JsonAlertJsonAlert Library – Convert TradingView Alerts to JSON for Server Processing! 📡

🚀 The JsonAlert library makes it easy to send TradingView alerts as structured JSON to your server, allowing seamless integration with automated trading systems, databases, or webhook-based services.

📌 Features:

✅ Converts TradingView alert data into JSON format

✅ Supports custom key-value pairs for flexibility

✅ Allows frequency control (once per bar, once per bar close, every update)

✅ Easy to integrate with server-side PHP or other languages

Note that you have to pass one string array for keys and one string array for values , also you should pass alert frequency .

📖 Example Usage in Pine Script:

//@version=6

indicator("My script" , overlay = true)

import Penhan/JsonAlert/1 as alrt

if high > low

var array keys = array.from("ticker", "timeframe", "pattern")

var array values = array.from( syminfo.ticker , timeframe.period , str.tostring(123.45) )

alrt.alarm (keys, values , alert.freq_once_per_bar)

📡 Json Output Example:

{"ticker": "BTCUSDT","timeframe": "1","pattern": "123.45"}

🖥️ Server-Side PHP Example:

There you can integrate JsonAlert with your server in seconds! :)

Indicators and strategies

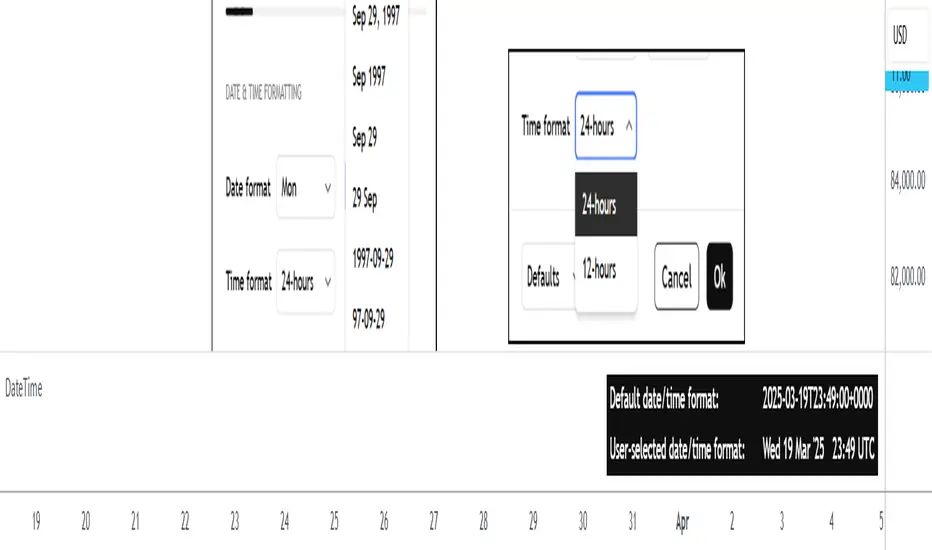

DateTimeLibrary with enums that can be used as script inputs to allow users to set their preferred date and/or time formats. The user-selected formats can be passed to the library functions (which use 𝚜𝚝𝚛.𝚏𝚘𝚛𝚖𝚊𝚝_𝚝𝚒𝚖𝚎() under the hood) to get formatted date and time strings from a UNIX time.

PREFACE

The target audience of this publication is users creating their own indicators/strategies.

Sometimes a date and/or time needs to be displayed to the user. As a Pine Coder, it is natural to focus our initial attention on the primary calculations or functions of a script, which can lead to the display format of dates and times being an afterthought. While it may not be crucial for the main use case of a script, increased customizability can help push indicators/strategies to the next level in the eyes of the user.

The purpose of this library is to provide an easy-to-use mechanism for allowing script users to choose the formats of dates and times that are displayed to them. Not only is this helpful for users from around the world who may be accustomed to different date/time formats, but it also makes it easier for the script author because it offloads the date/time formatting decision from the author to the user.

HOW TO USE

Step 1

Import the library. Replace with the latest available version number for this library.

//@version=6

indicator("Example")

import n00btraders/DateTime/ as dt

Step 2

Select a date format and/or time format enum to be used as an input.

dateFormatInput = input.enum(dt.DateFormat.FORMAT_3, "Date format")

timeFormatInput = input.enum(dt.TimeFormat.TWENTY_FOUR_HOURS, "Time hours format")

Step 3

Pass the user's selection as the `format` parameter in the formatting functions from this library. The `timestamp` & `timezone` parameters can be any value that would otherwise be used in 𝚜𝚝𝚛.𝚏𝚘𝚛𝚖𝚊𝚝_𝚝𝚒𝚖𝚎(𝚝𝚒𝚖𝚎, 𝚏𝚘𝚛𝚖𝚊𝚝, 𝚝𝚒𝚖𝚎𝚣𝚘𝚗𝚎).

string formattedDate = dt.formatDate(timestamp, dateFormatInput, timezone)

string formattedTime = dt.formatTime(timestamp, timeFormatInput, timezone)

LIMITATIONS

The library's ease-of-use comes at a few costs:

Fixed date/time formats.

Using the library's pre-defined date & time formats means that additional custom formats cannot be utilized. For example, this library does not include seconds or fractional seconds in formatted time strings. If a script's use case requires displaying the 'seconds' from a time of day, then 𝚜𝚝𝚛.𝚏𝚘𝚛𝚖𝚊𝚝_𝚝𝚒𝚖𝚎() must be used directly.

Fixed time zone offset format.

The `formatTime()` function of this library can optionally add the time zone offset at the end of the time string, but the format of the offset cannot be specified. Note: if the default format for time zone offset is not sufficient, the Timezone library can be imported directly to get the time zone offset string in a preferred format.

ADVANTAGES

There are benefits to utilizing this library instead of directly using 𝚜𝚝𝚛.𝚏𝚘𝚛𝚖𝚊𝚝_𝚝𝚒𝚖𝚎():

Easy to use from the user's perspective.

The date & time format enums provide a similar look and feel to the "Date format" and "Time hours format" options that already exist in the TradingView chart settings.

Easy to use from the author's perspective.

The exported functions from this library are modeled to behave similarly to the 𝚜𝚝𝚛.𝚏𝚘𝚛𝚖𝚊𝚝_𝚝𝚒𝚖𝚎(𝚝𝚒𝚖𝚎, 𝚏𝚘𝚛𝚖𝚊𝚝, 𝚝𝚒𝚖𝚎𝚣𝚘𝚗𝚎) built-in function from Pine Script.

Format quarter of the year.

The date formatting function from this library can display a fiscal quarter if it's included in the user-selected format. This is currently not possible with the built-in 𝚜𝚝𝚛.𝚏𝚘𝚛𝚖𝚊𝚝_𝚝𝚒𝚖𝚎().

EXPORTED ENUM TYPES

This section will list the available date/time formats that can be used as a script input. Each enum type has a detailed //@𝚏𝚞𝚗𝚌𝚝𝚒𝚘𝚗 description in the source code to help determine the best choice for your scripts.

Date Format Enums:

𝙳𝚊𝚝𝚎𝙵𝚘𝚛𝚖𝚊𝚝

𝙳𝚊𝚝𝚎𝙵𝚘𝚛𝚖𝚊𝚝𝙳𝚊𝚢𝙾𝚏𝚆𝚎𝚎𝚔𝙰𝚋𝚋𝚛

𝙳𝚊𝚝𝚎𝙵𝚘𝚛𝚖𝚊𝚝𝙳𝚊𝚢𝙾𝚏𝚆𝚎𝚎𝚔𝙵𝚞𝚕𝚕

𝙲𝚞𝚜𝚝𝚘𝚖𝙳𝚊𝚝𝚎𝙵𝚘𝚛𝚖𝚊𝚝

Supporting Date Enums:

𝙳𝚊𝚝𝚎𝙿𝚛𝚎𝚏𝚒𝚡

Time Format Enums:

𝚃𝚒𝚖𝚎𝙵𝚘𝚛𝚖𝚊𝚝

Supporting Time Enums:

𝚃𝚒𝚖𝚎𝙰𝚋𝚋𝚛𝚎𝚟𝚒𝚊𝚝𝚒𝚘𝚗

𝚃𝚒𝚖𝚎𝚂𝚎𝚙𝚊𝚛𝚊𝚝𝚘𝚛

𝚃𝚒𝚖𝚎𝙿𝚘𝚜𝚝𝚏𝚒𝚡

Note: all exported enums have custom titles for each field. This means that the supporting enums could also be exposed to the end-user as script inputs if necessary. The supporting enums are used as optional parameters in this library's formatting functions to allow further customizability.

