Multi-Regression StrategyIntroducing the "Multi-Regression Strategy" (MRS) , an advanced technical analysis tool designed to provide flexible and robust market analysis across various financial instruments.

This strategy offers users the ability to select from multiple regression techniques and risk management measures, allowing for customized analysis tailored to specific market conditions and trading styles.

Core Components:

Regression Techniques:

Users can choose one of three regression methods:

1 - Linear Regression: Provides a straightforward trend line, suitable for steady markets.

2 - Ridge Regression: Offers a more stable trend estimation in volatile markets by introducing a regularization parameter (lambda).

3 - LOESS (Locally Estimated Scatterplot Smoothing): Adapts to non-linear trends, useful for complex market behaviors.

Each regression method calculates a trend line that serves as the basis for trading decisions.

Risk Management Measures:

The strategy includes nine different volatility and trend strength measures. Users select one to define the trading bands:

1 - ATR (Average True Range)

2 - Standard Deviation

3 - Bollinger Bands Width

4 - Keltner Channel Width

5 - Chaikin Volatility

6 - Historical Volatility

7 - Ulcer Index

8 - ATRP (ATR Percentage)

9 - KAMA Efficiency Ratio

The chosen measure determines the width of the bands around the regression line, adapting to market volatility.

How It Works:

Regression Calculation:

The selected regression method (Linear, Ridge, or LOESS) calculates the main trend line.

For Ridge Regression, users can adjust the lambda parameter for regularization.

LOESS allows customization of the point span, adaptiveness, and exponent for local weighting.

Risk Band Calculation:

The chosen risk measure is calculated and normalized.

A user-defined risk multiplier is applied to adjust the sensitivity.

Upper and lower bounds are created around the regression line based on this risk measure.

Trading Signals:

Long entries are triggered when the price crosses above the regression line.

Short entries occur when the price crosses below the regression line.

Optional stop-loss and take-profit mechanisms use the calculated risk bands.

Customization and Flexibility:

Users can switch between regression methods to adapt to different market trends (linear, regularized, or non-linear).

The choice of risk measure allows adaptation to various market volatility conditions.

Adjustable parameters (e.g., regression length, risk multiplier) enable fine-tuning of the strategy.

Unique Aspects:

Comprehensive Regression Options:

Unlike many indicators that rely on a single regression method, MRS offers three distinct techniques, each suitable for different market conditions.

Diverse Risk Measures: The strategy incorporates a wide range of volatility and trend strength measures, going beyond traditional indicators to provide a more nuanced view of market dynamics.

Unified Framework:

By combining advanced regression techniques with various risk measures, MRS offers a cohesive approach to trend identification and risk management.

Adaptability:

The strategy can be easily adjusted to suit different trading styles, timeframes, and market conditions through its various input options.

How to Use:

Select a regression method based on your analysis of the current market trend (linear, need for regularization, or non-linear).

Choose a risk measure that aligns with your trading style and the market's current volatility characteristics.

Adjust the length parameter to match your preferred timeframe for analysis.

Fine-tune the risk multiplier to set the desired sensitivity of the trading bands.

Optionally enable stop-loss and take-profit mechanisms using the calculated risk bands.

Monitor the regression line for potential trend changes and the risk bands for entry/exit signals.

By offering this level of customization within a unified framework, the Multi-Regression Strategy provides traders with a powerful tool for market analysis and trading decision support. It combines the robustness of regression analysis with the adaptability of various risk measures, allowing for a more comprehensive and flexible approach to technical trading.

Std

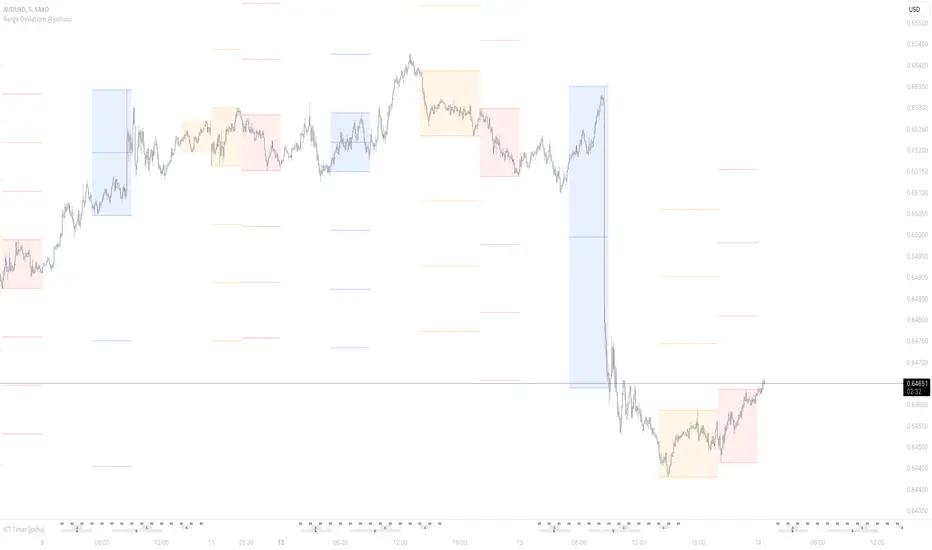

Range Deviations @joshuuuThis indicator is able to show ranges, the equlibrium (50%) and range deviations.

It has four pre-defined options and one custom version.

