Vix_Fix Enhanced MTF [Cometreon]The VIX Fix Enhanced is designed to detect market bottoms and spikes in volatility, helping traders anticipate major reversals with precision. Unlike standard VIX Fix tools, this version allows you to control the standard deviation logic, switch between chart styles, customize visual outputs, and set up advanced alerts — all with no repainting.

🧠 Logic and Calculation

This indicator is based on Larry Williams' VIX Fix and integrates features derived from community requests/advice, such as inverse VIX logic.

It calculates volatility spikes using a customizable standard deviation of the lows and compares it to a moving high to identify potential reversal points.

All moving average logic is based on Cometreon's proprietary library, ensuring accurate and optimized calculations on all 15 moving average types.

🔷 New Features and Improvements

🟩 Custom Visual Styles

Choose how you want your VIX data displayed:

Line

Step Line

Histogram

Area

Column

You can also flip the orientation (bottom-up or top-down), change the source ticker, and tailor the display to match your charting preferences.

🟩 Multi-MA Standard Deviation Calculation

Customize the standard deviation formula by selecting from 15 different moving averages:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

WMA (Weighted Moving Average)

RMA (Smoothed Moving Average)

HMA (Hull Moving Average)

JMA (Jurik Moving Average)

DEMA (Double Exponential Moving Average)

TEMA (Triple Exponential Moving Average)

LSMA (Least Squares Moving Average)

VWMA (Volume-Weighted Moving Average)

SMMA (Smoothed Moving Average)

KAMA (Kaufman’s Adaptive Moving Average)

ALMA (Arnaud Legoux Moving Average)

FRAMA (Fractal Adaptive Moving Average)

VIDYA (Variable Index Dynamic Average)

This gives you fine control over how volatility is measured and allows tuning the sensitivity for different market conditions.

🟩 Full Control Over Percentile and Deviation Conditions

You can enable or disable lines for standard deviation and percentile conditions, and define whether you want to trigger on over or under levels — adapting the indicator to your exact logic and style.

🟩 Chart Type Selection

You're no longer limited to candlestick charts! Now you can use Vix_Fix with different chart formats, including:

Candlestick

Heikin Ashi

Renko

Kagi

Line Break

Point & Figure

🟩 Multi-Timeframe Compatibility Without Repainting

Use a different timeframe from your chart with confidence. Signals remain stable and do not repaint. Perfect for spotting long-term reversal setups on lower timeframes.

🟩 Alert System Ready

Configure alerts directly from the indicator’s panel when conditions for over/under signals are met. Stay informed without needing to monitor the chart constantly.

🔷 Technical Details and Customizable Inputs

This indicator includes full control over the logic and appearance:

1️⃣ Length Deviation High - Adjusts the lookback period used to calculate the high deviation level of the VIX logic. Shorter values make it more reactive; longer values smooth out the signal.

2️⃣ Ticker - Choose a different chart type for the calculation, including Heikin Ashi, Renko, Kagi, Line Break, and Point & Figure.

3️⃣ Style VIX - Change the visual style (Line, Histogram, Column, etc.), adjust line width, and optionally invert the display (bottom-to-top).

📌 Fill zones for deviation and percentile are active only in Line and Step Line modes

4️⃣ Use Standard Deviation Up / Down - Enable the overbought and oversold zone logic based on upper and lower standard deviation bands.

5️⃣ Different Type MA (for StdDev) - Choose from 15 different moving averages to define the calculation method for standard deviation (SMA, EMA, HMA, JMA, etc.), with dedicated parameters like Phase, Sigma, and Offset for optimized responsiveness.

6️⃣ BB Length & Multiplier - Adjust the period and multiplier for the standard deviation bands, similar to how Bollinger Bands work.

7️⃣ Show StdDev Up / Down Line - Enable or disable the visibility of upper and lower standard deviation boundaries.

8️⃣ Use Percentile & Length High - Activate the percentile-based logic to detect extreme values in historical volatility using a customizable lookback length.

9️⃣ Highest % / Lowest % - Set the high and low percentile thresholds (e.g., 85 for high, 99 for low) that will be used to trigger over/under signals.

🔟 Show High / Low Percentile Line - Toggle the visual display of the percentile boundaries directly on the chart for clearer signal reference.

1️⃣1️⃣ Ticker Settings – Customize parameters for special chart types such as Renko, Heikin Ashi, Kagi, Line Break, and Point & Figure, adjusting reversal, number of lines, ATR length, etc.

