Value at Risk [OmegaTools]The "Value at Risk" (VaR) indicator is a powerful financial risk management tool that helps traders estimate the potential losses in a portfolio over a specified period of time, given a certain level of confidence. VaR is widely used by financial institutions, traders, and risk managers to assess the probability of portfolio losses in both normal and volatile market conditions. This TradingView script implements a comprehensive VaR calculation using several models, allowing users to visualize different risk scenarios and adjust their trading strategies accordingly.

Concept of Value at Risk

Value at Risk (VaR) is a statistical technique used to measure the likelihood of losses in a portfolio or financial asset due to market risks. In essence, it answers the question: "What is the maximum potential loss that could occur in a given portfolio over a specific time horizon, with a certain confidence level?" For instance, if a portfolio has a one-day 95% VaR of $10,000, it means that there is a 95% chance the portfolio will not lose more than $10,000 in a single day. Conversely, there is a 5% chance of losing more than $10,000. VaR is a key risk management tool for portfolio managers and traders because it quantifies potential losses in monetary terms, allowing for better-informed decision-making.

There are several ways to calculate VaR, and this indicator script incorporates three of the most commonly used models:

Historical VaR: This approach uses historical returns to estimate potential losses. It is based purely on past price data, assuming that the past distribution of returns is indicative of future risks.

Variance-Covariance VaR: This model assumes that asset returns follow a normal distribution and that the risk can be summarized using the mean and standard deviation of past returns. It is a parametric method that is widely used in financial risk management.

Exponentially Weighted Moving Average (EWMA) VaR: In this model, recent data points are given more weight than older data. This dynamic approach allows the VaR estimation to react more quickly to changes in market volatility, which is particularly useful during periods of market stress. This model uses the Exponential Weighted Moving Average Volatility Model.

How the Script Works

The script starts by offering users a set of customizable input settings. The first input allows the user to choose between two main calculation modes: "All" or "OCT" (Only Current Timeframe). In the "All" mode, the script calculates VaR using all available methodologies—Historical, Variance-Covariance, and EWMA—providing a comprehensive risk overview. The "OCT" mode narrows the calculation to the current timeframe, which can be particularly useful for intraday traders who need a more focused view of risk.

The next input is the lookback window, which defines the number of historical periods used to calculate VaR. Commonly used lookback periods include 21 days (approximately one month), 63 days (about three months), and 252 days (roughly one year), with the script supporting up to 504 days for more extended historical analysis. A longer lookback period provides a more comprehensive picture of risk but may be less responsive to recent market conditions.

The confidence level is another important setting in the script. This represents the probability that the loss will not exceed the VaR estimate. Standard confidence levels are 90%, 95%, and 99%. A higher confidence level results in a more conservative risk estimate, meaning that the calculated VaR will reflect a more extreme loss scenario.

In addition to these core settings, the script allows users to customize the visual appearance of the indicator. For example, traders can choose different colors for "Bullish" (Risk On), "Bearish" (Risk Off), and "Neutral" phases, as well as colors for highlighting "Breaks" in the data, where returns exceed the calculated VaR. These visual cues make it easy to identify periods of heightened risk at a glance.

The actual VaR calculation is broken down into several models, starting with the Historical VaR calculation. This is done by computing the logarithmic returns of the asset's closing prices and then using linear interpolation to determine the percentile corresponding to the desired confidence level. This percentile represents the potential loss in the asset over the lookback period.

Next, the script calculates Variance-Covariance VaR using the mean and standard deviation of the historical returns. The standard deviation is multiplied by a z-score corresponding to the chosen confidence level (e.g., 1.645 for 95% confidence), and the resulting value is subtracted from the mean return to arrive at the VaR estimate.

The EWMA VaR model uses the EWMA for the sigma parameter, the standard deviation, obtaining a specific dynamic in the volatility. It is particularly useful in volatile markets where recent price behavior is more indicative of future risk than older data.

For traders interested in intraday risk management, the script provides several methods to adjust VaR calculations for lower timeframes. By using intraday returns and scaling them according to the chosen timeframe, the script provides a dynamic view of risk throughout the trading day. This is especially important for short-term traders who need to manage their exposure during high-volatility periods within the same day. The script also incorporates an EWMA model for intraday data, which gives greater weight to the most recent intraday price movements.

In addition to calculating VaR, the script also attempts to detect periods where the asset's returns exceed the estimated VaR threshold, referred to as "Breaks." When the returns breach the VaR limit, the script highlights these instances on the chart, allowing traders to quickly identify periods of extreme risk. The script also calculates the average of these breaks and displays it for comparison, helping traders understand how frequently these high-risk periods occur.

