Blockunity Address Synthesis (BAS)Track the address status of the various cryptoassets and their evolution.

The Idea

The goal is to provide a simple tool for visualizing the evolution of different types of crypto addresses.

How to Use

This tool is to be used as fundamental information. It is not intended for investment or trading purposes.

Elements

Active Addresses

Active Addresses represent the subset of total addresses that made one or more on-chain transaction on a given day.

New Addresses

New Addresses refer to addresses that receive their first deposit in the selected crypto-asset.

Zero Balance Addresses

Zero Balance Addresses are addresses that transferred out (potentially sold) all of their holdings for the selected crypto-asset.

Total Addresses

Total Addresses refer to the overall count of unique addresses that have been created on a blockchain network.

Settings

In the settings, you can :

Adjust line smoothing (in terms of number of days).

Change the lookback period used to calculate the different variations.

Display or not the different address types (for better visualization, Total Addresses should be shown alone).

Show or hide labels and configure their offset.

Lastly, you can modify all table parameters.

Statistics

Open Interest Inflows & Outflows [LuxAlgo]The Open Interest Inflows & Outflows indicator focuses on highlighting alterations in the overall count of active contracts associated with a specific financial instrument.

The indicator also includes an oscillator highlighting the price sentiment to use in conjunction with the open interest flow sentiment and also includes a rolling correlation of the open interest flow sentiment with a user-selected source.

🔶 USAGE

Open Interest (OI) indicates the total number of active contracts, encompassing both long and short positions, for a specific financial instrument at any given moment. This key indicator helps traders and analysts assess market activity and sentiment.

An increase in open interest generally indicates new money flowing into the market, suggesting increased activity and the potential for a trending market. Conversely, a decrease in open interest indicates that traders are closing their positions, suggesting less interest in that particular contract.

Open Interest Flow Sentiment assesses the correlation between the initiation of new positions (inflows) and the closure of existing positions (outflows) for a particular instrument. Positive values suggest a prevalence of inflows, while negative values signify a prevalence of outflows.

The magnitude of the deviation from zero reflects the extent of dominance, either in inflows or outflows.

Price Sentiment estimates the relationship between the strength of bulls (buyers) and bears (sellers) on an instrument. Positive values indicate higher bull power and negative values indicate higher bear power.

The correlation feature is a key component of the indicator and helps analyze the relationship between trading volume and Open Interest changes. If volume increases along with rising Open Interest, it supports the validity of the price trend.

A divergence between price movement, volume, and Open Interest may signal potential reversals.

🔶 DETAILS

This indicator, based on Dr. Alexander Elder's acclaimed Elder-Ray concept, aids traders in evaluating the strength of both bulls and bears by delving beneath the surface of the markets. It uncovers data not immediately apparent from a superficial glance at prices. The indicator comprises two components: Bull Power and Bear Power.

Considering that the high price of any candle signifies the maximum power of buyers and the low price represents the maximum power of sellers, Elder employs the 13-period Exponential Moving Average (EMA) to depict the average consensus of price value. Bull Power assesses whether buyers can drive prices above the average consensus of value, while Bear Power assesses whether sellers can push prices below this average.

Here are the formulas for Bull Power and Bear Power:

bull_power = high - ema(close, 13)

bear_power = low - ema(close, 13)

This concept is utilized to calculate Open Interest Flow Sentiment and Price Sentiment. The Open Interest Flow Sentiment estimates the relationship between new positions (inflows) and positions being closed (outflows), providing insights into market dynamics. The Price Sentiment, on the other hand, gauges the correlation between price movements and the Elder-Ray components, aiding traders in identifying potential shifts in market sentiment and momentum.

🔶 SETTINGS

🔹Open Interest Inflows & Outflows

OI Sentiment Correlation: toggles the visibility of Open Interest correlation with a variety of sources.

Money Flow Estimates: toggles the visibility of Money Flow Estimates calculated for the last bar.

🔹Style

OI Flow Sentiment: toggles the visibility of Open Interest Flow Sentiment, along with color customization options.

Price Sentiment: toggles the visibility of Price Sentiment, along with color customization options.

Correlation Colors: color customization option for the Correlation Area.

🔹Others

Smoothing: smoothing length applicable for Open Interest Flow Sentiment and Price Sentiment.

🔶 RELATED SCRIPTS

Open-Interest-Chart

Liquidation-Estimates

Thanks to our community for recommending this script. For more conceptual scripts and related content, we welcome you to explore by visiting >>> LuxAlgo-Scripts .

Exceptional MovementThis indicator is a simple tracker for exceptional movement.

It compares the range of the latest candle with the average daily range of the past 20 candles.

The option for the multiplier defines how big the current movement should be to be defined as exceptional movement.

Volatility Adjusted Profit Target

In my 'Volatility Adjusted Profit Target' indicator, I've crafted a dynamic tool for calculating target profit percentages suitable for both long and short trading strategies. It evaluates the highest and lowest prices over the anticipated duration of your trade, establishing a profit target that shifts with market volatility. As volatility increases, the potential for profit follows, with the target percentage rising accordingly; conversely, it declines with decreasing volatility. As a trader, setting an optimal Take Profit level has always been a challenge. This indicator not only helps in determining that level but also dynamically adjusts it throughout the trade's duration, providing a strategic edge in volatile markets.

Within Standard Deviation Bounds ProbabilityThis indicator calculates the probability of the closing price remaining within the upper and lower bounds defined by the mean and standard deviation of historical percent changes. It also plots the probability line and a horizontal line at 68%, which would be the expected probability for a normal distribution. It is designed to be used with my other indicator "Mean and Standard Deviation Lines.

Inputs:

period (Days): This defines the number of bars used to calculate the mean and standard deviation.

Calculations:

Percent change: Calculates the daily percentage change between closing prices.

Mean and standard deviation: Calculates the mean and standard deviation of the percent changes over the specified period.

Bounds: Calculates the upper and lower bounds by adding/subtracting the standard deviation from the mean, multiplied by the closing price.

Crossover tracking: Iterates through bars and counts crosses above and below the bounds.

Probability calculation: Calculates the total crossover probability as a percentage of the period.

Plotting: Plots the probability line and the horizontal line at 68%.

