SLTP v3Sometimes when you are entrying a position or placing a limit/stop order, you only see one or even none key price level to set as TP (Take Profit) or SL (Stop Loss) conditional orders. You can use this SLTP to choose proper price levels to set as TP or SL. This indicator is highly custom. Remember to alter the color of the short side to your background color when you are about to long a security and do the same to the long side when you are about to short.

By the way the reference levels are based on volatility of last 14 bars of your security.

Will keep updating this indicator with high pratical value but not today. Peace out

有时当你进入一个头寸或设置限价/止损订单时,你可能只看到一个甚至没有关键价格水平可以设置为获利(Take Profit,TP)或止损(Stop Loss,SL)条件订单。你可以使用这个SLTP指标来选择合适的价格水平设置为TP或SL。这个指标高度可定制。当你打算买入证券时,记得将空头一侧的颜色改为与背景颜色一致;当你打算做空时,也对多头一侧做同样的调整。

顺便说一下,参考水平是基于证券最近14根K线的波动率来计算的。

我会持续更新这个具有高实用价值的指标,但不是今天。

祝好!

Riskmangement

Heikin-Ashi Mean Reversion Oscillator [Alpha Extract]The Heikin-Ashi Mean Reversion Oscillator combines the smoothing characteristics of Heikin-Ashi candlesticks with mean reversion analysis to create a powerful momentum oscillator. This indicator applies Heikin-Ashi transformation twice - first to price data and then to the oscillator itself - resulting in smoother signals while maintaining sensitivity to trend changes and potential reversal points.

🔶 CALCULATION

Heikin-Ashi Transformation: Converts regular OHLC data to smoothed Heikin-Ashi values

Component Analysis: Calculates trend strength, body deviation, and price deviation from mean

Oscillator Construction: Combines components with weighted formula (40% trend strength, 30% body deviation, 30% price deviation)

Double Smoothing: Applies EMA smoothing and second Heikin-Ashi transformation to oscillator values

Signal Generation: Identifies trend changes and crossover points with overbought/oversold levels

Formula:

HA Close = (Open + High + Low + Close) / 4

HA Open = (Previous HA Open + Previous HA Close) / 2

Trend Strength = Normalized consecutive HA candle direction

Body Deviation = (HA Body - Mean Body) / Mean Body * 100

Price Deviation = ((HA Close - Price Mean) / Price Mean * 100) / Standard Deviation * 25

Raw Oscillator = (Trend Strength * 0.4) + (Body Deviation * 0.3) + (Price Deviation * 0.3)

Final Oscillator = 50 + (EMA(Raw Oscillator) / 2)

🔶 DETAILS Visual Features:

Heikin-Ashi Candlesticks: Smoothed oscillator representation using HA transformation with vibrant teal/red coloring

Overbought/Oversold Zones: Horizontal lines at customizable levels (default 70/30) with background highlighting in extreme zones

Moving Averages: Optional fast and slow EMA overlays for additional trend confirmation

Signal Dashboard: Real-time table showing current oscillator status (Overbought/Oversold/Bullish/Bearish) and buy/sell signals

Reference Lines: Middle line at 50 (neutral), with 0 and 100 boundaries for range visualization

Interpretation:

Above 70: Overbought conditions, potential selling opportunity

Below 30: Oversold conditions, potential buying opportunity

Bullish HA Candles: Green/teal candles indicate upward momentum

Bearish HA Candles: Red candles indicate downward momentum

MA Crossovers: Fast EMA above slow EMA suggests bullish momentum, below suggests bearish momentum

Zone Exits: Price moving out of extreme zones (above 70 or below 30) often signals trend continuation

🔶 EXAMPLES

Mean Reversion Signals: When the oscillator reaches extreme levels (above 70 or below 30), it identifies potential reversal points where price may revert to the mean.

Example: Oscillator reaching 80+ levels during strong uptrends often precedes short-term pullbacks, providing profit-taking opportunities.

Trend Change Detection: The double Heikin-Ashi smoothing helps identify genuine trend changes while filtering out market noise.

Example: When oscillator HA candles change from red to teal after oversold readings, this confirms potential trend reversal from bearish to bullish.

Moving Average Confirmation: Fast and slow EMA crossovers on the oscillator provide additional confirmation of momentum shifts.

Example: Fast EMA crossing above slow EMA while oscillator is rising from oversold levels provides strong bullish confirmation signal.

Dashboard Signal Integration: The real-time dashboard combines oscillator status with directional signals for quick decision-making.

Example: Dashboard showing "Oversold" status with "BUY" signal when HA candles turn bullish provides clear entry timing.

🔶 SETTINGS

Customization Options:

Calculation: Oscillator period (default 14), smoothing factor (1-50, default 2)

Levels: Overbought threshold (50-100, default 70), oversold threshold (0-50, default 30)

Moving Averages: Toggle display, fast EMA length (default 9), slow EMA length (default 21)

Visual Enhancements: Show/hide signal dashboard, customizable table position

Alert Conditions: Oversold bounce, overbought reversal, bullish/bearish MA crossovers

The Heikin-Ashi Mean Reversion Oscillator provides traders with a sophisticated momentum tool that combines the smoothing benefits of Heikin-Ashi analysis with mean reversion principles. The double transformation process creates cleaner signals while the integrated dashboard and multiple confirmation methods help traders identify high-probability entry and exit points during both trending and ranging market conditions.

Correlation Coefficient📊 Correlation Coefficient (CC)

This indicator measures the statistical correlation between two selected securities over a defined period, scaled from -100 to +100.

It helps you quickly assess whether assets are moving:

Together (positive correlation)

Opposite (negative correlation)

Independently (zero correlation)

🔧 Features:

Select any two symbols (default: NIFTY & BANKNIFTY)

Adjustable length parameter for short-term or long-term correlation analysis

Clean, color-coded plot with horizontal levels to easily identify key correlation zones

📈 Useful For:

Pair trading setups

Hedging strategies

Detecting market regime shifts or intermarket divergences

⚠️ Disclaimer: This is not trading or investment advice.

This indicator is intended for informational purposes only and is not recommended for making

direct trading decisions.

Precision Entry Signals (RSI + MA12 Logic)Description:

This script provides precise entry signals based on a clean confluence of MA12 breakouts and RSI momentum, filtered by a VWMA (Volume-Weighted Moving Average) of the RSI.

-----------------------------------------------------------------------------------------------------------------

🔹 Long entry conditions:

- Candle opens below the 12-period MA and closes above it

- RSI crosses above its VWMA

- Previous candle is bearish (additional confirmation)

🔹 Short entry conditions:

- Candle opens above the 12-period MA and closes below it

- RSI crosses below its VWMA

- Previous candle is bullish

----------------------------------------------------------------------------------------------------------------

Once a signal is confirmed, the script automatically draws:

Entry line (at close price)

Stop Loss line (just below recent lows for long, or above highs for short)

Take Profit 1 (1R)

Take Profit 2 (2R)

Labels are attached to the lines for clarity: ENTRY, SL, TP1, and TP2.

⚠️ Note: This tool only provides entry signals and visual risk/reward guidance. It does not manage exits dynamically. Manual trade management is recommended.

This script is intended for active intraday traders, especially on lower timeframes like 3-minute, 5-minute or 15-minute charts.

---------------------------------------------------------------------------------------------------------------

🔧 Recommended companion indicator:

For better confirmation and visual tracking of the RSI/VWMA cross logic, it is strongly recommended to also use the companion script:

🔹 Relative Strength Index (with MA based cross signals)

→ Shows RSI and its moving average visually, with triangle plots on every valid cross.

→ Matches exactly the RSI/VWMA behavior used in this entry signal script.

