BacktestLibraryLibrary "BacktestLibrary"

A library providing functions for equity calculation and performance metrics.

since(date, active)

: Calculates the number of candles since a specified date.

Parameters:

date (simple float) : (simple float): The starting date in timestamp format (e.g., input.time(timestamp()))

active (simple bool) : (simple bool): If true, counts the number of candles since the date; if false, returns 0.

Returns: (int): The number of candles since the specified date.

buy_and_hold(r, startDate)

: Calculates the Buy and Hold Equity from a specified date.

Parameters:

r (float) : (series float): Daily returns of the asset (e.g., 0.02 for 2% move).

startDate (simple float) : (simple float): Timestamp of the starting date for the equity calculation.

Returns: (float): Buy and Hold Equity of the asset from the specified date.

equity(sig, threshold, r, startDate, signals)

: Calculates the strategy's equity on a candle-by-candle basis.

Parameters:

sig (float) : (series float): Signal values; positive for long, negative for short.

threshold (simple float) : (simple float): Signal threshold for entering trades.

r (float) : (series float): Daily returns of the asset (e.g., 0.02 for 2% move).

startDate (simple float) : (simple float): Timestamp of the starting date for the equity calculation.

signals (simple string) : (simple string): Type of signals to backtest ("Long & Short", "Long Only", "Short Only").

Returns: (float): Strategy equity on a candle-by-candle basis.

PerformanceMetrics(base, Lookback, startDate)

: Calculates performance metrics of a strategy from a specified date.

Parameters:

base (float) : (series float): Equity values of the strategy or Buy and Hold equity.

Lookback (int) : (series int): Number of periods since the start date; recommended to use the 'since' function.

startDate (simple float) : (simple float): Timestamp of the starting date for the equity calculation.

Returns: (float ): Array of performance metrics.

PerfMetricTable(buy_and_hold, strategy)

: Plots a table comparing performance metrics of Buy and Hold and Strategy equity.

Parameters:

buy_and_hold (array) : (float ): Metrics from the PerformanceMetrics() function for Buy and Hold.

strategy (array) : (float ): Metrics from the PerformanceMetrics() function for the strategy.

Returns: : Table displaying the performance metrics comparison.

Statistics

Portfolio [Afnan]🚀 Portfolio - Advanced Portfolio Management Indicator 📊

A game-changing portfolio management tool designed to help traders stay on top of their positions and manage risk efficiently. This indicator combines detailed tracking, real-time analytics, and visual clarity to ensure traders are well-equipped for the dynamic world of financial markets.

📈 Key Features 💡

Track up to 14 positions with ease

Real-time Profit & Loss (P&L) updates and risk metrics

Visual representation of entry, stop-loss (SL), and target levels

Alerts for stop-loss breaches and target achievements

Comprehensive portfolio summaries for quick analysis

Customizable options to suit individual trading styles

🔍 Main Components ⚙️

📊 1. Position Tracking

Detailed position data: entry, stop-loss, target levels, and more

Real-time risk-reward ratios

Insights into position size and exposure percentages

Continuous updates on P&L in real-time

📉 2. Visual Indicators

Clear visual markers for entry, SL, and target prices

Price labels with detailed percentage changes

Indicators that show the current position's market status

💼 3. Portfolio Summary

Aggregate account values and exposure

Summarized P&L metrics across all positions

Risk management insights for better decision-making

Daily performance tracking to evaluate strategies

⚠️ 4. Alert System

Instant notifications for stop-loss breaches

Alerts when target prices are hit

Alerts operate for the current chart symbol

⚡ Customization Options 🎨

Show or hide specific data columns

Adjust the table's position and size for better visibility

Personalize color schemes and text styles

Switch between full portfolio view and single symbol focus

📱 How to Use 📝

Input your positions in the indicator's settings

Enable or disable specific positions dynamically

Customize display preferences to your liking

Set up alerts for proactive risk management

Monitor all your trading activities in one comprehensive dashboard

📌 Important Notes ℹ️

Compatible with any trading symbol

Updates seamlessly during market hours

Alerts are specific to the currently active chart symbol

Maximum capacity: 14 simultaneous positions

Created by: @AfnanTAjuddin

⚠️ Disclaimer ⚠️

This indicator is a tool for informational purposes only. Ensure all calculations are verified and consult a financial professional before making investment decisions.

🎯 "Stay disciplined, trade smart, and let data guide your decisions." 📊

ArrayMovingAveragesLibrary "ArrayMovingAverages"

This library adds several moving average methods to arrays, so you can call, eg.:

myArray.ema(3)

method emaArray(id, length)

Calculate Exponential Moving Average (EMA) for Arrays

Namespace types: array

Parameters:

id (array) : (array) Input array

length (int) : (int) Length of the EMA

Returns: (array) Array of EMA values

method ema(id, length)

Get the last value of the EMA array

Namespace types: array

Parameters:

id (array) : (array) Input array

length (int) : (int) Length of the EMA

Returns: (float) Last EMA value or na if empty

method rmaArray(id, length)

Calculate Rolling Moving Average (RMA) for Arrays

Namespace types: array

Parameters:

id (array) : (array) Input array

length (int) : (int) Length of the RMA

Returns: (array) Array of RMA values

method rma(id, length)

Get the last value of the RMA array

Namespace types: array

Parameters:

id (array) : (array) Input array

length (int) : (int) Length of the RMA

Returns: (float) Last RMA value or na if empty

method smaArray(id, windowSize)

Calculate Simple Moving Average (SMA) for Arrays

Namespace types: array

Parameters:

id (array) : (array) Input array

windowSize (int) : (int) Window size for calculation, defaults to array size

Returns: (array) Array of SMA values

method sma(id, windowSize)

Get the last value of the SMA array

Namespace types: array

Parameters:

id (array) : (array) Input array

windowSize (int) : (int) Window size for calculation, defaults to array size

Returns: (float) Last SMA value or na if empty

method wmaArray(id, windowSize)

Calculate Weighted Moving Average (WMA) for Arrays

Namespace types: array

Parameters:

id (array) : (array) Input array

windowSize (int) : (int) Window size for calculation, defaults to array size

Returns: (array) Array of WMA values

method wma(id, windowSize)

Get the last value of the WMA array

Namespace types: array

Parameters:

id (array) : (array) Input array

windowSize (int) : (int) Window size for calculation, defaults to array size

Returns: (float) Last WMA value or na if empty

Quick scan for signal🙏🏻 Hey TV, this is QSFS, following:

^^ Quick scan for drift (QSFD)

^^ Quick scan for cycles (QSFC)

As mentioned before, ML trading is all about spotting any kind of non-randomness, and this metric (along with 2 previously posted) gonna help ya'll do it fast. This one will show you whether your time series possibly exhibits mean-reverting / consistent / noisy behavior, that can be later confirmed or denied by more sophisticated tools. This metric is O(n) in windowed mode and O(1) if calculated incrementally on each data update, so you can scan Ks of datasets w/o worrying about melting da ice.

^^ windowed mode

Now the post will be divided into several sections, and a couple of things I guess you’ve never seen or thought about in your life:

1) About Efficiency Ratios posted there on TV;

Some of you might say this is the Efficiency Ratio you’ve seen in Perry's book. Firstly, I can assure you that neither me nor Perry, just as X amount of quants all over the world and who knows who else, would say smth like, "I invented it," lol. This is just a thing you R&D when you need it. Secondly, I invite you (and mods & admin as well) to take a lil glimpse at the following screenshot:

^^ not cool...

So basically, all the Efficiency Ratios that were copypasted to our platform suffer the same bug: dudes don’t know how indexing works in Pine Script. I mean, it’s ok, I been doing the same mistakes as well, but loxx, cmon bro, you... If you guys ever read it, the lines 20 and 22 in da code are dedicated to you xD

2) About the metric;

This supports both moving window mode when Length > 0 and all-data expanding window mode when Length < 1, calculating incrementally from the very first data point in the series: O(n) on history, O(1) on live updates.