Limitations:

Assumes a normal distribution of price changes, which may not be accurate in real markets.

Overall:

This indicator provides a way to visualize the probability of the price staying within calculated bounds based on historical volatility. However, it's important to be aware of its limitations and interpret the results within the context of your trading strategy and risk management.

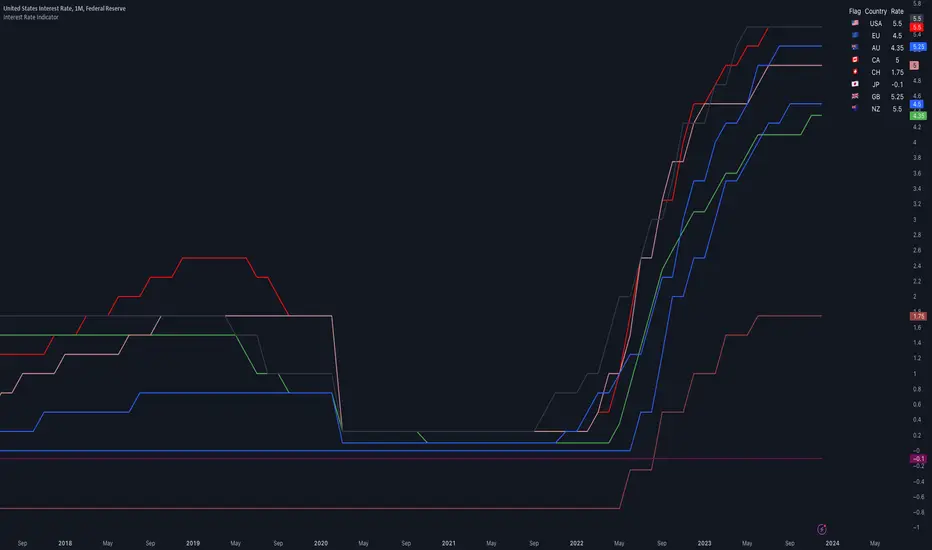

Interest Rate IndicatorThis script offers a overview of Year-over-Year (YoY) interest rates for key countries. The interest rate data utilized by default are sourced from TradingView Tickers, but they can be modified to any preferred source via the settings.

The script does not perform any calculations; its primary function is to present a comparative view of interest rates across different countries in a single indicator.

Key features include:

Interest rate data for the USA, European Union, Australia, Canada, Switzerland, Japan, United Kingdom, and New Zealand (Interest Rate Symbols are editable in the settings).

A table displaying country flags, names, and the latest interest rates, providing a clear and immediate comparison.

Country-representative colors for easy identification and visual distinction between different countries' data.

This indicator is designed for traders and analysts looking for a quick and efficient way to monitor and compare the interest rates of major economies directly within TradingView, facilitating better informed financial and investment decisions.

Mean and Standard Deviation Lines Description:

Calculates the mean and standard deviation of close-to-close price differences over a specified period, providing insights into price volatility and potential breakouts.

Manually calculates mean and standard deviation for a deeper understanding of statistical concepts.

Plots the mean line, upper bound (mean + standard deviation), and lower bound (mean - standard deviation) to visualize price behavior relative to these levels.

Highlights bars that cross the upper or lower bounds with green (above) or red (below) triangles for easy identification of potential breakouts or breakdowns.

Customizable period input allows for analysis of short-term or long-term volatility patterns.

Probability Interpretations based on Standard Deviation:

50% probability: mean or expected value

68% probability: Values within 1 standard deviation of the mean (mean ± stdev) represent roughly 68% of the data in a normal distribution. This implies that around 68% of closing prices in the past period fell within this range.

95% probability: Expanding to 2 standard deviations (mean ± 2*stdev) captures approximately 95% of the data. So, in theory, there's a 95% chance that future closing prices will fall within this wider range.

99.7% probability: Going further to 3 standard deviations (mean ± 3*stdev) encompasses nearly 99.7% of the data. However, these extreme values become less likely as you move further away from the mean.

Key Features:

Uses manual calculations for mean and standard deviation, providing a hands-on approach.

Excludes the current bar's close price from calculations for more accurate analysis of past data.

Ensures valid index usage for robust calculation logic.

Employs unbiased standard deviation calculation for better statistical validity.

Offers clear visual representation of mean and volatility bands.

Considerations:

Manual calculations might have a slight performance impact compared to built-in functions.

Not a perfect normal distribution: Financial markets often deviate from a perfect normal distribution. This means probability interpretations based on standard deviation shouldn't be taken as absolute truths.

Non-stationarity: Market conditions and price behavior can change over time, impacting the validity of past data as a future predictor.

Other factors: Many other factors influence price movements beyond just the mean and standard deviation.

Always consider other technical and fundamental factors when making trading decisions.

Potential Use Cases:

Identifying periods of high or low volatility.

Discovering potential breakout or breakdown opportunities.

Comparing volatility across different timeframes.

Complementing other technical indicators for confirmation.

Understanding statistical concepts for financial analysis.

US Yield Curve ComparisonIn finance, the yield curve is a graph which depicts how the yields on debt instruments – such as bonds – vary as a function of their years remaining to maturity. The graph's horizontal or x-axis is a time line of months and years remaining to maturity, with the shortest maturity on the left and progressively longer time periods on the right. The vertical or y-axis depicts the annualized yield to maturity.

To see changes of a definded timeframe, use this indicator to compare the current US yield curve with one in the past.

Monte Carlo Future Moves [ChartPrime]ORIGINS AND HISTORICAL BACKGROUND:

Prior to the the advent of the Monte Carlo method, examining well-understood deterministic problems via simulation generally utilized statistical sampling to gauge uncertainty estimations. The Monte Carlo (MC) approach inverts this paradigm by modeling with probabilistic metaheuristics to address deterministic problems. Addressing Buffon's needle problem, an early form of the Monte Carlo method estimated π (3.14159) by dropping needles on a floor. Later, the modern MC inception primarily began when Stanislaw Ulam was playing solitaire games while experiencing illness and recovery.