The script further visualizes the risk scenario using a risk phase classification system. Depending on the level of risk, the script categorizes the market as either "Risk On," "Risk Off," or "Risk Neutral." In "Risk On" mode, the market is considered bullish, and the indicator displays a green background. In "Risk Off" mode, the market is bearish, and the background turns red. If the market is neither strongly bullish nor bearish, the background turns neutral, signaling a balanced risk environment.

Traders can customize whether they want to see this risk phase background, along with toggling the display of the various VaR models, the intraday methods, and the break signals. This flexibility allows traders to tailor the indicator to their specific needs, whether they are day traders looking for quick intraday insights or longer-term investors focused on historical risk analysis.

The "Risk On" and "Risk Off" phases calculated by this Value at Risk (VaR) script introduce a novel approach to market risk assessment, offering traders an advanced toolset to gauge market sentiment and potential risk levels dynamically. These risk phases are built on a combination of traditional VaR methodologies and proprietary logic to create a more responsive and intuitive way to manage exposure in both normal and volatile market conditions. This method of classifying market conditions into "Risk On," "Risk Off," or "Risk Neutral" is not something that has been traditionally associated with VaR, making it a groundbreaking addition to this indicator.

How the "Risk On" and "Risk Off" Phases Are Calculated

In typical VaR implementations, the focus is on calculating the potential losses at a given confidence level without providing an overall market outlook. This script, however, introduces a unique risk classification system that takes the output of various VaR models and translates it into actionable signals for traders, marking whether the market is in a Risk On, Risk Off, or Risk Neutral phase.

The Risk On and Risk Off phases are primarily determined by comparing the current returns of the asset to the average VaR calculated across several different methods, including Historical VaR, Variance-Covariance VaR, and EWMA VaR. Here's how the process works:

1. Threshold Setting and Effect Calculation: The script first computes the average VaR using the selected models. It then checks whether the current returns (expressed as a negative value to signify loss) exceed the average VaR value. If the current returns surpass the calculated VaR threshold, this indicates that the actual market risk is higher than expected, signaling a potential shift in market conditions.

2. Break Analysis: In addition to monitoring whether returns exceed the average VaR, the script counts the number of instances within the lookback period where this breach occurs. This is referred to as the "break effect." For each period in the lookback window, the script checks whether the returns surpass the calculated VaR threshold and increments a counter. The percentage of periods where this breach occurs is then calculated as the "effect" or break percentage.

3. Dual Effect Check (if "Double" Risk Scenario is selected): When the user chooses the "Double" risk scenario mode, the script performs two layers of analysis. First, it calculates the effect of returns exceeding the VaR threshold for the current timeframe. Then, it calculates the effect for the lower intraday timeframe as well. Both effects are compared to the user-defined confidence level (e.g., 95%). If both effects exceed the confidence level, the market is deemed to be in a high-risk situation, thus triggering a Risk Off phase. If both effects fall below the confidence level, the market is classified as Risk On.

4. Risk Phases Determination: The final risk phase is determined by analyzing these effects in relation to the confidence level:

- Risk On: If the calculated effect of breaks is lower than the confidence level (e.g., fewer than 5% of periods show returns exceeding the VaR threshold for a 95% confidence level), the market is considered to be in a relatively safe state, and the script signals a "Risk On" phase. This is indicative of bullish conditions where the potential for extreme loss is minimal.

- Risk Off: If the break effect exceeds the confidence level (e.g., more than 5% of periods show returns breaching the VaR threshold), the market is deemed to be in a high-risk state, and the script signals a "Risk Off" phase. This indicates bearish market conditions where the likelihood of significant losses is higher.

- Risk Neutral: If the break effect hovers near the confidence level or if there is no clear trend indicating a shift toward either extreme, the market is classified as "Risk Neutral." In this phase, neither bulls nor bears are dominant, and traders should remain cautious.

The phase color that the script uses helps visualize these risk phases. The background will turn green in Risk On conditions, red in Risk Off conditions, and gray in Risk Neutral phases, providing immediate visual feedback on market risk. In addition to this, when the "Double" risk scenario is selected, the background will only turn green or red if both the current and intraday timeframes confirm the respective risk phase. This double-checking process ensures that traders are only given a strong signal when both longer-term and short-term risks align, reducing the likelihood of false signals.

A New Way of Using Value at Risk

This innovative Risk On/Risk Off classification, based on the interaction between VaR thresholds and market returns, represents a significant departure from the traditional use of Value at Risk as a pure risk measurement tool. Typically, VaR is employed as a backward-looking measure of risk, providing a static estimate of potential losses over a given timeframe with no immediate actionable feedback on current market conditions. This script, however, dynamically interprets VaR results to create a forward-looking, real-time signal that informs traders whether they are operating in a favorable (Risk On) or unfavorable (Risk Off) environment.

