PE BandThe PE Band shows the highest and lowest P/E in the previous period with TTM EPS. If the current P/E is lower than the minimum P/E, it is considered cheap. In other words, higher than the maximum P/E is considered expensive.

PE Band consists of 2 lines.

- Firstly, the historical P/E value in "green" (if TTM EPS is positive) or "red" (if TTM EPS is negative) states will change according to the latest high or low price of TTM EPS, such as: :

After the second quarter of 2023 (end of June), how do prices from 1 July – 30 September reflect net profits? The program will get the highest and lowest prices during that time.

After the 3rd quarter of 2023 (end of September), how do prices from 1 Oct. - 31 Dec. reflect net profits? The program will get the highest and lowest prices during that time.

- Second, the blue line is the closing price divided by TTM EPS, which shows the current P/E.

Statistics

Volatility DashboardThis indicator calculates and displays volatility metrics for a specified number of bars (rolling window) on a TradingView chart. It can be customized to display information in English or Thai and can position the dashboard at various locations on the chart.

Inputs

Language: Users can choose between English ("ENG") and Thai ("TH") for the dashboard's language.

Dashboard Position: Users can specify where the dashboard should appear on the chart. Options include various positions such as "Bottom Right", "Top Center", etc.

Calculation Method: Currently, the script supports "High-Low" for volatility calculation. This method calculates the difference between the highest and lowest prices within a specified timeframe.

Bars: Number of bars used to calculate the volatility.

Display Logic

Fills the islast_vol_points array with the calculated volatility points.

Sets the table cells with headers and corresponding values:

=> Highest Volatility: The maximum value in the islast_vol_points array

=> Mean Volatility: The average value in the islast_vol_points array,

=> Lowest Volatility: The minimum value in the islast_vol_points array, Number of Bars: The rolling window size.

Bull Market Drawdowns V1.0 [ADRIDEM]Bull Market Drawdowns V1.0

Overview

The Bull Market Drawdowns V1.0 script is designed to help visualize and analyze drawdowns during a bull market. This script calculates the highest high price from a specified start date, identifies drawdown periods, and plots the drawdown areas on the chart. It also highlights the maximum drawdowns and marks the start of the bull market, providing a clear visual representation of market performance and potential risk periods.

Unique Features of the New Script

Default Timeframe Configuration: Allows users to set a default timeframe for analysis, providing flexibility in adapting the script to different trading strategies and market conditions.

Customizable Bull Market Start Date: Users can define the start date of the bull market, ensuring the script calculates drawdowns from a specific point in time that aligns with their analysis.

Drawdown Calculation and Visualization: Calculates drawdowns from the highest high since the bull market start date and plots the drawdown areas on the chart with distinct color fills for easy identification.

Maximum Drawdown Tracking and Labeling: Tracks the maximum drawdown for each period and places labels on the chart to indicate significant drawdowns, helping traders identify and assess periods of higher risk.

Bull Market Start Marker: Marks the start of the bull market on the chart with a label, providing a clear reference point for the beginning of the analysis period.

Originality and Usefulness

This script provides a unique and valuable tool by combining drawdown analysis with visual markers and customizable settings. By calculating and plotting drawdowns from a user-defined start date, traders can better understand the performance and risks associated with a bull market. The script’s ability to track and label maximum drawdowns adds further depth to the analysis, making it easier to identify critical periods of market retracement.

Signal Description

The script includes several key visual elements that enhance its usefulness for traders:

Drawdown Area : Plots the upper and lower boundaries of the drawdown area, filling the space between with a semi-transparent color. This helps traders easily identify periods of market retracement.

Maximum Drawdown Labels : Labels are placed on the chart to indicate the maximum drawdown for each period, providing clear markers for significant drawdowns.

Bull Market Start Marker : A label is placed at the start of the bull market, marking the beginning of the analysis period and helping traders contextualize the drawdown data.

These visual elements help quickly assess the extent and impact of drawdowns within a bull market, aiding in risk management and decision-making.

Detailed Description

Input Variables

Default Timeframe (`default_timeframe`) : Defines the timeframe for the analysis. Default is 720 minutes

Bull Market Start Date (`start_date_input`) : The starting date for the bull market analysis. Default is January 1, 2023

Functionality

Highest High Calculation : The script calculates the highest high price on the specified timeframe from the user-defined start date.

```pine

var float highest_high = na

if (time >= start_date)

highest_high := na(highest_high ) ? high : math.max(highest_high , high)

```

Drawdown Calculation : Determines the drawdown starting point and calculates the drawdown percentage from the highest high.

```pine

var float drawdown_start = na

if (time >= start_date)

drawdown_start := na(drawdown_start ) or high >= highest_high ? high : drawdown_start

drawdown = (drawdown_start - low) / drawdown_start * 100

```

Maximum Drawdown Tracking : Tracks the maximum drawdown for each period and places labels above the highest high when a new high is reached.

```pine

var float max_drawdown = na

var int max_drawdown_bar_index = na

if (time >= start_date)

if na(max_drawdown ) or high >= highest_high

if not na(max_drawdown ) and not na(max_drawdown_bar_index) and max_drawdown > 10

label.new(x=max_drawdown_bar_index, y=drawdown_start , text="Max -" + str.tostring(max_drawdown , "#") + "%",

color=color.red, style=label.style_label_down, textcolor=color.white, size=size.normal)

max_drawdown := 0

max_drawdown_bar_index := na

else

if na(max_drawdown ) or drawdown > max_drawdown

max_drawdown := drawdown

max_drawdown_bar_index := bar_index

```

Drawdown Area Plotting : Plots the drawdown area with upper and lower boundaries and fills the area with a semi-transparent color.

```pine

drawdown_area_upper = time >= start_date ? drawdown_start : na

drawdown_area_lower = time >= start_date ? low : na

p1 = plot(drawdown_area_upper, title="Drawdown Area Upper", color=color.rgb(255, 82, 82, 60), linewidth=1)

p2 = plot(drawdown_area_lower, title="Drawdown Area Lower", color=color.rgb(255, 82, 82, 100), linewidth=1)

fill(p1, p2, color=color.new(color.red, 90), title="Drawdown Fill")

```

Current Maximum Drawdown Label : Places a label on the chart to indicate the current maximum drawdown if it exceeds 10%.

```pine

var label current_max_drawdown_label = na

if (not na(max_drawdown) and max_drawdown > 10)

current_max_drawdown_label := label.new(x=bar_index, y=drawdown_start, text="Max -" + str.tostring(max_drawdown, "#") + "%",

color=color.red, style=label.style_label_down, textcolor=color.white, size=size.normal)

if (not na(current_max_drawdown_label))

label.delete(current_max_drawdown_label )

```

Bull Market Start Marker : Places a label at the start of the bull market to mark the beginning of the analysis period.

```pine

var label bull_market_start_label = na

if (time >= start_date and na(bull_market_start_label))

bull_market_start_label := label.new(x=bar_index, y=high, text="Bull Market Start", color=color.blue, style=label.style_label_up, textcolor=color.white, size=size.normal)

```

How to Use

Configuring Inputs : Adjust the default timeframe and start date for the bull market as needed. This allows the script to be tailored to different market conditions and trading strategies.

Interpreting the Indicator : Use the drawdown areas and labels to identify periods of significant market retracement. Pay attention to the maximum drawdown labels to assess the risk during these periods.

Signal Confirmation : Use the bull market start marker to contextualize drawdown data within the overall market trend. The combination of drawdown visualization and maximum drawdown labels helps in making informed trading decisions.

This script provides a detailed view of drawdowns during a bull market, helping traders make more informed decisions by understanding the extent and impact of market retracements. By combining customizable settings with visual markers and drawdown analysis, traders can better align their strategies with the underlying market conditions, thus improving their risk management and decision-making processes.

signalLib_yashgode9Signal Generation Library = "signalLib_yashgode9"

This library, named "signalLib_yashgode9", is designed to generate buy and sell signals based on the price action of a financial instrument. It utilizes various technical indicators and parameters to determine the market direction and provide actionable signals for traders.