EXPORTED FUNCTIONS

formatDate(timestamp, format, timezone, prefix, trim)

Converts a UNIX time into a date string formatted according to the selected `format`.

Parameters:

timestamp (series int) : A UNIX time.

format (series DateFormat) : A date format.

timezone (series string) : A UTC/GMT offset or IANA time zone identifier.

prefix (series DatePrefix) : Optional day of week prefix.

trim (series bool) : Optional truncation of numeric month / day.

Returns: Calendar date string using the selected format.

⸻⸻⸻⸻⸻⸻⸻⸻

Required parameters: `timestamp`, `format`.

Note: there is a version of this function for each Date Format enum type. The only difference is the type of the `format` parameter.

Tip: hover over the `formatDate()` function in the Pine Editor to display useful details:

Function description

Parameter descriptions + default values

Example function usage

formatTime(timestamp, format, timezone, trim, separator, postfix, space, offset)

Converts a UNIX time into a formatted time string using the 24-hour clock or 12-hour clock.

Parameters:

timestamp (series int) : A UNIX time.

format (series TimeFormat) : A time format.

timezone (series string) : A UTC/GMT offset or IANA time zone identifier.

trim (series TimeAbbreviation) : Optional truncation of the hour and minute portion.

separator (series TimeSeparator) : Optional time separator.

postfix (series TimePostfix) : Optional format for the AM/PM postfix.

space (series bool) : Optional space between the time and the postfix.

offset (series bool) : Optional UTC offset as a suffix.

Returns: Time of day string using the selected format.

⸻⸻⸻⸻⸻⸻⸻⸻

Required parameters: `timestamp`, `format`.

Note: the `trim`, `postfix`, and `space` optional parameters are not applicable and will be ignored when using the 24-hour clock (`format` = TimeFormat.TWENTY_FOUR_HOURS).

Tip: hover over the `formatTime()` function in the Pine Editor to display useful details:

Function description

Parameter descriptions + default values

Example function usage

Example outputs for combinations of TimeFormat.* enum values & optional parameters

NOTES

This library can be used in conjunction with the Timezone library to increase the usability of scripts that can benefit from allowing the user to input their preferred time zone.

Credits to HoanGhetti for publishing an informative Markdown resource which I referenced to create the formatted function descriptions that pop up when hovering over `formatDate()` and `formatTime()` function calls in the Pine Editor.

dataTableUtilitiesLibrary "dataTableUtilities"

generate_dataTable(dataTable_map, title, tableYpos, tableXpos, textSize, includes_multiple_maps, include_comments)

: Generates and shows a data table.

Parameters:

dataTable_map (map)

title (string) : (string): Title of the table

tableYpos (string) : (string): Vertical position of the table

tableXpos (string) : (string): Horizontal position of the table

textSize (string) : (string): Text size

includes_multiple_maps (bool)

include_comments (bool)

Returns: : None

generate_dataTable_multiple_columns(dataTable_map, title, tableYpos, tableXpos, textSize, includes_multiple_maps, total_columns)

: Generates and shows a data table.

Parameters:

dataTable_map (map)

title (string) : (string): Title of the table

tableYpos (string) : (string): Vertical position of the table

tableXpos (string) : (string): Horizontal position of the table

textSize (string) : (string): Text size

includes_multiple_maps (bool)

total_columns (int)

Returns: : None

ootaLibrary "oota"

Collection of all custom and enhanced TA indicators - Object oriented methods implementation

method tr(c, useTrueRange)

returns true range of the candle

Namespace types: Candle

Parameters:

c (Candle) : Candle object containing ohlc data

useTrueRange (bool) : Use true range for atr calculation instead of just high/low difference

method ma(maType, length, source)

returns custom moving averages

Namespace types: simple CustomSeries

Parameters:

maType (simple CustomSeries) : Custom series type

length (simple int) : Moving Average Length

source (float) : Moving Average Source

Returns: moving average for the given type and length

method atr(maType, length, useTrueRange, c)

returns ATR with custom moving average

Namespace types: simple CustomSeries

Parameters:

maType (simple CustomSeries) : Custom series type

length (simple int) : Moving Average Length

useTrueRange (bool) : Use true range for atr calculation instead of just high/low difference

c (Candle) : Candle object containing ohlc

Returns: ATR for the given moving average type and length

method atrpercent(maType, length, useTrueRange, c)

returns ATR as percentage of close price

Namespace types: simple CustomSeries

Parameters:

maType (simple CustomSeries) : Custom series type

length (simple int) : Moving Average Length

useTrueRange (bool) : Use true range for atr calculation instead of just high/low difference

c (Candle) : Candle object containing ohlc

Returns: ATR as percentage of close price for the given moving average type and length

method bb(maType, length, multiplier, sticky, c)

returns Bollinger band for custom moving average

Namespace types: simple CustomSeries

Parameters:

maType (simple CustomSeries) : Custom series type

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

c (Candle) : Candle object containing ohlc

Returns: Bollinger band with custom moving average for given source, length and multiplier

method bbw(maType, length, multiplier, sticky, c)

returns Bollinger bandwidth for custom moving average

Namespace types: simple CustomSeries

Parameters:

maType (simple CustomSeries) : Custom series type

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

sticky (simple bool) : sticky boundaries which will only change when value is outside boundary.

c (Candle) : Candle object containing ohlc

Returns: Bollinger Bandwidth for custom moving average for given source, length and multiplier

method bpercentb(maType, length, multiplier, sticky, c)

returns Bollinger Percent B for custom moving average

Namespace types: simple CustomSeries

Parameters:

maType (simple CustomSeries) : Custom series type

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

c (Candle) : Candle object containing ohlc

Returns: Bollinger Percent B for custom moving average for given source, length and multiplier

method kc(maType, length, multiplier, useTrueRange, sticky, c)

returns Keltner Channel for custom moving average

Namespace types: simple CustomSeries

Parameters:

maType (simple CustomSeries) : Custom series type

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

useTrueRange (simple bool) : - if set to false, uses high-low.

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

c (Candle) : Candle object containing ohlc

Returns: Keltner Channel for custom moving average for given souce, length and multiplier

method kcw(maType, length, multiplier, useTrueRange, sticky, c)

returns Keltner Channel Width with custom moving average

Namespace types: simple CustomSeries

Parameters:

maType (simple CustomSeries) : Custom series type

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

useTrueRange (simple bool) : - if set to false, uses high-low.

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

c (Candle) : Candle object containing ohlc

Returns: Keltner Channel Width for custom moving average

method kpercentk(maType, length, multiplier, useTrueRange, sticky, c)

returns Keltner Channel Percent K Width with custom moving average

Namespace types: simple CustomSeries

Parameters:

maType (simple CustomSeries) : Custom series type

length (simple int) : Moving Average Length

multiplier (float) : Standard Deviation multiplier

useTrueRange (simple bool) : - if set to false, uses high-low.

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

c (Candle) : Candle object containing ohlc

Returns: Keltner Percent K for given moving average, source, length and multiplier

method dc(c, length, sticky)

returns Custom Donchian Channel

Namespace types: Candle

Parameters:

c (Candle) : Candle object containing ohlc

length (simple int) : - donchian channel length

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Donchian channel

method dcw(c, length, sticky)

returns Donchian Channel Width

Namespace types: Candle

Parameters:

c (Candle) : Candle object containing ohlc

length (simple int) : - donchian channel length

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Donchian channel width

method dpercentd(c, length, sticky)

returns Donchian Channel Percent of price

Namespace types: Candle

Parameters:

c (Candle) : Candle object containing ohlc

length (simple int) : - donchian channel length

sticky (simple bool) : - sticky boundaries which will only change when value is outside boundary.

