's pane the number of intrabars examined on each bar and its average. We also display an information box showing the user's selection of the LTF calculation mode, the resulting LTF calculated by `ltf()` and some statistics.

█ NOTES

• As in several of our recent publications, this script uses secondsToTfString() to produce a timeframe string in timeframe.period format from a timeframe expressed in seconds.

• The script utilizes display.data_window and display.status_line to restrict the display of certain plots.

These new built-ins allow coders to fine-tune where a script’s plot values are displayed.

• We implement a new recommended best practice for tables which works faster and reduces memory consumption.

Using this new method, tables are declared only once with var , as usual. Then, on bar zero only, we use table.cell() calls to populate the table.

Finally, table.set_*() functions are used to update attributes of table cells on the last bar of the dataset.

This greatly reduces the resources required to render tables. We encourage all Pine Script™ programmers to do the same.

Look first. Then leap.

█ FUNCTIONS

The library contains the following functions:

ltf(userSelection, choice1, choice2, choice3, choice4, choice5, choice6, choice7, choice8)

Selects a LTF from the chart's TF, depending on the `userSelection` input string.

Parameters:

userSelection : (simple string) User-selected input string which must be one of the `choicex` arguments.

choice1 : (simple string) Input selection corresponding to "Least precise, covering most chart bars".

choice2 : (simple string) Input selection corresponding to "Less precise, covering some chart bars".

choice3 : (simple string) Input selection corresponding to "More precise, covering less chart bars".

choice4 : (simple string) Input selection corresponding to "Most precise, 1min intrabars".

choice5 : (simple string) Input selection corresponding to "~12 intrabars per chart bar".

choice6 : (simple string) Input selection corresponding to "~24 intrabars per chart bar".

choice7 : (simple string) Input selection corresponding to "~50 intrabars per chart bar".

choice8 : (simple string) Input selection corresponding to "~100 intrabars per chart bar".

Returns: (simple string) A timeframe string to be used with `request.security_lower_tf()`.

ltfStats()

Returns statistics about analyzed intrabars and chart bars covered by calls to `request.security_lower_tf()`.

Parameters:

intrabarValues : (float [ ]) The ID of a float array containing values fetched by a call to `request.security_lower_tf()`.

Returns: A 3-element tuple: [ (series int) intrabarsInChartBar, (series int) chartBarsCovered, (series float) avgIntrabars ].

HSV and HSL gradient Tools ( Built-in Drop-in replacement )Library "hsvColor"

HSV and HSL Gradient Tool Alternatives and helpers. Demo'd is built-in in the middle with HSL/HSV gradients on top/bottom

TODO: Solve for #000000 issue

rgbhsv(_col)

RGB Color to HSV Values

Parameters:

_col : Color input (#abc012 or color.name or color.rgb(0,0,0,0))

Returns: values

rgbhsv(_r, _g, _b, _t)

RGB Color to HSV Values

Parameters:

_r : Red 0 - 255

_g : Green 0 - 255

_b : Blue 0 - 255

_t : Transp 0 - 100

Returns: values

hsv(_h, _s, _v, _a)

HSV colors, Auto fix if past boundaries

Parameters:

_h : Hue Input (-360 - 360) or further

_s : Saturation 0.- 1.

_v : Value 0.- 1.

_a : Alpha 0.- 1.

Returns: Color output

hue(_col)

returns 0-359 hue on color wheel

Parameters:

_col :

Returns: 360 degree hue value

hsv_gradient(signal, _startVal, _endVal, _startCol, _endCol)

Color Gradient Replacement Function for HSV calculated Gradents

Parameters:

signal : Control signal

_startVal : start color limit

_endVal : end color limit

_startCol : start color

_endCol : end color

Returns: HSV calculated gradient

hsl_gradient(signal, _startVal, _endVal, _startCol, _endCol)