Key Features:-

1.Trend Direction Identification: The library calculates the trend direction by comparing the number of bars since the highest and lowest prices within a specified depth. This allows the library to determine the overall market direction, whether it's bullish or bearish.

2.Dynamic Price Tracking: The library maintains two chart points, zee1 and zee2, which dynamically track the price levels based on the identified market direction. These points serve as reference levels for generating buy and sell signals.

3.Customizable Parameters: The library allows users to adjust several parameters, including the depth of the price analysis, the deviation threshold, and the number of bars to consider for the trend direction. This flexibility enables users to fine-tune the library's behavior to suit their trading strategies.

4.Visual Representation: The library provides a visual representation of the buy and sell signals by drawing a line between the zee1 and zee2 chart points. The line's color changes based on the identified market direction, with red indicating a bearish signal and green indicating a bullish signal.

Usage and Integration:

To use this library, you can call the "signalLib_yashgode9" function and pass in the necessary parameters, such as the lower and higher prices, the depth of the analysis, the deviation threshold, and the number of bars to consider for the trend direction. The function will return the direction of the market (1 for bullish, -1 for bearish), as well as the zee1 and zee2 chart points.You can then use these values to generate buy and sell signals in your trading strategy. For example, you could use the direction value to determine when to enter or exit a trade, and the zee1 and zee2 chart points to set stop-loss or take-profit levels.

Potential Use Cases:

This library can be particularly useful for traders who:

1.Trend-following Strategies: The library's ability to identify the market direction can be beneficial for traders who employ trend-following strategies, as it can help them identify the dominant trend and time their entries and exits accordingly.

2.Swing Trading: The dynamic price tracking provided by the zee1 and zee2 chart points can be useful for swing traders, who aim to capture medium-term price movements.

3.Automated Trading Systems: The library's functionality can be integrated into automated trading systems, allowing for the development of more sophisticated and rule-based trading strategies.

4.Educational Purposes: The library can also be used for educational purposes, as it provides a clear and concise way to demonstrate the application of technical analysis concepts in a trading context.

Important Notice:- This library effectively work on timeframe of 5-minute and 15-minute.

Vwap Z-Score with Signals [UAlgo]The "VWAP Z-Score with Signals " is a technical analysis tool designed to help traders identify potential buy and sell signals based on the Volume Weighted Average Price (VWAP) and its Z-Score. This indicator calculates the VWAP Z-Score to show how far the current price deviates from the VWAP in terms of standard deviations. It highlights overbought and oversold conditions with visual signals, aiding in the identification of potential market reversals. The tool is customizable, allowing users to adjust parameters for their specific trading needs.

🔶 Features

VWAP Z-Score Calculation: Measures the deviation of the current price from the VWAP using standard deviations.

Customizable Parameters: Allows users to set the length of the VWAP Z-Score calculation and define thresholds for overbought and oversold levels.

Reversal Signals: Provides visual signals when the Z-Score crosses the specified thresholds, indicating potential buy or sell opportunities.

🔶 Usage

Extreme Z-Score values (both positive and negative) highlight significant deviations from the VWAP, useful for identifying potential reversal points.

The indicator provides visual signals when the Z-Score crosses predefined thresholds:

A buy signal (🔼) appears when the Z-Score crosses above the lower threshold, suggesting the price may be oversold and a potential upward reversal.

A sell signal (🔽) appears when the Z-Score crosses below the upper threshold, suggesting the price may be overbought and a potential downward reversal.

These signals can help you identify potential entry and exit points in your trading strategy.

🔶 Disclaimer

The "VWAP Z-Score with Signals " indicator is designed for educational purposes and to assist traders in their technical analysis. It does not guarantee profitable trades and should not be considered as financial advice.

Users should conduct their own research and use this indicator in conjunction with other tools and strategies.

Trading involves significant risk, and it is possible to lose more than your initial investment.

Composite Risk IndicatorThe Composite Risk Indicator is a financial tool designed to assess market risk by analyzing the spreads between various asset classes. This indicator synthesizes information across six key spreads, normalizing each on a scale from 0 to 100 where higher values represent higher perceived risk. It provides a single, comprehensive measure of market sentiment and risk exposure.

Key Components of the CRI:

1. Stock Market to Bond Market Spread (SPY/BND): Measures the performance of stocks relative to bonds. Higher values indicate stronger stock performance compared to bonds, suggesting increased market optimism and higher risk.

2. Junk Bond to Treasury Bond Spread (HYG/GOVT): Assesses the performance of high-yield (riskier) bonds relative to government (safer) bonds. A higher ratio indicates increased appetite for risk.

3. Junk Bond to Investment Grade Bond Spread (HYG/LQD): Compares high-yield bonds to investment-grade corporate bonds. This ratio sheds light on the risk tolerance within the corporate bond market.

4. Growth to Value Spread (VUG/VTV): Evaluates the performance of growth stocks against value stocks. A higher value suggests a preference for growth stocks, often seen in risk-on environments.

5. Tech to Staples Spread (XLK/XLP): Measures the performance of technology stocks relative to consumer staples. This ratio highlights the market’s risk preference within equity sectors.

6. Small Cap Growth to Small Cap Value Spread (SLYG/SLYV): Compares small-cap growth stocks to small-cap value stocks, providing insight into risk levels in smaller companies.

Utility:

This indicator is particularly useful for investors and traders looking to gauge market sentiment, identify shifts in risk appetite, and make informed decisions based on a broad assessment of market conditions. The CRI can serve as a valuable addition to investment analysis and risk management strategies.

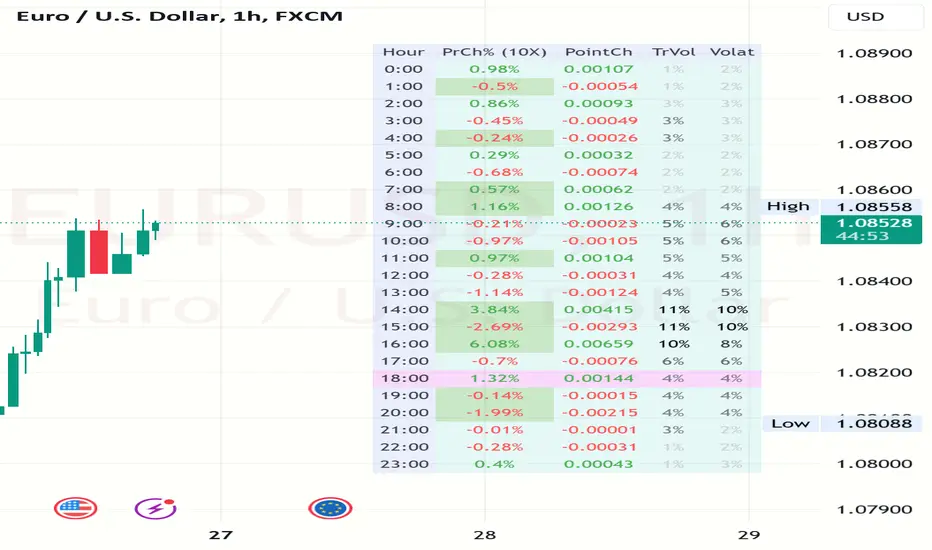

Volatility and Volume by Hour EXT(Extended republication, use this instead of the old one)

The goal of this indicator is to show a “characteristic” of the instrument, regarding the price change and trading volume. You can see how the instrument “behaved” throughout the day in the lookback period. I've found this useful for timing in day trading.

The indicator creates a table on the chart to display various statistics for each hour of the day.

Important: ONLY SHOWS THE TABLE IF THE CHART’S TIMEFRAME IS 1H!

Explanation of the columns:

1. Volatility Percentage (Volat): This column shows the volatility of the price as a percentage. For example, a value of "15%" means the price movement was 15% of the total daily price movement within the hour.

2. Hourly Point Change (PointCh): This column shows the change in price points for each hour in the lookback period. For example, a value of "5" means the price has increased by 5 points in the hour, while "-3" means it has decreased by 3 points.

3. Hourly Point Change Percentage (PrCh% (LeverageX)): This column shows the percentage change in price points for each hour, adjusted with leverage multiplier. Displayed green (+) or red (-) accordingly. For example, a value of "10%" with a leverage of 2X means the price has effectively changed by 5% due to the leverage.

