BTC Slayer 9000 - Relative Risk-adjusted performanceBTC Slayer 9000: Relative Risk-Adjusted Performance

Dear friends and fellow traders,

I am pleased to introduce the BTC Slayer 9000, a script designed to provide clear insights into risk-adjusted performance relative to a benchmark. Whether you're navigating the volatile world of cryptocurrencies or exploring opportunities in stocks, this tool helps you make informed decisions by comparing assets against your chosen benchmark.

What Does It Do?

This indicator is based on the Ulcer Index (UI), a metric that measures downside risk. It calculates the Ulcer Performance Index (UPI), which combines returns and downside risk, and compares it to a benchmark (like BTC/USDT, SPY500, or any trading pair).

The result is the Relative UPI (RUPI):

Positive RUPI (green area): The asset's risk-adjusted performance is better than the benchmark.

Negative RUPI (red area): The asset's risk-adjusted performance is worse than the benchmark.

Why Use It?

Risk vs. Reward: See if the extra risk of an asset is justified by its returns.

Customizable Benchmark: Compare any asset against BTC, SPY500, or another chart.

Dynamic Insights: Quickly identify outperforming assets for long positions and underperformers for potential shorts.

How to Use:

Inputs:

Adjust the lookback period to set the time frame for analysis. 720 Period is meant to represent 30 days. I like to use 168 period because I do not hold trades for long.

Choose your comparison chart (e.g., BTC/USDT, SPY500, AAPL, etc.).

Interpretation:

Green Area Above 0: The asset offers better risk-adjusted returns than the benchmark.

Red Area Below 0: The benchmark is a safer or more rewarding option.

Perfect for All Traders

Whether you:

Trade Cryptocurrencies: Compare altcoins to BTC.

Invest in Stocks: Compare individual stocks to indices like SPY500.

Evaluate Portfolio Options: Decide between assets like AAPL or TSLA.

This indicator equips you with a systematic way to evaluate "Is the extra risk worth it?".

The script was compiled in Collaboration with ChatGPT

Riskmangement

Tomas Ratio Strategy with Multi-Timeframe AnalysisHello,

I would like to present my new indicator I have compiled together inspired by Calmar Ratio which is a ratio that measures gains vs losers but with a little twist.

Basically the idea is that if HLC3 is above HLC3 (or previous one) it will count as a gain and it will calculate the percentage of winners in last 720 hourly bars and then apply 168 hour standard deviation to the weekly average daily gains.

The idea is that you're supposed to buy if the thick blue line goes up and not buy if it goes down (signalized by the signal line). I liked that idea a lot, but I wanted to add an option to fire open and close signals. I have also added a logic that it not open more trades in relation the purple line which shows confidence in buying.

As input I recommend only adjusting the amount of points required to fire a signal. Note that the lower amount you put, the more open trades it will allow (and vice versa)

Feel free to remove that limiter if you want to. It works without it as well, this script is meant for inexperienced eye.

I will also publish a indicator script with this limiter removed and alerts added for you to test this strategy if you so choose to.

Also, I have added that the trades will enter only if price is above 720 period EMA

Disclaimer

This strategy is for educational purposes only and should not be considered financial advice. Always backtest thoroughly and adjust parameters based on your trading style and market conditions.

Made in collaboration with ChatGPT.

Lot Size & Risk Calculator (All Pairs)this indicator is designed to simplify and optimize risk management. It automatically calculates the ideal lot size based on your account balance, risk percentage, and defined entry and exit levels. Additionally, it includes visual tools to represent stop-loss (SL) and take-profit (TP) levels, helping you trade with precision and consistency.

WHAT IS THIS INDICATOR FOR?

This indicator is essential for traders who want to:

Maintain consistent risk in their trades.

Quickly calculate lot sizes for Forex, XAUUSD, BTCUSD, and US100.

Visualize key levels (Entry, SL, and TP) on the chart.

Monitor potential losses and gains in real time.

COMPATIBLE ASSETS

The Lot Size Calculator works with the following assets:

Forex: Standard currency pairs.

XAUUSD: Gold versus the US dollar.

BTCUSD: Bitcoin versus the US dollar.

US100: Nasdaq 100 index.

Calculations adjust automatically based on the selected asset.

TAKE-PROFIT (TP) LEVELS

The indicator allows you to define up to three take-profit levels:

TP1

TP2

TP3

.

Each level is configurable based on your exit strategy.

DASHBOARD

The dashboard is a visual tool that consolidates key information about your trade:

Account balance: Total amount available in your account.

Lot size: Calculated based on your risk and parameters.

Potential loss (SL): Amount you could lose if the price hits your stop-loss.

Potential gain (TP): Expected profit if the take-profit level is reached.

SETTINGS

The indicator offers multiple configurable options to adapt to your trading style:

Levels

Entry: Initial trade price.

Stop-Loss (SL): Maximum allowed loss level.

Take-Profit (TP): Up to three configurable levels.

Risk Management

Account balance ($): Enter your total available balance.

Risk percentage: Define how much you're willing to risk per trade

.

Visual Options

Visualization style: Choose between simple lines or visual fills.

Colors: Customize the colors of lines and labels.

Dashboard Settings

Statistics: Enable or disable key data display.

Size and position: Adjust the dashboard's size and location on the chart.

HOW TO CHANGE AN ENTRY?

Open the indicator settings in TradingView and entering the new data manually

Removing and re-adding the indicator to the chart

Multi Fibonacci Supertrend with Signals【FIbonacciFlux】Multi Fibonacci Supertrend with Signals (MFSS)

Overview

The Multi Fibonacci Supertrend with Signals (MFSS) is an advanced technical analysis tool that combines multiple Supertrend indicators using Fibonacci ratios to identify trend directions and potential trading opportunities.

Key Features

1. Fibonacci-Based Supertrend Levels

* Factor 1 (Weak) : 0.618 - The golden ratio

* Factor 2 (Medium) : 1.618 - The Fibonacci ratio

* Factor 3 (Strong) : 2.618 - The extension ratio

2. Visual Components

* Multi-layered Trend Lines

* Different line weights for easy identification

* Progressive transparency from Factor 1 to Factor 3

* Color-coded trend directions (Green for bullish, Red for bearish)

* Dynamic Fill Areas

* Gradient fills between price and trend lines

* Visual representation of trend strength

* Automatic color adjustment based on trend direction

* Signal Indicators

* Clear BUY/SELL labels on chart

* Position-adaptive signal placement

* High-visibility color scheme

3. Signal Generation Logic

The system generates signals based on two key conditions:

* Primary Condition :

* BUY : Price crossunder Supertrend2 (Factor 1.618)

* SELL : Price crossover Supertrend2 (Factor 1.618)

* Confirmation Filter :

* Signals only trigger when Supertrend3 confirms the trend direction

* Reduces false signals in volatile markets

Technical Details

Input Parameters

* ATR Period : 10 (default)

* Customizable for different market conditions

* Affects sensitivity of all Supertrend levels

* Factor Settings :

* All factors are customizable

* Default values based on Fibonacci sequence

* Minimum value: 0.01

* Step size: 0.01

Alert System

* Built-in alert conditions

* Customizable alert messages

* Real-time notification support

Use Cases

* Trend Trading

* Identify strong trend directions

* Filter out weak signals

* Confirm trend continuations

* Risk Management

* Multiple trend levels for stop-loss placement

* Clear entry and exit signals

* Trend strength visualization

* Market Analysis

* Multi-timeframe analysis capability

* Trend strength assessment

* Market structure identification

Benefits

* Reliability

* Based on proven Supertrend algorithm

* Enhanced with Fibonacci mathematics

* Multiple confirmation levels

* Clarity

* Clear visual signals

* Easy-to-interpret interface

* Reduced noise in signal generation

* Flexibility

* Customizable parameters

* Adaptable to different markets

* Suitable for various trading styles

Performance Considerations

* Optimized code structure

* Efficient calculation methods

* Minimal resource usage

Installation and Usage

Setup

* Add indicator to chart

* Adjust parameters if needed

* Enable alerts as required

Best Practices

* Use with other confirmation tools

* Adjust factors based on market volatility

* Consider timeframe appropriateness

Backtesting Results and Strategy Performance

This indicator is specifically designed for pullback trading with optimized risk-reward ratios in trend-following strategies. Below are the detailed backtesting results from our proprietary strategy implementation:

BTCUSDT Performance (Binance)

* Test Period: Approximately 7 years

* Risk-Reward Ratio: 2:1

* Take Profit: 8%

* Stop Loss: 4%

Key Metrics (BTCUSDT):

* Net Profit: +2,579%

* Total Trades: 551

* Win Rate: 44.8%

* Profit Factor: 1.278

* Maximum Drawdown: 42.86%

ETHUSD Performance (Binance)

* Risk-Reward Ratio: 4.33:1

* Take Profit: 13%

* Stop Loss: 3%

Key Metrics (ETHUSD):

* Net Profit: +8,563%

* Total Trades: 581

* Win Rate: 32%

* Profit Factor: 1.32

* Maximum Drawdown: 55%

Strategy Highlights:

* Optimized for pullback trading in strong trends

* Focus on high risk-reward ratios

* Proven effectiveness in major cryptocurrency pairs

* Consistent performance across different market conditions

* Robust profit factor despite moderate win rates

Note: These results are from our proprietary strategy implementation and should be used as reference only. Individual results may vary based on market conditions and implementation.

