multi-tf standard devs [keypoems]Multi-Timeframe Standard Deviations Levels

A visual map of “how far is too far” across any three higher time-frames.

1. What it does

This script plots dynamic price “rails” built from standard deviation (StDev)—the same math that underpins the bell curve—on up to three higher-time-frames (HTFs) at once.

• It measures the volatility of intraday open-to-close increments, reaching back as far as 5000 bars (≈ 20 years on daily data).

• Each HTF can be extended to the next session or truncated at session close for tidy dashboards.

• Lines can be mirrored so you see symmetric positive/negative bands, and optional background fills shade the “probability cone.”

Because ≈ 68 % of moves live inside ±1 StDev, ≈ 95 % inside ±2, and ≈ 99.7 % inside ±3, the plot instantly shows when price is statistically stretched or compressed.

3. Key settings

Higher Time-Frame #1-3 Turn each HTF on/off, pick the interval (anything from 1 min to 1 year), and decide whether lines should extend into the next period.

Show levels for last X days Keep your chart clean by limiting how many historical sessions are displayed (1-50).

Based on last X periods Length of the StDev sample. Long look-backs (e.g. 5 000) iron-out day-to-day noise; short look-backs make the bands flex with recent volatility.

Fib Settings Toggle each multiple, line thickness/style/colour, label size, whether to print the numeric level, the live price, the HTF label, and whether to tint the background (choose your own opacity).

4. Under-the-hood notes

StDev is calculated on (close – open) / open rather than absolute prices, making the band width scale-agnostic.

Watch for tests of ±1:

Momentum traders ride the breakout with a target at the next band.

Mean-reversion traders wait for the first stall candle and trade back to zero line or VWAP.

Bottom line: Multi-Timeframe Standard-Deviations turns raw volatility math into an intuitive “price terrain map,” helping you instantly judge whether a move is ordinary, stretched, or extreme—across the time-frames that matter to you.

Original code by fadizeidan and stats by NQStats's ProbableChris.

Statistics

Bullish Volume AnomalyAnomaly is designed to spot hidden bullish accumulation before price actually breaks out, by blending a trend-aware volume measure with a volatility-adjusted price channel. Here’s how it works:

First, it runs a simple ATR-based zigzag to identify the current swing direction. Volume is then signed (+ for up-trends, – for down-trends) and cumulatively summed. By converting that cumulative signed volume into a z-score over the past 480 bars, we get a sense of when buying or selling pressure is unusually strong relative to its own history.

At the same time, price itself is normalized into a z-score over the same 480-bar window, and its change over that period is also tracked. These two measures—volume z-score (s) and price z-score (p)—are compared, and the indicator looks for moments when s outpaces p by at least two standard deviations (s – p > 2), while price momentum change remains low (c < 1) and the net volume is positive (s > 0). That combination flags instances where heavy buying is taking place but price hasn’t yet reacted.

To define a dynamic trading zone, it plots a 288-bar EMA of price as the middle band (t2), and builds upper and lower bands around it using the average close-to-open range multiplied by a user-set factor. The lower band (t1) sits beneath the EMA by that volatility-based margin. A signal fires only when the bar’s high stays below t1—meaning price is still “sleeping” under the lower volatility boundary even as bullish volume builds up.

Together, these filters home in on anomalies: strong, trend-aligned volume surges that outstrip price movement, occurring while price sits below its lower volatility band. In practice, that often marks early accumulation before a breakout. You can tweak the ATR length and multiplier for the zigzag, as well as the channel period and range factor, to suit different markets or timeframes.

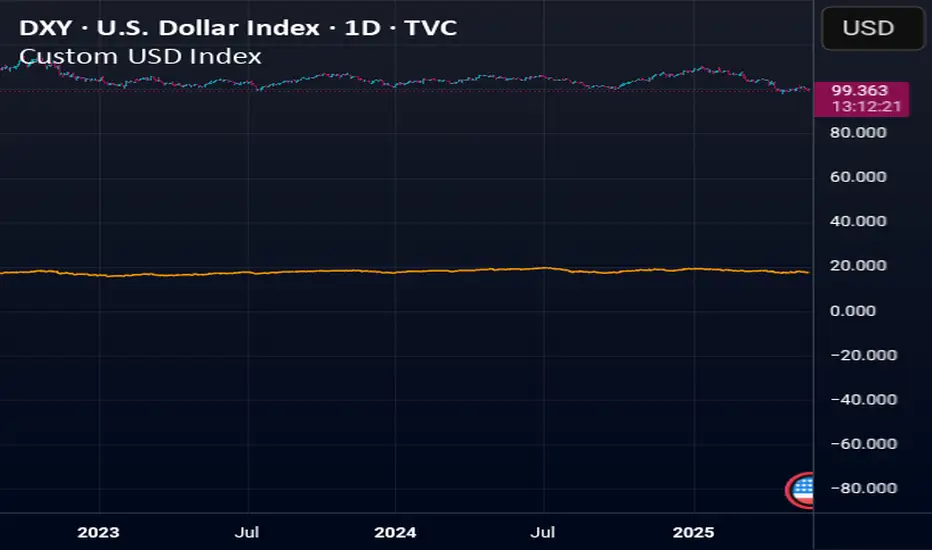

Normalized DXY+Custom USD Index (DXY+) – Normalized Dollar Strength with Bitcoin, Gold, and Yuan.

This custom USD strength index replicates the structure of the official U.S. Dollar Index (DXY), while expanding it to include modern financial assets such as Bitcoin (BTC), Ethereum (ETH), gold (XAU), and the Chinese yuan (CNY).

Weights for the core fiat currencies (EUR, JPY, GBP, CAD, SEK, CHF) follow the official ICE DXY methodology. Additional components are weighted proportionally based on their estimated global economic influence.

The index is normalized from its initial valid data point, meaning it starts at 100 on the first day all asset inputs are available. From that point forward, it tracks the relative strength of the U.S. dollar against this expanded basket.

This provides a more comprehensive and modernized view of the dollar's strength—not only against traditional fiat currencies, but also in the context of rising decentralized assets and non-Western trade power.

