time_and_sessionA library that provides utilities for working with trading sessions and time-based conditions. Functions include session checks, date range checks, day-of-week matching, and session high/low calculations for daily, weekly, monthly, and yearly timeframes. This library streamlines time-related calculations and enhances time-based strategies and indicators.

Library "time_and_session"

Provides functions for checking time and session-based conditions and retrieving session-specific high and low values.

is_session(session, timeframe, timezone)

Checks if the current time is within the specified trading session

Parameters:

session (string) : The trading session, defined using input.session()

timeframe (string) : The timeframe to use, defaults to the current chart's timeframe

timezone (string) : The timezone to use, defaults to the symbol's timezone

Returns: A boolean indicating whether the current time is within the specified trading session

is_date_range(start_time, end_time)

Checks if the current time is within a specified date range

Parameters:

start_time (int) : The start time, defined using input.time()

end_time (int) : The end time, defined using input.time()

Returns: A boolean indicating whether the current time is within the specified date range

is_day_of_week(sunday, monday, tuesday, wednesday, thursday, friday, saturday)

Checks if the current day of the week matches any of the specified days

Parameters:

sunday (bool) : A boolean indicating whether to check for Sunday

monday (bool) : A boolean indicating whether to check for Monday

tuesday (bool) : A boolean indicating whether to check for Tuesday

wednesday (bool) : A boolean indicating whether to check for Wednesday

thursday (bool) : A boolean indicating whether to check for Thursday

friday (bool) : A boolean indicating whether to check for Friday

saturday (bool) : A boolean indicating whether to check for Saturday

Returns: A boolean indicating whether the current day of the week matches any of the specified days

daily_high(source)

Returns the highest value of the specified source during the current daily session

Parameters:

source (float) : The data series to evaluate, defaults to high

Returns: The highest value during the current daily session, or na if the timeframe is not suitable

daily_low(source)

Returns the lowest value of the specified source during the current daily session

Parameters:

source (float) : The data series to evaluate, defaults to low

Returns: The lowest value during the current daily session, or na if the timeframe is not suitable

regular_session_high(source, persist)

Returns the highest value of the specified source during the current regular trading session

Parameters:

source (float) : The data series to evaluate, defaults to high

persist (bool) : A boolean indicating whether to retain the last value outside of regular market hours, defaults to true

Returns: The highest value during the current regular trading session, or na if the timeframe is not suitable

regular_session_low(source, persist)

Returns the lowest value of the specified source during the current regular trading session

Parameters:

source (float) : The data series to evaluate, defaults to low

persist (bool) : A boolean indicating whether to retain the last value outside of regular market hours, defaults to true

Returns: The lowest value during the current regular trading session, or na if the timeframe is not suitable

premarket_session_high(source, persist)

Returns the highest value of the specified source during the current premarket trading session

Parameters:

source (float) : The data series to evaluate, defaults to high

persist (bool) : A boolean indicating whether to retain the last value outside of premarket hours, defaults to true

Returns: The highest value during the current premarket trading session, or na if the timeframe is not suitable

premarket_session_low(source, persist)

Returns the lowest value of the specified source during the current premarket trading session

Parameters:

source (float) : The data series to evaluate, defaults to low

persist (bool) : A boolean indicating whether to retain the last value outside of premarket hours, defaults to true

Returns: The lowest value during the current premarket trading session, or na if the timeframe is not suitable

postmarket_session_high(source, persist)

Returns the highest value of the specified source during the current postmarket trading session

Parameters:

source (float) : The data series to evaluate, defaults to high

persist (bool) : A boolean indicating whether to retain the last value outside of postmarket hours, defaults to true

Returns: The highest value during the current postmarket trading session, or na if the timeframe is not suitable

postmarket_session_low(source, persist)

Returns the lowest value of the specified source during the current postmarket trading session

Parameters:

source (float) : The data series to evaluate, defaults to low

persist (bool) : A boolean indicating whether to retain the last value outside of postmarket hours, defaults to true

Returns: The lowest value during the current postmarket trading session, or na if the timeframe is not suitable

weekly_high(source)

Returns the highest value of the specified source during the current weekly session. Can fail on lower timeframes.

Parameters:

source (float) : The data series to evaluate, defaults to high

Returns: The highest value during the current weekly session, or na if the timeframe is not suitable

weekly_low(source)

Returns the lowest value of the specified source during the current weekly session. Can fail on lower timeframes.

Parameters:

source (float) : The data series to evaluate, defaults to low

Returns: The lowest value during the current weekly session, or na if the timeframe is not suitable

monthly_high(source)

Returns the highest value of the specified source during the current monthly session. Can fail on lower timeframes.

Parameters:

source (float) : The data series to evaluate, defaults to high

Returns: The highest value during the current monthly session, or na if the timeframe is not suitable

monthly_low(source)

Returns the lowest value of the specified source during the current monthly session. Can fail on lower timeframes.

Parameters:

source (float) : The data series to evaluate, defaults to low

Returns: The lowest value during the current monthly session, or na if the timeframe is not suitable

yearly_high(source)

Returns the highest value of the specified source during the current yearly session. Can fail on lower timeframes.

Parameters:

source (float) : The data series to evaluate, defaults to high

Returns: The highest value during the current yearly session, or na if the timeframe is not suitable

yearly_low(source)

Returns the lowest value of the specified source during the current yearly session. Can fail on lower timeframes.

Parameters:

source (float) : The data series to evaluate, defaults to low

Returns: The lowest value during the current yearly session, or na if the timeframe is not suitable

Timesessions

utilsLibrary "utils"

Provides a set of utility functions for use in strategies or indicators.

colorGreen(opacity)

Parameters:

opacity (int)

colorRed(opacity)

Parameters:

opacity (int)

colorTeal(opacity)

Parameters:

opacity (int)

colorBlue(opacity)

Parameters:

opacity (int)

colorOrange(opacity)

Parameters:

opacity (int)

colorPurple(opacity)

Parameters:

opacity (int)

colorPink(opacity)

Parameters:

opacity (int)

colorYellow(opacity)

Parameters:

opacity (int)

colorWhite(opacity)

Parameters:

opacity (int)

colorBlack(opacity)

Parameters:

opacity (int)

trendChangingUp(emaShort, emaLong)

Signals when the trend is starting to change in a positive direction.