Ulam further developed, applied, and ascribed "Monte Carlo" as a classified code name to maintain a level of secrecy for the modern method applications during collaborative investigations on neutron diffusion and collision intricacies with John von Neumann. Despite having relevant data, physicist's conventional deterministic mathematical methods were unable to solve mysterious "neutronion problems". Monte Carlo filled in the gaps necessary to resolve this perplexing neutron problem with innovative statistics, and the resilient MC continues onward to have diverse application in many fields of science. MC also extends into the realm of relevance within finance.

APPLICATION IN FINANCE:

Building on its historical roots, the Monte Carlo method's transition into finance opened new avenues for risk assessment and predictive analysis. In financial markets, characterized by uncertainty and complex variables, this method offers a powerful tool for simulating a wide range of scenarios and assessing probabilities of different outcomes. By employing probabilistic models to predict price movements, the Monte Carlo method helps in creating more resilient and informed trading strategies. This approach is particularly valuable in options pricing, portfolio management, and risk assessment, where understanding the range of potential outcomes is crucial for making sound investment decisions. Our indicator utilizes this methodology, blending traditional financial analysis with advanced statistical techniques.

THE INDICATOR:

The Monte Carlo Future Moves (ChartPrime) indicator is designed to predict future price movements. It simulates various possible price paths, showing the likelihood of different outcomes. We have designed it to be simple to use and understand by displaying lines indicating the most likely bullish and bearish outcomes. The arrows point to these areas making it intuitive to understand. Also included is extreme price levels shown in blue and yellow. This is the most likely extreme range that the price will move to. The outcome distribution is there to show you the range of outcomes along with a visual representation of the possible future outcomes. To make things more user friendly we have also included a representation of this distribution as a background heatmap. The brighter the price level, the more likely the price will end at that level. Finally, we have also included a market bias indication on the side that shows you the general bullish/bearish probabilities.

HOW TO USE:

To use this indicator you want to first assess the market bias. From there you want to target the most likely polar outcome. You can use the range of outcomes to assess your risk and set a stop within a reasonable range of the desired target. By default the indicator projects 10 steps into the future, however this can be easily adjusted in the settings. Generally this indicator excels at mid-term estimations and may yield inconclusive results if the prediction period is too short or too long. You can change the granularity of the outcomes to give you a more or less detailed view of the future. That being said, a lower resolution can make the predictions less useful while a higher resolution can give you a less useful picture. If you decide to use a higher resolution we have included an option to smooth the final result. This is intended to reduce the uncertainty and noise in the predicted outcomes. It is advised to use the minimum level of smoothing possible as a high level of smoothing will greatly reduce the accuracy.

INPUT SECTION:

Derivative Source changes how the indicator sees the price movements. When you set this to Candle it will use the difference between the open and close of each candle. If set to Move, it will use the difference between closing prices. If you are in a market with gaps, you might want to use Candle as this will prevent the indicator from seeing gaps.

Number of Simulations is a crucial setting as it is the core of this indicator. This determines the number of simulations the indicator will use to get its final result. By default it is set to 1000 as we feel like that is around the minimum number of simulations required to get a reasonable output while maintaining stability. In tests the maximum number of simulations we have been able to consistently achieve is 2000.

Lookback is the number of historical candles to account for. A lookback that is too short will not have enough data to accurately assess the likelihood of a price movement, while a period that is too large can make the data less relevant. By default this is set to 1000 as we feel like this is a reasonable tradeoff between volume of data and relevance.

Steps Into Future is the prediction period. By default we have picked a period of 10 steps as this has a good balance between accuracy and usability. The more steps into the future you go, the more uncertain the future outcome will be.

Outcome Granularity controls the precision of the simulated outcomes. By default this is set to 40 as its a good balance between resolution and accuracy.

Outcome Smoothing allows you to smooth the outcome distribution. By default this is set to 0 as it is generally not needed for lower resolutions. Smoothing levels beyond 2 are not recommended as it will negatively impact the output.

Returns Granularity controls the level of definition in the collected price movements. This directly impacts indicator performance and is set to 50 by default because its a good balance between fidelity and usability. When this number is too small, the simulations will be less accurate while numbers too large will negatively impact the probabilities of the movements.

Drift is the trend component in the simulation. This adds the directionality of the simulations by biasing the movements in the current direction of the market. We have included both the standard formula for drift and linear regression. Both methods are well suited for simulating future price movements and have their own advantages. The drift period is set to 100 by default as its a good balance between current and historical directionality. You may want to increase or decrease this number depending on the current market conditions but it is advised to use a period that isn't too small. If your period is too small it can skew the outcomes too much resulting in poor performance. When this is set to 0 it will use the same period as your lookback.

Volatility Adjust , adjusts the simulation to include current volatility. This makes sure that the price movements in the simulation reflects the current market conditions better by making sure that each price move is at least a minimum size.

Returns Style allows you to pick between using percent moves and log returns. We have opted to make percent move the default as it is more intuitive for beginners however both settings yield similar results. Log returns can be less cpu intensive so it might be desirable for longer term predictions.

Precision adjusts the rounding of used when collecting the frequency of price movement sizes. By default this is set to 4 as its is fairly accurate without impacting performance too much. A larger number will make the indicator more precise but at the cost of cpu time. Precision levels that are too small can greatly reduce the accuracy of the simulation and even break the indicator all together.

Update Every Bar allows you to recalculate the prediction every bar and is there for you if you want to strictly use the market bias. It is not recommended to enable this feature but it is there for flexibility.

Side of Chart allows you to pick what side of the price action you want the visuals to be on. When its set to the right everything will be to the right of the starting point and when its set to Left it will position everything to the left of the starting point.

Move Visualization is there to give you an arrow to the most likely bullish and bearish moves. It is meant as a visual aid and visualization tool. The color of these arrows use the same colors as the distribution.

Most Likely Move is a horizontal line that indicates the most likely move. It is positioned in the same location as the Move Visualization.

Standard Deviation is horizontal lines at the extremities of the simulated price action. These represent the most likely range of the future outcomes. You can adjust the multiplier of the standard deviation but by default it is set to 2.

Most Likely Direction is a vertical bar that shows you the sum of the up and down probabilities. It is there to show you the bias of the outcomes and guide you in decision making.

Max Probability Zone is a horizontal line that highlights the location of the highest probability move. You can think of it almost like the POC in a volume distribution but in this case it is the "most likely" single outcome.