1️⃣2️⃣ Timeframe – Enables using SuperTrend on a higher timeframe.

1️⃣3️⃣ Wait for Timeframe Closes -

✅ Enabled – Displays Vix_Fix smoothly with interruptions.

❌ Disabled – Displays Vix_Fix smoothly without interruptions.

☄️ If you find this indicator useful, leave a Boost to support its development!

Every feedback helps to continuously improve the tool, offering an even more effective trading experience. Share your thoughts in the comments! 🚀🔥

Standarddeviations

Uptrick: Dynamic Z-Score DeviationOverview

Uptrick: Dynamic Z‑Score Deviation is a trading indicator built in Pine Script that combines statistical filters and adaptive smoothing to highlight potential reversal points in price action. It combines a hybrid moving average, dual Z‑Score analysis on both price and RSI, and visual enhancements like slope‑based coloring, ATR‑based shadow bands, and dynamically scaled reversal signals.

Introduction

Statistical indicators like Z‑Scores measure how far a value deviates from its average relative to the typical variation (standard deviation). Standard deviation quantifies how dispersed a set of values is around its mean. A Z‑Score of +2 indicates a value two standard deviations above the mean, while -2 is two below. Traders use Z‑Scores to spot unusually high or low readings that may signal overbought or oversold conditions.

Moving averages smooth out price data to reveal trends. The Arnaud Legoux Moving Average (ALMA) reduces lag and noise through weighted averaging. A Zero‑Lag EMA (approximated here using a time‑shifted EMA) seeks to further minimize delay in following price. The RSI (Relative Strength Index) is a momentum oscillator that measures recent gains against losses over a set period.

ATR (Average True Range) gauges market volatility by averaging the range between high and low over a lookback period. Shadow bands built using ATR give a visual mood of volatility around a central trend line. Together, these tools inform a dynamic but statistically grounded view of market extremes.

Purpose

The main goal of this indicator is to help traders spot short‑term reversal opportunities on lower timeframes. By requiring both price and momentum (RSI) to exhibit statistically significant deviations from their norms, it filters out weak setups and focuses on higher‑probability mean‑reversion zones. Reversal signals appear when price deviates far enough from its hybrid moving average and RSI deviates similarly in the same direction. This makes it suitable for discretionary traders seeking clean entry cues in volatile environments.

Originality and Uniqueness

Uptrick: Dynamic Z‑Score Deviation distinguishes itself from standard reversal or mean‑reversion tools by combining several elements into a single framework:

A composite moving average (ALMA + Zero‑Lag EMA) for a smooth yet responsive baseline

Dual Z‑Score filters on price and RSI rather than relying on a single measure

Adaptive visual elements, including slope‑aware coloring, multi‑layer ATR shadows, and signal sizing based on combined Z‑Score magnitude

Most indicators focus on one aspect—price envelopes or RSI thresholds—whereas Uptrick: Dynamic Z‑Score Deviation requires both layers to align before signaling. Its visual design aids quick interpretation without overwhelming the chart.

Why these indicators were merged

Every component in Uptrick: Dynamic Z‑Score Deviation has a purpose:

• ALMA: provides a smooth moving average with reduced lag and fewer false crossovers than a simple SMA or EMA.

• Zero‑Lag EMA (ZLMA approximation): further reduces the delay relative to price by applying a time shift to EMA inputs. This keeps the composite MA closer to current price action.

• RSI and its EMA filter: RSI measures momentum. Applying an EMA filter on RSI smooths out false spikes and confirms genuine overbought or oversold momentum.

• Dual Z‑Scores: computing Z‑Scores on both the distance between price and the composite MA, and on smoothed RSI, ensures that signals only fire when both price and momentum are unusually stretched.

• ATR bands: using ATR‑based shadow layers visualizes volatility around the MA, guiding traders on potential support and resistance zones.

At the end, these pieces merge into a single indicator that detects statistically significant mean reversions while staying adaptive to real‑time volatility and momentum.

