Dynamic Supply and Demand Zones [AlgoAlpha]Introducing the Dynamic Supply and Demand Zones by AlgoAlpha. This indicator is designed to automatically identify and visualize dynamic supply and demand zones on your chart, helping traders pinpoint potential reversal areas and assess market sentiment with enhanced clarity. It adapts to market conditions using a dynamic look-back mechanism, making it more responsive to recent price movements. 📈💡

Key Features

📊 Dynamic Look-Back : Automatically adjusts the look-back period based on the most recent pivot point, ensuring the most relevant data is analyzed.

🎯 Pivot Point Detection : Utilizes a user-defined period to detect significant pivot highs and lows, marking potential reversal points with precision.

🛠 Customizable Parameters : Offers extensive customization options including look-back period, pivot detection sensitivity, resolution, and zone tolerance.

🗺 Visual Display : Shows supply and demand zones as boxes on the chart, with optional profiles and background highlighting to differentiate between bullish and bearish zones.

🖍 Color-Coded Zones : Zones are color-coded for easy identification: green for bullish, red for bearish, and gray for neutral levels.

🔔 Alert Conditions : Triggers alerts when new pivot points are detected, ensuring you never miss a key market movement.

How to Use

🚀 Adding the Indicator : Press the star icon and add the indicator to favorites. Add it to your chart and adjust settings to fit your trading strategy.

🔍 Zone Analysis : Observe the color-coded zones on the chart. Bullish zones indicate potential support areas, while bearish zones suggest resistance. Monitor price interactions with these zones for potential entry and exit signals.

🔔 Alerts : Activate alert conditions for new pivot detections to stay ahead of market reversals.

How It Works

The indicator starts by detecting pivot highs and lows over a specified period. These pivots serve as reference points for determining the analysis range. If the Dynamic Look-Back feature is enabled, the look-back range dynamically adjusts from the most recent pivot to the current bar. Otherwise, a fixed look-back period is used. The price range is divided into multiple bins based on a specified resolution, and each bin’s volume is calculated by accumulating the volume of candles that fall within its price range. A zone is defined as significant if its volume is less than the adjacent bins, and the difference meets the Zone Tolerance criteria, indicating a potential area of support or resistance. These zones are then plotted on the chart as boxes. Bullish zones are shown in green, and bearish zones in red, helping traders visually identify key levels where supply and demand imbalances may cause price reversals.

Sentiment

Distance From moving averageDistance From Moving Average is designed to help traders visualize the deviation of the current price from a specified moving average. Users can select from four different types of moving averages: Simple Moving Average (SMA), Exponential Moving Average (EMA), Weighted Moving Average (WMA), and Hull Moving Average (HMA).

Key Features:

User-Friendly Input Options:

Choose the type of moving average from a dropdown menu.

Set the length of the moving average, with a default value of 200.

Custom Moving Average Calculations:

The script computes the selected moving average using the appropriate mathematical formula, allowing for versatile analysis based on individual trading strategies.

Distance Calculation:

The indicator calculates the distance between the current price and the chosen moving average, providing insight into market momentum. A positive value indicates that the price is above the moving average, while a negative value shows it is below.

Visual Representation:

The distance is plotted on the chart, with color coding:

Lime: Indicates that the price is above the moving average (bullish sentiment).

Red: Indicates that the price is below the moving average (bearish sentiment).

Customization:

Users can further customize the appearance of the plotted line, enhancing clarity and visibility on the chart.

This indicator is particularly useful for traders looking to gauge market conditions and make informed decisions based on the relationship between current prices and key moving averages.

LiquidityFlow Dominance+Alerts (btc.d, T3, Stables)LiquidityFlow Dominance+Alerts: Overview & Usage Guide

Overview

The LiquidityFlow Dominance+Alerts indicator provides a dynamic view of liquidity flow across Bitcoin, Altcoins, and Stablecoins, helping track liquidity shifts and identify market sentiment. By integrating moving averages, custom alerts, and thresholds for extreme outliers, this indicator helps to anticipate bullish and bearish shifts in liquidity and alert market tops and bottoms.

Key features include:

1. Liquidity Flow Monitoring : Track liquidity flow across Bitcoin (BTC), Altcoins (TOTAL3), and Stablecoins (USDT, USDC, DAI).

2. Custom Alerts : Set alerts for key liquidity shifts and extreme conditions in Stablecoin dominance, both with static and moving average (MA)-based calculations.

3. Moving Averages : Use Simple, Exponential, or Weighted Moving Averages to smooth out market data for more reliable signals.

4. Outlier Detection : Identify potential tops and bottoms using thresholds for Stablecoin dominance, with alerts for extreme movements.

Functionality

Data Inputs and Key Metrics

- Symbols Monitored:

- Bitcoin Dominance (BTC.D)

- Altcoin Market Cap (TOTAL3)

- Stablecoins (USDT.D, USDC.D, DAI.D)

- Liquidity Flow Conditions:

- Track percentage changes in dominance across sectors to detect liquidity flow into Bitcoin, Altcoins, or Stablecoins.

- Custom Metrics:

- Liquidity Flow Index: BTC Dominance minus Stablecoin Dominance.

- Liquidity Flow Ratio: BTC Dominance divided by the combined dominance of Stablecoins and Altcoins.

Moving Average Integration

- Select from SMA, EMA, or WMA to apply moving averages to the dominance metrics. Moving averages help smooth out short-term volatility and provide more consistent signals.

- Moving averages are applied to each sector (BTC, Altcoins, and Stablecoins) and compared to their previous period values to determine shifts in liquidity.

Alerts and Thresholds

- % Change Lookback Period: Adjust the lookback period to align with the timeframe of your chart. Shorter timeframes may require a lower lookback period, while higher timeframes may benefit from longer periods.

- Stables Bull/Bear % for Alerts: Set a threshold for when Stablecoin dominance becomes a bullish or bearish signal relative to BTC and Altcoins. A higher threshold may be used in volatile markets to filter out noise.

- Extreme Outliers Detection: Use the **Stables Up/Down Extreme Threshold** to identify potential market tops or bottoms when Stablecoin dominance deviates significantly from historical trends. The **Extreme Lookback Period** controls the time window for detecting these anomalies.

How to Use the Indicator

Adjusting the % Change Lookback Period

- The `% Change Lookback Period` should be adjusted based on your chart’s timeframe. For example, a shorter period (e.g., 7) works well for intraday charts, while longer periods (e.g., 14) might be more suitable for daily or weekly charts.

Setting Thresholds for Alerts

- Stables Bull/Bear % for Alerts: Adjust this setting to define when Stablecoin dominance triggers bullish or bearish alerts. A value like 1% could be a good starting point for most market conditions but can be fine-tuned based on volatility.

- Extreme Lookback Period: Define the lookback period for detecting extreme moves in Stablecoin dominance. This will help identify major tops and bottoms in the market. For shorter-term trades, consider using a shorter extreme lookback (e.g., 7-10 periods).

Alerts for Liquidity Shifts

- The indicator supports alerts for key liquidity shifts, which are useful for staying ahead of market movements. Alerts can be set to notify you when liquidity moves into:

- Bitcoin: Indicating a potential bullish trend for Bitcoin.

- Altcoins: Signaling altcoins are bullish.

- Stablecoins: Suggesting a risk-off environment or market correction.

Extreme Alerts for Stables

- Extreme Up/Down Alerts: These are triggered when Stablecoin dominance crosses extreme thresholds. For example, if Stablecoin dominance rises more than 14% over a set period, it could signal a market top, while a significant drop could indicate a market bottom.

Moving Average Calculations

- In addition to static percentage changes, moving averages can be applied to smooth out dominance values. The type and length of the moving average can be customized:

- SMA (Simple Moving Average): Best for smoothing out volatility in a linear way.

- EMA (Exponential Moving Average): More responsive to recent data, making it useful in faster markets.

- WMA (Weighted Moving Average): Emphasizes more recent data, but less reactive than the EMA.

Additional Usage Tips:

- Background Colors: The indicator visually highlights the dominant liquidity flow:

- Orange: Liquidity is shifting toward Bitcoin.

- Aqua: Liquidity is flowing into Altcoins.

- Red: Liquidity is moving into Stablecoins.