📌 Important:

After adding the RSI script to your chart, make sure to set:

RSI Length = 14

MA Type = VWMA

MA Length = 20

This ensures it visually matches the logic used by the entry signal script.

Both indicators are fully open source and meant to be used together — especially when trading manually.

Median True Range {Darkoexe}Simple and sweet, this is the median true range. It reviews the size of the previous period amount of candles, and displays the candle size value that is the median of those previous values.

//Darkoexe

Risk Calculator PRO — manual lot size + auto lot-suggestionWhy risk management?

90 % of traders blow up because they size positions emotionally. This tool forces Risk-First Thinking: choose the amount you’re willing to lose, and the script reverse-engineers everything else.

Key features

1. Manual or Market Entry – click “Use current price” or type a custom entry.

2. Setup-based ₹-Risk – four presets (A/B/C/D). Edit to your workflow.

3. Lot-Size Input + Auto Lot Suggestion – you tell the contract size ⇒ script tells you how many lots.

4. Auto-SL (optional) – tick to push stop-loss to exactly 1-lot risk.

5. Instant Targets – 1 : 2, 1 : 3, 1 : 4, 1 : 5 plotted and alert-ready.

6. P&L Preview – table shows potential profit at each R-multiple plus real ₹ at SL.

7. Margin Column – enter per-lot margin once; script totals it for any size.

8. Clean Table UI – dark/light friendly; updates every 5 bars.

9. Alert Pack – SL, each target, plus copy-paste journal line on the chart.

How to use

1. Add to chart > “Format”.

2. Type the lot size for the symbol (e.g., 1250 for Natural Gas, 1 for cash equity).

3. Pick Side (Buy / Sell) & Setup grade.

4. ✅ If you want the script to place SL for you, tick Auto-SL (risk = 1 lot).

5. Otherwise type your own Stop-loss.

6. Read the table:

• Suggested lots = how many to trade so risk ≤ setup ₹.

• Risk (currency) = real money lost if SL hits.

7. Set TradingView alerts on the built-in conditions (T1_2, SL_hit, etc.) if you’d like push / email.

8. Copy the orange CSV label to Excel / Sheets for journalling.

Best practices

• Never raise risk to “fit” a trade. Lower size instead.

• Review win-rate vs. R multiple monthly; adjust setups A–D accordingly.

• Test Auto-SL in replay before going live.

Disclaimer

This script is educational. Past performance ≠ future results. The author isn’t responsible for trading losses.

TCP | Money Management indicator | Crypto Version📌 TCP | Money Management Indicator | Crypto Version

A robust, multi-target risk and capital management indicator tailored for crypto traders. Whether you're trading spot, perpetual futures, or leverage tokens, this tool empowers you with precise control over risk, reward, and position sizing—directly on your chart. Eliminate guesswork and trade with confidence.

🔰 Introduction: Master Your Capital, Master Your Trades

Poor money management is the number one reason traders lose their accounts, even with solid strategies. The TCP Money Management Indicator, built by Trade City Pro (TCP), solves this problem by providing a structured, rule-based approach to capital allocation.

Want to dive deeper into the concept of money management? Check out our comprehensive tutorial on TradingView, " TradeCityPro Academy: Money Management ", to understand the principles that power this indicator and transform your trading mindset.

This indicator equips you to:

• Calculate optimal position sizes based on your capital, risk percentage, and leverage

• Set up to 5 customizable take-profit targets with partial close percentages

• Access real-time metrics like Risk-to-Reward (R/R), USD profit, and margin usage

• Trade with discipline, avoiding emotional or inconsistent decisions

💸 Money Management Formula

The indicator uses a professional capital allocation model:

Position Size = (Capital × Risk %) ÷ (Stop Loss % × Leverage)

From this, it calculates:

• Total risk amount in USD

• Optimal position size for your trade

• Margin required for each take-profit target

• Adjusted R/R for each target, accounting for partial position closures

🛠 How to Use

Enter Trade Parameters: Input your capital, risk %, leverage, entry price, and stop-loss price.

Set Take-Profit Targets: Enable 1 to 5 take-profit levels and specify the percentage of the position to close at each.

Real-Time Calculations: The indicator automatically computes:

• R/R ratio for each target

• Profit in USD for each partial close

• Margin used per target (in % and USD)

Visualize Your Trade:

• Price levels for entry, stop-loss, and take-profits are plotted on the chart.

• A dynamic info panel on the left side displays all key metrics.

🔄 Dynamic Adjustments: As each take-profit target is hit and a portion of the position is closed, the indicator recalculates the remaining position size, expected profit, R/R, and margin for subsequent targets. This ensures accuracy and reflects real-world trade behavior.

📊 Table Overview

The left-side panel provides a clear snapshot:

• Trade Setup: Capital, entry price, stop-loss, risk amount, and position size

• Per Target: Percentage closed, R/R, profit in USD, and margin used

• Summary: Total expected profit across all targets

⚙️ Settings Panel

• Total Capital ($): Your account size for the trade

• Risk per Trade (%): The percentage of capital you’re willing to risk

• Leverage: The leverage applied to the trade

• Entry/Stop-Loss Prices: Define your trade’s risk zone

• Take-Profit Targets (1–5): Set price levels and percentage to close at each

🔍 Use Case Example

Imagine you have $1,000 capital, risking 1%, using 10x leverage:

• Entry: $100 | Stop-Loss: $95

• TP1: $110 (close 50%) | TP2: $115 (close 50%)

The indicator calculates the exact position size, profit at each target, and margin allocation in real time, with all metrics displayed on the chart.

✅ Why Traders Love It

• Precision: No more manual calculations or guesswork

• Versatility: Works on all crypto pairs (BTC, ETH, altcoins, etc.)

• Flexibility: Perfect for scalping, swing trading, or futures strategies

• Universal: Compatible with all timeframes

• Transparency: Fully manual, with clear and reliable outputs

🧩 Built by Trade City Pro (TCP)

Developed by TCP, a trusted name in trading tools, used by over 150,000 traders worldwide. This indicator is coded in Pine Script v5, ensuring compatibility with TradingView’s platform.

🧾 Final Notes

• No Auto-Trading: This is a manual tool for disciplined traders

• No Repainting: All calculations are accurate and non-repainting

• Tested: Rigorously validated across major crypto pairs

• Publish-Ready: Built for seamless use on TradingView

🔗 Resources

• Money Management Tutorial: Learn the fundamentals of capital management with our detailed guide: TradeCityPro Academy: Money Management

• TradingView Profile: Explore more tools by TCP on TradingView

Risk ModuleRisk Module

This indicator provides a visual reference to determine position sizing and approximate stop placement. It is designed to support trade planning by calculating equalized risk per trade based on a stop distance derived from volatility. The tool offers supportive reference points that allow for quick evaluation of risk and position size consistency across varying markets.

Equalized Risk Per Trade

The indicator calculates the number of shares that can be traded to maintain consistent monetary risk. The formula is based on the distance between the current price and the visual stop reference, adjusting the position size proportionally.

Position Size = Dollar Risk / (Entry Price – Stop Price)

The risk is calculated as a percentage of account size; both of which can be set in the indicator’s settings tab. This creates a consistent risk exposure across trades regardless of volatility or structural stop distance.

Stop Placement Reference

The visual stop reference is derived from the Average True Range (ATR), providing a volatility-based anchor. The default value is set to 2 × ATR, but this can be customized.

Price Model: Uses the current price ± ATR × multiplier. This model reacts to price movement and is set as the default option.

EMA Model: Uses the 20-period EMA ± ATR × multiplier. This model is less reactive and can be an option when used in combination with an envelope indicator.

Chart Elements

Stop Levels: Plotted above and below either the current price or EMA, depending on the selected model. These serve as visual reference points for stop placement; the lower level a sell stop for long trades, the upper level a buy stop for short trades.