By incorporating the "break effect" analysis and allowing users to view the VaR breaches as a percentage of past occurrences, the script adds a predictive element that can be used to time market entries and exits more effectively. This **dual-layer risk analysis**, particularly when using the "Double" scenario mode, adds further granularity by considering both current timeframe and intraday risks. Traders can therefore make more informed decisions not just based on historical risk data, but on how the market is behaving in real-time relative to those risk benchmarks.

This approach transforms the VaR indicator from a risk monitoring tool into a decision-making system that helps identify favorable trading opportunities while alerting users to potential market downturns. It provides a more holistic view of market conditions by combining both statistical risk measurement and intuitive phase-based market analysis. This level of integration between VaR methodologies and real-time signal generation has not been widely seen in the world of trading indicators, marking this script as a cutting-edge tool for risk management and market sentiment analysis.

I would like to express my sincere gratitude to @skewedzeta for his invaluable contribution to the final script. From generating fresh ideas to applying his expertise in reviewing the formula, his support has been instrumental in refining the outcome.

Riskoff

Risk Matrix [QuantraSystems]Risk Matrix

The Risk Matrix is a sophisticated tool that aggregates a variety of fundamental inputs, primarily external (non-crypto) market data is used to assess investor risk appetite. By combining external macroeconomic factors and proxies for liquidity data with specific signals from the cryptomarket - the Risk Matrix provides a holistic view of market risk conditions. These insights are designed to help traders and investors make informed decisions on when to adopt a risk-on or risk-off approach.

Core Concept

The Risk Matrix functions as a dynamic risk assessment tool that integrates both fundamental and technical market indicators to generate an aggregated Z-score. This score helps traders to identify where the market is in a risk-off or risk-on state, The system provides both binary risk signals and a more nuanced “risk seasonality” mode for deeper analysis.

Key Features

Global Liquidity Aggregate - The Liquidity score is a custom measure of global liquidity, built by combining a variety of traditional financial metrics. These include data from central bank balance sheets, reverse repo operations and credit availability. This data is sourced from organizations such as the U.S. Federal Reserve, the European Central Bank, and the People’s Bank of China. The purpose of this aggregate is to gauge how much liquidity is available in the global financial system - which often correlates with risk sentiment. Rising liquidity tends to boost risk-on appetite, while liquidity contractions signal increased caution (risk-off) in the markets. The data sources used in this global liquidity aggregate include:

- U.S. Commercial Bank Credit data

- Federal Reserve balance sheet and reverse repo operations

- Liquidity from major central banks including the Fed, Bank of Japan, ECB, and PBoC

- Asset performance from major global financial indices such as the S&P 500, TLT, DXY (U.S. Dollar Index), MOVE (bond market volatility), and commodities like gold and oil.

Other key Z-scores (measured individually) - The Risk Matrix also incorporates other major Z-scores that represent different facets of the financial markets:

- Collateral Risk - A measure of US bond volatility, where higher values indicate higher interest rate risk - leading to potential market instability and cautious market behaviors.

- Stablecoin Dominance - The dominance of stablecoins in the crypto markets - which can signal risk aversion the total capital allocated to stables increases relative to other cryptocurrencies.

- US Currency Strength - The U.S. Dollar Index Z-score reflects currency market strength, with higher values typically indicating risk aversion as investors sell more volatile assets and flock to the dollar.

- Trans-pacific Monetary Bias - Signals capital flow and monetary trends that link between the East and West, heavily influencing global risk sentiment.

- Total - A measure of the total cryptocurrency market cap, signaling broader risk sentiment with the crypto market.

Neural Network Synthesis - The NNSYNTH component adds a machine learning inspired layer to the Risk Matrix. This custom indicator synthesizes inputs from various technical indicators (such as RSI, MACD, Bollinger Bands, and others) to generate a composite signal that reflects the health of the cryptomarket. While highly complex in its design, the NNSYNTH ultimately helps detect market shifts early by synthesizing multiple signals into one cohesive output. This score is particularly useful for gauging momentum and identifying potential turning points in market trends. Because the NNSYNTH is a closed source indicator, and it is included here, the Risk Matrix by extension is a closed source indicator.

How it Works

Z-score Aggregation - The Risk Matrix computes a final risk score by aggregating several Z-scores from different asset classes and data sources, all of which contribute proportionally to the overall market risk assessment. Each input is equally weighted - normalization allows for direct comparisons across global liquidity trends, currency fluctuations, bond market volatility and crypto market conditions. Furthermore, this system employs multi-calibration aggregation - where each individual matrix is itself an aggregate of multiple Z-scores derived from various timeframes. This ensures that each matrix captures a distinct average across different time horizons before being combined into the overall Risk Matrix. This layered, multi timeframe approach enhances the precision and robustness of the final Z-score.

