Odd_DVEnds Dividend True Value💸 True Value = Close Price + Accumulated Dividends

◆ Using only the time displayed on screen of the chart, the script will calculate the True Value of the symbol. (Calculations start from first bar you can see to the last bar you can see.)

Why do you need the true value?

Anytime an asset pays a dividend the current market price doesn't reflect the actual value you would have received over time from holding said asset. Without this price information fairly comparing assets is difficult.

🗻 Selectable themed legend

🎨 Highly Customizable

⚠️ As of the first release moving multiple charts on the same layout using sync will not always update all charts. Its recommended to use the bottom toolbar to move times if using indicator on multiple charts. Check for updates to see if this has been resolved.

T-BOND

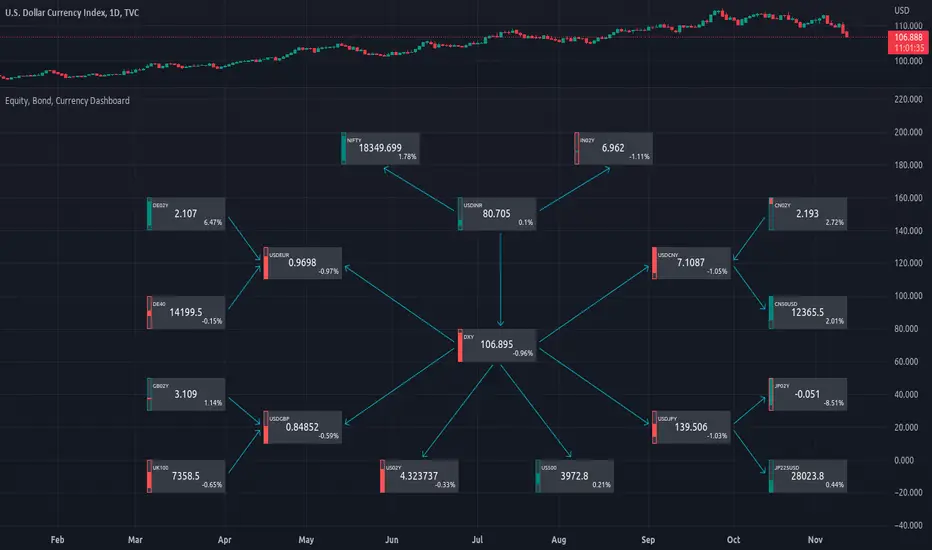

Equity Bond Currency DashboardDepicts demand-flow between Equities, Bonds and Currencies of 6 countries. Useful in tracking the flow of smart money and checking the dynamics of inter-connected markets.

Principle:

DXY lies at the heart of the diagram with usd-currency pairs of 5 countries connected to it. When demand for a currency increases it strengthens against Dollar. This is depicted by a line from DXY to the currency indicating demand flow from Dollar to the currency (DXY is only an indicative symbol for Dollar, the currency may not be part of the dollar index). Similarly when Dollar strengthens against the currency, demand flow is depicted by a line from the currency to DXY. Currency blocks are connected to Equity and Bond Yields of the respective countries. Equities and Bonds, when bought, takes the demand from the respective currencies and vice versa.

Overall, the demand flows in the direction of arrows. The flow is incomplete without commodities, import/export, interest/inflation rates of countries, however, the diagram most of the times explains why an asset class is performing the way it is.

Left side bar of each block is very similar to OHLC candles except for the following -

Instead of wicks, top and bottom of the bar represents high and low for the selected time-frame

Open and close are normalised for high and low

Bar border is red if close < prev.close, green if close >= prev.close

Other notes:

The diagram requires at least 200 bars in the chart to render. Please select the symbol and time-frame that contain at least 200 bars.

The diagram requires a live market to render the flow. To check flows on historical bars, set the option from settings.

Desired indices could be selected for countries of choice. Default settings point to futures wherever possible to have the markets live simultaneously across the countries.

Historical US Bond Yield CurvePreface: I'm just the bartender serving today's freshly blended concoction; I'd like to send a massive THANK YOU to all the coders and PineWizards for the locally-sourced ingredients. I am simply a code editor, not a code author. Many thanks to these original authors!