HGDA Hany Ghazy Digital Analytics area zone'sIndicator Name: HGDA Hany Ghazy Digital Analytics area zones

Description:

This indicator plots several key price zones based on the highest high and lowest low over a user-defined lookback period.

The plotted zones represent dynamic support and resistance levels calculated using specific ratios of the price range (High - Low), as follows:

- Zone 1 (Light Red): Represents an upper resistance zone.

- Zone 2 (Medium Green): Represents a medium support zone.

- Zone 3 (Dark Red): Represents a lower resistance zone.

- Zone 4 (Dark Green): Represents a strong support zone.

Additionally, the indicator plots a yellow "Zero" line representing the midpoint price of the selected period, serving as a balance point for price action.

This indicator is ideal for identifying the overall market trend, as prices typically move from the upper resistance zones (light red) downwards to the end of the wave in the lower zones (dark green). This helps traders better understand wave nature and direction.

Usage:

- The colored zones assist in identifying potential reversal or continuation areas.

- These zones can be used to plan entries, exits, and risk management.

- Default lookback period is 20 bars, adjustable in the settings to suit the timeframe.

Notes:

- This indicator relies on historical price data and does not guarantee market predictions.

- It is recommended to combine it with other indicators and analytical tools for improved trading decisions.

---

Developed by Hany Ghazy Digital Analytics (HGDA).

Custom USD IndexThis is a modernized, expanded version of the U.S. Dollar Index (DXY), designed to provide a more accurate representation of the dollar’s global strength in today’s diversified economy.

Unlike the traditional DXY, which excludes major players like China and entirely omits real-world stores of value, this custom index (DXY+) includes:

Fiat Currencies (78.3% total weight):

EUR, JPY, GBP, CAD, AUD, CHF, and CNY — equally weighted to reflect the global currency landscape.

Gold (17.5%):

Gold (XAUUSD) is included as a traditional reserve asset and inflation hedge, acknowledging its continued monetary relevance.

Cryptocurrencies (2.8% total weight):

Bitcoin (BTC) and Ethereum (ETH) represent the emerging digital monetary layer.

The index rises when the U.S. dollar strengthens relative to this blended basket, and falls when the dollar weakens against it. This is ideal for traders, economists, and macro analysts seeking a more inclusive and up-to-date measure of dollar performance.

Float, Daily % Change & Short %This TradingView Pine Script displays a compact table on your chart showing four key metrics for any stock:

📊 What It Shows:

Float – Number of publicly available shares, formatted in K/M/B.

Daily % Change – Price change from yesterday’s close to the current price.

Intraday % Change – Price change from today’s open to the current price.

Short Volume % – Estimated short volume as a percentage of total daily volume.

⚙️ How to Use:

Add the script to your TradingView chart.

Choose table size and screen position from the settings panel.

The values update in real-time on the latest candle only, so they stay out of the way but always visible.

Ideal for momentum traders, short float hunters, and day traders who need quick access to real-time float, price action, and short volume stats.

SOFR Spread (proxy: FEDFUNDS - US03MY)📊 SOFR Spread (Proxy: FEDFUNDS - US03MY) – Monitoring USD Money Market Liquidity

In 2008, the spread exhibits a sharp vertical spike, signaling a severe liquidity dislocation: investors rushed into short-term U.S. Treasuries, pushing their yields down dramatically, while the FEDFUNDS rate remained relatively high.

This behavior indicates extreme systemic stress in the interbank lending market, preceding massive Federal Reserve interventions such as rate cuts, emergency liquidity operations, and the launch of quantitative easing (QE).

Description:

This indicator plots the spread between the Effective Federal Funds Rate (FEDFUNDS) and the 3-Month US Treasury Bill yield (US03MY), used here as a proxy for the SOFR spread.

It serves as a simple yet powerful tool to detect liquidity dislocations and stress signals in the US short-term funding markets.

Interpretation:

🔴 Spread > 0.20% → Possible liquidity stress: elevated repo rates, cash shortage, interbank distrust.

🟡 Spread ≈ 0% → Normal market conditions, balanced liquidity.

🟢 Spread < 0% → Excess liquidity: strong demand for T-Bills, “flight to safety”, or distortion due to expansionary monetary policy.

Ideal for:

Monitoring Fed policy impact

Anticipating market-wide liquidity squeezes

Correlation with DXY, SPX, VIX, MOVE Index, and risk sentiment

🧠 Note: As SOFR is not directly available on TradingView, FEDFUNDS is used as a reliable proxy, closely tracking the same trends in most macro conditions.

LANZ Strategy 2.0 [Backtest]🔷 LANZ Strategy 2.0 — Structural Breakout Logic with Dynamic Swing Protection

LANZ Strategy 2.0 is a precision-focused backtesting system built for intraday traders who rely on structural confirmations before the London session to guide directional bias. This tool uses smart swing detection, risk-defined position sizing, and strict time-based execution to simulate real trading conditions with clarity and control.

🧠 Core Components:

Structural Confirmation (Trend & BoS): Detects trend direction and break of structure (BoS) using a three-swing logic, aligning trade entries with valid structural movement.

Time-Based Execution: Trades are triggered exclusively at 02:00 a.m. New York time, ensuring disciplined and repeatable intraday testing.

Swing-Based SL Models: Traders can select between three stop-loss protection types:

First Swing: Most recent structural level

Second Swing: Prior level

Full Coverage: All recent swing levels + configurable pip buffer

Dynamic TP Calculation: Take-Profit is projected as a risk-based multiple (RR), fully adjustable via input.

Capital-Based Risk Management: Risk is defined as a percentage of a fixed account size (e.g., $100 per trade from $10,000), and lot size is automatically calculated based on SL distance.

Fallback Entry Logic: If structural breakout is present but trend is not confirmed, a secondary entry is triggered.

End-of-Session Management: Any open trades are automatically closed at 11:45 a.m. NY time, with optional manual labeling or review.

📊 Visual Features (Optional in Indicator Version):

(Note: Visuals apply to the indicator version of LANZ 2.0, not this backtest script)

Swing level labels (1st, 2nd) and dynamic SL/TP lines.

Real-time session coloring for clarity: Pre-London, Entry Window, and NY Close.

Outcome labels: +RR, -RR, or net % at close.

Auto-cleanup of previous drawings for a clean chart per session.