Risk-On / Risk-Off Mode - The system’s binary mode provides a clear Risk On and Off signal. This nature of this signal is determined by the behavior of the Z-score relative to the midline, or Standard Deviation Bands, depending on specific conditions:

Risk-On is signaled when the aggregated final Z-score crosses above 0. However, in extreme oversold conditions, Risk-On can trigger early if the upper standard deviation band falls below the zero line. In such cases, the Risk-On signal is triggered when the z-score crosses the upper standard deviation band - without waiting to cross the midline.

Risk-Off is signaled when the final Z-score moves below 0. Similarly, Risk-Off can also be triggered early if the lower standard deviation band rises above the midline. In this instance, Risk-Off is triggered when the Z-score crosses below the lower band.

Risk Seasonality Mode - This mode offers a more gradual transition between risk states, measuring the change in the Z-score to visualize the shifts in risk appetite over time. It's useful for traders seeking to understand broader market cycles and risk phases. The seasonality view breaks down the market into the following phases:

Risk-On - High risk appetite where risk/cyclical markets are generally bullish.

Weakening - Markets showing signs of cooling off, here the higher beta assets tend to sell off first.

Risk-Off - Investors pull back, and bearish sentiment prevails.

Recovery - Signs of bottoming out, potential for market re-entry.

Component Matrices - Each individual Z-score is visualized as part of the component matrices - scaled to a 3 Sigma range. These component matrices allow traders to view how each data source is contributing to the overall risk assessment in real time - offering transparency and granularity.

Visuals and UI

Main Risk Matrix - The aggregated Z-Score is displayed saliently in the main risk matrix. Traders and investors can quickly see what season the Risk Matrix is signaling and adjust their strategies accordingly.

Overview Table - A detailed overview table shows the current confirmed Z-scores for each component, along with values from 2, and 3 bars back. This helps traders spot trends and the rate of change (RoC) between signals, offering additional insights for shorter-term risk management.

Customizability - Users can customize the visual elements of the matrix, including color palettes, table sizes, and positions. This allows for optimal integration into any trader’s existing workspace.

Usage Summary

The Risk Matrix is an incredibly versatile tool. It is especially valuable as a means of achieving a cross-market view of risk, incorporating both crypto-specific and macroeconomic factors. Some key use cases include:

Adjusting Capital Allocation Based on Risk Seasons - Traders can use the Risk Matrix to adjust their capital allocation dynamically. During Risk-On periods, they might increase exposure to long positions, capitalizing on stronger market conditions. Conversely, during Risk-Off periods, traders could reduce or hedge long positions and potentially scale up short positions or move into safer assets.

Complementing Other Trading Systems - The Risk Matrix can work alongside other technical systems to provide context to market moves. For instance, a trend-following strategy might suggest an entry, but the Risk Matrix could be used to verify whether the broader market conditions support this trade. If the Matrix is in a Risk-Off period, a trader might opt for more conservative trade sizes or avoid the trade entirely.

This flexibility allows traders to adjust their strategies and portfolio risk dynamically, enhancing decision making based on broader market conditions - as indicated by external macroeconomic factors, liquidity, and risk sentiment.

Important Note

The Risk Matrix always uses the most up-to-date data available, ensuring analysis reflects the latest market conditions and macroeconomic inputs. In rare cases, governments or financial institutions revise past data - and the Risk Matrix will adjust accordingly. This behavior can only be seen in the Liquidity Matrix. and can affect the final score. While this is uncommon, it highlights the benefit of using a system that adapts in real-time, incorporating the most accurate and current information to enhance decision making processes.

Macro Risk On/Off SentimentOverview

As an Ichimoku trader, I've always found it crucial to understand the broader market sentiment before entering trades. That's why I developed this Macro Risk On/Off Sentiment Indicator. It's designed to provide a comprehensive view of global market risk sentiment by analysing multiple factors across different asset classes. By combining nine key market indicators, it produces an overall risk sentiment score, giving me a clearer picture of the market's mood before I apply my Ichimoku strategy.

Rationale

While Ichimoku is powerful for identifying trends and potential entry points, I realised it doesn't always capture the broader market context. Markets don't exist in isolation—they're influenced by a myriad of factors including volatility, economic indicators, and cross-asset relationships. By creating this indicator, I aimed to fill that gap, providing myself with a macro view that complements my Ichimoku analysis.