Source 1 (Aug 8, 2019):

Source 2 (Aug 11, 2019):

About the Indicator: The term yield curve refers to the yields of U.S. treasury bills, notes, and bonds in order from shortest to longest maturity date. The yield curve describes the shapes of the term structures of interest rates and their respective terms to maturity in years. The slope of the yield curve tells us how the bond market expects short-term interest rates to move in the future based on bond traders' expectations about economic activity and inflation. The best use of the yield curve is to get a sense of the economy's direction rather than to try to make an exact prediction. This indicator plots the U.S. yield curve as maturity (x-axis/time) vs yield (y-axis/price) in addition to historical yield curves and advanced data tickers . The visual array of historical yield curves helps investors visualize shifts in the yield curve that are useful when identifying & forecasting economic conditions. The bond market can help predict the direction of the economy which can be useful in crafting your investment strategy. An inverted 10y/2y yield curve for durations longer than 5 consecutive trading days signals an almost certain recession on the horizon. An inversion happens when short-term bonds pay better than longer-term bonds. There is Federal Reserve Board data that suggests the 10y3m may be a better predictor of recessions.

Features: Advanced dual data ticker that performs curve & important spread analysis, plus additional hover info. Advanced yield curve data labels with additional hover info. Customizable historical curves and color theme.

‼ IMPORTANT: Hover over labels/tables for advanced information. Chart asset and timeframe may affect the yield curve results; I have found consistently accurate results using BINANCE:BTCUSDT on 1d timeframe. Historical curve lookbacks will have an effect on whether the curve analysis says the curve is bull/bear steepening/flattening, so please use appropriate lookbacks.

⚠ DISCLAIMER: Not financial advice. Not a trading system. DYOR. I am not affiliated with the original authors, TradingView, Binance, or the Federal Reserve Board.

About the Editor: I am a former FINRA Registered Representative, inventor/patent holder, futures trader, and hobby PineScripter.

Portfolio Performance - Effects of RebalancingFunction:

- Can be used to evaluate the performance of a portfolio containing 2 assets over a set time interval

- Shows the % return of the portfolio over the time interval defined by the user

- Includes a threshold rebalancing algorithm to show the effects that rebalancing has on the portfolio over the long term

- Created to evaluate of the performance of portfolios containing different weightings of stocks and bonds over time assuming that the user would rebalance the portfolio when asset weights crossed a threshold

Instructions:

- To be used with dividends adjustments turned on

- Add this script to a symbol. e.g. AMEX:SPY

- Click the chart to define the entry time and the exit time. i.e. the time interval

- Define the initial investment of the portfolio. Default setting is $100,000

- Define the second asset to be included in the portfolio. e.g. BATS:AGG

- The strategy comes pre-populated with a portfolio that has a weight of 80% asset 1 and 20% asset 2. i.e. 80% AMEX:SPY and 20% BATS:AGG if the symbols mentioned above were chosen

- The 7 lines show the weighted % return of each portfolio over the time period defined by the user

- Each line (except the blue) is the return based on a different rebalancing threshold. The default settings are 1%, 2.5%, 5%, 10%, 15%, 20%, 30%

- The blue line is the % return of a portfolio that was made up of 100% asset 1 over the time interval. i.e. 100% AMEX:SPY

- Asset weights and rebalancing thresholds are adjustable via the settings

- Each plot can be turned on and turned off via a tick box in the settings

Portfolio Performance - 2 AssetsFunction:

- Can be used to evaluate the performance of portfolios containing 2 assets over a set time interval

- Created to evaluate of the performance of portfolios containing different weightings of stocks and bonds over time

- Shows the % return of each portfolio over the time interval defined by the user

- Capable of showing the risk adjusted % return of each portfolio over the time interval defined by the user (setting turned off by default)

Instructions:

- To be used with dividends adjustments turned on

- Add this script to a symbol. e.g. NASDAQ:BND

- Click the chart to define the entry time and the exit time. i.e. the time interval

- Define the second asset to be included in the portfolio. e.g. AMEX:VOO

- The strategy comes pre-populated with 6 portfolios with the most common stock/bond weightings (100% stocks/0% bonds, 80% stocks/20% bonds, 60% stocks/40% bonds, et cetera)

- The 6 lines show the weighted % return of each portfolio over the time period defined by the user

- All asset weights are adjustable via the settings

- Each plot can be turned on and turned off via a tick box in the settings

- There are 6 plots that show the risk adjusted returns of each portfolio (setting turned off by default)