Trendlines with Breaks [LuxAlgo]The trendlines with breaks indicator return pivot point based trendlines with highlighted breakouts. Users can control the steepness of the trendlines as well as their slope calculation method.

Trendline breakouts occur in real-time and are not subject to backpainting. Trendlines can however be subject to repainting unless turned off from the user settings.

The indicator includes integrated alerts for trendline breakouts.

🔶 USAGE

Any valid trendlines methodology can be used with the indicator, users can identify breakouts in order to infer future price movements.

The calculation method of the slope greatly affects the trendline's behaviors. By default, an average true range is used, returning a more constant slope amongst trendlines. Other methods might return trendlines with significantly different slopes.

Stdev makes use of the standard deviation for the slope calculation, while Linreg makes use of the slope of a linear regression.

The above chart shows the indicator using "Stdev" as a slope calculation method. The chart below makes use of the "Linreg" method.

By default trendlines are subject to backpainting, and as such are offset by length bars in the past. Disabling backpainting will not offset the trendlines.

🔶 SETTINGS

Length: Pivot points period

Slope: Slope steepness, values greater than 1 return a steeper slope. Using a slope of 0 would be equivalent to obtaining levels.

Slope Calculation Method: Determines how the slope is calculated.

Backpaint: Determine whether trendlines are backpainted, that is offset to past.

Standard Deviation (Volatility)

Standard Deviation Candles (With Emoji)In crypto, significant price moves can be a sign of continuation or reversal. This script measures if price move is greater than a certain number of standard deviations vs. previous periods, then alters bar colours and/or prints an emoji signal.

DMI & ST DEV zone intersection [LM]Hello Traders,

This indicator uses two indicators st dev extremes and DMI extremes and visualize intersection of both indicators extreme zones using crosses. It means where cross is rendered intersection of extremes has occurred.

The standard deviation uses the same calculation as my Standard deviation zones Support & Resistance indicator, DMI indicator measures both the strength and direction of a price movement. I am using both indicators to find the intersection of extreme zones between them.

ST DEV settings:

source

tops setting

bottom setting

DMI settings:

length settings

extreme zone setting

Enjoy,

Lukas

Ultimate Moving Average Bands [CC+RedK]The Ultimate Moving Average Bands were created by me and @RedKTrader and this converts our Ultimate Moving Average into volatility bands that use the same adaptive logic to create the bands. I have enabled everything to be fully adjustable so please let me know if you find a more useful setting than what I have here by default. I'm sure everyone is familiar with volatility bands but generally speaking if a price goes above the volatility bands then this is either a sign of an extremely strong uptrend or a potential reversal point and vice versa. I have included strong buy and sell signals in addition to normal ones so darker colors are strong signals and lighter colors are normal ones. Buy when the lines turn green and sell when they turn red.

Let me know if there are any other scripts you would like to see me publish!

STDev % by Alejandro PThis is a simple indicator that expands the usability of Standard deviation into a universally usable indicator.

This indicator displays the volatility as standard deviation as a % of asset value, this allows using more standardized and comparable values across multiple instruments and asset classes.

[EG] Fib RSIExtrapolated Fibonacci MA (FMA) into an RSI

i.e. FMA(up) and FMA(dn) of lengths 2, 3, 5, 8, 13, 21, 34, 55, 89 etc. averaged into RSI values.

Keep in mind it does not use 'Length' - it uses 'Interval' - how many fib intervals to include in the RSI calculation.

I threw in Ehler's Smoothing as well - seems to work quite well, thanks to TV Community for inspiration and code to look at for help

(Standard RSI included for comparison)

VWAP St. Dev BandsThis indicator allows you to add up to 3 volatility bands to VWAP based on its Standard Deviation.

Best use is for intraday but you can choose higher timeframes too.

For day trading a band of 3 standard deviations usually works well as an overbought/oversold region, allowing for mean reversion trading, but you are free to come up with your own strategies.

Enjoy!