How It Works

The indicator analyses nine different market factors:

VIX (Volatility Index): Measures market expectations of near-term volatility.

S&P 500 Performance: Represents the overall US stock market performance.

US 10-Year Treasury Yield: Indicates bond market sentiment and economic outlook.

Gold Price Movement: Often seen as a safe-haven asset.

US Dollar Index: Measures the strength of the USD against a basket of currencies.

Emerging Markets Performance: Represents risk appetite for higher-risk markets.

High Yield Bond Spreads: Indicates credit market risk sentiment.

Copper/Gold Ratio: An economic growth indicator.

Put/Call Ratio: Measures overall market sentiment based on options trading.

Each factor is assigned a score based on its z-score relative to its recent history, then weighted according to its perceived importance. The overall risk score is a weighted average of these individual scores.

How I Use It

Before applying my Ichimoku strategy, I first check this indicator to gauge the overall market sentiment:

I look at the blue line plotted on the chart, which represents the overall risk score.

I note the background colour: green for risk-on (positive score) and red for risk-off (negative score).

I check the label in the lower-left corner, which provides specific FX pair recommendations and market expectations.

In a risk-on environment (positive score):

I focus on long positions in AUD/JPY, NZD/JPY, EUR/USD, etc.

I look for short opportunities in USD/CAD, USD/NOK, etc.

I expect commodities and yields to rise

In a risk-off environment (negative score):

I focus on long positions in USD/JPY, USD/CHF, USD/CAD

I look for short opportunities in AUD/USD, NZD/USD, EUR/USD

I expect increased volatility and falling yields

The strength of the sentiment is reflected in how close the score is to either 1 (strong risk-on) or -1 (strong risk-off). This helps me gauge how aggressive or conservative I should be with my Ichimoku trades.

Customisation

I've designed this indicator to be flexible. You can modify it to:

Adjust the lookback period and moving average length (both default to 30)

Change the weighting of different factors in the final score calculation

Include or exclude specific factors based on your analysis needs

By combining this Macro Risk On/Off Sentiment Indicator with my Ichimoku analysis, I've found I can make more informed trading decisions, taking into account both the technical setups I see on the chart and the broader market context.

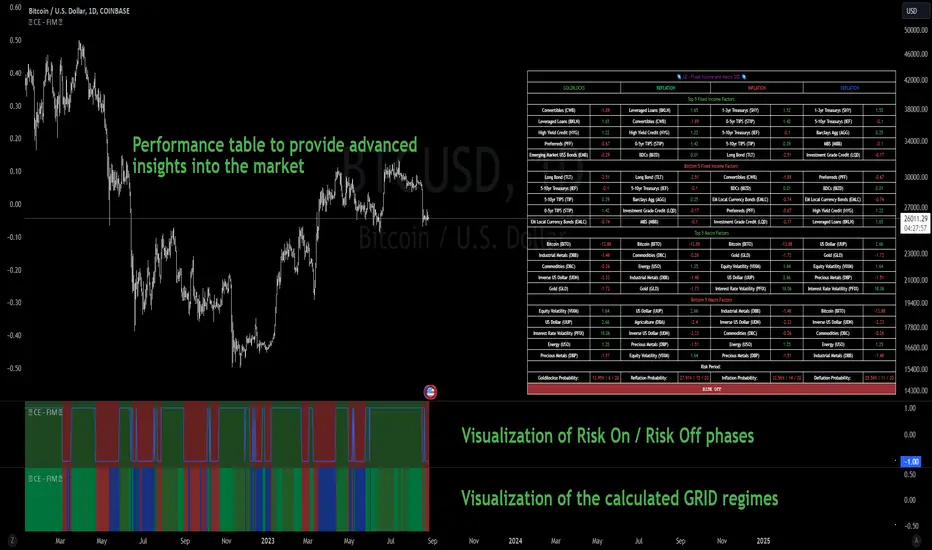

CE - 42MACRO Fixed Income and Macro This is Part 2 of 2 from the 42MACRO Recreation Series

However, there will be a bonus Indicator coming soon!

The CE - 42MACRO Fixed Income and Macro Table is a next level Macroeconomic and market analysis indicator.

It aims to provide a probabilistic insight into the market realized GRID Macro regimes,

track a multiplex of important Assets, Indices, Bonds and ETF's to derive extra market insights by showing the most important aggregates and their performance over multiple timeframes... and what that might mean for the whole market direction.

For traders and especially investors, the unique functionalities will be of high value.

Quick guide on how to use it:

docs.google.com

WARNING

By the nature of the macro regimes, the outcomes are more accurate over longer Chart Timeframes (Week to Months).

However, it is also a valuable tool to form an advanced,

market realized, short to medium term bias.