Now, why do I SQRT transform the result? This is a natural action since the metric (being a ratio in essence) is bounded between 0 and 1, so it can be modeled with a beta distribution. When you SQRT transform it, it still stays beta (think what happens when you apply a square root to 0.01 or 0.99), but it becomes symmetric around its typical value and starts to follow a bell-shaped curve. This can be easily checked with a normality test or by applying a set of percentiles and seeing the distances between them are almost equal.

Then I noticed that on different moving window sizes, the typical value of the metric seems to slide: higher window sizes lead to lower typical values across the moving windows. Turned out this can be modeled the same way confidence intervals are made. Lines 34 and 35 explain it all, I guess. You can see smth alike on an autocorrelogram. These two match the mean & mean + 1 stdev applied to the metric. This way, we’ve just magically received data to estimate alpha and beta parameters of the beta distribution using the method of moments. Having alpha and beta, we can now estimate everything further. Btw, there’s an alternative parameterization for beta distributions based on data length.

Now what you’ll see next is... u guys actually have no idea how deep and unrealistically minimalistic the underlying math principles are here.

I’m sure I’m not the only one in the universe who figured it out, but the thing is, it’s nowhere online or offline. By calculating higher-order moments & combining them, you can find natural adaptive thresholds that can later be used for anomaly detection/control applications for any data. No hardcoded thresholds, purely data-driven. Imma come back to this in one of the next drops, but the truest ones can already see it in this code. This way we get dem thresholds.

Your main thresholds are: basis, upper, and lower deviations. You can follow the common logic I’ve described in my previous scripts on how to use them. You just register an event when the metric goes higher/lower than a certain threshold based on what you’re looking for. Then you take the time series and confirm a certain behavior you were looking for by using an appropriate stat test. Or just run a certain strategy.

To avoid numerous triggers when the metric jitters around a threshold, you can follow this logic: forget about one threshold if touched, until another threshold is touched.

In general, when the metric gets higher than certain thresholds, like upper deviation, it means the signal is stronger than noise. You confirm it with a more sophisticated tool & run momentum strategies if drift is in place, or volatility strategies if there’s no drift in place. Otherwise, you confirm & run ~ mean-reverting strategies, regardless of whether there’s drift or not. Just don’t operate against the trend—hedge otherwise.

3) Flex;

Extension and limit thresholds based on distribution moments gonna be discussed properly later, but now you can see this:

^^ magic

Look at the thresholds—adaptive and dynamic. Do you see any optimizations? No ML, no DL, closed-form solution, but how? Just a formula based on a couple of variables? Maybe it’s just how the Universe works, but how can you know if you don’t understand how fundamentally numbers 3 and 15 are related to the normal distribution? Hm, why do they always say 3 sigmas but can’t say why? Maybe you can be different and say why?

This is the primordial power of statistical modeling.

4) Thanks;

I really wanna dedicate this to Charlotte de Witte & Marion Di Napoli, and their new track "Sanctum." It really gets you connected to the Source—I had it in my soul when I was doing all this ∞

MTF ADX TableThis Indicator displays a table on the chart with the Average Directional Index (ADX) values for two different timeframes. It calculates the ADX using a custom formula and shows the ADX values along with their corresponding timeframes. The table's position, font size, and background color can be customized, and the timeframes are labeled with "ADX" appended to their unit (e.g., "5m ADX", "1D ADX"). The table updates dynamically with the latest ADX values for each timeframe. The indicator also provides a rating, based of the thresholds settings

BTC vs Altcoin CorrelationThis Pine Script indicator calculates and visualizes the rolling correlation between Bitcoin (BTC) and a selected altcoin, while providing insights into the percentage of time the correlation remains above a user-defined threshold. Users can independently configure the correlation calculation period and the lookback period for measuring the percentage of time above the threshold. The correlation is displayed as a color-coded line: green when above the threshold and red otherwise, with a dashed horizontal line marking the threshold level. A dynamic table displays the current correlation value and the percentage of time spent above the threshold within the specified period, enabling quick evaluation of correlation dynamics between BTC and the chosen altcoin.

Consecutive Lower Highs/Higher Lows v1 [tradinggeniusberlin]This indicator counts the lower highs and higher low streaks. If the streak is above a certain threshold a buy or exit arrow is shown.

Idea:

The probability of a reversal is rising the more lower highs the asset had already because if mean reversion tendencies of asset prices. Especially in uptrend above the 20ma and/or 50ma.

How to use it:

In Uptrends, lower high streak of 3 or more, enter at first new high.

Daily PlayDaily Play Indicator

The Daily Play Indicator is a clean and versatile tool designed to help traders organize and execute their daily trading plan directly on their charts. This indicator simplifies your workflow by visually displaying key inputs like market trend, directional bias, and key levels, making it easier to focus on your trading strategy.

Features

Dropdown Selection for Trend and Bias:

• Set the overall market trend (Bullish, Bearish, or Neutral) and your directional bias (Long, Short, or Neutral) using intuitive dropdown menus. No more manual typing or guesswork!

Key Levels:

Quickly input and display the Previous Day High and Previous Day Low. These levels are essential for many trading strategies, such as breakouts.

Real-Time News Notes:

Add a quick note about impactful news or market events (e.g., “Fed meeting today” or “Earnings season”) to keep contextual awareness while trading.

Simple On-Chart Display:

The indicator creates a “table-like” structure on the chart, aligning your inputs in an easy-to-read format. The data is positioned dynamically so it doesn’t obstruct the price action.

Customisable Visual Style:

Simple labels with clear text to ensure that your chart remains neat and tidy.

----

Use Case

The Daily Play Indicator is ideal for:

• Day traders and scalpers who rely on precise planning and real-time execution.

• Swing traders looking to mark critical levels and develop a trade plan before the session begins.

• Anyone who needs a structured way to stay focused and disciplined during volatile market conditions.

By integrating this tool into your workflow, you can easily align your daily preparation with live market action.

----

How to Use

Open the indicator settings to configure your inputs:

• Trend: Use the dropdown to choose between Bullish, Bearish, or Neutral.

• Bias: Select Long, Short, or Neutral to align your personal bias with the market.

• Previous Day Levels: Enter the High and Low of the previous trading session for key reference points.

• News: Add a short description of any relevant market-moving events.

MadTrend [InvestorUnknown]The MadTrend indicator is an experimental tool that combines the Median and Median Absolute Deviation (MAD) to generate signals, much like the popular Supertrend indicator. In addition to identifying Long and Short positions, MadTrend introduces RISK-ON and RISK-OFF states for each trade direction, providing traders with nuanced insights into market conditions.

Core Concepts

Median and Median Absolute Deviation (MAD)

Median: The middle value in a sorted list of numbers, offering a robust measure of central tendency less affected by outliers.

Median Absolute Deviation (MAD): Measures the average distance between each data point and the median, providing a robust estimation of volatility.

Supertrend-like Functionality

MadTrend utilizes the median and MAD in a manner similar to how Supertrend uses averages and volatility measures to determine trend direction and potential reversal points.

RISK-ON and RISK-OFF States

RISK-ON: Indicates favorable conditions for entering or holding a position in the current trend direction.

RISK-OFF: Suggests caution, signaling RISK-ON end and potential trend weakening or reversal.

Calculating MAD

The mad function calculates the median of the absolute deviations from the median, providing a robust measure of volatility.

// Function to calculate the Median Absolute Deviation (MAD)

mad(series float src, simple int length) =>

med = ta.median(src, length) // Calculate median

abs_deviations = math.abs(src - med) // Calculate absolute deviations from median

ta.median(abs_deviations, length) // Return the median of the absolute deviations

MADTrend Function

The MADTrend function calculates the median and MAD-based upper (med_p) and lower (med_m) bands. It determines the trend direction based on price crossing these bands.

