Daily, Weekly, Monthly Current/Average RangeThe "Daily, Weekly, Monthly Current/Average Range" calculates and displays current and average price ranges (high - low) for daily, weekly, and monthly timeframes in a customizable table.

Users can adjust the lookback period, table size, and font color, with the table updating on the last bar for efficiency.

When the current range exceeds the average for a timeframe, the corresponding cell highlights green, signaling price possibly reaching maximum expansion and potential retracement or consolidation may follow.

Statistical

Statistical Pairs Trading IndicatorZ-Score Stat Trading — Statistical Pairs Trading Indicator

📊🔗

---

What is it?

Z-Score Stat Trading is a powerful indicator for statistical pairs trading and quantitative analysis of two correlated assets.

It calculates the Z-Score of the log-price spread between any two symbols you choose, providing both long-term and short-term Z-Score signals.

You’ll also see real-time correlation, volatility, spread, and the number of long/short signals in a handy on-chart table!

---

How to Use 🛠️

1. Add the indicator to your chart.

2. Select two assets (symbols) to analyze in the settings.

3. Watch the Z-Score plots (blue and orange lines) and threshold levels (+2, -2 by default).

4. Check the info table for:

- Correlation

- Volatility

- Spread

- Number of long (NL) and short (NS) signals in the last 1000 bars

5. Set up alerts for signal generation or threshold crossings if you want to be notified automatically.

---

Trading Strategy 💡

- This indicator is designed for statistical arbitrage (mean reversion) strategies.

- Long Signal (🟢):

When both Z-Scores drop below the negative threshold (e.g., -2), a long signal is generated.

→ Buy Symbol A, Sell Symbol B, expecting the spread to revert to the mean.

- Short Signal (🔴):

When both Z-Scores rise above the positive threshold (e.g., +2), a short signal is generated.

→ Sell Symbol A, Buy Symbol B, again expecting mean reversion.

- The info table helps you quickly assess the frequency of signals and the current statistical relationship between your chosen assets.

---

Best Practices & Warnings 🚦

- Avoid high leverage! Pairs trading can be risky, especially during periods of divergence. Use conservative position sizing.

- Check for cointegration: Before using this indicator, make sure both assets are cointegrated or have a strong historical relationship. This increases the reliability of mean reversion signals.

- Check correlation: Only use asset pairs with a high correlation (preferably 0.8–0.9 or higher) for best results. The correlation value is shown in the info table.

- Scale in and out gradually: When entering or exiting positions, consider doing so in parts rather than all at once. This helps manage slippage and risk, especially in volatile markets.

---

⚠️ Note on Performance:

This indicator may work a bit slowly, especially on large timeframes or long chart histories, because the calculation of NL and NS (number of long/short signals) is computationally intensive.

---

Disclaimer ⚠️

This script is provided for educational and informational purposes only .

It is not financial advice or a recommendation to buy or sell any asset.

Use at your own risk. The author assumes no responsibility for any trading decisions or losses.

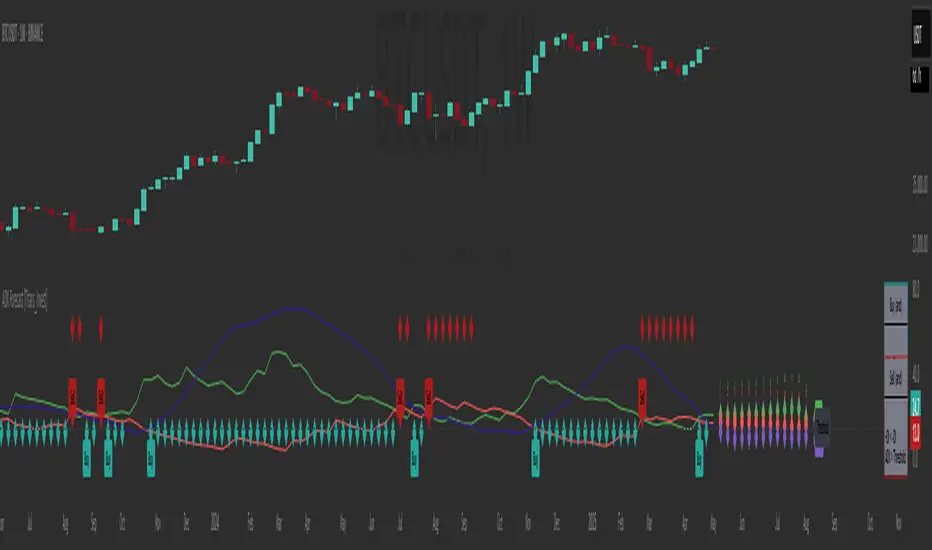

ADX Forecast [Titans_Invest]ADX Forecast

This isn’t just another ADX indicator — it’s the most powerful and complete ADX tool ever created, and without question the best ADX indicator on TradingView, possibly even the best in the world.

ADX Forecast represents a revolutionary leap in trend strength analysis, blending the timeless principles of the classic ADX with cutting-edge predictive modeling. For the first time on TradingView, you can anticipate future ADX movements using scientifically validated linear regression — a true game-changer for traders looking to stay ahead of trend shifts.

1. Real-Time ADX Forecasting

By applying least squares linear regression, ADX Forecast projects the future trajectory of the ADX with exceptional accuracy. This forecasting power enables traders to anticipate changes in trend strength before they fully unfold — a vital edge in fast-moving markets.

2. Unmatched Customization & Precision

With 26 long entry conditions and 26 short entry conditions, this indicator accounts for every possible ADX scenario. Every parameter is fully customizable, making it adaptable to any trading strategy — from scalping to swing trading to long-term investing.

3. Transparency & Advanced Visualization

Visualize internal ADX dynamics in real time with interactive tags, smart flags, and fully adjustable threshold levels. Every signal is transparent, logic-based, and engineered to fit seamlessly into professional-grade trading systems.

4. Scientific Foundation, Elite Execution

Grounded in statistical precision and machine learning principles, ADX Forecast upgrades the classic ADX from a reactive lagging tool into a forward-looking trend prediction engine. This isn’t just an indicator — it’s a scientific evolution in trend analysis.

⯁ SCIENTIFIC BASIS LINEAR REGRESSION

Linear Regression is a fundamental method of statistics and machine learning, used to model the relationship between a dependent variable y and one or more independent variables 𝑥.

The general formula for a simple linear regression is given by:

y = β₀ + β₁x + ε

β₁ = Σ((xᵢ - x̄)(yᵢ - ȳ)) / Σ((xᵢ - x̄)²)

β₀ = ȳ - β₁x̄

Where:

y = is the predicted variable (e.g. future value of RSI)

x = is the explanatory variable (e.g. time or bar index)

β0 = is the intercept (value of 𝑦 when 𝑥 = 0)

𝛽1 = is the slope of the line (rate of change)

ε = is the random error term

The goal is to estimate the coefficients 𝛽0 and 𝛽1 so as to minimize the sum of the squared errors — the so-called Random Error Method Least Squares.

⯁ LEAST SQUARES ESTIMATION

To minimize the error between predicted and observed values, we use the following formulas:

β₁ = /

β₀ = ȳ - β₁x̄

Where:

∑ = sum

x̄ = mean of x

ȳ = mean of y

x_i, y_i = individual values of the variables.

Where:

x_i and y_i are the means of the independent and dependent variables, respectively.

i ranges from 1 to n, the number of observations.

These equations guarantee the best linear unbiased estimator, according to the Gauss-Markov theorem, assuming homoscedasticity and linearity.

⯁ LINEAR REGRESSION IN MACHINE LEARNING

Linear regression is one of the cornerstones of supervised learning. Its simplicity and ability to generate accurate quantitative predictions make it essential in AI systems, predictive algorithms, time series analysis, and automated trading strategies.

By applying this model to the ADX, you are literally putting artificial intelligence at the heart of a classic indicator, bringing a new dimension to technical analysis.

⯁ VISUAL INTERPRETATION

Imagine an ADX time series like this:

Time →

ADX →

The regression line will smooth these values and extend them n periods into the future, creating a predicted trajectory based on the historical moment. This line becomes the predicted ADX, which can be crossed with the actual ADX to generate more intelligent signals.

⯁ SUMMARY OF SCIENTIFIC CONCEPTS USED

Linear Regression Models the relationship between variables using a straight line.

Least Squares Minimizes the sum of squared errors between prediction and reality.

Time Series Forecasting Estimates future values based on historical data.

Supervised Learning Trains models to predict outputs from known inputs.

Statistical Smoothing Reduces noise and reveals underlying trends.

⯁ WHY THIS INDICATOR IS REVOLUTIONARY

Scientifically-based: Based on statistical theory and mathematical inference.

Unprecedented: First public ADX with least squares predictive modeling.