Information Table: Displays the number of shares to trade, stop level and percentage risk. A compact mode is available to reduce the table to essential information (H/L and Shares).

Settings Overview

Stop Model: Choose between “Price” or “EMA” stop calculation logic.

ATR Multiplier: Change the distance between price/EMA and the stop reference.

Account Size / Risk %: These risk parameters are used to calculate dollar risk per trade.

Visible Bars: Number of recent bars to show stop markers on.

Compact Mode: Minimal table view for reduced chart footprint.

Table Position / Size: Controls table placement and scale on the chart.

Bitcoin Monthly Seasonality [Alpha Extract]The Bitcoin Monthly Seasonality indicator analyzes historical Bitcoin price performance across different months of the year, enabling traders to identify seasonal patterns and potential trading opportunities. This tool helps traders:

Visualize which months historically perform best and worst for Bitcoin.

Track average returns and win rates for each month of the year.

Identify seasonal patterns to enhance trading strategies.

Compare cumulative or individual monthly performance.

🔶 CALCULATION

The indicator processes historical Bitcoin price data to calculate monthly performance metrics

Monthly Return Calculation

Inputs:

Monthly open and close prices.

User-defined lookback period (1-15 years).

Return Types:

Percentage: (monthEndPrice / monthStartPrice - 1) × 100

Price: monthEndPrice - monthStartPrice

Statistical Measures

Monthly Averages: ◦ Average return for each month calculated from historical data.

Win Rate: ◦ Percentage of positive returns for each month.

Best/Worst Detection: ◦ Identifies months with highest and lowest average returns.

Cumulative Option

Standard View: Shows discrete monthly performance.

Cumulative View: Shows compounding effect of consecutive months.

Example Calculation (Pine Script):

monthReturn = returnType == "Percentage" ?

(monthEndPrice / monthStartPrice - 1) * 100 :

monthEndPrice - monthStartPrice

calcWinRate(arr) =>

winCount = 0

totalCount = array.size(arr)

if totalCount > 0

for i = 0 to totalCount - 1

if array.get(arr, i) > 0

winCount += 1

(winCount / totalCount) * 100

else

0.0

🔶 DETAILS

Visual Features

Monthly Performance Bars: ◦ Color-coded bars (teal for positive, red for negative returns). ◦ Special highlighting for best (yellow) and worst (fuchsia) months.

Optional Trend Line: ◦ Shows continuous performance across months.

Monthly Axis Labels: ◦ Clear month names for easy reference.

Statistics Table: ◦ Comprehensive view of monthly performance metrics. ◦ Color-coded rows based on performance.

Interpretation

Strong Positive Months: Historically bullish periods for Bitcoin.

Strong Negative Months: Historically bearish periods for Bitcoin.

Win Rate Analysis: Higher win rates indicate more consistently positive months.

Pattern Recognition: Identify recurring seasonal patterns across years.

Best/Worst Identification: Quickly spot the historically strongest and weakest months.

🔶 EXAMPLES

The indicator helps identify key seasonal patterns

Bullish Seasons: Visualize historically strong months where Bitcoin tends to perform well, allowing traders to align long positions with favorable seasonality.

Bearish Seasons: Identify historically weak months where Bitcoin tends to underperform, helping traders avoid unfavorable periods or consider short positions.

Seasonal Strategy Development: Create trading strategies that capitalize on recurring monthly patterns, such as entering positions in historically strong months and reducing exposure during weak months.

Year-to-Year Comparison: Assess how current year performance compares to historical seasonal patterns to identify anomalies or confirmation of trends.

🔶 SETTINGS

Customization Options

Lookback Period: Adjust the number of years (1-15) used for historical analysis.

Return Type: Choose between percentage returns or absolute price changes.

Cumulative Option: Toggle between discrete monthly performance or cumulative effect.

Visual Style Options: Bar Display: Enable/disable and customize colors for positive/negative bars, Line Display: Enable/disable and customize colors for trend line, Axes Display: Show/hide reference axes.

Visual Enhancement: Best/Worst Month Highlighting: Toggle special highlighting of extreme months, Custom highlight colors for best and worst performing months.

The Bitcoin Monthly Seasonality indicator provides traders with valuable insights into Bitcoin's historical performance patterns throughout the year, helping to identify potentially favorable and unfavorable trading periods based on seasonal tendencies.

Win-Loss Streak PlotterWin-Loss Streak Plotter

This indicator tracks the win/loss streaks of moving average crossovers (using simple moving averages for illustration purposes). It calculates the price change after each crossover, marking each as a win (green) or loss (red). The win rate is shown separately.

Inputs:

Source: Price series (default: open)

Fast MA: Fast moving average (default: open)

Slow MA: Slow moving average (default: open)

Total Crosses to Analyze: Number of crossovers to track

Crosses per Row: Number of crossovers per row in the table

Output:

A table displays each crossover’s result (win/loss).

A separate win rate table shows the percentage of wins.

Suggestions are always welcomed!

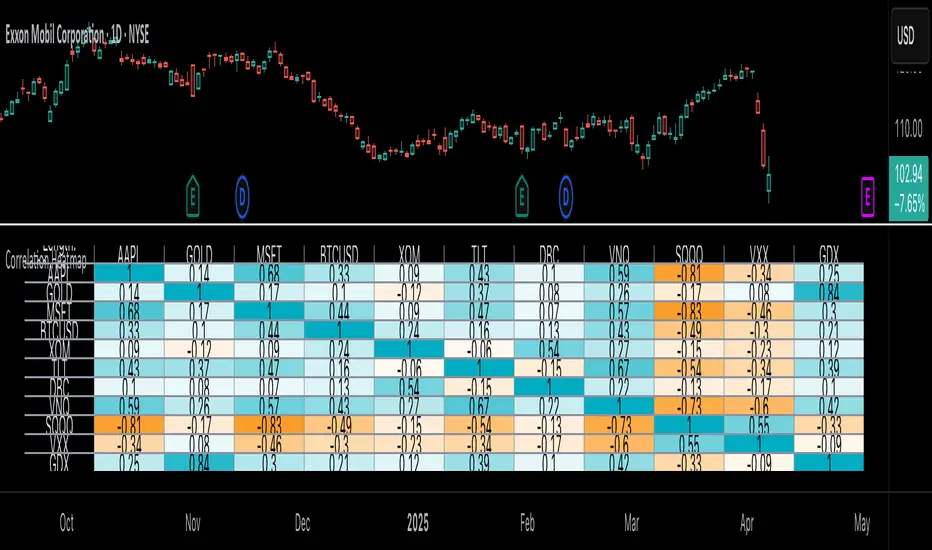

Correlation Heatmap█ OVERVIEW

This indicator creates a correlation matrix for a user-specified list of symbols based on their time-aligned weekly or monthly price returns. It calculates the Pearson correlation coefficient for each possible symbol pair, and it displays the results in a symmetric table with heatmap-colored cells. This format provides an intuitive view of the linear relationships between various symbols' price movements over a specific time range.

█ CONCEPTS

Correlation

Correlation typically refers to an observable statistical relationship between two datasets. In a financial time series context, it usually represents the extent to which sampled values from a pair of datasets, such as two series of price returns, vary jointly over time. More specifically, in this context, correlation describes the strength and direction of the relationship between the samples from both series.

If two separate time series tend to rise and fall together proportionally, they might be highly correlated. Likewise, if the series often vary in opposite directions, they might have a strong anticorrelation . If the two series do not exhibit a clear relationship, they might be uncorrelated .