⚙️ How It Works:

Detects last trend and BoS using swing logic before 02:00 a.m. NY.

At 02:00 a.m., evaluates directional bias and executes BUY or SELL if confirmed.

Applies selected SL logic (1st, 2nd, or full swing protection).

Sets TP based on the RR multiplier.

Closes the trade either on SL, TP, or at 11:45 a.m. NY manually.

🔔 Alerts:

Time-of-day alert at 02:00 a.m. NY to monitor execution.

Can be extended to cover SL/TP triggers or new BoS events.

📝 Notes:

Designed for backtesting precision and discretionary decision-making.

Ideal for Forex pairs, indices, or assets active during the London session.

Fully customizable: session timing, swing logic, SL buffer, and RR.

👤 Credits:

Strategy built by @rau_u_lanz using Pine Script v6, combining structural logic, capital-based risk control, and London-session timing in a backtest-ready framework for traders who demand accuracy and structure.

Statistical Pairs Trading IndicatorZ-Score Stat Trading — Statistical Pairs Trading Indicator

📊🔗

---

What is it?

Z-Score Stat Trading is a powerful indicator for statistical pairs trading and quantitative analysis of two correlated assets.

It calculates the Z-Score of the log-price spread between any two symbols you choose, providing both long-term and short-term Z-Score signals.

You’ll also see real-time correlation, volatility, spread, and the number of long/short signals in a handy on-chart table!

---

How to Use 🛠️

1. Add the indicator to your chart.

2. Select two assets (symbols) to analyze in the settings.

3. Watch the Z-Score plots (blue and orange lines) and threshold levels (+2, -2 by default).

4. Check the info table for:

- Correlation

- Volatility

- Spread

- Number of long (NL) and short (NS) signals in the last 1000 bars

5. Set up alerts for signal generation or threshold crossings if you want to be notified automatically.

---

Trading Strategy 💡

- This indicator is designed for statistical arbitrage (mean reversion) strategies.

- Long Signal (🟢):

When both Z-Scores drop below the negative threshold (e.g., -2), a long signal is generated.

→ Buy Symbol A, Sell Symbol B, expecting the spread to revert to the mean.

- Short Signal (🔴):

When both Z-Scores rise above the positive threshold (e.g., +2), a short signal is generated.

→ Sell Symbol A, Buy Symbol B, again expecting mean reversion.

- The info table helps you quickly assess the frequency of signals and the current statistical relationship between your chosen assets.

---

Best Practices & Warnings 🚦

- Avoid high leverage! Pairs trading can be risky, especially during periods of divergence. Use conservative position sizing.

- Check for cointegration: Before using this indicator, make sure both assets are cointegrated or have a strong historical relationship. This increases the reliability of mean reversion signals.

- Check correlation: Only use asset pairs with a high correlation (preferably 0.8–0.9 or higher) for best results. The correlation value is shown in the info table.

- Scale in and out gradually: When entering or exiting positions, consider doing so in parts rather than all at once. This helps manage slippage and risk, especially in volatile markets.

---

⚠️ Note on Performance:

This indicator may work a bit slowly, especially on large timeframes or long chart histories, because the calculation of NL and NS (number of long/short signals) is computationally intensive.

---

Disclaimer ⚠️

This script is provided for educational and informational purposes only .

It is not financial advice or a recommendation to buy or sell any asset.

Use at your own risk. The author assumes no responsibility for any trading decisions or losses.

Fibo Normalized RSI & RSI RibbonPlots both standard and Z-score normalized RSI ribbons using Fibonacci-based periods. Supports adjustable normalization, optional 0–100 scaling, and multi-line visualizations for momentum and deviation analysis.

This tool is designed for traders who want to go beyond standard RSI by adding:

Statistical normalization (Z-score)

Multi-period analysis (Fibonacci structure)

Advanced divergence and exhaustion detection

It gives you both classical momentum context and mathematically rigorous deviation insight, making it ideal for:

Swing traders

Quant-inclined discretionary traders

Multi-timeframe analysts

Trend Confirmation

When both RSI and normalized RSI across short and long periods are stacked in the same direction (e.g., above 50 or with high Z-scores), the trend is likely strong.

Disagreement between the two ribbons (e.g., RSI high but normalized RSI flat) may indicate late-stage trend or false strength.

Mean Reversion Trades

Look for normalized RSI values > +2 or < -2 (i.e., ~2 standard deviations).

Cross-check with standard RSI to see if the move aligns with a traditional overbought/oversold level.

Great for fade/reversal setups when Z-score RSI is extreme but classic RSI is just beginning to turn.

Divergence Detection

Compare the slope of RSI vs. normalized RSI over same period:

If RSI is rising but normalized RSI is falling → momentum is fading despite apparent strength.

Excellent for early warnings before reversals.

Multi-Timeframe Confluence

Use short-period ribbons (e.g., 3–13) for tactical entries/exits.

Use long-period ribbons (e.g., 55–233) for macro trend bias.

Alignment across both = high-confidence zone.

Risk Calculator PRO — manual lot size + auto lot-suggestionWhy risk management?

90 % of traders blow up because they size positions emotionally. This tool forces Risk-First Thinking: choose the amount you’re willing to lose, and the script reverse-engineers everything else.

Key features

1. Manual or Market Entry – click “Use current price” or type a custom entry.

2. Setup-based ₹-Risk – four presets (A/B/C/D). Edit to your workflow.

3. Lot-Size Input + Auto Lot Suggestion – you tell the contract size ⇒ script tells you how many lots.

4. Auto-SL (optional) – tick to push stop-loss to exactly 1-lot risk.

5. Instant Targets – 1 : 2, 1 : 3, 1 : 4, 1 : 5 plotted and alert-ready.

6. P&L Preview – table shows potential profit at each R-multiple plus real ₹ at SL.

7. Margin Column – enter per-lot margin once; script totals it for any size.

8. Clean Table UI – dark/light friendly; updates every 5 bars.

9. Alert Pack – SL, each target, plus copy-paste journal line on the chart.

How to use

1. Add to chart > “Format”.

2. Type the lot size for the symbol (e.g., 1250 for Natural Gas, 1 for cash equity).

3. Pick Side (Buy / Sell) & Setup grade.

4. ✅ If you want the script to place SL for you, tick Auto-SL (risk = 1 lot).