Bitcoin CME-Spot Z-Spread - Strategy [presentTrading]This time is a swing trading strategy! It measures the sentiment of the Bitcoin market through the spread of CME Bitcoin Futures and Bitfinex BTCUSD Spot prices. By applying Bollinger Bands to the spread, the strategy seeks to capture mean-reversion opportunities when prices deviate significantly from their historical norms

█ Introduction and How it is Different

The Bitcoin CME-Spot Bollinger Bands Strategy is designed to capture mean-reversion opportunities by exploiting the spread between CME Bitcoin Futures and Bitfinex BTCUSD Spot prices. The strategy uses Bollinger Bands to detect when the spread between these two correlated assets has deviated significantly from its historical norm, signaling potential overbought or oversold conditions.

What sets this strategy apart is its focus on spread trading between futures and spot markets rather than price-based indicators. By applying Bollinger Bands to the spread rather than individual prices, the strategy identifies price inefficiencies across markets, allowing traders to take advantage of the natural reversion to the mean that often occurs in these correlated assets.

BTCUSD 8hr Performance

█ Strategy, How It Works: Detailed Explanation

The strategy relies on Bollinger Bands to assess the volatility and relative deviation of the spread between CME Bitcoin Futures and Bitfinex BTCUSD Spot prices. Bollinger Bands consist of a moving average and two standard deviation bands, which help measure how much the spread deviates from its historical mean.

🔶 Spread Calculation:

The spread is calculated by subtracting the Bitfinex spot price from the CME Bitcoin futures price:

Spread = CME Price - Bitfinex Price

This spread represents the difference between the futures and spot markets, which may widen or narrow based on supply and demand dynamics in each market. By analyzing the spread, the strategy can detect when prices are too far apart (potentially overbought or oversold), indicating a trading opportunity.

🔶 Bollinger Bands Calculation:

The Bollinger Bands for the spread are calculated using a simple moving average (SMA) and the standard deviation of the spread over a defined period.

1. Moving Average (SMA):

The simple moving average of the spread (mu_S) over a specified period P is calculated as:

mu_S = (1/P) * sum(S_i from i=1 to P)

Where S_i represents the spread at time i, and P is the lookback period (default is 200 bars). The moving average provides a baseline for the normal spread behavior.

2. Standard Deviation:

The standard deviation (sigma_S) of the spread is calculated to measure the volatility of the spread:

sigma_S = sqrt((1/P) * sum((S_i - mu_S)^2 from i=1 to P))

3. Upper and Lower Bollinger Bands:

The upper and lower Bollinger Bands are derived by adding and subtracting a multiple of the standard deviation from the moving average. The number of standard deviations is determined by a user-defined parameter k (default is 2.618).

- Upper Band:

Upper Band = mu_S + (k * sigma_S)

- Lower Band:

Lower Band = mu_S - (k * sigma_S)

These bands provide a dynamic range within which the spread typically fluctuates. When the spread moves outside of these bands, it is considered overbought or oversold, potentially offering trading opportunities.

Local view

🔶 Entry Conditions:

- Long Entry: A long position is triggered when the spread crosses below the lower Bollinger Band, indicating that the spread has become oversold and is likely to revert upward.

Spread < Lower Band

- Short Entry: A short position is triggered when the spread crosses above the upper Bollinger Band, indicating that the spread has become overbought and is likely to revert downward.

Spread > Upper Band

🔶 Risk Management and Profit-Taking:

The strategy incorporates multi-step take profits to lock in gains as the trade moves in favor. The position is gradually reduced at predefined profit levels, reducing risk while allowing part of the trade to continue running if the price keeps moving favorably.

Additionally, the strategy uses a hold period exit mechanism. If the trade does not hit any of the take-profit levels within a certain number of bars, the position is closed automatically to avoid excessive exposure to market risks.

█ Trade Direction

The trade direction is based on deviations of the spread from its historical norm:

- Long Trade: The strategy enters a long position when the spread crosses below the lower Bollinger Band, signaling an oversold condition where the spread is expected to narrow.

- Short Trade: The strategy enters a short position when the spread crosses above the upper Bollinger Band, signaling an overbought condition where the spread is expected to widen.

These entries rely on the assumption of mean reversion, where extreme deviations from the average spread are likely to revert over time.

█ Usage

The Bitcoin CME-Spot Bollinger Bands Strategy is ideal for traders looking to capitalize on price inefficiencies between Bitcoin futures and spot markets. It’s especially useful in volatile markets where large deviations between futures and spot prices occur.

- Market Conditions: This strategy is most effective in correlated markets, like CME futures and spot Bitcoin. Traders can adjust the Bollinger Bands period and standard deviation multiplier to suit different volatility regimes.

- Backtesting: Before deployment, backtesting the strategy across different market conditions and timeframes is recommended to ensure robustness. Adjust the take-profit steps and hold periods to reflect the trader’s risk tolerance and market behavior.

█ Default Settings

The default settings provide a balanced approach to spread trading using Bollinger Bands but can be adjusted depending on market conditions or personal trading preferences.

🔶 Bollinger Bands Period (200 bars):

This defines the number of bars used to calculate the moving average and standard deviation for the Bollinger Bands. A longer period smooths out short-term fluctuations and focuses on larger, more significant trends. Adjusting the period affects the responsiveness of the strategy:

- Shorter periods (e.g., 100 bars): Makes the strategy more reactive to short-term market fluctuations, potentially generating more signals but increasing the risk of false positives.

- Longer periods (e.g., 300 bars): Focuses on longer-term trends, reducing the frequency of trades and focusing only on significant deviations.

🔶 Standard Deviation Multiplier (2.618):

The multiplier controls how wide the Bollinger Bands are around the moving average. By default, the bands are set at 2.618 standard deviations away from the average, ensuring that only significant deviations trigger trades.

- Higher multipliers (e.g., 3.0): Require a more extreme deviation to trigger trades, reducing trade frequency but potentially increasing the accuracy of signals.

- Lower multipliers (e.g., 2.0): Make the bands narrower, increasing the number of trade signals but potentially decreasing their reliability.

🔶 Take-Profit Levels:

The strategy has four take-profit levels to gradually lock in profits:

- Level 1 (3%): 25% of the position is closed at a 3% profit.

- Level 2 (8%): 20% of the position is closed at an 8% profit.

- Level 3 (14%): 15% of the position is closed at a 14% profit.

- Level 4 (21%): 10% of the position is closed at a 21% profit.

Adjusting these take-profit levels affects how quickly profits are realized:

- Lower take-profit levels: Capture gains more quickly, reducing risk but potentially cutting off larger profits.

- Higher take-profit levels: Let trades run longer, aiming for bigger gains but increasing the risk of price reversals before profits are locked in.

🔶 Hold Days (20 bars):

The strategy automatically closes the position after 20 bars if none of the take-profit levels are hit. This feature prevents trades from being held indefinitely, especially if market conditions are stagnant. Adjusting this:

- Shorter hold periods: Reduce the duration of exposure, minimizing risks from market changes but potentially closing trades too early.

- Longer hold periods: Allow trades to stay open longer, increasing the chance for mean reversion but also increasing exposure to unfavorable market conditions.

By understanding how these default settings affect the strategy’s performance, traders can optimize the Bitcoin CME-Spot Bollinger Bands Strategy to their preferences, adapting it to different market environments and risk tolerances.

US Sentiment Index [CryptoSea]The US Sentiment Index is an advanced analytical tool designed for traders seeking to uncover patterns, correlations, and potential leading signals across key market tickers. This indicator surpasses traditional sentiment measures, providing a data-driven approach that offers deeper insights compared to conventional indices like the Fear and Greed Index.

Key Features

Multi-Ticker Analysis: Integrates data from a diverse set of market indicators, including gold, S&P 500, U.S. Dollar Index, Volatility Index, and more, to create a comprehensive view of market sentiment.

Customisable Sensitivity Settings: Allows users to adjust the moving average period to fine-tune the sensitivity of sentiment calculations, adapting the tool to various market conditions and trading strategies.

Detailed Sentiment Scaling: Utilises a 0-100 scale to quantify sentiment strength, with colour gradients that visually represent bearish, neutral, and bullish conditions, aiding in quick decision-making.

Below is an example where the sentiment index can give leading signals. We see a first sign of wekaness in the index as it drops below its moving average. Shortly after we see it dip below our median 50 level, another sign of weakeness. We see the SPX price action to take a hit following the sentiment index decrease.

Tickers Used and Their Impact on Sentiment

The impact of each ticker on sentiment can be bullish or bearish, depending on their behaviour:

Gold (USGD): Typically seen as a safe-haven asset, rising gold prices often indicate increased market fear or bearish sentiment. Conversely, falling gold prices can signal reduced fear and a shift towards bullish sentiment in riskier assets.