Important Considerations:

* The strategy demonstrates strong profitability despite lower win rates, emphasizing the importance of proper risk-reward ratios

* Higher drawdowns are compensated by significant overall returns

* The system shows adaptability across different cryptocurrencies with consistent profit factors

* Results suggest optimal performance in volatile crypto markets

Real Trading Examples

BTCUSDT 4-Hour Chart Analysis

Example of pullback strategy implementation on Bitcoin, showing clear trend definition and entry points

ETHUSDT 4-Hour Chart Analysis

Ethereum chart demonstrating effective signal generation during strong trends

BTCUSDT Detailed Signal Example (15-Minute Scalping)

Close-up view of signal generation and trend confirmation process on 15-minute timeframe, demonstrating the indicator's effectiveness for scalping operations

Chart Analysis Notes:

* Green and red zones clearly indicate trend direction

* Multiple timeframe confirmation visible through different Supertrend levels

* Clear entry signals during pullbacks in established trends

* Precise stop-loss placement opportunities below support levels

Implementation Guidelines:

* Wait for main trend confirmation from Factor 3 (2.618)

* Enter trades on pullbacks to Factor 2 (1.618)

* Use Factor 1 (0.618) for fine-tuning entry points

* Place stops below the relevant Supertrend level

Footnotes:

* Charts provided are from Binance exchange, using both 4-hour and 15-minute timeframes

* Trading view screenshots captured during actual market conditions

* Indicators shown: Multi Fibonacci Supertrend with all three factors

* Time period: Recent market activity showing various market conditions

Important Notice:

These charts are for educational purposes only. Past performance does not guarantee future results. Always conduct your own analysis and risk management.

Disclaimer

This indicator is for informational purposes only. Past performance is not indicative of future results. Always conduct proper risk management and due diligence.

License

Open source under MIT License

Author's Note

Contributions and suggestions for improvement are welcome. Please feel free to fork and enhance.

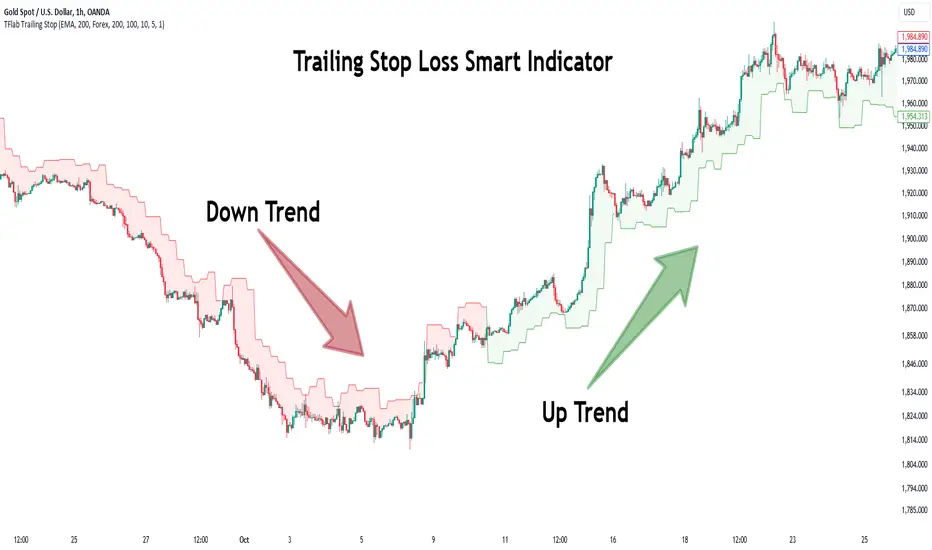

Trailing Stop Loss Smart [TradingFinder] Market Trend + CVD/EMA🔵 Introduction

Trailing Stop Loss (TSL) is one of the most powerful tools available. A Trailing Stop Loss is a modification of a typical stop order that adjusts dynamically based on market price movement. It can be set at a defined percentage or dollar amount away from the security's current market price, making it a flexible tool for locking in profits while minimizing risk. Unlike standard stop-loss orders, a Trailing Stop follows the market in the direction of the trade, protecting gains without requiring constant manual adjustments.

The Trailing Stop Loss Smart (TFlab Trailing Stop) indicator takes this concept even further by incorporating advanced metrics like Cumulative Volume Delta (CVD), volume dynamics, and Average True Range (ATR). This combination not only enhances risk management but also acts as a trend identifier, providing traders with a powerful tool to capitalize on both short-term and long-term price movements.

This indicator also supports various Order Types, allowing for flexible strategies that include a trailing stop/stop-loss combo to maximize winning trades while minimizing losses. The trailing stop limit is particularly useful for traders who want to set their stop at a precise level relative to the current market price, either by a percentage or a dollar amount. The Trailing Stop Loss Smart indicator can help ensure that traders do not exit too early during trends, while the stop-loss feature kicks in during reversals.

The advantages of using a Trailing Stop Loss are its ability to protect profits and reduce the emotional decision-making process in volatile markets. However, like all trading strategies, it has disadvantages, such as the risk of triggering too early during normal market fluctuations. By understanding how the Trailing Stop Loss Smart indicator integrates features like CVD, ATR, and volume analysis, traders can leverage its full potential while navigating these pros and cons.

With its unique ability to track market movements and trends using Cumulative Volume Delta, volume dynamics, and ATR-based trailing stops, this indicator offers a complete solution for traders looking to secure profits while minimizing downside risk. Whether you're employing a simple trailing stop or a trailing stop/stop-loss combo, this tool provides all the flexibility and precision needed to execute winning trades in various markets, including Forex, Crypto, and Stock.

🔵 How to Use

The Trailing Stop Loss Smart indicator integrates multiple advanced components to provide traders with superior risk management and trend identification.

Here’s how each part of the logic works :

🟣 Cumulative Volume Delta (CVD) Logic

The CVD tracks buying and selling pressure by calculating the difference between upward and downward price movements. When there’s more buying pressure, the CVD is positive, indicating a potential bullish trend. Conversely, more selling pressure results in a negative CVD, pointing to a bearish trend.

CVD Trend Detection : The indicator determines whether the market is in a bullish or bearish phase by comparing the CVD to its moving average. A bullish trend is confirmed when the CVD is above its moving average and the price is closing higher.

A bearish trend occurs when the CVD is below its moving average and the price is closing lower. This trend detection is critical for determining whether the trailing stop should be placed below the price (bullish) or above it (bearish).

🟣 Volume Dynamics

Volume is a key factor in identifying market strength. The Trailing Stop Loss Smart indicator pulls volume data based on the market selected (Forex, Crypto, or Stock) and adjusts the trailing stop based on whether the market is experiencing high volume or low volume.

High Volume : When the current volume exceeds the average volume, the market is in a high-volume state. During these conditions, the trailing stop is placed closer to the price, as high volume often indicates strong trends with less chance of reversals.

Low Volume : In low-volume conditions, the trailing stop gives the market more room to breathe by placing the stop further away from the price. This prevents premature stop-outs in periods of reduced market activity.

🟣 ATR-Based Trailing Stop

The Average True Range (ATR) is used to measure market volatility. The Trailing Stop Loss Smart uses the ATR to dynamically adjust the stop-loss distance.

Bullish Market : When a bullish trend is detected, the trailing stop is placed below the lowest price of the recent bars (determined by the Bar Back parameter), and adjusted by the ATR Multiplier. This allows for tighter protection during strong bullish trends.