Outcome Distribution allows you to toggle the distribution on or off. This is the distribution of all of the simulated outcomes. You can toggle the scale width of the distribution to fit your visual style.

Distribution Text toggles the probability text inside of the distribution bars. When you have a large number for the outcome granularity this text may not be visible and you may want to disable this feature.

Background is a heatmap of the outcome distribution. This allows you to visualize the underlying distribution without the need for the distribution histogram. The brighter the color, the more likely the outcome is for that level. It can be useful for visualizing the range of possible outcomes.

Starting Line is simply a horizontal line indicating the starting point of the simulation. It just the opening price for the starting position.

Extend Lines allows you to extend the lines and background past the prediction period.

CONCLUSION:

With its intuitive visuals and flexible settings, the Monte Carlo Future Moves (ChartPrime) indicator is practice and easy to use. It brings clarity to price movement predictions, helping you to build confidence in your strategies. This indicator not only reflects the evolution of technical analysis but also touches on data-driven insights.

Enjoy

[S] Rolling TrendlineThe Rolling Linear Regression Trendline is a sophisticated technical analysis tool designed to offer traders a dynamic view of market trends over a selectable period. This indicator employs linear regression to calculate and plot a trendline that best fits the closing prices within a specified window, either defined by a number of bars or a set period in days, independent of the chart's timeframe.

Key Features:

Dynamic Window Selection: Users can choose the calculation window based on a fixed number of bars or days, providing flexibility to adapt to different trading strategies and timeframes. For the 'days' option, the indicator calculates the equivalent number of bars based on the chart's timeframe, ensuring relevance across various market conditions and trading sessions.

Linear Regression Analysis: At its core, the indicator uses linear regression to identify the trend direction by calculating the slope and intercept of the trendline. This method offers a statistical approach to trend analysis, highlighting potential uptrends or downtrends based on the positioning and direction of the trendline.

Customizable Period: Traders can input their desired period (N), allowing for tailored analysis. Whether it's short-term movements or longer-term trends, the indicator can adjust to focus on specific time horizons, enhancing its utility across different trading styles and objectives.

Applications:

Trend Identification: By plotting a trendline that mathematically fits the closing prices over the chosen period, traders can quickly identify the prevailing market trend, aiding in bullish or bearish decision-making.

Support and Resistance: The trendline can also serve as a dynamic level of support or resistance, offering potential entry or exit points based on the price's interaction with the trendline.

Strategic Planning: With the ability to adjust the calculation window, traders can align the indicator with their trading strategy, whether focusing on intraday movements or broader swings.

Using this indicator with other parameters can widen you view of the market and help identifying trends

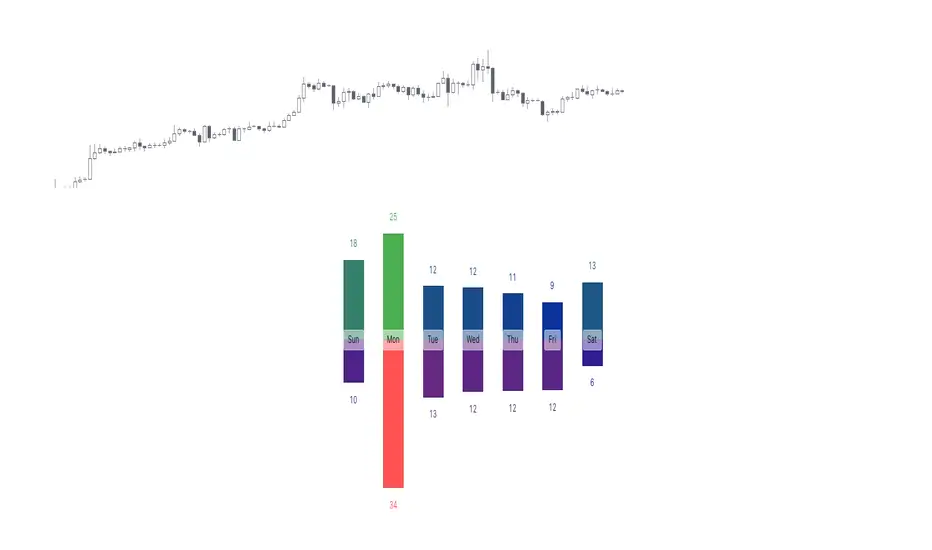

Tops & Bottoms - Day of Week Report█ OVERVIEW

The indicator tracks when the weekly tops and bottoms occur and reports the statistics by the days of the week.

█ CONCEPTS

Not all the days of the week are equal, and the market dynamic can follow through or shift over the trading week. Tops and bottoms are vital when entering a trade, as they will decide if you are catching the train or being straight offside. They are equally crucial when exiting a position, as they will determine if you are closing at the optimal price or seeing your unrealized profits vanish.

This indicator is before all for educational purposes. It aims to make the knowledge available to all traders, facilitate understanding of the various markets, and ultimately get to know your trading pairs by heart (and saving a lot of your time backtesting!).

USDJPY tops and bottoms percentages on any given week.

USDJPY tops and bottoms percentages on up weeks versus down weeks.

█ FEATURES

Custom interval

By default, the indicator uses the weekly interval defined by the symbol (e.g., Monday to Sunday). This option allows you to specify your custom interval.

Weekly interval type filter

Analyze the weekly interval on any weeks, up weeks, or down weeks.

Configurable time range filter

Select the period to report from.

█ NOTES

Trading session

The indicator analyzes the days of the week from the daily chart. The daily trading sessions are defined by the symbol (e.g., 17:00 - 17:00 on EURUSD).

Extended/electronic trading session

The indicator can include the extended hours when activated on the chart, using the 24-hour or 1440-minute timeframe.

█ HOW TO USE

Plot the indicator and navigate on the 1-day or 24-hour timeframe.

Blockunity Level Presets (BLP)A simple tool for setting performance targets.

Level Presets (BLP) is a simple tool for setting upside and downside levels relative to the current price of any asset. In this way, you can track which price the asset needs to move towards in order to achieve a defined performance.

How to Use

This indicator is very easy to use, you can set up to 5 upward and downward targets in the parameters.

Elements

The main elements of this tool are upward (default green) and downward (default red) levels.