Traders frequently analyze asset correlations to help optimize portfolios, assess market behaviors, identify potential risks, and support trading decisions. For instance, correlation often plays a key role in diversification . When two instruments exhibit a strong correlation in their returns, it might indicate that buying or selling both carries elevated unsystematic risk . Therefore, traders often aim to create balanced portfolios of relatively uncorrelated or anticorrelated assets to help promote investment diversity and potentially offset some of the risks.

When using correlation analysis to support investment decisions, it is crucial to understand the following caveats:

• Correlation does not imply causation . Two assets might vary jointly over an analyzed range, resulting in high correlation or anticorrelation in their returns, but that does not indicate that either instrument directly influences the other. Joint variability between assets might occur because of shared sensitivities to external factors, such as interest rates or global sentiment, or it might be entirely coincidental. In other words, correlation does not provide sufficient information to identify cause-and-effect relationships.

• Correlation does not predict the future relationship between two assets. It only reflects the estimated strength and direction of the relationship between the current analyzed samples. Financial time series are ever-changing. A strong trend between two assets can weaken or reverse in the future.

Correlation coefficient

A correlation coefficient is a numeric measure of correlation. Several coefficients exist, each quantifying different types of relationships between two datasets. The most common and widely known measure is the Pearson product-moment correlation coefficient , also known as the Pearson correlation coefficient or Pearson's r . Usually, when the term "correlation coefficient" is used without context, it refers to this correlation measure.

The Pearson correlation coefficient quantifies the strength and direction of the linear relationship between two variables. In other words, it indicates how consistently variables' values move together or in opposite directions in a proportional, linear manner. Its formula is as follows:

𝑟(𝑥, 𝑦) = cov(𝑥, 𝑦) / (𝜎𝑥 * 𝜎𝑦)

Where:

• 𝑥 is the first variable, and 𝑦 is the second variable.

• cov(𝑥, 𝑦) is the covariance between 𝑥 and 𝑦.

• 𝜎𝑥 is the standard deviation of 𝑥.

• 𝜎𝑦 is the standard deviation of 𝑦.

In essence, the correlation coefficient measures the covariance between two variables, normalized by the product of their standard deviations. The coefficient's value ranges from -1 to 1, allowing a more straightforward interpretation of the relationship between two datasets than what covariance alone provides:

• A value of 1 indicates a perfect positive correlation over the analyzed sample. As one variable's value changes, the other variable's value changes proportionally in the same direction .

• A value of -1 indicates a perfect negative correlation (anticorrelation). As one variable's value increases, the other variable's value decreases proportionally.

• A value of 0 indicates no linear relationship between the variables over the analyzed sample.

Aligning returns across instruments

In a financial time series, each data point (i.e., bar) in a sample represents information collected in periodic intervals. For instance, on a "1D" chart, bars form at specific times as successive days elapse.

However, the times of the data points for a symbol's standard dataset depend on its active sessions , and sessions vary across instrument types. For example, the daily session for NYSE stocks is 09:30 - 16:00 UTC-4/-5 on weekdays, Forex instruments have 24-hour sessions that span from 17:00 UTC-4/-5 on one weekday to 17:00 on the next, and new daily sessions for cryptocurrencies start at 00:00 UTC every day because crypto markets are consistently open.

Therefore, comparing the standard datasets for different asset types to identify correlations presents a challenge. If two symbols' datasets have bars that form at unaligned times, their correlation coefficient does not accurately describe their relationship. When calculating correlations between the returns for two assets, both datasets must maintain consistent time alignment in their values and cover identical ranges for meaningful results.

To address the issue of time alignment across instruments, this indicator requests confirmed weekly or monthly data from spread tickers constructed from the chart's ticker and another specified ticker. The datasets for spreads are derived from lower-timeframe data to ensure the values from all symbols come from aligned points in time, allowing a fair comparison between different instrument types. Additionally, each spread ticker ID includes necessary modifiers, such as extended hours and adjustments.

In this indicator, we use the following process to retrieve time-aligned returns for correlation calculations:

1. Request the current and previous prices from a spread representing the sum of the chart symbol and another symbol ( "chartSymbol + anotherSymbol" ).

2. Request the prices from another spread representing the difference between the two symbols ( "chartSymbol - anotherSymbol" ).

3. Calculate half of the difference between the values from both spreads ( 0.5 * (requestedSum - requestedDifference) ). The results represent the symbol's prices at times aligned with the sample points on the current chart.

4. Calculate the arithmetic return of the retrieved prices: (currentPrice - previousPrice) / previousPrice

5. Repeat steps 1-4 for each symbol requiring analysis.

It's crucial to note that because this process retrieves prices for a symbol at times consistent with periodic points on the current chart, the values can represent prices from before or after the closing time of the symbol's usual session.

Additionally, note that the maximum number of weeks or months in the correlation calculations depends on the chart's range and the largest time range common to all the requested symbols. To maximize the amount of data available for the calculations, we recommend setting the chart to use a daily or higher timeframe and specifying a chart symbol that covers a sufficient time range for your needs.

█ FEATURES

This indicator analyzes the correlations between several pairs of user-specified symbols to provide a structured, intuitive view of the relationships in their returns. Below are the indicator's key features:

Requesting a list of securities

The "Symbol list" text box in the indicator's "Settings/Inputs" tab accepts a comma-separated list of symbols or ticker identifiers with optional spaces (e.g., "XOM, MSFT, BITSTAMP:BTCUSD"). The indicator dynamically requests returns for each symbol in the list, then calculates the correlation between each pair of return series for its heatmap display.

Each item in the list must represent a valid symbol or ticker ID. If the list includes an invalid symbol, the script raises a runtime error.

To specify a broker/exchange for a symbol, include its name as a prefix with a colon in the "EXCHANGE:SYMBOL" format. If a symbol in the list does not specify an exchange prefix, the indicator selects the most commonly used exchange when requesting the data.

Note that the number of symbols allowed in the list depends on the user's plan. Users with non-professional plans can compare up to 20 symbols with this indicator, and users with professional plans can compare up to 32 symbols.

Timeframe and data length selection

The "Returns timeframe" input specifies whether the indicator uses weekly or monthly returns in its calculations. By default, its value is "1M", meaning the indicator analyzes monthly returns. Note that this script requires a chart timeframe lower than or equal to "1M". If the chart uses a higher timeframe, it causes a runtime error.

To customize the length of the data used in the correlation calculations, use the "Max periods" input. When enabled, the indicator limits the calculation window to the number of periods specified in the input field. Otherwise, it uses the chart's time range as the limit. The top-left corner of the table shows the number of confirmed weeks or months used in the calculations.

It's important to note that the number of confirmed periods in the correlation calculations is limited to the largest time range common to all the requested datasets, because a meaningful correlation matrix requires analyzing each symbol's returns under the same market conditions. Therefore, the correlation matrix can show different results for the same symbol pair if another listed symbol restricts the aligned data to a shorter time range.

Heatmap display

This indicator displays the correlations for each symbol pair in a heatmap-styled table representing a symmetric correlation matrix. Each row and column corresponds to a specific symbol, and the cells at their intersections correspond to symbol pairs . For example, the cell at the "AAPL" row and "MSFT" column shows the weekly or monthly correlation between those two symbols' returns. Likewise, the cell at the "MSFT" row and "AAPL" column shows the same value.

Note that the main diagonal cells in the display, where the row and column refer to the same symbol, all show a value of 1 because any series of non-na data is always perfectly correlated with itself.

The background of each correlation cell uses a gradient color based on the correlation value. By default, the gradient uses blue hues for positive correlation, orange hues for negative correlation, and white for no correlation. The intensity of each blue or orange hue corresponds to the strength of the measured correlation or anticorrelation. Users can customize the gradient's base colors using the inputs in the "Color gradient" section of the "Settings/Inputs" tab.