5. Otherwise type your own Stop-loss.

6. Read the table:

• Suggested lots = how many to trade so risk ≤ setup ₹.

• Risk (currency) = real money lost if SL hits.

7. Set TradingView alerts on the built-in conditions (T1_2, SL_hit, etc.) if you’d like push / email.

8. Copy the orange CSV label to Excel / Sheets for journalling.

Best practices

• Never raise risk to “fit” a trade. Lower size instead.

• Review win-rate vs. R multiple monthly; adjust setups A–D accordingly.

• Test Auto-SL in replay before going live.

Disclaimer

This script is educational. Past performance ≠ future results. The author isn’t responsible for trading losses.

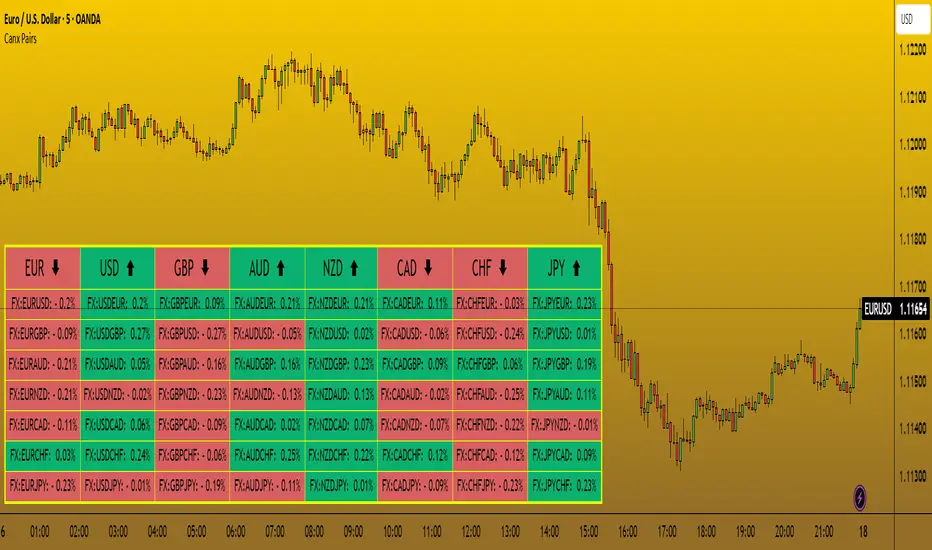

CANX Pairs Table© CanxStixTrader

This Indicator simply shows the change in movement of all the major currency pairs using custom time frames and percentage.

Customize time frame, background, text colors and indicator location to suit.

Keep it simple!

Index Futures vs Cash ArbitrageThis indicator measures the statistical spread between major stock index futures and their corresponding cash indices (e.g., ES vs SPX, NQ vs NDX) using Z-score normalization. It automatically detects commonly traded index pairs (S&P 500, Nasdaq, Dow Jones, Russell 2000) and calculates a smoothed spread between futures and spot prices. A Z-score is then derived from this spread to highlight potential overpricing or underpricing conditions.

Traders can use customizable thresholds to identify mean-reversion opportunities where the futures contract may be temporarily overvalued or undervalued relative to the index. The histogram highlights the direction of the Z-score (green = futures > index, red = futures < index), while built-in alerts notify users of key threshold breaches or zero-line crosses.

This tool is designed for discretionary traders, pairs traders, or anyone exploring statistical arbitrage strategies between futures and spot markets. It is not a buy/sell signal by itself and should be used with additional confluence or risk management techniques.

Seasonality DOW CombinedOverall Purpose

This script analyzes historical daily returns based on two specific criteria:

Month of the year (January through December)

Day of the week (Sunday through Saturday)

It summarizes and visually displays the average historical performance of the selected asset by these criteria over multiple years.

Step-by-Step Breakdown

1. Initial Settings:

Defines minimum year (i_year_start) from which data analysis will start.

Ensures the user is using a daily timeframe, otherwise prompts an error.

Sets basic display preferences like text size and color schemes.

2. Data Collection and Variables:

Initializes matrices to store and aggregate returns data:

month_data_ and month_agg_: store monthly performance.

dow_data_ and dow_agg_: store day-of-week performance.

COUNT tracks total number of occurrences, and COUNT_POSITIVE tracks positive-return occurrences.

3. Return Calculation:

Calculates daily percentage change (chg_pct_) in price:

chg_pct_ = close / close - 1

Ensures it captures this data only for the specified years (year >= i_year_start).

4. Monthly Performance Calculation:

Each daily return is grouped by month:

matrix.set updates total returns per month.

The script tracks:

Monthly cumulative returns

Number of occurrences (how many days recorded per month)

Positive occurrences (days with positive returns)

5. Day-of-Week Performance Calculation:

Similarly, daily returns are also grouped by day-of-the-week (Sunday to Saturday):

Daily return values are summed per weekday.

The script tracks:

Cumulative returns per weekday

Number of occurrences per weekday

Positive occurrences per weekday

6. Visual Display (Tables):

The script creates two visual tables:

Left Table: Monthly Performance.

Right Table: Day-of-the-Week Performance.

For each table, it shows:

Yearly data for each month/day.

Summaries at the bottom:

SUM row: Shows total accumulated returns over all selected years for each month/day.

+ive row: Shows percentage (%) of times the month/day had positive returns, along with a tooltip displaying positive occurrences vs total occurrences.

Cells are color-coded:

Green for positive returns.

Red for negative returns.

Gray for neutral/no change.

7. Interpreting the Tables:

Monthly Table (left side):

Helps identify seasonal patterns (e.g., historically bullish/bearish months).

Day-of-Week Table (right side):

Helps detect recurring weekday patterns (e.g., historically bullish Mondays or bearish Fridays).

Practical Use:

Traders use this to:

Identify patterns based on historical data.

Inform trading strategies, e.g., avoiding historically bearish days/months or leveraging historically bullish periods.

Example Interpretation:

If the table shows consistently green (positive) for March and April, historically the asset tends to perform well during spring. Similarly, if the "Friday" column is often red, historically Fridays are bearish for this asset.