Asia (2000-0000) ny time

CBDR(1400-2000) ny time

Flout(1400-0000) ny time

ONS (OverNightSession)(0400-0800) chicago time

Custom (you can choose the times)

ICT (Inner Circle Traders) teaches, that those range deviations of asia,cbdr,flout can be used to find the daily high/low.

TCM (The Currency Merchant) teaches, that a move out of the range often is a false move to trap traders into the wrong direction.

Click VWAP Anchored with Standard Devation BandsSimply use it by clicking on your chart on the places you find important to determine whether you entries or exits look strong or weak.

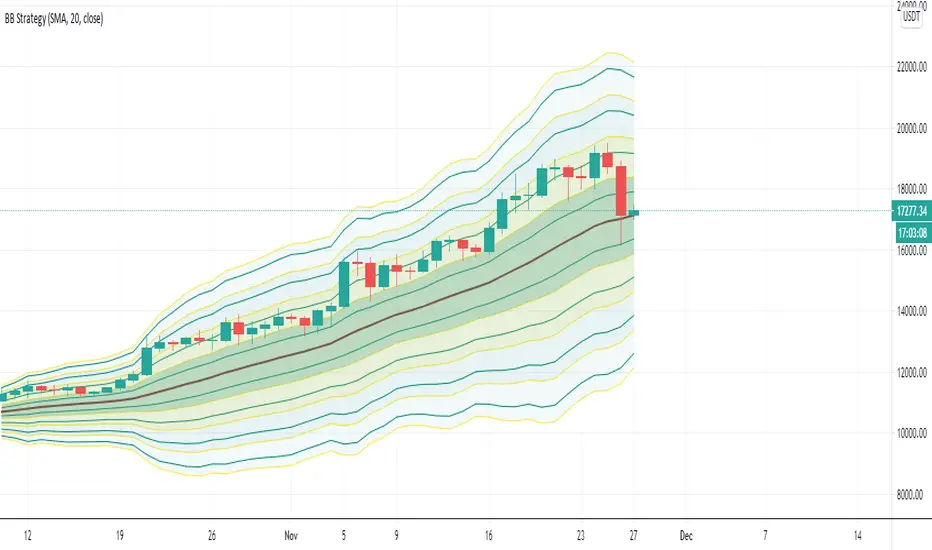

Mulitple Bollinger Bands with MAsIn this indicator, I used Bollinger Bands and many standard deviation values together. These values are: 0.618 (Yellow), 1, 1.618 (Yellow), 2, 2.618 (Yellow), 3, 3.618 (Yellow), 4, 4.618 (Yellow). Like the indicator I just published, I also added multiple moving average options for the Bollinger Bands calculation. You can create your own strategies for where it bounces in ups and downs.

Türkçe:

Bu indikatörde Bollinger Bantları ile birçok standart sapma değerini birlikte kullandım. Bu değerler: 0.618 (Sarı), 1, 1.618 (Sarı), 2, 2.618 (Sarı), 3, 3.618 (Sarı), 4, 4.618 (Sarı). Daha yayınladığım indikatör gibi burada da Bollinger Bantları hesaplaması için birden çok hareketli ortalama seçeneği de ekledim. Yükseliş ve düşüşlerde sektiği yerler için kendi stratejileriniz oluşturabilirsiniz.

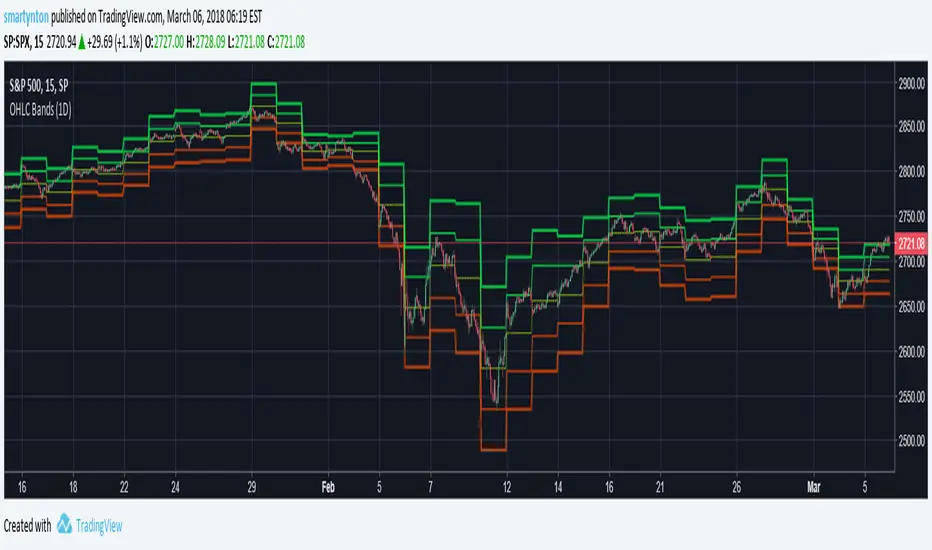

OHLC Daily Resolution BandsShout out to nPE- for the idea.

Bands made with stdev from 10 day OHLC.

Keeps resolution to daily, so you can use bands as daily pivots for day trading.

Upper band 1=yesterday close + 0.5 std(ohlc,10)

Upper band 1=yesterday close + 1 std(ohlc,10)

Mid=yesterday close

Lower band 1=yesterday close - 0.5 std(ohlc,10)

Lower band 2=yesterday close - 1 std(ohlc,1