█ FOR Pine Script® CODERS

• This script uses the `getArrayFromString()` function from our ValueAtTime library to process the input list of symbols. The function splits the "string" value by its commas, then constructs an array of non-empty strings without leading or trailing whitespaces. Additionally, it uses the str.upper() function to convert each symbol's characters to uppercase.

• The script's `getAlignedReturns()` function requests time-aligned prices with two request.security() calls that use spread tickers based on the chart's symbol and another symbol. Then, it calculates the arithmetic return using the `changePercent()` function from the ta library. The `collectReturns()` function uses `getAlignedReturns()` within a loop and stores the data from each call within a matrix . The script calls the `arrayCorrelation()` function on pairs of rows from the returned matrix to calculate the correlation values.

• For consistency, the `getAlignedReturns()` function includes extended hours and dividend adjustment modifiers in its data requests. Additionally, it includes other settings inherited from the chart's context, such as "settlement-as-close" preferences.

• A Pine script can execute up to 40 or 64 unique `request.*()` function calls, depending on the user's plan. The maximum number of symbols this script compares is half the plan's limit, because `getAlignedReturns()` uses two request.security() calls.

• This script can use the request.security() function within a loop because all scripts in Pine v6 enable dynamic requests by default. Refer to the Dynamic requests section of the Other timeframes and data page to learn more about this feature, and see our v6 migration guide to learn what's new in Pine v6.

• The script's table uses two distinct color.from_gradient() calls in a switch structure to determine the cell colors for positive and negative correlation values. One call calculates the color for values from -1 to 0 based on the first and second input colors, and the other calculates the colors for values from 0 to 1 based on the second and third input colors.

Look first. Then leap.

BB Breakout + Momentum Squeeze [Strategy]This Strategy is Based on 3 free indicators

- Bollinger Bands Breakout Oscillator: Link

- TTM Squeeze Pro: Link

- Rolling ATR Bands: Link

Bollinger Bands Breakout Oscillator - This tool shows how strong a market trend is by measuring how often prices move outside their normal Bollinger bands range. It helps you see whether prices are strongly moving in one direction or just moving sideways. By looking at how much and how frequently prices push beyond their typical boundaries, you can identify which direction the market is heading over your selected time period.

TM Squeeze Pro - This is a custom version of the TTM Squeeze indicator.

It's designed to help traders spot consolidation phases in the market (when price is coiling or "squeezing") and to catch breakouts early when volatility returns. The logic is based on the relationship between Bollinger Bands and Keltner Channels, combined with a momentum oscillator to show direction and strength.

Rolling ATR Bands - This indicator combines volatility bands (ATR) with momentum and trend signals to show where the market might be breaking out, retesting, or trending. It's highly visual and helpful for traders looking to time entries/exits during trending or volatile moves.

Logic Of the Strategy:

We are going to use the Bollinger Bands Breakout to determine the direction of the market. Than check the Volatility of the price by looking at the TTM Squeeze indicator. And use the ATR Bands to determine dynamic Stop Losses and based on the calculate the Take Profit targets and quantity for each position dynamically.

For the Long Setup:

1. We need to see the that Bull Power (Green line of the Bollinger Bands Breakout Oscilator) is crossing the level of 50.

2. Check the presence of volatility (Green dot based on the TTM Squeeze indicator)

For the Short Setup:

1. We need to see the that Bear Power (Red line of the Bollinger Bands Breakout Oscilator) is crossing the level of 50.

2. Check the presence of volatility (Green dot based on the TTM Squeeze indicator)

Stop Loss is determined by the Lower ATR Band (for the Long entry) and Upper ATR Band (For the Short entry)

Take Profit is 1:1.5 risk reward ration, which means if the Stop loss is 1% the TP target will be 1.5%

Move stop Loss to Breakeven: If the price will go in the direction of the trade for at least half of the Risk Reward target then the stop will automatically be adjusted to the entry price. For Example: the Stop Loss is 1%, the price has move at least 0.5% in the direction of your trade and that will move the Stop Loss level to the Entry point.

You can Adjust the parameters for each indicator used in that script and also adjust the Risk and Money management block to see how the PnL will change.

Live Risk/Reward Lines (Dynamic Update: Tick or Bar Close)This script displays dynamic Risk and Reward target lines directly on the chart.

You can choose whether the updates happen live with each price tick or only once a bar closes.

It supports both long and short trading directions, with customizable risk and reward percentages.

Key Features:

Dynamic live updates (per tick or per bar close).

Choose Long or Short trade direction.

Customize risk and reward percentages individually.

Adjustable line length and color.

Option to show or hide risk and reward lines.

How It Works:

For long trades: Risk = Close Price * (1 - Risk %), Reward = Close Price * (1 + Reward %).

For short trades: Risk = Close Price * (1 + Risk %), Reward = Close Price * (1 - Reward %).

Lines are automatically centered around the current bar.

Why It Is Unique:

Unlike static risk/reward indicators, this script allows traders to see real-time dynamic changes based on the latest tick or bar close.

It offers full flexibility for scalpers and swing traders by allowing manual control over update timing and visualization style.

Usage Instructions:

Select your trade direction (Long or Short) from the settings.

Set your preferred risk and reward percentages.

Choose whether lines should update with every tick or only on bar close.

Optionally adjust the length and colors of the lines.

Important:

The script focuses on visualizing risk and reward directly on the price chart without giving buy or sell signals.

Disclaimer:

This tool is intended for educational and informational purposes only and should not be considered financial advice.

Option Contract Size CalculatorOption Contract Size Calculator

This indicator helps you to figure out the ideal number of contracts for your trade and its only used for options day trading.

The indicator needs to fill the input section in order to give you the information table that includes Contract size .

The input section consists of two sections. The first section requires user entry of the delta of the options contract from the broker chain and the stop loss size on the chart.

The second section allows you to enter your account balance and risk per trade

(2% recommended) .

There is also the option for where you wish to display your table like bottom right , bottom left or top right, top left.

special thanks to @Mohamedawke for the open source script this code is based off

Nasan Risk Score & Postion Size Estimator** THE RISK SCORE AND POSITION SIZE WILL ONLY BE CALCUTAED ON DIALY TIMEFRAME NOT IN OTHER TIMEFRAMES.

The typically accepted generic rule for risk management is not to risk more than 1% - 2 % of the capital in any given trade. It has its own basis however it does not take into account the stocks historic & current performance and does not consider the traders performance metrics (like win rate, profit ratio).

The Nasan Risk Score & Position size calculator takes into account all the listed parameters into account and estimates a Risk %. The position size is calculated using the estimated risk % , current ATR and a dynamically adjusted ATR multiple (ATR multiple is adjusted based on true range's volatility and stocks relative performance).

It follows a series of calculations:

Unadjusted Nasan Risk Score = (Min Risk)^a + b*

Min Risk = ( 5 year weighted avg Annual Stock Return - 5 year weighted avg Annual Bench Return) / 5 year weighted avg Annual Max ATR%

Max Risk = ( 5 year weighted avg Annual Stock Return - 5 year weighted avg Annual Bench Return) / 5 year weighted avg Annual Min ATR%

The min and max return is calculated based on stocks excess return in comparison to the Benchmark return and adjusted for volatility of the stock.

When a stock underperforms the benchmark, the default is, it does not calculate a position size , however if we opt it to calculate it will use 1% for Min Risk% and 2% for Max Risk% but all the other calculations and scaling remain the same.

Rationale:

Stocks outperforming their benchmark with lower volatility (ATR%) score higher.

A stock with high returns but excessive volatility gets penalized.

This ensures volatility-adjusted performance is emphasized rather than absolute returns.