MADTrend(series float src, simple int length, simple float mad_mult) =>

// Calculate MAD (volatility measure)

mad_value = mad(close, length)

// Calculate the MAD-based moving average by scaling the price data with MAD

median = ta.median(close, length)

med_p = median + (mad_value * mad_mult)

med_m = median - (mad_value * mad_mult)

var direction = 0

if ta.crossover(src, med_p)

direction := 1

else if ta.crossunder(src, med_m)

direction := -1

Trend Direction and Signals

Long Position (direction = 1): When the price crosses above the upper MAD band (med_p).

Short Position (direction = -1): When the price crosses below the lower MAD band (med_m).

RISK-ON: When the price moves further in the direction of the trend (beyond median +- MAD) after the initial signal.

RISK-OFF: When the price retraces towards the median, signaling potential weakening of the trend.

RISK-ON and RISK-OFF States

RISK-ON LONG: Price moves above the upper band after a Long signal, indicating strengthening bullish momentum.

RISK-OFF LONG: Price falls back below the upper band, suggesting potential weakness in the bullish trend.

RISK-ON SHORT: Price moves below the lower band after a Short signal, indicating strengthening bearish momentum.

RISK-OFF SHORT: Price rises back above the lower band, suggesting potential weakness in the bearish trend.

Picture below show example RISK-ON periods which can be identified by “cloud”

Note: Highlighted areas on the chart indicating RISK-ON and RISK-OFF periods for both Long and Short positions.

Implementation Details

Inputs and Parameters:

Source (input_src): The price data used for calculations (e.g., close, open, high, low).

Median Length (length): The number of periods over which the median and MAD are calculated.

MAD Multiplier (mad_mult): Determines the distance of the upper and lower bands from the median.

Calculations:

Median and MAD are recalculated each period based on the specified length.

Upper (med_p) and Lower (med_m) Bands are computed by adding and subtracting the scaled MAD from the median.

Visual representation of the indicator on a price chart:

Backtesting and Performance Metrics

The MadTrend indicator includes a Backtesting Mode with a performance metrics table to evaluate its effectiveness compared to a simple buy-and-hold strategy.

Equity Calculation:

Calculates the equity curve based on the signals generated by the indicator.

Performance Metrics:

Metrics such as Mean Returns, Standard Deviation, Sharpe Ratio, Sortino Ratio, and Omega Ratio are computed.

The metrics are displayed in a table for both the strategy and the buy-and-hold approach.

Note: Due to the use of labels and plot shapes, automatic chart scaling may not function ideally in Backtest Mode.

Alerts and Notifications

MadTrend provides alert conditions to notify traders of significant events:

Trend Change Alerts

RISK-ON and RISK-OFF Alerts - Provides real-time notifications about the RISK-ON and RISK-OFF states for proactive trade management.

Customization and Calibration

Default Settings: The provided default settings are experimental and not optimized. They serve as a starting point for users.

Parameter Adjustment: Traders are encouraged to calibrate the indicator's parameters (e.g., length, mad_mult) to suit their specific trading style and the characteristics of the asset being analyzed.

Source Input: The indicator allows for different price inputs (open, high, low, close, etc.), offering flexibility in how the median and MAD are calculated.

Important Notes

Market Conditions: The effectiveness of the MadTrend indicator can vary across different market conditions. Regular calibration is recommended.

Backtest Limitations: Backtesting results are historical and do not guarantee future performance.

Risk Management: Always apply sound risk management practices when using any trading indicator.

Mean Price

^^ Plotting switched to Line.

This method of financial time series (aka bars) downsampling is literally, naturally, and thankfully the best you can do in terms of maximizing info gain. You can finally chill and feed it to your studies & eyes, and probably use nothing else anymore.

(HL2 and occ3 also have use cases, but other aggregation methods? Not really, even if they do, the use cases are ‘very’ specific). Tho in order to understand why, you gotta read the following wall, or just believe me telling you, ‘I put it on my momma’.

The true story about trading volumes and why this is all a big misdirection

Actually, you don’t need to be a quant to get there. All you gotta do is stop blindly following other people’s contextual (at best) solutions, eg OC2 aggregation xD, and start using your own brain to figure things out.

Every individual trade (basically an imprint on 1D price space that emerges when market orders hit the order book) has several features like: price, time, volume, AND direction (Up if a market buy order hits the asks, Down if a market sell order hits the bids). Now, the last two features—volume and direction—can be effectively combined into one (by multiplying volume by 1 or -1), and this is probably how every order matching engine should output data. If we’re not considering size/direction, we’re leaving data behind. Moreover, trades aren’t just one-price dots all the time. One trade can consume liquidity on several levels of the order book, so a single trade can be several ticks big on the price axis.

You may think now that there are no zero-volume ticks. Well, yes and no. It depends on how you design an exchange and whether you allow intra-spread trades/mid-spread trades (now try to Google it). Intra-spread trades could happen if implemented when a matching engine receives both buy and sell orders at the same microsecond period. This way, you can match the orders with each other at a better price for both parties without even hitting the book and consuming liquidity. Also, if orders have different sizes, the remaining part of the bigger order can be sent to the order book. Basically, this type of trade can be treated as an OTC trade, having zero volume because we never actually hit the book—there’s no imprint. Another reason why it makes sense is when we think about volume as an impact or imbalance act, and how the medium (order book in our case) responds to it, providing information. OTC and mid-spread trades are not aggressive sells or buys; they’re neutral ticks, so to say. However huge they are, sometimes many blocks on NYSE, they don’t move the price because there’s no impact on the medium (again, which is the order book)—they’re not providing information.

... Now, we need to aggregate these trades into, let’s say, 1-hour bars (remember that a trade can have either positive or negative volume). We either don’t want to do it, or we don’t have this kind of information. What we can do is take already aggregated OHLC bars and extract all the info from them. Given the market is fractal, bars & trades gotta have the same set of features:

- Highest & lowest ticks (high & low) <- by price;

- First & last ticks (open & close) <- by time;

- Biggest and smallest ticks <- by volume.*

*e.g., in the array ,

2323: biggest trade,

-1212: smallest trade.

Now, in our world, somehow nobody started to care about the biggest and smallest trades and their inclusion in OHLC data, while this is actually natural. It’s the same way as it’s done with high & low and open & close: we choose the minimum and maximum value of a given feature/axis within the aggregation period.

So, we don’t have these 2 values: biggest and smallest ticks. The best we can do is infer them, and given the fact the biggest and smallest ticks can be located with the same probability everywhere, all we can do is predict them in the middle of the bar, both in time and price axes. That’s why you can see two HL2’s in each of the 3 formulas in the code.

So, summed up absolute volumes that you see in almost every trading platform are actually just a derivative metric, something that I call Type 2 time series in my own (proprietary ‘for now’) methods. It doesn’t have much to do with market orders hitting the non-uniform medium (aka order book); it’s more like a statistic. Still wanna use VWAP? Ok, but you gotta understand you’re weighting Type 1 (natural) time series by Type 2 (synthetic) ones.

How to combine all the data in the right way (khmm khhm ‘order’)

Now, since we have 6 values for each bar, let’s see what information we have about them, what we don’t have, and what we can do about it:

- Open and close: we got both when and where (time (order) and price);

- High and low: we got where, but we don’t know when;

- Biggest & smallest trades: we know shit, we infer it the way it was described before.'

By using the location of the close & open prices relative to the high & low prices, we can make educated guesses about whether high or low was made first in a given bar. It’s not perfect, but it’s ultimately all we can do—this is the very last bit of info we can extract from the data we have.

There are 2 methods for inferring volume delta (which I call simply volume) that are presented everywhere, even here on TradingView. Funny thing is, this is actually 2 parts of the 1 method. I wonder how many folks see through it xD. The same method can be used for both inferring volume delta AND making educated guesses whether high or low was made first.

Imagine and/or find the cases on your charts to understand faster:

* Close > open means we have an up bar and probably the volume is positive, and probably high was made later than low.

* Close < open means we have a down bar and probably the volume is negative, and probably low was made later than high.