Crypto_in_details_MAlibCrypto_in_details_MaLib — Advanced Moving Average Library for Pine Script

Overview:

Crypto_in_details_MaLib is a comprehensive, performance-optimized Moving Average (MA) library designed specifically for Pine Script v6 users seeking advanced technical analysis tools. Developed by Crypto_in_details, this library consolidates the most popular and sophisticated MA calculation methods — including classical, weighted, exponential, and Hull variants — into one seamless package.

Key Features:

Implements a wide range of Moving Averages: SMA, EMA, WMA, RMA, VWMA, HMA, TEMA, EHMA, THMA.

Designed for precision and flexibility — suitable for diverse trading strategies and indicator development.

Fully typed functions compatible with Pine Script v6 standards.

Simplifies your scripting workflow by providing ready-to-use MA functions via clean and easy-to-import methods.

Well-documented and maintained by an experienced Pine Script developer.

Why Use Crypto_in_details_MaLib?

Gain access to advanced MA calculations that enhance trend analysis, smoothing, and signal accuracy.

Save time on coding complex moving averages from scratch.

Easily extend or combine with your own strategies or indicators for improved performance.

Rely on a tested and community-driven solution backed by a prolific Pine Script author.

Ideal for:

Traders and developers building custom indicators or strategies requiring versatile MA techniques.

Anyone looking to improve their Pine Script efficiency and code maintainability.

Pine Script enthusiasts wanting a professional-grade MA toolkit.

VolumeFlowOscillatorLibVolume Flow Oscillator Library

Overview

The Volume Flow Oscillator library provides a comprehensive framework for analyzing directional volume flow in financial markets. It creates a multi-band oscillator system that transforms price and volume data into a spectrum of sensitivity bands, revealing the underlying buying and selling pressure.

Technical Approach

The library combines price direction with trading volume to generate an oscillator that fluctuates around a zero line, with positive values indicating buying pressure and negative values showing selling pressure. Using sophisticated ALMA (Arnaud Legoux Moving Average) smoothing techniques with asymmetric sensitivity, the library creates seven distinct bands that help identify various intensity levels of volume flow.

Key Features

Multi-band oscillator system with seven sensitivity levels

Directional volume flow analysis combining price movement and volume

Zero-line oscillation showing the balance between buying and selling pressure

Asymmetric ALMA smoothing for different sensitivity on positive/negative bands

Customizable lookback periods and multipliers for fine-tuning

Color-coded visualization for intuitive chart reading

Applications

This library offers developers a versatile foundation for creating volume-based indicators that go beyond simple volume measurement to reveal the directional force behind market movements. Ideal for confirming price trends, detecting divergences, identifying volume climaxes, and assessing overall market strength.

MVRV | Lyro RS📊 MVRV | Lyro RS is a powerful on-chain valuation tool designed to assess the relative market positioning of Bitcoin (BTC) or Ethereum (ETH) based on the Market Value to Realized Value (MVRV) ratio. It highlights potential undervaluation or overvaluation zones, helping traders and investors anticipate cyclical tops and bottoms.

✨ Key Features :

🔁 Dual Asset Support: Analyze either BTC or ETH with a single toggle.

📐 Dynamic MVRV Thresholds: Automatically calculates median-based bands at 50%, 64%, 125%, and 170%.

📊 Median Calculation: Period-based median MVRV for long-term trend context.

💡 Optional Smoothing: Use SMA to smooth MVRV for cleaner analysis.

🎯 Visual Threshold Alerts: Background and bar colors change based on MVRV position relative to thresholds.

⚠️ Built-in Alerts: Get notified when MVRV enters under- or overvalued territory.

📈 How It Works :

💰 MVRV Calculation: Uses data from IntoTheBlock and CoinMetrics to obtain real-time MVRV values.

🧠 Threshold Bands: Median MVRV is used as a baseline. Ratios like 50%, 64%, 125%, and 170% signal various levels of market extremes.

🎨 Visual Zones: Green zones for undervaluation and red zones for overvaluation, providing intuitive visual cues.

🛠️ Custom Highlights: Toggle individual threshold zones on/off for a cleaner view.

⚙️ Customization Options :

🔄 Switch between BTC or ETH for analysis.

📏 Adjust period length for median MVRV calculation.

🔧 Enable/disable threshold visibility (50%, 64%, 125%, 170%).

📉 Toggle smoothing to reduce noise in volatile markets.

📌 Use Cases :

🟢 Identify undervalued zones for long-term entry opportunities.

🔴 Spot potential overvaluation zones that may precede corrections.

🧭 Use in confluence with price action or macro indicators for better timing.

⚠️ Disclaimer :

This indicator is for educational purposes only. It should not be used in isolation for making trading or investment decisions. Always combine with price action, fundamentals, and proper risk management.

Anchored Probability Cone by TenozenFirst of all, credit to @nasu_is_gaji for the open source code of Log-Normal Price Forecast! He teaches me alot on how to use polylines and inverse normal distribution from his indicator, so check it out!

What is this indicator all about?

This indicator draws a probability cone that visualizes possible future price ranges with varying levels of statistical confidence using Inverse Normal Distribution , anchored to the start of a selected timeframe (4h, W, M, etc.)

Feutures:

Anchored Cone: Forecasts begin at the first bar of each chosen higher timeframe, offering a consistent point for analysis.

Drift & Volatility-Based Forecast: Uses log returns to estimate market volatility (smoothed using VWMA) and incorporates a trend angle that users can set manually.

Probabilistic Price Bands: Displays price ranges with 5 customizable confidence levels (e.g., 30%, 68%, 87%, 99%, 99,9%).

Dynamic Updating: Recalculates and redraws the cone at the start of each new anchor period.

How to use:

Choose the Anchored Timeframe (PineScript only be able to forecast 500 bars in the future, so if it doesn't plot, try adjusting to a lower anchored period).

You can set the Model Length, 100 sample is the default. The higher the sample size, the higher the bias towards the overall volatility. So better set the sample size in a balanced manner.

If the market is inside the 30% conifidence zone (gray color), most likely the market is sideways. If it's outside the 30% confidence zone, that means it would tend to trend and reach the other probability levels.