Bearish Market : When the market is bearish, the trailing stop is placed above the highest price of recent bars, also adjusted by the ATR Multiplier. This ensures that short positions are safeguarded against sudden reversals.

🟣 Dynamic Stop-Loss Updates

The trailing stop is updated every few bars (according to the Refiner parameter), ensuring it remains relevant to the most recent price action and volume changes. This dynamic feature ensures the stop-loss adapts to both trending and volatile market conditions, without requiring manual intervention.

High Volume with Trends : In periods of high volume and a confirmed trend, the stop-loss is positioned tightly to lock in profits while minimizing the risk of reversal.

Low Volume with Trends : In low-volume conditions, the stop-loss is placed further from the price, allowing the market to move freely without triggering premature exits.

🟣 Visual Representation

The indicator visually represents the trailing stop on the chart, with green lines indicating bullish trends and red lines for bearish trends. This visual aid helps traders quickly assess the state of the market and the position of their trailing stop in real-time.

🔵 Settings

The Trailing Stop Loss Smart indicator offers several customizable settings to suit various trading strategies. Understanding these inputs is key to optimizing the tool for your specific trading style.

🟣 General Settings

Cumulative Mode : This controls how the CVD is calculated.

You can choose between :

EMA : Exponential Moving Average smoothing.

Periodic : Sums the delta over a fixed period.

CVD Period : Defines the look-back period for CVD calculation. A longer period smooths the data, making it less sensitive to short-term fluctuations.

Ultra Data : This Boolean input aggregates volume across multiple exchanges for a more comprehensive view of market activity.

Market Ultra Data : Select between Forex, Crypto, and Stock to ensure the indicator pulls accurate volume data for your market.

🟣 Logical Settings

Moving Average CVD Period : Defines the period for the moving average of the CVD. A longer period smooths the trend, reducing noise.

Moving Average Volume Period : Sets the period for the moving average used to distinguish between high and low volume conditions.

Level Finder Bar Back : Determines how many bars to look back when identifying the highest or lowest price for trailing stop placement.

Levels update per candles : Sets how often (in bars) the trailing stop should be updated to remain in sync with market movements.

ATR On : Toggles the use of ATR to adjust the trailing stop based on volatility.

ATR Multiplie r: Defines how far the stop is placed from the price based on the ATR. A larger multiplier increases the stop distance, reducing the likelihood of getting stopped out during market fluctuations.

ATR Multiplier Adjusts the distance of the trailing stop based on the ATR. A higher multiplier places the stop further from the price, providing more breathing room in volatile markets.

🔵 Conclusion

The Trailing Stop Loss Smart indicator is a comprehensive tool for traders looking to manage risk while identifying market trends. By incorporating Cumulative Volume Delta (CVD) to detect buying and selling pressure, volume dynamics to gauge market activity, and ATR to adjust for volatility, this indicator ensures that stop-loss levels are both adaptive and protective.

Whether you’re trading in Forex, Crypto, or Stock markets, the Trailing Stop Loss Smart allows you to capitalize on trends while dynamically adjusting to changing market conditions. Its ability to distinguish between high-volume and low-volume periods ensures that you’re not stopped out prematurely during periods of consolidation or market hesitation.

By providing real-time visual feedback, dynamic adjustments, and trend identification, this indicator serves as a vital tool for traders aiming to maximize profits while minimizing risk. Its versatility and adaptability make it an essential part of any trader’s toolkit, helping you stay ahead in fast-moving markets while safeguarding your positions.

Risk Manage Position SizerThis is a risk management tool for traders. It calculates position sizes based on account balance and risk tolerance, and provides automated stop-loss suggestions. The script displays key information in a small table on the chart and plots important price levels.

How to use it:

Input Parameters:

Account Size: Enter your total trading account balance.

Risk Percentage: Set the percentage of your account you're willing to risk per trade.

Use Custom Stop Loss: Toggle this to use a manually entered stop loss price.

Custom Stop Loss Price: If enabled, enter your desired stop loss price.

Reading the Table:

The table displays:

Current Price

Stop Loss Price

Total Position Size (number of shares/contracts to trade)

1/3 Position Size (for scaling in/out)

Auto Stop 1, 2, and 3 (suggested stop loss levels)

Chart Indicators:

Red Line: Your stop loss level

Green Line: Auto Stop 1 (33% of range from entry to stop)

Yellow Line: Auto Stop 2 (67% of range)

Red Line: Auto Stop 3 (final stop, same as initial stop loss)

Trading Application:

Use the Total Position Size to determine how many shares/contracts to trade.

Consider using the 1/3 Position Size for scaling in or out of trades.

Use the Auto Stops to manage your risk as the trade progresses.

Customization:

Adjust the input parameters to fit your trading style and risk tolerance.

The script can be modified to add more features or change the calculation methods if needed.

This tool helps traders make more informed decisions about position sizing and stop placement, potentially improving risk management in their trading strategy. Remember, while this script provides suggestions, all trading decisions should be made based on your own analysis and risk tolerance.

Asymmetric volatilityThe "Asymmetric Volatility" indicator is designed to visualize the differences in volatility between upward and downward price movements of a selected instrument. It operates on the principle of analyzing price movements over a specified time period, with particular focus on the symmetrical evaluation of both price rises and falls.

User Parameters:

- Length: This parameter specifies the number of bars (candles) used to calculate the average volatility. The larger the value, the longer the time period, and the smoother the volatility data will be.

- Source: This represents the input data for the indicator calculations. By default, the close value of each bar is used, but the user can choose another data source (such as open, high, low, or any custom value).

Operational Algorithm:

1. Movement Calculation:

- UpMoves: Computed as the positive difference between the current bar value and the previous bar value, if it is greater than zero.

- DownMoves: Computed as the positive difference between the previous bar value and the current bar value, if it is greater than zero.

2. Volatility Calculation:

- UpVolatility: This is the arithmetic mean of the UpMoves values over the specified period.

- DownVolatility: This is the arithmetic mean of the DownMoves values over the specified period.

3. Graphical Representation:

- The indicator displays two plots: upward and downward volatility, represented by green and red lines, respectively.

- The background color changes based on which volatility is dominant: a green background indicates that upward volatility prevails, while a red background indicates downward volatility.

The indicator allows traders to quickly assess in which direction the market is more volatile at the moment, which can be useful for making trading decisions and evaluating the current market situation.

Multi-Step Vegas SuperTrend - strategy [presentTrading]Long time no see! I am back : ) Please allow me to gain some warm-up.

█ Introduction and How it is Different

The "Vegas SuperTrend Strategy" is an enhanced trading strategy that leverages both the Vegas Channel and SuperTrend indicators to generate buy and sell signals.

What sets this strategy apart from others is its dynamic adjustment to market volatility and its multi-step take profit mechanism. Unlike traditional single-step profit-taking approaches, this strategy allows traders to systematically scale out of positions at predefined profit levels, thereby optimizing their risk-reward ratio and maximizing potential gains.

BTCUSD 6hr performance

█ Strategy, How it Works: Detailed Explanation

The Vegas SuperTrend Strategy combines the strengths of the Vegas Channel and SuperTrend indicators to identify market trends and generate trade signals. The following subsections delve into the details of how each component works and how they are integrated.

🔶 Vegas Channel Calculation

The Vegas Channel is based on a simple moving average (SMA) and the standard deviation (STD) of the closing prices over a specified period. The channel is defined by upper and lower bounds that are dynamically adjusted based on market volatility.

Simple Moving Average (SMA):

SMA_vegas = (1/N) * Σ(Close_i) for i = 0 to N-1

where N is the length of the Vegas Window.

Standard Deviation (STD):

STD_vegas = sqrt((1/N) * Σ(Close_i - SMA_vegas)^2) for i = 0 to N-1

Vegas Channel Upper and Lower Bounds:

VegasChannelUpper = SMA_vegas + STD_vegas

VegasChannelLower = SMA_vegas - STD_vegas

The details are here:

🔶 Trend Detection and Trade Signals

The strategy determines the current market trend based on the closing price relative to the SuperTrend bounds:

Market Trend:

MarketTrend = 1 if Close > SuperTrendPrevLower

-1 if Close < SuperTrendPrevUpper

Previous Trend otherwise

Trade signals are generated when there is a shift in the market trend:

Bullish Signal: When the market trend shifts from -1 to 1.