Parameters:

emaShort (float)

emaLong (float)

Returns: bool

trendChangingDown(emaShort, emaLong)

Signals when the trend is starting to change in a negative direction.

Parameters:

emaShort (float)

emaLong (float)

Returns: bool

percentChange(start, end)

Returns the percent change between a start number and end number. A positive change returns a positive value and vice versa.

Parameters:

start (float)

end (float)

Returns: float

percentOf(percent, n)

Returns the number that's the percentage of the provided value.

Parameters:

percent (float) : Use 0.2 for 20 percent, 0.35 for 35 percent, etc.

n (float) : The number to calculate the percentage of.

Returns: float

targetPriceByPercent(percent, n)

Parameters:

percent (float)

n (float)

hasNegativeSlope(start, end)

Parameters:

start (float)

end (float)

timeinrange(resolution, session, timezone)

Returns true when the current time is within a given session window. Note, the time is calculated in the "America/New_York" timezone.

Parameters:

resolution (simple string) : The time interval to use to start/end the background color. Use "1" for the coloring the background up to the minute.

session (simple string) : The session string to use to identify the time window. Example: "0930-1600:23456" means normal market hours on weekdays.

timezone (simple string)

Returns: series bool

barsSinceLastEntry()

Returns the number of bars since the last entry order.

Returns: series int

barsSinceLastExit()

Returns the number of bars since the last exit order.

Returns: series int

calcSlope(ln, lookback)

Calculates the slope of the provided line based on its x,y coordinates in the previous bar to the current bar.

Parameters:

ln (float)

lookback (int)

Returns: series float

openPL()

Returns slope of the line given the start and end x,y coordinates.

Returns: series float

hasConsecutiveNegativeCandles(lookbackInput)

Returns true if the number of consecutive red candles matches the provided count.

Parameters:

lookbackInput (int) : The amount of bars to look back to check for consecutive negative bars. Default = 1.

Returns: series bool

stdevPercent(stdev, price)

Returns the standard deviation as a percentage of price.

Parameters:

stdev (float) : The standard deviation value

price (float) : The current price of the target ticker.

Returns: series float

HT: Functions LibLibrary "Functions"

is_date_equal(date1, date2, time_zone)

Parameters:

date1 (int)

date2 (int)

time_zone (string)

is_date_equal(date1, date2_str, time_zone)

Parameters:

date1 (int)

date2_str (string)

time_zone (string)

is_date_between(date_, start_year, start_month, end_year, end_month, time_zone_)

Parameters:

date_ (int)

start_year (int)

start_month (int)

end_year (int)

end_month (int)

time_zone_ (string)

is_time_equal(time1, time2_str, time_zone)

Parameters:

time1 (int)

time2_str (string)

time_zone (string)

is_time_equal(time1, time2, time_zone)

Parameters:

time1 (int)

time2 (int)

time_zone (string)

is_time_between(time_, start_hour, start_minute, end_hour, end_minute, time_zone_)

Parameters:

time_ (int)

start_hour (int)

start_minute (int)

end_hour (int)

end_minute (int)

time_zone_ (string)

is_time_between(time_, start_time, end_time, time_zone_)

Parameters:

time_ (int)

start_time (string)

end_time (string)

time_zone_ (string)

is_close(value, level, ticks)

Parameters:

value (float)

level (float)

ticks (int)

is_inrange(value, lb, hb)

Parameters:

value (float)

lb (float)

hb (float)

is_above(value, level, ticks)

Parameters:

value (float)

level (float)

ticks (int)

is_below(value, level, ticks)

Parameters:

value (float)

level (float)

ticks (int)

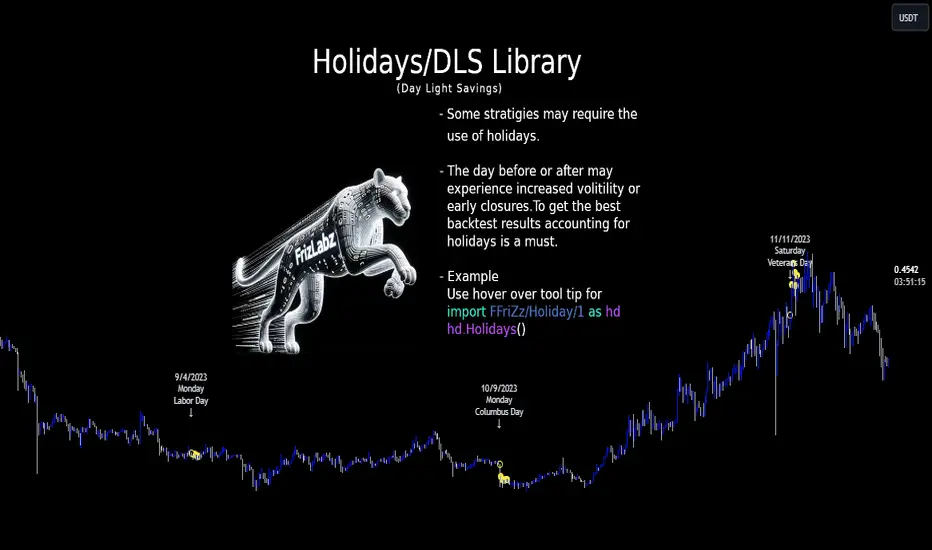

HolidayLibrary "Holiday"

- Full Control over Holidays and Daylight Savings Time (DLS)

The Holiday Library is an essential tool for traders and analysts who engage in backtesting and live trading . This comprehensive library enables the incorporation of crucial calendar elements - specifically Daylight Savings Time (DLS) adjustments and public holidays - into trading strategies and backtesting environments.

Key Features:

- DLS Adjustments: The library takes into account the shifts in time due to Daylight Savings. This feature is particularly vital for backtesting strategies, as DLS can impact trading hours, which in turn affects the volatility and liquidity in the market. Accurate DLS adjustments ensure that backtesting scenarios are as close to real-life conditions as possible.

- Comprehensive Holiday Metadata: The library includes a rich set of holiday metadata, allowing for the detailed scheduling of trading activities around public holidays. This feature is crucial for avoiding skewed results in backtesting, where holiday trading sessions might differ significantly in terms of volume and price movement.