Always follow the trend, don't ever try to trade mean reversions if you don't know what you're doing, as mean reversion trades are riskier.

That's all guys! I hope this indicator helps! If there's any suggestions, I'm open for it! Thanks and goodluck on your trading journey!

BPCO Z-ScoreBPCO Z-Score with Scaled Z-Value and Table

Description:

This custom indicator calculates the Z-Score of a specified financial instrument (using the closing price as a placeholder for the BPCO value), scales the Z-Score between -2 and +2 based on user-defined thresholds, and displays it in a table for easy reference.

The indicator uses a simple moving average (SMA) and standard deviation to calculate the original Z-Score, and then scales the Z-Score within a specified range (from -2 to +2) based on the upper and lower thresholds set by the user.

Additionally, the scaled Z-Score is displayed in a separate table on the right side of the chart, providing a clear, numerical value for users to track and interpret.

Key Features:

BPCO Z-Score: Calculates the Z-Score using a simple moving average and standard deviation over a user-defined window (default: 365 days). This provides a measure of how far the current price is from its historical average in terms of standard deviations.

Scaled Z-Score: The original Z-Score is then scaled between -2 and +2, based on the user-specified upper and lower thresholds. The thresholds default to 3.5 (upper) and -1.5 (lower), and can be adjusted as needed.

Threshold Bands: Horizontal lines are plotted on the chart to represent the upper and lower thresholds. These help visualize when the Z-Score crosses critical levels, indicating potential market overbought or oversold conditions.

Dynamic Table Display: The scaled Z-Score is shown in a dynamic table at the top-right of the chart, providing a convenient reference for traders. The table updates automatically as the Z-Score fluctuates.

How to Use:

Adjust Time Window: The "Z-Score Period (Days)" input allows you to adjust the time period used for calculating the moving average and standard deviation. By default, this is set to 365 days (1 year), but you can adjust this depending on your analysis needs.

Set Upper and Lower Thresholds: Use the "BPCO Upper Threshold" and "BPCO Lower Threshold" inputs to define the bands for your Z-Score. The default values are 3.5 for the upper band and -1.5 for the lower band, but you can adjust them based on your strategy.

Interpret the Z-Score: The Z-Score provides a standardized measure of how far the current price (or BPCO value) is from its historical mean, relative to the volatility. A value above the upper threshold (e.g., 3.5) may indicate overbought conditions, while a value below the lower threshold (e.g., -1.5) may indicate oversold conditions.

Use the Scaled Z-Score: The scaled Z-Score is calculated based on the original Z-Score, but it is constrained to a range between -2 and +2. When the BPCO value hits the upper threshold (3.5), the scaled Z-Score will be +2, and when it hits the lower threshold (-1.5), the scaled Z-Score will be -2. This gives you a clear, easy-to-read value to interpret the market's condition.

Data Sources:

BPCO Data: In this indicator, the BPCO value is represented by the closing price of the asset. The calculation of the Z-Score and scaled Z-Score is based on this price data, but you can modify it to incorporate other data streams as needed (e.g., specific economic indicators or custom metrics).

Indicator Calculation: The Z-Score is calculated using the following formulas:

Mean (SMA): A simple moving average of the BPCO (close price) over the selected period (365 days by default).

Standard Deviation (Std): The standard deviation of the BPCO (close price) over the same period.

Z-Score: (Current BPCO - Mean) / Standard Deviation

Scaled Z-Score: The Z-Score is normalized to fall within a specified range (from -2 to +2), based on the upper and lower threshold inputs.

Important Notes:

Customization: The indicator allows users to adjust the period (window) for calculating the Z-Score, as well as the upper and lower thresholds to suit different timeframes and trading strategies.

Visual Aids: Horizontal lines are drawn to represent the upper and lower threshold levels, making it easy to visualize when the Z-Score crosses critical levels.

Limitations: This indicator relies on historical price data (or BPCO) and assumes that the standard deviation and mean are representative of future price behavior. It does not account for potential market shifts or extreme events that may fall outside historical norms.

SOPR with Z-Score Table📊 Glassnode SOPR with Dynamic Z-Score Table

ℹ️ Powered by Glassnode On-Chain Metrics

📈 Description:

This indicator visualizes the Spent Output Profit Ratio (SOPR) for major cryptocurrencies — Bitcoin, Ethereum, and Litecoin — along with a dynamically normalized Z-Score. SOPR is a key on-chain metric that reflects whether coins moved on-chain are being sold at a profit or a loss.

🔍 SOPR is calculated using Glassnode’s entity-adjusted SOPR feed, and a custom SMA is applied to smooth the signal. The normalized Z-Score helps identify market sentiment extremes by scaling SOPR relative to its historical context.

📊 Features:

Selectable cryptocurrency: Bitcoin, Ethereum, or Litecoin

SOPR smoothed by user-defined SMA (default: 10 periods)

Upper & lower bounds (±4%) for SOPR, shown as red/green lines

Background highlighting when SOPR moves outside normal range

Normalized Z-Score scaled between –2 and +2

Live Z-Score display in a compact top-right table

🧮 Calculations:

SOPR data is sourced daily from Glassnode:

Bitcoin: XTVCBTC_SOPR

Ethereum: XTVCETH_SOPR

Litecoin: XTVCLTC_SOPR

Z-Score is calculated as:

SMA of SOPR over zscore_length periods

Standard deviation of SOPR

Z-Score = (SOPR – mean) / standard deviation

Z-Score is clamped between –2 and +2 for visual consistency

🎯 Interpretation:

SOPR > 1 implies coins are sold in profit

SOPR < 1 suggests coins are sold at a loss

When SOPR is significantly above or below its recent range (e.g., +4% or –4%), it may signal overheating or capitulation

The Z-Score contextualizes how extreme the current SOPR is relative to history

📌 Notes:

Best viewed on daily charts

Works across selected assets (BTC, ETH, LTC)

MVRVZ BTCMVRVZ BTC (Market Value to Realized Value Z-Score)

Description:

The MVRVZ BTC indicator provides insights into the relationship between the market value and realized value of Bitcoin, using the Market Value to Realized Value (MVRV) ratio, which is then adjusted using a Z-Score. This indicator highlights potential market extremes and helps in identifying overbought or oversold conditions, offering a unique perspective on Bitcoin's valuation.