Returns: Donchian channel Percent D

method supertrend(maType, length, multiplier, useTrueRange, waitForClose, delayed, c)

supertrend Simple supertrend based on atr but also takes into consideration of custom MA Type, sources

Namespace types: simple CustomSeries

Parameters:

maType (simple CustomSeries) : Custom Series

length (simple int) : ATR Length

multiplier (simple float) : ATR Multiplier

useTrueRange (simple bool) : - if set to false, uses high-low.

waitForClose (simple bool) : : Considers source for direction change crossover if checked. Else, uses highSource and lowSource.

delayed (simple bool) : : if set to true lags supertrend atr stop based on target levels.

c (Candle) : Candle object containing ohlc

Returns: dir : Supertrend direction

supertrend : BuyStop if direction is 1 else SellStop

method oscillatorRange(seriesType, source, highlowLength, rangeLength, sticky)

oscillatorRange - returns Custom overbought/oversold areas for an oscillator input

Namespace types: simple CustomSeries

Parameters:

seriesType (simple CustomSeries) : - Custom series type

source (float) : - Osillator source such as RSI, COG etc.

highlowLength (simple int) : - length on which highlow of the oscillator is calculated

rangeLength (simple int) : - length used for calculating oversold/overbought range - usually same as oscillator length

sticky (simple bool) : - overbought, oversold levels won't change unless crossed

Returns: Dynamic overbought and oversold range for oscillator input

method oscillator(oscillatorType, length, shortLength, longLength, c)

oscillator - returns Choice of oscillator with custom overbought/oversold range

Namespace types: simple OscillatorType

Parameters:

oscillatorType (simple OscillatorType) : OscillatorType object

length (simple int) : - Oscillator length - not used for TSI

shortLength (simple int) : - shortLength only used for TSI

longLength (simple int) : - longLength only used for TSI

c (Candle) : Candle object containing ohlc

Returns: Oscillator value

method oscillatorWithRange(oscillatorType, length, shortLength, longLength, seriesType, highlowLength, sticky, c)

oscillatorWithRange - returns Choice of oscillator with custom overbought/oversold range

Namespace types: simple OscillatorType

Parameters:

oscillatorType (simple OscillatorType) : OscillatorType object

length (simple int) : - Oscillator length - not used for TSI

shortLength (simple int) : - shortLength only used for TSI

longLength (simple int) : - longLength only used for TSI

seriesType (simple CustomSeries) : - CustomSeries enum type

highlowLength (simple int) : - length on which highlow of the oscillator is calculated

sticky (simple bool) : - overbought, oversold levels won't change unless crossed

c (Candle) : Candle object containing ohlc

Returns: Oscillator value along with dynamic overbought and oversold range for oscillator input

Candle

Custom candle object

Fields:

o (series float) : open

h (series float) : high

l (series float) : low

c (series float) : close

barindex (series int) : bar_index

bartime (series int) : time

bartimeclose (series int) : time_close

v (series float) : volume

regressionUtilitiesLibrary "regressionUtilities"

get_linear_regression(bar_index_array, prices_array, stdDev_mult)

: Generates the linear regression channel for an array of values.

Parameters:

bar_index_array (array) : (array): Array with bar indexes

prices_array (array) : (array): Array with prices

stdDev_mult (float) : (float): Standard deviation multiple for the channels

Returns: : Returns x1, x2, y1_mid, y2_mid, y1_up, y2_up, y1_dn, y2_dn, m, b, R2, stdDev

get_optimal_linearRegression_channel(max_length, min_length, source, stdDev_mult, show_data_table, tableYpos, tableXpos, table_textSize, barsToRight, plot_labels, include_levels)

: Gets the best fitting linear regression using optimum length

Parameters:

max_length (int) : (int): Maximum bar length

min_length (int) : (int): Minimum bar length

source (float) : (float): Source for the regression

stdDev_mult (float) : (float): Array with prices

show_data_table (bool) : (bool): Activates and shows the data table

tableYpos (string)

tableXpos (string)

table_textSize (string)

barsToRight (int)

plot_labels (bool)

include_levels (bool)

Returns: : Returns three line objects that conform the regression channel, plus the optimal length and maximum r2

get_regressionChannel_data(max_length, min_length, source, stdDev_mult, plot_linearRegression, plot_labels, include_levels, barsToRight)

: Gets data for the linear regression channel

Parameters:

max_length (int) : (int): Maximum length for the linear regression.

min_length (int) : (int): Minimum length for the linear regression.

source (float) : (float): Source for the linear regression

stdDev_mult (float) : (float): Multiple for the standar deviations for the linear regression channel.

plot_linearRegression (bool)

plot_labels (bool)

include_levels (bool)

barsToRight (int)

Returns: : Returns a maps with the regression levels, the direction flag and the datatable map.

get_regressionChannel_data_v2(max_length, min_length, source, stdDev_mult, plot_linearRegression, plot_labels, include_levels, barsToRight)

Parameters:

max_length (int)

min_length (int)

source (float)

stdDev_mult (float)

plot_linearRegression (bool)

plot_labels (bool)

include_levels (bool)

barsToRight (int)

get_cuadratic_regression(x_array, y_array, bars_to_project, max_length)

: Gets the best fitting linear regression using optimum length

Parameters:

x_array (array) : (array): Maximum bar length

y_array (array) : (array): Minimum bar length

bars_to_project (int) : (int): Array with prices

max_length (int)

Returns: : Returns three line objects

rate_of_changeLibrary "rate_of_change"

// @description: Applies ROC algorithm to any pair of values.

// This library function is used to scale change of value (price, volume) to a percentage value, just as the ROC indicator would do. It is good practice to scale arbitrary ranges to set boundaries when you try to train statistical model.

rateOfChange(value, base, hardlimit)

This function is a helper to scale a value change to its percentage value.

Parameters:

value (float)

base (float)

hardlimit (int)

Returns: per: A float comprised between 0 and 100

real_time_candlesIntroduction

The Real-Time Candles Library provides comprehensive tools for creating, manipulating, and visualizing custom timeframe candles in Pine Script. Unlike standard indicators that only update at bar close, this library enables real-time visualization of price action and indicators within the current bar, offering traders unprecedented insight into market dynamics as they unfold.

This library addresses a fundamental limitation in traditional technical analysis: the inability to see how indicators evolve between bar closes. By implementing sophisticated real-time data processing techniques, traders can now observe indicator movements, divergences, and trend changes as they develop, potentially identifying trading opportunities much earlier than with conventional approaches.

Key Features

The library supports two primary candle generation approaches:

Chart-Time Candles: Generate real-time OHLC data for any variable (like RSI, MACD, etc.) while maintaining synchronization with chart bars.

Custom Timeframe (CTF) Candles: Create candles with custom time intervals or tick counts completely independent of the chart's native timeframe.

Both approaches support traditional candlestick and Heikin-Ashi visualization styles, with options for moving average overlays to smooth the data.

Configuration Requirements

For optimal performance with this library:

Set max_bars_back = 5000 in your script settings

When using CTF drawing functions, set max_lines_count = 500, max_boxes_count = 500, and max_labels_count = 500

These settings ensure that you will be able to draw correctly and will avoid any runtime errors.