NOTE

This Indicator is intended to be used alongside the 1nd part "CE - 42MACRO Equity Factor"

for a more wholistic approach and higher accuracy.

Methodology:

The Equity Factor Table tracks specifically chosen Assets to identify their performance and add the combined performances together to visualize 42MACRO's GRID Equity Model.

For this it uses the below Assets:

Convertibles ( AMEX:CWB )

Leveraged Loans ( AMEX:BKLN )

High Yield Credit ( AMEX:HYG )

Preferreds ( NASDAQ:PFF )

Emerging Market US$ Bonds ( NASDAQ:EMB )

Long Bond ( NASDAQ:TLT )

5-10yr Treasurys ( NASDAQ:IEF )

5-10yr TIPS ( AMEX:TIP )

0-5yr TIPS ( AMEX:STIP )

EM Local Currency Bonds ( AMEX:EMLC )

BDCs ( AMEX:BIZD )

Barclays Agg ( AMEX:AGG )

Investment Grade Credit ( AMEX:LQD )

MBS ( NASDAQ:MBB )

1-3yr Treasurys ( NASDAQ:SHY )

Bitcoin ( AMEX:BITO )

Industrial Metals ( AMEX:DBB )

Commodities ( AMEX:DBC )

Gold ( AMEX:GLD )

Equity Volatility ( AMEX:VIXM )

Interest Rate Volatility ( AMEX:PFIX )

Energy ( AMEX:USO )

Precious Metals ( AMEX:DBP )

Agriculture ( AMEX:DBA )

US Dollar ( AMEX:UUP )

Inverse US Dollar ( AMEX:UDN )

Functionalities:

Fixed Income and Macro Table

Shows relative market Asset performance

Comes with different Calculation options like RoC,

Sharpe ratio, Sortino ratio, Omega ratio and Normalization

Allows for advanced market (health) performance

Provides the calculated, realized GRID market regimes

Informs about "Risk ON" and "Risk OFF" market states

Visuals - for your best experience only use one (+ BarColoring) at a time:

You can visualize all important metrics:

- GRID regimes of the currently chosen calculation type

- Risk On/Risk Off with background colouring and additional +1/-1 values

- a smoother GRID model

- a smoother Risk On/ Risk Off metric

- Barcoloring for enabled metric of the above

If you have more suggestions, please write me

Fixed Income and Macro:

The visualisation of the relative performance of the different assets provides valuable information about the current market environment and the actual market performance.

It furthermore makes it possible to obtain a deeper understanding of how the interconnected market works and makes it simple to identify the actual market direction,

thus also providing all the information to derive overall market health, market strength or weakness.

Utility:

The Fixed Income and Macro Table is divided in 4 Columns which are the GRID regimes:

Economic Growth:

Goldilocks

Reflation

Economic Contraction:

Inflation

Deflation

Top 5 Fixed Income/ Macro Factors:

Are the values green for a specific Column?

If so then the market reflects the corresponding GRID behavior.

Bottom 5 Fixed Income/ Macro Factors:

Are the values red for a specific Column?

If so then the market reflects the corresponding GRID behavior.

So if we have Goldilocks as current regime we would see green values in the Top 5 Goldilocks Cells and red values in the Bottom 5 Goldilocks Cells.

You will find that Reflation will look similar, as it is also a sign of Economic Growth.

Same is the case for the two Contraction regimes.

******

This Indicator again is based to a majority on 42MACRO's models.

I only brought them into TV and added things on top of it.

If you have questions or need a more in-depth guide DM me.

GM

CE - 42MACRO Equity Factor Table This is Part 1 of 2 from the 42MACRO Recreation Series

The CE - 42MACRO Equity Factor Table is a whole toolbox packaged in a single indicator.

It aims to provide a probabilistic insight into the market realized GRID Macro Regime, use a multiplex of important Assets and Indices to form a high probability Implied Correlation expectation and allows to derive extra market insights by showing the most important aggregates and their performance over multiple timeframes... and what that might mean for the whole market direction, as well as the underlying asset.

WARNING

By the nature of the macro regimes, the outcomes are more accurate over longer Chart Timeframes (Week to Months).

However, it is also a valuable tool to form a proper,

market realized, short to medium term bias.

NOTE

This Indicator is intended to be used alongside the 2nd part "CE - 42MACRO Yield and Macro"

for a more wholistic approach and higher accuracy.

Due to coding limitations they can not be merged into one Indicator.

Methodology:

The Equity Factor Table tracks specifically chosen Assets to identify their performance and add the combined performances together to visualize 42MACRO's GRID Equity Model.