- Customizable Holiday Schedules: Users can add or remove specific holidays, tailoring the library to fit various regional market schedules or specific trading requirements.

- Visualization Aids: The library supports on-chart labels, making it visually intuitive to identify holidays and DLS shifts directly on trading charts.

Use Cases:

1. Strategy Development: When developing trading strategies, it’s important to account for non-trading days and altered trading hours due to holidays and DLS. This library enables a realistic and accurate representation of these factors.

2. Risk Management: Trading around holidays can be riskier due to thinner liquidity and greater volatility. By integrating holiday data, traders can better manage their risk exposure.

3. Backtesting Accuracy: For backtesting to be effective, it must simulate the actual market conditions as closely as possible. Incorporating holidays and DLS adjustments contributes to more reliable and realistic backtesting results.

4. Global Trading: For traders active in multiple global markets, this library provides an easy way to handle different holiday schedules and DLS shifts across regions.

The Holiday Library is a versatile tool that enhances the precision and realism of trading simulations and strategy development . Its integration into the trading workflow is straightforward and beneficial for both novice and experienced traders.

EasterAlgo(_year)

Calculates the date of Easter Sunday for a given year using the Anonymous Gregorian algorithm.

`Gauss Algorithm for Easter Sunday` was developed by the mathematician Carl Friedrich Gauss

This algorithm is based on the cycles of the moon and the fact that Easter always falls on the first Sunday after the first ecclesiastical full moon that occurs on or after March 21.

While it's not considered to be 100% accurate due to rare exceptions, it does give the correct date in most cases.

It's important to note that Gauss's formula has been found to be inaccurate for some 21st-century years in the Gregorian calendar. Specifically, the next suggested failure years are 2038, 2051.

This function can be used for Good Friday (Friday before Easter), Easter Sunday, and Easter Monday (following Monday).

en.wikipedia.org

Parameters:

_year (int) : `int` - The year for which to calculate the date of Easter Sunday. This should be a four-digit year (YYYY).

Returns: tuple - The month (1-12) and day (1-31) of Easter Sunday for the given year.

easterInit()

Inits the date of Easter Sunday and Good Friday for a given year.

Returns: tuple - The month (1-12) and day (1-31) of Easter Sunday and Good Friday for the given year.

isLeapYear(_year)

Determine if a year is a leap year.

Parameters:

_year (int) : `int` - 4 digit year to check => YYYY

Returns: `bool` - true if input year is a leap year

method timezoneHelper(utc)

Helper function to convert UTC time.

Namespace types: series int, simple int, input int, const int

Parameters:

utc (int) : `int` - UTC time shift in hours.

Returns: `string`- UTC time string with shift applied.

weekofmonth()

Function to find the week of the month of a given Unix Time.

Returns: number - The week of the month of the specified UTC time.

dayLightSavingsAdjustedUTC(utc, adjustForDLS)

dayLightSavingsAdjustedUTC

Parameters:

utc (int) : `int` - The normal UTC timestamp to be used for reference.

adjustForDLS (bool) : `bool` - Flag indicating whether to adjust for daylight savings time (DLS).

Returns: `int` - The adjusted UTC timestamp for the given normal UTC timestamp.

getDayOfYear(monthOfYear, dayOfMonth, weekOfMonth, dayOfWeek, lastOccurrenceInMonth, holiday)

Function gets the day of the year of a given holiday (1-366)

Parameters:

monthOfYear (int)

dayOfMonth (int)

weekOfMonth (int)

dayOfWeek (int)

lastOccurrenceInMonth (bool)

holiday (string)

Returns: `int` - The day of the year of the holiday 1-366.

method buildMap(holidayMap, holiday, monthOfYear, weekOfMonth, dayOfWeek, dayOfMonth, lastOccurrenceInMonth, closingTime)

Function to build the `holidaysMap`.

Namespace types: map

Parameters:

holidayMap (map) : `map` - The map of holidays.

holiday (string) : `string` - The name of the holiday.

monthOfYear (int) : `int` - The month of the year of the holiday.

weekOfMonth (int) : `int` - The week of the month of the holiday.

dayOfWeek (int) : `int` - The day of the week of the holiday.

dayOfMonth (int) : `int` - The day of the month of the holiday.

lastOccurrenceInMonth (bool) : `bool` - Flag indicating whether the holiday is the last occurrence of the day in the month.

closingTime (int) : `int` - The closing time of the holiday.

Returns: `map` - The updated map of holidays

holidayInit(addHolidaysArray, removeHolidaysArray, defaultHolidays)

Initializes a HolidayStorage object with predefined US holidays.

Parameters:

addHolidaysArray (array) : `array` - The array of additional holidays to be added.

removeHolidaysArray (array) : `array` - The array of holidays to be removed.

defaultHolidays (bool) : `bool` - Flag indicating whether to include the default holidays.

Returns: `map` - The map of holidays.

Holidays(utc, addHolidaysArray, removeHolidaysArray, adjustForDLS, displayLabel, defaultHolidays)

Main function to build the holidays object, this is the only function from this library that should be needed. \

all functionality should be available through this function. \

With the exception of initializing a `HolidayMetaData` object to add a holiday or early close. \

\

**Default Holidays:** \

`DLS begin`, `DLS end`, `New Year's Day`, `MLK Jr. Day`, \

`Washington Day`, `Memorial Day`, `Independence Day`, `Labor Day`, \

`Columbus Day`, `Veterans Day`, `Thanksgiving Day`, `Christmas Day` \

\

**Example**

```

HolidayMetaData valentinesDay = HolidayMetaData.new(holiday="Valentine's Day", monthOfYear=2, dayOfMonth=14)

HolidayMetaData stPatricksDay = HolidayMetaData.new(holiday="St. Patrick's Day", monthOfYear=3, dayOfMonth=17)

HolidayMetaData addHolidaysArray = array.from(valentinesDay, stPatricksDay)

string removeHolidaysArray = array.from("DLS begin", "DLS end")

܂Holidays = Holidays(

܂ utc=-6,

܂ addHolidaysArray=addHolidaysArray,

܂ removeHolidaysArray=removeHolidaysArray,

܂ adjustForDLS=true,

܂ displayLabel=true,

܂ defaultHolidays=true,

܂ )

plot(Holidays.newHoliday ? open : na, title="newHoliday", color=color.red, linewidth=4, style=plot.style_circles)