Intelligent: Built with machine learning logic.

Practical: Generates forward-thinking signals.

Customizable: Flexible for any trading strategy.

⯁ CONCLUSION

By combining ADX with linear regression, this indicator allows a trader to predict market momentum, not just follow it.

ADX Forecast is not just an indicator — it is a scientific breakthrough in technical analysis technology.

⯁ Example of simple linear regression, which has one independent variable:

⯁ In linear regression, observations ( red ) are considered to be the result of random deviations ( green ) from an underlying relationship ( blue ) between a dependent variable ( y ) and an independent variable ( x ).

⯁ Visualizing heteroscedasticity in a scatterplot against 100 random fitted values using Matlab:

⯁ The data sets in the Anscombe's quartet are designed to have approximately the same linear regression line (as well as nearly identical means, standard deviations, and correlations) but are graphically very different. This illustrates the pitfalls of relying solely on a fitted model to understand the relationship between variables.

⯁ The result of fitting a set of data points with a quadratic function:

_______________________________________________________________________

🥇 This is the world’s first ADX indicator with: Linear Regression for Forecasting 🥇_______________________________________________________________________

_________________________________________________

🔮 Linear Regression: PineScript Technical Parameters 🔮

_________________________________________________

Forecast Types:

• Flat: Assumes prices will remain the same.

• Linreg: Makes a 'Linear Regression' forecast for n periods.

Technical Information:

ta.linreg (built-in function)

Linear regression curve. A line that best fits the specified prices over a user-defined time period. It is calculated using the least squares method. The result of this function is calculated using the formula: linreg = intercept + slope * (length - 1 - offset), where intercept and slope are the values calculated using the least squares method on the source series.

Syntax:

• Function: ta.linreg()

Parameters:

• source: Source price series.

• length: Number of bars (period).

• offset: Offset.

• return: Linear regression curve.

This function has been cleverly applied to the RSI, making it capable of projecting future values based on past statistical trends.

______________________________________________________

______________________________________________________

⯁ WHAT IS THE ADX❓

The Average Directional Index (ADX) is a technical analysis indicator developed by J. Welles Wilder. It measures the strength of a trend in a market, regardless of whether the trend is up or down.

The ADX is an integral part of the Directional Movement System, which also includes the Plus Directional Indicator (+DI) and the Minus Directional Indicator (-DI). By combining these components, the ADX provides a comprehensive view of market trend strength.

⯁ HOW TO USE THE ADX❓

The ADX is calculated based on the moving average of the price range expansion over a specified period (usually 14 periods). It is plotted on a scale from 0 to 100 and has three main zones:

• Strong Trend: When the ADX is above 25, indicating a strong trend.

• Weak Trend: When the ADX is below 20, indicating a weak or non-existent trend.

• Neutral Zone: Between 20 and 25, where the trend strength is unclear.

______________________________________________________

______________________________________________________

⯁ ENTRY CONDITIONS

The conditions below are fully flexible and allow for complete customization of the signal.

______________________________________________________

______________________________________________________

🔹 CONDITIONS TO BUY 📈

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

🔹 +DI > -DI

🔹 +DI < -DI

🔹 +DI > ADX

🔹 +DI < ADX

🔹 -DI > ADX

🔹 -DI < ADX

🔹 ADX > Threshold

🔹 ADX < Threshold

🔹 +DI > Threshold

🔹 +DI < Threshold

🔹 -DI > Threshold

🔹 -DI < Threshold

🔹 +DI (Crossover) -DI

🔹 +DI (Crossunder) -DI

🔹 +DI (Crossover) ADX

🔹 +DI (Crossunder) ADX

🔹 +DI (Crossover) Threshold

🔹 +DI (Crossunder) Threshold

🔹 -DI (Crossover) ADX

🔹 -DI (Crossunder) ADX

🔹 -DI (Crossover) Threshold

🔹 -DI (Crossunder) Threshold

🔮 +DI (Crossover) -DI Forecast

🔮 +DI (Crossunder) -DI Forecast

🔮 ADX (Crossover) +DI Forecast

🔮 ADX (Crossunder) +DI Forecast

______________________________________________________

______________________________________________________

🔸 CONDITIONS TO SELL 📉

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

🔸 +DI > -DI

🔸 +DI < -DI

🔸 +DI > ADX

🔸 +DI < ADX

🔸 -DI > ADX

🔸 -DI < ADX

🔸 ADX > Threshold

🔸 ADX < Threshold

🔸 +DI > Threshold

🔸 +DI < Threshold

🔸 -DI > Threshold

🔸 -DI < Threshold

🔸 +DI (Crossover) -DI

🔸 +DI (Crossunder) -DI

🔸 +DI (Crossover) ADX

🔸 +DI (Crossunder) ADX

🔸 +DI (Crossover) Threshold

🔸 +DI (Crossunder) Threshold

🔸 -DI (Crossover) ADX

🔸 -DI (Crossunder) ADX

🔸 -DI (Crossover) Threshold

🔸 -DI (Crossunder) Threshold

🔮 +DI (Crossover) -DI Forecast

🔮 +DI (Crossunder) -DI Forecast

🔮 ADX (Crossover) +DI Forecast

🔮 ADX (Crossunder) +DI Forecast

______________________________________________________

______________________________________________________

🤖 AUTOMATION 🤖

• You can automate the BUY and SELL signals of this indicator.

______________________________________________________

______________________________________________________

⯁ UNIQUE FEATURES

______________________________________________________

Linear Regression: (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

Linear Regression (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Table of Conditions: BUY/SELL

Conditions Label: BUY/SELL

Plot Labels in the graph above: BUY/SELL

Automate & Monitor Signals/Alerts: BUY/SELL

______________________________________________________

📜 SCRIPT : ADX Forecast

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

______________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

RSI Full Forecast [Titans_Invest]RSI Full Forecast

Get ready to experience the ultimate evolution of RSI-based indicators – the RSI Full Forecast, a boosted and even smarter version of the already powerful: RSI Forecast

Now featuring over 40 additional entry conditions (forecasts), this indicator redefines the way you view the market.

AI-Powered RSI Forecasting:

Using advanced linear regression with the least squares method – a solid foundation for machine learning - the RSI Full Forecast enables you to predict future RSI behavior with impressive accuracy.

But that’s not all: this new version also lets you monitor future crossovers between the RSI and the MA RSI, delivering early and strategic signals that go far beyond traditional analysis.

You’ll be able to monitor future crossovers up to 20 bars ahead, giving you an even broader and more precise view of market movements.

See the Future, Now:

• Track upcoming RSI & RSI MA crossovers in advance.

• Identify potential reversal zones before price reacts.

• Uncover statistical behavior patterns that would normally go unnoticed.

40+ Intelligent Conditions:

The new layer of conditions is designed to detect multiple high-probability scenarios based on historical patterns and predictive modeling. Each additional forecast is a window into the price's future, powered by robust mathematics and advanced algorithmic logic.

Full Customization:

All parameters can be tailored to fit your strategy – from smoothing periods to prediction sensitivity. You have complete control to turn raw data into smart decisions.

Innovative, Accurate, Unique:

This isn’t just an upgrade. It’s a quantum leap in technical analysis.

RSI Full Forecast is the first of its kind: an indicator that blends statistical analysis, machine learning, and visual design to create a true real-time predictive system.

⯁ SCIENTIFIC BASIS LINEAR REGRESSION

Linear Regression is a fundamental method of statistics and machine learning, used to model the relationship between a dependent variable y and one or more independent variables 𝑥.

The general formula for a simple linear regression is given by:

y = β₀ + β₁x + ε

β₁ = Σ((xᵢ - x̄)(yᵢ - ȳ)) / Σ((xᵢ - x̄)²)

β₀ = ȳ - β₁x̄

Where:

y = is the predicted variable (e.g. future value of RSI)

x = is the explanatory variable (e.g. time or bar index)

β0 = is the intercept (value of 𝑦 when 𝑥 = 0)

𝛽1 = is the slope of the line (rate of change)

ε = is the random error term

The goal is to estimate the coefficients 𝛽0 and 𝛽1 so as to minimize the sum of the squared errors — the so-called Random Error Method Least Squares.

⯁ LEAST SQUARES ESTIMATION

To minimize the error between predicted and observed values, we use the following formulas:

β₁ = /

β₀ = ȳ - β₁x̄

Where:

∑ = sum

x̄ = mean of x

ȳ = mean of y

x_i, y_i = individual values of the variables.

Where:

x_i and y_i are the means of the independent and dependent variables, respectively.

i ranges from 1 to n, the number of observations.

These equations guarantee the best linear unbiased estimator, according to the Gauss-Markov theorem, assuming homoscedasticity and linearity.