For this it uses the below Assets, with more to come:

Dividend Compounders ( AMEX:SPHD )

Mid Caps ( AMEX:VO )

Emerging Markets ( AMEX:EEM )

Small Caps ( AMEX:IWM )

Mega Cap Growth ( NASDAQ:QQQ )

Brazil ( AMEX:EWZ )

United Kingdom ( AMEX:EWU )

Growth ( AMEX:IWF )

United States ( AMEX:SPY )

Japan ( AMEX:DXJ )

Momentum ( AMEX:MTUM )

China ( AMEX:FXI )

Low Beta ( AMEX:SPLV )

International ex-US ( NASDAQ:ACWX )

India ( AMEX:INDA )

Eurozone ( AMEX:EZU )

Quality ( AMEX:QUAL )

Size ( AMEX:OEF )

Functionalities:

1. Correlations

Takes a measure of Cross Market Correlations

2. Implied Trend

Calculates the trend for each Asset and uses the Correlation to obtain the Implied Trend for the underlying Asset

There are multiple functionalities to enhance Signal Speed and precision...

Reading a signal only over a certain threshold, otherwise being colored in gray to signal noise or unclear market behavior

Normalization of Signal

Double Normalization of Signal for more Speed... ideal for the Crypto Market

Using an additional Hull Moving Average to enhance Signal Speed

Additional simple Background coloring to get a Signal from the HMA

Barcoloring based on the Implied Correlation

3. Equity Factor Table

Shows market realized Asset performance

Provides the approximate realized GRID market regimes

Informs about "Risk ON" and "Risk OFF" market states

Now into the juicy stuff...

Visuals:

There is a variety of options to change visual settings of what is plotted and where

+ additional considerations.

Everything that is relevant in the underlying logic which can improve comprehension can be visualized with these options.

More to come

Market Correlation:

The Market Correlation Table takes the Correlation of all the Assets to the Asset on the Chart,

it furthermore uses the Normalized KAMA Oscillator by IkkeOmar to analyse the current trend of every single Asset.

(To enhance the Signal you can apply the mentioned Indicator on the relevant Assets to find your target Asset movements that you intend to capture...

and then change the length of the Indicator in here)

It then Implies a Correlation based on the Trend and the Correlation to give a probabilistically adjusted expectation for the future Chart Asset Movement.

This is strengthened by taking the average of all Implied Trends.

Thus the Correlation Table provides valuable insights about probabilistically likely Movement of the Asset over the defined time duration,

providing alpha for Traders and Investors alike.

Equity Factors:

The table provides valuable information about the current market environment (whether it's risk on or risk off),

the rough GRID models from 42MACRO and the actual market performance.

This allows you to obtain a deeper understanding of how the market works and makes it simple to identify the actual market direction,

makes it possible to derive overall market Health and shows market strength or weakness.

Utility:

The Equity Factor Table is divided in 4 Sections which are the GRID regimes:

Economic Growth:

Goldilocks

Reflation

Economic Contraction:

Inflation

Deflation

Top 5 Equity Factors:

Are the values green for a specific Column?

If so then the market reflects the corresponding GRID behavior.

Bottom 5 Equity Factors:

Are the values red for a specific Column?

If so then the market reflects the corresponding GRID behavior.

So if we have Goldilocks as current regime we would see green values in the Top 5 Goldilocks Cells and red values in the Bottom 5 Goldilocks Cells.

You will find that Reflation will look similar, as it is also a sign of Economic Growth.

Same is the case for the two Contraction regimes.

This whole Indicator, as well as the second part, is based to a majority on 42MACRO's models.

I only brought them into TV and added things on top of it.

If you have questions or need a more in-depth guide DM me.

Will make a guide to all functionalities if necessity becomes apparent.

GM

Bull / Bear Market RegimeBull / Bear Market Regime

Instructions:

- A simple risk on or risk off indicator based on CBOE's Implied Correlation and VIX to highlight and indicate Bull / Bear Markets. To be used with the S&P500 index as that's the source from where the CBOE calculates and measures implied volatility & implied correlation. Can also be used with the other indices such as: Dow Jones, S&P 500, Nasdaq, & Nasdaq100, & Index ETF's such as DIA, SPY, QQQ, etc.

- Know the active regime, see the larger picture using the Daily or Weekly view, and visualize the current "Risk On (Bull) or Risk Off (Bear)" environment.

Description:

- Risk On and Risk Off simplified & visualized. Know if we are in a RISK ON or RISK OFF environment (Bull or Bear Market). (Absolute bottoms and tops will occur BEFORE a Risk On (Bull Market) or Risk Off (Bear Market) environment is confirmed!) This indicator is not meant to bottom tick or uptick market price action, but to show the active regime.