How It Works:

MVRVZ is calculated by taking the difference between Bitcoin's Market Capitalization (MC) and Realized Capitalization (MCR), then dividing that by the Standard Deviation (Stdev) of the price over a specified period (usually 104 weeks).

The resulting value is plotted as the MVRVZ line, representing how far the market price deviates from its realized value.

Z-Score is then applied to the MVRVZ line, with the Z-Score bounded between +2 and -2, which allows it to be used within a consistent evaluation framework, regardless of how high or low the MVRVZ line goes. The Z-Score will reflect overbought or oversold conditions:

A Z-Score above +2 indicates the market is likely overbought (possible market top).

A Z-Score below -2 indicates the market is likely oversold (possible market bottom).

Values between -2 and +2 indicate more neutral market conditions.

How to Read the Indicator:

MVRVZ Line:

The MVRVZ line shows the relationship between market cap and realized cap. A higher value indicates the market is overvalued relative to the actual capital realized by holders.

The MVRVZ line can move above or below the top and bottom lines you define, which are adjustable according to your preferences. These lines act as trigger levels.

Top and Bottom Trigger Lines:

You can customize the Top Line and Bottom Line values to your preference.

When the MVRVZ line crosses the Top Line, the market might be considered overbought.

When the MVRVZ line crosses the Bottom Line, the market might be considered oversold.

SCDA Z-Score:

The Z-Score is displayed alongside the MVRVZ line and is bounded between -2 and +2. It scales proportionally based on the MVRVZ line's position relative to the top and bottom trigger lines.

The Z-Score ensures that even if the MVRVZ line moves beyond the trigger lines, the Z-Score will stay within the limits of -2 to +2, making it ideal for your custom evaluation system (SCDA).

Background Highlighting:

The background color changes when the MVRVZ line crosses key levels:

When the MVRVZ line exceeds the Top Trigger, the background turns red, indicating overbought conditions.

When the MVRVZ line falls below the Bottom Trigger, the background turns green, indicating oversold conditions.

Data Sources:

The data for the MVRVZ indicator is sourced from Glassnode and Coinmetrics, which provide the necessary values for:

BTC Market Cap (MC) – The total market capitalization of Bitcoin.

BTC Realized Market Cap (MCR) – The capitalization based on the price at which Bitcoin was last moved on the blockchain (realized value).

How to Use the Indicator:

Market Extremes:

Use the MVRVZ and Z-Score to spot potential market tops or bottoms.

A high Z-Score (above +2) suggests the market is overbought, while a low Z-Score (below -2) suggests the market is oversold.

Adjusting the Triggers:

Customize the Top and Bottom Trigger Lines to suit your trading strategy. These lines can act as dynamic reference points for when to take action based on the Z-Score or MVRVZ line crossing these levels.

Market Evaluation (SCDA Framework):

The bounded Z-Score (from -2 to +2) is tailored for your SCDA evaluation system, allowing you to assess market conditions based on consistent criteria, no matter how volatile the MVRVZ line becomes.

Conclusion:

The MVRVZ BTC indicator is a powerful tool for assessing the relative valuation of Bitcoin based on its market and realized capitalization. By combining it with the Z-Score, you get an easy-to-read, bounded evaluation system that highlights potential market extremes and helps you make informed decisions about Bitcoin's price behavior.

Correlation Drift📈 Correlation Drift

The Correlation Drift indicator is designed to detect shifts in market momentum by analyzing the relationship between correlation and price lag. It combines the principles of correlation analysis and lag factor measurement to provide a unique perspective on trend alignment and momentum shifts.

🔍 Core Concept:

The indicator calculates the Correlation vs PLF Ratio, which measures the alignment between an asset’s price movement and a chosen benchmark (e.g., BTCUSD). This ratio reflects how well the asset’s momentum matches the market trend while accounting for price lag.

📊 How It Works:

Correlation Calculation:

The script calculates the correlation between the asset and the selected benchmark over a specified period.

A higher correlation indicates that the asset’s price movements are in sync with the benchmark.

Price Lag Factor (PLF) Calculation:

The PLF measures the difference between long-term and short-term price momentum, dynamically scaled by recent volatility.

It highlights potential overextensions or lags in the asset’s price movements.

Combining Correlation and PLF:

The Correlation vs PLF Ratio combines these metrics to detect momentum shifts relative to the trend.

The result is a dynamic, smoothed histogram that visualizes whether the asset is leading or lagging behind the trend.

💡 How to Interpret:

Positive Values (Green/Aqua Bars):

Indicates bullish alignment with the trend.

Aqua: Rising bullish momentum, suggesting continuation.

Teal: Decreasing bullish momentum, signaling caution.

Negative Values (Purple/Fuchsia Bars):

Indicates bearish divergence from the trend.

Fuchsia: Falling bearish momentum, indicating increasing pressure.

Purple: Rising bearish momentum, suggesting potential reversal.

Clipping for Readability:

Values are clipped between -3 and +3 to prevent outliers from compressing the histogram.

This ensures clear visualization of typical momentum shifts while still marking extreme cases.

🚀 Best Practices:

Use Correlation Drift as a confirmation tool in conjunction with trend indicators (e.g., moving averages) to identify momentum alignment or divergence.

Look for transitions from positive to negative (or vice versa) as signals of potential trend shifts.

Combine with volume analysis to strengthen confidence in breakout or breakdown signals.

⚠️ Key Features:

Customizable Settings: Adjust the correlation length, PLF length, and smoothing factor to fine-tune the indicator for different market conditions.

Visual Gradient: The histogram changes color based on the strength and direction of the ratio, making it easy to identify shifts at a glance.

Zero Line Reference: Clearly distinguishes between bullish and bearish momentum zones.

🔧 Recommended Settings:

Correlation Length: 14 (for short to medium-term analysis)

PLF Length: 50 (to smooth out noise while capturing trend shifts)

Smoothing Factor: 3 (for enhanced clarity without excessive lag)

Benchmark Symbol: BTCUSD (or another relevant market indicator)

By providing a quantitative measure of trend alignment while accounting for price lag, the Correlation Drift indicator helps traders make more informed decisions during periods of momentum change. Whether you are trading crypto, forex, or equities, this tool can be a powerful addition to your momentum-based trading strategies.