Depending on the risk preference aggressive or conservative

Aggressive Risk Scaling: a = max (m, n) and b = min (m, n)

Conservative Scaling: a = min (m, n) and b = max (m, n)

where n = traders win % /100 and m = 1 - (1/ (1+ profit ratio))

A default of 50% is used for win factor and 1.5 for profit ratio.

Aggressive risk scaling increases exposure when the strategy's strongest factor is favorable.

Conservative risk scaling ensures more stable risk levels by focusing on the weaker factor.

The Unadjusted Nasan risk is score is further refined based on a tolerance factor which is based on the stocks maximum annual drawdown and the trader's maximum draw down tolerance.

Tolerance = /100

The correction factor (Tolerance) adjusts the risk score based on downside risk. Here's how it works conceptually:

The formula calculates how much the stock's actual drawdown exceeds your acceptable limit.

If stocks maximum Annual drawdown is smaller than Trader's maximum acceptable drawdown % , this results in a positive correction factor (indicating the drawdown is within your acceptable range and increases the unadjusted score.

If stocks maximum Annual drawdown exceeds Trader's maximum acceptable drawdown %, the correction factor will decrease (indicating that the downside risk is greater than what you are comfortable with, so it will adjust the risk exposure).

Once the Risk Score (numerically equal to Risk %) The position size is calculated based on the current market conditions.

Nasan Risk Score (Risk%) = Unadjusted Nasan Risk Score * Tolerance.

Position Size = (Capital * Risk% )/ ATR-Multiplier * ATR

The ATR Multiplier is dynamically adjusted based on the stocks recent relative performance and the variability of the true range itself. It would range between 1 - 3.5.

The multiplier widens when conditions are not favorable decreasing the position size and increases position size when conditions are favorable.

This Calculation /Estimate Does not give you a very different result than the arbitrary 1% - 2%. However it does fine tune the % based on sock performance, traders performance and tolerance level.

Stop/Take BoundsThe Stop/Take Bounds indicator is tool for setting dynamic stop-loss and take-profit levels based on percentage distance from the price. Unlike traditional ATR-based methods, this indicator allows traders to set stop levels as a fixed percentage of the price and define the take-profit multiple.

- Stop-loss distanceis determined as a percentage of the current price (e.g., 1% means the stop-loss is always 1% away from the price).

- Take-profit distance is calculated by multiplying the stop-loss distance by a user-defined multiplier (e.g., a multiplier of 2 places the take-profit level twice as far as the stop-loss).

- The indicator plots red lines for stop-loss levels and green lines for take-profit levels, making it easy to visualize risk-to-reward scenarios.

How to Use

1. Set Stop-Loss Distance (%) – Define how far the stop-loss should be from the price.

2. Set Take-Profit Multiplier – Choose how many times larger the take-profit should be compared to the stop-loss.

3. Apply to Long and Short Trades – The indicator automatically plots levels for both long and short positions.

4. Use in Manual or Algorithmic Trading – Ideal for discretionary traders as well as for integration into algorithmic strategies.

Use Cases

- Risk Management – Helps maintain disciplined risk-to-reward ratios.

- Strategy Development – Can be used in the creation of algorithmic trading systems.

- Trailing Stop Simulation – Can act as a trailing stop mechanism when used dynamically.

This indicator is a great addition to any trading strategy!

Breakouts With Timefilter Strategy [LuciTech]This strategy captures breakout opportunities using pivot high/low breakouts while managing risk through dynamic stop-loss placement and position sizing. It includes a time filter to limit trades to specific sessions.

How It Works

A long trade is triggered when price closes above a pivot high, and a short trade when price closes below a pivot low.

Stop-loss can be set using ATR, prior candle high/low, or a fixed point value. Take-profit is based on a risk-reward multiplier.

Position size adjusts based on the percentage of equity risked.

Breakout signals are marked with triangles, and entry, stop-loss, and take-profit levels are plotted.

moving average filter: Bullish breakouts only trigger above the MA, bearish breakouts below.

The time filter shades the background during active trading hours.

Customization:

Adjustable pivot length for breakout sensitivity.

Risk settings: percentage risked, risk-reward ratio, and stop-loss type.

ATR settings: length, smoothing method (RMA, SMA, EMA, WMA).

Moving average filter (SMA, EMA, WMA, VWMA, HMA) to confirm breakouts.

Price Action Trend and Margin EquityThe Price Action Trend and Margin Equity indicator is a multifunctional market analysis tool that combines elements of money management and price pattern analysis. The indicator helps traders identify key price action patterns and determine optimal entry, exit and stop loss levels based on the current trend.

The main components of the indicator:

Money Management:

Allows the trader to set risk management parameters such as the percentage of possible loss on the position, the use of fixed leverage and the total capital.

Calculates the required leverage level to achieve a specified percentage of loss.

Price Action:

Correctly identifies various price patterns such as Pin Bar, Engulfing Bar, PPR Bar and Inside Bar.

Displays these patterns on the chart with the ability to customize candle colors and display styles.

Allows the trader to customize take profit and stop loss points to display them on the chart.

The ability to display patterns only in the direction of the trend.

Trend: (some code taken from ChartPrime)

Uses a trend cloud to visualize the current market direction.

The trend cloud is displayed on the chart and helps traders determine whether the market is in an uptrend or a downtrend.

Alert:

Allows you to set an alert that will be triggered when the pattern is formed.

Example of use:

Let's say a trader uses the indicator to trade the crypto market. He sets the money management parameters, setting the maximum loss per position to 5% and using a fixed leverage of 1:100. The indicator automatically calculates the required position size to meet these parameters ($: on the label). Or displays the leverage (X: on the label) to achieve the required risk.

The trader receives an alert when a Pin Bar is formed. The indicator displays the entry, exit, and stop loss levels based on this pattern. The trader opens a position for the recommended amount in the direction indicated by the indicator and sets the stop loss and take profit at the recommended levels.

General Settings:

Position Loss Percentage: Sets the maximum loss percentage you are willing to take on a single position.

Use Fixed Leverage: Enables or disables the use of fixed leverage.

Fixed Leverage: Sets the fixed leverage level.

Total Equity: Specifies the total equity you are using for trading. (Required for calculation when using fixed leverage)

Turn Patterns On/Off: You can turn on or off the display of various price patterns such as Pin Bar, Outside Bar (Engulfing), Inside Bar, and PPR Bar.

Pattern Colors: Sets the colors for displaying each pattern on the chart.

Candle Color: Allows you to set a neutral color for candles that do not match the price action.

Show Lines: Allows you to turn on or off the display of labels and lines.

Line Length: Sets the length of the stop, entry, and take profit lines.

Label color: One color for all labels (configured below) or the color of the labels in the color of the candle pattern.

Pin entry: Select the entry point for the pin bar: candle head, bar close, or 50% of the candle.

Coefficients for stop and take lines.

Use trend for price action: When enabled, will show price action signals only in the direction of the trend.

Display trend cloud: Enables or disables the display of the trend cloud.

Cloud calculation period: Sets the period for which the maximum and minimum values for the cloud are calculated. The longer the period, the smoother the cloud will be.

Cloud colors: Sets the colors for uptrends and downtrends, as well as the transparency of the cloud.

The logic of the indicator:

Pin Bar is a candle with a long upper or lower shadow and a short body.

Logic: If the length of one shadow is twice the body and the opposite shadow of the candle, it is considered a Pin Bar.

An Inside Bar is a candle that is completely engulfed by the previous candle.

Logic: If the high and low of the current candle are inside the previous candle, it is an Inside Bar.

An Outside Bar or Engulfing is a candle that completely engulfs the previous candle.

Logic: If the high and low of the current candle are outside the previous candle and close outside the previous candle, it is an Outside Bar.