S&P 500 (SPX): A rising S&P 500 is usually a sign of bullish sentiment, reflecting confidence in economic growth and market stability. A decline, however, suggests bearish sentiment and a potential move towards risk aversion.

U.S. Dollar Index (DXY): A strengthening U.S. Dollar can be a sign of fear as investors seek safety in the dollar, which is bearish for risk assets. A weakening dollar, on the other hand, can signal bullish sentiment as capital flows into riskier assets.

Volatility Index (VIX): Known as the "fear gauge," a rising VIX indicates increased market fear and bearish sentiment. A falling VIX suggests a calm, bullish market environment.

Junk Bonds (JNK): Rising junk bond prices often reflect bullish sentiment as investors take on more risk for higher returns. Conversely, falling junk bond prices signal increased fear and bearish sentiment.

Long-Term Treasury Bonds (TLT): Higher prices for long-term treasuries usually indicate a flight to safety, reflecting bearish sentiment. Lower prices suggest a shift towards riskier assets, indicating bullish sentiment.

Financial Sector ETF (XLF): Strength in the financial sector is typically bullish, indicating confidence in economic conditions. Weakness in this sector can reflect bearish sentiment and concerns about financial stability.

Unemployment Rate (USUR): A rising unemployment rate is a bearish signal, indicating economic weakness. A declining unemployment rate is bullish, reflecting economic strength and job growth.

U.S. Interest Rates (USINTR, USIRYY): Higher interest rates can be bearish, as they increase borrowing costs and reduce spending. Lower rates are generally bullish, promoting economic growth and risk-taking.

How it Works

Sentiment Calculation: The US Sentiment Index combines data from multiple tickers, calculating sentiment by scaling the distance from their respective moving averages. Each asset's behaviour is interpreted within the context of market fear or greed, providing a refined sentiment reading that adjusts dynamically.

Market Strength Analysis: When the index is above 50 and also above its moving average, it indicates particularly strong or bullish market conditions, driven by greed. Conversely, when the index is below 50 and under its moving average, it signals bearish or weak market conditions, associated with fear.

Correlation and Pattern Detection: The indicator analyses correlations among the included assets to detect patterns that might signal potential market movements, giving traders a leading edge over simpler sentiment measures.

Adaptive Background Colouring: Utilises a colour gradient that dynamically adjusts based on sentiment values, highlighting extreme fear, neutral, and extreme greed levels directly on the chart.

Flexible Display Options: Offers settings to toggle the moving average plot and adjust its period, giving users the ability to tailor the indicator's sensitivity and display to their specific needs.

In this example below, we can see the Sentiment rise above the Moving Average (MA). Price action goes on to follow this, although there is an instance where it dips below the MA, it quickly rises back above again as a sign of strength.

Another way you can use this index is by simply using the MA, if its trending up, we know the macro sentiment is bullish.

Application

Data-Driven Insights: Offers traders a detailed, data-driven approach to sentiment analysis, incorporating a broad spectrum of market indicators to deliver actionable insights.

Pattern Recognition: Helps identify patterns and correlations that may lead to market reversals or continuations, providing a nuanced view that goes beyond simple sentiment gauges.

Enhanced Decision-Making: Equips traders with a robust tool to validate trading strategies and make informed decisions based on comprehensive sentiment analysis.

The US Sentiment Index by is an essential addition to the toolkit of any trader looking to navigate market complexities with precision and confidence. Its advanced features and data-driven approach offer unparalleled insights into market sentiment, setting it apart from conventional sentiment indicators.

Momentum Cloud.V33🌟 Introducing MomentumCloud.V33 🌟

MomentumCloud.V33 is a cutting-edge indicator designed to help traders capture market momentum with clarity and precision. This versatile tool combines moving averages, directional movement indexes (DMI), and volume analysis to provide real-time insights into trend direction and strength. Whether you’re a scalper, day trader, or swing trader, MomentumCloud.V33 adapts to your trading style and timeframe, making it an essential addition to your trading toolkit. 📈💡

🔧 Customizable Parameters:

• Moving Averages: Adjust the periods of the fast (MA1) and slow (MA2) moving averages to fine-tune your trend analysis.

• DMI & ADX: Customize the DMI length and ADX smoothing to focus on strong, actionable trends.

• Volume Multiplier: Modify the cloud thickness based on trading volume, emphasizing trends with significant market participation.

📊 Trend Detection:

• Color-Coded Clouds:

• Green Cloud: Indicates a strong uptrend, suggesting buying opportunities.

• Red Cloud: Indicates a strong downtrend, signaling potential short trades.

• Gray Cloud: Reflects a range-bound market, helping you avoid low-momentum periods.

• Dynamic Volume Integration: The cloud thickness adjusts dynamically with trading volume, highlighting strong trends supported by high market activity.

📈 Strength & Momentum Analysis:

• Strength Filtering: The ADX component ensures that only strong trends are highlighted, filtering out market noise and reducing false signals.

• Visual Momentum Gauge: The cloud color and thickness provide a quick visual representation of market momentum, enabling faster decision-making.

🔔 Alerts:

• Custom Alerts: Set up alerts for when the trend shifts or reaches critical levels, keeping you informed without needing to constantly monitor the chart.

🎨 Visual Enhancements:

• Gradient Cloud & Shadows: The indicator features a gradient-filled cloud with shadowed moving averages, enhancing both aesthetics and clarity on your charts.

• Adaptive Visual Cues: MomentumCloud.V33’s color transitions and dynamic thickness provide an intuitive feel for the market’s rhythm.

🚀 Quick Guide to Using MomentumCloud.V33

1. Add the Indicator: Start by adding MomentumCloud.V33 to your chart. Customize the settings such as MA periods, DMI length, and volume multiplier to match your trading style.

2. Analyze the Market: Observe the color-coded cloud and its thickness to gauge market momentum and trend direction. The thicker the cloud, the stronger the trend.

3. Set Alerts: Activate alerts for trend changes or key levels to capture trading opportunities without needing to watch the screen continuously.

⚙️ How It Works:

MomentumCloud.V33 calculates market momentum by combining moving averages, DMI, and volume. The cloud color changes based on the trend direction, while its thickness reflects the strength of the trend as influenced by trading volume. This integrated approach ensures you can quickly identify robust market movements, making it easier to enter and exit trades at optimal points.

Settings Overview:

• Moving Averages: Define the lengths for the fast and slow moving averages.

• DMI & ADX: Adjust the DMI length and ADX smoothing to focus on significant trends.

• Volume Multiplier: Customize the multiplier to control cloud thickness, highlighting volume-driven trends.

📚 How to Use MomentumCloud.V33:

• Trend Identification: The direction and color of the cloud indicate the prevailing trend, while the cloud’s thickness suggests the trend’s strength.

• Trade Execution: Use the green cloud to look for long entries and the red cloud for short positions. The gray cloud advises caution, as it represents a range-bound market.

• Alerts: Leverage the custom alerts to stay on top of market movements and avoid missing critical trading opportunities.

Unleash the power of trend and momentum analysis with MomentumCloud.V33! Happy trading! 📈🚀✨

Multi-Step FlexiSuperTrend - Indicator [presentTrading]This version of the indicator is built upon the foundation of a strategy version published earlier. However, this indicator version focuses on providing visual insights and alerts for traders, rather than executing trades. This one is mostly for @thorcmt.

█ Introduction and How it is Different

The **Multi-Step FlexiSuperTrend Indicator** is a versatile tool designed to provide traders with a highly customizable and flexible approach to trend analysis. Unlike traditional supertrend indicators, which focus on a single factor or threshold, the **FlexiSuperTrend** allows users to define multiple levels of take-profit targets and incorporate different trend normalization methods.

It comes with several advanced customization features, including multi-step take profits, deviation plotting, and trend normalization, making it suitable for both novice and expert traders.

BTCUSD 6hr Performance

█ Strategy, How It Works: Detailed Explanation

The **Multi-Step FlexiSuperTrend** works by calculating a supertrend based on multiple factors and incorporating oscillations from trend deviations. Here’s a breakdown of how it functions:

🔶 SuperTrend Calculation

At the heart of the indicator is the SuperTrend formula, which dynamically adjusts based on price movements.

🔶 Normalization of Deviations

To enhance accuracy, the **FlexiSuperTrend** calculates multiple deviations from the trend and normalizes them.

🔶 Multi-Step Take Profit Levels

The indicator allows setting up to three take profit levels, which are displayed via price level alerts. lows traders to exit part of their position at various profit intervals.