⯁ LINEAR REGRESSION IN MACHINE LEARNING

Linear regression is one of the cornerstones of supervised learning. Its simplicity and ability to generate accurate quantitative predictions make it essential in AI systems, predictive algorithms, time series analysis, and automated trading strategies.

By applying this model to the RSI, you are literally putting artificial intelligence at the heart of a classic indicator, bringing a new dimension to technical analysis.

⯁ VISUAL INTERPRETATION

Imagine an RSI time series like this:

Time →

RSI →

The regression line will smooth these values and extend them n periods into the future, creating a predicted trajectory based on the historical moment. This line becomes the predicted RSI, which can be crossed with the actual RSI to generate more intelligent signals.

⯁ SUMMARY OF SCIENTIFIC CONCEPTS USED

Linear Regression Models the relationship between variables using a straight line.

Least Squares Minimizes the sum of squared errors between prediction and reality.

Time Series Forecasting Estimates future values based on historical data.

Supervised Learning Trains models to predict outputs from known inputs.

Statistical Smoothing Reduces noise and reveals underlying trends.

⯁ WHY THIS INDICATOR IS REVOLUTIONARY

Scientifically-based: Based on statistical theory and mathematical inference.

Unprecedented: First public RSI with least squares predictive modeling.

Intelligent: Built with machine learning logic.

Practical: Generates forward-thinking signals.

Customizable: Flexible for any trading strategy.

⯁ CONCLUSION

By combining RSI with linear regression, this indicator allows a trader to predict market momentum, not just follow it.

RSI Full Forecast is not just an indicator — it is a scientific breakthrough in technical analysis technology.

⯁ Example of simple linear regression, which has one independent variable:

⯁ In linear regression, observations ( red ) are considered to be the result of random deviations ( green ) from an underlying relationship ( blue ) between a dependent variable ( y ) and an independent variable ( x ).

⯁ Visualizing heteroscedasticity in a scatterplot against 100 random fitted values using Matlab:

⯁ The data sets in the Anscombe's quartet are designed to have approximately the same linear regression line (as well as nearly identical means, standard deviations, and correlations) but are graphically very different. This illustrates the pitfalls of relying solely on a fitted model to understand the relationship between variables.

⯁ The result of fitting a set of data points with a quadratic function:

_________________________________________________

🔮 Linear Regression: PineScript Technical Parameters 🔮

_________________________________________________

Forecast Types:

• Flat: Assumes prices will remain the same.

• Linreg: Makes a 'Linear Regression' forecast for n periods.

Technical Information:

ta.linreg (built-in function)

Linear regression curve. A line that best fits the specified prices over a user-defined time period. It is calculated using the least squares method. The result of this function is calculated using the formula: linreg = intercept + slope * (length - 1 - offset), where intercept and slope are the values calculated using the least squares method on the source series.

Syntax:

• Function: ta.linreg()

Parameters:

• source: Source price series.

• length: Number of bars (period).

• offset: Offset.

• return: Linear regression curve.

This function has been cleverly applied to the RSI, making it capable of projecting future values based on past statistical trends.

______________________________________________________

______________________________________________________

⯁ WHAT IS THE RSI❓

The Relative Strength Index (RSI) is a technical analysis indicator developed by J. Welles Wilder. It measures the magnitude of recent price movements to evaluate overbought or oversold conditions in a market. The RSI is an oscillator that ranges from 0 to 100 and is commonly used to identify potential reversal points, as well as the strength of a trend.

⯁ HOW TO USE THE RSI❓

The RSI is calculated based on average gains and losses over a specified period (usually 14 periods). It is plotted on a scale from 0 to 100 and includes three main zones:

• Overbought: When the RSI is above 70, indicating that the asset may be overbought.

• Oversold: When the RSI is below 30, indicating that the asset may be oversold.

• Neutral Zone: Between 30 and 70, where there is no clear signal of overbought or oversold conditions.

______________________________________________________

______________________________________________________

⯁ ENTRY CONDITIONS

The conditions below are fully flexible and allow for complete customization of the signal.

______________________________________________________

______________________________________________________

🔹 CONDITIONS TO BUY 📈

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

📈 RSI Conditions:

🔹 RSI > Upper

🔹 RSI < Upper

🔹 RSI > Lower

🔹 RSI < Lower

🔹 RSI > Middle

🔹 RSI < Middle

🔹 RSI > MA

🔹 RSI < MA

📈 MA Conditions:

🔹 MA > Upper

🔹 MA < Upper

🔹 MA > Lower

🔹 MA < Lower

📈 Crossovers:

🔹 RSI (Crossover) Upper

🔹 RSI (Crossunder) Upper

🔹 RSI (Crossover) Lower

🔹 RSI (Crossunder) Lower

🔹 RSI (Crossover) Middle

🔹 RSI (Crossunder) Middle

🔹 RSI (Crossover) MA

🔹 RSI (Crossunder) MA

🔹 MA (Crossover) Upper

🔹 MA (Crossunder) Upper

🔹 MA (Crossover) Lower

🔹 MA (Crossunder) Lower

📈 RSI Divergences:

🔹 RSI Divergence Bull

🔹 RSI Divergence Bear

📈 RSI Forecast:

🔹 RSI (Crossover) MA Forecast

🔹 RSI (Crossunder) MA Forecast

🔹 RSI Forecast 1 > MA Forecast 1

🔹 RSI Forecast 1 < MA Forecast 1

🔹 RSI Forecast 2 > MA Forecast 2

🔹 RSI Forecast 2 < MA Forecast 2

🔹 RSI Forecast 3 > MA Forecast 3

🔹 RSI Forecast 3 < MA Forecast 3

🔹 RSI Forecast 4 > MA Forecast 4

🔹 RSI Forecast 4 < MA Forecast 4

🔹 RSI Forecast 5 > MA Forecast 5

🔹 RSI Forecast 5 < MA Forecast 5

🔹 RSI Forecast 6 > MA Forecast 6

🔹 RSI Forecast 6 < MA Forecast 6

🔹 RSI Forecast 7 > MA Forecast 7

🔹 RSI Forecast 7 < MA Forecast 7

🔹 RSI Forecast 8 > MA Forecast 8

🔹 RSI Forecast 8 < MA Forecast 8

🔹 RSI Forecast 9 > MA Forecast 9

🔹 RSI Forecast 9 < MA Forecast 9

🔹 RSI Forecast 10 > MA Forecast 10

🔹 RSI Forecast 10 < MA Forecast 10

🔹 RSI Forecast 11 > MA Forecast 11

🔹 RSI Forecast 11 < MA Forecast 11

🔹 RSI Forecast 12 > MA Forecast 12

🔹 RSI Forecast 12 < MA Forecast 12

🔹 RSI Forecast 13 > MA Forecast 13

🔹 RSI Forecast 13 < MA Forecast 13

🔹 RSI Forecast 14 > MA Forecast 14

🔹 RSI Forecast 14 < MA Forecast 14

🔹 RSI Forecast 15 > MA Forecast 15

🔹 RSI Forecast 15 < MA Forecast 15

🔹 RSI Forecast 16 > MA Forecast 16

🔹 RSI Forecast 16 < MA Forecast 16

🔹 RSI Forecast 17 > MA Forecast 17

🔹 RSI Forecast 17 < MA Forecast 17

🔹 RSI Forecast 18 > MA Forecast 18

🔹 RSI Forecast 18 < MA Forecast 18

🔹 RSI Forecast 19 > MA Forecast 19

🔹 RSI Forecast 19 < MA Forecast 19

🔹 RSI Forecast 20 > MA Forecast 20

🔹 RSI Forecast 20 < MA Forecast 20

______________________________________________________

______________________________________________________

🔸 CONDITIONS TO SELL 📉

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

📉 RSI Conditions:

🔸 RSI > Upper

🔸 RSI < Upper

🔸 RSI > Lower

🔸 RSI < Lower

🔸 RSI > Middle

🔸 RSI < Middle

🔸 RSI > MA

🔸 RSI < MA

📉 MA Conditions:

🔸 MA > Upper

🔸 MA < Upper

🔸 MA > Lower

🔸 MA < Lower

📉 Crossovers:

🔸 RSI (Crossover) Upper

🔸 RSI (Crossunder) Upper

🔸 RSI (Crossover) Lower

🔸 RSI (Crossunder) Lower

🔸 RSI (Crossover) Middle

🔸 RSI (Crossunder) Middle

🔸 RSI (Crossover) MA

🔸 RSI (Crossunder) MA

🔸 MA (Crossover) Upper

🔸 MA (Crossunder) Upper

🔸 MA (Crossover) Lower

🔸 MA (Crossunder) Lower

📉 RSI Divergences:

🔸 RSI Divergence Bull

🔸 RSI Divergence Bear

📉 RSI Forecast:

🔸 RSI (Crossover) MA Forecast

🔸 RSI (Crossunder) MA Forecast

🔸 RSI Forecast 1 > MA Forecast 1

🔸 RSI Forecast 1 < MA Forecast 1

🔸 RSI Forecast 2 > MA Forecast 2

🔸 RSI Forecast 2 < MA Forecast 2

🔸 RSI Forecast 3 > MA Forecast 3

🔸 RSI Forecast 3 < MA Forecast 3

🔸 RSI Forecast 4 > MA Forecast 4

🔸 RSI Forecast 4 < MA Forecast 4

🔸 RSI Forecast 5 > MA Forecast 5

🔸 RSI Forecast 5 < MA Forecast 5

🔸 RSI Forecast 6 > MA Forecast 6

🔸 RSI Forecast 6 < MA Forecast 6

🔸 RSI Forecast 7 > MA Forecast 7

🔸 RSI Forecast 7 < MA Forecast 7

🔸 RSI Forecast 8 > MA Forecast 8

🔸 RSI Forecast 8 < MA Forecast 8

🔸 RSI Forecast 9 > MA Forecast 9

🔸 RSI Forecast 9 < MA Forecast 9

🔸 RSI Forecast 10 > MA Forecast 10

🔸 RSI Forecast 10 < MA Forecast 10

🔸 RSI Forecast 11 > MA Forecast 11

🔸 RSI Forecast 11 < MA Forecast 11

🔸 RSI Forecast 12 > MA Forecast 12

🔸 RSI Forecast 12 < MA Forecast 12

🔸 RSI Forecast 13 > MA Forecast 13

🔸 RSI Forecast 13 < MA Forecast 13

🔸 RSI Forecast 14 > MA Forecast 14

🔸 RSI Forecast 14 < MA Forecast 14

🔸 RSI Forecast 15 > MA Forecast 15

🔸 RSI Forecast 15 < MA Forecast 15

🔸 RSI Forecast 16 > MA Forecast 16

🔸 RSI Forecast 16 < MA Forecast 16

🔸 RSI Forecast 17 > MA Forecast 17

🔸 RSI Forecast 17 < MA Forecast 17

🔸 RSI Forecast 18 > MA Forecast 18

🔸 RSI Forecast 18 < MA Forecast 18

🔸 RSI Forecast 19 > MA Forecast 19

🔸 RSI Forecast 19 < MA Forecast 19

🔸 RSI Forecast 20 > MA Forecast 20

🔸 RSI Forecast 20 < MA Forecast 20

______________________________________________________

______________________________________________________

🤖 AUTOMATION 🤖

• You can automate the BUY and SELL signals of this indicator.

______________________________________________________

______________________________________________________

⯁ UNIQUE FEATURES

______________________________________________________

Linear Regression: (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

Linear Regression (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

______________________________________________________

📜 SCRIPT : RSI Full Forecast

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

______________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

RSI Forecast [Titans_Invest]RSI Forecast

Introducing one of the most impressive RSI indicators ever created – arguably the best on TradingView, and potentially the best in the world.

RSI Forecast is a visionary evolution of the classic RSI, merging powerful customization with groundbreaking predictive capabilities. While preserving the core principles of traditional RSI, it takes analysis to the next level by allowing users to anticipate potential future RSI movements.

Real-Time RSI Forecasting:

For the first time ever, an RSI indicator integrates linear regression using the least squares method to accurately forecast the future behavior of the RSI. This innovation empowers traders to stay one step ahead of the market with forward-looking insight.

Highly Customizable:

Easily adapt the indicator to your personal trading style. Fine-tune a variety of parameters to generate signals perfectly aligned with your strategy.

Innovative, Unique, and Powerful:

This is the world’s first RSI Forecast to apply this predictive approach using least squares linear regression. A truly elite-level tool designed for traders who want a real edge in the market.

⯁ SCIENTIFIC BASIS LINEAR REGRESSION

Linear Regression is a fundamental method of statistics and machine learning, used to model the relationship between a dependent variable y and one or more independent variables 𝑥.

The general formula for a simple linear regression is given by:

y = β₀ + β₁x + ε

Where:

y = is the predicted variable (e.g. future value of RSI)

x = is the explanatory variable (e.g. time or bar index)

β0 = is the intercept (value of 𝑦 when 𝑥 = 0)

𝛽1 = is the slope of the line (rate of change)

ε = is the random error term

The goal is to estimate the coefficients 𝛽0 and 𝛽1 so as to minimize the sum of the squared errors — the so-called Random Error Method Least Squares.

⯁ LEAST SQUARES ESTIMATION

To minimize the error between predicted and observed values, we use the following formulas:

β₁ = /

β₀ = ȳ - β₁x̄

Where:

∑ = sum

x̄ = mean of x

ȳ = mean of y

x_i, y_i = individual values of the variables.

Where:

x_i and y_i are the means of the independent and dependent variables, respectively.

i ranges from 1 to n, the number of observations.

These equations guarantee the best linear unbiased estimator, according to the Gauss-Markov theorem, assuming homoscedasticity and linearity.

⯁ LINEAR REGRESSION IN MACHINE LEARNING

Linear regression is one of the cornerstones of supervised learning. Its simplicity and ability to generate accurate quantitative predictions make it essential in AI systems, predictive algorithms, time series analysis, and automated trading strategies.

By applying this model to the RSI, you are literally putting artificial intelligence at the heart of a classic indicator, bringing a new dimension to technical analysis.

⯁ VISUAL INTERPRETATION

Imagine an RSI time series like this:

Time →

RSI →

The regression line will smooth these values and extend them n periods into the future, creating a predicted trajectory based on the historical moment. This line becomes the predicted RSI, which can be crossed with the actual RSI to generate more intelligent signals.

⯁ SUMMARY OF SCIENTIFIC CONCEPTS USED

Linear Regression Models the relationship between variables using a straight line.

Least Squares Minimizes the sum of squared errors between prediction and reality.

Time Series Forecasting Estimates future values based on historical data.

Supervised Learning Trains models to predict outputs from known inputs.

Statistical Smoothing Reduces noise and reveals underlying trends.

⯁ WHY THIS INDICATOR IS REVOLUTIONARY

Scientifically-based: Based on statistical theory and mathematical inference.

Unprecedented: First public RSI with least squares predictive modeling.

Intelligent: Built with machine learning logic.

Practical: Generates forward-thinking signals.

Customizable: Flexible for any trading strategy.

⯁ CONCLUSION

By combining RSI with linear regression, this indicator allows a trader to predict market momentum, not just follow it.

RSI Forecast is not just an indicator — it is a scientific breakthrough in technical analysis technology.

⯁ Example of simple linear regression, which has one independent variable:

⯁ In linear regression, observations ( red ) are considered to be the result of random deviations ( green ) from an underlying relationship ( blue ) between a dependent variable ( y ) and an independent variable ( x ).

⯁ Visualizing heteroscedasticity in a scatterplot against 100 random fitted values using Matlab:

⯁ The data sets in the Anscombe's quartet are designed to have approximately the same linear regression line (as well as nearly identical means, standard deviations, and correlations) but are graphically very different. This illustrates the pitfalls of relying solely on a fitted model to understand the relationship between variables.

⯁ The result of fitting a set of data points with a quadratic function:

_______________________________________________________________________

🥇 This is the world’s first RSI indicator with: Linear Regression for Forecasting 🥇_______________________________________________________________________

_________________________________________________

🔮 Linear Regression: PineScript Technical Parameters 🔮

_________________________________________________

Forecast Types:

• Flat: Assumes prices will remain the same.

• Linreg: Makes a 'Linear Regression' forecast for n periods.

Technical Information:

ta.linreg (built-in function)

Linear regression curve. A line that best fits the specified prices over a user-defined time period. It is calculated using the least squares method. The result of this function is calculated using the formula: linreg = intercept + slope * (length - 1 - offset), where intercept and slope are the values calculated using the least squares method on the source series.

Syntax:

• Function: ta.linreg()

Parameters:

• source: Source price series.

• length: Number of bars (period).

• offset: Offset.

• return: Linear regression curve.

This function has been cleverly applied to the RSI, making it capable of projecting future values based on past statistical trends.

______________________________________________________

______________________________________________________

⯁ WHAT IS THE RSI❓

The Relative Strength Index (RSI) is a technical analysis indicator developed by J. Welles Wilder. It measures the magnitude of recent price movements to evaluate overbought or oversold conditions in a market. The RSI is an oscillator that ranges from 0 to 100 and is commonly used to identify potential reversal points, as well as the strength of a trend.

⯁ HOW TO USE THE RSI❓

The RSI is calculated based on average gains and losses over a specified period (usually 14 periods). It is plotted on a scale from 0 to 100 and includes three main zones:

• Overbought: When the RSI is above 70, indicating that the asset may be overbought.