```

Parameters:

utc (int) : `int` - The UTC time shift in hours

addHolidaysArray (array) : `array` - The array of additional holidays to be added

removeHolidaysArray (array) : `array` - The array of holidays to be removed

adjustForDLS (bool) : `bool` - Flag indicating whether to adjust for daylight savings time (DLS)

displayLabel (bool) : `bool` - Flag indicating whether to display a label on the chart

defaultHolidays (bool) : `bool` - Flag indicating whether to include the default holidays

Returns: `HolidayObject` - The holidays object | Holidays = (holidaysMap: map, newHoliday: bool, holiday: string, dayString: string)

HolidayMetaData

HolidayMetaData

Fields:

holiday (series string) : `string` - The name of the holiday.

dayOfYear (series int) : `int` - The day of the year of the holiday.

monthOfYear (series int) : `int` - The month of the year of the holiday.

dayOfMonth (series int) : `int` - The day of the month of the holiday.

weekOfMonth (series int) : `int` - The week of the month of the holiday.

dayOfWeek (series int) : `int` - The day of the week of the holiday.

lastOccurrenceInMonth (series bool)

closingTime (series int) : `int` - The closing time of the holiday.

utc (series int) : `int` - The UTC time shift in hours.

HolidayObject

HolidayObject

Fields:

holidaysMap (map) : `map` - The map of holidays.

newHoliday (series bool) : `bool` - Flag indicating whether today is a new holiday.

activeHoliday (series bool) : `bool` - Flag indicating whether today is an active holiday.

holiday (series string) : `string` - The name of the holiday.

dayString (series string) : `string` - The day of the week of the holiday.

ForecastingThis Forecasting library has a couple of Novel and traditional approaches to forecasting stock prices.

Traditionally, it provides a basic ARIMA forecaster using simple autoregression, as well as a linear regression and quadratic regression channel forecaster.

Novel approaches to forecasting include:

1) A Moving Average based Forecaster (modelled after ARIMA), it is capable of forecasting based on a user selected SMA.

2) Z-Score Forecast: Forecasting based on Z-Score (example displayed in chart).

Library "Forecasting"

ARIMA_Modeller(src)

: Creates a generic autoregressive ARIMA model

Parameters:

src (float)

Returns: : arima_result, arima_ucl, arima_lcl, arima_cor, arima_r2, arima_err, y1, y2, y3, y0

machine_learning_regression(output, x1, x2, x3, x4, x5, show_statistics)

: Creates an automatic regression based forecast model (can be used for other regression operations) from a list of possible independent variables.

Parameters:

output (float)

x1 (float)

x2 (float)

x3 (float)

x4 (float)

x5 (float)

show_statistics (bool)

Returns: : result, upper bound levels, lower bound levels, optional statitics table that displays the model parameters and statistics

time_series_linear_forecast(src, forecast_length, standard_deviation_extension_1, standard_deviation_extension_2)

: Creates a simple linear regression time series channel

Parameters:

src (float)

forecast_length (int)

standard_deviation_extension_1 (float)

standard_deviation_extension_2 (float)

Returns: : Linreg Channel

quadratic_time_series_forecast(src, forecast_length)

: Creates a simple quadratic regression time series channel

Parameters:

src (float)

forecast_length (int)

Returns: : Quadratic Regression Channel

moving_average_forecaster(source, train_time, ma_length, forecast_length, forecast_result, upper_bound_result, lower_bound_result)

: Creates an ARIMA style moving average forecaster

Parameters:

source (float)

train_time (int)

ma_length (int)

forecast_length (int)

forecast_result (float )

upper_bound_result (float )

lower_bound_result (float )

Returns: : forecast_result, upper_bound_result, lower_bound_result, moving_average, ucl, lcl

zscore_forecast(z_length, z_source, show_alerts, forecast_length, show_forecast_table)

: Creates a Z-Score Forecast and is capable of plotting the immediate forecast via a Polyline

Parameters:

z_length (int)

z_source (float)

show_alerts (bool)

forecast_length (int)

show_forecast_table (bool)

Returns: : The export is void, it will export the Polyline forecast and the Z-forecast table if you enable it.

chrono_utilsLibrary "chrono_utils"

Collection of objects and common functions that are related to datetime windows session days and time

ranges. The main purpose of this library is to handle time-related functionality and make it easy to reason about a

future bar and see if it is part of a predefined user session and/or inside a datetime window. All existing session

functions I found in the documentation e.g. "not na(time(timeframe, session, timezone))" are not suitable for

strategies, since the execution of the orders is delayed by one bar due to the execution happening at the bar close.

So a prediction for the next bar is necessary. Moreover, a history operator with a negative value is not allowed e.g.

`not na(time(timeframe, session, timezone) )` expression is not valid. Thus, I created this library to overcome

this small but very important limitation. In the meantime, I added useful functionality to handle session-based

behavior. An interesting utility that emerged from this development is data anomaly detection where a comparison

between the prediction and the actual value is happening. If those two values are different then a data inconsistency

happens between the prediction bar and the actual bar (probably due to a holiday or half session day etc..)

exTimezone(timezone)

exTimezone - Convert extended timezone to timezone string

Parameters:

timezone (simple string) : - The timezone or a special string

Returns: string representing the timezone

nameOfDay(day)

nameOfDay - Convert the day id into a short nameOfDay

Parameters:

day (int) : - The day id to convert

Returns: - The short name of the day

today()

today - Get the day id of this day

Returns: - The day id

nthDayAfter(day, n)

nthDayAfter - Get the day id of n days after the given day

Parameters:

day (int) : - The day id of the reference day

n (int) : - The number of days to go forward

Returns: - The day id of the day that is n days after the reference day

nextDayAfter(day)

nextDayAfter - Get the day id of next day after the given day

Parameters:

day (int) : - The day id of the reference day

Returns: - The day id of the next day after the reference day

nthDayBefore(day, n)

nthDayBefore - Get the day id of n days before the given day

Parameters:

day (int) : - The day id of the reference day

n (int) : - The number of days to go forward

Returns: - The day id of the day that is n days before the reference day

prevDayBefore(day)

prevDayBefore - Get the day id of previous day before the given day

Parameters:

day (int) : - The day id of the reference day

Returns: - The day id of the previous day before the reference day

tomorrow()

tomorrow - Get the day id of the next day

Returns: - The next day day id

normalize(num, min, max)

normalizeHour - Check if number is inthe range of

Parameters:

num (int)

min (int)

max (int)