For more detail, please check the strategy version - Multi-Step-FlexiSuperTrend-Strategy:

and 'FlexiSuperTrend-Strategy'

█ Trade Direction

The **Multi-Step FlexiSuperTrend Indicator** supports both long and short trade directions.

This flexibility allows traders to adapt to trending, volatile, or sideways markets.

█ Usage

To use the **FlexiSuperTrend Indicator**, traders can set up their preferences for the following key features:

- **Trading Direction**: Choose whether to focus on long, short, or both signals.

- **Indicator Source**: The price source to calculate the trend (e.g., close, hl2).

- **Indicator Length**: The number of periods to calculate the ATR and trend (the larger the value, the smoother the trend).

- **Starting and Increment Factor**: These adjust how reactive the trend is to price movements. The starting factor dictates how far the initial trend band is from the price, and the increment factor adjusts subsequent trend deviations.

The indicator then displays buy and sell signals on the chart, along with alerts for each take-profit level.

Local picture

█ Default Settings

The default settings of the **Multi-Step FlexiSuperTrend** are carefully designed to provide an optimal balance between sensitivity and accuracy. Let’s examine these default parameters and their effect on performance:

🔶 Indicator Length (Default: 10)

The **Indicator Length** determines the lookback period for the ATR calculation. A smaller value makes the indicator more reactive to price changes, but may generate more false signals. A longer length smooths the trend and reduces noise but may delay signals.

Effect on performance: Shorter lengths perform better in volatile markets, while longer lengths excel in trending markets.

🔶 Starting Factor (Default: 0.618)

This factor adjusts the starting distance of the SuperTrend from the current price. The smaller the starting factor, the closer the trend is to the price, making it more sensitive. Conversely, a larger factor allows more distance, reducing sensitivity but filtering out false signals.

Effect on performance: A smaller factor provides quicker signals but can lead to frequent false positives. A larger factor generates fewer but more reliable signals.

🔶 Increment Factor (Default: 0.382)

The **Increment Factor** controls how the trend bands adjust as the price moves. It increases the distance of the bands from the price with each iteration.

Effect on performance: A higher increment factor can result in wider stop-loss or trend reversal bands, allowing for longer trends to develop without frequent exits. A lower factor keeps the bands closer to the price and is more suited for shorter-term trades.

🔶 Take Profit Levels (Default: 2%, 8%, 18%)

The default take-profit levels are set at 2%, 8%, and 18%. These values represent the thresholds at which the trader can partially exit their positions. These multi-step levels are highly customizable depending on the trader’s risk tolerance and strategy.

Effect on performance: Lower take-profit levels (e.g., 2%) capture small, quick profits in volatile markets, while higher levels (8%-18%) allow for a more gradual exit in strong trends.

🔶 Normalization Method (Default: None)

The default normalization method is **None**, meaning the deviations are not normalized. However, enabling normalization (e.g., **Max-Min**) can improve the clarity of the indicator’s signals in volatile or choppy markets by smoothing out the noise.

Effect on performance: Using a normalization method can reduce the effect of extreme deviations, making signals more stable and less prone to false positives.

MCDX+RSI+SMA[THANHCONG]### Detailed Analysis of the MCDX+RSI+SMA Indicator

The MCDX+RSI+SMA indicator is designed to help investors conduct a deeper analysis of market trends by combining multiple technical factors into a single chart. This integration of popular indicators such as RSI, SMA, and Stochastic RSI provides investors with a comprehensive view of market movements, particularly in distinguishing between "Banker" and "Hot Money"—representing large and small capital flows.

#### Key Components of the Indicator:

1. **RSI for Banker and Hot Money:**

- **RSI (Relative Strength Index)** is a momentum oscillator that measures the speed and change of price movements, indicating overbought or oversold conditions. In this indicator, there are two distinct RSI lines configured for Banker (large capital) and Hot Money (small capital).

- Investors can adjust parameters like the RSI calculation period, baseline levels, and sensitivity for each type of capital flow, providing flexibility to adapt to varying market conditions.

2. **Moving Average (MA) of RSI:**

- The indicator employs two common types of Moving Averages: **SMA (Simple Moving Average)** and **EMA (Exponential Moving Average)**. These help smooth the RSI signals for Banker, offering a clearer view of the long-term trend of large capital in the market.

- Investors can select the type and period of the MA, allowing them to optimize the indicator for their trading style.

3. **Stochastic RSI:**

- The **Stochastic RSI** is incorporated to monitor overbought and oversold conditions over a specified timeframe. Parameters related to %K and %D of the Stochastic can also be adjusted to refine the accuracy of market signal analysis.

- A notable feature is the normalization of %K and %D on a 0-20 scale, making these lines compatible with other RSI charts, thus providing consistency in evaluating market strength.

4. **Overbought and Oversold Levels:**

- The indicator includes reference lines for overbought and oversold levels, aiding investors in identifying potential reversal zones in the market. This helps to avoid buying at excessively high prices or selling at excessively low prices.

#### Benefits for Investors:

- **Comprehensive View:** The indicator combines insights from both large (Banker) and small (Hot Money) capital flows, enabling investors to analyze not just trends but also the participation of each type of capital in the market.

- **Enhanced Technical Analysis:** By integrating multiple technical indicators within a single chart, investors can track important factors such as market momentum, overbought/oversold conditions, and capital flow shifts without needing to switch between various charts.

- **Flexibility and Customization:** The indicator allows adjustment of key parameters like the RSI period, sensitivity, type of MA, and Stochastic RSI settings, enabling investors to tailor the indicator to their trading strategy and timeframe.

- **Higher Reliability:** The combination of indicators like RSI, Stochastic RSI, and MA helps investors confirm trading signals more confidently. For instance, when both RSI and Stochastic RSI indicate overbought conditions, the likelihood of a reversal may be higher, reducing risk for investors.

#### Unique Features of the Indicator:

The MCDX+RSI+SMA indicator is a unique tool that integrates various market analysis factors into a single framework. This not only provides investors with a complete view of capital flows but also aids in optimizing decision-making based on multiple market aspects. Furthermore, its customizable parameters make it suitable for various trading strategies, from short-term to long-term.

S&R Precision Cloud by Dr. Abiram Sivprasad -4 directional biasDescription of the Script

**Script Name:** S&R Precision Cloud by Dr. Abhiram Sivprasad

**Overview:**

This script is designed to identify key support and resistance levels using the Central Pivot Range (CPR) methodology along with daily, weekly, and monthly pivots. It incorporates the Lagging Span from the Ichimoku Cloud to enhance decision-making in trading strategies for intraday, swing, and long-term positions mainly for directional bias.

---

### Key Components:

1. **Central Pivot Range (CPR):**

- **Central Pivot (CP):** Calculated as the average of the high, low, and close prices. This serves as a reference point for price action.

- **Below Central Pivot (BC) and Top Central Pivot (TC):** Derived to create a range that aids in identifying support and resistance levels.

2. **Support and Resistance Levels:**

- The script computes three support (S1, S2, S3) and resistance (R1, R2, R3) levels based on the Central Pivot.

- These levels are plotted for daily, weekly, and monthly time frames, providing traders with multiple reference points.

3. **Lagging Span:**

- The Lagging Span is plotted as the closing price shifted backward by 26 periods (as per Ichimoku settings).

- This serves as a filter for trade entries, where positions should only be taken in the direction opposite to where the price is relative to this line.

4. **User Inputs:**

- The script allows customization through checkboxes to plot daily, weekly, and monthly support and resistance levels as needed.

- Users can choose whether to display CPR and various support/resistance levels for better visual clarity.

5. **Color Coding:**

- The support and resistance lines are color-coded to distinguish between different levels (green for support, red for resistance, and blue for pivots).

---

### Trading Strategies:

- **Intraday Trading:**

- Utilize price movements around the Lagging Span and support/resistance levels for quick trades.

- **Swing Trading:**

- Identify potential reversal points at S2 and R2 levels, confirmed by divergences in price movement.

- **Long-Term Trading:**

- Monitor price behavior against the Lagging Span and significant pivot levels to capture longer trends.

---

### Summary:

This script equips traders with essential tools for technical analysis by clearly defining critical price levels and incorporating the Lagging Span for directional bias. It is suitable for various trading styles, including intraday, swing, and long-term strategies, making it a versatile addition to any trader’s toolkit.