• Oversold: When the RSI is below 30, indicating that the asset may be oversold.

• Neutral Zone: Between 30 and 70, where there is no clear signal of overbought or oversold conditions.

______________________________________________________

______________________________________________________

⯁ ENTRY CONDITIONS

The conditions below are fully flexible and allow for complete customization of the signal.

______________________________________________________

______________________________________________________

🔹 CONDITIONS TO BUY 📈

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

📈 RSI Conditions:

🔹 RSI > Upper

🔹 RSI < Upper

🔹 RSI > Lower

🔹 RSI < Lower

🔹 RSI > Middle

🔹 RSI < Middle

🔹 RSI > MA

🔹 RSI < MA

📈 MA Conditions:

🔹 MA > Upper

🔹 MA < Upper

🔹 MA > Lower

🔹 MA < Lower

📈 Crossovers:

🔹 RSI (Crossover) Upper

🔹 RSI (Crossunder) Upper

🔹 RSI (Crossover) Lower

🔹 RSI (Crossunder) Lower

🔹 RSI (Crossover) Middle

🔹 RSI (Crossunder) Middle

🔹 RSI (Crossover) MA

🔹 RSI (Crossunder) MA

🔹 MA (Crossover) Upper

🔹 MA (Crossunder) Upper

🔹 MA (Crossover) Lower

🔹 MA (Crossunder) Lower

📈 RSI Divergences:

🔹 RSI Divergence Bull

🔹 RSI Divergence Bear

📈 RSI Forecast:

🔮 RSI (Crossover) MA Forecast

🔮 RSI (Crossunder) MA Forecast

______________________________________________________

______________________________________________________

🔸 CONDITIONS TO SELL 📉

______________________________________________________

• Signal Validity: The signal will remain valid for X bars .

• Signal Sequence: Configurable as AND or OR .

📉 RSI Conditions:

🔸 RSI > Upper

🔸 RSI < Upper

🔸 RSI > Lower

🔸 RSI < Lower

🔸 RSI > Middle

🔸 RSI < Middle

🔸 RSI > MA

🔸 RSI < MA

📉 MA Conditions:

🔸 MA > Upper

🔸 MA < Upper

🔸 MA > Lower

🔸 MA < Lower

📉 Crossovers:

🔸 RSI (Crossover) Upper

🔸 RSI (Crossunder) Upper

🔸 RSI (Crossover) Lower

🔸 RSI (Crossunder) Lower

🔸 RSI (Crossover) Middle

🔸 RSI (Crossunder) Middle

🔸 RSI (Crossover) MA

🔸 RSI (Crossunder) MA

🔸 MA (Crossover) Upper

🔸 MA (Crossunder) Upper

🔸 MA (Crossover) Lower

🔸 MA (Crossunder) Lower

📉 RSI Divergences:

🔸 RSI Divergence Bull

🔸 RSI Divergence Bear

📉 RSI Forecast:

🔮 RSI (Crossover) MA Forecast

🔮 RSI (Crossunder) MA Forecast

______________________________________________________

______________________________________________________

🤖 AUTOMATION 🤖

• You can automate the BUY and SELL signals of this indicator.

______________________________________________________

______________________________________________________

⯁ UNIQUE FEATURES

______________________________________________________

Linear Regression: (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

Linear Regression (Forecast)

Signal Validity: The signal will remain valid for X bars

Signal Sequence: Configurable as AND/OR

Condition Table: BUY/SELL

Condition Labels: BUY/SELL

Plot Labels in the Graph Above: BUY/SELL

Automate and Monitor Signals/Alerts: BUY/SELL

______________________________________________________

📜 SCRIPT : RSI Forecast

🎴 Art by : @Titans_Invest & @DiFlip

👨💻 Dev by : @Titans_Invest & @DiFlip

🎑 Titans Invest — The Wizards Without Gloves 🧤

✨ Enjoy!

______________________________________________________

o Mission 🗺

• Inspire Traders to manifest Magic in the Market.

o Vision 𐓏

• To elevate collective Energy 𐓷𐓏

TradeDots - Buy Sell Signals ProThe TradeDots - Buy Sell Signals Pro is an advanced technical analysis tool engineered to identify key market turning points and trend continuations. By combining multiple confirmation methods, this indicator provides traders with a comprehensive system for recognizing high-probability entry and exit points across various market conditions.

📝 HOW IT WORKS

Enhanced Supertrend Implementation

Unlike the traditional Supertrend indicator that simply changes color when price crosses above or below a calculated line, our implementation incorporates multiple layers of confirmation:

Advanced Calculation: Uses an enhanced ATR-based algorithm that incorporates trend bias detection and momentum filtering

Multi-Factor Confirmation: Considers price interaction with previous Supertrend values, not just current crossovers

Contextual Awareness: Distinguishes between different entry types based on market risk levels and momentum conditions

Visual Enhancement: Provides background shading to clearly indicate trend direction and strength

Smart Trendline Algorithm

The indicator employs a proprietary Smart Trendline that adapts to market conditions using an advanced moving average system. Unlike traditional moving averages that simply track price, the Smart Trendline incorporates volatility data to change colors based on momentum strength, providing immediate visual feedback about the current market phase with zero lag.

Calculation: Processes price data through selectable advanced calculation methods (including Hull, Jurik, and McGinley averages) with dynamic color-coding based on a modified Keltner Channel system.

Visualization: Green indicates strong bullish momentum, purple represents bearish momentum, and gray signals consolidation or uncertain conditions.

Multi-Signal Confirmation System

The indicator integrates three distinct signal mechanisms to confirm trading opportunities:

1. RSI-Sequential Reversal Signals: Combines RSI levels with seq count patterns to identify potential short-term reversals.

Calculation: Analyzes RSI conditions against specific thresholds while tracking consecutive pattern formations.

Visualization: Green triangles for buy signals and red triangles for sell signals.

2. Statistical Reversal Signals: Identifies statistically significant deviations from normal price behavior.

Calculation: Uses a modified standard deviation approach to determine when price has moved too far from its statistical average.

Visualization: Large green arrows emoji for powerful buy signals and red arrows emoji for powerful sell signals.

3. Supply & Demand Zone Detection: Automatically identifies key price levels where significant buying or selling pressure may exist.

Calculation: Uses RSI extremes combined with confirmation periods to establish high-probability reversal zones.

Visualization: Green-filled areas mark support (demand) zones and red-filled areas mark resistance (supply) zones.

Buy/Sell Signal Generation

The system generates several types of signals with varying strengths:

1. Regular Buy/Sell Signals: Generated when:

Price crosses with MA above/below the Supertrend line

RSI conditions confirm the direction

Candlestick patterns support the signal direction (bullish/bearish candle formation)

Visualized as green/red triangles

2. Strong Buy/Sell Signals: Appear when multiple confirmation factors align:

Regular buy/sell condition is met

Price is interacting with a Supply/Demand zone

Additional momentum confirmation from auxiliary indicators

Seq count reaches significant levels

Statistical Reversal signal confirms the direction

3. Breakout Signals: Special case signals that appear during:

Trend transitions after consolidation

When price breaks through significant resistance/support levels from previous trend

Following pattern completions that suggest increased momentum

Market Structure Analysis

The indicator categorizes market conditions and provides visual cues for traders:

Trend Identification: Supertrend-based algorithm with enhanced visual presentation identifies the prevailing market direction.

Bar Coloring System: Candles change color based on price position relative to EMAs to clearly display strength and direction of momentum

🛠️ HOW TO USE

Signal Interpretation

Buy Signals: "Buy" signals, Green triangles (RSI-Sequential) and large green arrows (Statistical Reversals) appear at potential buy points.

Sell Signals: "Sell" signals, Red triangles (RSI-Sequential) and large red arrows (Statistical Reversals) appear at potential sell points.

Highest Probability Entries: Occur when signals appear near or within Supply & Demand zones.

Trading Strategies

Trend-Following Strategy

1. Identify the main trend using the Smart Trendline color

2. Enter long positions during uptrends when:

Price pulls back to the Smart Trendline

Green triangles or arrows appear

Signals occur near green demand zones

3. Enter short positions during downtrends when:

Price bounces up to the Smart Trendline

Red triangles or arrows appear

Signals occur near red supply zones

Counter-Trend/Reversal Strategy

1. Look for Statistical Reversal arrows at significant price extremes

2. Confirm with an RSI-Sequential signal in the same direction

3. Pay special attention when these signals appear inside Supply & Demand zones

4. Use the Smart Trendline color change as additional confirmation

Multiple Confirmation Technique

For highest probability trades, look for:

Signal alignment (both signal types in same direction)

Supply/Demand zone interaction

Smart Trendline color supporting the signal direction

❗️LIMITATIONS

Signal Lag: The system identifies reversals after they have begun, potentially missing the absolute bottom or top.