Calculations

1. Compute ALMA over the chosen MA length, offset, and sigma.

2. Approximate ZLMA by applying EMA to twice the price minus the price shifted by the MA length.

3. Calculate the composite moving average as the average of ALMA and ZLMA.

4. Compute raw RSI and smooth it with ALMA. Apply an EMA filter to raw RSI to reduce noise.

5. For both price and smoothed RSI, calculate the mean and standard deviation over the Z‑Score lookback period.

6. Compute Z‑Scores:

• z_price = (current price − composite MA mean) / standard deviation of price deviations

• z_rsi = (smoothed RSI − mean RSI) / standard deviation of RSI

7. Determine reversal conditions: both Z‑Scores exceed their thresholds in the same direction, RSI EMA is in oversold/overbought zones (below 40 or above 60), and price movement confirms directionality.

8. Compute signal strength as the sum of the absolute Z‑Scores, then classify into weak, medium, or strong.

9. Calculate ATR over the chosen period and multiply by layer multipliers to form shadow widths.

10.Derive slope over the chosen slope length and color the MA line and bars based on direction, optionally smoothing color transitions via EMA on RGB channels.

How this indicator actually works

1. The script begins by smoothing price data with ALMA and approximating a zero‑lag EMA, then averaging them for the main MA.

2. RSI is calculated, then smoothed and filtered.

3. Using a rolling window, the script computes statistical measures for both price deviations and RSI.

4. Z‑Scores tell how far current values lie from their recent norms.

5. When both Z‑Scores cross configured thresholds and momentum conditions align, reversal signals are flagged.

6. Signals are drawn with size and color reflecting strength.

7. The MA is plotted with dynamic coloring; ATR shadows are layered beneath to show volatility envelopes.

8. Bars can be colored to match MA slope, reinforcing trend context.

9. Alert conditions allow automated notifications when signals occur.

Inputs

Main Length: Main MA Length. Sets the period for ALMA and ZLMA.

RSI Length: RSI Length. Determines the lookback for momentum calculations.

Z-Score Lookback: Z‑Score Lookback. Window for mean and standard deviation computations.

Price Z-Score Threshold: Price Z‑Score Threshold. Minimum deviation required for price.

RSI Z-Score threshold: RSI Z‑Score Threshold. Minimum deviation required for momentum.

RSI EMA Filter Length: RSI EMA Filter Length. Smooths raw RSI readings.

ALMA Offset: Controls ALMA’s focal point in the window.

ALMA Sigma: Adjusts ALMA’s smoothing strength.

Show Reversal Signals : Toggle to display reversal signal markers.

Slope Sensitivity: Length for slope calculation. Higher values smooth slope changes.

Use Bar Coloring: Enables coloring of price bars based on MA slope.

Show MA Shadow: Toggle for ATR‑based shadow bands.

Shadow Layer Count: Number of shadow layers (1–4).

Base Shadow ATR Multiplier: Multiplier for ATR when sizing the first band.

Smooth Color Transitions (boolean): Smooths RGB transitions for line and shadows, if enabled.

ATR Length for Shadow: ATR Period for computing volatility bands.

Use Dynamic Signal Size: Toggles dynamic scaling of reversal symbols.

Features

Moving average smoothing: a hybrid of ALMA and Zero‑Lag EMA that balances responsiveness and noise reduction.

Slope coloring: MA line and optionally price bars change color based on trend direction; color transitions can be smoothed for visual continuity.

ATR shadow layers: translucent bands around the MA show volatility envelopes; up to four concentric layers help gauge distance from normal price swings.

Dual Z‑Score filters: price and momentum must both deviate beyond thresholds to trigger signals, reducing false positives.

Dynamic signal sizing: reversal markers scale in size based on the combined Z‑Score magnitude, making stronger signals more prominent.

Adaptive visuals: optional smoothing of color channels creates gradient effects on lines and fills for a polished look.

Alert conditions: built‑in buy and sell alerts notify traders when reversal setups emerge.

Conclusion

Uptrick: Dynamic Z‑Score Deviation delivers a structured way to identify short‑term reversal opportunities by fusing statistical rigor with adaptive smoothing and clear visual cues. It guides traders through multiple confirmation layers—hybrid moving average, dual Z‑Score analysis, momentum filtering, and volatility envelopes—while keeping the chart clean and informative.

Disclaimer

This indicator is provided for informational and educational purposes only and does not constitute financial advice. Trading carries risk and may not be suitable for all participants. Past performance is not indicative of future results. Always do your own analysis and risk management before making trading decisions.

RawCuts_01Library "RawCuts_01"

A collection of functions by:

mutantdog

The majority of these are used within published projects, some useful variants have been included here aswell.

This is volume one consisting mainly of smaller functions, predominantly the filters and standard deviations from Weight Gain 4000.