Now that’s the point when you see that these 2 mentioned methods are actually parts of the 1 method:

If close = open, we still have another clue: distance from open/close pair to high (HC), and distance from open/close pair to low (LC):

* HC < LC, probably high was made later.

* HC > LC, probably low was made later.

And only if close = open and HC = LC, only in this case we have no clue whether high or low was made earlier within a bar. We simply don’t have any more information to even guess. This bar is called a neutral bar.

At this point, we have both time (order) and price info for each of our 6 values. Now, we have to solve another weighted average problem, and that’s it. We’ll weight prices according to the order we’ve guessed. In the neutral bar case, open has a weight of 1, close has a weight of 3, and both high and low have weights of 2 since we can’t infer which one was made first. In all cases, biggest and smallest ticks are modeled with HL2 and weighted like they’re located in the middle of the bar in a time sense.

P.S.: I’ve also included a "robust" method where all the bars are treated like neutral ones. I’ve used it before; obviously, it has lesser info gain -> works a bit worse.

Cryptocurrency StrengthMulti-Currency Analysis: Monitor up to 19 different currencies simultaneously, including major pairs like USD, EUR, JPY, and GBP, as well as emerging market currencies such as CNY, INR, and BRL.

Customizable Display: Easily toggle the visibility of each currency and personalize their colors to suit your preferences, allowing for a tailored analysis experience.

Real-Time Strength Measurement: The indicator calculates and displays the relative strength of each currency in real-time, helping you identify potential trends and trading opportunities.

Clear Visual Representation: With color-coded lines and a dynamic legend, the indicator presents complex currency relationships in an easy-to-understand format.

Advantages

Comprehensive Market View: Gain insights into the broader forex market dynamics by analyzing multiple currencies at once.

Trend Identification: Quickly spot strong and weak currencies, aiding in the identification of potential trending pairs.

Divergence Detection: Use the indicator to identify divergences between currency strength and price action, potentially signaling reversals or continuation patterns.

Flexible Time Frames: Apply the indicator across various time frames to align with your trading strategy, from intraday to long-term analysis.

Enhanced Decision Making: Make more informed trading decisions by understanding the relative strength of currencies involved in your trades.

Unique Qualities

TSI-Based Calculations: Utilizes the True Strength Index for a more nuanced and responsive measure of currency strength compared to simple price-based indicators.

Adaptive Legend: The indicator features a dynamic legend that updates automatically based on the selected currencies, ensuring a clutter-free and relevant display.

Emerging Market Inclusion: Unlike many standard currency strength indicators, this tool includes a wide range of emerging market currencies, providing a truly global perspective.

Whether you're a seasoned forex trader or just starting out, this Currency Strength Indicator offers valuable insights that can complement your existing strategy and potentially improve your trading outcomes. Its combination of comprehensive analysis, customization options, and clear visualization makes it an essential tool for navigating the complex world of currency trading.

Currency StrengthThis innovative Currency Strength Indicator is a powerful tool for forex traders, offering a comprehensive and visually intuitive way to analyze the relative strength of multiple currencies simultaneously. Here's what makes this indicator stand out:

Extensive Currency Coverage

One of the most striking features of this indicator is its extensive coverage of currencies. While many similar tools focus on just the major currencies, this indicator includes:

Major currencies: USD, EUR, JPY, GBP, CHF, CAD, AUD, NZD

Additional currencies: CNY, HKD, KRW, MXN, INR, RUB, SGD, TRY, BRL, ZAR, THB

This wide range allows traders to gain insights into a broader spectrum of the forex market, including emerging markets and less commonly traded currencies.

Unique Visual Presentation

The indicator boasts a clear and user-friendly interface:

Each currency is represented by a distinct colored line for easy identification

A legend is prominently displayed at the top of the chart, using color-coded labels for quick reference

Users can customize which currencies to display, allowing for a tailored analysis

This clean, organized presentation enables traders to quickly grasp the relative strengths of different currencies at a glance.

Robust Measurement Methodology

The indicator employs the True Strength Index (TSI) to calculate currency strength, which provides several advantages:

TSI is a momentum oscillator that shows both trend direction and overbought/oversold conditions

It uses two smoothing periods (fast and slow), which helps filter out market noise and provides more reliable signals

The indicator calculates TSI for each currency index (e.g., DXY for USD, EXY for EUR), ensuring a comprehensive strength measurement

By using TSI, this indicator offers a more nuanced and accurate representation of currency strength compared to simpler moving average-based indicators.

Customization and Flexibility

Traders can fine-tune the indicator to suit their needs:

Adjustable TSI parameters (fast and slow periods)

Ability to show/hide specific currencies

Customizable color scheme for each currency line

Practical Applications

This Currency Strength Indicator can be used for various trading strategies:

Identifying potential trend reversals when a currency reaches extreme overbought or oversold levels

Spotting divergences between currency pairs

Confirming trends across multiple timeframes

Enhancing multi-pair trading strategies

By providing a clear, comprehensive, and customizable view of currency strength across a wide range of currencies, this indicator equips traders with valuable insights for making informed trading decisions in the complex world of forex.

BTC Seasonality Strategy (Weekly)This strategy identifies potential weekend opportunities in Bitcoin (BTC) markets by leveraging the concept of seasonality, entering a position at a predefined time and day, and exiting at a specified time and day.

Key Features

Customizable Time and Day Selection:

Users can select the entry and exit days and corresponding times (in EST).

Directional Flexibility:

The strategy allows traders to choose between long or short positions.

TradingView Compliance:

The script adheres to TradingView's house rules, avoids overly complex conditions, and provides clear user-configurable inputs.

How It Works

The script determines the current weekday and hour in EST, converting TradingView's UTC time for accurate comparisons.

If the current day and hour match the selected entry conditions, a trade (long or short) is opened.

The position is closed when the current day and hour match the specified exit conditions.

Theoretical Basis

Market Seasonality:

The concept of seasonality in financial markets refers to predictable patterns based on time, such as weekends or specific days of the week. Studies have shown that cryptocurrency markets exhibit unique trading behaviors during weekends due to reduced institutional activity and higher retail participation behavioral Biases**:

Retail traders often dominate weekend markets, potentially causing predictable inefficiencies .

Reverences**

Baur, D. G., Hong, K., & Lee, A. D. (2018). Bitcoin: Medium of exchange or speculative assets? Journal of International Financial Markets, Institutions and Money, 54, 177–189.

Urquhart, A. (2016). The inefficiency of Bitcoin. Economics Letters, 148, 80–82.

simple swing indicator-KTRNSE:NIFTY

1. Pivot High/Low as Lines:

Purpose: Identifies local peaks (pivot highs) and troughs (pivot lows) in price and draws horizontal lines at these levels.

How it Works:

A pivot high occurs when the price is higher than the surrounding bars (based on the pivotLength parameter).

A pivot low occurs when the price is lower than the surrounding bars.

These pivots are drawn as horizontal lines at the price level of the pivot.

Visualization:

Pivot High: A red horizontal line is drawn at the price level of the pivot high.

Pivot Low: A green horizontal line is drawn at the price level of the pivot low.

Example:

Imagine the price is trending up, and at some point, it forms a peak. The script identifies this peak as a pivot high and draws a red line at the price of that peak. Similarly, if the price forms a trough, the script will draw a green line at the low point.

2. Moving Averages (20-day and 50-day):

Purpose: Plots the 20-day and 50-day simple moving averages (SMA) on the chart.

How it Works:

The 20-day SMA smooths the closing price over the last 20 days.

The 50-day SMA smooths the closing price over the last 50 days.

These lines provide an overview of short-term and long-term price trends.

Visualization:

20-day SMA: A blue line showing the 20-day moving average.

50-day SMA: An orange line showing the 50-day moving average.

Example:

When the price is above both moving averages, it indicates an uptrend. If the price crosses below these averages, it might signal a downtrend.

3. Supertrend:

Purpose: The Supertrend is an indicator based on the Average True Range (ATR) and is used to track the market trend.