False Signals: Can occur during periods of high volatility or range-bound markets.

Timeframe Sensitivity: Some signals work better on higher timeframes for long-term trading, while others are more effective on lower timeframes for short-term trading.

Bar Closing Requirement: All signals are based on closed candles and may be subject to change until the candle closes.

RISK DISCLAIMER

Trading involves substantial risk, and most traders may incur losses. All content, tools, scripts, articles, and education provided by TradeDots are for informational and educational purposes only. Past performance is not indicative of future results.

This indicator should be used as part of a complete trading approach that includes proper risk management, consideration of the broader market context, and confirmation from price action patterns. No trading system can guarantee profits, and users should always exercise caution and use appropriate position sizing.

Bull vs Bear CandlesThe Bull vs Bear Candles indicator helps you analyze market sentiment by counting and comparing bullish and bearish candles. It tracks the number of bullish candles and calculates their percentage, then does the same for bearish candles. Based on this data, the indicator determines whether bulls or bears are in control. Additionally, it counts the total number of candles within the selected range, giving you a clearer picture of price action. Use this tool to quickly assess market trends and make more informed trading decisions. 🚀

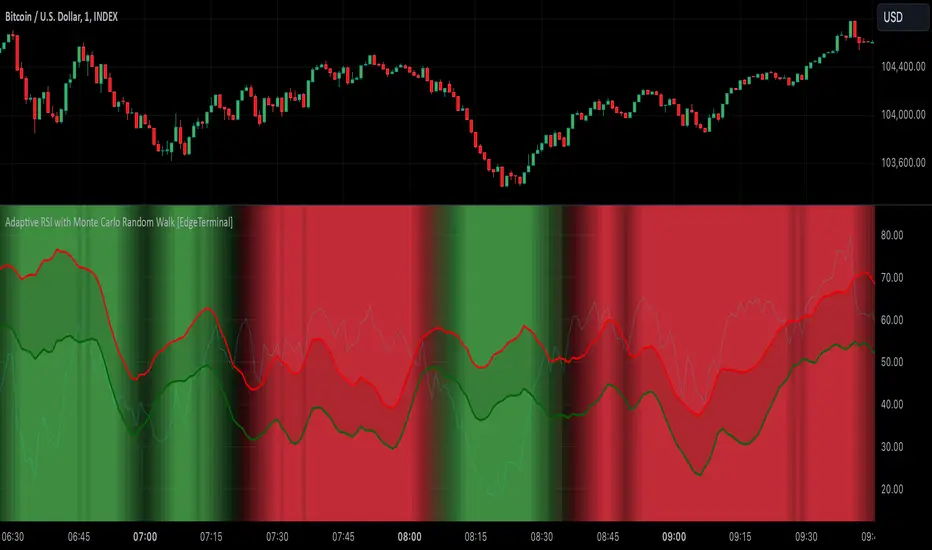

Adaptive RSI with Monte Carlo Random Walk [EdgeTerminal]The Monte Carlo Random Walk RSI indicator revolutionizes the traditional RSI by replacing static overbought/oversold levels with dynamic, statistically-driven bands that adapt to market conditions. Enhanced with smooth transitions, visual cues, and advanced filtering, this indicator provides a sophisticated approach to market analysis.

How it works:

In this indicator, the machine learning simulation works by combining multiple market signals in a weighted system that adapts to market conditions. Instead of just using simple RSI overbought/oversold levels, it analyzes the relationships between RSI, price momentum, and volatility to generate a comprehensive score.

The RSI component contributes 40% to the final signal, while momentum and volatility each contribute 30%. These signals are normalized and combined to create a score between 0-100, similar to how a machine learning model would generate probability predictions.

When this score is very high (above 80) along with traditional RSI signals, it suggests a stronger likelihood of a price reversal than using RSI alone.

The indicator doesn't use actual Monte Carlo simulations, but it does incorporate the concept of probability through its scoring system. Rather than giving simple buy/sell signals, it provides different levels of conviction (strong vs weak signals) based on how multiple factors align.

For example, a strong buy signal only occurs when both the ML score is above 80 AND the RSI is in oversold territory, indicating that multiple market conditions are favorable. This multi-factor approach helps reduce false signals that might occur with traditional RSI and provides traders with more nuanced information about potential trade opportunities.

Key Innovations:

Dynamic Bands vs Static Levels: Traditional RSI uses fixed 70/30 or 80/20 levels, this adaptive RSI creates adaptive bands based on market behavior and automatically adjusts to volatility and trend changes to reduce false signals in trending markets.

1. Calculate price volatility: σ = stdDev(returns)

2. Generate random walks: R(t) = R(t-1) + N(0,σ)

3. Transform to RSI space

4. Create probability distribution

5. Extract confidence intervals

Statistical Analysis: We use Monte Carlo simulations to generate probability bands. This allows the indicator levels to automatically adapt to current market conditions, generating more accurate overbought and oversold levels.

1. Measure deviation: D = |RSI - nearestBand|

2. Normalize by volatility: N = D/ATR

3. Calculate strength multiplier: max(1, N)

The indicator uses Monte Carlo simulations to model potential RSI paths. For each simulation, we generate random returns using market volatility, then calculate RSI components, calculate RSI, and finally, repeat N times (default 200 simulations)

Settings:

RSI Length: Controls the lookback period for the RSI calculation. Higher values result in smoother RSI, and slower signals. It affects exponential smoothing factor, impacts volatility measurement and influences random walk generation.

Number of Simulations: Controls Monte Carlo simulation count. Higher values result in more accurate bands, but lower calculation. More simulation means you get a better normal distribution, reducing random variation in bands.

Confidence Level: this controls statistical significance of bands. Higher values result in wider bands, meaning fewer trading signals are generated.

- 0.95 = 95% confidence interval

- Captures 2 standard deviations

- Controls false signal probability

Band Smoothing: Applies SMA to raw band values. Higher values mean smoother brands but result in more lag.

Minimum Signal Strength: Normalizes RSI deviation by ATR. The higher the value, it requires stronger moves. It uses ATR for volatility normalization and creates standard deviation equivalent.

Trend Sensitivity: Measures trend strength relative to volatility. Higher values filter more trending conditions

Volume Threshold: Compares current volume to average. Higher values require stronger volume confirmation. It validates price movement and confirms institutional participation.

How to Use:

Background gradually turns red in overbought and turns green in oversold conditions. Based on your trade direction, you want to pay attention when overbought or oversold levels start shifting.

For example, if you're going long on a trade, wait for oversold conditions (green) to start shifting toward red, this can indicate a move into a long direction, helping you catch the trend.

Additionally, the bands represent statistically significant levels where the RSI is likely to reverse, based on recent market behavior. The indicator runs multiple simulations of potential RSI paths. Each simulation uses recent market volatility and characteristics, then creates a statistical distribution of where RSI tends to turn around.

The Upper Band (red line) represents a statistically significant overbought level, when RSI crosses above this band and stays there for a while, the background starts to turn red, indicating it's more extended than normal. This is a lot more reliable than fixed RSI 70 level because it adapts to market conditions. Finally, the probability of reversal increases above this band. You can think of it as a dynamic overbought level.

The Lower Band (green line) is the opposite of the red line, and it represents a statistically significant oversold level. When RSI crosses below this band, it's more oversold than normal. This is a lot more reliable than fixed RSI 30 level because it adapts to market trend and the probability of reversal increases below this band.

Finally, the band width itself represents how volatile the market is. A wider band means the market is more volatile and a narrower band means the market is not as volatile. The width automatically adjusts based on market conditions.

[BRAIN] Absolute Volatility of Price

Hello traders!

Today I want to share with you a series of scripts and strategies that I developed a few years ago. This is one of my first works, born from the curiosity of seeing a candlestick representation in a different way, without considering the price movement along the y-axis.

Imagine observing the price movement in dollars and percentages, always starting from the same reference point: the 0 axis. This approach can offer new insights and ideas on how and how much prices move.

To explain it better, the open of each candle does not start from the previous close negotiations but always starts from the 0 axis . In this way, it is possible to clearly compare the bodies of the candles with each other.

Script Visualization Methods and Input

- Study Normal: Simply reports the prices, including the negative ones of the red candles, on the same scale in absolute terms (ABS), as shown in the first indicator above.

- Study Normal Neg: In this version, the red candles vary negatively below zero, instead of in absolute terms above zero, as shown in the second indicator above.

- Study Perc: Similar to "Study Normal" but uses percentage values instead of dollars, useful for very low timeframes and low variations with many decimals, such as 1 minute on EUR/USD.

- Study Perc Neg: Similar to "Study Normal Neg" but uses percentage values.