RSI Div at Daily VWAP StDevMean Reversion indicator based on RSI Divergences at Overbought/Oversold conditions with Price above/below a Standard Deviation from Daily VWAP. Useful for intra-day trading.

Signal criteria:

1. RSI is at Overbought/Oversold

2. RSI Divergence present (not hidden)

3. RSI has not reached Neutral level (i.e. 50)

4. Price has crossed above/below a Standard Deviation from Daily VWAP

Config Options:

- RSI length (default:14)

- Divergence Lookback Period (default:14)

- RSI Oversold/Overbought tresholds (default: 70/30)

- RSI Reset Level (default: 55/45)

- Use VWAP Std Dev (default: yes)

- Standard Deviation from Daily VWAP (default: 1.51)

Use with discretion.

Erzurum Indicators (By DadashKadir)Erzurum Indicators (By DadashKadir)

An indicator in which you will keep track of the buying and selling movements by adding the movements of the three moving averages together. The parameters were determined as Moving Average (SMA), Exponential Moving Average (EMA), Weighted Moving Average (WMA) and Volume Weighted Moving Average (VWMA). Its constant value was taken as WMA. It is used to calculate the averages of 3 - 5 and 7. You can include the standard deviation (STDEV) in these moving averages.

The name of the indicator is taken from our city of Erzurum, the pearl of Eastern Anatolia.

Weighted stdev/BBThe basis/mean is the equivalent to the pine built in function wma(). It assigns greater weighting to recent data points and less weighting on past data points. The weighted moving average is calculated by multiplying each observation in the data set by a predetermined weighting factor.

Similarly the stdev is calculated using the same weighting factors where recent deviations are given greater weight than past deviations.

Stdev Breakout StrategyStdev Breakout Strategy

Description:

This script generates a long entry signal when the Standard Deviation crosses over the Simple Moving Average and the Close is greater than the Open, and/or generates a short entry signal when the Standard Deviation crosses under the Simple Moving Average and the Close is less than the Open.

CV_VWAP_GMECoefficient of variance GME ‰

Gray area: Regional price variance of GME in per milles

Light gray thick line: NYSE:GME deviation from global mean

1. Select a chart 24-hour ticker like FX_IDC:USDEUR

2. Select a timescale (5 min, 15 min, ...)

3. Monitor the regional price variance

Exchanges included: NYSE, XETR, BMV, FWB, SWB, BITTREX, FTX

Currency conversion: Forex

Adapted from Detecting the great short squeeze on Volkswagen, Godfrey, K. (2016, February 18).

ATR Without OutliersIt is an ATR indicator which filters out outliers.

Outliers are values which are higher than the standard deviation of the true range.

It may be better than normal ATR for stop loss, because it does not keep large values after pump or dump.

It is very useful for high volatile markets like crypto markets.

SuperTrendRange by DGTSuperTrendRange study attempts to determine the state of the market

• whether a well-established bull/bear trend is present

• whether the market is trading in a range

SuperTrendRange (STR) takes into account the volatility of the market - further details regarding volatility can be found in the description of “Volatility Bands by DGT” study

Due to its similarities to SupertTrend (ST) and Parabolic SAR (SAR), I will try to explain by stating differences between them

SuperTrendRange uses both the ATR (Average True Range) and STDEV (Standard Deviation) as part of its calculations - unlike ST and SAR where they use only ATR

Sensitivity of the indicator is adjusted using the multiplier setting of both ATR and STDEV

Additionally, unlike ST, the source of the basis of SuperTrendRange can be selected among the assets price value or its moving average

Source and Length are adjustable too

The SuperTrendRange, like Parabolic SAR indicator, appears on a chart as a series of dots, either above, below or unlike Parabolic SAR both above and below of the asset's price