Optimized Comprehensive Analysis Table# Enhanced Comprehensive Analysis Table

This advanced indicator provides a holistic view of market sentiment by analyzing multiple technical indicators simultaneously. It's designed to give traders a quick, at-a-glance summary of market conditions across various timeframes and analysis methods.

## Key Features:

- Analyzes 9 popular technical indicators

- Weighted voting system for overall market sentiment

- Customizable indicator weights

- Clear, color-coded table display

## Indicators Analyzed:

1. MACD (Moving Average Convergence Divergence)

2. RSI (Relative Strength Index)

3. Moving Averages (50, 100, 200-period)

4. Stochastic Oscillator

5. Parabolic SAR

6. MFI (Money Flow Index)

7. CCI (Commodity Channel Index)

8. OBV (On Balance Volume)

9. ADX (Average Directional Index)

## How It Works:

Each indicator's signal is calculated and classified as bullish, bearish, or neutral. These signals are then weighted according to user-defined inputs. The weighted votes are summed to determine an overall market sentiment.

## Interpretation:

- The table displays the state of each indicator and the overall market sentiment.

- Green indicates bullish conditions, red bearish, and yellow neutral.

- The "Overall State" row at the bottom provides a quick summary of the combined analysis.

## Customization:

Users can adjust the weight of each indicator to fine-tune the analysis according to their trading strategy or market conditions.

This indicator is ideal for traders who want a comprehensive overview of market conditions without having to monitor multiple indicators separately. It's particularly useful for confirming trade setups, identifying potential trend reversals, and managing risk.

Note: This indicator is meant to be used as part of a broader trading strategy. Always combine with other forms of analysis and proper risk management.

The Strat Candle State Table (Two Symbols)The Strat Candle State Table (Two Symbols) – Multi-Timeframe Analysis

This advanced indicator is designed for traders who follow The Strat methodology, providing a quick, clear, and actionable view of candle states across two selected symbols and a chosen timeframe. It allows you to seamlessly integrate multi-symbol analysis into your trading, offering real-time insights into price action and market momentum based on **The Strat’s** powerful principles.

What It Does:

For each selected symbol, the indicator retrieves and analyzes the price data for three candles:

- Candle 1 (C1): The third candle from the current one.

- Candle 2 (C2): The candle directly before the current one (previous candle).

- Current Candle (CC): The live candle, which is still forming.

Using this information, it plots the Scenario 1 (Inside Bar), Scenario 2 (Directional), and **Scenario 3 (Outside Bar)** states for each candle, color-coding them to help you quickly assess market conditions and price action.

Strat Candle States:

- Scenario 1 (Inside Bar): The candle stays within the high and low of the previous candle (indicating consolidation or indecision).

- Scenario 2 (Directional)* The candle breaks either the high (2-up) or low (2-down) of the previous candle, indicating potential continuation in that direction.

- Scenario 3 (Outside Bar): The candle breaks both the high and low of the previous candle, signaling increased volatility and a potential reversal.

Customizable Color Scheme:

The default colors follow these settings (but can be changed to your preference):

- 1U (Inside and Up): Yellow (indicating an inside bar that closed higher).

- 1D (Inside and Down): Orange (indicating an inside bar that closed lower).

- 2U (Two Up): Green if the candle closes higher, Red if the candle closes lower (conflict).

- 2D (Two Down): Red if the candle closes lower, Green if the candle closes higher (conflict).

- 3U (Three Up): Lighter Purple.

- 3D (Three Down): Darker Purple/Magenta.

Each state is dynamically updated based on the actual price action and whether the candle closes above or below the open. Conflict candles (like a 2-up closing red or 2-down closing green) are highlighted, making it easier to spot potential reversals or weakness in the trend.

Timeframe Flexibility:

You can overlay this indicator on any chart regardless of the timeframe. The key is to select the timeframe you want the indicator to plot for when setting up. Whether you're working on a 5-minute chart, daily, or even weekly, the indicator will analyze the candles according to the selected timeframe, giving you the versatility to adapt it to various trading strategies.

Powerful Use Cases:

1. Multi-Symbol Analysis in Real-Time: The Strat Candle State Table displays the candle states for two symbols at once, helping you track multiple instruments without switching charts. This is extremely useful when monitoring correlated assets like SPY and QQQ, or sector-related pairs such as DIA and IWM

2. Seamless Top-Down View: By analyzing the three most recent candles (C1, C2, and the current candle), the indicator allows you to maintain a top-down perspective on price action, spotting setups early and tracking candle state changes across different symbols and timeframes.

3. Enhanced Conflict Detection: The background shading automatically adjusts for conflict candles, such as a 2-up that closes red or a 2-down that closes green. This provides a quick visual cue to warn you when the current trend may be weakening or reversing.

4. Trade Execution Precision: With this table providing constant feedback on price action and candle state, traders can more easily time their entries and exits, whether they are looking for reversals or continuations

5. Focus on Timeframe Continuity: Use this indicator to stay in alignment with The Strat's Timeframe Continuity, ensuring you are trading in the direction of the most aligned candles, across both symbols. This allows for more precise trade management and higher-probability setups.

6. Customizable to Your Strategy: Change the color coding and candle states to match your personal preferences or trading strategy, making this indicator adaptable to your specific needs.

Most Powerful Use Case – Simultaneous Break Detection:

The Strat Candle State Table shines in setups where simultaneous breaks are being monitored across multiple symbols. For example, if both symbols trigger a 2-up or 3-up at the same time, this confirms that momentum is flowing in the same direction for multiple instruments, giving you stronger trade conviction.

By seeing real-time data for two key symbols, you can ensure that you're catching simultaneous breaks, where multiple instruments are signaling the same move. This can be especially effective in index-based trading, where the strength or weakness of multiple sectors or assets must align for a higher probability of success

Connors RSI with Down GapThe Connors RSI with Down Gap indicator is a technical tool designed to support Larry Connors' Terror Gap Strategy, which is part of his broader framework outlined in the book "Buy the Fear, Sell the Greed: 7 Behavioral Quant Strategies for Traders." This specific indicator integrates the ConnorsRSI calculation with a focus on detecting down gaps in price, providing insights into moments when panic selling may occur.

The ConnorsRSI

ConnorsRSI is a composite indicator developed by Larry Connors that combines three core components:

RSI: A short-term relative strength index measuring the speed and magnitude of price changes.

Streak RSI: Tracks consecutive up or down closes to assess momentum.

Percent Rank: Evaluates how the current close ranks in relation to past prices.

When combined, these three elements provide a nuanced view of short-term overbought or oversold conditions. ConnorsRSI readings below a certain threshold (commonly 30 or lower) suggest that the asset has been heavily sold, indicating potential exhaustion of selling pressure.

Behavioral Finance Insights

The Terror Gap Strategy is grounded in principles from behavioral finance, which studies how psychological factors affect market participants' decision-making. Specifically, the indicator exploits the fear and irrational behavior that often arise when traders face persistent losses, especially after a down gap. According to behavioral finance theories like prospect theory (Kahneman & Tversky, 1979), people tend to overreact to losses, leading to panic selling. This creates opportunities for contrarian traders who understand the psychology behind these market movements.

The ConnorsRSI with Down Gap indicator works because it identifies:

Overextended selling through the ConnorsRSI, where persistent price declines result in low RSI values (indicating panic).

Gap down days, where the opening price is below the previous day’s close, typically amplifying the sense of loss and fear for traders already in losing positions.

Why This Indicator Works

The psychology of losses makes traders more prone to selling during periods of fear, especially when confronted with a gap down after sustained price declines. This indicator, by combining ConnorsRSI with down gaps, offers a quantitative way to spot these moments of panic. Traders can take advantage of these signals to enter positions when the market is in a state of fear, often when there is potential for a reversion to the mean.

Indicator Mechanics

In the current implementation:

The ConnorsRSI is calculated using three components: a short-term RSI, streak RSI, and percent rank.

When the ConnorsRSI drops below a user-defined lower threshold, the indicator highlights oversold conditions.

If there is a down gap (open price lower than the previous close) and the ConnorsRSI is below the threshold, a label is displayed, signaling a potential opportunity to buy.

Practical Use and Application

For traders looking to implement the Terror Gap Strategy, this indicator provides a clear visual cue (via background coloring and labels) when conditions are ripe for a contrarian trade. It can be particularly useful for traders who thrive on taking advantage of fear-driven sell-offs.

However, to fully understand and apply this strategy effectively, it is recommended to purchase Larry Connors' book "Buy the Fear, Sell the Greed." The book provides detailed explanations of how to execute the strategy with precision, including insights into exit conditions, scaling into positions, and managing risk.