Settings

Several parameters can be defined in the indicator configuration.

In addition to configuring which performance value to set the level at, you can choose not to display it if you don't need it. For example, here we display only two levels:

You can also choose not to display the labels:

Also concerning labels, you can choose not to display them in currency format, but in numerical format only (for example, if you're viewing a non-USD pair, such as ETHBTC):

Finally, you can modify design elements such as colors, level widths and text size:

How it Works

Here's how upside (_u) and downside (_d) levels are calculated:

source = close

level_1_u = source + (source * (level_1 / 100))

level_1_d = math.max(source - (source * (level_1 / 100)), 0)

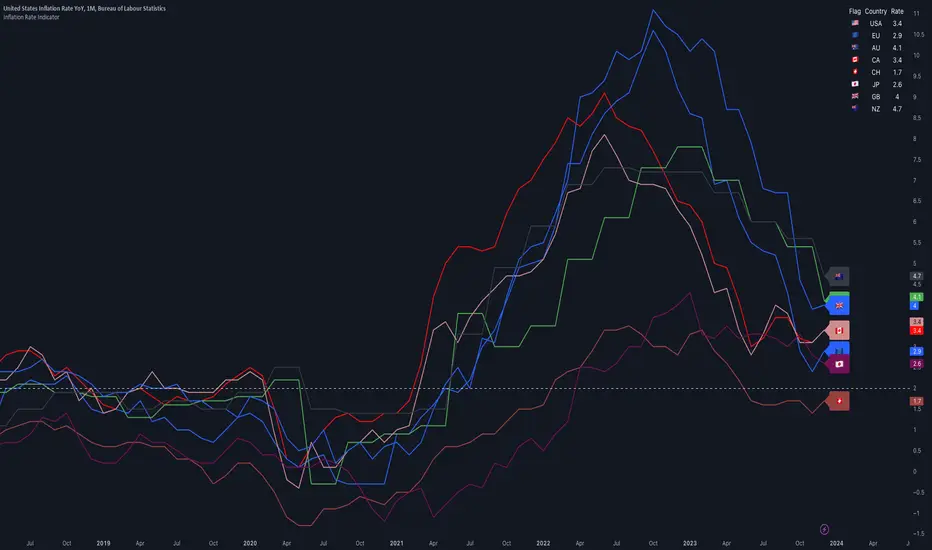

Inflation IndicatorThis script provides a great view of Year-over-Year (YoY) inflation rates for key countries.

The inflation data used per default are TradingView Tickers, but you can change them to anything you want from the settings.

There is no calculation in this script, all it does is providing a overview of inflation rates in a single indicator.

Inflation data for the USA, European Union, Australia, Canada, Switzerland, Japan, United Kingdom, and New Zealand (Inflation Symbols editable in the settings)

Customizable static line to indicate a specific threshold value (default: 2.0).

Table displaying country flags, names, and the latest inflation rates.

Country-representative colors for easy identification.

TimeSeriesRecurrencePlotLibrary "TimeSeriesRecurrencePlot"

In descriptive statistics and chaos theory, a recurrence plot (RP) is a plot showing, for each moment i i in time, the times at which the state of a dynamical system returns to the previous state at `i`, i.e., when the phase space trajectory visits roughly the same area in the phase space as at time `j`.

```

A recurrence plot (RP) is a graphical representation used in the analysis of time series data and dynamical systems. It visualizes recurring states or events over time by transforming the original time series into a binary matrix, where each element represents whether two consecutive points are above or below a specified threshold. The resulting Recurrence Plot Matrix reveals patterns, structures, and correlations within the data while providing insights into underlying mechanisms of complex systems.

```

~starling7b

___

Reference:

en.wikipedia.org

github.com

github.com

github.com

github.com

juliadynamics.github.io

distance_matrix(series1, series2, max_freq, norm)

Generate distance matrix between two series.

Parameters:

series1 (float) : Source series 1.

series2 (float) : Source series 2.

max_freq (int) : Maximum frequency to inpect or the size of the generated matrix.

norm (string) : Norm of the distance metric, default=`euclidean`, options=`euclidean`, `manhattan`, `max`.

Returns: Matrix with distance values.

method normalize_distance(M)

Normalizes a matrix within its Min-Max range.

Namespace types: matrix

Parameters:

M (matrix) : Source matrix.

Returns: Normalized matrix.

method threshold(M, threshold)

Updates the matrix with the condition `M(i,j) > threshold ? 1 : 0`.

Namespace types: matrix

Parameters:

M (matrix) : Source matrix.

threshold (float)

Returns: Cross matrix.

rolling_window(a, b, sample_size)

An experimental alternative method to plot a recurrence_plot.

Parameters:

a (array) : Array with data.

b (array) : Array with data.

sample_size (int)

Returns: Recurrence_plot matrix.

Test - Most correlated assetThis is a simple test to find the most and least correlated assets in a list.

TimeSeriesGrammianAngularFieldLibrary "TimeSeriesGrammianAngularField"

provides Grammian angular field and associated utility functions.

___

Reference:

*Time Series Classification: A review of Algorithms and Implementations*.

www.researchgate.net

method normalize(data, a, b)

Normalize the series to a optional range, usualy within `(-1, 1)` or `(0, 1)`.

Namespace types: array

Parameters:

data (array) : Sample data to normalize.

a (float) : Minimum target range value, `default=-1.0`.

b (float) : Minimum target range value, `default= 1.0`.

Returns: Normalized array within new range.

___

Reference:

*Time Series Classification: A review of Algorithms and Implementations*.

normalize_series(source, length, a, b)

Normalize the series to a optional range, usualy within `(-1, 1)` or `(0, 1)`.\

*Note that this may provide a different result than the array version due to rolling range*.

Parameters:

source (float) : Series to normalize.

length (int) : Number of bars to sample the range.

a (float) : Minimum target range value, `default=-1.0`.

b (float) : Minimum target range value, `default= 1.0`.

Returns: Normalized series within new range.

method polar(data)

Turns a normalized sample array into polar coordinates.

Namespace types: array

Parameters:

data (array) : Sampled data values.

Returns: Converted array into polar coordinates.

polar_series(source)

Turns a normalized series into polar coordinates.

Parameters:

source (float) : Source series.