4. Trading Volume Percentage (TrVol): This column shows the percentage of the daily total volume that was traded in a specific hour. For example, a value of "10%" would mean that 10% of the day's total trading volume occurred in that hour.

5. Added New! - Relevancy Check: The indicator checks the last 24 candle. If the direction of the price movement was the same in the last 24 hour as the statistical direction in that hour, the background of the relevant hour in the second column goes green.

For example: if today at 9 o'clock the price went lower, so as at 9 o'clock in the loopback period, the instrument "behaves" according to statistics . So the statistics is probably more relevant for today. The more green background row the more relevancy.

Settings:

1. Lookback period: The lookback period is the number of previous bars from which data is taken to perform calculations. In this script, it's used in a loop that iterates over a certain number of past bars to calculate the statistics. TIP: Select a period the contains a trend in one direction, because an upward and a downward trend compensate the price movement in opposite directions.

2. Timezone: This is a string input that represents the user's timezone. The default value is "UTC+2". Adjust it to your timezone in order to view the hours properly.

3. Leverage: The default value is 10(!). This input is used to adjust the hourly point change percentage. For FOREX traders (for example) the statistics can show the leveraged percentage of price change. Set that according the leverage you trade the instrument with.

Use at your own risk, provided “as is” basis!

Hope you find it useful! Cheers!

trend_switch

█ Description

Asset price data was time series data, commonly consisting of trends, seasonality, and noise. Many applicable indicators help traders to determine between trend or momentum to make a better trading decision based on their preferences. In some cases, there is little to no clear market direction, and price range. It feels much more appropriate to use a shorter trend identifier, until clearly defined market trend. The indicator/strategy developed with the notion aims to automatically switch between shorter and longer trend following indicator. There were many methods that can be applied and switched between, however in this indicator/strategy will be limited to the use of predictive moving average and MESA adaptive moving average (Ehlers), by first determining if there is a strong trend identified by calculating the slope, if slope value is between upper and lower threshold assumed there is not much price direction.

█ Formula

// predictive moving average

predict = (2*wma1-wma2)

trigger = (4*predict+3*predict +2*predict *predict)

// MESA adaptive moving average

mama = alpha*src+(1-alpha)*mama

fama = .5*alpha*mama+(1-.5-alpha)*fama

█ Feature

The indicator will have a specified default parameter of:

source = ohlc4

lookback period = 10

threshold = 10

fast limit = 0.5

slow limit = 0.05

Strategy type can be switched between Long/Short only and Long-Short strategy

Strategy backtest period

█ How it works

If slope between the upper (red) and lower (green) threshold line, assume there is little to no clear market direction, thus signal predictive moving average indicator

If slope is above the upper (red) or below the lower (green) threshold line, assume there is a clear trend forming, the signal generated from the MESA adaptive moving average indicator

█ Example 1 - Slope fall between the Threshold - activate shorter trend

█ Example 2 - Slope fall above/below Threshold - activate longer trend

Normalized Z-ScoreThe Normalized Z-Score indicator is designed to help traders identify overbought or oversold conditions in a security's price. This indicator can provide valuable signals for potential buy or sell opportunities by analyzing price deviations from their average values.

How It Works :

-- Z-Score Calculation:

---- The indicator calculates the Z-Score for both high and low prices over a user-defined period (default is 14 periods).

---- The Z-Score measures how far a price deviates from its average in terms of standard deviations.

-- Average Z-Score:

---- The average Z-Score is derived by taking the mean of the high and low Z-Scores.

-- Normalization:

---- The average Z-Score is then normalized to a range between -1 and 1. This helps in standardizing the indicator's values, making it easier to interpret.

-- Signal Line:

---- A signal line, which is the simple moving average (SMA) of the normalized Z-Score, is calculated to smooth out the data and highlight trends.

-- Color-Coding:

---- The signal line changes color based on its value: green when it is positive (indicating a potential buy signal) and red when it is negative (indicating a potential sell signal). This coloration is also used for the candle/bar coloration.

How to Use It:

-- Adding the Indicator:

---- Add the Normalized Z-Score indicator to your TradingView chart. It will appear in a separate pane below the price chart.

-- Interpreting the Histogram:

---- The histogram represents the normalized Z-Score. High positive values suggest overbought conditions, while low negative values suggest oversold conditions.

-- Using the Signal Line:

---- The signal line helps to confirm the conditions indicated by the histogram. A green signal line suggests a potential buying opportunity, while a red signal line suggests a potential selling opportunity.

-- Adjusting the Period:

---- You can adjust the period for the Z-Score calculation to suit your trading strategy. The default period is 14, but you can change this based on your preference.

Example Scenario:

-- Overbought Condition: If the histogram shows a high positive value and the signal line is green, the security may be overbought. This could indicate that it is a good time to consider selling.

-- Oversold Condition: If the histogram shows a low negative value and the signal line is red, the security may be oversold. This could indicate that it is a good time to consider buying.

By using the Normalized Z-Score indicator, traders can gain insights into price deviations and potential market reversals, aiding in making more informed trading decisions.

Alert Before Bar Closei.imgur.com

Alert Before Bar Close

==========================

Example Figure

Originality and usefulness

This indicator/alert mechanism is unique in two ways. First, it provides alerts before the close of a candlestick, allowing time-based traders to prepare early to determine if the market is about to form a setup. Second, it introduces an observation time mechanism, enabling time-based traders to observe when the market is active, thereby avoiding too many false signals during electronic trading or when trading is light.

Detail

Regarding the settings (Arrow 1). The first input is to select the candlestick period you want to observe. The second is to notify a few seconds in advance. The third input sets the observation time. For example, if you set "1,2,3,4,5," the alert mechanism will only be activated during the period from 01:00:00 to 05:59:59, consistent with the time zone you set in TradingView. Additionally, I have set it so that the alert will only trigger once per candlestick, so don't worry about repeated alerts.

The alert setup is very simple, too. Follow the steps (Arrow 2, 3) to complete the setup. I have tested several periods and successfully received alerts on both mobile and computer. If anyone encounters any issues, feel free to let me know.

Seasonality Widget [LuxAlgo]The Seasonality Widget tool allows users to easily visualize seasonal trends from various data sources.

Users can select different levels of granularity as well as different statistics to express seasonal trends.

🔶 USAGE

Seasonality allows us to observe general trends occurring at regular intervals. These intervals can be user-selected from the granularity setting and determine how the data is grouped, these include:

Hour

Day Of Week

Day Of Month

Month

Day Of Year

The above seasonal chart shows the BTCUSD seasonal price change for every hour of the day, that is the average price change taken for every specific hour. This allows us to obtain an estimate of the expected price move at specific hours of the day.

Users can select when data should start being collected using the "From Date" setting, any data before the selected date will not be included in the calculation of the Seasonality Widget.

🔹 Data To Analyze

The Seasonality Widget can return the seasonality for the following data:

Price Change

Closing price minus the previous closing price.

Price Change (%)

Closing price minus the previous closing price, divided by the

previous closing price, then multiplied by 100.

Price Change (Sign)

Sign of the price change (-1 for negative change, 1 for positive change), normalized in a range (0, 100). Values above 50 suggest more positive changes on average.

Range

High price minus low price.

Price - SMA

Price minus its simple moving average. Users can select the SMA period.

Volume

Amount of contracts traded. Allow users to see which periods are generally the most /least liquid.

Volume - SMA

Volume minus its simple moving average. Users can select the SMA period.

🔹 Filter

In addition to the "From Date" threshold users can exclude data from specific periods of time, potentially removing outliers in the final results.

The period type can be specified in the "Filter Granularity" setting. The exact time to exclude can then be specified in the "Numerical Filter Input" setting, multiple values are supported and should be comma separated.

For example, if we want to exclude the entire 2008 period we can simply select "Year" as filter granularity, then input 2008 in the "Numerical Filter Input" setting.

Do note that "Sunday" uses the value 1 as a day of the week.