Conclusion

The ConnorsRSI with Down Gap indicator combines quantitative analysis with behavioral finance principles to exploit fear-driven market behavior. By utilizing this tool within a disciplined trading strategy, traders can potentially profit from temporary market inefficiencies caused by panic selling.

References

Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263-291.

Connors, L. (2013). Buy the Fear, Sell the Greed: 7 Behavioral Quant Strategies for Traders.

This indicator can be a valuable asset, but understanding its proper use within a broader strategy framework is essential. Purchasing Connors' book is a recommended step toward mastering the approach.

Larry Conners SMTP StrategyThe Spent Market Trading Pattern is a strategy developed by Larry Connors, typically used for short-term mean reversion trading. This strategy takes advantage of the exhaustion in market momentum by entering trades when the market is perceived as "spent" after extended trends or extreme moves, expecting a short-term reversal. Connors uses indicators like RSI (Relative Strength Index) and price action patterns to identify these opportunities.

Key Elements of the Strategy:

Overbought/Oversold Conditions: The strategy looks for extreme overbought or oversold conditions, often indicated by low RSI values (below 30 for oversold and above 70 for overbought).

Mean Reversion: Connors believed that markets, especially in short-term scenarios, tend to revert to the mean after periods of strong momentum. The "spent" market is assumed to have expended its energy, making a reversal likely.

Entry Signals:

In an uptrend, a stock or market index making a significant number of consecutive up days (e.g., 5-7 consecutive days with higher closes) indicates overbought conditions.

In a downtrend, a similar number of consecutive down days indicates oversold conditions.

Reversal Anticipation: Once an extreme in price movement is identified (such as consecutive gains or losses), the strategy places trades anticipating a reversion to the mean, which is usually the 5-day or 10-day moving average.

Exit Points: Trades are exited when prices move back toward their mean or when the extreme conditions dissipate, usually based on RSI or moving average thresholds.

Why the Strategy Works:

Human Psychology: The strategy capitalizes on the fact that markets, in the short term, often behave irrationally due to the emotions of traders—fear and greed lead to overextended moves.

Mean Reversion Tendency: Financial markets often exhibit mean-reverting behavior, where prices temporarily deviate from their historical norms but eventually return. Short-term exhaustion after a strong rally or sell-off offers opportunities for quick profits.

Overextended Moves: Markets that rise or fall too quickly tend to become overextended, as buyers or sellers get exhausted, making reversals more probable. Connors’ approach identifies these moments when the market is "spent" and ripe for a reversal.

Risks of the Spent Market Trading Pattern Strategy:

Trend Continuation: One of the key risks is that the market may not revert as expected and instead continues in the same direction. In trending markets, mean-reversion strategies can suffer because strong trends can last longer than anticipated.

False Signals: The strategy relies heavily on technical indicators like RSI, which can produce false signals in volatile or choppy markets. There can be times when a market appears "spent" but continues in its current direction.

Market Timing: Mean reversion strategies often require precise market timing. If the entry or exit points are mistimed, it can lead to losses, especially in short-term trades where small price movements can significantly impact profitability.

High Transaction Costs: This strategy requires frequent trades, which can lead to higher transaction costs, especially in markets with wide bid-ask spreads or high commissions.

Conclusion:

Larry Connors’ Spent Market Trading Pattern strategy is built on the principle of mean reversion, leveraging the concept that markets tend to revert to a mean after extreme moves. While effective in certain conditions, such as range-bound markets, it carries risks—especially during strong trends—where price momentum may not reverse as quickly as expected.

For a more in-depth explanation, Larry Connors’ books such as "Short-Term Trading Strategies That Work" provide a comprehensive guide to this and other strategies .

Connors VIX Reversal III invented by Dave LandryThis strategy is based on trading signals derived from the behavior of the Volatility Index (VIX) relative to its 10-day moving average. The rules are split into buying and selling conditions:

Buy Conditions:

The VIX low must be above its 10-day moving average.

The VIX must close at least 10% above its 10-day moving average.

If both conditions are met, a buy signal is generated at the market's close.

Sell Conditions:

The VIX high must be below its 10-day moving average.

The VIX must close at least 10% below its 10-day moving average.

If both conditions are met, a sell signal is generated at the market's close.

Exit Conditions:

For long positions, the strategy exits when the VIX trades intraday below its previous day’s 10-day moving average.

For short positions, the strategy exits when the VIX trades intraday above its previous day’s 10-day moving average.

This strategy is primarily a mean-reversion strategy, where the market is expected to revert to a more normal state after the VIX exhibits extreme behavior (i.e., large deviations from its moving average).

About Dave Landry

Dave Landry is a well-known figure in the world of trading, particularly in technical analysis. He is an author, trader, and educator, best known for his work on swing trading strategies. Landry focuses on trend-following and momentum-based techniques, teaching traders how to capitalize on shorter-term price swings in the market. He has written books like "Dave Landry on Swing Trading" and "The Layman's Guide to Trading Stocks," which emphasize practical, actionable trading strategies.

About Connors Research

Connors Research is a financial research firm known for its quantitative research in financial markets. Founded by Larry Connors, the firm specializes in developing high-probability trading systems based on historical market behavior. Connors’ work is widely respected for its data-driven approach, including systems like the RSI(2) strategy, which focuses on short-term mean reversion. The firm also provides trading education and tools for institutional and retail traders alike, emphasizing strategies that can be backtested and quantified.

Risks of the Strategy

While this strategy may appear to offer promising opportunities to exploit extreme VIX movements, it carries several risks:

Market Volatility: The VIX itself is a measure of market volatility, meaning the strategy can be exposed to sudden and unpredictable market swings. This can result in whipsaws, where positions are opened and closed in rapid succession due to sharp reversals in the VIX.

Overfitting: Strategies based on specific conditions like the VIX closing 10% above or below its moving average can be subject to overfitting, meaning they work well in historical tests but may underperform in live markets. This is a common issue in quantitative trading systems that are not adaptable to changing market conditions .

Mean-Reversion Assumption: The core assumption behind this strategy is that markets will revert to their mean after extreme movements. However, during periods of sustained trends (e.g., market crashes or rallies), this assumption may break down, leading to prolonged drawdowns.

Liquidity and Slippage: Depending on the asset being traded (e.g., S&P 500 futures, ETFs), liquidity issues or slippage could occur when executing trades at market close, particularly in volatile conditions. This could increase costs or worsen trade execution.

Scientific Explanation of the Strategy

The VIX is often referred to as the "fear gauge" because it measures the market's expectations of volatility based on options prices. Research has shown that the VIX tends to spike during periods of market stress and revert to lower levels when conditions stabilize . Mean reversion strategies like this one assume that extreme VIX levels are unsustainable in the long run, which aligns with findings from academic literature on volatility and market behavior.

Studies have found that the VIX is inversely correlated with stock market returns, meaning that higher VIX levels often correspond to lower stock prices and vice versa . By using the VIX’s relationship with its 10-day moving average, this strategy aims to capture reversals in market sentiment. The 10% threshold is designed to identify moments when the VIX is significantly deviating from its norm, signaling a potential reversal.

However, academic research also highlights the limitations of relying on the VIX alone for trading signals. The VIX does not predict market direction, only volatility, meaning that it cannot indicate the magnitude of price movements . Furthermore, extreme VIX levels can persist longer than expected, particularly during financial crises.

In conclusion, while the strategy is grounded in well-established financial principles (e.g., mean reversion and the relationship between volatility and market performance), it carries inherent risks and should be used with caution. Backtesting and careful risk management are essential before applying this strategy in live markets.

No Buyers or Sellers (Volume Threshold)This indicator shows areas on the second or minute charts that lack buyer or seller activity in the form of volume. This is configurable in the code itself by the user.

This can be used to close a trade because there is no desire shown by the market to continue the trend.

TRIN (Arms Index) Trading StrategyThe TRIN (Arms Index), also known as the Short-Term Trading Index, is a technical indicator designed to gauge the internal strength or weakness of the market. It compares the number of advancing and declining stocks to the advancing and declining volume (AD Volume). A TRIN value above 1.0 generally indicates bearish market conditions, while a value below 1.0 suggests bullish market sentiment.

Strategy Rules:

Entry Condition (Long Position): When the TRIN value is above 1.0, the strategy enters a long position, indicating that the market may be oversold, and a potential reversal could occur.

Exit Condition: The strategy exits the long position when the closing price is higher than the previous day’s high, signaling a potential rebound in the market.