Returns: Converted series into polar coordinates.

method gasf(data)

Gramian Angular Summation Field *`GASF`*.

Namespace types: array

Parameters:

data (array) : Sampled data values.

Returns: Matrix with *`GASF`* values.

method gasf_id(data)

Trig. identity of Gramian Angular Summation Field *`GASF`*.

Namespace types: array

Parameters:

data (array) : Sampled data values.

Returns: Matrix with *`GASF`* values.

Reference:

*Time Series Classification: A review of Algorithms and Implementations*.

method gadf(data)

Gramian Angular Difference Field *`GADF`*.

Namespace types: array

Parameters:

data (array) : Sampled data values.

Returns: Matrix with *`GADF`* values.

method gadf_id(data)

Trig. identity of Gramian Angular Difference Field *`GADF`*.

Namespace types: array

Parameters:

data (array) : Sampled data values.

Returns: Matrix with *`GADF`* values.

Reference:

*Time Series Classification: A review of Algorithms and Implementations*.

CCOMET_Scanner_LibraryLibrary "CCOMET_Scanner_Library"

- A Trader's Edge (ATE)_Library was created to assist in constructing CCOMET Scanners

Loc_tIDs_Col(_string, _firstLocation)

TickerIDs: You must form this single tickerID input string exactly as described in the scripts info panel (little gray 'i' that

is circled at the end of the settings in the settings/input panel that you can hover your cursor over this 'i' to read the

details of that particular input). IF the string is formed correctly then it will break up this single string parameter into

a total of 40 separate strings which will be all of the tickerIDs that the script is using in your CCOMET Scanner.

Locations: This function is used when there's a desire to print an assets ALERT LABELS. A set Location on the scale is assigned to each asset.

This is created so that if a lot of alerts are triggered, they will stay relatively visible and not overlap each other.

If you set your '_firstLocation' parameter as 1, since there are a max of 40 assets that can be scanned, the 1st asset's location

is assigned the value in the '_firstLocation' parameter, the 2nd asset's location is the (1st asset's location+1)...and so on.

Parameters:

_string (simple string) : (string)

A maximum of 40 Tickers (ALL joined as 1 string for the input parameter) that is formulated EXACTLY as described

within the tooltips of the TickerID inputs in my CCOMET Scanner scripts:

assets = input.text_area(tIDset1, title="TickerID (MUST READ TOOLTIP)", tooltip="Accepts 40 TICKERID's for each

copy of the script on the chart. TEXT FORMATTING RULES FOR TICKERID'S:

(1) To exclude the EXCHANGE NAME in the Labels, de-select the next input option.

(2) MUST have a space (' ') AFTER each TickerID.

(3) Capitalization in the Labels will match cap of these TickerID's.

(4) If your asset has a BaseCurrency & QuoteCurrency (ie. ADAUSDT ) BUT you ONLY want Labels

to show BaseCurrency(ie.'ADA'), include a FORWARD SLASH ('/') between the Base & Quote (ie.'ADA/USDT')", display=display.none)

_firstLocation (simple int) : (simple int)

Optional (starts at 1 if no parameter added).

Location that you want the first asset to print its label if is triggered to do so.

ie. loc2=loc1+1, loc3=loc2+1, etc.

Returns: Returns 40 output variables in the tuple (ie. between the ' ') with the TickerIDs, 40 variables for the locations for alert labels, and 40 Colors for labels/plots

TickeridForLabelsAndSecurity(_ticker, _includeExchange)

This function accepts the TickerID Name as its parameter and produces a single string that will be used in all of your labels.

Parameters:

_ticker (simple string) : (string)

For this parameter, input the varible named '_coin' from your 'f_main()' function for this parameter. It is the raw

Ticker ID name that will be processed.

_includeExchange (simple bool) : (bool)

Optional (if parameter not included in function it defaults to false ).

Used to determine if the Exchange name will be included in all labels/triggers/alerts.

Returns: ( )

Returns 2 output variables:

1st ('_securityTickerid') is to be used in the 'request.security()' function as this string will contain everything

TV needs to pull the correct assets data.

2nd ('lblTicker') is to be used in all of the labels in your CCOMET Scanner as it will only contain what you want your labels

to show as determined by how the tickerID is formulated in the CCOMET Scanner's input.

InvalID_LblSz(_barCnt, _close, _securityTickerid, _invalidArray, _tablePosition, _stackVertical, _lblSzRfrnce)

INVALID TICKERIDs: This is to add a table in the middle right of your chart that prints all the TickerID's that were either not formulated

correctly in the '_source' input or that is not a valid symbol and should be changed.

LABEL SIZES: This function sizes your Alert Trigger Labels according to the amount of Printed Bars the chart has printed within

a set time period, while also keeping in mind the smallest relative reference size you input in the 'lblSzRfrnceInput'

parameter of this function. A HIGHER % of Printed Bars(aka...more trades occurring for that asset on the exchange),

the LARGER the Name Label will print, potentially showing you the better opportunities on the exchange to avoid

exchange manipulation liquidations.

*** SHOULD NOT be used as size of labels that are your asset Name Labels next to each asset's Line Plot...

if your CCOMET Scanner includes these as you want these to be the same size for every asset so the larger ones dont cover the

smaller ones if the plots are all close to each other ***

Parameters:

_barCnt (float) : (float)

Get the 1st variable('barCnt') from the Security function's tuple and input it as this functions 1st input

parameter which will directly affect the size of the 2nd output variable ('alertTrigLabel') that is also outputted by this function.

_close (float) : (float)

Put your 'close' variable named '_close' from the security function here.

_securityTickerid (string) : (string)

Throughout the entire charts updates, if a '_close' value is never registered then the logic counts the asset as INVALID.

This will be the 1st TickerID variable (named _securityTickerid) outputted from the tuple of the TickeridForLabels()

function above this one.

_invalidArray (array) : (array string)

Input the array from the original script that houses all of the invalidArray strings.

_tablePosition (simple string) : (string)

Optional (if parameter not included, it defaults to position.middle_right). Location on the chart you want the table printed.

Possible strings include: position.top_center, position.top_left, position.top_right, position.middle_center,

position.middle_left, position.middle_right, position.bottom_center, position.bottom_left, position.bottom_right.