Bearish Signal: When the market trend shifts from 1 to -1.

🔶 Multi-Step Take Profit Mechanism

The strategy incorporates a multi-step take profit mechanism that allows for partial exits at predefined profit levels. This helps in locking in profits gradually and reducing exposure to market reversals.

Take Profit Levels:

The take profit levels are calculated as percentages of the entry price:

TakeProfitLevel_i = EntryPrice * (1 + TakeProfitPercent_i/100) for long positions

TakeProfitLevel_i = EntryPrice * (1 - TakeProfitPercent_i/100) for short positions

Multi-steps take profit local picture:

█ Trade Direction

The trade direction can be customized based on the user's preference:

Long: The strategy only takes long positions.

Short: The strategy only takes short positions.

Both: The strategy can take both long and short positions based on the market trend.

█ Usage

To use the Vegas SuperTrend Strategy, follow these steps:

Configure Input Settings:

- Set the ATR period, Vegas Window length, SuperTrend Multiplier, and Volatility Adjustment Factor.

- Choose the desired trade direction (Long, Short, Both).

- Enable or disable the take profit mechanism and set the take profit percentages and amounts for each step.

█ Default Settings

The default settings of the strategy are designed to provide a balanced approach to trading. Below is an explanation of each setting and its effect on the strategy's performance:

ATR Period (10): This setting determines the length of the ATR used in the SuperTrend calculation. A longer period smoothens the ATR, making the SuperTrend less sensitive to short-term volatility. A shorter period makes the SuperTrend more responsive to recent price movements.

Vegas Window Length (100): This setting defines the period for the Vegas Channel's moving average. A longer window provides a broader view of the market trend, while a shorter window makes the channel more responsive to recent price changes.

SuperTrend Multiplier (5): This base multiplier adjusts the sensitivity of the SuperTrend to the ATR. A higher multiplier makes the SuperTrend less sensitive, reducing the frequency of trade signals. A lower multiplier increases sensitivity, generating more signals.

Volatility Adjustment Factor (5): This factor dynamically adjusts the SuperTrend multiplier based on the width of the Vegas Channel. A higher factor increases the sensitivity of the SuperTrend to changes in market volatility, while a lower factor reduces it.

Take Profit Percentages (3.0%, 6.0%, 12.0%, 21.0%): These settings define the profit levels at which portions of the trade are exited. They help in locking in profits progressively as the trade moves in favor.

Take Profit Amounts (25%, 20%, 10%, 15%): These settings determine the percentage of the position to exit at each take profit level. They are distributed to ensure that significant portions of the trade are closed as the price reaches the set levels, reducing exposure to reversals.

Adjusting these settings can significantly impact the strategy's performance. For instance, increasing the ATR period or the SuperTrend multiplier can reduce the number of trades, potentially improving the win rate but also missing out on some profitable opportunities. Conversely, lowering these values can increase trade frequency, capturing more short-term movements but also increasing the risk of false signals.

ADR (Log Scale) with MTF LabelsHere's a detailed presentation of the Average Daily Range (ADR) indicator, with a focus on its advantages compared to the classic ADR, its unique features, utility, and interpretation:

Advantages Compared to Classic ADR

1. Logarithmic Scale: Unlike the classic ADR, which uses a linear scale, this version uses a logarithmic scale for calculations. This approach provides a more accurate representation of relative price movements, especially for assets with large price ranges.

2. Multi-Timeframe Analysis: This enhanced ADR indicator allows traders to view daily, weekly, and monthly ADRs simultaneously. This multi-timeframe capability helps traders understand volatility trends over different periods, offering a more comprehensive market analysis.

3. Optional Smoothing: The inclusion of an optional smoothing feature (using Exponential Moving Average, EMA) helps reduce noise in the data. This makes the indicator more reliable by filtering out short-term fluctuations and highlighting the underlying volatility trend.

4. Information Display Labels: The indicator includes labels that display precise ADR values for each timeframe directly on the chart. This feature provides immediate, clear insights without requiring additional calculations or references.

Utility of the Indicator

1. Volatility Analysis: The ADR indicator is essential for assessing market volatility. By showing the average daily price range, it helps traders gauge how much an asset typically moves within a day, week, or month.

2. Risk Management: ADR levels can be used to set stop-loss points, improving risk management strategies. Knowing the average range helps traders avoid setting stops too close to the current price, which might otherwise be triggered by normal market fluctuations.

3. Setting Realistic Targets: By understanding the average daily range, traders can set more realistic profit targets. This helps in avoiding over-ambitious goals that are unlikely to be reached within the typical market movement.

4. Identifying Entry and Exit Points: The ADR can signal potential entry and exit points. For example, if the price approaches the upper or lower ADR boundary, it might indicate an overbought or oversold condition, respectively.

Interpretation and Examples

1. Increasing Volatility: If the ADR is increasing, it indicates rising market volatility. Traders might adjust their strategies accordingly, such as widening their stop-losses to accommodate larger price swings.

2. Range Breakout: If the price significantly exceeds the daily ADR, it may signal a strong trend or exceptional market movement. Traders can use this information to stay in the trade longer or to anticipate a potential reversal.

3. Mean Reversion: Prices often revert to the ADR mean. A trader might consider mean reversion trades when the price approaches the extremes of the ADR range, expecting it to move back towards the average.

4. Multi-Timeframe Comparison: If the daily ADR is higher than the weekly ADR, it may indicate unusually high short-term volatility. This can be a signal for traders to be cautious or to capitalize on the increased movement.

While the ADR indicator provides valuable insights into market volatility and can significantly enhance trading strategies, it is essential to remember that no indicator is foolproof. Market conditions can change rapidly, and past performance is not always indicative of future results. Traders should use the ADR indicator in conjunction with other tools and follow sound risk management practices to protect their capital.

[SGM Geometric Brownian Motion]Description:

This indicator uses Geometric Brownian Motion (GBM) simulations to predict possible price trajectories of a financial asset. It helps traders visualize potential price movements, assess risks, and make informed decisions.

Geometric Brownian Motion:

Geometric Brownian Motion is an extension of standard Brownian motion (or Wiener process) used to model the random behavior of particles in physics. In finance, this concept is used to model the evolution of asset prices over time in a continuous manner. The basic idea is that the price of an asset does not only change randomly but also exponentially depending on certain parameters.

Basic formula

The formula for the evolution of the price of an asset S(t) under MBG is given by the following stochastic differential equation:

𝑑𝑆(𝑡) = 𝜇𝑆(𝑡)𝑑𝑡 + 𝜎𝑆(𝑡)𝑑𝑊(𝑡)

where:

S(t) is the price of the asset at time

μ is the expected growth rate (or drift).

σ is the volatility of the price of the asset.

dW(t) represents the noise term, i.e. the standard Brownian motion.

Explanations of the terms

Expected growth rate (μ):

This is the expected average return on the asset. If you think your asset will grow by 5% per year,

μ will be 0.05.

Volatility (σ):

It is a measure of the uncertainty or risk associated with the asset. If the asset price varies a lot, σ will be high.

Noise term (dW(t)):

It represents the randomness of the price change, modeled by a Wiener process.

Features:

Customizable number of simulations: Choose the number of price trajectories to simulate to get a better estimate of future movements.

Adjustable simulation length: Set the duration of the simulations in number of periods to adapt the indicator to your trading horizons.

Trajectory display: Visualize the simulated price trajectories directly on the chart to better understand possible future scenarios.

Dispersion calculations: Display the distribution of simulated final prices to assess dispersion and potential variations.

Sharpe ratio distribution: Analyze the risk-adjusted performance of simulations using the Sharpe ratio distribution.

Risk Statistics: Get key risk metrics like maximum drawdown, average return, and Value at Risk (VaR) at different confidence levels.

User Inputs:

Number of Simulations: 200 by default.

Simulation Length: 10 periods by default.

Brownian Motion Transparency: Adjust the transparency of simulated lines for better visualization.

Brownian Motion Display: Enable or disable the display of simulated paths.

Brownian Dispersion Display: Display the distribution of simulated final prices.

Sharpe Dispersion Display: Display the distribution of Sharpe ratios.

Customizable Colors: Choose colors for lines and tables.

Usage:

Configure Settings: Adjust the number of simulations, simulation length, and display preferences to suit your needs.

Analyze Simulated Paths: Simulated path lines appear on the chart, representing possible price developments.