This strategy aims to capitalize on short-term market inefficiencies by entering trades during periods of potential market weakness and exiting when signs of recovery appear.

How the TRIN Index Works:

The TRIN is calculated as follows:

TRIN=Advancing Issues / Declining IssuesAdvancing Volume / Declining Volume

TRIN=Advancing Volume / Declining VolumeAdvancing Issues / Declining Issues

A TRIN value above 1.0 indicates that the market is potentially oversold (more declining stocks with higher volume), while a value below 1.0 suggests the market may be overbought (more advancing stocks with higher volume) .

Empirical Evidence:

Market Sentiment Indicator: The TRIN has been widely used as a sentiment indicator. Research by Zweig (1997) suggests that extreme TRIN values can serve as a contrarian signal, indicating potential turning points in the market. For instance, a TRIN above 2.0 is often considered a sign of panic selling, which can precede a market bottom .

Overbought/Oversold Conditions: Studies have shown that indicators like TRIN, which measure market breadth and volume, can be effective in identifying overbought and oversold conditions. According to Fama and French (1988), market sentiment indicators that consider both price and volume data can offer insights into future price movements .

Risks and Limitations:

False Signals:

One of the primary risks of using the TRIN-based strategy is the possibility of false signals. A TRIN value above 1.0 does not always guarantee a market rebound, especially in sustained bearish trends. In such cases, the strategy might enter long positions prematurely, leading to losses.

Research by Brock, Lakonishok, and LeBaron (1992) found that while market indicators like TRIN can be useful, they are not foolproof and can generate multiple false positives, particularly in volatile markets .

Market Regimes:

The effectiveness of the TRIN index can vary depending on the market regime. In strongly trending markets, either bullish or bearish, the TRIN may not provide reliable reversal signals, and relying on it could result in trades that go against the prevailing trend. For instance, during strong bear markets, the TRIN may frequently remain above 1.0, leading to multiple losing trades as the market continues to decline.

Short-Term Focus:

The TRIN strategy is inherently short-term focused, aiming to capture quick market reversals. This makes it sensitive to market noise and less effective for longer-term investors. Moreover, short-term trading strategies often require more frequent adjustments and can incur higher transaction costs, which may erode profitability over time.

Liquidity and Execution Risk:

Since the TRIN strategy requires entering and exiting trades based on short-term market movements, it is vulnerable to liquidity and execution risks. In fast-moving markets, the execution of trades may be delayed, leading to slippage and potentially unfavorable entry or exit points.

Conclusion:

The TRIN (Arms Index) Trading Strategy can be an effective tool for traders looking to capitalize on short-term market inefficiencies and potential reversals. However, it is important to recognize the risks associated with this strategy, including false signals, sensitivity to market regimes, and execution risks. Traders should employ proper risk management techniques and consider combining the TRIN with other indicators to improve the robustness of the strategy.

While the TRIN provides valuable insights into market sentiment, it is not a standalone solution and should be used in conjunction with a broader trading plan that takes into account both technical and fundamental analysis.

References:

Arms, Richard W. "Volume Adjusted Moving Averages." Technical Analysis of Stocks & Commodities, 1993.

Zweig, Martin. Winning on Wall Street. Warner Books, 1997.

Fama, Eugene F., and Kenneth R. French. "Permanent and Temporary Components of Stock Prices." Journal of Political Economy, 1988.

Brock, William, Josef Lakonishok, and Blake LeBaron. "Simple Technical Trading Rules and the Stochastic Properties of Stock Returns." Journal of Finance, 1992.

S&P500 Market Breadth /MA20Introduction

It calculates the percentage of assets trading above their 20-day moving average (MA20), providing a clear view of market breadth and highlighting the strength of an uptrend or downtrend.

Features

• Market Breadth Analysis: The MA20 Market Breadth Indicator tracks the number of assets trading above their 20-day moving average, offering an intuitive view of the proportion of rising versus falling assets. A high breadth suggests a strong uptrend, while low breadth indicates that most assets are in a downtrend.

• Trend Following: This indicator allows traders to easily identify whether the overall market trend is healthy and upward or potentially weakening and downward.

• Simple and Intuitive: The breadth is displayed as a percentage, enabling users to quickly assess market conditions and make informed decisions.

How to Use

1. Assess Market Sentiment: When the MA20 market breadth is above the 50% zone, it indicates that the market is in a broad uptrend, favoring long positions. When it falls below 50%, it signals downward pressure, making it a time for caution or short opportunities.

2. Spot Trend Reversals: Sudden changes in market breadth, such as a sharp decline from a high level, can indicate an upcoming market reversal or correction, signaling traders to adjust their positions.

3. Confirm Trends: Combine the MA20 market breadth with other indicators, such as momentum or volume, to further validate the overall direction of the market.

Applicable Markets

This indicator works across various markets and asset classes, including but not limited to:

• Stock markets (indices and individual stocks)

• Cryptocurrencies

• Forex markets

Conclusion

The MA20 Market Breadth Indicator provides traders with a clear picture of market health, helping to identify broader trends and confirm shifts in market sentiment. It’s an essential tool for traders of all types, particularly those focused on medium to short-term trend following and market reversals.

Disclaimer

This indicator is for educational purposes only. Please use it in conjunction with your own trading strategies and adjust according to your risk tolerance.

This introduction should work well for your TradingView release. You can adjust it as needed for specific features or updates in the indicator.

TradeTracker v33 - Interactive Journal [AR33_]TradeTracker v33 - Interactive Journal is a unique tool designed to enhance your trading experience by integrating an interactive journal directly onto your charts. Unlike traditional trading journals that require manual entries outside of TradingView, this script allows traders to document, track, and review their trades in real-time, right where the action happens.

What sets TradeTracker v33 apart from existing tools is its seamless blend of note-taking, task management, and performance tracking—all within a single, intuitive interface. With features like customizable checklists, due dates, and color-coded status indicators, this script provides a powerful and practical solution for traders who want to stay organized and disciplined.

2. Description

. TradeTracker v33 - Interactive Journal is designed to keep traders on track by allowing them to record trade-related notes, set tasks, and mark progress directly on their charts.

Here’s how it works:

• Purpose: The script serves as an all-in-one journal and task manager, helping traders document their trading strategies, track ongoing tasks, and review completed actions. It’s particularly useful for maintaining discipline and ensuring that every trade is executed according to a well-thought-out plan.

• How It Works:

• Interactive Notes and Tasks: Users can create and manage notes and tasks directly on their charts. Each note can be customized with a title, description, due date, and completion status.

• Status Indicators: Tasks are color-coded based on their status—green for completed, red for overdue, and default colors for pending tasks—allowing traders to quickly assess their progress.

• Dynamic Display: Notes are displayed in a clean, organized table on the chart, making it easy to review multiple tasks without cluttering the trading interface.

• Usage:

• Adding Notes: Simply fill in the note title, content, and optional due date within the script’s input settings, and the note will appear on your chart.

• Tracking Progress: Mark tasks as completed with a simple toggle, and the script will update their status in real-time.

• Customizing Your Workflow: Adjust the position, size, and visibility of notes to fit your trading style, ensuring that your journal supports rather than distracts from your trading activities.

3. Chart Presentation

To provide a clear and focused user experience, TradeTracker v33 - Interactive Journal is designed to be the sole feature on your chart when published. This ensures that users can easily identify and interact with their notes and tasks without any unnecessary distractions.

• Clean and Focused Display: The chart will exclusively display the interactive journal, showcasing how tasks and notes appear and update in real-time as you manage them.

• Useful Annotations: Annotations such as checkboxes and status indicators are clearly explained within the script’s description and are vital to understanding the functionality of the tool.

• Minimal Distractions: Only elements directly related to the script’s functionality are included on the chart, ensuring that users can easily follow along and implement the script in their own trading setup.

True Strength Index with Buy/Sell Signals and AlertsThe True Strength Index (TSI) is a momentum oscillator that helps traders identify trends and potential reversal points in the market. Here’s how it works:

1. **Price Change Calculation**:

- **`pc = ta.change(price)`**: This calculates the change in price (current price minus the previous price).

2. **Double Smoothing**:

- **`double_smooth(src, long, short)`**: This function smooths the price change data twice using two Exponential Moving Averages (EMAs):

- The first EMA smooths the raw data.

- The second EMA smooths the result of the first EMA.

- **`double_smoothed_pc`**: The double-smoothed price change.