_stackVertical (simple bool) : (bool)

Optional (if parameter not included, it defaults to true). All of the assets that are counted as INVALID will be

created in a list. If you want this list to be prited as a column then input 'true' here, otherwise they will all be in a row.

_lblSzRfrnce (string) : (string)

Optional (if parameter not included, it defaults to size.small). This will be the size of the variable outputted

by this function named 'assetNameLabel' BUT also affects the size of the output variable 'alertTrigLabel' as it uses this parameter's size

as the smallest size for 'alertTrigLabel' then uses the '_barCnt' parameter to determine the next sizes up depending on the "_barCnt" value.

Returns: ( )

Returns 2 variables:

1st output variable ('AssetNameLabel') is assigned to the size of the 'lblSzRfrnceInput' parameter.

2nd output variable('alertTrigLabel') can be of variying sizes depending on the 'barCnt' parameter...BUT the smallest

size possible for the 2nd output variable ('alertTrigLabel') will be the size set in the 'lblSzRfrnceInput' parameter.

PrintedBarCount(_time, _barCntLength, _barCntPercentMin)

The Printed BarCount Filter looks back a User Defined amount of minutes and calculates the % of bars that have printed

out of the TOTAL amount of bars that COULD HAVE been printed within the same amount of time.

Parameters:

_time (int) : (int)

The time associated with the chart of the particular asset that is being screened at that point.

_barCntLength (int) : (int)

The amount of time (IN MINUTES) that you want the logic to look back at to calculate the % of bars that have actually

printed in the span of time you input into this parameter.

_barCntPercentMin (int) : (int)

The minimum % of Printed Bars of the asset being screened has to be GREATER than the value set in this parameter

for the output variable 'bc_gtg' to be true.

Returns: ( )

Returns 2 outputs:

1st is the % of Printed Bars that have printed within the within the span of time you input in the '_barCntLength' parameter.

2nd is true/false according to if the Printed BarCount % is above the threshold that you input into the '_barCntPercentMin' parameter.

Volume Footprint Voids [BigBeluga]Volume Footprint Voids is a unique tool that uses lower timeframe calculation to plot different styles of single candle POC.

This indicator is very powerful for scalping and finding very precise entry and exits, spotting potential trapped traders, and more.

Unlike many other volume profiles, this aims to plot single candle profiles as well as their own footprints.

🔶 FEATURES

The script includes the following settings:

Windows: Plotting style and calculations

Coloring modes

Display modes

lower-timeframe calculations

🔶 CALCULATION

In the image above we can see how the script calculates each level position that will serve as a calculation process to see how much volume/closes there are within the levels.

In the image above, we can have a more clear example of how we count each candle close.

We use the prior screenshot as an example, after setting each level we will use the lower-timeframe input to measure the amount of closes within the ranges.

Depending on the lot size, the box will be larger or smaller, usually the POC will always have the highest box size.

NOTE: Size is the starting point, always from the low of the candle.

To find more voids, select a closer LTF to the current one you're using.

To find fewer voids, select a timeframe away from your current one.

Due to Pine Script limitations, we are only able to plot a certain amount of footprints, and we can't plot the whole history chart.

POC will be the largest block displayed, indicating the time point of control

Gray areas are closes above the average

Black are Void or imbalance that price will fill in the future, like FVG

The image above shows an incorrect size input that will lead to bad calculations, while on the other side, a correct size input that will lead to a clear vision and better calculation.

🔶 WINDOWS

The "▲▼" Mode will display delta buyers and delta sellers coloring with voids as black.

It also offers a gradient mode for a beautier visualization

The "Total Volume" mode will display the net volume within the lot size (closes within the levels).

This is useful to spot possible highest net volume within the same highest lot size.

The "POC + Gaps" will show both POC and Gaps as the highest block while all the rest will be considered as the smaller block.

This is useful to see where the highest lot were and if there are higher or lower imbalances within the candle

The last option "Gaps" will simply display the gaps as the highest block, while the POC as the lowest block.

This is useful to have a better view of the gaps areas

🔶 EXAMPLE

This is one of the most basic examples of how this script can be used. POC at the bottom creating a strong support area as price holds and creates higher voids gap that price fills while rising.

🔶 SETTINGS

Users have full control over the script, from colors to choosing the lower-timeframe inputs to disabling the lot size.

Drawdown % (with SMA)This script, titled "Drawdown % (with SMA)" and designed for Pine Script version 5

offers a sophisticated tool for traders to monitor drawdown percentages, a crucial metric in assessing investment risks. The script calculates the drawdown as the percentage decrease from the all-time high value of the selected financial instrument.

Portfolio Management [TrendX_]Portfolio Management is a powerful tool that helps you create and manage your own portfolio of stocks, based on your risk and return preferences.

*** Note: You should select the appropriate index for each stock as the benchmark to compare your portfolio’s performance.

*** Note: You should apply the indicator to the same chart as the benchmark, so that it can capture the historical trends of all the 10 stocks in your portfolio.

USAGE

Analyze your portfolio’s return factor, which shows the compound annual growth rate (CAGR) of each stock and the portfolio as a whole, as well as the weight of each stock in the portfolio.

The Weighting approach contains 2 options, Equal and Growth-based method:

Customize your portfolio by selecting up to 10 stocks from a wide range of markets and sectors:

Compare your portfolio’s performance with a benchmark of your choice, which is the S&P500 by default setting.

Evaluate your portfolio’s risk factor, which includes the capital asset pricing model (CAPM), the portfolio beta, and the Sharpe ratio of both the portfolio and the benchmark:

- CAPM is a model that calculates the expected return of the portfolio based on its risk and the risk-free rate of return.

- Portfolio beta is a measure of how sensitive the portfolio is to the movements of the benchmark. A beta of 1 means the portfolio moves in sync with the benchmark, a beta of less than 1 means the portfolio is less volatile than the benchmark, and a beta of more than 1 means the portfolio is more volatile than the benchmark.

- Sharpe ratio measures how much excess return the portfolio generates per unit of risk. It is calculated by subtracting the risk-free rate of return from the portfolio’s return, and dividing by the portfolio’s standard deviation. A higher Sharpe ratio means the portfolio has a better risk-adjusted return. A Sharpe ratio of more than 1 is considered good, a Sharpe ratio of more than 2 is considered very good, and a Sharpe ratio of more than 3 is considered excellent .