Review Dispersion Charts: Review the charts to understand the distribution of final prices and Sharpe ratios, as well as key risk statistics. This indicator is ideal for traders looking to anticipate future price movements and assess the associated risks. With its detailed simulations and dispersion analyses, it provides valuable insight into the financial markets.

Strategic Multi-Step Supertrend - Strategy [presentTrading]The code is mainly developed for me to stimulate the multi-step taking profit function for strategies. The result shows the drawdown can be reduced but at the same time reduced the profit as well. It can be a heuristic for futures leverage traders.

█ Introduction and How it is Different

The "Strategic Multi-Step Supertrend" is a trading strategy designed to leverage the power of multiple steps to optimize trade entries and exits across the Supertrend indicator. Unlike traditional strategies that rely on single entry and exit points, this strategy employs a multi-step approach to take profit, allowing traders to lock in gains incrementally. Additionally, the strategy is adaptable to both long and short trades, providing a comprehensive solution for dynamic market conditions.

This template strategy lies in its dual Supertrend calculation, which enhances the accuracy of trend detection and provides more reliable signals for trade entries and exits. This approach minimizes false signals and increases the overall profitability of trades by ensuring that positions are entered and exited at optimal points.

BTC 6h L/S Performance

█ Strategy, How It Works: Detailed Explanation

The "Strategic Multi-Step Supertrend Trader" strategy utilizes two Supertrend indicators calculated with different parameters to determine the direction and strength of the market trend. This dual approach increases the robustness of the signals, reducing the likelihood of entering trades based on false signals. Here is a detailed breakdown of how the strategy operates:

🔶 Supertrend Indicator Calculation

The Supertrend indicator is a trend-following overlay on the price chart, typically used to identify the direction of the trend. It is calculated using the Average True Range (ATR) to ensure that the indicator adapts to market volatility. The formula for the Supertrend indicator is:

Upper Band = (High + Low) / 2 + (Factor * ATR)

Lower Band = (High + Low) / 2 - (Factor * ATR)

Where:

- High and Low are the highest and lowest prices of the period.

- Factor is a user-defined multiplier.

- ATR is the Average True Range over a specified period.

The Supertrend changes its direction based on the closing price in relation to these bands.

🔶 Entry-Exit Conditions

The strategy enters long positions when both Supertrend indicators signal an uptrend, and short positions when both indicate a downtrend. Specifically:

- Long Condition: Supertrend1 < 0 and Supertrend2 < 0

- Short Condition: Supertrend1 > 0 and Supertrend2 > 0

- Long Exit Condition: Supertrend1 > 0 and Supertrend2 > 0

- Short Exit Condition: Supertrend1 < 0 and Supertrend2 < 0

🔶 Multi-Step Take Profit Mechanism

The strategy features a multi-step take profit mechanism, which allows traders to lock in profits incrementally. This is achieved through four user-configurable take profit levels. For each level, the strategy specifies a percentage increase (for long trades) or decrease (for short trades) in the entry price at which a portion of the position is exited:

- Step 1: Exit a portion of the trade at Entry Price * (1 + Take Profit Percent1 / 100)

- Step 2: Exit a portion of the trade at Entry Price * (1 + Take Profit Percent2 / 100)

- Step 3: Exit a portion of the trade at Entry Price * (1 + Take Profit Percent3 / 100)

- Step 4: Exit a portion of the trade at Entry Price * (1 + Take Profit Percent4 / 100)

This staggered exit strategy helps in locking profits at multiple levels, thereby reducing risk and increasing the likelihood of capturing the maximum possible profit from a trend.

BTC Local

█ Trade Direction

The strategy is highly flexible, allowing users to specify the trade direction. There are three options available:

- Long Only: The strategy will only enter long trades.

- Short Only: The strategy will only enter short trades.

- Both: The strategy will enter both long and short trades based on the Supertrend signals.

This flexibility allows traders to adapt the strategy to various market conditions and their own trading preferences.

█ Usage

1. Add the strategy to your trading platform and apply it to the desired chart.

2. Configure the take profit settings under the "Take Profit Settings" group.

3. Set the trade direction under the "Trade Direction" group.

4. Adjust the Supertrend settings in the "Supertrend Settings" group to fine-tune the indicator calculations.

5. Monitor the chart for entry and exit signals as indicated by the strategy.

█ Default Settings

- Use Take Profit: True

- Take Profit Percentages: Step 1 - 6%, Step 2 - 12%, Step 3 - 18%, Step 4 - 50%

- Take Profit Amounts: Step 1 - 12%, Step 2 - 8%, Step 3 - 4%, Step 4 - 0%

- Number of Take Profit Steps: 3

- Trade Direction: Both

- Supertrend Settings: ATR Length 1 - 10, Factor 1 - 3.0, ATR Length 2 - 11, Factor 2 - 4.0

These settings provide a balanced starting point, which can be customized further based on individual trading preferences and market conditions.

RiskMetrics█ OVERVIEW

This library is a tool for Pine programmers that provides functions for calculating risk-adjusted performance metrics on periodic price returns. The calculations used by this library's functions closely mirror those the Broker Emulator uses to calculate strategy performance metrics (e.g., Sharpe and Sortino ratios) without depending on strategy-specific functionality.

█ CONCEPTS

Returns, risk, and volatility

The return on an investment is the relative gain or loss over a period, often expressed as a percentage. Investment returns can originate from several sources, including capital gains, dividends, and interest income. Many investors seek the highest returns possible in the quest for profit. However, prudent investing and trading entails evaluating such returns against the associated risks (i.e., the uncertainty of returns and the potential for financial losses) for a clearer perspective on overall performance and sustainability.

One way investors and analysts assess the risk of an investment is by analyzing its volatility , i.e., the statistical dispersion of historical returns. Investors often use volatility in risk estimation because it provides a quantifiable way to gauge the expected extent of fluctuation in returns. Elevated volatility implies heightened uncertainty in the market, which suggests higher expected risk. Conversely, low volatility implies relatively stable returns with relatively minimal fluctuations, thus suggesting lower expected risk. Several risk-adjusted performance metrics utilize volatility in their calculations for this reason.

Risk-free rate

The risk-free rate represents the rate of return on a hypothetical investment carrying no risk of financial loss. This theoretical rate provides a benchmark for comparing the returns on a risky investment and evaluating whether its excess returns justify the risks. If an investment's returns are at or below the theoretical risk-free rate or the risk premium is below a desired amount, it may suggest that the returns do not compensate for the extra risk, which might be a call to reassess the investment.

Since the risk-free rate is a theoretical concept, investors often utilize proxies for the rate in practice, such as Treasury bills and other government bonds. Conventionally, analysts consider such instruments "risk-free" for a domestic holder, as they are a form of government obligation with a low perceived likelihood of default.

The average yield on short-term Treasury bills, influenced by economic conditions, monetary policies, and inflation expectations, has historically hovered around 2-3% over the long term. This range also aligns with central banks' inflation targets. As such, one may interpret a value within this range as a minimum proxy for the risk-free rate, as it may correspond to the minimum rate required to maintain purchasing power over time.

The built-in Sharpe and Sortino ratios that strategies calculate and display in the Performance Summary tab use a default risk-free rate of 2%, and the metrics in this library's example code use the same default rate. Users can adjust this value to fit their analysis needs.

Risk-adjusted performance

Risk-adjusted performance metrics gauge the effectiveness of an investment by considering its returns relative to the perceived risk. They aim to provide a more well-rounded picture of performance by factoring in the level of risk taken to achieve returns. Investors can utilize such metrics to help determine whether the returns from an investment justify the risks and make informed decisions.

The two most commonly used risk-adjusted performance metrics are the Sharpe ratio and the Sortino ratio.

1. Sharpe ratio

The Sharpe ratio , developed by Nobel laureate William F. Sharpe, measures the performance of an investment compared to a theoretically risk-free asset, adjusted for the investment risk. The ratio uses the following formula:

Sharpe Ratio = (𝑅𝑎 − 𝑅𝑓) / 𝜎𝑎

Where:

• 𝑅𝑎 = Average return of the investment

• 𝑅𝑓 = Theoretical risk-free rate of return

• 𝜎𝑎 = Standard deviation of the investment's returns (volatility)

A higher Sharpe ratio indicates a more favorable risk-adjusted return, as it signifies that the investment produced higher excess returns per unit of increase in total perceived risk.