Color Gradient Replacement Function for HSV calculated Gradents

Parameters:

signal : Control signal

_startVal : start color limit

_endVal : end color limit

_startCol : start color

_endCol : end color

Returns: HSV calculated gradient

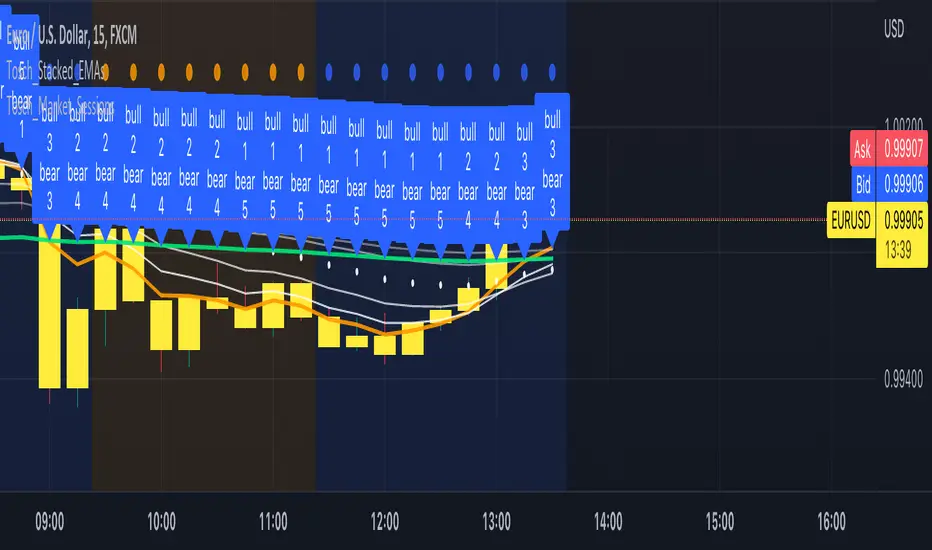

Tosch Stacked EMAs (Fibonacci)Library "Tosch_Stacked_EMAs (Fibonacci)"

stacked()

Returns true if all EMAs are stacked, either way.

bullish()

Returns true if the EMAs are stacked bullish, false otherwise

emas()

Returns the EMA values for lengths 5, 8, 13, 21, 34, 55, 89

Tosch Market Sessions (US/GB/JP)Library "Tosch Market Sessions"

Returns if the NYSE, London SE, Tokyo SE are open

@function Returns if the NYSE (US), London SE (GB), Tokyo SE (JP) are open

@returns

bus, bgb, bjp - bool: true if the corresponding exchange is open

count - int: count of how many exchanges are open at the moment

ccolor - color: color that indicates the number of open exchanges

0 => color.black

1 => color.blue

2 => color.orange

3 => color.white

Chaikin Money Flow - LibraryLibrary "Chaikin Money Flow"

cmf()

Developed by Marc Chaikin, Chaikin Money Flow measures the amount of Money Flow Volume over a specific period.

Money Flow Volume forms the basis for the Accumulation Distribution Line. Instead of a cumulative total of

Money Flow Volume, Chaikin Money Flow simply sums Money Flow Volume for a specific look-back period, typically

20 or 21 days. The resulting indicator fluctuates above/below the zero line just like an oscillator. Chartists

weigh the balance of buying or selling pressure with the absolute level of Chaikin Money Flow. Chartists can

also look for crosses above or below the zero line to identify changes on money flow.

The Accumulation Distribution Line was developed by Marc Chaikin to measure the cumulative flow of money into and

out of an index or security. The Accumulation/Distribution Line can be compared to the OBV (On Balance Volume),

which adds or subtracts volume depending on the closing price. Marc Chaikin chose a different approach, instead

of relying on the closing price, he used CLV (Close Location Value).

Library: ArrayLibrary "xarray"

Additional functions for array.

remove_duplicates(array_in)

Remove duplicates in array.

Parameters:

array_in : (int /float /string ) Array contains duplicates.

Returns: Array without duplicates.