Adjust your portfolio’s rebalancing strategy, which determines when and how to change the weight of each stock in the portfolio to optimize your return and risk objectives. The tool also suggests a default hedging-stock asset, which is the US dollar interpreted through the dollar index (DXY):

- The dollar index is a measure of the value of the US dollar relative to a basket of other major currencies. It is often used as a proxy for the global economic sentiment and the demand for safe-haven assets. A rising dollar index means the US dollar is strengthening, which may indicate a bearish outlook for the stock market. A falling dollar index means the US dollar is weakening, which may indicate a bullish outlook for the stock market.

- The rebalancing strategy suggest increasing the weight of the hedging-stock asset when the dollar index is under positive supertrend condition, and decreasing the weight of the hedging-stock asset when the dollar index is in the downward supertrend. This way, you can hedge against the adverse effects of the stock market fluctuations on your portfolio, simply you can just cash out at the suggested hedging weight.

CONCLUSION

Investors can gain a deeper insight into their portfolio’s performance, risk, and potential, and make informed decisions to achieve their financial goals with confidence and ease.

DISCLAIMER

The results achieved in the past are not all reliable sources of what will happen in the future. There are many factors and uncertainties that can affect the outcome of any endeavor, and no one can guarantee or predict with certainty what will occur.

Therefore, you should always exercise caution and judgment when making decisions based on past performance.

Qullamaggie ADR and Volatility and Price Change IndicatorElevate your trading strategy with Qullamaggie ADR, a dynamic indicator inspired by the Kristjan Qullamaggie trading approach. Gain a deeper understanding of market dynamics, daily price movements, and potential turning points.

Key Features:

Qullamaggie ADR: Assess market volatility through the QullaADR, offering customizable time intervals (5, 10, 15, 20 days) to adapt to various trading styles.

Today's Change: Monitor price changes relative to the low of the current trading day, providing valuable intraday insights.

PrevDay price differentials from the previous day's low, aiding in the identification of potential trend reversals.

Track the percentage change from the opening price, offering a snapshot of intraday market sentiment.

Percent from 10-day SMA: Visualize the percentage difference between the closing price and a 10-day Simple Moving Average (SMA), a key trend-following indicator.

Usage:

Utilize QullaADR to set realistic profit targets and stop-loss levels based on current market conditions.

Identify potential trend shifts by observing changes from the previous day's low with Today's QullaChange.

Incorporate QullaPercent from 10-day SMA for trend confirmation and well-informed trading decisions.

Strategy Inspiration:

QullaADR draws inspiration from the Kristjan Qullamaggie trading strategy, aiming to complement your trading toolkit and enhance decision-making.

Disclaimer:

Trading involves risk, and past performance is not indicative of future results. Use this indicator as a supplementary tool within a comprehensive trading strategy.

Version: 1.0

Sessions [TradingFinder] New York, London, Tokyo & Sydney ForexTiming is one of the influential factors in a trader's position. This indicator categorizes transactions into three sessions (Asia, Europe, and America). Five significant trading cities (New York, London, Frankfurt, Tokyo, and Sydney) are selectable.

I recommend using the tool on a 5-minute time frame, but it is usable on all time frames.

Settings:

• Trading sessions: Display or hide each trading session as needed.

• Color: Change the color of each box.

• Session time intervals: The default is based on the main working hours for each time interval and can be adjusted.

• Information table: Delete or display additional information table.

Information Table:

• Trading sessions

• Opening and closing times of each trading session

How to Use:

Initiating trading sessions involves entering with increased liquidity, and the market usually experiences significant movements. Many trading strategies are based on "time" and "session openings." This tool empowers traders to focus intensely on each time interval.

These trading sessions are crucial for all Forex, stock, and index traders:

The total price ceiling and floor in the Asia session (Tokyo and Sydney) are crucial for traders in the European session.

The European session starts with Frankfurt, and an hour later, London begins, collectively forming the European session.

The dashboard provides additional information, displaying hours based on UTC.

Customization options are considered in all sections so that everyone can apply their own settings.

Important: Default times are the most accurate for each region, and in most indicators, this time is not correctly selected. Therefore, the level of influence and time intervals are specified at the beginning of each session. If you are using another indicator, match its default time to the announced time and share the results with me in the comments.

Kendall's Tau Correlation Regimes [NariCapitalTrading]The "Kendall's Tau Correlation Regimes" indicator is designed to analyze price data and determine market regimes based on Kendall's Tau correlation coefficient. It provides insight into the strength and direction of the correlation between two data series: close price and a selected moving average.

User Inputs:

Period: Defines the lookback period for calculating Kendall's Tau correlation. It can be adjusted using the input slider, with a minimum value of 1.

Threshold: Sets the threshold for identifying bullish and bearish market regimes. The user can adjust this value within the range of 0.1 to 1.0 with step increments of 0.1.

MA Type: Allows users to select the type of moving average to be used in the correlation calculation. Options include Simple Moving Average (SMA), Exponential Moving Average (EMA), and Hull Moving Average (HMA).

Kendall's Tau Correlation Calculation:

Calculates Kendall's Tau correlation coefficient between the closing price and the selected moving average.

Kendall's Tau measures the strength and direction of the ordinal association between two data series. It assesses whether the data pairs are in the same order or not.

The calculation involves counting concordant and discordant pairs of data points and then computing the coefficient.

Market Regime Identification:

Based on the threshold defined by the user, the indicator identifies two market regimes: bullish and bearish.

A regime is considered bullish when the Kendall's Tau correlation coefficient is greater than the threshold.

A regime is considered bearish when the Kendall's Tau correlation coefficient is less than the negative of the threshold.

Plotting:

The indicator plots the calculated Kendall's Tau correlation coefficient as a blue line on a separate indicator pane.

It also highlights bullish regimes with a green background and bearish regimes with a red background.

Conclusion:

The "Kendall's Tau Correlation Regimes" indicator provides traders with a visual aid for assessing market regimes based on the strength of correlation between price and a selected moving average.

Disclaimer: This indicator is for educational and informational purposes only.