Returns: - The normalized number

normalizeHour(hourInDay)

normalizeHour - Check if hour is valid and return a noralized hour range from

Parameters:

hourInDay (int)

Returns: - The normalized hour

normalizeMinute(minuteInHour)

normalizeMinute - Check if minute is valid and return a noralized minute from

Parameters:

minuteInHour (int)

Returns: - The normalized minute

monthInMilliseconds(mon)

monthInMilliseconds - Calculate the miliseconds in one bar of the timeframe

Parameters:

mon (int) : - The month of reference to get the miliseconds

Returns: - The number of milliseconds of the month

barInMilliseconds()

barInMilliseconds - Calculate the miliseconds in one bar of the timeframe

Returns: - The number of milliseconds in one bar

method init(this, fromDateTime, toDateTime)

init - Initialize the time window object from boolean values of each session day

Namespace types: DateTimeWindow

Parameters:

this (DateTimeWindow) : - The time window object that will hold the from and to datetimes

fromDateTime (int) : - The starting datetime of the time window

toDateTime (int) : - The ending datetime of the time window

Returns: - The time window object

method init(this, refTimezone, chTimezone, fromDateTime, toDateTime)

init - Initialize the time window object from boolean values of each session day

Namespace types: DateTimeWindow

Parameters:

this (DateTimeWindow) : - The time window object that will hold the from and to datetimes

refTimezone (simple string) : - The timezone of reference of the 'from' and 'to' dates

chTimezone (simple string) : - The target timezone to convert the 'from' and 'to' dates

fromDateTime (int) : - The starting datetime of the time window

toDateTime (int) : - The ending datetime of the time window

Returns: - The time window object

method init(this, sun, mon, tue, wed, thu, fri, sat)

init - Initialize the session days object from boolean values of each session day

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object that will hold the day selection

sun (bool) : - Is Sunday a trading day?

mon (bool) : - Is Monday a trading day?

tue (bool) : - Is Tuesday a trading day?

wed (bool) : - Is Wednesday a trading day?

thu (bool) : - Is Thursday a trading day?

fri (bool) : - Is Friday a trading day?

sat (bool) : - Is Saturday a trading day?

Returns: - The session days objectfrom_chart

method init(this, unixTime)

init - Initialize the object from the hour and minute of the session time in exchange timezone (syminfo.timezone)

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

unixTime (int) : - The unix time

Returns: - The session time object

method init(this, hourInDay, minuteInHour)

init - Initialize the object from the hour and minute of the session time in exchange timezone (syminfo.timezone)

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

hourInDay (int) : - The hour of the time

minuteInHour (int) : - The minute of the time

Returns: - The session time object

method init(this, hourInDay, minuteInHour, refTimezone)

init - Initialize the object from the hour and minute of the session time

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

hourInDay (int) : - The hour of the time

minuteInHour (int) : - The minute of the time

refTimezone (string) : - The timezone of reference of the 'hour' and 'minute'

Returns: - The session time object

method init(this, startTime, endTime)

init - Initialize the object from the start and end session time in exchange timezone (syminfo.timezone)

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object that will hold the start and end time of the daily session

startTime (SessionTime) : - The time the session begins

endTime (SessionTime) : - The time the session ends

Returns: - The session time range object

method init(this, startTimeHour, startTimeMinute, endTimeHour, endTimeMinute, refTimezone)

init - Initialize the object from the start and end session time

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object that will hold the start and end time of the daily session

startTimeHour (int) : - The time hour the session begins

startTimeMinute (int) : - The time minute the session begins

endTimeHour (int) : - The time hour the session ends

endTimeMinute (int) : - The time minute the session ends

refTimezone (string)

Returns: - The session time range object

method init(this, days, timeRanges)

init - Initialize the user session object from session days and time range

Namespace types: UserSession

Parameters:

this (UserSession) : - The user-defined session object that will hold the day and the time range selection

days (SessionDays) : - The session days object that defines the days the session is happening

timeRanges (SessionTimeRange ) : - The array of all the session time ranges during a session day

Returns: - The user session object

method to_string(this)

to_string - Formats the time window into a human-readable string

Namespace types: DateTimeWindow

Parameters:

this (DateTimeWindow) : - The time window object with the from and to datetimes

Returns: - The string of the time window

method to_string(this)

to_string - Formats the session days into a human-readable string with short day names

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object with the day selection

Returns: - The string of the session day short names

method to_string(this)

to_string - Formats the session time into a human-readable string

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

Returns: - The string of the session time

method to_string(this)

to_string - Formats the session time into a human-readable string

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object with the start and end time of the daily session

Returns: - The string of the session time

method to_string(this)

to_string - Formats the user session into a human-readable string

Namespace types: UserSession

Parameters:

this (UserSession) : - The user-defined session object with the day and the time range selection

Returns: - The string of the user session

method to_string(this)

to_string - Formats the bar into a human-readable string

Namespace types: Bar

Parameters:

this (Bar) : - The bar object with the open and close times

Returns: - The string of the bar times

method to_string(this)

to_string - Formats the chart session into a human-readable string

Namespace types: ChartSession

Parameters:

this (ChartSession) : - The chart session object that contains the days and the time range shown in the chart

Returns: - The string of the chart session

method get_size_in_secs(this)

get_size_in_secs - Count the seconds from start to end in the given timeframe

Namespace types: DateTimeWindow

Parameters:

this (DateTimeWindow) : - The time window object with the from and to datetimes

Returns: - The number of seconds inside the time widow for the given timeframe

method get_size_in_secs(this)

get_size_in_secs - Calculate the seconds inside the session

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object with the start and end time of the daily session

Returns: - The number of seconds inside the session

method get_size_in_bars(this)

get_size_in_bars - Count the bars from start to end in the given timeframe

Namespace types: DateTimeWindow

Parameters:

this (DateTimeWindow) : - The time window object with the from and to datetimes

Returns: - The number of bars inside the time widow for the given timeframe

method get_size_in_bars(this)

get_size_in_bars - Calculate the bars inside the session

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object with the start and end time of the daily session