Usage Examples

Basic Chart-Time Candle Visualization

// Create real-time candles for RSI

float rsi = ta.rsi(close, 14)

Candle rsi_candle = candle_series(rsi, CandleType.candlestick)

// Plot the candles using Pine's built-in function

plotcandle(rsi_candle.Open, rsi_candle.High, rsi_candle.Low, rsi_candle.Close,

"RSI Candles", rsi_candle.candle_color, rsi_candle.candle_color)

Multiple Access Patterns

The library provides three ways to access candle data, accommodating different programming styles:

// 1. Array-based access for collection operations

Candle candles = candle_array(source)

// 2. Object-oriented access for single entity manipulation

Candle candle = candle_series(source)

float value = candle.source(Source.HLC3)

// 3. Tuple-based access for functional programming styles

= candle_tuple(source)

Custom Timeframe Examples

// Create 20-second candles with EMA overlay

plot_ctf_candles(

source = close,

candle_type = CandleType.candlestick,

sample_type = SampleType.Time,

number_of_seconds = 20,

timezone = -5,

tied_open = true,

ema_period = 9,

enable_ema = true

)

// Create tick-based candles (new candle every 15 ticks)

plot_ctf_tick_candles(

source = close,

candle_type = CandleType.heikin_ashi,

number_of_ticks = 15,

timezone = -5,

tied_open = true

)

Advanced Usage with Custom Visualization

// Get custom timeframe candles without automatic plotting

CandleCTF my_candles = ctf_candles_array(

source = close,

candle_type = CandleType.candlestick,

sample_type = SampleType.Time,

number_of_seconds = 30

)

// Apply custom logic to the candles

float ema_values = my_candles.ctf_ema(14)

// Draw candles and EMA using time-based coordinates

my_candles.draw_ctf_candles_time()

ema_values.draw_ctf_line_time(line_color = #FF6D00)

Library Components

Data Types

Candle: Structure representing chart-time candles with OHLC, polarity, and visualization properties

CandleCTF: Extended candle structure with additional time metadata for custom timeframes

TickData: Structure for individual price updates with time deltas

Enumerations

CandleType: Specifies visualization style (candlestick or Heikin-Ashi)

Source: Defines price components for calculations (Open, High, Low, Close, HL2, etc.)

SampleType: Sets sampling method (Time-based or Tick-based)

Core Functions

get_tick(): Captures current price as a tick data point

candle_array(): Creates an array of candles from price updates

candle_series(): Provides a single candle based on latest data

candle_tuple(): Returns OHLC values as a tuple

ctf_candles_array(): Creates custom timeframe candles without rendering

Visualization Functions

source(): Extracts specific price components from candles

candle_ctf_to_float(): Converts candle data to float arrays

ctf_ema(): Calculates exponential moving averages for candle arrays

draw_ctf_candles_time(): Renders candles using time coordinates

draw_ctf_candles_index(): Renders candles using bar index coordinates

draw_ctf_line_time(): Renders lines using time coordinates

draw_ctf_line_index(): Renders lines using bar index coordinates

Technical Implementation Notes

This library leverages Pine Script's varip variables for state management, creating a sophisticated real-time data processing system. The implementation includes:

Efficient tick capturing: Samples price at every execution, maintaining temporal tracking with time deltas

Smart state management: Uses a hybrid approach with mutable updates at index 0 and historical preservation at index 1+

Temporal synchronization: Manages two time domains (chart time and custom timeframe)

The tooltip implementation provides crucial temporal context for custom timeframe visualizations, allowing users to understand exactly when each candle formed regardless of chart timeframe.

Limitations

Custom timeframe candles cannot be backtested due to Pine Script's limitations with historical tick data

Real-time visualization is only available during live chart updates

Maximum history is constrained by Pine Script's array size limits

Applications

Indicator visualization: See how RSI, MACD, or other indicators evolve in real-time

Volume analysis: Create custom volume profiles independent of chart timeframe

Scalping strategies: Identify short-term patterns with precisely defined time windows

Volatility measurement: Track price movement characteristics within bars

Custom signal generation: Create entry/exit signals based on custom timeframe patterns

Conclusion

The Real-Time Candles Library bridges the gap between traditional technical analysis (based on discrete OHLC bars) and the continuous nature of market movement. By making indicators more responsive to real-time price action, it gives traders a significant edge in timing and decision-making, particularly in fast-moving markets where waiting for bar close could mean missing important opportunities.

Whether you're building custom indicators, researching price patterns, or developing trading strategies, this library provides the foundation for sophisticated real-time analysis in Pine Script.

Implementation Details & Advanced Guide

Core Implementation Concepts

The Real-Time Candles Library implements a sophisticated event-driven architecture within Pine Script's constraints. At its heart, the library creates what's essentially a reactive programming framework handling continuous data streams.

Tick Processing System

The foundation of the library is the get_tick() function, which captures price updates as they occur:

export get_tick(series float source = close, series float na_replace = na)=>

varip float price = na

varip int series_index = -1

varip int old_time = 0

varip int new_time = na

varip float time_delta = 0

// ...

This function:

Samples the current price

Calculates time elapsed since last update

Maintains a sequential index to track updates

The resulting TickData structure serves as the fundamental building block for all candle generation.

State Management Architecture

The library employs a sophisticated state management system using varip variables, which persist across executions within the same bar. This creates a hybrid programming paradigm that's different from standard Pine Script's bar-by-bar model.

For chart-time candles, the core state transition logic is:

// Real-time update of current candle

candle_data := Candle.new(Open, High, Low, Close, polarity, series_index, candle_color)

candles.set(0, candle_data)

// When a new bar starts, preserve the previous candle

if clear_state

candles.insert(1, candle_data)

price.clear()

// Reset state for new candle

Open := Close

price.push(Open)

series_index += 1

This pattern of updating index 0 in real-time while inserting completed candles at index 1 creates an elegant solution for maintaining both current state and historical data.

Custom Timeframe Implementation

The custom timeframe system manages its own time boundaries independent of chart bars:

bool clear_state = switch settings.sample_type

SampleType.Ticks => cumulative_series_idx >= settings.number_of_ticks

SampleType.Time => cumulative_time_delta >= settings.number_of_seconds

This dual-clock system synchronizes two time domains:

Pine's execution clock (bar-by-bar processing)

The custom timeframe clock (tick or time-based)

The library carefully handles temporal discontinuities, ensuring candle formation remains accurate despite irregular tick arrival or market gaps.

Advanced Usage Techniques

1. Creating Custom Indicators with Real-Time Candles

To develop indicators that process real-time data within the current bar:

// Get real-time candles for your data

Candle rsi_candles = candle_array(ta.rsi(close, 14))

// Calculate indicator values based on candle properties

float signal = ta.ema(rsi_candles.first().source(Source.Close), 9)

// Detect patterns that occur within the bar

bool divergence = close > close and rsi_candles.first().Close < rsi_candles.get(1).Close

2. Working with Custom Timeframes and Plotting

For maximum flexibility when visualizing custom timeframe data:

// Create custom timeframe candles

CandleCTF volume_candles = ctf_candles_array(

source = volume,

candle_type = CandleType.candlestick,

sample_type = SampleType.Time,

number_of_seconds = 60

)

// Convert specific candle properties to float arrays

float volume_closes = volume_candles.candle_ctf_to_float(Source.Close)

// Calculate derived values

float volume_ema = volume_candles.ctf_ema(14)

// Create custom visualization

volume_candles.draw_ctf_candles_time()

volume_ema.draw_ctf_line_time(line_color = color.orange)

3. Creating Hybrid Timeframe Analysis

One powerful application is comparing indicators across multiple timeframes:

// Standard chart timeframe RSI

float chart_rsi = ta.rsi(close, 14)

// Custom 5-second timeframe RSI

CandleCTF ctf_candles = ctf_candles_array(

source = close,

candle_type = CandleType.candlestick,

sample_type = SampleType.Time,

number_of_seconds = 5

)

float fast_rsi_array = ctf_candles.candle_ctf_to_float(Source.Close)

float fast_rsi = fast_rsi_array.first()

// Generate signals based on divergence between timeframes

bool entry_signal = chart_rsi < 30 and fast_rsi > fast_rsi_array.get(1)

Final Notes

This library represents an advanced implementation of real-time data processing within Pine Script's constraints. By creating a reactive programming framework for handling continuous data streams, it enables sophisticated analysis typically only available in dedicated trading platforms.

The design principles employed—including state management, temporal processing, and object-oriented architecture—can serve as patterns for other advanced Pine Script development beyond this specific application.

------------------------

Library "real_time_candles"

A comprehensive library for creating real-time candles with customizable timeframes and sampling methods.

Supports both chart-time and custom-time candles with options for candlestick and Heikin-Ashi visualization.