A PPR Bar is a candle that closes above or below the previous candle.

Logic: If the current candle closes above the high of the previous candle or below its low, it is a PPR Bar.

Stop Loss Levels: Calculated based on the specified ratios. If set to 1.0, it shows the correct stop for the pattern by pushing away from the entry point.

Take Profit Levels: Calculated based on the specified ratios.

Create a Label: The label is created at the stop loss level and contains information about the potential leverage and loss.

The formula for calculating the $ value is:

=(Total Capital x (Maximum Loss Percentage on Position/100)) / (Difference between Entry Level and Stop Loss Level × Ratio that sets the stop loss level relative to the length of the candlestick shadow × Fixed Leverage Value) .

Labels contain the following information:

The percentage of price change from the recommended entry point to the stop loss level.

Required Leverage (X: ): The amount of leverage required to achieve the specified loss percentage. (Or a fixed value if selected).

Required Capital ($: ): The amount of capital required to open a position with the specified leverage and loss percentage (only displayed when using fixed leverage).

The trend cloud identifies the maximum and minimum price values for the specified period.

The cloud value is set depending on whether the current price is equal to the high or low values.

If the current closing price is equal to the high value, the cloud is set at the low value, and vice versa.

RU

Индикатор "Price Action Trend and Margin Equity" представляет собой многофункциональный инструмент для анализа рынка, объединяющий в себе элементы управления капиталом и анализа ценовых паттернов. Индикатор помогает трейдерам идентифицировать ключевые прайс экшн паттерны и определять оптимальные уровни входа, выхода и стоп-лосс на основе текущего тренда.

Основные компоненты индикатора:

Управление капиталом:

Позволяет трейдеру задавать параметры управления рисками, такие как процент возможного убытка по позиции, использование фиксированного плеча и общий капитал.

Рассчитывает необходимый уровень плеча для достижения заданного процента убытка.

Price Action:

Правильно идентифицирует различные ценовые паттерны, такие как Pin Bar, Поглащение Бар, PPR Bar и Внутренний Бар.

Отображает эти паттерны на графике с возможностью настройки цветов свечей и стилей отображения.

Позволяет трейдеру настраивать точки тейк профита и стоп лосса для отображения их на графике.

Возможность отображения паттернов только в натправлении тренда.

Trend: (часть кода взята у ChartPrime)

Использует облако тренда для визуализации текущего направления рынка.

Облако тренда отображается на графике и помогает трейдерам определить, находится ли рынок в восходящем или нисходящем тренде.

Оповещение:

Дает возможность установить оповещение которое будет срабатывать при формировании паттерна.

Пример применения:

Предположим, трейдер использует индикатор для торговли на крипто рынке. Он настраивает параметры управления капиталом, устанавливая максимальный убыток по позиции в 5% и используя фиксированное плечо 1:100. Индикатор автоматически рассчитывает необходимый объем позиции для соблюдения этих параметров ($: на лейбле). Или отображает плечо (Х: на лейбле) для достижения необходимого риска.

Трейдер получает оповещение о формировании Pin Bar. Индикатор отображает уровни входа, выхода и стоп-лосс, основанные на этом паттерне. Трейдер открывает позицию на рекомендуемую сумму в направлении, указанном индикатором, и устанавливает стоп-лосс и тейк-профит на рекомендованных уровнях.

Общие настройки:

Процент убытка по позиции: Устанавливает максимальный процент убытка, который вы готовы понести по одной позиции.

Использовать фиксированное плечо: Включает или отключает использование фиксированного плеча.

Уровень фиксированного плеча: Задает уровень фиксированного плеча.

Общий капитал: Указывает общий капитал, который вы используете для торговли. (Необходим для расчета при использовании фиксированного плеча)

Включение/отключение паттернов: Вы можете включить или отключить отображение различных ценовых паттернов, таких как Pin Bar, Outside Bar (Поглощение), Inside Bar и PPR Bar.

Цвета паттернов: Задает цвета для отображения каждого паттерна на графике.

Цвет свечей: Позволяет задать нейтральный цвет для свечей неподходящих под прйс экшн.

Показывать линии: Позволяет включить или отключить отображение лейблов и линий.

Длинна линий: Настройка длинны линий стопа, линии входа и тейк профита.

Цвет лейбла: Один цвет для всех лейблов (настраивается ниже) или цвет лейблов в цвет паттерна свечи.

Вход в пин: Выбор точки входа для пин бара: голова свечи, точка закрытия бара или 50% свечи.

Коэффиценты для стоп и тейк линий.

Использовать тренд для прайс экшна: При включении будет показывать прайс экшн сигналы только в направлении тренда.

Отображение облака тренда: Включает или отключает отображение облака тренда.

Период расчета облака: Устанавливает период, за который рассчитываются максимальные и минимальные значения для облака. Чем больше период, тем более сглаженным будет облако.

Цвета облака: Задает цвета для восходящего и нисходящего трендов, а также прозрачность облака.

Логика работы индикатора:

Pin Bar — это свеча с длинной верхней или нижней тенью и коротким телом.

Логика: Если длина одной тени вдвое больше тела и противоположной тени свечи, считается, что это Pin Bar.

Inside Bar — это свеча, полностью поглощенная предыдущей свечой.

Логика: Если максимум и минимум текущей свечи находятся внутри предыдущей свечи, это Inside Bar.

Outside Bar или Поглощение — это свеча, которая полностью поглощает предыдущую свечу.

Логика: Если максимум и минимум текущей свечи выходят за пределы предыдущей свечи и закрывается за пределами предыдущей свечи, это Outside Bar.

PPR Bar — это свеча, которая закрывается выше или ниже предыдущей свечи.

Логика: Если текущая свеча закрывается выше максимума предыдущей свечи или ниже ее минимума, это PPR Bar.

Уровни стоп-лосс: Рассчитываются на основе заданных коэффициентов. При значении 1.0 показывает правильный стоп для паттерна отталкиваясь от точки входа.

Уровки тейк-профита: Рассчитываются на основе заданных коэффициентов.

Создание метки: Метка создается на уровне стоп-лосс и содержит информацию о потенциальном плече и убытке.

Формула для вычисления значения $:

=(Общий капитал x (Максимальный процент убытка по позиции/100)) / (Разница между уровнем входа и уровнем стоп-лосс × Коэффициент, задающий уровень стоп-лосс относительно длины тени свечи × Значение фиксированного плеча).

Метки содержат следующую информацию:

Процент изменения цены от рекомендованной точки входа до уровня стоп-лосс.

Необходимое плечо (Х: ): Уровень плеча, необходимый для достижения заданного процента убытка. (Или фиксированное значение если оно выбрано).

Необходимый капитал ($: ): Сумма капитала, необходимая для открытия позиции с заданным плечом и процентом убытка (отображается только при использовании фиксированного плеча).

Облако тренда определяет максимальные и минимальные значения цены за указанный период.

Значение облака устанавливается в зависимости от того, совпадает ли текущая цена с максимальными или минимальными значениями.

Если текущая цена закрытия равна максимальному значению, облако устанавливается на уровне минимального значения, и наоборот.

ATR stop lossPlots the stop loss level based on average true range (ATR) and a multiplier of choice (1 to 2.5, default is 1.5), subtracted from closing price.

Additions in this version:

You can now show percentage labels to help evaluate the level of risk.

The color of the plotted line and the text labels can be picked by the user.

John Bob-Trading-BotDeveloped by Ayebale John Bob with the help of his bestie, this innovative strategy combines advanced Smart Money Concepts with practical risk management tools to help traders identify and capitalize on key market moves.

Key Features:

Smart Money Concepts & Fair Value Gaps (FVG):

The strategy monitors price action for fair value gaps, which are visualized as extremely faint horizontal lines on the chart. These FVGs signal potential areas where institutional traders might have entered or exited positions.