How it Works:

When the market is in an uptrend, the Supertrend line will be green.

When the market is in a downtrend, the Supertrend line will be red.

Visualization:

Uptrend: The Supertrend line will be plotted in green.

Downtrend: The Supertrend line will be plotted in red.

Example:

If the price is above the Supertrend, the market is considered to be in an uptrend, and if the price is below the Supertrend, the market is in a downtrend.

4. Momentum (Rate of Change):

Purpose: Measures the rate at which the price changes over a set period, showing if the momentum is positive or negative.

How it Works:

The Rate of Change (ROC) measures how much the price has changed over a certain number of periods (e.g., 14).

Positive ROC indicates upward momentum, and negative ROC indicates downward momentum.

Visualization:

Positive ROC: A purple line is plotted above the zero line.

Negative ROC: A purple line is plotted below the zero line.

Example:

If the ROC line is above zero, it means the price is increasing, suggesting bullish momentum. If the ROC is below zero, it indicates bearish momentum.

5. Volume:

Purpose: Displays the volume of traded assets, giving insight into the strength of price movements.

How it Works:

The script will color the volume bars based on whether the price closed higher or lower than the previous bar.

Green bars indicate bullish volume (closing price higher than the previous bar), and red bars indicate bearish volume (closing price lower than the previous bar).

Visualization:

Bullish Volume: Green volume bars when the price closes higher.

Bearish Volume: Red volume bars when the price closes lower.

Example:

If you see a green volume bar, it suggests that the market is participating in an uptrend, and the price has closed higher than the previous period. Red bars indicate a downtrend or selling pressure.

6. MACD (Moving Average Convergence Divergence):

Purpose: The MACD is a trend-following momentum indicator that shows the relationship between two moving averages of the price.

How it Works:

The MACD Line is the difference between the 12-period EMA (Exponential Moving Average) and the 26-period EMA.

The Signal Line is the 9-period EMA of the MACD Line.

The MACD Histogram shows the difference between the MACD line and the Signal line.

Visualization:

MACD Line: A blue line representing the difference between the 12-period and 26-period EMAs.

Signal Line: An orange line representing the 9-period EMA of the MACD line.

MACD Histogram: A red or green histogram that shows the difference between the MACD line and the Signal line.

Example:

When the MACD line crosses above the Signal line, it’s considered a bullish signal. When the MACD line crosses below the Signal line, it’s considered a bearish signal.

Full Chart Example:

Imagine you're looking at a price chart with all the indicators:

Pivot High/Low Lines are drawn as red and green horizontal lines.

20-day and 50-day SMAs are plotted as blue and orange lines, respectively.

Supertrend shows a green or red line indicating the trend.

Momentum (ROC) is shown as a purple line oscillating around zero.

Volume bars are green or red based on whether the close is higher or lower.

MACD appears as a blue line and orange line, with a red or green histogram showing the MACD vs. Signal line difference.

How the Indicators Work Together:

Trend Confirmation: If the price is above the Supertrend line and both SMAs are trending up, it indicates a strong bullish trend.

Momentum: If the ROC is positive and the MACD line is above the Signal line, it further confirms bullish momentum.

Volume: Increasing volume, especially with green bars, suggests that the trend is being supported by active participation.

By using these combined indicators, you can get a comprehensive view of the market's trend, momentum, and potential reversal points (via pivot highs and lows).

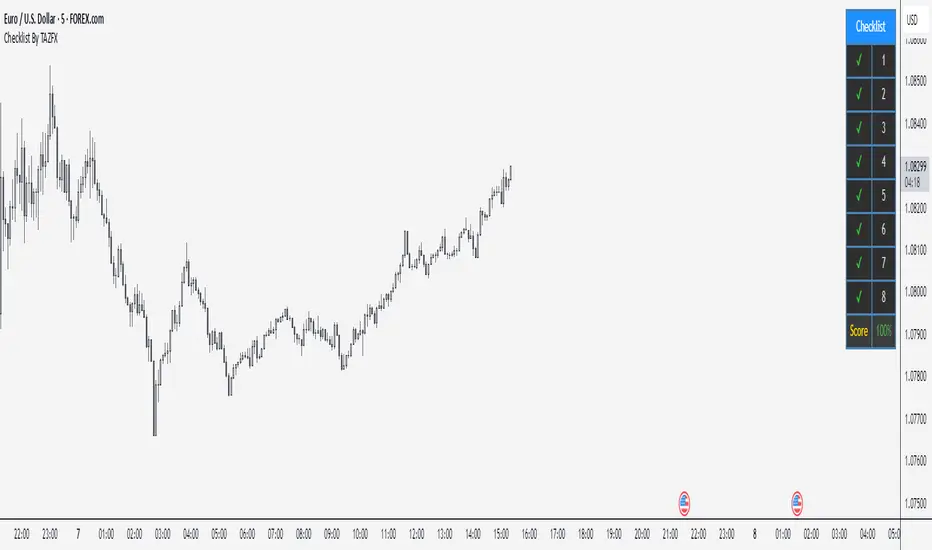

Checklist By TAZFX with Trade ScoreTrading Checklist is a customizable indicator designed for traders who want to stay disciplined and stick to their trading rules. Using this indicator, you can easily create and display your own personalized checklist of trading rules directly on your TradingView chart.

1. Customizable Settings:

• Positioning : Place the table in one of nine positions on the chart (e.g., bottom left, top right).

• Header : Modify the banner text, size, and color.

• Row Content : Define text for each row and control visibility.

• Appearance : Adjust text and background colors.

2. Checklist Table:

•Displays up to 8 rows with checkboxes (✅/❌) and custom labels for trade evaluation.

•Useful for tracking whether specific trade conditions or rules are met.

3. Trade Score Calculation:

•The Trade Score is a percentage that shows how many of your checklist items are checked compared to the total visible items.

[SGM Auto Regressiv - significant lags only]This Pine Script™ is designed for traders seeking advanced statistical analysis based on autoregressive (AR) models, with automatic filtering of significant lags according to a customizable confidence threshold.

Key Features:

AR(p) Model with Significance Filtering:

Only statistically significant lags (based on the selected confidence level) are included in the model calculations.

Coefficient Weighting Options:

Uniform weighting.

Weighting based on the t-statistic.

Visualization of Key Indicators:

Dynamic plotting of autoregressive values, upper and lower bounds (based on standard deviation).

Buy ("Buy") and Sell ("Sell") signals when values exceed the defined bounds.

Robust Analysis:

Calculation of statistical parameters: T-stat, p-value, skewness, kurtosis, r², and the Jarque-Bera test to assess the robustness and normality of residuals.

Summary of results displayed in a visual table for simplified interpretation.

Interactive Tables:

Display of lags, coefficients, t-statistics, p-values, and their significance via a dynamic table.

Overall robustness indicator and interpretation of results ("Good," "Non-significant," etc.).

Easy Customization:

Adjustable confidence level (90% to 99%).

Configurable lengths for moving average and standard deviation to fine-tune signal thresholds.

Benefits for Traders:

Effortless Analysis:

Automatically identifies significant relationships between past and present values, removing unnecessary assumptions.

Enhanced Accuracy:

Filters signals based on rigorous statistical criteria to avoid false signals.

Clear Visualization:

Interactive tables and plots to quickly understand critical parameters.

Default Configuration:

Confidence level: 95%.

Lag weighting: Uniform.

Moving average length: 20 periods.

Standard deviation length: 15 periods.

Usage Recommendations:

Ideal for analyzing volatile assets or identifying potential reversal zones.

Use alongside other indicators to confirm signals.

QuantifyPS - 1Library "QuantifyPS"

normdist(z)

Parameters:

z (float) : (float): The z-score for which the CDF is to be calculated.

Returns: (float): The cumulative probability corresponding to the input z-score.

Notes:

- Uses an approximation method for the normal distribution CDF, which is computationally efficient.

- The result is accurate for most practical purposes but may have minor deviations for extreme values of `z`.