Allows for tick-based or time-based sampling with moving average overlay capabilities.

get_tick(source, na_replace)

Captures the current price as a tick data point

Parameters:

source (float) : Optional - Price source to sample (defaults to close)

na_replace (float) : Optional - Value to use when source is na

Returns: TickData structure containing price, time since last update, and sequential index

candle_array(source, candle_type, sync_start, bullish_color, bearish_color)

Creates an array of candles based on price updates

Parameters:

source (float) : Optional - Price source to sample (defaults to close)

candle_type (simple CandleType) : Optional - Type of candle chart to create (candlestick or Heikin-Ashi)

sync_start (simple bool) : Optional - Whether to synchronize with the start of a new bar

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

Returns: Array of Candle objects ordered with most recent at index 0

candle_series(source, candle_type, wait_for_sync, bullish_color, bearish_color)

Provides a single candle based on the latest price data

Parameters:

source (float) : Optional - Price source to sample (defaults to close)

candle_type (simple CandleType) : Optional - Type of candle chart to create (candlestick or Heikin-Ashi)

wait_for_sync (simple bool) : Optional - Whether to wait for a new bar before starting

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

Returns: A single Candle object representing the current state

candle_tuple(source, candle_type, wait_for_sync, bullish_color, bearish_color)

Provides candle data as a tuple of OHLC values

Parameters:

source (float) : Optional - Price source to sample (defaults to close)

candle_type (simple CandleType) : Optional - Type of candle chart to create (candlestick or Heikin-Ashi)

wait_for_sync (simple bool) : Optional - Whether to wait for a new bar before starting

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

Returns: Tuple representing current candle values

method source(self, source, na_replace)

Extracts a specific price component from a Candle

Namespace types: Candle

Parameters:

self (Candle)

source (series Source) : Type of price data to extract (Open, High, Low, Close, or composite values)

na_replace (float) : Optional - Value to use when source value is na

Returns: The requested price value from the candle

method source(self, source)

Extracts a specific price component from a CandleCTF

Namespace types: CandleCTF

Parameters:

self (CandleCTF)

source (simple Source) : Type of price data to extract (Open, High, Low, Close, or composite values)

Returns: The requested price value from the candle as a varip

method candle_ctf_to_float(self, source)

Converts a specific price component from each CandleCTF to a float array

Namespace types: array

Parameters:

self (array)

source (simple Source) : Optional - Type of price data to extract (defaults to Close)

Returns: Array of float values extracted from the candles, ordered with most recent at index 0

method ctf_ema(self, ema_period)

Calculates an Exponential Moving Average for a CandleCTF array

Namespace types: array

Parameters:

self (array)

ema_period (simple float) : Period for the EMA calculation

Returns: Array of float values representing the EMA of the candle data, ordered with most recent at index 0

method draw_ctf_candles_time(self, sample_type, number_of_ticks, number_of_seconds, timezone)

Renders custom timeframe candles using bar time coordinates

Namespace types: array

Parameters:

self (array)

sample_type (simple SampleType) : Optional - Method for sampling data (Time or Ticks), used for tooltips

number_of_ticks (simple int) : Optional - Number of ticks per candle (used when sample_type is Ticks), used for tooltips

number_of_seconds (simple float) : Optional - Time duration per candle in seconds (used when sample_type is Time), used for tooltips

timezone (simple int) : Optional - Timezone offset from UTC (-12 to +12), used for tooltips

Returns: void - Renders candles on the chart using time-based x-coordinates

method draw_ctf_candles_index(self, sample_type, number_of_ticks, number_of_seconds, timezone)

Renders custom timeframe candles using bar index coordinates

Namespace types: array

Parameters:

self (array)

sample_type (simple SampleType) : Optional - Method for sampling data (Time or Ticks), used for tooltips

number_of_ticks (simple int) : Optional - Number of ticks per candle (used when sample_type is Ticks), used for tooltips

number_of_seconds (simple float) : Optional - Time duration per candle in seconds (used when sample_type is Time), used for tooltips

timezone (simple int) : Optional - Timezone offset from UTC (-12 to +12), used for tooltips

Returns: void - Renders candles on the chart using index-based x-coordinates

method draw_ctf_line_time(self, source, line_size, line_color)

Renders a line representing a price component from the candles using time coordinates

Namespace types: array

Parameters:

self (array)

source (simple Source) : Optional - Type of price data to extract (defaults to Close)

line_size (simple int) : Optional - Width of the line

line_color (simple color) : Optional - Color of the line

Returns: void - Renders a connected line on the chart using time-based x-coordinates

method draw_ctf_line_time(self, line_size, line_color)

Renders a line from a varip float array using time coordinates

Namespace types: array

Parameters:

self (array)

line_size (simple int) : Optional - Width of the line, defaults to 2

line_color (simple color) : Optional - Color of the line

Returns: void - Renders a connected line on the chart using time-based x-coordinates

method draw_ctf_line_index(self, source, line_size, line_color)

Renders a line representing a price component from the candles using index coordinates

Namespace types: array

Parameters:

self (array)

source (simple Source) : Optional - Type of price data to extract (defaults to Close)

line_size (simple int) : Optional - Width of the line

line_color (simple color) : Optional - Color of the line

Returns: void - Renders a connected line on the chart using index-based x-coordinates

method draw_ctf_line_index(self, line_size, line_color)

Renders a line from a varip float array using index coordinates

Namespace types: array

Parameters:

self (array)

line_size (simple int) : Optional - Width of the line, defaults to 2

line_color (simple color) : Optional - Color of the line

Returns: void - Renders a connected line on the chart using index-based x-coordinates

plot_ctf_tick_candles(source, candle_type, number_of_ticks, timezone, tied_open, ema_period, bullish_color, bearish_color, line_width, ema_color, use_time_indexing)

Plots tick-based candles with moving average

Parameters:

source (float) : Input price source to sample

candle_type (simple CandleType) : Type of candle chart to display

number_of_ticks (simple int) : Number of ticks per candle

timezone (simple int) : Timezone offset from UTC (-12 to +12)

tied_open (simple bool) : Whether to tie open price to close of previous candle

ema_period (simple float) : Period for the exponential moving average

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

line_width (simple int) : Optional - Width of the moving average line, defaults to 2

ema_color (color) : Optional - Color of the moving average line

use_time_indexing (simple bool) : Optional - When true the function will plot with xloc.time, when false it will plot using xloc.bar_index

Returns: void - Creates visual candle chart with EMA overlay

plot_ctf_tick_candles(source, candle_type, number_of_ticks, timezone, tied_open, bullish_color, bearish_color, use_time_indexing)

Plots tick-based candles without moving average

Parameters:

source (float) : Input price source to sample

candle_type (simple CandleType) : Type of candle chart to display

number_of_ticks (simple int) : Number of ticks per candle

timezone (simple int) : Timezone offset from UTC (-12 to +12)

tied_open (simple bool) : Whether to tie open price to close of previous candle

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

use_time_indexing (simple bool) : Optional - When true the function will plot with xloc.time, when false it will plot using xloc.bar_index

Returns: void - Creates visual candle chart without moving average

plot_ctf_time_candles(source, candle_type, number_of_seconds, timezone, tied_open, ema_period, bullish_color, bearish_color, line_width, ema_color, use_time_indexing)

Plots time-based candles with moving average

Parameters:

source (float) : Input price source to sample

candle_type (simple CandleType) : Type of candle chart to display

number_of_seconds (simple float) : Time duration per candle in seconds

timezone (simple int) : Timezone offset from UTC (-12 to +12)

tied_open (simple bool) : Whether to tie open price to close of previous candle

ema_period (simple float) : Period for the exponential moving average

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

line_width (simple int) : Optional - Width of the moving average line, defaults to 2

ema_color (color) : Optional - Color of the moving average line

use_time_indexing (simple bool) : Optional - When true the function will plot with xloc.time, when false it will plot using xloc.bar_index

Returns: void - Creates visual candle chart with EMA overlay

plot_ctf_time_candles(source, candle_type, number_of_seconds, timezone, tied_open, bullish_color, bearish_color, use_time_indexing)