Also included at the bottom are various snippets of related code for demonstration. These can be copied and adjusted according to your needs.

A full up-to-date table of contents is located at the top of the main script.

WEIGHT GAIN FILTERS

A collection of moving average type filters with adjustable volume weighting.

Based upon the two most common methods of volume weighting.

'Simple' uses the standard method in which a basic VWMA is analogous to SMA.

'Elastic' uses exponential method found in EVWMA which is analogous to RMA.

Volume weighting is applied according to an exponent multiplier of input volume.

0 >> volume^0 (unweighted), 1 >> volume^1 (fully weighted), use float values for intermediate weighting.

Additional volume filter switch for smoothing of outlier events.

DIVA MODULAR DEVIATIONS

A small collection of standard and absolute deviations.

Includes the weightgain functionality as above.

Basic modular functionality for more creative uses.

Optional input (ct) for external central tendency (aka: estimator).

Can be assigned to alternative filter or any float value. Will default to internal filter when no ct input is received.

Some other useful or related functions included at the bottom along with basic demonstration use.

weightgain_sma(src, len, xVol, fVol)

Simple Moving Average (SMA): Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Standard Simple Moving Average with Simple Weight Gain applied.

weightgain_hsma(src, len, xVol, fVol)

Harmonic Simple Moving Average (hSMA): Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Harmonic Simple Moving Average with Simple Weight Gain applied.

weightgain_gsma(src, len, xVol, fVol)

Geometric Simple Moving Average (gSMA): Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Geometric Simple Moving Average with Simple Weight Gain applied.

weightgain_wma(src, len, xVol, fVol)

Linear Weighted Moving Average (WMA): Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Basic Linear Weighted Moving Average with Simple Weight Gain applied.

weightgain_hma(src, len, xVol, fVol)

Hull Moving Average (HMA): Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Basic Hull Moving Average with Simple Weight Gain applied.

diva_sd_sma(src, len, xVol, fVol, ct)

Standard Deviation (SD SMA): Diva / Weight Gain (Simple Volume)

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_sma().

Returns:

diva_sd_wma(src, len, xVol, fVol, ct)

Standard Deviation (SD WMA): Diva / Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_wma().

Returns:

diva_aad_sma(src, len, xVol, fVol, ct)

Average Absolute Deviation (AAD SMA): Diva / Weight Gain (Simple Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_sma().

Returns:

diva_aad_wma(src, len, xVol, fVol, ct)

Average Absolute Deviation (AAD WMA): Diva / Weight Gain (Simple Volume) .

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_wma().

Returns:

weightgain_ema(src, len, xVol, fVol)

Exponential Moving Average (EMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Exponential Moving Average with Elastic Weight Gain applied.

weightgain_dema(src, len, xVol, fVol)

Double Exponential Moving Average (DEMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Double Exponential Moving Average with Elastic Weight Gain applied.

weightgain_tema(src, len, xVol, fVol)

Triple Exponential Moving Average (TEMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Triple Exponential Moving Average with Elastic Weight Gain applied.

weightgain_rma(src, len, xVol, fVol)

Rolling Moving Average (RMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Rolling Moving Average with Elastic Weight Gain applied.

weightgain_drma(src, len, xVol, fVol)

Double Rolling Moving Average (DRMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Double Rolling Moving Average with Elastic Weight Gain applied.

weightgain_trma(src, len, xVol, fVol)

Triple Rolling Moving Average (TRMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: Triple Rolling Moving Average with Elastic Weight Gain applied.

diva_sd_ema(src, len, xVol, fVol, ct)

Standard Deviation (SD EMA): Diva / Weight Gain: (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_ema().

Returns:

diva_sd_rma(src, len, xVol, fVol, ct)

Standard Deviation (SD RMA): Diva / Weight Gain: (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_rma().

Returns:

weightgain_vidya_rma(src, len, xVol, fVol)

VIDYA v1 RMA base (VIDYA-RMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: VIDYA v1, RMA base with Elastic Weight Gain applied.

weightgain_vidya_ema(src, len, xVol, fVol)

VIDYA v1 EMA base (VIDYA-EMA): Weight Gain (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

Returns: VIDYA v1, EMA base with Elastic Weight Gain applied.

diva_sd_vidya_rma(src, len, xVol, fVol, ct)

Standard Deviation (SD VIDYA-RMA): Diva / Weight Gain: (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_vidya_rma().