A dot placed

- below the price when the market is trending upward

- above the price when it is trending downward

- both above and below when the price starts moving sideways – this is a feature that both SuperTrend and Parabolic SAR misses, where they are known to produce false signals and losing trades, whereas SuperTrendRange emphasis the zones of the ranges occurring and in most cases are considered no trade recommended zones. Please note that the range width may vary depending on how the market is volatile. It is up to the users to trade if it fits their trading strategies

Dots plotted above and below can be assumed as Support and Resistance levels

Example usages – with trading opportunities

Gold Monthly Chart

Bitcoin Daily Chart

Disclaimer:

Trading success is all about following your trading strategy and the indicators should fit within your trading strategy, and not to be traded upon solely

The script is for informational and educational purposes only. Use of the script does not constitute professional and/or financial advice. You alone have the sole responsibility of evaluating the script output and risks associated with the use of the script. In exchange for using the script, you agree not to hold dgtrd TradingView user liable for any possible claim for damages arising from any decision you make based on use of the script

Z-Score 'Bollinger Bands'The following script is an application of the Z-Score (previous script).

Z-Scores can be used in place of standard deviation (sigma) in 'Bollinger Bands'.

The average of the sample (x-bar) over 21 days (N)

21 average trading days per month, fixed value

The average of the population (mu) over 63 days (n)

63 days per quarter, default is set to 63

Z-Score is calculated by formula in previous script, and the absolute value is taken of "Z".

Z-High = absolute value of Z + (x-bar).

Z-Low = absolute value of Z - (x-bar).

Will update with Z from mu and Z from avg (working on UX and visualization details).

Portfolio: alpha, beta, stdev, variance, mean, max drawdown...Portfolio Metrics **New**

'returns'

'log returns'

'geometric returns'

portfolio alpha

portfolio beta

portfolio,market correlation

portfolio standard deviation

portfolio variance

mean portfolio returns

maximum drawdown

maximum gain

Portfolio Metrics = α(Jensen's), β, CAPM(Ra), Sharpe, TreynorPortfolio Metrics...

Standard Deviation

Jensen's Alpha

Beta

Expected Return (CAPM, Ra)

Sharpe Ratio

Treynor Ratio

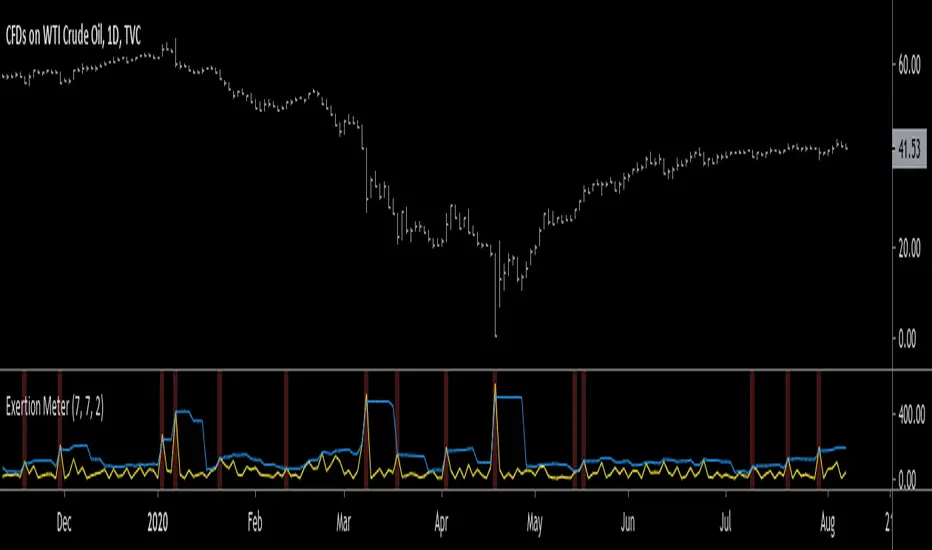

Exertion MeterHello traders, today I wanted to present you something special. I present you the Exertion Meter!

Created from scratch, this idea is based on a theory of mine called "Exertion".

Exertion occurs when price moves beyond the previous bar's range thus it has "exerted itself".