Plots time-based candles without moving average

Parameters:

source (float) : Input price source to sample

candle_type (simple CandleType) : Type of candle chart to display

number_of_seconds (simple float) : Time duration per candle in seconds

timezone (simple int) : Timezone offset from UTC (-12 to +12)

tied_open (simple bool) : Whether to tie open price to close of previous candle

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

use_time_indexing (simple bool) : Optional - When true the function will plot with xloc.time, when false it will plot using xloc.bar_index

Returns: void - Creates visual candle chart without moving average

plot_ctf_candles(source, candle_type, sample_type, number_of_ticks, number_of_seconds, timezone, tied_open, ema_period, bullish_color, bearish_color, enable_ema, line_width, ema_color, use_time_indexing)

Unified function for plotting candles with comprehensive options

Parameters:

source (float) : Input price source to sample

candle_type (simple CandleType) : Optional - Type of candle chart to display

sample_type (simple SampleType) : Optional - Method for sampling data (Time or Ticks)

number_of_ticks (simple int) : Optional - Number of ticks per candle (used when sample_type is Ticks)

number_of_seconds (simple float) : Optional - Time duration per candle in seconds (used when sample_type is Time)

timezone (simple int) : Optional - Timezone offset from UTC (-12 to +12)

tied_open (simple bool) : Optional - Whether to tie open price to close of previous candle

ema_period (simple float) : Optional - Period for the exponential moving average

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

enable_ema (bool) : Optional - Whether to display the EMA overlay

line_width (simple int) : Optional - Width of the moving average line, defaults to 2

ema_color (color) : Optional - Color of the moving average line

use_time_indexing (simple bool) : Optional - When true the function will plot with xloc.time, when false it will plot using xloc.bar_index

Returns: void - Creates visual candle chart with optional EMA overlay

ctf_candles_array(source, candle_type, sample_type, number_of_ticks, number_of_seconds, tied_open, bullish_color, bearish_color)

Creates an array of custom timeframe candles without rendering them

Parameters:

source (float) : Input price source to sample

candle_type (simple CandleType) : Type of candle chart to create (candlestick or Heikin-Ashi)

sample_type (simple SampleType) : Method for sampling data (Time or Ticks)

number_of_ticks (simple int) : Optional - Number of ticks per candle (used when sample_type is Ticks)

number_of_seconds (simple float) : Optional - Time duration per candle in seconds (used when sample_type is Time)

tied_open (simple bool) : Optional - Whether to tie open price to close of previous candle

bullish_color (color) : Optional - Color for bullish candles

bearish_color (color) : Optional - Color for bearish candles

Returns: Array of CandleCTF objects ordered with most recent at index 0

Candle

Structure representing a complete candle with price data and display properties

Fields:

Open (series float) : Opening price of the candle

High (series float) : Highest price of the candle

Low (series float) : Lowest price of the candle

Close (series float) : Closing price of the candle

polarity (series bool) : Boolean indicating if candle is bullish (true) or bearish (false)

series_index (series int) : Sequential index identifying the candle in the series

candle_color (series color) : Color to use when rendering the candle

ready (series bool) : Boolean indicating if candle data is valid and ready for use

TickData

Structure for storing individual price updates

Fields:

price (series float) : The price value at this tick

time_delta (series float) : Time elapsed since the previous tick in milliseconds

series_index (series int) : Sequential index identifying this tick

CandleCTF

Structure representing a custom timeframe candle with additional time metadata

Fields:

Open (series float) : Opening price of the candle

High (series float) : Highest price of the candle

Low (series float) : Lowest price of the candle

Close (series float) : Closing price of the candle

polarity (series bool) : Boolean indicating if candle is bullish (true) or bearish (false)

series_index (series int) : Sequential index identifying the candle in the series

open_time (series int) : Timestamp marking when the candle was opened (in Unix time)

time_delta (series float) : Duration of the candle in milliseconds

candle_color (series color) : Color to use when rendering the candle

MonthlyReturnTableLibrary "MonthlyReturnTable"

TODO: The table displays monthly returns, profits, MDD, and number of trades.

get_table(mode, tablePosition, precision, textSize, marginTop, marginBottom, marginLeft, marginRight, colorHead, colorBull, colorBear, colorZero)

: get_table

Parameters:

mode (string)

tablePosition (string)

precision (int)

textSize (int)

marginTop (int)

marginBottom (int)

marginLeft (int)

marginRight (int)

colorHead (color)

colorBull (color)

colorBear (color)

colorZero (color)

Returns: : null, plot perfTable

UtilLibrary "Util"

defines commonly used utility functions and constants

calc_shares(entry_price, stop, fund, riskPerc)

Calculate number of shares for a trade

Parameters:

entry_price (float)

stop (float) : stop loss price

fund (float) : amount of fund to put in this trade

riskPerc (float) : percentage of fund to be risked in this trade. Default is 5%

Returns: number of shares

trade_exist(trade_id)

Returns if a trade with the specific ID is already open

Parameters:

trade_id (string)

Returns: true/false

trade

Fields:

id (series string)

direction (series TradeDir)

entry_price (series float)

shares (series float)

bars_open (series int)

TimezoneLibrary with pre-defined timezone enums that can be used to request a timezone input from the user. The library provides a `tostring()` function to convert enum values to a valid string that can be used as a `timezone` parameter in pine script built-in functions. The library also includes a bonus function to get a formatted UTC offset from a UNIX timestamp.

The timezone enums in this library were compiled by referencing the available timezone options from TradingView chart settings as well as multiple Wikipedia articles relating to lists of time zones.

Some enums from this library are used to retrieve an IANA time zone identifier, while other enums only use UTC/GMT offset notation. It is important to note that the Pine Script User Manual recommends using IANA notation in most cases.

HOW TO USE

This library is intended to be used by Pine Coders who wish to provide their users with a simple way to input a timezone. Using this library is as easy as 1, 2, 3:

Step 1

Import the library into your script. Replace with the latest available version number for this library.

//@version=6

indicator("Example")

import n00btraders/Timezone/ as tz

Step 2

Select one of the available enums from the library and use it as an input. Tip: view the library source code and scroll through the enums at the top to find the best choice for your script.

timezoneInput = input.enum(tz.TimezoneID.EXCHANGE, "Timezone")

Step 3

Convert the user-selected input into a valid string that can be used in one of the pine script built-in functions that have a `timezone` parameter.

string timezone = tz.tostring(timezoneInput)

EXPORTED FUNCTIONS

There are multiple 𝚝𝚘𝚜𝚝𝚛𝚒𝚗𝚐() functions in this library: one for each timezone enum. The function takes a single parameter: any enum field from one of the available timezone enums that are exported by this library. Depending on the selected enum, the function will return a time zone string in either UTC/GMT notation or IANA notation.

Note: to avoid confusion with the built-in `str.tostring()` function, it is recommended to use this library's `tostring()` as a method rather than a function:

string timezone = timezoneInput.tostring()

offset(timestamp, format, timezone, prefix, colon)

Formats the time offset from a UNIX timestamp represented in a specified timezone.

Namespace types: series OffsetFormat

Parameters:

timestamp (int) : (series int) A UNIX time.

format (series OffsetFormat) : (series OffsetFormat) A time offset format.

timezone (string) : (series string) A UTC/GMT offset or IANA time zone identifier.

prefix (string) : (series string) Optional 'UTC' or 'GMT' prefix for the result.

colon (bool) : (series bool) Optional usage of colon separator.

Returns: Time zone offset using the selected format.

The 𝚘𝚏𝚏𝚜𝚎𝚝() function is provided as a convenient alternative to manually using `str.format_time()` and then manipulating the result.

The OffsetFormat enum is used to decide the format of the result from the `offset()` function. The library source code contains comments above this enum declaration that describe how each enum field will modify a time offset.

Tip: hover over the `offset()` function call in the Pine Editor to display a pop-up containing:

Function description

Detailed parameter list, including default values

Example function calls

Example outputs for different OffsetFormat.* enum values

NOTES

At the time of this publication, Pine cannot be used to access a chart's selected time zone. Therefore, the main benefit of this library is to provide a quick and easy way to create a pine script input for a time zone (most commonly, the same time zone selected in the user's chart settings).