🔶 DETAILS

🔹 Supported Statistics

Users can apply different statistics to the grouped data to process. These include:

Mean

Median

Max

Min

Max-Min Average

Using the median allows for obtaining a measure more robust to outliers and potentially more representative of the actual central tendency of the data.

Max and Min do not express a general tendency but allow obtaining information on the highest/lowest value of the analyzed data for specific periods.

🔶 SETTINGS

Granularity: Periods used to group data.

From Data: Starting point where data starts being collected

🔹 Data

Analyze: Specific data to be processed by the seasonality widget.

SMA Length: Period of the simple moving average used for "Price - SMA" and "Volume - SMA" options in "Analyze".

Statistic: Statistic applied to the grouped data.

🔹 Filter

Filter Granularity: Period type to exclude in the processed data.

Numerical Filter Input: Determines which of the selected hour/day of week/day of month/month/year to exclude depending on the selected Filter Granularity. Only numerical inputs can be provided. Multiple values are supported and must be comma-separated.

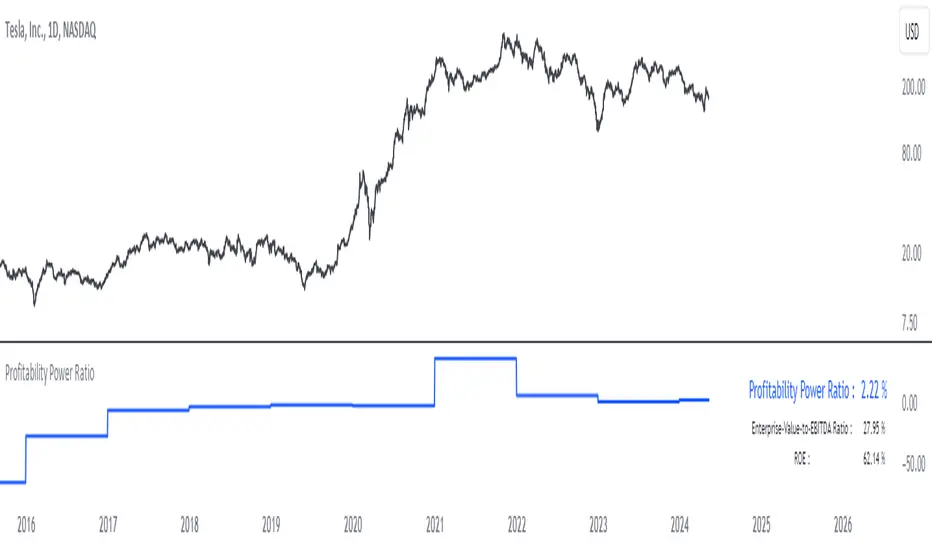

Profitability Power RatioProfitability Power Ratio

The Profitability Power Ratio is a financial metric designed to assess the efficiency of a company's operations by evaluating the relationship between its Enterprise Value (EV) and Return on Equity (ROE). This ratio provides insights into how effectively a company generates profits relative to its equity and overall valuation.

Qualities and Interpretations:

1. Efficiency Benchmark: The Profitability Power Ratio serves as a benchmark for evaluating how efficiently a company utilizes its equity capital to generate profits. A higher ratio indicates that the company is generating significant profits relative to its valuation, reflecting efficient use of invested capital.

2. Financial Health Indicator: This ratio can be used as an indicator of financial health. A consistently high or improving ratio over time suggests strong operational efficiency and sustainable profitability.

3. Investment Considerations: Investors can use this ratio to assess the attractiveness of an investment opportunity. A high ratio may signal potential for good returns, but it's important to consider the underlying reasons for the ratio's level to avoid misinterpretation.

4. Risk Evaluation: An excessively high Profitability Power Ratio could also signal elevated risk. It may indicate aggressive financial leveraging or unsustainable growth expectations, which could pose risks during economic downturns or market fluctuations.

Interpreting the Ratio:

1. Higher Ratio: A higher Profitability Power Ratio typically signifies efficient capital utilization and strong profitability relative to the company's valuation.

2. Lower Ratio: A lower ratio may suggest inefficiencies in capital allocation or lower profitability relative to enterprise value.

3. Benchmarking: Compare the company's ratio with industry peers and historical performance to gain deeper insights into its financial standing and operational efficiency.

Using the Indicator:

The Profitability Power Ratio is plotted on a chart to visualize trends and fluctuations over time. Users can customize the color of the plot to emphasize this metric and integrate it into their financial analysis toolkit for comprehensive decision-making.

Disclaimer: The Profitability Power Ratio is a financial metric designed for informational purposes only and should not be considered as financial or investment advice. Users should conduct thorough research and analysis before making any investment decisions based on this indicator. Past performance is not indicative of future results. All investments involve risks, and users are encouraged to consult with a qualified financial advisor or professional before making investment decisions.

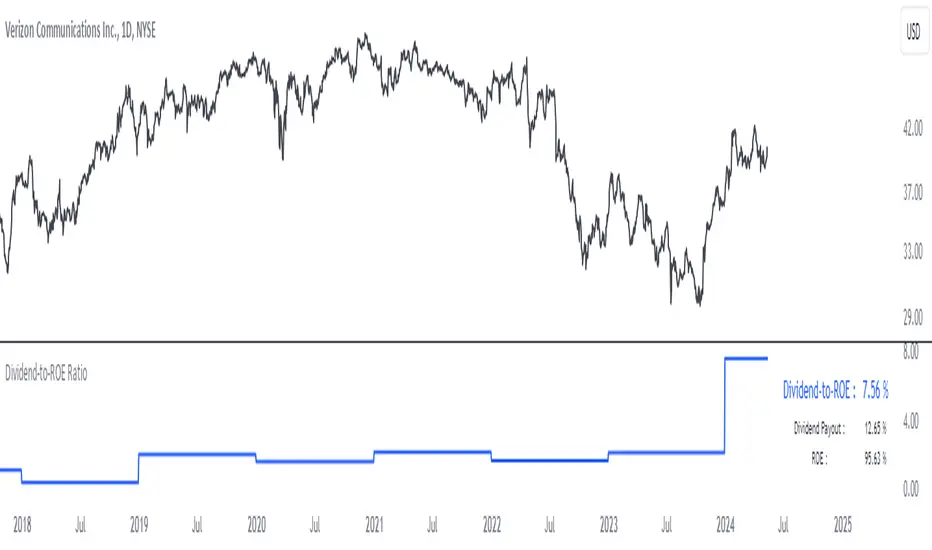

Dividend-to-ROE RatioDividend-to-ROE Ratio Indicator

The Dividend-to-ROE Ratio indicator offers valuable insights into a company's dividend distribution relative to its profitability, specifically comparing the Dividend Payout Ratio (proportion of earnings as dividends) to the Return on Equity (ROE), a measure of profitability from shareholder equity.

Interpretation:

1. Higher Ratio: A higher Dividend-to-ROE Ratio suggests a stable dividend policy, where a significant portion of earnings is returned to shareholders. This can indicate consistent dividend payments, often appealing to income-seeking investors.

2. Lower Ratio: Conversely, a lower ratio implies that the company retains more earnings for growth, potentially signaling a focus on reinvestment for future expansion rather than immediate dividend payouts.

3. Excessively High Ratio: An exceptionally high ratio may raise concerns. While it could reflect a generous dividend policy, excessively high ratios might indicate that a company is distributing more earnings than it can sustainably afford. This could potentially hinder the company's ability to reinvest in its operations, research, or navigate economic downturns effectively.

Utility and Applications:

The Dividend-to-ROE Ratio can be particularly useful in the following scenarios:

1. Income-Oriented Investors: For investors seeking consistent dividend income, a higher ratio signifies a company's commitment to distributing profits to shareholders, potentially aligning with income-oriented investment strategies.

2. Financial Health Assessment: Analysts and stakeholders can use this ratio to gauge a company's financial health and dividend sustainability. It provides insights into management's capital allocation decisions and strategic focus.

3. Comparative Analysis: When comparing companies within the same industry, this ratio helps in benchmarking dividend policies and identifying outliers with unusually high or low ratios.

Considerations:

1. Contextual Analysis: Interpretation should be contextualized within industry standards and the company's financial history. Comparing the ratio with peers in the same sector can provide meaningful insights.