Additionally, I have added the possibility to display or not, through two buttons, an average of the candle bodies adjustable in length via input and the range of each candle, always correlated in dollars or percentages, as per the main study setting.

I hope this work can be useful to many of you. I invite you to like if you appreciate my scripts and want to see more like these. Do not hesitate to comment or contact me for any doubts or questions.

PS: If you notice that in the script the sum of the percentage values between the shadow and the body of the candle does not correspond to the range, it is only a rounding issue. Change the precision setting to a lower value and you will see that the rounding disappears.

PS: In the script, to better visualize the percentage growth and decline of the instrument on very high timeframes, I decided to represent it as follows:

- If close ≥ open: (high - low) / low * 100

- If close < open: (high - low) / high * 100

The same method is also applied for calculating the percentage variations of the shadows relative to themselves.

I hope you like this version! If you need any further modifications or adjustments, let me know. Good luck with your project!

(In the photos below I show 3 versions of the indicator open on 3 different tickers as an example: from top to bottom in the 3 indicators are set these Study: Study Normal, Study Perc and Study Perc Neg)

[DarkTrader] Intersection Level & PredictionLinear Regression Function Reference by @RicardoSantos :

The Intersection Level Calculation process identifies critical price levels where significant market reactions are expected. It starts by analyzing historical price action and technical indicators to pinpoint key support and resistance levels.

Price Forecast Min represents the predicted lowest price level that the asset might reach, while Price Forecast Max indicates the anticipated highest price level. These projections are calculated using statistical methods and historical price patterns, allowing traders to anticipate potential support and resistance zones. By providing these forecasts, traders can better manage their risk and set more informed entry and exit points based on projected price movements.

Example Of Prediction (Before & After)

Predicting Future Price Movements :

Once the intersection levels are identified, the indicator uses various predictive models to forecast what price might do next when it approaches these levels. Here’s a breakdown of how it achieves this :

Price Reaction Analysis: The indicator assesses how price has historically reacted to similar intersection levels. For instance, if price has reversed from a certain support level multiple times, the indicator can predict a potential reversal or bounce when price approaches that level again.

Trend Continuation or Reversal: It examines the strength of the current trend by analyzing momentum indicators, volume, and the angle or direction of trendlines. Based on this, it can predict whether price is likely to break through an intersection level, signaling trend continuation, or bounce off it, indicating a potential reversal.

Confluence of Factors: The prediction mechanism becomes more accurate when multiple factors converge at the same intersection level. For example, if a trendline, moving average, and support zone all intersect at the same price point, the indicator predicts a stronger likelihood of significant price movement.

Market Volatility and Momentum: The indicator also considers current market volatility and momentum in its prediction. For example, if price approaches an intersection level with high momentum, it might predict a breakout, whereas low momentum might suggest consolidation or a weaker price reaction.

In this indicator, I utilize Linear Regression to forecast price movements by analyzing historical data trends. Linear Regression involves fitting a straight line to past price data, enabling me to model and project future price levels based on identified trends. This method calculates a trend line that best represents the historical price behavior, providing a foundation for predicting future price points. By extending this trend line, I can estimate where prices might move, incorporating a range to account for potential deviations. This approach helps in identifying both minimum and maximum forecasted prices, offering valuable insights into potential market directions.

Volatility DashboardThis indicator calculates and displays volatility metrics for a specified number of bars (rolling window) on a TradingView chart. It can be customized to display information in English or Thai and can position the dashboard at various locations on the chart.

Inputs

Language: Users can choose between English ("ENG") and Thai ("TH") for the dashboard's language.

Dashboard Position: Users can specify where the dashboard should appear on the chart. Options include various positions such as "Bottom Right", "Top Center", etc.

Calculation Method: Currently, the script supports "High-Low" for volatility calculation. This method calculates the difference between the highest and lowest prices within a specified timeframe.

Bars: Number of bars used to calculate the volatility.

Display Logic

Fills the islast_vol_points array with the calculated volatility points.

Sets the table cells with headers and corresponding values:

=> Highest Volatility: The maximum value in the islast_vol_points array

=> Mean Volatility: The average value in the islast_vol_points array,

=> Lowest Volatility: The minimum value in the islast_vol_points array, Number of Bars: The rolling window size.

Inflation CorrelationHeyo fellas,

In today’s dynamic economic landscape, understanding the relationship of market prices to other economical factors like inflation rate is crucial. The Inflation Correlation Indicator is designed to provide traders with a clear visualization of this relationship. By correlating average inflation rates from selected countries with market closing prices, this indicator offers a unique perspective on potential market movements influenced by inflationary trends.

Features:

Country Selection: Choose from the European Union (EU), Germany (DE), or the United States (US) to tailor the correlation analysis to your specific market interest.

Correlation Length Customization: Adjust the correlation length to refine the sensitivity of the indicator to recent inflation data.

Visual Clarity: The correlation histogram changes color based on the direction of the correlation, providing an intuitive understanding of the inflation correlation.

Whether you’re a fundamental analyst seeking to incorporate macroeconomic indicators into your strategy or a trader looking for an edge in inflation-sensitive markets, the Inflation Correlation Indicator is an indispensable tool in your TradingView arsenal.

Thanks for checking this out!

Best regards,

simwai

Statistics • Chi Square • P-value • SignificanceThe Statistics • Chi Square • P-value • Significance publication aims to provide a tool for combining different conditions and checking whether the outcome is significant using the Chi-Square Test and P-value.

🔶 USAGE

The basic principle is to compare two or more groups and check the results of a query test, such as asking men and women whether they want to see a romantic or non-romantic movie.

–––––––––––––––––––––––––––––––––––––––––––––

| | ROMANTIC | NON-ROMANTIC | ⬅︎ MOVIE |

–––––––––––––––––––––––––––––––––––––––––––––

| MEN | 2 | 8 | 10 |

–––––––––––––––––––––––––––––––––––––––––––––

| WOMEN | 7 | 3 | 10 |

–––––––––––––––––––––––––––––––––––––––––––––

|⬆︎ SEX | 10 | 10 | 20 |

–––––––––––––––––––––––––––––––––––––––––––––

We calculate the Chi-Square Formula, which is:

Χ² = Σ ( (Observed Value − Expected Value)² / Expected Value )

In this publication, this is:

chiSquare = 0.

for i = 0 to rows -1

for j = 0 to colums -1

observedValue = aBin.get(i).aFloat.get(j)

expectedValue = math.max(1e-12, aBin.get(i).aFloat.get(colums) * aBin.get(rows).aFloat.get(j) / sumT) //Division by 0 protection

chiSquare += math.pow(observedValue - expectedValue, 2) / expectedValue

Together with the 'Degree of Freedom', which is (rows − 1) × (columns − 1) , the P-value can be calculated.

In this case it is P-value: 0.02462

A P-value lower than 0.05 is considered to be significant. Statistically, women tend to choose a romantic movie more, while men prefer a non-romantic one.

Users have the option to choose a P-value, calculated from a standard table or through a math.ucla.edu - Javascript-based function (see references below).

Note that the population (10 men + 10 women = 20) is small, something to consider.

Either way, this principle is applied in the script, where conditions can be chosen like rsi, close, high, ...

🔹 CONDITION

Conditions are added to the left column ('CONDITION')

For example, previous rsi values (rsi ) between 0-100, divided in separate groups

🔹 CLOSE

Then, the movement of the last close is evaluated

UP when close is higher then previous close (close )

DOWN when close is lower then previous close

EQUAL when close is equal then previous close

It is also possible to use only 2 columns by adding EQUAL to UP or DOWN

UP

DOWN/EQUAL

or

UP/EQUAL

DOWN

In other words, when previous rsi value was between 80 and 90, this resulted in:

19 times a current close higher than previous close

14 times a current close lower than previous close

0 times a current close equal than previous close

However, the P-value tells us it is not statistical significant.

NOTE: Always keep in mind that past behaviour gives no certainty about future behaviour.

A vertical line is drawn at the beginning of the chosen population (max 4990)

Here, the results seem significant.

🔹 GROUPS

It is important to ensure that the groups are formed correctly. All possibilities should be present, and conditions should only be part of 1 group.

In the example above, the two top situations are acceptable; close against close can only be higher, lower or equal.

The two examples at the bottom, however, are very poorly constructed.

Several conditions can be placed in more than 1 group, and some conditions are not integrated into a group. Even if the results are significant, they are useless because of the group formation.

A population count is added as an aid to spot errors in group formation.

In this example, there is a discrepancy between the population and total count due to the absence of a condition.

The results when rsi was between 5-25 are not included, resulting in unreliable results.

🔹 PRACTICAL EXAMPLES

In this example, we have specific groups where the condition only applies to that group.

For example, the condition rsi > 55 and rsi <= 65 isn't true in another group.