- **`double_smoothed_abs_pc`**: The double-smoothed absolute price change, which helps normalize the TSI value.

3. **TSI Calculation**:

- **`tsi_value = 100 * (double_smoothed_pc / double_smoothed_abs_pc)`**: This calculates the TSI by dividing the double-smoothed price change by the double-smoothed absolute price change, then multiplying by 100 to scale the value.

- The TSI oscillates around the zero line, indicating momentum. Positive values suggest bullish momentum, while negative values suggest bearish momentum.

4. **Signal Line**:

- **`signal_line = ta.ema(tsi_value, signal)`**: This creates a signal line by applying another EMA to the TSI value. The signal line is typically used to identify entry and exit points.

5. **Buy and Sell Signals**:

- **Buy Signal**: Occurs when the TSI crosses above the signal line (`ta.crossover(tsi_value, signal_line)`), indicating that bullish momentum is strengthening, which might suggest a buying opportunity.

- **Sell Signal**: Occurs when the TSI crosses below the signal line (`ta.crossunder(tsi_value, signal_line)`), indicating that bearish momentum is strengthening, which might suggest a selling opportunity.

6. **Visual Representation**:

- The TSI line and the signal line are plotted on the chart.

- Buy signals are marked with green "BUY" labels below the bars, and sell signals are marked with red "SELL" labels above the bars.

**How to Use It**:

- **Trend Identification**: When the TSI is above zero, it suggests an uptrend; when it's below zero, it suggests a downtrend.

- **Buy/Sell Signals**: Traders often enter a buy trade when the TSI crosses above the signal line and enter a sell trade when the TSI crosses below the signal line.

- **Divergences**: TSI can also be used to spot divergences between the indicator and price action, which can signal potential reversals.

The TSI is particularly useful in identifying the strength of a trend and the potential turning points, making it valuable for trend-following and swing trading strategies.

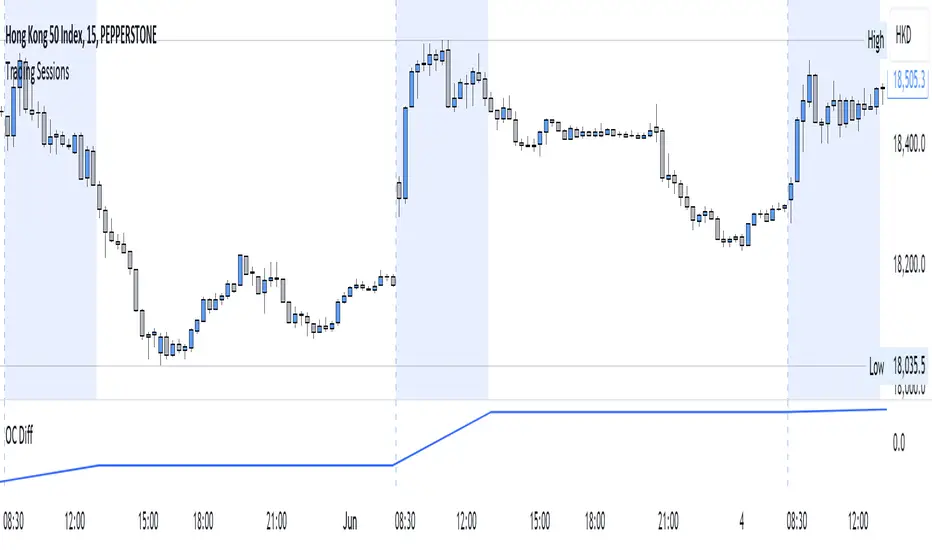

Open-Close Price DifferenceInput time A (open time) and time B (closing time)

do not do anything with the year-month-date, it's there because I don't know how to fix it and it needs to be in such format.

the difference of price will be shown on the indicator window one candle after the closing time (opening at such time)

For research purpose only, no other intended purposes.

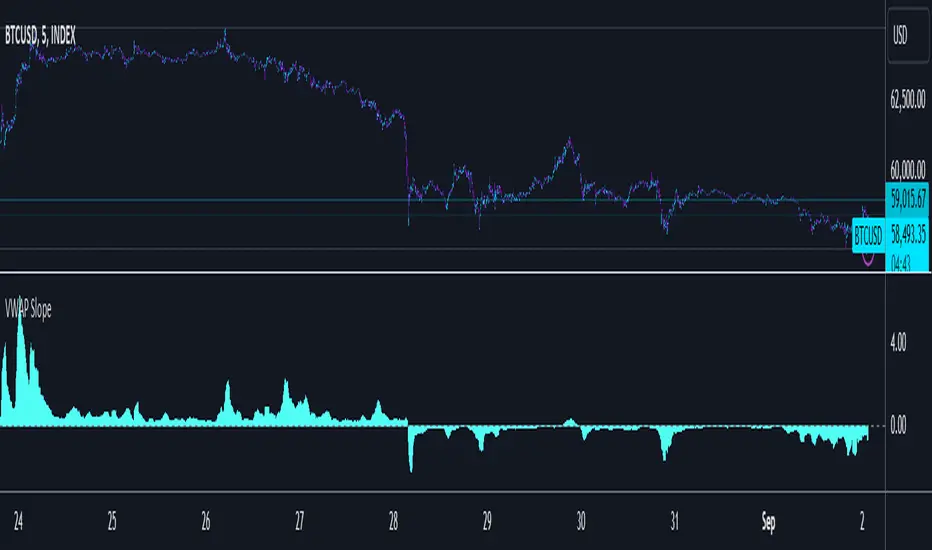

VWAP SlopePublishing one of the simplest yet one of my favorite concepts. Had to publish since I didn't really find any script for this on TV.

VWAP slope.

This is nothing fancy because it's just calculating "slope" with a very basic level formula

vwap_slope = (vwap - vwap ) / length

Above zero line, it's positive zone.

Below zero line, it's a negative zone.

The idea is to avoid choppy conditions and stay true to larger readings, sometimes when we have vwap directly on chart and when price interacts with it, we tend to take the lot of bad trades.

The intention here is to avoid just that.

This is also good at tracking failure of change in sentiments, this failure is very important, because one's failure occurs there is significant movement in the opposite direction of the failure.

Since there isn't much alteration to this idea, there is not much to talk about tbh.

Just remember, this is an educational idea and not assurance of future performance.

Regards.

Market Sessions - by Alexander RottasMarket Sessions - Alexander Rottas

This TradingView indicator displays market sessions for USA, EUROPE, and ASIA on your chart. It provides a clear and intuitive way to identify the active market periods, making it easier to plan your trades.

Features:

Session Display: Optionally show market sessions for USA, EUROPE, and ASIA.

Customizable Timings: Set start and end times in UTC for each market session.

Visual Indicators: Color-coded squares indicate active sessions and their combinations:

USA Session: Blue

EUROPE Session: Purple

ASIA Session: Dull Orange

Combined Sessions: Lighter shades to show overlapping sessions

Session Labels: Dynamic labels at the start of each session to easily identify session beginnings on weekdays.

User-Friendly Design: This indicator is designed to be non-intrusive and easy to use, with a simple setup and clear visual cues. Unlike other complex tools, it integrates seamlessly into your chart without overwhelming your view, making it an ideal choice for traders seeking a straightforward way to track market sessions.

DISCLAIMER: This script is provided for educational purposes only. It cannot be used for commercial purposes or plagiarized. All rights reserved by the author. Unauthorized use or distribution of this script is prohibited. For more details, please contact the author directly.

Wick Strength [MS]Overview

The Wick Strength indicator is a unique script designed to measure and visualize the relative strength of candlestick wicks over time. By analyzing the relationship between upper and lower wicks, this indicator provides insights into potential market dynamics and price action patterns.

How It Works

The Wick Strength indicator calculates the "strength" of candlestick wicks by comparing the upward and downward movements within each candle's range. This calculation results in a dynamic line plot that represents the evolving wick strength across your chosen timeframe.

Strength is not range-bound, allowing the score to reach extremes and be compared relatively across time.

Interpretation

Positive values indicate stronger upper wicks (potential bearish pressure)

Negative values suggest stronger lower wicks (potential bullish pressure)

Extreme readings might signal overextended moves or potential reversals

Key Features

Measures relative wick strength candle by candle

Smooths the values by summation based on user preference

Adaptable to all timeframes and markets

Potential Applications

While extensive backtesting has not been performed, the Wick Strength indicator may offer valuable insights for:

Identifying potential divergences between price action and wick strength

Spotting changes in market sentiment or volatility