At the time of the creation of this library, there are 95 Time Zones made available in the TradingView chart settings. If any changes are made to the time zone settings, this library will be updated to match the new changes.

All time zone enums (and their individual fields) in this library were manually verified and tested to ensure correctness.

An example usage of this library is included at the bottom of the source code.

Credits to HoanGhetti for providing a nice Markdown resource which I referenced to be able to create a formatted informational pop-up for this library's `offset()` function.

merge_pinbar_babyblueLibrary "merge_pinbar_babyblue"

merge_pinbar: merge bars and check whether the bar is a pinbar

merge_pinbar_babyblue(period, max_bars)

merge_pinbar: merge bars and check whether the bar is a pinbar

Parameters:

period (simple int)

max_bars (simple int)

Returns: array:

TimeframeUtilsLibrary "TimeframeUtils"

Timeframe Utilities Library – Provides functions to convert timeframe resolutions to minutes and generate human‐readable timeframe text.

tfResInMinutes(_res)

tfResInMinutes

Parameters:

_res (string)

Returns: float - The specified timeframe's resolution in minutes.

getTimeFrameText(_tf)

getTimeFrameText

Parameters:

_tf (string)

Returns: string - A human-readable representation of the specified timeframe.

TickerLibLibrary "TickerLib"

Ticker Library

exists(tickerId)

Test if a tickerId exists

Parameters:

tickerId (string)

Returns: (bool)

notExist(tickerId)

Test if a tickerId do not exists

Parameters:

tickerId (string)

Returns: (bool)

getExchange(tickerId)

Pass a tickerId return the exchange

Parameters:

tickerId (string)

Returns: (string) exchange

isPerp(tickerId)

Test if tickerId is a perps pair

Parameters:

tickerId (string)

Returns: (bool)

isNotPerp(tickerId)

Test if tickerId is not a perps pair

Parameters:

tickerId (string)

Returns: (bool)

getPair(tickerId)

Pass a tickerId return the pair without exchange

Parameters:

tickerId (string)

Returns: (string) the pair

getSpotPair(tickerId)

Pass a tickerId return the pair without exchange and perps

Parameters:

tickerId (string)

Returns: (string) the pair

rzigzagLibrary "rzigzag"

Recursive Zigzag Using Matrix allows to create zigzags recursively on multiple levels. This is an old library converted to V6

zigzag(length, ohlc, numberOfPivots, offset)

calculates plain zigzag based on input

Parameters:

length (int) : Zigzag Length

ohlc (array) : Array containing ohlc values. Can also contain custom series

numberOfPivots (simple int) : Number of max pivots to be returned

offset (simple int) : Offset from current bar. Can be used for calculations based on confirmed bars

Returns: [matrix zigzagmatrix, bool flags]

iZigzag(length, h, l, numberOfPivots)

calculates plain zigzag based on input array

Parameters:

length (int) : Zigzag Length

h (array) : array containing high values of a series

l (array) : array containing low values of a series

numberOfPivots (simple int) : Number of max pivots to be returned

Returns: matrix zigzagmatrix

nextlevel(zigzagmatrix, numberOfPivots)

calculates next level zigzag based on present zigzag coordinates

Parameters:

zigzagmatrix (matrix) : Matrix containing zigzag pivots, bars, bar time, direction and level

numberOfPivots (simple int) : Number of max pivots to be returned

Returns: matrix zigzagmatrix

draw(zigzagmatrix, flags, lineColor, lineWidth, lineStyle, showLabel, xloc)

draws zigzag based on the zigzagmatrix input

Parameters:

zigzagmatrix (matrix) : Matrix containing zigzag pivots, bars, bar time, direction and level

flags (array) : Zigzag pivot flags

lineColor (color) : Zigzag line color

lineWidth (int) : Zigzag line width

lineStyle (string) : Zigzag line style

showLabel (bool) : Flag to indicate display pivot labels

xloc (string) : xloc preference for drawing lines/labels

Returns:

draw(length, ohlc, numberOfPivots, offset, lineColor, lineWidth, lineStyle, showLabel, xloc)

calculates and draws zigzag based on zigzag length and source input

Parameters:

length (int) : Zigzag Length

ohlc (array) : Array containing ohlc values. Can also contain custom series

numberOfPivots (simple int) : Number of max pivots to be returned

offset (simple int) : Offset from current bar. Can be used for calculations based on confirmed bars

lineColor (color) : Zigzag line color

lineWidth (int) : Zigzag line width

lineStyle (string) : Zigzag line style

showLabel (bool) : Flag to indicate display pivot labels

xloc (string) : xloc preference for drawing lines/labels

Returns: [matrix zigzagmatrix, array zigzaglines, array zigzaglabels, bool flags]

drawfresh(zigzagmatrix, zigzaglines, zigzaglabels, lineColor, lineWidth, lineStyle, showLabel, xloc)

draws fresh zigzag for all pivots in the input matrix.

Parameters:

zigzagmatrix (matrix) : Matrix containing zigzag pivots, bars, bar time, direction and level

zigzaglines (array) : array to which all newly created lines will be added

zigzaglabels (array) : array to which all newly created lables will be added

lineColor (color) : Zigzag line color

lineWidth (int) : Zigzag line width

lineStyle (string) : Zigzag line style

showLabel (bool) : Flag to indicate display pivot labels

xloc (string) : xloc preference for drawing lines/labels

Returns:

_matrixLibrary "_matrix"

Library helps visualize matrix as array of arrays and enables users to use array methods such as push, pop, shift, unshift etc along with cleanup activities on drawing objects wherever required

method delete(mtx, rowNumber)

deletes row from a matrix

Namespace types: matrix

Parameters:

mtx (matrix) : matrix of objects

rowNumber (int) : row index to be deleted

Returns: void

method delete(mtx, rowNumber)

Namespace types: matrix

Parameters:

mtx (matrix)

rowNumber (int)

method delete(mtx, rowNumber)

Namespace types: matrix

Parameters:

mtx (matrix)

rowNumber (int)

method delete(mtx, rowNumber)

Namespace types: matrix

Parameters:

mtx (matrix)

rowNumber (int)

method delete(mtx, rowNumber)

Namespace types: matrix

Parameters:

mtx (matrix)

rowNumber (int)

method delete(mtx, rowNumber)

Namespace types: matrix

Parameters:

mtx (matrix)

rowNumber (int)

method delete(mtx, rowNumber)

Namespace types: matrix

Parameters:

mtx (matrix)

rowNumber (int)

method delete(mtx, rowNumber)

Namespace types: matrix

Parameters:

mtx (matrix)

rowNumber (int)

method delete(mtx, rowNumber)

Namespace types: matrix

Parameters:

mtx (matrix)

rowNumber (int)

method delete(mtx, rowNumber)

Namespace types: matrix

Parameters:

mtx (matrix)

rowNumber (int)

method remove(mtx, rowNumber)

remove row from a matrix and returns them to caller

Namespace types: matrix

Parameters:

mtx (matrix) : matrix of objects

rowNumber (int) : row index to be deleted

Returns: type

method remove(mtx, rowNumber)

Namespace types: matrix

Parameters:

mtx (matrix)

rowNumber (int)

method remove(mtx, rowNumber)

Namespace types: matrix

Parameters:

mtx (matrix)

rowNumber (int)

method remove(mtx, rowNumber)

Namespace types: matrix

Parameters:

mtx (matrix)

rowNumber (int)

method remove(mtx, rowNumber)

Namespace types: matrix

Parameters:

mtx (matrix)

rowNumber (int)

method remove(mtx, rowNumber)

Namespace types: matrix

Parameters:

mtx (matrix)

rowNumber (int)

method remove(mtx, rowNumber)

Namespace types: matrix

Parameters:

mtx (matrix)

rowNumber (int)

method remove(mtx, rowNumber)

Namespace types: matrix

Parameters:

mtx (matrix)

rowNumber (int)

method remove(mtx, rowNumber)