Dynamic Entry Signals:

Buy signals are triggered when the price crosses above the 50-bar lowest low or when a bullish FVG is detected. Conversely, sell signals are generated when the price falls below the 50-bar highest high or a bearish FVG is identified. Each signal is visually marked on the chart with clear buy (green) and sell (red) labels.

Multi-Level Order Execution:

Once an entry signal occurs, the strategy places five separate orders, each with its own take-profit (TP) level. The TP levels are calculated dynamically using the Average True Range (ATR) and a set of predefined multipliers. This allows traders to scale out of positions as the market moves favorably.

Dynamic Risk Management:

A stop-loss is automatically set at a distance determined by the ATR, ensuring that risk is managed in accordance with current market volatility.

Real-Time Trade Information Table:

In the bottom-right corner of the chart, a trade information table displays essential details about the current trade:

Side: Displays "BUY NOW" (with a dark green background) for long entries or "SELL NOW" (with a dark red background) for short entries.

Entry Price & Stop-Loss: Shows the entry price (highlighted in green) and the corresponding stop-loss level (highlighted in red).

Take-Profit Levels: Lists the five TP levels, each of which turns green once the market price reaches that target.

Timer: A live timer in minutes counts from the moment the current trade trigger started, helping traders track the duration of their active trades.

Visual Progress Bar:

A histogram-style progress bar is plotted on the chart, visually representing the percentage gain (or loss) relative to the entry price.

This strategy was meticulously designed to incorporate both technical analysis and smart risk management, offering a robust trading solution that adapts to changing market conditions. Whether you're a seasoned trader or just starting out, the AyebaleJohnBob Trading Bot equips you with the tools and visual cues needed to make well-informed trading decisions. Enjoy a seamless blend of strategy and style—crafted with passion by Ayebale John Bob and his bestie!

Sharpe and Sortino Ratios with Date RangeThis indicator calculates the Sharpe and Sortino ratios using a chart symbol's periodic price returns.

I added the ability to calculate SORTINO and Sharpe based on CUSTOM DATES within the option menu.

It builds on the script here: by adding this feature.

A little about the Sortino Ratio.

www.nasdaq.com

I want equity market returns, but I don’t want equity market volatility. This is the sentiment many investors naturally feel. This sentiment often grows stronger as one approaches or is in the phase where they desire distributions from their savings to improve lifestyle. This is why there is a need for active management in the investment arena. The desire to control downside volatility, but also participate in the upside growth is a very fundamental human desire. The Sortino Ratio measures how well a particular investment meets this fundamental human desire.

There is the old adage, “volatility is the price you pay for returns.” However, what if we could measure the historical performance of an investment and see if it has given above average returns compared to the downside volatility. This is a simple division problem. It will tell us if the volatility “price we are paying for returns” is good. We can then compare that to other investments to see how they compare.

Let us take the return and subtract the risk-free interest rate and then simply divide that by the downside movement from the average. A basic division problem yielding a number that measures a very basic human desire: How well did this investment do compared to the downside risk it experienced.

In the world of financial analysis and investment management, ratios are abundant. There are many ratios that are truly important to a particular analysis. However, the sheer abundance of ratios that are available often overwhelms the casual investor, leading them to disregard ratios altogether. I would argue for those investors that desire a way to rank an investment by its ability to satisfy this very fundamental human desire, the Sortino Ratio is the number they need to consider.

Disappointing in the marketplace for research, the Sortino Ratio is not featured prominently. It is much easier to find the inflows a particular ETF has experienced than the Sortino Ratio. Inflows are important. They measure how much people are investing into an ETF. However, they are mostly only important to the fund manager, not the investor. What investors care about is the Risk-Adjusted Return. This is the Sortino Ratio.

measure last swing [keypoems]MEASURE LAST SWING

Version: v0.0.7

An indicator for measuring market swings and calculating position sizing based on pivot points and risk parameters. Helps traders visualize price swings and automatically compute position sizes based on their desired risk amount.

FEATURES:

• Identifies and tracks last pivot point in price action

• Displays visual measurements of price swing

• Calculates position sizes based on risk parameters

• Supports major futures contracts with automatic multiplier detection

HOW IT WORKS:

The indicator detects pivot highs and lows using your specified pivot strength, then draws measurement lines and calculates position sizes based on your risk parameters. It automatically cleans up old drawings when new pivot points are identified.

INPUT PARAMETERS:

General Settings:

• Risk Amount - Amount you want to risk per trade

• Pivot Strength - Bars required on either side to confirm a pivot

• Offset - Number of bars to offset the vertical line

Visual Settings:

• Horizontal and Vertical Lines - Customizable colors, widths (1-4), and styles

• Labels - Adjustable text color and size

CONTRACT MULTIPLIERS:

Automatically detects and applies the correct multiplier:

• ES (E-mini S&P 500): 50.0

• MES (Micro E-mini S&P 500): 5.0

• NQ (E-mini Nasdaq): 20.0

• MNQ (Micro E-mini Nasdaq): 2.0

• YM (E-mini Dow): 5.0

• MYM (Micro E-mini Dow): 0.5

• Other symbols: 1.0 (default)

DISPLAY ELEMENTS:

1. Horizontal line showing the level of the last pivot point

2. Vertical line measuring the distance to current price

3. Distance label showing point distance

4. Risk/Position label showing risk amount and calculated position size

POSITION SIZING:

Position Size = Floor(Risk Amount / (Distance in Points × Contract Multiplier))

IDEAL FOR:

• Measuring price swings for technical analysis

• Position sizing based on risk management rules

• Identifying potential entry and exit points

• Visual analysis of market structure

• Risk management automation

BTC Slayer 9000 - Relative Risk-adjusted performanceBTC Slayer 9000: Relative Risk-Adjusted Performance

Dear friends and fellow traders,

I am pleased to introduce the BTC Slayer 9000, a script designed to provide clear insights into risk-adjusted performance relative to a benchmark. Whether you're navigating the volatile world of cryptocurrencies or exploring opportunities in stocks, this tool helps you make informed decisions by comparing assets against your chosen benchmark.

What Does It Do?

This indicator is based on the Ulcer Index (UI), a metric that measures downside risk. It calculates the Ulcer Performance Index (UPI), which combines returns and downside risk, and compares it to a benchmark (like BTC/USDT, SPY500, or any trading pair).

The result is the Relative UPI (RUPI):

Positive RUPI (green area): The asset's risk-adjusted performance is better than the benchmark.

Negative RUPI (red area): The asset's risk-adjusted performance is worse than the benchmark.

Why Use It?

Risk vs. Reward: See if the extra risk of an asset is justified by its returns.

Customizable Benchmark: Compare any asset against BTC, SPY500, or another chart.

Dynamic Insights: Quickly identify outperforming assets for long positions and underperformers for potential shorts.

How to Use:

Inputs:

Adjust the lookback period to set the time frame for analysis. 720 Period is meant to represent 30 days. I like to use 168 period because I do not hold trades for long.

Choose your comparison chart (e.g., BTC/USDT, SPY500, AAPL, etc.).

Interpretation:

Green Area Above 0: The asset offers better risk-adjusted returns than the benchmark.

Red Area Below 0: The benchmark is a safer or more rewarding option.

Perfect for All Traders

Whether you:

Trade Cryptocurrencies: Compare altcoins to BTC.

Invest in Stocks: Compare individual stocks to indices like SPY500.

Evaluate Portfolio Options: Decide between assets like AAPL or TSLA.

This indicator equips you with a systematic way to evaluate "Is the extra risk worth it?".

The script was compiled in Collaboration with ChatGPT