Returns:

diva_sd_vidya_ema(src, len, xVol, fVol, ct)

Standard Deviation (SD VIDYA-EMA): Diva / Weight Gain: (Elastic Volume).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

xVol (float) : Volume exponent multiplier (0 = unweighted, 1 = fully weighted).

fVol (bool) : Volume smoothing filter.

ct (float) : Central tendency (optional, na = bypass). Internal: weightgain_vidya_ema().

Returns:

weightgain_sema(src, len, xVol, fVol)

Parameters:

src (float)

len (simple int)

xVol (float)

fVol (bool)

diva_sd_sema(src, len, xVol, fVol)

Parameters:

src (float)

len (simple int)

xVol (float)

fVol (bool)

diva_mad_mm(src, len, ct)

Median Absolute Deviation (MAD MM): Diva (no volume weighting).

Parameters:

src (float) : Source input.

len (int) : Length (number of bars).

ct (float) : Central tendency (optional, na = bypass). Internal: ta.median()

Returns:

source_switch(slct, aux1, aux2, aux3, aux4)

Custom Source Selector/Switch function. Features standard & custom 'weighted' sources with additional aux inputs.

Parameters:

slct (string) : Choose from custom set of string values.

aux1 (float) : Additional input for user-defined source, eg: standard input.source(). Optional, use na to bypass.

aux2 (float) : Additional input for user-defined source, eg: standard input.source(). Optional, use na to bypass.

aux3 (float) : Additional input for user-defined source, eg: standard input.source(). Optional, use na to bypass.

aux4 (float) : Additional input for user-defined source, eg: standard input.source(). Optional, use na to bypass.

Returns: Float value, to be used as src input for other functions.

colour_gradient_ma_div(ma1, ma2, div, bull, bear, mid, mult)

Colour Gradient for plot fill between two moving averages etc, with seperate bull/bear and divergence strength.

Parameters:

ma1 (float) : Input for fast moving average (eg: bullish when above ma2).

ma2 (float) : Input for slow moving average (eg: bullish when below ma1).

div (float) : Input deviation/divergence value used to calculate strength of colour.

bull (color) : Colour when ma1 above ma2.

bear (color) : Colour when ma1 below ma2.

mid (color) : Neutral colour when ma1 = ma2.

mult (int) : Opacity multiplier. 100 = maximum, 0 = transparent.

Returns: Colour with transparency (according to specified inputs)

Buy Sell Strategy With Z-Score [TradeDots]The "Buy Sell Strategy With Z-Score" is a trading strategy that harnesses Z-Score statistical metrics to identify potential pricing reversals, for opportunistic buying and selling opportunities.

HOW DOES IT WORK

The strategy operates by calculating the Z-Score of the closing price for each candlestick. This allows us to evaluate how significantly the current price deviates from its typical volatility level.

The strategy first takes the scope of a rolling window, adjusted to the user's preference. This window is used to compute both the standard deviation and mean value. With these values, the strategic model finalizes the Z-Score. This determination is accomplished by subtracting the mean from the closing price and dividing the resulting value by the standard deviation.

This approach provides an estimation of the price's departure from its traditional trajectory, thereby identifying market conditions conducive to an asset being overpriced or underpriced.

APPLICATION

Firstly, it is better to identify a stable trading pair for this technique, such as two stocks with considerable correlation. This is to ensure conformance with the statistical model's assumption of a normal Gaussian distribution model. The ideal performance is theoretically situated within a sideways market devoid of skewness.

Following pair selection, the user should refine the span of the rolling window. A broader window smoothens the mean, more accurately capturing long-term market trends, while potentially enhancing volatility. This refinement results in fewer, yet precise trading signals.

Finally, the user must settle on an optimal Z-Score threshold, which essentially dictates the timing for buy/sell actions when the Z-Score exceeds with thresholds. A positive threshold signifies the price veering away from its mean, triggering a sell signal. Conversely, a negative threshold denotes the price falling below its mean, illustrating an underpriced condition that prompts a buy signal.

Within a normal distribution, a Z-Score of 1 records about 68% of occurrences centered at the mean, while a Z-Score of 2 captures approximately 95% of occurrences.

The 'cool down period' is essentially the number of bars that await before the next signal generation. This feature is employed to dodge the occurrence of multiple signals in a short period.