Namespace types: matrix

Parameters:

mtx (matrix)

rowNumber (int)

method remove(mtx, rowNumber)

Namespace types: matrix

Parameters:

mtx (matrix)

rowNumber (int)

method unshift(mtx, row, maxItems)

unshift array of lines to first row of the matrix

Namespace types: matrix

Parameters:

mtx (matrix) : matrix of lines

row (array) : array of lines to be inserted in row

maxItems (simple int)

Returns: resulting matrix of type

method unshift(mtx, row, maxItems)

Namespace types: matrix

Parameters:

mtx (matrix)

row (array)

maxItems (simple int)

method unshift(mtx, row, maxItems)

Namespace types: matrix

Parameters:

mtx (matrix)

row (array)

maxItems (simple int)

method unshift(mtx, row, maxItems)

Namespace types: matrix

Parameters:

mtx (matrix)

row (array)

maxItems (simple int)

method unshift(mtx, row, maxItems)

Namespace types: matrix

Parameters:

mtx (matrix)

row (array)

maxItems (simple int)

method unshift(mtx, row, maxItems)

Namespace types: matrix

Parameters:

mtx (matrix)

row (array)

maxItems (simple int)

method unshift(mtx, row, maxItems)

Namespace types: matrix

Parameters:

mtx (matrix)

row (array)

maxItems (simple int)

method unshift(mtx, row, maxItems)

Namespace types: matrix

Parameters:

mtx (matrix)

row (array)

maxItems (simple int)

method unshift(mtx, row, maxItems)

Namespace types: matrix

Parameters:

mtx (matrix)

row (array)

maxItems (simple int)

method unshift(mtx, row, maxItems)

Namespace types: matrix

Parameters:

mtx (matrix)

row (array)

maxItems (simple int)

method push(mtx, row, maxItems)

push array of lines to end of the matrix row

Namespace types: matrix

Parameters:

mtx (matrix) : matrix of lines

row (array) : array of lines to be inserted in row

maxItems (simple int)

Returns: resulting matrix of lines

method push(mtx, row, maxItems)

Namespace types: matrix

Parameters:

mtx (matrix)

row (array)

maxItems (simple int)

method push(mtx, row, maxItems)

Namespace types: matrix

Parameters:

mtx (matrix)

row (array)

maxItems (simple int)

method push(mtx, row, maxItems)

Namespace types: matrix

Parameters:

mtx (matrix)

row (array)

maxItems (simple int)

method push(mtx, row, maxItems)

Namespace types: matrix

Parameters:

mtx (matrix)

row (array)

maxItems (simple int)

method push(mtx, row, maxItems)

Namespace types: matrix

Parameters:

mtx (matrix)

row (array)

maxItems (simple int)

method push(mtx, row, maxItems)

Namespace types: matrix

Parameters:

mtx (matrix)

row (array)

maxItems (simple int)

method push(mtx, row, maxItems)

Namespace types: matrix

Parameters:

mtx (matrix)

row (array)

maxItems (simple int)

method push(mtx, row, maxItems)

Namespace types: matrix

Parameters:

mtx (matrix)

row (array)

maxItems (simple int)

method push(mtx, row, maxItems)

Namespace types: matrix

Parameters:

mtx (matrix)

row (array)

maxItems (simple int)

method shift(mtx)

shift removes first row from matrix of lines

Namespace types: matrix

Parameters:

mtx (matrix) : matrix of lines from which the shift operation need to be performed

Returns: void

method shift(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method shift(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method shift(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method shift(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method shift(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method shift(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method shift(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method shift(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method shift(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method rshift(mtx)

rshift removes first row from matrix of lines and returns them as array

Namespace types: matrix

Parameters:

mtx (matrix) : matrix of lines from which the rshift operation need to be performed

Returns: type

method rshift(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method rshift(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method rshift(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method rshift(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method rshift(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method rshift(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method rshift(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method rshift(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method rshift(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method pop(mtx)

pop removes last row from matrix of lines

Namespace types: matrix

Parameters:

mtx (matrix) : matrix of lines from which the pop operation need to be performed

Returns: void

method pop(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method pop(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method pop(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method pop(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method pop(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method pop(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method pop(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method pop(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method pop(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method rpop(mtx)

rpop removes last row from matrix of lines and reutnrs the array to caller

Namespace types: matrix

Parameters:

mtx (matrix) : matrix of lines from which the rpop operation need to be performed

Returns: void

method rpop(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method rpop(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method rpop(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method rpop(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method rpop(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method rpop(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method rpop(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method rpop(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method rpop(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method clear(mtx)

clear clears the matrix

Namespace types: matrix

Parameters:

mtx (matrix) : matrix of lines which needs to be cleared

Returns: void

method clear(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method clear(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method clear(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method clear(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method clear(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method clear(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method clear(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method clear(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method clear(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method flush(mtx)

clear clears the matrix but retains the drawing objects

Namespace types: matrix

Parameters:

mtx (matrix) : matrix of lines which needs to be cleared

Returns: void

method flush(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method flush(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method flush(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method flush(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method flush(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method flush(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method flush(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method flush(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

method flush(mtx)

Namespace types: matrix

Parameters:

mtx (matrix)

TALibrary "TA"

Technical analysis library that provides convenience functions and overrides for tradingview's own ta.* functions in order to work around various limitations.

sma(src, length)

Override for ta.sma that allows you to provide series values

Parameters:

src (float) : The source values to process

length (int) : The length of the source to evaluate for the moving average

Returns: float The moving average

ema(src, length)

Override for ta.ema that allows you to provide series values

Parameters:

src (float) : The source values to process

length (int) : The length of the source to evaluate for the moving average

Returns: float The moving average

rma(src, length)

Override for ta.rma that allows you to provide series values

Parameters:

src (float) : The source values to process

length (int) : The length of the source to evaluate for the moving average

Returns: float The moving average

wma(src, length)

Override for ta.wma that allows you to provide series values

Parameters:

src (float) : The source values to process

length (int) : The length of the source to evaluate for the moving average

Returns: float The moving average

vwma(src, length)

Override for ta.vwma that allows you to provide series values

Parameters:

src (float) : The source values to process

length (int) : The length of the source to evaluate for the moving average

Returns: float The moving average

ma(src, length, maType)

Provide the requested moving average

Parameters:

src (float) : The source values to process

length (int) : The length of the source to evaluate for the moving average

maType (string) : The type of moving average to return: SMA (default), EMA, SMMA (RMA), WMA, VWMA

Returns: float The moving average

alert_formatLibrary "alert_format"

library to call alert with parameters specified

alert_format(message, param_names, param_values, params_format, freq)

alert with named parameters message

Parameters:

message (string) : message header that prefixes named parameters

param_names (array) : names for parameters specified in param_values

param_values (array) : values for parameters specified in param_names

params_format (string) : format for all param values, 2 decimals by default

freq (string) : Determines the allowed frequency of the alert trigger (see alert). alert.freq_once_per_bar_close by default

Cometreon_Public📚 Cometreon Public Library – Advanced Functions for Pine Script

This library contains advanced functions used in my public indicators on TradingView. The goal is to make the code more modular and efficient, allowing users to call pre-built functions for complex calculations without rewriting them from scratch.

🔹 Currently Available Functions:

1️⃣ Moving Average Function – Provides multiple types of moving averages to choose from, including:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

WMA (Weighted Moving Average)

RMA (Smoothed Moving Average)

HMA (Hull Moving Average)

JMA (Jurik Moving Average)

DEMA (Double Exponential Moving Average)

TEMA (Triple Exponential Moving Average)

LSMA (Least Squares Moving Average)

VWMA (Volume-Weighted Moving Average)

SMMA (Smoothed Moving Average)

KAMA (Kaufman’s Adaptive Moving Average)

ALMA (Arnaud Legoux Moving Average)

FRAMA (Fractal Adaptive Moving Average)

VIDYA (Variable Index Dynamic Average)

2️⃣ Custom RSI – Uses the Moving Average function to modify the calculation method, with an additional option for a dynamic version.