2. Financial Health: It's crucial to evaluate this indicator alongside other financial metrics (like cash flow, debt levels, and profit margins) to grasp the company's overall financial health and sustainability of its dividend policy.

Disclaimer: This indicator is for informational purposes only and does not constitute financial advice. Investors should conduct thorough research and consult with financial professionals before making investment decisions based on this ratio.

Fourier Adjusted Average True Range [BackQuant]Fourier Adjusted Average True Range

1. Conceptual Foundation and Innovation

The FA-ATR leverages the principles of Fourier analysis to dissect market prices into their constituent cyclical components. By applying Fourier Transform to the price data, the FA-ATR captures the dominant cycles and trends which are often obscured in noisy market data. This integration allows the FA-ATR to adapt its readings based on underlying market dynamics, offering a refined view of volatility that is sensitive to both market direction and momentum.

2. Technical Composition and Calculation

The core of the FA-ATR involves calculating the traditional ATR, which measures market volatility by decomposing the entire range of price movements. The FA-ATR extends this by incorporating a Fourier Transform of price data to assess cyclical patterns over a user-defined period 'N'. This process synthesizes both the magnitude of price changes and their rhythmic occurrences, resulting in a more comprehensive volatility indicator.

Fourier Transform Application: The Fourier series is calculated using price data to identify the fundamental frequency of market movements. This frequency helps in adjusting the ATR to reflect more accurately the current market conditions.

Dynamic Adjustment: The ATR is then adjusted by the magnitude of the dominant cycle from the Fourier analysis, enhancing or reducing the ATR value based on the intensity and phase of market cycles.

3. Features and User Inputs

Customizability: Traders can modify the Fourier period, ATR period, and the multiplication factor to suit different trading styles and market environments.

Visualization : The FA-ATR can be plotted directly on the chart, providing a visual representation of volatility. Additionally, the option to paint candles according to the trend direction enhances the usability and interpretative ease of the indicator.

Confluence with Moving Averages: Optionally, a moving average of the FA-ATR can be displayed, serving as a confluence factor for confirming trends or potential reversals.

4. Practical Applications

The FA-ATR is particularly useful in markets characterized by periodic fluctuations or those that exhibit strong cyclical trends. Traders can utilize this indicator to:

Adjust Stop-Loss Orders: More accurately set stop-loss orders based on a volatility measure that accounts for cyclical market changes.

Trend Confirmation: Use the FA-ATR to confirm trend strength and sustainability, helping to avoid false signals often encountered in volatile markets.

Strategic Entry and Exit: The indicator's responsiveness to changing market dynamics makes it an excellent tool for planning entries and exits in a trend-following or a breakout trading strategy.

5. Advantages and Strategic Value

By integrating Fourier analysis, the FA-ATR provides a volatility measure that is both adaptive and anticipatory, giving traders a forward-looking tool that adjusts to changes before they become apparent through traditional indicators. This anticipatory feature makes it an invaluable asset for traders looking to gain an edge in fast-paced and rapidly changing market conditions.

6. Summary and Usage Tips

The Fourier Adjusted Average True Range is a cutting-edge development in technical analysis, offering traders an enhanced tool for assessing market volatility with increased accuracy and responsiveness. Its ability to adapt to the market's cyclical nature makes it particularly useful for those trading in highly volatile or cyclically influenced markets.

Traders are encouraged to integrate the FA-ATR into their trading systems as a supplementary tool to improve risk management and decision-making accuracy, thereby potentially increasing the effectiveness of their trading strategies.

INDEX:BTCUSD

INDEX:ETHUSD

BINANCE:SOLUSD

CAPEX RatioUnderstanding the CAPEX Ratio: An Essential Financial Metric

Introduction

In the world of finance, understanding how companies allocate their resources and reinvest their earnings is crucial for investors and analysts. One fundamental metric used to assess a company's investment behavior is the CAPEX Ratio. This article delves into what the CAPEX Ratio signifies, its advantages, and how to interpret its implications.

What is the CAPEX Ratio?

The CAPEX Ratio, short for Capital Expenditure Ratio, is a financial indicator that measures the proportion of a company's capital expenditures (CAPEX) relative to various financial metrics such as revenue, free cash flow, net income, or total assets. CAPEX represents investments made by a company to acquire or maintain its physical assets.

Interpreting the Results

Each variant of the CAPEX Ratio provides unique insights into a company's financial strategy:

• CAPEX to Revenue Ratio: This ratio shows what portion of a company's revenue is being reinvested into capital investments. A higher ratio might indicate aggressive expansion plans or a need for infrastructure upgrades.

• CAPEX to Free Cash Flow Ratio: By comparing CAPEX with free cash flow, this ratio reveals how much of a company's available cash is dedicated to capital investments. It helps assess financial health and sustainability.

• CAPEX to Net Income Ratio: This ratio measures how much of a company's net income is being channeled back into capital expenditures. A high ratio relative to net income could signal a company's commitment to growth and development.

• CAPEX to Total Assets Ratio: This metric assesses the proportion of total assets being allocated towards capital expenditures. It provides a perspective on the company's investment intensity relative to its overall asset base.

Advantages of Using CAPEX Ratios

• Insight into Investment Strategy: Helps investors understand where a company is directing its resources.

• Evaluation of Financial Health: Indicates how efficiently a company is reinvesting profits or available cash.

• Comparative Analysis: Enables comparisons across companies or industries to gauge investment priorities.

How to Use the CAPEX Ratio

• Comparative Analysis: Compare the CAPEX Ratios over time or against industry peers to spot trends or outliers.

• Investment Decision-Making: Consider CAPEX Ratios alongside other financial metrics when making investment decisions.

Conclusion

In conclusion, the CAPEX Ratio is a valuable financial metric that offers deep insights into a company's investment behavior and financial health. By analyzing different variants of this ratio, investors and analysts can make informed decisions about a company's growth prospects and financial stability.

Useful_lib_publicLibrary "Useful_lib_public"

Useful functions

CountBarsOfDay()

count bars for one for the diffrent time frames

Returns: number of bars for one day

LastBarsOfDay()

Index number for the las bar for one day

Returns: TRUE is that the last bar from day

isTuesday()

TRUE is tuesday

Returns: TRUE is tuesday else FALSE

Rsi(src, len)

RSI calulation

Parameters:

src (float) : RSI Source

len (simple int) : RSI Length

Returns: RSI Value

CalcIndex(netPos, weeks)

Index calulation

Parameters:

netPos (float) : Source

weeks (simple int) : Length

Returns: "COT Index"

RsiStock(src, len, smoothK)

TRUE is tuesday

Parameters:

src (float)

len (simple int)

smoothK (int)

Returns: RSI Stochastik

Offset()

Use Offset for Day time frame

Returns: Offset

PercentChange(Data, LastData)

Calc different in Percent

Parameters:

Data (float)

LastData (float)

Returns: Change in percent

Dynamic Date and Price Tracker with Entry PriceThe Dynamic Date and Price Tracker indicator is a simple tool designed for traders to visualize and monitor their trade's progress in real-time from a specified starting point.

This tool provides an intuitive graphical representation of your trade's profitability based on a custom entry date and price.

Features:

-Starting Date Selection: Choose a specific starting date, after which the indicator begins tracking your trade's performance.

-Custom Entry Price: Input a starting price to accurately reflect your actual entry price for performance tracking across different timeframes.

-Real-Time Tracking: As new bars form, the indicator automatically adjusts a dynamic line to the current closing price.

-Profit/Loss Color Coding: The dynamic line color changes based on whether the current price is above (green for profit) or below (red for loss) your specified entry price.

-Performance Label: A real-time label displays the absolute and percentage change in price since your initial entry, color-coded for positive (green) or negative (red) performance.

-Entry Price Line: The horizontal line marks your starting price for easy visual comparison.