2. Sortino ratio

The Sortino ratio is a modified form of the Sharpe ratio that only considers downside volatility , i.e., the volatility of returns below the theoretical risk-free benchmark. Although it shares close similarities with the Sharpe ratio, it can produce very different values, especially when the returns do not have a symmetrical distribution, since it does not penalize upside and downside volatility equally. The ratio uses the following formula:

Sortino Ratio = (𝑅𝑎 − 𝑅𝑓) / 𝜎𝑑

Where:

• 𝑅𝑎 = Average return of the investment

• 𝑅𝑓 = Theoretical risk-free rate of return

• 𝜎𝑑 = Downside deviation (standard deviation of negative excess returns, or downside volatility)

The Sortino ratio offers an alternative perspective on an investment's return-generating efficiency since it does not consider upside volatility in its calculation. A higher Sortino ratio signifies that the investment produced higher excess returns per unit of increase in perceived downside risk.

█ CALCULATIONS

Return period detection

Calculating risk-adjusted performance metrics requires collecting returns across several periods of a given size. Analysts may use different period sizes based on the context and their preferences. However, two widely used standards are monthly or daily periods, depending on the available data and the investment's duration. The built-in ratios displayed in the Strategy Tester utilize returns from either monthly or daily periods in their calculations based on the following logic:

• Use monthly returns if the history of closed trades spans at least two months.

• Use daily returns if the trades span at least two days but less than two months.

• Do not calculate the ratios if the trade data spans fewer than two days.

This library's `detectPeriod()` function applies related logic to available chart data rather than trade data to determine which period is appropriate:

• It returns true if the chart's data spans at least two months, indicating that it's sufficient to use monthly periods.

• It returns false if the chart's data spans at least two days but not two months, suggesting the use of daily periods.

• It returns na if the length of the chart's data covers less than two days, signifying that the data is insufficient for meaningful ratio calculations.

It's important to note that programmers should only call `detectPeriod()` from a script's global scope or within the outermost scope of a function called from the global scope, as it requires the time value from the first bar to accurately measure the amount of time covered by the chart's data.

Collecting periodic returns

This library's `getPeriodicReturns()` function tracks price return data within monthly or daily periods and stores the periodic values in an array . It uses a `detectPeriod()` call as the condition to determine whether each element in the array represents the return over a monthly or daily period.

The `getPeriodicReturns()` function has two overloads. The first overload requires two arguments and outputs an array of monthly or daily returns for use in the `sharpe()` and `sortino()` methods. To calculate these returns:

1. The `percentChange` argument should be a series that represents percentage gains or losses. The values can be bar-to-bar return percentages on the chart timeframe or percentages requested from a higher timeframe.

2. The function compounds all non-na `percentChange` values within each monthly or daily period to calculate the period's total return percentage. When the `percentChange` represents returns from a higher timeframe, ensure the requested data includes gaps to avoid compounding redundant values.

3. After a period ends, the function queues the compounded return into the array , removing the oldest element from the array when its size exceeds the `maxPeriods` argument.

The resulting array represents the sequence of closed returns over up to `maxPeriods` months or days, depending on the available data.

The second overload of the function includes an additional `benchmark` parameter. Unlike the first overload, this version tracks and collects differences between the `percentChange` and the specified `benchmark` values. The resulting array represents the sequence of excess returns over up to `maxPeriods` months or days. Passing this array to the `sharpe()` and `sortino()` methods calculates generalized Information ratios , which represent the risk-adjustment performance of a sequence of returns compared to a risky benchmark instead of a risk-free rate. For consistency, ensure the non-na times of the `benchmark` values align with the times of the `percentChange` values.

Ratio methods

This library's `sharpe()` and `sortino()` methods respectively calculate the Sharpe and Sortino ratios based on an array of returns compared to a specified annual benchmark. Both methods adjust the annual benchmark based on the number of periods per year to suit the frequency of the returns:

• If the method call does not include a `periodsPerYear` argument, it uses `detectPeriod()` to determine whether the returns represent monthly or daily values based on the chart's history. If monthly, the method divides the `annualBenchmark` value by 12. If daily, it divides the value by 365.

• If the method call does specify a `periodsPerYear` argument, the argument's value supersedes the automatic calculation, facilitating custom benchmark adjustments, such as dividing by 252 when analyzing collected daily stock returns.

When the array passed to these methods represents a sequence of excess returns , such as the result from the second overload of `getPeriodicReturns()`, use an `annualBenchmark` value of 0 to avoid comparing those excess returns to a separate rate.

By default, these methods only calculate the ratios on the last available bar to minimize their resource usage. Users can override this behavior with the `forceCalc` parameter. When the value is true , the method calculates the ratio on each call if sufficient data is available, regardless of the bar index.

Look first. Then leap.

█ FUNCTIONS & METHODS

This library contains the following functions:

detectPeriod()

Determines whether the chart data has sufficient coverage to use monthly or daily returns

for risk metric calculations.

Returns: (bool) `true` if the period spans more than two months, `false` if it otherwise spans more

than two days, and `na` if the data is insufficient.

getPeriodicReturns(percentChange, maxPeriods)

(Overload 1 of 2) Tracks periodic return percentages and queues them into an array for ratio

calculations. The span of the chart's historical data determines whether the function uses

daily or monthly periods in its calculations. If the chart spans more than two months,

it uses "1M" periods. Otherwise, if the chart spans more than two days, it uses "1D"

periods. If the chart covers less than two days, it does not store changes.

Parameters:

percentChange (float) : (series float) The change percentage. The function compounds non-na values from each

chart bar within monthly or daily periods to calculate the periodic changes.

maxPeriods (simple int) : (simple int) The maximum number of periodic returns to store in the returned array.

Returns: (array) An array containing the overall percentage changes for each period, limited

to the maximum specified by `maxPeriods`.

getPeriodicReturns(percentChange, benchmark, maxPeriods)

(Overload 2 of 2) Tracks periodic excess return percentages and queues the values into an

array. The span of the chart's historical data determines whether the function uses

daily or monthly periods in its calculations. If the chart spans more than two months,

it uses "1M" periods. Otherwise, if the chart spans more than two days, it uses "1D"

periods. If the chart covers less than two days, it does not store changes.

Parameters:

percentChange (float) : (series float) The change percentage. The function compounds non-na values from each

chart bar within monthly or daily periods to calculate the periodic changes.

benchmark (float) : (series float) The benchmark percentage to compare against `percentChange` values.

The function compounds non-na values from each bar within monthly or

daily periods and subtracts the results from the compounded `percentChange` values to

calculate the excess returns. For consistency, ensure this series has a similar history

length to the `percentChange` with aligned non-na value times.

maxPeriods (simple int) : (simple int) The maximum number of periodic excess returns to store in the returned array.

Returns: (array) An array containing monthly or daily excess returns, limited

to the maximum specified by `maxPeriods`.

method sharpeRatio(returnsArray, annualBenchmark, forceCalc, periodsPerYear)

Calculates the Sharpe ratio for an array of periodic returns.

Callable as a method or a function.

Namespace types: array

Parameters:

returnsArray (array) : (array) An array of periodic return percentages, e.g., returns over monthly or

daily periods.

annualBenchmark (float) : (series float) The annual rate of return to compare against `returnsArray` values. When

`periodsPerYear` is `na`, the function divides this value by 12 to calculate a

monthly benchmark if the chart's data spans at least two months or 365 for a daily

benchmark if the data otherwise spans at least two days. If `periodsPerYear`

has a specified value, the function divides the rate by that value instead.

forceCalc (bool) : (series bool) If `true`, calculates the ratio on every call. Otherwise, ratio calculation

only occurs on the last available bar. Optional. The default is `false`.

periodsPerYear (simple int) : (simple int) If specified, divides the annual rate by this value instead of the value

determined by the time span of the chart's data.

Returns: (float) The Sharpe ratio, which estimates the excess return per unit of total volatility.

method sortinoRatio(returnsArray, annualBenchmark, forceCalc, periodsPerYear)

Calculates the Sortino ratio for an array of periodic returns.

Callable as a method or a function.