- Green: Bull Market, Risk On, low volatility, and low risk.

- Red: Bear Market, Risk Off, high volatility, and higher risk.

Buy & Sell Indicators (DAILY time frame)

- Nothing is 100% guaranteed! Can be used for short to medium term trades at the users discretion in BEAR MARKETS!!

- These signals are meant to be used during a RISK OFF / BEAR MARKET environment that tends to be accompanied with high volatility. A Risk on / Bull Market environment tends to have low volatility and endless rallies, so the signals will differ and in most instances not apply for Bull market / Risk on regime.

- The SELL signal will more often than not signal that a pullback is near in a BULL market and that a BMR-Bear Market Rally is almost over in a BEAR market.

- The BUY signal will have far more accuracy in a BEAR market-high volatility environment and can Identify short-term and major bottoms.

Always use proper sizing and risk management!

VIX Strategy : Risk-ON, Risk-OFF

VRatio is the ratio of VIX3M and VIX. This ratio rises above 1.1; in a bear market, it decreases and goes below 1. VRatio=VIX3M/VIX. More details in Part 2.

VRatio > 1: Risk-On signal

Contango is the ratio of VX2 (first back-month contract) and VX1 (front-month contract) minus one. In a bull market, this indicator rises above 5%’ in a downtrend market, this indicator goes below -5%. More details in Part 2.

Contango > -5%: Risk-On signal

Contango Roll is the ratio of VX2 first back-month contract) and the VIX minus one. In a bull market, this indicator rises above 10%’ in a downtrend market, this indicator goes below -10%. More details in Part 2.

Contango Roll > 10%: Risk-On signal

Volatility Risk Premium (VRP) compares the implied volatility to the recent realized volatility; it attempts to quantify how much “extra” premium (in volatility term) S&P500 option sellers are charging investors for the protection of their portfolio. It can be seen as an insurance premium. A simple way to compute the VRP is VRP= VIX -HV10 where HV10 is the 10-day historical volatility of S&P500. Some people also look at the 5-day moving average of the VRP to smooth this indicator.

VRP > 0: Risk-On signal

Fast Volatility Risk Premium (FVRP) is a variant of the VRP. FVRP=EMA(VIX,7)-HV5 where HV5 the 5-day historical volatility of S&P500.

FVRP > 0: Risk-On signal

Volatility Momentum compares today’s VIX to last 50 days. It has, therefore, quite a bit of lag but it is a useful measure when combined with other indicators. Volatility Momentum=SMA(VIX,50) -VIX.

Volatility Momentum > 0: Risk-On signal

VIX Mean Reversion looks at today’s VIX compared to certain thresholds. We avoid investing in the S&P500 when the VIX is too high (above 20) or too low (below 12).

VIX Mean Reversion > 12 and VIX Mean Reversion < 20: Risk-On signal

VIX3M Mean Reversion works the same way as VIX Mean Reversion.

VIX3M Mean Reversion > 12 and VIX3M Mean Reversion < 20: Risk-On signal

RiskONessUtilizing tedtalksmacro's risk-on/off indicators to help determine whether the global macro environment is risk-on or off.

Higher values imply that global markets are risk-on, while lower values imply risk-off.

Mavara Market Mood"Mavara Market Mood" is a fundamental-based Indicator that shows the overall mood of the financial markets.

When people are willing to buy USD as a reserve currency against other instruments and feel uncertain and don't want to risk their trades, the Market Mood is Risk-OFF.

Conversely, When the traders are optimistic about the economic situation and are willing to sell USD against other instruments, the Market Mood is Risk-ON.

While DXY is trending up and US500 is trending down, the indicator shows a risk-OFF mood with red and refers to the traders' eagerness to make riskier trades.

While DXY is trending down and US500 is trending up, the indicator shows a risk-ON mood with green and refers to the traders' reluctance to make riskier trades.

When you find the histogram below zero, the market is on a high-risk-Off mode. Conversely, When you find the histogram above zero, the market is in a high-risk-ON mood.

In summary, you can buy USDCAD in a risk-OFF mood and sell it in the risk-on mood.

Mayfair Risk On/OffWe take the relative strength of the 4 Risk-On currencies (AUD, NZD, CAD, GBP) all together, and compare with the relative strength of the Risk-Off currencies (USD, EUR, JPY, CHF).

Green line above the 50? We are generally Risk-On. Red line above? Risk-Off.

You can switch between RSI and TSI, see what you prefer.

Gold-Stocks RatioA historic risk-off flag.

When the Gold-Stocks Ratio is above the 200 week moving average, investors may fair better holding gold and avoiding equities, as was the case for the last 20 years.