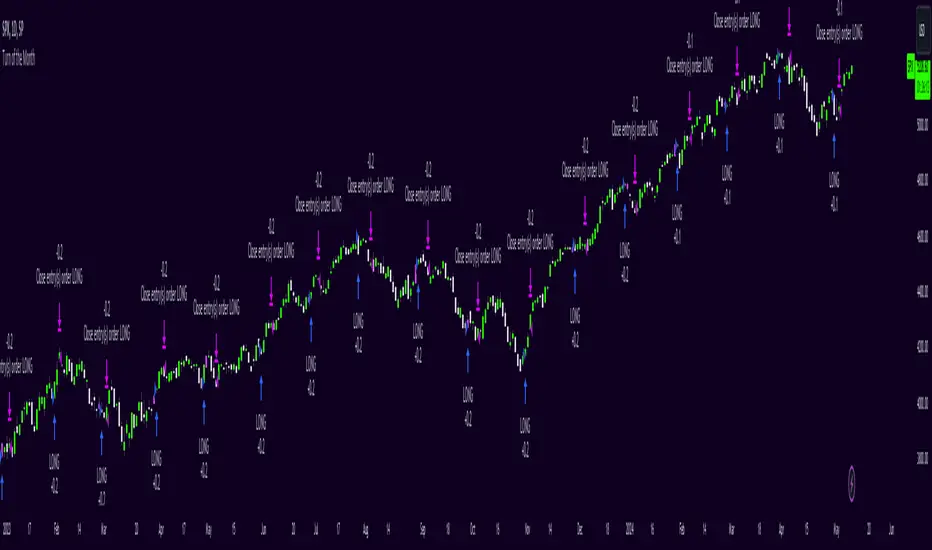

Turn of the Month Strategy [Honestcowboy]The end of month effect is a well known trading strategy in the stock market. Quite simply, most stocks go up at the end of the month. What's even better is that this effect spills over to the next phew days of the next month.

In this script we backtest this theory which should work especially well on SP500 pair.

By default the strategy buys 2 days before the end of each month and exits the position 3 days into the next month.

The strategy is a long only strategy and is extremely simple. The SP500 is one of the #1 assets people use for long term investing due to it's "9.8%" annualised return. However as a trader you want the best deal possible. This strategy is only inside the market for about 25% of the time while delivering a similar return per exposure with a lower drawdown.

Here are some hypothesis why turn of the month effect happens in the stock markets:

Increased inflow from savings accounts to stocks at end of month

Rebalancing of portfolios by fund managers at end of month

The timing of monthly cash flows received by pension funds, which are reinvested in the stock market.

The script also has some inputs to define how many days before end of the month you want to buy the asset and how long you want to hold it into the next month.

It is not possible to buy the asset exactly on this day every month as the market closes on the weekend. I've added some logic where it will check if that day is a friday, saturdady or sunday. If that is the case it will send the buy signal on the end of thursday, this way we enter on the friday and don't lose that months trading opportunity.

The backtest below uses 4% exposure per trade as to show the equity curve more clearly and because of publishing rules. However, most fund managers and investors use 100% exposure. This way you actually risk money to earn money. Feel free to adjust the settings to your risk profile to get a clearer picture of risks and rewards before implementing in your portfolio.

strategy_helpersThis library is designed to aid traders and developers in calculating risk metrics efficiently across different asset types like equities, futures, and forex. It includes comprehensive functions that calculate the number of units or contracts to trade, the value at risk, and the total value of the position based on provided entry prices, stop levels, and risk percentages. Whether you're managing a portfolio or developing trading strategies, this library provides essential tools for risk management. Functions also automatically select the appropriate risk calculation method based on asset type, calculate leverage levels, and determine potential liquidation points for leveraged positions. Perfect for enhancing the precision and effectiveness of your trading strategies.

Library "strategy_helpers"

Provides tools for calculating risk metrics across different types of trading strategies including equities, futures, and forex. Functions allow for precise control over risk management by calculating the number of units or contracts to trade, the value at risk, and the total position value based on entry prices, stop levels, and desired risk percentage. Additional utilities include automatic risk calculation based on asset type, leverage level calculations, and determination of liquidation levels for leveraged trades.

calculate_risk(entry, stop_level, stop_range, capital, risk_percent, trade_direction, whole_number_buy)

Calculates risk metrics for equity trades based on entry, stop level, and risk percent

Parameters:

entry (float) : The price at which the position is entered. Use close if you arent adding to a position. Use the original entry price if you are adding to a position.

stop_level (float) : The price level where the stop loss is placed

stop_range (float) : The price range from entry to stop level

capital (float) : The total capital available for trading

risk_percent (float) : The percentage of capital risked on the trade. 100% is represented by 100.

trade_direction (bool) : True for long trades, false for short trades

whole_number_buy (bool) : True to adjust the quantity to whole numbers

Returns: A tuple containing the number of units to trade, the value at risk, and the total value of the position:

calculate_risk_futures(risk_capital, stop_range)

Calculates risk metrics for futures trades based on the risk capital and stop range

Parameters:

risk_capital (float) : The capital allocated for the trade

stop_range (float) : The price range from entry to stop level

Returns: A tuple containing the number of contracts to trade, the value at risk, and the total value of the position:

calculate_risk_forex(entry, stop_level, stop_range, capital, risk_percent, trade_direction)

Calculates risk metrics for forex trades based on entry, stop level, and risk percent

Parameters:

entry (float) : The price at which the position is entered. Use close if you arent adding to a position. Use the original entry price if you are adding to a position.

stop_level (float) : The price level where the stop loss is placed

stop_range (float) : The price range from entry to stop level

capital (float) : The total capital available for trading

risk_percent (float) : The percentage of capital risked on the trade. 100% is represented by 100.

trade_direction (bool) : True for long trades, false for short trades

Returns: A tuple containing the number of lots to trade, the value at risk, and the total value of the position:

calculate_risk_auto(entry, stop_level, stop_range, capital, risk_percent, trade_direction, whole_number_buy)

Automatically selects the risk calculation method based on the asset type and calculates risk metrics

Parameters:

entry (float) : The price at which the position is entered. Use close if you arent adding to a position. Use the original entry price if you are adding to a position.

stop_level (float) : The price level where the stop loss is placed

stop_range (float) : The price range from entry to stop level

capital (float) : The total capital available for trading

risk_percent (float) : The percentage of capital risked on the trade. 100% is represented by 100.

trade_direction (bool) : True for long trades, false for short trades

whole_number_buy (bool) : True to adjust the quantity to whole numbers, applicable only for non-futures and non-forex trades

Returns: A tuple containing the number of units or contracts to trade, the value at risk, and the total value of the position:

leverage_level(account_equity, position_value)

Calculates the leverage level used based on account equity and position value

Parameters:

account_equity (float) : Total equity in the trading account

position_value (float) : Total value of the position taken

Returns: The leverage level used in the trade

calculate_liquidation_level(entry, leverage, trade_direction, maintenance_margine)

Calculates the liquidation price level for a leveraged trade

Parameters:

entry (float) : The price at which the position is entered

leverage (float) : The leverage level used in the trade

trade_direction (bool) : True for long trades, false for short trades

maintenance_margine (float) : The maintenance margin requirement, expressed as a percentage

Returns: The price level at which the position would be liquidated, or na if leverage is zero

US Net LiquidityAnalysis of US Net Liquidity: A Comprehensive Overview

Introduction:

The "US Net Liquidity" indicator offers a detailed analysis of liquidity conditions within the United States, drawing insights from critical financial metrics related to the Federal Reserve (FED) and other government accounts. This tool enables economists to assess liquidity dynamics, identify trends, and inform economic decision-making.

Key Metrics and Interpretation:

1. Smoothing Period: This parameter adjusts the level of detail in the analysis by applying a moving average to the liquidity data. A longer smoothing period results in a smoother trend line, useful for identifying broader liquidity patterns over time.

2. Data Source (Timeframe): Specifies the timeframe of the data used for analysis, typically daily (D). Different timeframes can provide varying perspectives on liquidity trends.

3. Data Categories:

- FED Balance Sheet: Represents the assets and liabilities of the Federal Reserve, offering insights into monetary policy and market interventions.

- US Treasury General Account (TGA): Tracks the balance of the US Treasury's general account, reflecting government cash management and financial stability.