Formula:

- Based on the approximation formula:

`Φ(z) ≈ 1 - f(z) * P(t)` if `z > 0`, otherwise `Φ(z) ≈ f(z) * P(t)`,

where:

`f(z) = 0.3989423 * exp(-z^2 / 2)` (PDF of standard normal distribution)

`P(t) = Σ [c * t^i]` with constants `c` and `t = 1 / (1 + 0.2316419 * |z|)`.

Implementation details:

- The approximation uses five coefficients for the polynomial part of the CDF.

- Handles both positive and negative values of `z` symmetrically.

Constants:

- The coefficients and scaling factors are chosen to minimize approximation errors.

gamma(x)

Parameters:

x (float) : (float): The input value for which the Gamma function is to be calculated.

Must be greater than 0. For x <= 0, the function returns `na` as it is undefined.

Returns: (float): Approximation of the Gamma function for the input `x`.

Notes:

- The Lanczos approximation provides a numerically stable and efficient method to compute the Gamma function.

- The function is not defined for `x <= 0` and will return `na` in such cases.

- Uses precomputed Lanczos coefficients for accuracy.

- Includes handling for small numerical inaccuracies.

Formula:

- The Gamma function is approximated as:

`Γ(x) ≈ sqrt(2π) * t^(x + 0.5) * e^(-t) * Σ(p / (x + k))`

where `t = x + g + 0.5` and `p` is the array of Lanczos coefficients.

Implementation details:

- Lanczos coefficients (`p`) are precomputed and stored in an array.

- The summation iterates over these coefficients to compute the final result.

- The constant `g` controls the precision of the approximation (commonly `g = 7`).

t_cdf(t, df)

Parameters:

t (float) : (float): The t-statistic for which the CDF value is to be calculated.

df (int) : (int): Degrees of freedom of the t-distribution.

Returns: (float): Approximate CDF value for the given t-statistic.

Notes:

- This function computes a one-tailed p-value.

- Relies on an approximation formula using gamma functions and standard t-distribution properties.

- May not be as accurate as specialized statistical libraries for extreme values or very high degrees of freedom.

Formula:

- Let `x = df / (t^2 + df)`.

- The approximation formula is derived using:

`CDF(t, df) ≈ 1 - * x^((df + 1) / 2) / 2`,

where Γ represents the gamma function.

Implementation details:

- Computes the gamma ratio for normalization.

- Applies the t-distribution formula for one-tailed probabilities.

tStatForPValue(p, df)

Parameters:

p (float) : (float): P-value for which the t-statistic needs to be calculated.

Must be in the interval (0, 1).

df (int) : (int): Degrees of freedom of the t-distribution.

Returns: (float): The t-statistic corresponding to the given p-value.

Notes:

- If `p` is outside the interval (0, 1), the function returns `na` as an error.

- The function uses binary search with a fixed number of iterations and a defined tolerance.

- The result is accurate to within the specified tolerance (default: 0.0001).

- Relies on the cumulative density function (CDF) `t_cdf` for the t-distribution.

Formula:

- Uses the cumulative density function (CDF) of the t-distribution to iteratively find the t-statistic.

Implementation details:

- `low` and `high` define the search interval for the t-statistic.

- The midpoint (`mid`) is iteratively refined until the difference between the cumulative probability

and the target p-value is smaller than the tolerance.

jarqueBera(n, s, k)

Parameters:

n (float) : (series float): Number of observations in the dataset.

s (float) : (series float): Skewness of the dataset.

k (float) : (series float): Kurtosis of the dataset.

Returns: (float): The Jarque-Bera test statistic.

Formula:

JB = n *

Notes:

- A higher JB value suggests that the data deviates more from a normal distribution.

- The test is asymptotically distributed as a chi-squared distribution with 2 degrees of freedom.

- Use this value to calculate a p-value to determine the significance of the result.

skewness(data)

Parameters:

data (float) : (series float): Input data series.

Returns: (float): The skewness value.

Notes:

- Handles missing values (`na`) by ignoring invalid points.

- Includes error handling for zero variance to avoid division-by-zero scenarios.

- Skewness is calculated as the normalized third central moment of the data.

kurtosis(data)

Parameters:

data (float) : (series float): Input data series.

Returns: (float): The kurtosis value.

Notes:

- Handles missing values (`na`) by ignoring invalid points.

- Includes error handling for zero variance to avoid division-by-zero scenarios.

- Kurtosis is calculated as the normalized fourth central moment of the data.

regression(y, x, lag)

Parameters:

y (float) : (series float): Dependent series (observed values).

x (float) : (series float): Independent series (explanatory variable).

lag (int) : (int): Number of lags applied to the independent series (x).

Returns: (tuple): Returns a tuple containing the following values:

- n: Number of valid observations.

- alpha: Intercept of the regression line.

- beta: Slope of the regression line.

- t_stat: T-statistic for the beta coefficient.

- p_value: Two-tailed p-value for the beta coefficient.

- r_squared: Coefficient of determination (R²) indicating goodness of fit.

- skew: Skewness of the residuals.

- kurt: Kurtosis of the residuals.

Notes:

- Handles missing data (`na`) by ignoring invalid points.

- Includes basic error handling for zero variance and division-by-zero scenarios.

- Computes residual-based statistics (skewness and kurtosis) for model diagnostics.

Correlation Confluence Trend IndicatorCorrelation Confluence Trend Indicator

Overview

The Correlation Confluence Trend Indicator combines exponential moving averages (EMAs) and statistical correlation measures to identify high-confidence trend alignments between an asset and a benchmark. By filtering signals through correlation strength, this indicator highlights opportunities when the asset and benchmark move together. In other words, it defines a trend and then uses correlation strength and the trend of a second asset to identify high-confidence trends.

Key Features

Dual EMA Trend Analysis :

Calculates fast and slow EMAs for both the asset and the selected benchmark (e.g., SPY) to identify bullish and bearish trends.

Correlation Strength Filtering :

Evaluates correlation between the asset and benchmark, identifying stronger-than-average relationships based on the mean and standard deviation.

Background Color Coding :

- Green : Strong correlation, both asset and benchmark bullish.

- Aqua : Weak correlation, both asset and benchmark bullish.

- Red : Strong correlation, both asset and benchmark bearish.

- Fuchsia : Weak correlation, both asset and benchmark bearish.

- Orange : Strong correlation, benchmark bullish, asset bearish.

- Yellow : Weak correlation, benchmark bullish, asset bearish.

- Purple : Strong correlation, benchmark bearish, asset bullish.

- Lime : Weak correlation, benchmark bearish, asset bullish.

Visual Trend Indicators :

Plots fast and slow EMAs for the asset, dynamically colored based on aggregate trend signals. The color of this corresponds to the main trend signal.

Inputs

Benchmark Symbol : Symbol of the benchmark asset to compare against.

Fast EMA Length : Period for the fast EMA calculation.

Slow EMA Length : Period for the slow EMA calculation.

Correlation Length : Number of bars for correlation calculation.

Correlation Mean Length : Number of bars for mean and standard deviation calculation.

Std Dev Multiplier : Multiplier for standard deviation to define correlation strength. When the correlation is Std Dev Multiplier standard deviations above the mean, it counts as a strong correlation.

Set Background Color : Toggle background coloring on or off.

Notes

This indicator is primarily designed for trend-following strategies. By combining trend analysis and correlation filtering, it ensures that signals occur during aligned market conditions, reducing false signals.

Before incorporating this indicator into your trading strategy:

Always backtest on historical data to evaluate its performance before committing capital.

Use proper risk management to control position sizes and mitigate potential losses.

Remember that no indicator guarantees success. I'm quite proud of this one, but it's not the holy grail.

GaussianDistributionLibrary "GaussianDistribution"

This library defines a custom type `distr` representing a Gaussian (or other statistical) distribution.

It provides methods to calculate key statistical moments and scores, including mean, median, mode, standard deviation, variance, skewness, kurtosis, and Z-scores.