Returns: - The number of bars inside the session for the given timeframe

method from_chart(this)

from_chart - Initialize the session days object from the chart

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object that will hold the day selection

Returns: - The user session object

method from_chart(this)

from_chart - Initialize the session time range object from the chart

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object that will hold the start and end time of the daily session

Returns: - The session time range object

method from_chart(this)

from_chart - Initialize the session object from the chart

Namespace types: ChartSession

Parameters:

this (ChartSession) : - The chart session object that will hold the days and the time range shown in the chart

Returns: - The chart session object

method to_sess_string(this)

to_sess_string - Formats the session days into a session string with day ids

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object

Returns: - The string of the session day ids

method to_sess_string(this)

to_sess_string - Formats the session time into a session string

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

Returns: - The string of the session time

method to_sess_string(this)

to_sess_string - Formats the session time into a session string

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object with the start and end time of the daily session

Returns: - The string of the session time

method to_sess_string(this)

to_sess_string - Formats the user session into a session string

Namespace types: UserSession

Parameters:

this (UserSession) : - The user-defined session object with the day and the time range selection

Returns: - The string of the user session

method to_sess_string(this)

to_sess_string - Formats the chart session into a session string

Namespace types: ChartSession

Parameters:

this (ChartSession) : - The chart session object that contains the days and the time range shown in the chart

Returns: - The string of the chart session

method from_sess_string(this, sess)

from_sess_string - Initialize the session days object from the session string

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object that will hold the day selection

sess (string) : - The session string part that represents the days

Returns: - The session days object

method from_sess_string(this, sess)

from_sess_string - Initialize the session time object from the session string in exchange timezone (syminfo.timezone)

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object that will hold the hour and minute of the time

sess (string) : - The session string part that represents the time HHmm

Returns: - The session time object

method from_sess_string(this, sess, refTimezone)

from_sess_string - Initialize the session time object from the session string

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object that will hold the hour and minute of the time

sess (string) : - The session string part that represents the time HHmm

refTimezone (simple string) : - The timezone of reference of the 'hour' and 'minute'

Returns: - The session time object

method from_sess_string(this, sess)

from_sess_string - Initialize the session time range object from the session string in exchange timezone (syminfo.timezone)

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object that will hold the start and end time of the daily session

sess (string) : - The session string part that represents the time range HHmm-HHmm

Returns: - The session time range object

method from_sess_string(this, sess, refTimezone)

from_sess_string - Initialize the session time range object from the session string

Namespace types: SessionTimeRange

Parameters:

this (SessionTimeRange) : - The session time range object that will hold the start and end time of the daily session

sess (string) : - The session string part that represents the time range HHmm-HHmm

refTimezone (simple string) : - The timezone of reference of the time ranges

Returns: - The session time range object

method from_sess_string(this, sess)

from_sess_string - Initialize the user session object from the session string in exchange timezone (syminfo.timezone)

Namespace types: UserSession

Parameters:

this (UserSession) : - The user-defined session object that will hold the day and the time range selection

sess (string) : - The session string that represents the user session HHmm-HHmm,HHmm-HHmm:ddddddd

Returns: - The session time range object

method from_sess_string(this, sess, refTimezone)

from_sess_string - Initialize the user session object from the session string

Namespace types: UserSession

Parameters:

this (UserSession) : - The user-defined session object that will hold the day and the time range selection

sess (string) : - The session string that represents the user session HHmm-HHmm,HHmm-HHmm:ddddddd

refTimezone (simple string) : - The timezone of reference of the time ranges

Returns: - The session time range object

method nth_day_after(this, day, n)

nth_day_after - The nth day after the given day that is a session day (true) in the object

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object with the day selection

day (int) : - The day id of the reference day

n (int) : - The number of days after

Returns: - The day id of the nth session day of the week after the given day

method nth_day_before(this, day, n)

nth_day_before - The nth day before the given day that is a session day (true) in the object

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object with the day selection

day (int) : - The day id of the reference day

n (int) : - The number of days after

Returns: - The day id of the nth session day of the week before the given day

method next_day(this)

next_day - The next day that is a session day (true) in the object

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object with the day selection

Returns: - The day id of the next session day of the week

method previous_day(this)

previous_day - The previous day that is session day (true) in the object

Namespace types: SessionDays

Parameters:

this (SessionDays) : - The session days object with the day selection

Returns: - The day id of the previous session day of the week

method get_sec_in_day(this)

get_sec_in_day - Count the seconds since the start of the day this session time represents

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

Returns: - The number of seconds passed from the start of the day until that session time

method get_ms_in_day(this)

get_ms_in_day - Count the milliseconds since the start of the day this session time represents

Namespace types: SessionTime

Parameters:

this (SessionTime) : - The session time object with the hour and minute of the time of the day

Returns: - The number of milliseconds passed from the start of the day until that session time

method eq(this, other)

eq - Compare two bars

Namespace types: Bar

Parameters:

this (Bar) : - The bar object with the open and close times

other (Bar) : - The bar object to compare with

Returns: - Whether this bar is equal to the other one

method get_open_time(this)

get_open_time - The open time object

Namespace types: Bar

Parameters:

this (Bar) : - The bar object with the open and close times

Returns: - The open time object

method get_close_time(this)

get_close_time - The close time object

Namespace types: Bar

Parameters:

this (Bar) : - The bar object with the open and close times

Returns: - The close time object

method get_time_range(this)

get_time_range - Get the time range of the bar

Namespace types: Bar

Parameters:

this (Bar) : - The bar object with the open and close times

Returns: - The time range that the bar is in

getBarNow()

getBarNow - Get the current bar object with time and time_close timestamps

Returns: - The current bar

getFixedBarNow()

getFixedBarNow - Get the current bar with fixed width defined by the timeframe. Note: There are case like SPX 15min timeframe where the last session bar is only 10min. This will return a bar of 15 minutes

Returns: - The current bar

method is_in_window(this, win)

is_in_window - Check if the given bar is between the start and end dates of the window