Also, every possible rsi value (0 - 100) is present in 1 of the groups.

rsi > 15 and rsi <= 25 28 times UP, 19 times DOWN and 2 times EQUAL. P-value: 0.01171

When looking in detail and examining the area 15-25 RSI, we see this:

The population is now not representative (only checking for RSI between 15-25; all other RSI values are not included), so we can ignore the P-value in this case. It is merely to check in detail. In this case, the RSI values 23 and 24 seem promising.

NOTE: We should check what the close price did without any condition.

If, for example, the close price had risen 100 times out of 100, this would make things very relative.

In this case (at least two conditions need to be present), we set 1 condition at 'always true' and another at 'always false' so we'll get only the close values without any condition:

Changing the population or the conditions will change the P-value.

In the following example, the outcome is evaluated when:

close value from 1 bar back is higher than the close value from 2 bars back

close value from 1 bar back is lower/equal than the close value from 2 bars back

Or:

close value from 1 bar back is higher than the close value from 2 bars back

close value from 1 bar back is equal than the close value from 2 bars back

close value from 1 bar back is lower than the close value from 2 bars back

In both examples, all possibilities of close against close are included in the calculations. close can only by higher, equal or lower than close

Both examples have the results without a condition included (5 = 5 and 5 < 5) so one can compare the direction of current close.

🔶 NOTES

• Always keep in mind that:

Past behaviour gives no certainty about future behaviour.

Everything depends on time, cycles, events, fundamentals, technicals, ...

• This test only works for categorical data (data in categories), such as Gender {Men, Women} or color {Red, Yellow, Green, Blue} etc., but not numerical data such as height or weight. One might argue that such tests shouldn't use rsi, close, ... values.

• Consider what you're measuring

For example rsi of the current bar will always lead to a close higher than the previous close, since this is inherent to the rsi calculations.

• Be careful; often, there are na -values at the beginning of the series, which are not included in the calculations!

• Always keep in mind considering what the close price did without any condition

• The numbers must be large enough. Each entry must be five or more. In other words, it is vital to make the 'population' large enough.

• The code can be developed further, for example, by splitting UP, DOWN in close UP 1-2%, close UP 2-3%, close UP 3-4%, ...

• rsi can be supplemented with stochRSI, MFI, sma, ema, ...

🔶 SETTINGS

🔹 Population

• Choose the population size; in other words, how many bars you want to go back to. If fewer bars are available than set, this will be automatically adjusted.

🔹 Inputs

At least two conditions need to be chosen.

• Users can add up to 11 conditions, where each condition can contain two different conditions.

🔹 RSI

• Length

🔹 Levels

• Set the used levels as desired.

🔹 Levels

• P-value: P-value retrieved using a standard table method or a function.

• Used function, derived from Chi-Square Distribution Function; JavaScript

LogGamma(Z) =>

S = 1

+ 76.18009173 / Z

- 86.50532033 / (Z+1)

+ 24.01409822 / (Z+2)

- 1.231739516 / (Z+3)

+ 0.00120858003 / (Z+4)

- 0.00000536382 / (Z+5)

(Z-.5) * math.log(Z+4.5) - (Z+4.5) + math.log(S * 2.50662827465)

Gcf(float X, A) => // Good for X > A +1

A0=0., B0=1., A1=1., B1=X, AOLD=0., N=0

while (math.abs((A1-AOLD)/A1) > .00001)

AOLD := A1

N += 1

A0 := A1+(N-A)*A0

B0 := B1+(N-A)*B0

A1 := X*A0+N*A1

B1 := X*B0+N*B1

A0 := A0/B1

B0 := B0/B1

A1 := A1/B1

B1 := 1

Prob = math.exp(A * math.log(X) - X - LogGamma(A)) * A1

1 - Prob

Gser(X, A) => // Good for X < A +1

T9 = 1. / A

G = T9

I = 1

while (T9 > G* 0.00001)

T9 := T9 * X / (A + I)

G := G + T9

I += 1

G *= math.exp(A * math.log(X) - X - LogGamma(A))

Gammacdf(x, a) =>

GI = 0.

if (x<=0)

GI := 0

else if (x

Chisqcdf = Gammacdf(Z/2, DF/2)

Chisqcdf := math.round(Chisqcdf * 100000) / 100000

pValue = 1 - Chisqcdf

🔶 REFERENCES

mathsisfun.com, Chi-Square Test

Chi-Square Distribution Function

Hedge Coin M - Statistical Support and ResistanceHedge Coin M - Statistical Support and Resistance

Introduction

"Hedge Coin M - Statistical Support and Resistance" is a sophisticated, statistically-driven indicator designed specifically for traders in the COIN-M market on Binance. It offers a nuanced approach to identifying key market levels, focusing on the dynamics of support and resistance through advanced volatility analysis.

Foundation and Credits:

This script is an advanced adaptation of TradingView's standard code for the Bollinger Bands indicator. It extends the foundational concept of Bollinger Bands by integrating additional volatility metrics.

Calculation Method

This indicator employs Volume Weighted Moving Averages (VWMA) to create two distinct sets of Bollinger Bands, named BB-a and BB-b.

BB-a is derived from the VWMA of high prices, targeting potential resistance levels.

BB-b is based on the VWMA of low prices, aimed at identifying critical support levels.

Users can independently adjust the standard deviation (SD) multipliers for the upper and lower bands of both BB-a and BB-b, accommodating different market conditions.

Enhanced Volatility Analysis

The indicator calculates additional standard deviation lines for the upper band of BB-a and the lower band of BB-b. These lines provide deeper insights into market volatility.

Plotted Graphs

The primary plots include the upper and lower bands of BB-a and BB-b, marked in distinct colors for clarity.

Additional SD lines are plotted to indicate potential extended levels of support and resistance, offering traders a broader view of possible market movements.

Purpose and Usage

"Hedge Coin M - Statistical Support and Resistance" is designed to provide traders with a consistent, statistical method for identifying significant price levels.

It aids in scaling entry into positions, helping traders to navigate the COIN-M market with more informed decision-making.

This tool is especially useful for traders who combine long-term holding with swing trading strategies, offering a balanced approach to market engagement.

Integration and Adaptation

Easily integrate this indicator into your TradingView chart for the COIN-M market.

Use the insights provided to complement your overall trading strategy, particularly in identifying and reacting to significant market movements.

Disclaimer

Important Note: This indicator is provided for informational purposes only. It does not constitute financial advice, investment advice, trading advice, or any other sort of advice. Trading decisions should be made based on your own analysis, prudence, and judgment. Please be aware of the risks involved in trading and consult a financial advisor if necessary.

Normalized Fisher Transformed VolumeGreetings Traders,

I am thrilled to introduce a game-changing tool that I've passionately developed to enhance your trading precision – the Normalized Fisher Transformed Volume indicator. Let's dive into the specifics and explore how this tool can empower you in the markets.

Unlocking Trading Precision:

Normalization and Transformation:

Normalize raw volume data to ensure a consistent scale for analysis.

The Fisher Transformation converts normalized volume data into a Gaussian distribution, providing enhanced insights into trend dynamics.

Flexible Modes for Tailored Strategies:

Choose from three distinct modes:

Volume T3 (MA) + Heatmap: Identify trends with T3 Moving Average and visualize volume strength with Heatmap.

Volume Percent Rank: Evaluate the position of current volume relative to historical data.

Volume T3 (MA) Percent Rank: Combine T3 Moving Average with percentile ranking for a comprehensive analysis.

Heatmap Visualization for Quick Insights:

Heatmap Zones and Lines visually represent volume strength relative to historical data.

Customize threshold multipliers and color options for precise Heatmap interpretation.

T3 Moving Average Integration:

Smoothed representation of volume trends with the T3 Moving Average enhances trend identification.

Percent Rank Analysis for Context:

Gauge the position of normalized volume within historical context using Percent Rank analysis.

User-Friendly Customization:

Easily adjust parameters such as length, T3 Moving Average length, Heatmap standard deviation length, and threshold multipliers.

Intuitive interface with colored bars and customizable background options for personalized analysis.

How to Use Effectively:

Mode Selection:

Identify your preferred trading strategy and select the mode that aligns with your approach.

Parameter Adjustment:

Fine-tune the indicator by adjusting parameters to match your preferred trading style.

Interpret Heatmap and T3 Analysis:

Leverage Heatmap and T3 Moving Average analysis to spot potential trend reversals, overbought/oversold conditions, and market sentiment shifts.

Conclusion:

The Normalized Fisher Transformed Volume indicator is not just a tool; it's your key to unlocking precision in trading. Crafted by Simwai, this indicator offers unique insights tailored to your specific trading needs. Dive in, explore its features, experiment with parameters, and let it guide you to more informed and precise trading decisions.

Trade wisely and prosper,

simwai