This library is useful for analyzing probability distributions in financial data.

Disclaimer:

I am not a mathematician, but I have implemented this library to the best of my understanding and capacity. Please be indulgent as I tried to translate statistical concepts into code as accurately as possible. Feedback, suggestions, and corrections are welcome to improve the reliability and robustness of this library.

mean(source, length)

Calculate the mean (average) of the distribution

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

Returns: Mean (μ)

stdev(source, length)

Calculate the standard deviation (σ) of the distribution

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

Returns: Standard deviation (σ)

skewness(source, length, mean, stdev)

Calculate the skewness (γ₁) of the distribution

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

mean (float) : the mean (average) of the distribution

stdev (float) : the standard deviation (σ) of the distribution

@return Skewness (γ₁)

skewness(source, length)

Overloaded skewness to calculate from source and length

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

@return Skewness (γ₁)

mode(mean, stdev, skewness)

Estimate mode - Most frequent value in the distribution (approximation based on skewness)

Parameters:

mean (float) : the mean (average) of the distribution

stdev (float) : the standard deviation (σ) of the distribution

skewness (float) : the skewness (γ₁) of the distribution

@return Mode

mode(source, length)

Overloaded mode to calculate from source and length

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

@return Mode

median(mean, stdev, skewness)

Estimate median - Middle value of the distribution (approximation)

Parameters:

mean (float) : the mean (average) of the distribution

stdev (float) : the standard deviation (σ) of the distribution

skewness (float) : the skewness (γ₁) of the distribution

@return Median

median(source, length)

Overloaded median to calculate from source and length

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

@return Median

variance(stdev)

Calculate variance (σ²) - Square of the standard deviation

Parameters:

stdev (float) : the standard deviation (σ) of the distribution

@return Variance (σ²)

variance(source, length)

Overloaded variance to calculate from source and length

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

@return Variance (σ²)

kurtosis(source, length, mean, stdev)

Calculate kurtosis (γ₂) - Degree of "tailedness" in the distribution

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

mean (float) : the mean (average) of the distribution

stdev (float) : the standard deviation (σ) of the distribution

@return Kurtosis (γ₂)

kurtosis(source, length)

Overloaded kurtosis to calculate from source and length

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

@return Kurtosis (γ₂)

normal_score(source, mean, stdev)

Calculate Z-score (standard score) assuming a normal distribution

Parameters:

source (float) : Distribution source (typically a price or indicator series)

mean (float) : the mean (average) of the distribution

stdev (float) : the standard deviation (σ) of the distribution

@return Z-Score

normal_score(source, length)

Overloaded normal_score to calculate from source and length

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

@return Z-Score

non_normal_score(source, mean, stdev, skewness, kurtosis)

Calculate adjusted Z-score considering skewness and kurtosis

Parameters:

source (float) : Distribution source (typically a price or indicator series)

mean (float) : the mean (average) of the distribution

stdev (float) : the standard deviation (σ) of the distribution

skewness (float) : the skewness (γ₁) of the distribution

kurtosis (float) : the "tailedness" in the distribution

@return Z-Score

non_normal_score(source, length)

Overloaded non_normal_score to calculate from source and length

Parameters:

source (float) : Distribution source (typically a price or indicator series)

length (int) : Window length for the distribution (must be >= 30 for meaningful statistics)

@return Z-Score

method init(this)

Initialize all statistical fields of the `distr` type

Namespace types: distr

Parameters:

this (distr)

method init(this, source, length)

Overloaded initializer to set source and length

Namespace types: distr

Parameters:

this (distr)

source (float)

length (int)

distr

Custom type to represent a Gaussian distribution

Fields:

source (series float) : Distribution source (typically a price or indicator series)

length (series int) : Window length for the distribution (must be >= 30 for meaningful statistics)

mode (series float) : Most frequent value in the distribution

median (series float) : Middle value separating the greater and lesser halves of the distribution

mean (series float) : μ (1st central moment) - Average of the distribution

stdev (series float) : σ or standard deviation (square root of the variance) - Measure of dispersion

variance (series float) : σ² (2nd central moment) - Squared standard deviation

skewness (series float) : γ₁ (3rd central moment) - Asymmetry of the distribution

kurtosis (series float) : γ₂ (4th central moment) - Degree of "tailedness" relative to a normal distribution

normal_score (series float) : Z-score assuming normal distribution

non_normal_score (series float) : Adjusted Z-score considering skewness and kurtosis

MACD -- Normalized█ OVERVIEW

This indicator is a normalized and scaled version of the Moving Average Convergence Divergence ( MACD ) indicator, inspired by the work in "Statistically Sound Indicators" by Timothy Masters. It enhances the traditional MACD by applying statistical normalization and scaling techniques, providing more consistent and reliable signals across different markets and timeframes.

█ CONCEPTS

The traditional MACD measures the difference between two Exponential Moving Averages ( EMAs ) of different lengths to identify momentum changes. However, its raw values are unbounded, making it challenging to compare across different instruments or timeframes.

This normalized MACD addresses this limitation by:

• Normalization : Adjusting the MACD values using the Average True Range ( ATR ) to account for market volatility.

• Scaling : Applying the Cumulative Distribution Function ( CDF ) to constrain the output between -50 and +50.

• Smoothing : Providing a smoothed signal line and histogram to effectively visualize momentum shifts.

█ FEATURES

• Normalized MACD Line : Computes the difference between the short-term and long-term EMAs, normalized by market volatility.

• Signal Line : Applies EMA smoothing to the normalized MACD line over a user-defined period.

• Histogram : Visualizes the difference between the normalized MACD line and the signal line, highlighting momentum changes.

• Customization Options :

• Adjustable lengths for the short-term EMA, long-term EMA, and signal line smoothing.

• Ability to toggle the visibility of the MACD line, signal line, and histogram.

• Statistical Scaling : Utilizes statistical methods from Timothy Masters' work to provide consistent scaling across different instruments.

█ HOW TO USE

1 — Identify Momentum Shifts :

• A crossover of the MACD line above the signal line may indicate a bullish momentum shift.

• A crossover of the MACD line below the signal line may indicate a bearish momentum shift.

2 — Analyze the Histogram :

• A rising histogram suggests strengthening momentum in the current trend direction.

• A falling histogram may signal weakening momentum or a potential reversal.

3 — Customize Parameters :

• Adjust the EMA lengths and smoothing periods to fit the specific instrument or timeframe.

• Use the visibility toggles to focus on the components most relevant to your analysis.

4 — Combine with Other Tools :

• Use in conjunction with support/resistance levels, trend lines, or other indicators to confirm signals.

• Consider the overall market context to enhance decision-making.

█ LIMITATIONS

• The indicator is based on historical price data; it may not predict future market movements accurately.

• May produce false signals during low volatility or ranging market conditions.

• Initial periods may display na values due to insufficient data for calculations.

█ NOTES

• Ensure that the MathHelpers library by HuntGatherTrade is imported for the indicator to function correctly.

• The default parameters are commonly used settings but may require adjustments based on the trading instrument and timeframe.

• The normalization and scaling techniques are designed to make the indicator's outputs more comparable across different markets.

Close Minus Moving Average█ OVERVIEW

The Close Minus Moving Average (CMMA) is a statistically robust mean reversion indicator designed to identify potential reversal points in the market. By analyzing the relationship between the closing price and its moving average, CMMA provides traders with actionable insights to enhance their trading strategies.

Important

This indicator requires the use of the MathHelpers library published by HuntGatherTrade

█ CONCEPTS

The CMMA indicator operates by calculating the logarithmic difference between the current closing price and its simple moving average (SMA). This difference is then normalized using the Average True Range (ATR) to account for market volatility. The resulting value is transformed using the Cumulative Distribution Function (CDF) to produce a standardized metric that oscillates around zero.

Key Steps :

Logarithmic Calculation: Computes the natural logarithm of the closing prices.