- Overnight Reverse Repurchase Agreements (RRP): Highlights short-term borrowing and lending operations between financial institutions and the Federal Reserve, influencing liquidity conditions.

- Earnings Remittances to the Treasury: Indicates revenues transferred to the US Treasury from various sources, impacting government cash flow and liquidity.

4. Moving Average Length: Determines the duration of the moving average applied to the data. A longer moving average length smoothens out short-term fluctuations, emphasizing longer-term liquidity trends.

Variation Lookback Length: Specifies the historical period used to assess changes and variations in liquidity. A longer lookback length captures more extended trends and fluctuations.

Interpretation:

1. Data Retrieval: Real-time data from specified financial instruments (assets) is retrieved to calculate balances for each category (FED, TGA, RRP, Earnings Remittances).

2. Global Balance Calculation: The global liquidity balance is computed by aggregating the balances of individual categories (FED Balance - TGA Balance - RRP Balance - Earnings Remittances Balance). This metric provides a comprehensive view of net liquidity.

3. Smoothed Global Balance (SMA): The Simple Moving Average (SMA) is applied to the global liquidity balance to enhance clarity and identify underlying trends. A rising SMA suggests improving liquidity conditions, while a declining SMA may indicate tightening liquidity.

Insight Generation and Decision-Making:

1. Trend Analysis: By analyzing smoothed liquidity trends over time, economists can identify periods of liquidity surplus or deficit, which can inform monetary policy decisions and market interventions.

2. Forecasting: Understanding liquidity dynamics aids in economic forecasting, particularly in predicting market liquidity, interest rate movements, and financial stability.

3. Policy Implications: Insights derived from this analysis tool can guide policymakers in formulating effective monetary policies, managing government cash flow, and ensuring financial stability.

Conclusion:

The "US Net Liquidity" analysis tool serves as a valuable resource for economists, offering a data-driven approach to understanding liquidity dynamics within the US economy. By interpreting key metrics and trends, economists can make informed decisions and contribute to macroeconomic stability and growth.

Disclaimer: This analysis is based on real-time financial data and should be used for informational purposes only. It is not intended as financial advice or a substitute for professional expertise.

mathLibrary "math"

It's a library of discrete aproximations of a price or Series float it uses Fourier Discrete transform, Laplace Discrete Original and Modified transform and Euler's Theoreum for Homogenus White noice operations. Calling functions without source value it automatically take close as the default source value.

Here is a picture of Laplace and Fourier approximated close prices from this library:

Copy this indicator and try it yourself:

import AutomatedTradingAlgorithms/math/1 as math

//@version=5

indicator("Close Price with Aproximations", shorttitle="Close and Aproximations", overlay=false)

// Sample input data (replace this with your own data)

inputData = close

// Plot Close Price

plot(inputData, color=color.blue, title="Close Price")

ltf32_result = math.LTF32(a=0.01)

plot(ltf32_result, color=color.green, title="LTF32 Aproximation")

fft_result = math.FFT()

plot(fft_result, color=color.red, title="Fourier Aproximation")

wavelet_result = math.Wavelet()

plot(wavelet_result, color=color.orange, title="Wavelet Aproximation")

wavelet_std_result = math.Wavelet_std()

plot(wavelet_std_result, color=color.yellow, title="Wavelet_std Aproximation")

DFT3(xval, _dir)

Discrete Fourier Transform with last 3 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

Returns: Aproxiated source value

DFT2(xval, _dir)

Discrete Fourier Transform with last 2 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

Returns: Aproxiated source value

FFT(xval)

Fast Fourier Transform once. It aproximates usig last 3 points.

Parameters:

xval (float) : Source series

Returns: Aproxiated source value

DFT32(xval)

Combined Discrete Fourier Transforms of DFT3 and DTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

Returns: Aproxiated source value

DTF32(xval)

Combined Discrete Fourier Transforms of DFT3 and DTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

Returns: Aproxiated source value

LFT3(xval, _dir, a)

Discrete Laplace Transform with last 3 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

a (float) : laplace coeficient

Returns: Aproxiated source value

LFT2(xval, _dir, a)

Discrete Laplace Transform with last 2 points

Parameters:

xval (float) : Source series

_dir (int) : Direction parameter

a (float) : laplace coeficient

Returns: Aproxiated source value

LFT(xval, a)

Fast Laplace Transform once. It aproximates usig last 3 points.

Parameters:

xval (float) : Source series

a (float) : laplace coeficient

Returns: Aproxiated source value

LFT32(xval, a)

Combined Discrete Laplace Transforms of LFT3 and LTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

a (float) : laplace coeficient

Returns: Aproxiated source value

LTF32(xval, a)

Combined Discrete Laplace Transforms of LFT3 and LTF2 it aproximates last point by first

aproximating last 3 ponts and than using last 2 points of the previus.

Parameters:

xval (float) : Source series

a (float) : laplace coeficient

Returns: Aproxiated source value

whitenoise(indic_, _devided, minEmaLength, maxEmaLength, src)

Ehler's Universal Oscillator with White Noise, without extra aproximated src.

It uses dinamic EMA to aproximate indicator and thus reducing noise.

Parameters:

indic_ (float) : Input series for the indicator values to be smoothed

_devided (int) : Divisor for oscillator calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed indicator value

whitenoise(indic_, dft1, _devided, minEmaLength, maxEmaLength, src)

Ehler's Universal Oscillator with White Noise and DFT1.

It uses src and sproxiated src (dft1) to clearly define white noice.

It uses dinamic EMA to aproximate indicator and thus reducing noise.

Parameters:

indic_ (float) : Input series for the indicator values to be smoothed

dft1 (float) : Aproximated src value for white noice calculation

_devided (int) : Divisor for oscillator calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed indicator value

smooth(dft1, indic__, _devided, minEmaLength, maxEmaLength, src)

Smoothing source value with help of indicator series and aproximated source value

It uses src and sproxiated src (dft1) to clearly define white noice.

It uses dinamic EMA to aproximate src and thus reducing noise.

Parameters:

dft1 (float) : Value to be smoothed.

indic__ (float) : Optional input for indicator to help smooth dft1 (default is FFT)

_devided (int) : Divisor for smoothing calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed source (src) series

smooth(indic__, _devided, minEmaLength, maxEmaLength, src)

Smoothing source value with help of indicator series

It uses dinamic EMA to aproximate src and thus reducing noise.

Parameters:

indic__ (float) : Optional input for indicator to help smooth dft1 (default is FFT)

_devided (int) : Divisor for smoothing calculations

minEmaLength (int) : Minimum EMA length

maxEmaLength (int) : Maximum EMA length

src (float) : Source series

Returns: Smoothed src series

vzo_ema(src, len)

Volume Zone Oscillator with EMA smoothing

Parameters:

src (float) : Source series

len (simple int) : Length parameter for EMA

Returns: VZO value

vzo_sma(src, len)

Volume Zone Oscillator with SMA smoothing

Parameters:

src (float) : Source series

len (int) : Length parameter for SMA

Returns: VZO value

vzo_wma(src, len)

Volume Zone Oscillator with WMA smoothing

Parameters:

src (float) : Source series

len (int) : Length parameter for WMA

Returns: VZO value

alma2(series, windowsize, offset, sigma)

Arnaud Legoux Moving Average 2 accepts sigma as series float

Parameters:

series (float) : Input series

windowsize (int) : Size of the moving average window

offset (float) : Offset parameter

sigma (float) : Sigma parameter

Returns: ALMA value

Wavelet(src, len, offset, sigma)

Aproxiates srt using Discrete wavelet transform.

Parameters:

src (float) : Source series

len (int) : Length parameter for ALMA

offset (simple float)

sigma (simple float)

Returns: Wavelet-transformed series

Wavelet_std(src, len, offset, mag)

Aproxiates srt using Discrete wavelet transform with standard deviation as a magnitude.