DEFAULT SETUP

The following is the default setup on EURUSD 1h timeframe

Rolling Window: 80

Z-Score Threshold: 2.8

Signal Cool Down Period: 5

Commission: 0.03%

Initial Capital: $10,000

Equity per Trade: 30%

RISK DISCLAIMER

Trading entails substantial risk, and most day traders incur losses. All content, tools, scripts, articles, and education provided by TradeDots serve purely informational and educational purposes. Past performances are not definitive predictors of future results.

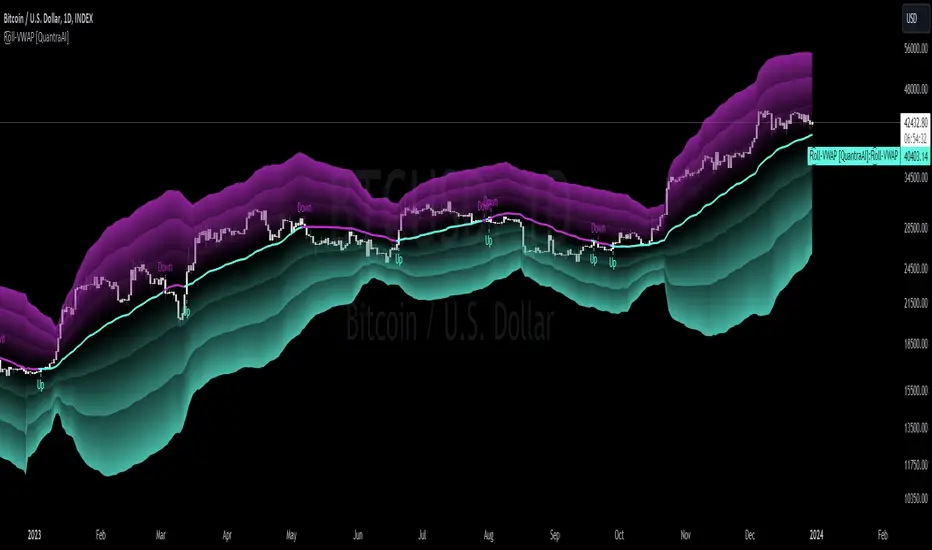

Rolling VWAP [QuantraSystems]Rolling VWAP

Introduction

The Rolling VWAP (R͜͡oll-VWAP) indicator modernizes the traditional VWAP by recalculating continuously on a rolling window, making it adept at pinpointing market trends and breakout points.

Its dual functionality includes both the dynamic rolling VWAP and a customizable anchored VWAP, enhanced by color-coded visual cues, thereby offering traders valuable flexibility and insight for their market analysis.

Legend

In the Image you can see the BTCUSD 1D Chart with the R͜͡oll-VWAP overlay.

You can see the individually activatable Standard Deviation (SD) Bands and the main VWAP Line.

It also features a Trend Signal which is deactivated by default and can be enabled if required.

Furthermore you can find the coloring of the VWAP line to represent the Trend.

In this case the trend itself is defined as:

Close being greater than the VWAP line -> Uptrend

Close below the VWAP line -> Downtrend

Notes

The R͜͡oll-VWAP can be used in a variety of ways.

Volatility adjusted expected range

This aims to identify in which range the asset is likely to move - according to the historical values the SD Bands are calculated and thus their according probabilities displayed.

Trend analysis

Trending above or below the VWAP shows up or down trends accordingly.

S/R Levels

Based on the probability distribution the 2. SD often works as a Resistance level and either mid line or 1. SD lines can act as S/R levels

Unsustainable levels

Based on the probability distributions a SD level of beyond 2.5, especially 3 and higher is hit very seldom and highly unsustainable.

This can either mean a mean reversion state or a momentum slowdown is necessary to get back to a sustainable level.

Please note that we always advise to find more confluence by additional indicators.

Traders are encouraged to test and determine the most suitable settings for their specific trading strategies and timeframes.

Methodology

The R͜͡oll-VWAP is based on the inbuilt TV VWAP.

It expands upon the limitations of having an anchored timeframe and thus a limited data set that is being reset constantly.

Instead we have integrated a rolling nature that continuously calculates the VWAP over a customizable lookback.

To also keep the base utility it is possible to use the anchored timeframes as well.

Furthermore the visualization has been improved and we added the coloring of the main VWAP line according to the Trend as stated above.

The applicable Trend signals are also part of that.

The parameter settings and also the visualizations allow for ample customizations by the trader.

For questions or recommendations, please feel free to seek contact in the comments.