Moving Average: Applies a simple moving average to the logarithmic closing prices.

ATR Normalization: Utilizes ATR to normalize the difference, ensuring the indicator adapts to varying market conditions.

CDF Transformation: Transforms the normalized difference to a scale that highlights mean reversion tendencies.

Mean Reversion

Mean reversion is a financial theory suggesting that asset prices and historical returns eventually return to the long-term mean or average level of the entire dataset. The CMMA leverages this concept to signal potential entry and exit points based on deviations from the moving average.

█ FEATURES

Adaptive Normalization: Utilizes ATR to adjust for market volatility, ensuring consistent performance across different market conditions.

Statistical Robustness: Built upon methodologies from Timothy Masters, ensuring reliable mean reversion signals.

Clear Visuals: Differentiates positive and negative deviations with distinct color coding for easy interpretation.

Customizable Parameters: Allows users to adjust lookback periods and ATR lengths to tailor the indicator to their specific trading needs

.

█ HOW TO USE

Add the Indicator :

Navigate to the Pine Script editor on TradingView.

Paste the CMMA script and add it to your chart.

Adjust Parameters :

Lookback Period: Determines the number of periods for calculating the moving average of the logarithmic close. Default is 1.

ATR Length: Sets the number of periods for ATR calculation. Default is 252.

Interpret Signals :

Green Plot: Indicates that the closing price is above the moving average, suggesting bullish momentum.

Red Plot: Indicates that the closing price is below the moving average, suggesting bearish momentum.

Zero Line: Serves as a reference point for mean reversion signals.

Trading Strategy :

Buy Signal: When CMMA crosses above the zero line, indicating a potential upward reversal.

Sell Signal: When CMMA crosses below the zero line, indicating a potential downward reversal.

█ LIMITATIONS

Lagging Indicator: As with all moving averages, CMMA is based on historical data and may lag during rapid market movements.

Parameter Sensitivity: The effectiveness of CMMA can vary based on the chosen lookback and ATR periods. Users should optimize these parameters based on the specific asset and timeframe.

Market Conditions: Best suited for mean-reverting markets and may underperform in trending or highly volatile environments.

█ NOTES

Version Compatibility: The CMMA script is written in Pine Script™ version 6. Ensure your TradingView environment supports this version.

License: This Pine Script™ code is subject to the terms of the Mozilla Public License 2.0. Read the license here.

MathHelpersLibrary "MathHelpers"

Overview

A collection of helper functions for designing indicators and strategies.

calculateATR(length, log)

Calculates the Average True Range (ATR) or Log ATR based on the 'log' parameter. Sans Wilder's Smoothing

Parameters:

length (simple int)

log (simple bool)

Returns: float The calculated ATR value. Returns Log ATR if `log` is true, otherwise returns standard ATR.

CDF(z)

Computes the Cumulative Distribution Function (CDF) for a given value 'z', mimicking the CDF function in "Statistically Sound Indicators" by Timothy Masters.

Parameters:

z (simple float)

Returns: float The CDF value corresponding to the input `z`, ranging between 0 and 1.

logReturns(lookback)

Calculates the logarithmic returns over a specified lookback period.

Parameters:

lookback (simple int)

Returns: float The calculated logarithmic return. Returns `na` if insufficient data is available.

Global Index Spread RSI StrategyThis strategy leverages the relative strength index (RSI) to monitor the price spread between a global benchmark index (such as AMEX) and the currently opened asset in the chart window. By calculating the spread between these two, the strategy uses RSI to identify oversold and overbought conditions to trigger buy and sell signals.

Key Components:

Global Benchmark Index: The strategy compares the current asset with a predefined global index (e.g., AMEX) to measure relative performance. The choice of a global benchmark allows the trader to analyze the current asset's movement in the context of broader market trends.

Spread Calculation:

The spread is calculated as the percentage difference between the current asset's closing price and the global benchmark index's closing price:

Spread=Current Asset Close−Global Index CloseGlobal Index Close×100

Spread=Global Index CloseCurrent Asset Close−Global Index Close×100

This metric provides a measure of how the current asset is performing relative to the global index. A positive spread indicates the asset is outperforming the benchmark, while a negative spread signals underperformance.

RSI of the Spread: The RSI is then calculated on the spread values. The RSI is a momentum oscillator that ranges from 0 to 100 and is commonly used to identify overbought or oversold conditions in asset prices. An RSI below 30 is considered oversold, indicating a potential buying opportunity, while an RSI above 70 is overbought, suggesting that the asset may be due for a pullback.

Strategy Logic:

Entry Condition: The strategy enters a long position when the RSI of the spread falls below the oversold threshold (default 30). This suggests that the asset may have been oversold relative to the global benchmark and might be due for a reversal.

Exit Condition: The strategy exits the long position when the RSI of the spread rises above the overbought threshold (default 70), indicating that the asset may have become overbought and a price correction is likely.

Visual Reference:

The RSI of the spread is plotted on the chart for visual reference, making it easier for traders to monitor the relative strength of the asset in relation to the global benchmark.

Overbought and oversold levels are also drawn as horizontal reference lines (70 and 30), along with a neutral level at 50 to show market equilibrium.

Theoretical Basis:

The strategy is built on the mean reversion principle, which suggests that asset prices tend to revert to a long-term average over time. When prices move too far from this mean—either being overbought or oversold—they are likely to correct back toward equilibrium. By using RSI to identify these extremes, the strategy aims to profit from price reversals.

Mean Reversion: According to financial theory, asset prices oscillate around a long-term average, and any extreme deviation (overbought or oversold conditions) presents opportunities for price corrections (Poterba & Summers, 1988).

Momentum Indicators (RSI): The RSI is widely used in technical analysis to measure the momentum of an asset. Its application to the spread between the asset and a global benchmark allows for a more nuanced view of relative performance and potential turning points in the asset's price trajectory.

Practical Application:

This strategy works best in markets where relative strength is a key factor in decision-making, such as in equity indices, commodities, or forex markets. By assessing the performance of the asset relative to a global benchmark and utilizing RSI to identify extremes in price movements, the strategy helps traders to make more informed decisions based on potential mean reversion points.

While the "Global Index Spread RSI Strategy" offers a method for identifying potential price reversals based on relative strength and oversold/overbought conditions, it is important to recognize that no strategy is foolproof. The strategy assumes that the historical relationship between the asset and the global benchmark will hold in the future, but financial markets are subject to a wide array of unpredictable factors that can lead to sudden changes in price behavior.

Risk of False Signals:

The strategy relies heavily on the RSI to trigger buy and sell signals. However, like any momentum-based indicator, RSI can generate false signals, particularly in highly volatile or trending markets. In such conditions, the strategy may enter positions too early or exit too late, leading to potential losses.

Market Context:

The strategy may not account for macroeconomic events, news, or other market forces that could cause sudden shifts in asset prices. External factors, such as geopolitical developments, monetary policy changes, or financial crises, can cause a divergence between the asset and the global benchmark, leading to incorrect conclusions from the strategy.

Overfitting Risk:

As with any strategy that uses historical data to make decisions, there is a risk of overfitting the model to past performance. This could result in a strategy that works well on historical data but performs poorly in live trading conditions due to changes in market dynamics.

Execution Risks:

The strategy does not account for slippage, transaction costs, or liquidity issues, which can impact the execution of trades in real-market conditions. In fast-moving markets, prices may move significantly between order placement and execution, leading to worse-than-expected entry or exit prices.

No Guarantee of Profit:

Past performance is not necessarily indicative of future results. The strategy should be used with caution, and risk management techniques (such as stop losses and position sizing) should always be implemented to protect against significant losses.

Traders should thoroughly test and adapt the strategy in a simulated environment before applying it to live trades, and consider seeking professional advice to ensure that their trading activities align with their risk tolerance and financial goals.

References:

Poterba, J. M., & Summers, L. H. (1988). Mean Reversion in Stock Prices: Evidence and Implications. Journal of Financial Economics, 22(1), 27-59.