Namespace types: array

Parameters:

returnsArray (array) : (array) An array of periodic return percentages, e.g., returns over monthly or

daily periods.

annualBenchmark (float) : (series float) The annual rate of return to compare against `returnsArray` values. When

`periodsPerYear` is `na`, the function divides this value by 12 to calculate a

monthly benchmark if the chart's data spans at least two months or 365 for a daily

benchmark if the data otherwise spans at least two days. If `periodsPerYear`

has a specified value, the function divides the rate by that value instead.

forceCalc (bool) : (series bool) If `true`, calculates the ratio on every call. Otherwise, ratio calculation

only occurs on the last available bar. Optional. The default is `false`.

periodsPerYear (simple int) : (simple int) If specified, divides the annual rate by this value instead of the value

determined by the time span of the chart's data.

Returns: (float) The Sortino ratio, which estimates the excess return per unit of downside

volatility.

Wolf DCA CalculatorThe Wolf DCA Calculator is a powerful and flexible indicator tailored for traders employing the Dollar Cost Averaging (DCA) strategy. This tool is invaluable for planning and visualizing multiple entry points for both long and short positions. It also provides a comprehensive analysis of potential profit and loss based on user-defined parameters, including leverage.

Features

Entry Price: Define the initial entry price for your trade.

Total Lot Size: Specify the total number of lots you intend to trade.

Percentage Difference: Set the fixed percentage difference between each DCA point.

Long Position: Toggle to switch between long and short positions.

Stop Loss Price: Set the price level at which you plan to exit the trade to minimize losses.

Take Profit Price: Set the price level at which you plan to exit the trade to secure profits.

Leverage: Apply leverage to your trade, which multiplies the potential profit and loss.

Number of DCA Points: Specify the number of DCA points to strategically plan your entries.

How to Use

1. Add the Indicator to Your Chart:

Search for "Wolf DCA Calculator" in the TradingView public library and add it to your chart.

2. Configure Inputs:

Entry Price: Set your initial trade entry price.

Total Lot Size: Enter the total number of lots you plan to trade.

Percentage Difference: Adjust this to set the interval between each DCA point.

Long Position: Use this toggle to choose between a long or short position.

Stop Loss Price: Input the price level at which you plan to exit the trade to minimize losses.

Take Profit Price: Input the price level at which you plan to exit the trade to secure profits.

Leverage: Set the leverage you are using for the trade.

Number of DCA Points: Specify the number of DCA points to plan your entries.

3. Analyze the Chart:

The indicator plots the DCA points on the chart using a stepline style for clear visualization.

It calculates the average entry point and displays the potential profit and loss based on the specified leverage.

Labels are added for each DCA point, showing the entry price and the lots allocated.

Horizontal lines mark the Stop Loss and Take Profit levels, with corresponding labels showing potential loss and profit.

Benefits

Visual Planning: Easily visualize multiple entry points and understand how they affect your average entry price.

Risk Management: Clearly see your Stop Loss and Take Profit levels and their impact on your trade.

Customizable: Adapt the indicator to your specific strategy with a wide range of customizable parameters.

IV Rank Oscillator by dinvestorqShort Title: IVR OscSlg

Description:

The IV Rank Oscillator is a custom indicator designed to measure and visualize the Implied Volatility (IV) Rank using Historical Volatility (HV) as a proxy. This indicator helps traders determine whether the current volatility level is relatively high or low compared to its historical levels over a specified period.

Key Features :

Historical Volatility (HV) Calculation: Computes the historical volatility based on the standard deviation of logarithmic returns over a user-defined period.

IV Rank Calculation: Normalizes the current HV within the range of the highest and lowest HV values over the past 252 periods (approximately one year) to generate the IV Rank.

IV Rank Visualization: Plots the IV Rank, along with reference lines at 50 (midline), 80 (overbought), and 20 (oversold), making it easy to interpret the relative volatility levels.

Historical Volatility Plot: Optionally plots the Historical Volatility for additional reference.

Usage:

IV Rank : Use the IV Rank to assess the relative level of volatility. High IV Rank values (close to 100) indicate that the current volatility is high relative to its historical range, while low IV Rank values (close to 0) indicate low relative volatility.

Reference Lines: The overbought (80) and oversold (20) lines help identify extreme volatility conditions, aiding in trading decisions.

Example Use Case:

A trader can use the IV Rank Oscillator to identify potential entry and exit points based on the volatility conditions. For instance, a high IV Rank may suggest a period of high market uncertainty, which could be a signal for options traders to consider strategies like selling premium. Conversely, a low IV Rank might indicate a more stable market condition.

Parameters:

HV Calculation Length: Adjustable period length for the historical volatility calculation (default: 20 periods).

This indicator is a powerful tool for options traders, volatility analysts, and any market participant looking to gauge market conditions based on historical volatility patterns.

ATR Grid Levels [By MUQWISHI]▋ INTRODUCTION :

The “ATR Levels” produces a sequence of horizontal line levels above and below the Center Line (reference level). They are sized based on the instrument's volatility, representing the average historical price movement on a selected higher timeframe using the average true range (ATR) indicator.

_______________________

▋ OVERVIEW:

_______________________

▋ IMPLEMENTATION:

The indicator starts by drawing a Center Line that is selected by the user from a variety of common levels. Then, it draws a sequence of horizontal lines above and below the Center Line, which are sized based on the most confirmed average true range (ATR) at the selected higher timeframe.

In the top right corner of the chart, there is a table displaying both the selected ATR (in the right cell) and the ATR of the current bar (in the left cell). This feature enables users to compare these two values. It's important to note that the ATR of the current bar may not be confirmed yet, as the market is still active.

_______________________

▋ INDICATOR SETTINGS:

# Section (1): ATR Settings

(1) ATR Period & Smoothing.

(2) Timeframe where ATR value imported from.

(3) To show/hide the table comparison between the current ATR and the ATR for the selected period. Also, ability to color the current ATR cell if it’s greater.

# Section (2): Levels Settings

(1) Selecting a Center Line level among a variety of common levels, which is taken as reference level where a sequence of horizontal lines plot above and below it.

(2) Size of grid in ATR unit.

(3) Number of horizontal lines to plot in a single side.

(4) Grid Side. Ability to plot above or below the Center Line.

(5) Lines colors, and mode.

(6) Line style.

(7) Label style.

(8) Ability to remove old lines, from previous HTF.

_____________________

▋ COMMENT:

The ATR Levels should not be taken as a major concept to build a trading decision.

Please let me know if you have any questions.

Thank you.

Portfolio HeatThe "Portfolio Heat" indicator offers a visual representation of potential risk exposure for a portfolio across up to eight different symbols. It dynamically calculates three risk metrics based on current price, the number of shares owned, your designated stop loss, and total account size.

Open Dollar Risk – the total dollar amount you will lose if your stop loss is hit.

Open % of Portfolio Risk – the risk as a percentage of your total account size.

Starting Capital Risk – the dollar amount risked based on the difference between the entry price and stop price.

These metrics adjust in real-time, allowing you to monitor and manage risk more effectively.

Open portfolio heat refers to how much you would lose if all your currently held stock positions hit their stop-losses, whether those stop-losses are below what you paid for them - referred to as your “cost basis” - at your cost basis (breakeven) or above your cost basis (in the money). Admittedly, it’s a pretty bad day when all your stops are hit at once, but as traders we need to prepare for the worst. To visualize what “open heat” looks like on a single stock position, please note the chart below:

In the example above you can see that if you were to purchase 100 shares of this stock at a cost-basis of $18/share, and your stop-loss is placed at $15, if the current price of the stock is at $20 and the stock price drops to hit your stop-loss, it would result in a $500 total drawdown in your portfolio. Keep in mind this is just one stock position. Hypothetically, if you were even holding two stocks that had the above open heat, with a $10,000 account size, you could experience a 10% drawdown quite fast if the market corrects.

The “Portfolio Heat” indicator is fully customizable allowing traders to select the number of positions in the portfolio, colors and a detailed or a summary view of risk.

Note if entering a short position, you will enter the number of shares owned as a negative number.

Drawdown Dynamics IndicatorDescription :

The Drawdown Dynamics Indicator is a straightforward tool that offers insights into three critical aspects of an asset’s financial performance: Total Max Drawdown, Rolling Period Max Drawdown, and Current Max Drawdown. Inside of the indicator, you can select to view either the rolling period max drawdown or the all-time max drawdown. This is represented by the gray line. The blue line represents the asset's current drawdown.

Rolling Period Max Drawdown is more about a snapshot view, highlighting the maximum loss from a peak to a trough for an adjustable rolling time frame. This is a feature not available with other indicators that exist on TradingView.

Total Max Drawdown gives a broad view, showcasing the all-time deepest decline in an asset’s value.