The idea is that when price moves a lot, it exerts a lot of energy which eventually leads to calmer motion, usually in the direction price has exerted itself.

Now, when price has exerted itself a lot in a particular direction, it's telling you that it will likely continue in that direction.

Once this happens, it will gradually calm down until price begins the cycle again, exerting itself in either the same or opposite direction.

This theory is similar to the theory of expansion & contraction phases.

This indicator attempts to show you where price has exerted itself by giving you a two lines cross signal.

The default settings are recommended, but experimentation is encouraged to fit your own personal system.

Both settings control the standard deviation line ( aka . Upper Bollinger Band ).

Enjoy, and hit the follow button to get easy access to all my indicators and to follow my latest publications!

Volatility based Standarde Deviation and Fib. Pivot PointsThis indicator plots Standard deviation levels and Fib. Pivot Points. I prefer to use only SD levels but Fib. levels also come handy in providing support and resistance.

How to use this indicator:

You have to manually enter instrument's Closing Price / Settlement Price and VIX closing price to draw each day's levels.

For NQ, I use VXN closign price and for ES or RTY, I use VIX closing price.

This indicator can be used on individual stocks and forex pairs.

VAMA Volume Adjusted Moving Average BandsThis indicator is standard deviation bands using a live analysis adaptation of Richard Arms' Volume Adjusted Moving Average as their basis. VAMA utilizes a period length that is based on volume increments rather than time.

• SampleN - N volume bars used as sample to calculate average volume , 0 equals all bars.

• VAMA Source - Price used for volume weighted calculations.

• VAMA Length - Specified number of volume ratio buckets to be reached.

• VAMA VI Fct - Size of volume ratio buckets.

• VAMA Strict - Must meet desired volume requirements, even if number of bars has to exceed VAMA Length to do it.

• STDV Factor - Standard Deviation multiplier.

• STDV Length - Standard Deviation period.

• Brightness - Color opaqueness for the band fills.

Please see previous published example here for more details on VAMA's usage and inability to redraw the past on time based charts.

NOTICE: This is an example script and not meant to be used as an actual strategy. By using this script or any portion thereof, you acknowledge that you have read and understood that this is for research purposes only and I am not responsible for any financial losses you may incur by using this script!

StDev Based Trendlines - JDAs a second alternatively based trendline script this is the Standard Deviation vesrion.

This script draws trendlines from the pivot points in the price chart.

The angle of the trendlines is determined by (a percentage of) the Standard Deviation.

The angle follows the change in price, compared to the StDev at the moment where the pivot point is detected

The StDev percentage determines if the trendline follows the rate of change of the StDev or a fraction ( value < 100) or a multiple ( value > 100) of that

JD.

#NotTradingAdvice #DYOR

Disclaimer.

I AM NOT A FINANCIAL ADVISOR.

THESE IDEAS ARE NOT ADVICE AND ARE FOR EDUCATION PURPOSES ONLY.

ALWAYS DO YOUR OWN RESEARCH!

Trend Analysis IndicatorThe Trend Analysis Indicator was created by Adam White (Stocks & Commodities V. 10:8 (358-360)) and this is not to be confused with the Trend Analysis Index which was also created by Adam White. The stock is trending when it is above the signal and loses steam when it falls below the signal. Generally you should buy when it is above it's signal and sell when it goes below the signal.

Let me know if you would like me to write more scripts!

Variable Length Moving AverageThe Variable Length Moving Average was created by George R. Arrington Ph.D. (Stocks & Commodities V. 9:6 (219-223)) and I'm really loving this indicator. It is a great moving average that hugs the price very closely and it is fully adjustable to your needs. It detects signals extremely well and I have color coded the moving average line to make it very easy to interpret.

This is not to be confused with the Variable Moving Average created by Tushar S. Chande and as of now I haven't seen any other script for this moving average out there yet.

Please let me know if you would like me to write any other scripts for indicators you would like to see!