Namespace types: Bar

Parameters:

this (Bar) : - The bar to check if it is between the from and to datetimes of the window

win (DateTimeWindow) : - The time window object with the from and to datetimes

Returns: - Whether the current bar is inside the datetime window

method is_in_timerange(this, rng)

is_in_timerange - Check if the given bar is inside the session time range

Namespace types: Bar

Parameters:

this (Bar) : - The bar to check if it is between the from and to datetimes

rng (SessionTimeRange) : - The session time range object with the start and end time of the daily session

Returns: - Whether the bar is inside the session time range and if this part of the next trading day

method is_in_days(this, days)

is_in_days - Check if the given bar is inside the session days

Namespace types: Bar

Parameters:

this (Bar) : - The bar to check if its day is a trading day

days (SessionDays) : - The session days object with the day selection

Returns: - Whether the current bar day is inside the session

method is_in_session(this, sess)

is_in_session - Check if the given bar is inside the session as defined by the input params (what "not na(time(timeframe.period, this.to_sess_string()) )" should return if you could write it

Namespace types: Bar

Parameters:

this (Bar) : - The bar to check if it is between the from and to datetimes

sess (UserSession) : - The user-defined session object with the day and the time range selection

Returns: - Whether the current time is inside the session

method next_bar(this, offsetBars)

next_bar - Predicts the next bars open and close time based on the charts session

Namespace types: ChartSession

Parameters:

this (ChartSession) : - The chart session object that contains the days and the time range shown in the chart

offsetBars (simple int) : - The number of bars forward

Returns: - Whether the current time is inside the session

DateTimeWindow

DateTimeWindow - Object that represents a datetime window with a beginning and an end

Fields:

fromDateTime (series int) : - The beginning of the datetime window

toDateTime (series int) : - The end of the datetime window

SessionDays

SessionDays - Object that represent the trading days of the week

Fields:

days (map) : - The map that contains all days of the week and their session flag

SessionTime

SessionTime - Object that represents the time (hour and minutes)

Fields:

hourInDay (series int) : - The hour of the day that ranges from 0 to 24

minuteInHour (series int) : - The minute of the hour that ranges from 0 to 59

minuteInDay (series int) : - The minute of the day that ranges from 0 to 1440. They will be calculated based on hourInDay and minuteInHour when method is called

SessionTimeRange

SessionTimeRange - Object that represents a range that extends from the start to the end time

Fields:

startTime (SessionTime) : - The beginning of the time range

endTime (SessionTime) : - The end of the time range

isOvernight (series bool) : - Whether or not this is an overnight time range

UserSession

UserSession - Object that represents a user-defined session

Fields:

days (SessionDays) : - The map of the user-defined trading days

timeRanges (SessionTimeRange ) : - The array with all time ranges of the user-defined session during the trading days

Bar

Bar - Object that represents the bars' open and close times

Fields:

openUnixTime (series int) : - The open time of the bar

closeUnixTime (series int) : - The close time of the bar

chartDayOfWeek (series int)

ChartSession

ChartSession - Object that represents the default session that is shown in the chart

Fields:

days (SessionDays) : - A map with the trading days shown in the chart

timeRange (SessionTimeRange) : - The time range of the session during a trading day

isFinalized (series bool)

High Risk Trading TimeLibrary "HighRiskTradingTime"

Utilities for time range labeling

openTime()

timeMinInDay(t, timezone)

Convert given time to minutes of day

Parameters:

t (int) : Time

timezone (string) : Timezone of the input h:m

@return Minutes of day

All exported functions args should be typified

timeMinInDayManual(h, m)

Convert given hour and minute to minutes of day

Parameters:

h (int) : Hour in a day

m (int) : Minute in a day

isForexHighRiskTime()

Return if current time is High Risk for Forex

TimeFormattingLibraryLibrary "TimeFormattingLibrary"

Time formatting functions: formating functions to make timestrings more human readable friendly (for both fixed time and time-elapsed).

Also functions for last and first instance in month of day of week input.

Also a function for identifying bank holiday Mondays.

timeFormatFxn(showDayOfWeek, showDayOfMonth, showMonth, showYear, showHrMin, _time, _timezone)

converts time into readable format

Parameters:

showDayOfWeek (bool) : if you want to show day of week (i.e. Mon, Tues etc)

showDayOfMonth (bool) : if you want to show day number of month with superscript ordinals (i.e. 1ˢᵗ, 2ⁿᵈ, etc)

showMonth (bool) : if you want to show the month (i.e. Jan, Feb, etc)

showYear (bool) : if you want to show the year (i.e. 2023)

showHrMin (bool) : if you want to show time in 24hr clock format

_time (int) : is the unix time (i.e. time or time_close)

_timezone (string) : the user timezone input as string (e.g. "America/New_York", "UTC-5", "GMT+0530")

Returns: time date string

timeElapsedFxn(timespan)

converts timespan into readable format

Parameters:

timespan (int) : is the length of time in milliseconds to be converted into a human readable string

Returns: timespan string (whether it be a for showing 'time-elapsed' or for showing a 'countdown timer')

isFirstXdayofmonth(_dayofweek)

gives bool result for when first occurence in month of the day-of-week input

Parameters:

_dayofweek (int) : (can be integer 1-7 or can be dayofweek variable; i.e. dayofweek.wednesday)

isLastXdayofmonth(_dayofweek)

gives bool result for when last occurence in month of the day-of-week input

Parameters:

_dayofweek (int) : (can be integer 1-7 or can be dayofweek variable; i.e. dayofweek.wednesday)

wasBankHolidayMonday()

gives bool result for if yesterday was a bank holiday monday. Only for use with with request.security() function, see example code below

MarketHolidaysLibrary "MarketHolidays"

The MarketHolidays library compiles market holidays (including historical special market closures) into arrays, which can then be utilized in TradingView indicators and strategies to account for non-trading days. The datasets were split into different libraries to overcome compiling limitations, streamline the process of removing specific time frames if not needed, and to enhance code execution speed. The timestamps are generated using a custom Python script that employs the 'pandas_market_calendars' library. To build your own set of arrays, you can find the script and instructions at github.com

getHolidays(_country)

The getHolidays function aggregates holiday data from different time periods to create a single array with market holidays for a specified country.

Parameters:

_country (string) : The country code for which to retrieve market holidays. Accepts syminfo.country or pre-set country code in ISO 3166-1 alpha-2 format.