Parameters:

src (float) : Source series

len (int) : Length parameter for ALMA

offset (float) : Offset parameter for ALMA

mag (int) : Magnitude parameter for standard deviation

Returns: Wavelet-transformed series

LaplaceTransform(xval, N, a)

Original Laplace Transform over N set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

Returns: Aproxiated source value

NLaplaceTransform(xval, N, a, repeat)

Y repetirions on Original Laplace Transform over N set of close prices, each time N-k set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

LaplaceTransformsum(xval, N, a, b)

Sum of 2 exponent coeficient of Laplace Transform over N set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

Returns: Aproxiated source value

NLaplaceTransformdiff(xval, N, a, b, repeat)

Difference of 2 exponent coeficient of Laplace Transform over N set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

N_divLaplaceTransformdiff(xval, N, a, b, repeat)

N repetitions of Difference of 2 exponent coeficient of Laplace Transform over N set of close prices, with dynamic rotation

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

LaplaceTransformdiff(xval, N, a, b)

Difference of 2 exponent coeficient of Laplace Transform over N set of close prices

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

Returns: Aproxiated source value

NLaplaceTransformdiffFrom2(xval, N, a, b, repeat)

N repetitions of Difference of 2 exponent coeficient of Laplace Transform over N set of close prices, second element has for 1 higher exponent factor

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

N_divLaplaceTransformdiffFrom2(xval, N, a, b, repeat)

N repetitions of Difference of 2 exponent coeficient of Laplace Transform over N set of close prices, second element has for 1 higher exponent factor, dynamic rotation

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

repeat (int) : number of repetitions

Returns: Aproxiated source value

LaplaceTransformdiffFrom2(xval, N, a, b)

Difference of 2 exponent coeficient of Laplace Transform over N set of close prices, second element has for 1 higher exponent factor

Parameters:

xval (float) : series to aproximate

N (int) : number of close prices in calculations

a (float) : laplace coeficient

b (float) : second laplace coeficient

Returns: Aproxiated source value

[BT] NedDavis Series: CPI Minus 5-Year Moving Average🟧 GENERAL

The script works on the Monthly Timeframe and has 2 main settings (explained in FEATURES ). It uses the US CPI data, reported by the Bureau of Labour Statistics.

🔹Functionality 1: The main idea is to plot the distance between the CPI line and the 5 year moving average of the CPI line. This technique in mathematics is called "deviation from the moving average". This technique is used to analyse how has CPI previously acted and can give clues at what it might do in the future. Economic historians use such analysis, together with specific period analysis to predict potential risks in the future (see an example of such analysis in HOW TO USE section. The mathematical technique is a simple subtraction between 2 points (CPI - 5yr SMA of CPI).

▶︎Interpretation for deviation from a moving average:

Positive Deviation: When the line is above its moving average, it indicates that the current value is higher than the average, suggesting potential strength or bullish sentiment.

Negative Deviation: Conversely, when the line falls below its moving average, it suggests weakness or bearish sentiment as the current value is lower than the average.

▶︎Applications:

Trend Identification: Deviations from moving averages can help identify trends, with sustained deviations indicating strong trends.

Reversal Signals: Significant deviations from moving averages may signal potential trend reversals, especially when combined with other technical indicators.

Volatility Measurement: Monitoring the magnitude of deviations can provide insights into market volatility and price movements.

Remember the indicator is applying this only for the US CPI - not the ticker you apply the indicator on!

🔹Functionality 2: It plots on a new pane below information about the Consumer Price Index. You can also find the information by plotting the ticker symbol USACPIALLMINMEI on TradingView, which is a Monthly economic data by the OECD for the CPI in the US. The only addition you would get from the indicator is the plot of the 5 year Simple Moving Average.

🔹What is the US Consumer Price Index?

Measures the change in the price of goods and services purchased by consumers;

Traders care about the CPI because consumer prices account for a majority of overall inflation. Inflation is important to currency valuation because rising prices lead the central bank to raise interest rates out of respect for their inflation containment mandate;

It is measured as the average price of various goods and services are sampled and then compared to the previous sampling.

Source: Bureau of Labor Statistics;

FEATURES OF INDICATOR

1) The US Consumer Price Index Minus the Five Year Moving Average of the same.

As shown on the picture above and explained in previous section. Here a more detailed view.

2) The actual US Consumer Price Index (Annual Rate of change) and the Five year average of the US Consumer Price Index. Explained above and shown below:

To activate 2) go into settings and toggle the check box.

HOW TO USE

It can be used for a fundamental analysis on the relationship between the stock market, the economy and the Feds decisions to hike or cut rates, whose main mandate is to control inflation over time.

I have created this indicator to show my analysis in this idea:

What does a First Fed Rate cut really mean?

CREDITS

I have seen such idea in the past posted by the institutional grade research of NedDavis and have recreated it for the TradingView platform, open-source for the community.

Order Block Refiner [TradingFinder]🔵 Introduction

The "Refinement" feature allows you to adjust the width of the order block according to your strategy. There are two modes, "Aggressive" and "Defensive," in the "Order Block Refine". The difference between "Aggressive" and "Defensive" lies in the width of the order block.

For risk-averse traders, the "Defensive" mode is suitable as it provides a lower loss limit and a greater reward-to-risk ratio. For risk-taking traders, the "Aggressive" mode is more appropriate. These traders prefer to enter trades at higher prices, and this mode, which has a wider order block width, is more suitable for this group of individuals.

Important :

One of the advantages of using this library is increased code accuracy. Not only does it have the capability to create order blocks, but you can also simply define the condition for order block creation (true/false) and "bar_index," and you'll find the primary range without applying any filters.

🟣 Order Block Refinement Algorithm

The order block ranges are filtered in two stages. In the first stage, the "Open," "High," "Low," and "Close" of the current order block candle, its two or three previous candles, and one subsequent candle (if available) are examined. In this stage, minimum and maximum distances are calculated, and logical range filters are applied.

In the second stage, two modes, "Aggressive" and "Defensive," are calculated.

For the "Defensive" mode, the width of these ranges is compared with the "ATR" (Average True Range) of period 55, and if they are smaller than "ATR" or 1 to more than 4 times "ATR," the width of the range is reduced from 0 to 80 percent.

For the "Aggressive" mode, you get the same output as the first filter, which usually has a wider width than the "Defensive" mode.

• Order Block Refiner : Off

• Order Block Refiner : On / "Aggressive Mode"

• Order Block Refiner : On / "Defensive Mode"

🔵 How to Use

OBRefiner(string OBType, string OBRefine, string RefineMethod, bool TriggerCondition, int Index) =>

Parameters:

• OBType (string)

• OBRefine (string)

• RefineMethod (string)

• TriggerCondition (bool)

• Index (int)

To add "Order Block Refiner Library", you must first add the following code to your script.

import TFlab/OrderBlockRefiner_TradingFinder/1

OBType : This parameter receives 2 inputs. If the order block you want to "Refine" is of type demand, you should enter "Demand," and if it's of type supply, you should enter "Supply."

OBRefine : Set to "On" if you want the "Refine" operation to be performed. Otherwise, set to "Off."

RefineMethod : This input receives 2 modes, "Aggressive" and "Defensive." You can switch between these modes according to your needs.

TriggerCondition : Enter the condition with which the order block is formed in this parameter.

Index : Enter the "bar_index" of the candle where the order block is formed in this parameter.

🟣 Function Outputs

This function has 6 outputs: "bar_index" at the beginning of the "Distal" line, "bar_index+1" at the end of the "Distal" line, "Price" at the "Distal" line, "bar_index" at the beginning of the "Proximal" line, "bar_index+1" at the end of the "Proximal" line, and "Price" at the "Proximal" line, which can be used to draw order blocks.

Sample :

= Refiner.OBRefiner('Demand', 'Off', 'Aggressive',BuMChMain_Trigger, BuMChMain_Index)

if BuMChMain_Trigger

BuMChHlineMain := line.new(BuMChMain_Xp1 , BuMChMain_Yp12 , bar_index , BuMChMain_Yp12, color = color.black , style = line.style_dotted)

BuMChLlineMain := line.new(BuMChMain_Xd1 , BuMChMain_Yd12 , bar_index , BuMChMain_Yd12, color = color.black , style = line.style_dotted)

BuMChFilineMain := linefill.new(BuMChHlineMain ,BuMChLlineMain , color = color.rgb(76, 175, 80 , 75 ) )