⚠️ Disclaimer:

The Correlation Drift indicator is a technical analysis tool designed to aid in identifying potential shifts in market momentum and trend alignment. It is intended for informational and educational purposes only and should not be considered as financial advice or a recommendation to buy, sell, or hold any financial instrument.

Trading financial instruments, including cryptocurrencies, involves significant risk and may result in the loss of your capital. Past performance is not indicative of future results. Always conduct thorough research and seek advice from a certified financial professional before making any trading decisions.

The developer (RWCS_LTD) is not responsible for any trading losses or adverse outcomes resulting from the use of this indicator. Users are encouraged to test and validate the indicator in a simulated environment before applying it to live trading. Use at your own risk.

Hurst Exponent Oscillator [PhenLabs]📊 Hurst Exponent Oscillator -

Version: PineScript™ v5

📌 Description

The Hurst Exponent Oscillator (HEO) by PhenLabs is a powerful tool developed for traders who want to distinguish between trending, mean-reverting, and random market behaviors with clarity and precision. By estimating the Hurst Exponent—a statistical measure of long-term memory in financial time series—this indicator helps users make sense of underlying market dynamics that are often not visible through traditional moving averages or oscillators.

Traders can quickly know if the market is likely to continue its current direction (trending), revert to the mean, or behave randomly, allowing for more strategic timing of entries and exits. With customizable smoothing and clear visual cues, the HEO enhances decision-making in a wide range of trading environments.

🚀 Points of Innovation

Integrates advanced Hurst Exponent calculation via Rescaled Range (R/S) analysis, providing unique market character insights.

Offers real-time visual cues for trending, mean-reverting, or random price action zones.

User-controllable EMA smoothing reduces noise for clearer interpretation.

Dynamic coloring and fill for immediate visual categorization of market regime.

Configurable visual thresholds for critical Hurst levels (e.g., 0.4, 0.5, 0.6).

Fully customizable appearance settings to fit different charting preferences.

🔧 Core Components

Log Returns Calculation: Computes log returns of the selected price source to feed into the Hurst calculation, ensuring robust and scale-independent analysis.

Rescaled Range (R/S) Analysis: Assesses the dispersion and cumulative deviation over a rolling window, forming the core statistical basis for the Hurst exponent estimate.

Smoothing Engine: Applies Exponential Moving Average (EMA) smoothing to the raw Hurst value for enhanced clarity.

Dynamic Rolling Windows: Utilizes arrays to maintain efficient, real-time calculations over user-defined lengths.

Adaptive Color Logic: Assigns different highlight and fill colors based on the current Hurst value zone.

🔥 Key Features

Visually differentiates between trending, mean-reverting, and random market modes.

User-adjustable lookback and smoothing periods for tailored sensitivity.

Distinct fill and line styles for each regime to avoid ambiguity.

On-chart reference lines for strong trending and mean-reverting thresholds.

Works with any price series (close, open, HL2, etc.) for versatile application.

🎨 Visualization

Hurst Exponent Curve: Primary plotted line (smoothed if EMA is used) reflects the ongoing estimate of the Hurst exponent.

Colored Zone Filling: The area between the Hurst line and the 0.5 reference line is filled, with color and opacity dynamically indicating the current market regime.

Reference Lines: Dash/dot lines mark standard Hurst thresholds (0.4, 0.5, 0.6) to contextualize the current regime.

All visual elements can be customized for thickness, color intensity, and opacity for user preference.

📖 Usage Guidelines

Data Settings

Hurst Calculation Length

Default: 100

Range: 10-300

Description: Number of bars used in Hurst calculation; higher values mean longer-term analysis, lower values for quicker reaction.

Data Source

Default: close

Description: Select which data series to analyze (e.g., Close, Open, HL2).

Smoothing Length (EMA)

Default: 5

Range: 1-50

Description: Length for smoothing the Hurst value; higher settings yield smoother but less responsive results.

Style Settings

Trending Color (Hurst > 0.5)

Default: Blue tone

Description: Color used when trending regime is detected.

Mean-Reverting Color (Hurst < 0.5)

Default: Orange tone

Description: Color used when mean-reverting regime is detected.

Neutral/Random Color

Default: Soft blue

Description: Color when market behavior is indeterminate or shifting.

Fill Opacity

Default: 70-80

Range: 0-100

Description: Transparency of area fills—higher opacity for stronger visual effect.

Line Width

Default: 2

Range: 1-5

Description: Thickness of the main indicator curve.

✅ Best Use Cases

Identifying if a market is regime-shifting from trending to mean-reverting (or vice versa).

Filtering signals in automated or systematic trading strategies.

Spotting periods of randomness where trading signals should be deprioritized.

Enhancing mean-reversion or trend-following models with regime-awareness.

⚠️ Limitations

Not predictive: Reflects current and recent market state, not future direction.

Sensitive to input parameters—overfitting may occur if settings are changed too frequently.

Smoothing can introduce lag in regime recognition.

May not work optimally in markets with structural breaks or extreme volatility.

💡 What Makes This Unique

Employs advanced statistical market analysis (Hurst exponent) rarely found in standard toolkits.

Offers immediate regime visualization through smart dynamic coloring and zone fills.

🔬 How It Works

Rolling Log Return Calculation:

Each new price creates a log return, forming the basis for robust, non-linear analysis. This ensures all price differences are treated proportionally.

Rescaled Range Analysis:

A rolling window maintains cumulative deviations and computes the statistical “range” (max-min of deviations). This is compared against the standard deviation to estimate “memory”.

Exponent Calculation & Smoothing:

The raw Hurst value is translated from the log of the rescaled range ratio, and then optionally smoothed via EMA to dampen noise and false signals.

Regime Detection Logic:

The smoothed value is checked against 0.5. Values above = trending; below = mean-reverting; near 0.5 = random. These control plot/fill color and zone display.

💡 Note:

Use longer calculation lengths for major market character study, and shorter ones for tactical, short-term adaptation. Smoothing balances noise vs. lag—find a best fit for your trading style. Always combine regime awareness with broader technical/fundamental context for best results.