Current Max Drawdown offers a live update, focusing on the asset's present phase and how it's performing in real-time.

Practical Uses :

The utility of this indicator becomes evident when you start exploring the risks and performance metrics of assets. A notable use of this indicator is in comparing the drawdowns of a trading strategy against the inherent drawdowns of an asset. It helps in painting a clearer picture of risk and performance of both the asset and the strategy.

Risk Understanding : By comparing the strategy drawdown to the asset drawdown, traders get to understand if the risk they’re taking aligns with the asset’s natural risk behavior.

Evaluating Strategy’s Strength : If a strategy can weather the storms of the asset's natural drawdown phases and come out relatively unscathed, it can speak to its strength.

Performance Comparison : It also acts as a benchmark tool. Traders can pit different strategies against each other, using the asset’s drawdown as a baseline, to see which one manages risks better.

Disclaimer : This is not financial advice. Open-source scripts I publish in the community are largely meant to spark ideas that can be used as building blocks for part of a more robust trade management strategy. If you would like to implement a version of any script, I would recommend making significant additions/modifications to the strategy & risk management functions. If you don’t know how to program in Pine, then hire a Pine-coder. We can help!

Curved Management (Zeiierman)█ Overview

The Curved Management (Zeiierman) is a trade management indicator tailored for traders looking to visualize their entry, stop loss, and take profit levels. Unique in its design, this indicator doesn't just display lines; it offers rounded or curved visualizations, setting it apart from conventional tools.

█ How It Works

At its core, this indicator leverages the power of the Average True Range (ATR), a metric for volatility, to establish logical stop-loss levels based on recent price action. By incorporating the ATR, the tool dynamically adapts to the market's changing volatility. What sets it apart is the unique curved visualization. Instead of the usual straight lines representing entry/sl levels, users can choose between rounded and straight edges for their take profit and stop loss levels. This aesthetic tweak gives the chart a cleaner look and offers a more intuitive understanding of risk management.

█ How to Apply the Indicator

Upon initially loading the indicator, a label appears that reads, "Set the 'xy' time and price for 'Curved Management (Zeiierman).'" This prompts you to click on the chart at your entry point. After selecting your entry point on the chart, the indicator will load. Ensure you adjust the trend direction in the settings panel based on whether you took a long or short position.

█ How to Use

Use the tool to manage your active position.

Long Entry

Short Entry

█ Settings

The indicator comes packed with various settings allowing customization:

Trade Direction

Decide the direction of the trade (long/short).

Reward multiplier

Sets the ratio for take profit relative to stop loss. Increasing this value will set your take profit further from the entry, and decreasing it will bring it closer.

Risk multiplier

Multiplier for calculating stop loss based on the ATR value. Increasing this makes your stop loss further from the entry, while decreasing brings it closer.

█ Related Free Scripts

Trade & Risk Management Tool

-----------------

Disclaimer

The information contained in my Scripts/Indicators/Ideas/Algos/Systems does not constitute financial advice or a solicitation to buy or sell any securities of any type. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

My Scripts/Indicators/Ideas/Algos/Systems are only for educational purposes!

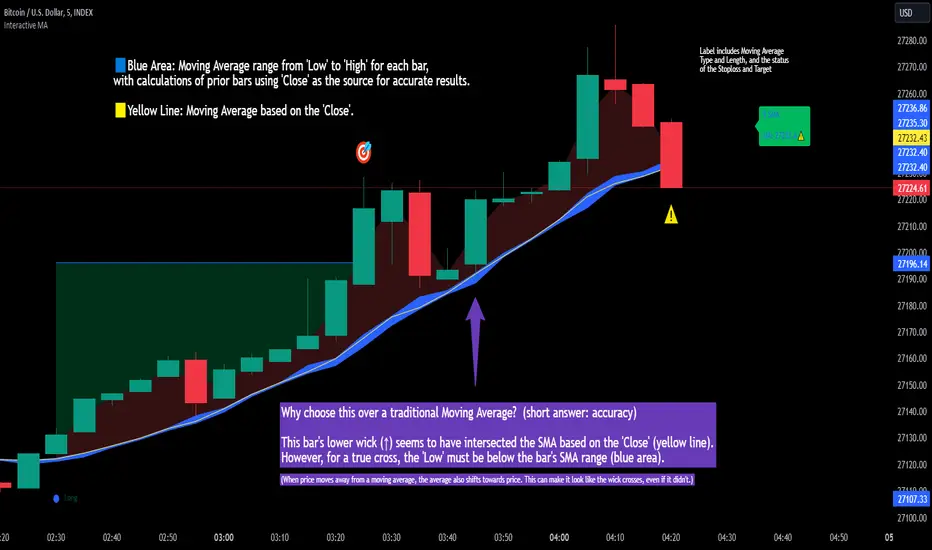

Interactive MA Stop Loss [TANHEF]This indicator is "Interactive." Once added to the chart, you need to click the start point for the moving average stoploss. Dragging it afterward will modify its position.

Why choose this indicator over a traditional Moving Average?

To accurately determine that a wick has crossed a moving average, you must examine the moving average's range on that bar (blue area on this indicator) and ensure the wick fully traverses this area.

When the price moves away from a moving average, the average also shifts towards the price. This can make it look like the wick crossed the average, even if it didn't.

How is the moving average area calculated?

For each bar, the moving average calculation is standard, but when the current bar is involved, its high or low is used instead of the close. For precise results, simply setting the source in a typical moving average calculation to 'Low' or 'High' is not sufficient in calculating the moving average area on a current bar.

Moving Average Options:

Simple Moving Average

Exponential Moving Average

Relative Moving Average

Weighted Moving Average

Indicator Explanation

After adding indicator to chart, you must click on a location to begin an entry.

The moving average type can be set and length modified to adjust the stoploss. An optional profit target may be added.

A symbol is display when the stoploss and profit target are hit. If a position is create that is not valid, "Overlapping MA and Bar" is displayed.

Alerts

'Check' alerts to use within indicator settings (stop hit and/or profit target hit).

Select 'Create Alert'

Set the condition to 'Interactive MA''

Select create.

Alert messages can have additional details using these words in between two Curly (Brace) Brackets:

{{stop}} = MA stop-loss (price)

{{upper}} = Upper MA band (price)

{{lower}} = Lower MA band (price)

{{band}} = Lower or Upper stoploss (word)

{{type}} = Long or Short stop-loss (word)

{{stopdistance}} = Stoploss Distance (%)

{{targetdistance}} = Target Distance (%)

{{starttime}} = Start time of stoploss (day:hour:minute)

{{maLength}} = MA Length (input)

{{maType}} = MA Type (input)

{{target}} = Price target (price)

{{trigger}} = Wick or Close Trigger input (input)

{{ticker}} = Ticker of chart (word)

{{exchange}} = Exchange of chart (word)

{{description}} = Description of ticker (words)

{{close}} = Bar close (price)

{{open}} = Bar open (price)

{{high}} = Bar high (price)

{{low}} = Bar low (price)

{{hl2}} = Bar HL2 (price)

{{volume}} = Bar volume (value)

{{time}} = Current time (day:hour:minute)

{{interval}} = Chart timeframe

{{newline}} = New line for text

I will add further moving averages types in the future. If you suggestions post them below.

Moving Average Cross trade PLAbstract

This script evaluates the potential trading proceeding and loss of the moving average cross strategy and plot it as a chart.

We can use it as a reference to whether we follow the original trading signals or not.

Introduction

Moving average cross is a popular trading strategy.

The strategy suggests traders buy when the short term moving average is above the long term moving average and sell when the short term moving average is below the long term moving average.

However, just like the most technical indicators, the signals are not always accurate.

This problem causes traders don't have sufficient confidence to trade with these signals.

On the other hand, the natural risk management suggests us only invest after major risks are past.

Therefore, we wait until many counterexamples of trading signals are past.

What will happen if we imagine that following a specific trading signal is a fund?

We can evaluate the potential trading proceeding and loss and plot it as a chart.

And then, we can measure how much loss may encounter in many worst cases and regard it as a reference to whether we follow the original trading signals or not.

How it works

1. Determine the instruments and time frames we are interested in.

2. Determine the long term moving average and the short term moving average.

3. The strategy suggests traders buy when the short term moving average is above the long term moving average and sell when the short term moving average is below the long term moving average.

4. The potential trading proceeding and loss is plotted as a chart.