// Example: int

import tuele99/xarray/1 as xarray

c = xarray.remove_duplicates(array.from(1, 4, 2, 1, 2))

plot(array.size(c))

plot(array.get(c, 0))

plot(array.get(c, 1))

// Example: float

import tuele99/xarray/1 as xarray

c = xarray.remove_duplicates(array.from(1.0, 4.0, 2.0, 1.0, 2.0))

plot(array.size(c))

plot(array.get(c, 0))

plot(array.get(c, 1))

// Example: string

import tuele99/xarray/1 as xarray

c = xarray.remove_duplicates(array.from("green", "red", "green", "red", "green"))

plot(array.size(c)) // value = 2

label0 = label.new(x=last_bar_index, y=0, yloc=yloc.belowbar, text=array.get(c, 0), style=label.style_label_left, color=color.new(color.black, 100), textcolor=color.green) // below text = "green"

label1 = label.new(x=last_bar_index, y=0, yloc=yloc.abovebar, text=array.get(c, 1), style=label.style_label_left, color=color.new(color.black, 100), textcolor=color.red) // above text = "red"

Demand IndexLibrary "DemandIndex"

di()

The Demand Index is a complex technical indicator that uses price and volume to assess buying and selling pressure affecting a security.

James Sibbet established six rules for using Demand Index when the technical indicator was originally published. While traders may use variations of these rules, they serve as a great baseline for using the indicator in practice.

The six rules are as follows:

A divergence between the Demand Index and price is a bearish indication.

Prices often rally to new highs following an extreme peak in the Demand Index.

Higher prices with a low Demand Index often indicate a top in the market.

The Demand Index moving through the zero line suggests a change in trend.

The Demand Index remaining near the zero line indicates weak price movement that won’t last long.

A long-term divergence between the Demand Index and price predicts a major top or bottom.

Traders should use the Demand Index in conjunction with other technical indicators and chart patterns to maximize their odds of success.

myAutoviewAlertsLibrary "myAutoviewAlerts"

My Alerts Functions - To use with autoview

@returns - These functions returns a string to use in alerts to send commands to autoview. You can open an order, place a stop or take order, close an opened order or a opened position, or open a hedge position.

@param a = String - Account Identification

@param e = String - Exchange

@param s = String - Symbol

@param b = String - Book Side

@param q = Float - Quantity

@param fp = Float - Fixed Price

@param delay = Integer - In Seconds

@param i = Integer - Account Index (to multiple accounts allerts)

@param base = String - Base Currency (bitmex) - "Tether" or "Bitcoin"

@param fsl = Float - Stop Loss Limit Price

@param c = String - Close -> "order" or "position"

@param ro = Bool - Reduce Only

@param sl = Bool - Stop Loss -> bitfinex

@param t = String - Type -> "market" or "limit"

@function f_order => Open Orders

@function f_stop => Set Stop Loss Order

@function f_take => Set Take Order

@function f_closeOrder => Close Open Orders

@function f_closePosition => Close Open Positions

@function f_hedge => To Open a Hedge Position (short 100% of balance)

AllTimeHighLowLibrary "AllTimeHighLow"

Provides functions calculating the all-time high/low of values.

hi(val)

Calculates the all-time high of a series.

Parameters:

val : Series to use (`high` is used if no argument is supplied).

Returns: The all-time high for the series.

lo(val)

Calculates the all-time low of a series.

Parameters:

val : Series to use (`low` is used if no argument is supplied).

Returns: The all-time low for the series.

L_BetaLibrary "L_Beta"

TODO: add library description here

length()

beta()

simple_beta()

index_selector()

L_Index_4khansoloLibrary "L_Index_4khansolo"

countrySelect()

colorPositron()

indexName()

indexRSI()

maRSI()

colorRSIfull()

rsiColor()

rsiFillColor()

rsiCompartments()

fiatIndexer()

colorMACD()

indexMACD()

colour()