Returns: An array of timestamps of market holidays \ non-trading days for the given country.

holidays_2020to2025Library "holidays_2020to2025"

This dataset is part of my "MarketHolidays" library. The datasets were split into different libraries to overcome compiling limitations, streamline the process of removing specific time frames if not needed, and to enhance code execution speed. The timestamps are generated using a custom Python script that employs the 'pandas_market_calendars' library. To build your own set of arrays, you can find the script and instructions at github.com

holidays(_country)

Parameters:

_country (string)

holidays_2015to2020Library "holidays_2015to2020"

This dataset is part of my "MarketHolidays" library. The datasets were split into different libraries to overcome compiling limitations, streamline the process of removing specific time frames if not needed, and to enhance code execution speed. The timestamps are generated using a custom Python script that employs the 'pandas_market_calendars' library. To build your own set of arrays, you can find the script and instructions at github.com

holidays(_country)

Parameters:

_country (string)

holidays_2010to2015Library "holidays_2010to2015"

This dataset is part of my "MarketHolidays" library. The datasets were split into different libraries to overcome compiling limitations, streamline the process of removing specific time frames if not needed, and to enhance code execution speed. The timestamps are generated using a custom Python script that employs the 'pandas_market_calendars' library. To build your own set of arrays, you can find the script and instructions at github.com

holidays(_country)

Parameters:

_country (string)

holidays_2005to2010Library "holidays_2005to2010"

This dataset is part of my "MarketHolidays" library. The datasets were split into different libraries to overcome compiling limitations, streamline the process of removing specific time frames if not needed, and to enhance code execution speed. The timestamps are generated using a custom Python script that employs the 'pandas_market_calendars' library. To build your own set of arrays, you can find the script and instructions at github.com

holidays(_country)

Parameters:

_country (string)

holidays_2000to2005Library "holidays_2000to2005"

This dataset is part of my "MarketHolidays" library. The datasets were split into different libraries to overcome compiling limitations, streamline the process of removing specific time frames if not needed, and to enhance code execution speed. The timestamps are generated using a custom Python script that employs the 'pandas_market_calendars' library. To build your own set of arrays, you can find the script and instructions at github.com

holidays(_country)

Parameters:

_country (string)

holidays_1990to2000Library "holidays_1990to2000"

This dataset is part of my "MarketHolidays" library. The datasets were split into different libraries to overcome compiling limitations, streamline the process of removing specific time frames if not needed, and to enhance code execution speed. The timestamps are generated using a custom Python script that employs the 'pandas_market_calendars' library. To build your own set of arrays, you can find the script and instructions at github.com

holidays(_country)

Parameters:

_country (string)

holidays_1980to1990Library "holidays_1980to1990"

This dataset is part of my "MarketHolidays" library. The datasets were split into different libraries to overcome compiling limitations, streamline the process of removing specific time frames if not needed, and to enhance code execution speed. The timestamps are generated using a custom Python script that employs the 'pandas_market_calendars' library. To build your own set of arrays, you can find the script and instructions at github.com

holidays(_country)

Parameters:

_country (string)

holidays_1970to1980Library "holidays_1970to1980"

This dataset is part of my "MarketHolidays" library. The datasets were split into different libraries to overcome compiling limitations, streamline the process of removing specific time frames if not needed, and to enhance code execution speed. The timestamps are generated using a custom Python script that employs the 'pandas_market_calendars' library. To build your own set of arrays, you can find the script and instructions at github.com

holidays(_country)

Parameters:

_country (string)

holidays_1962to1970Library "holidays_1962to1970"

This dataset is part of my "MarketHolidays" library. The datasets were split into different libraries to overcome compiling limitations, streamline the process of removing specific time frames if not needed, and to enhance code execution speed. The timestamps are generated using a custom Python script that employs the 'pandas_market_calendars' library. To build your own set of arrays, you can find the script and instructions at github.com

holidays(_country)

Parameters:

_country (string)

chrono_utilsLibrary "chrono_utils"

📝 Description

Collection of objects and common functions that are related to datetime windows session days and time ranges. The main purpose of this library is to handle time-related functionality and make it easy to reason about a future bar checking if it will be part of a predefined session and/or inside a datetime window. All existing session functionality I found in the documentation e.g. "not na(time(timeframe, session, timezone))" are not suitable for strategy scripts, since the execution of the orders is delayed by one bar, due to the script execution happening at the bar close. Moreover, a history operator with a negative value that looks forward is not allowed in any pinescript expression. So, a prediction for the next bar using the bars_back argument of "time()"" and "time_close()" was necessary. Thus, I created this library to overcome this small but very important limitation. In the meantime, I added useful functionality to handle session-based behavior. An interesting utility that emerged from this development is data anomaly detection where a comparison between the prediction and the actual value is happening. If those two values are different then a data inconsistency happens between the prediction bar and the actual bar (probably due to a holiday, half session day, a timezone change etc..)

🤔 How to Guide

To use the functionality this library provides in your script you have to import it first!

Copy the import statement of the latest release by pressing the copy button below and then paste it into your script. Give a short name to this library so you can refer to it later on. The import statement should look like this:

import jason5480/chrono_utils/2 as chr

To check if a future bar will be inside a window first of all you have to initialize a DateTimeWindow object.

A code example is the following:

var dateTimeWindow = chr.DateTimeWindow.new().init(fromDateTime = timestamp('01 Jan 2023 00:00'), toDateTime = timestamp('01 Jan 2024 00:00'))

Then you have to "ask" the dateTimeWindow if the future bar defined by an offset (default is 1 that corresponds th the next bar), will be inside that window:

// Filter bars outside of the datetime window

bool dateFilterApproval = dateTimeWindow.is_bar_included()

You can visualize the result by drawing the background of the bars that are outside the given window:

bgcolor(color = dateFilterApproval ? na : color.new(color.fuchsia, 90), offset = 1, title = 'Datetime Window Filter')

In the same way, you can "ask" the Session if the future bar defined by an offset it will be inside that session.

First of all, you should initialize a Session object.

A code example is the following:

var sess = chr.Session.new().from_sess_string(sess = '0800-1700:23456', refTimezone = 'UTC')

Then check if the given bar defined by the offset (default is 1 that corresponds th the next bar), will be inside the session like that:

// Filter bars outside the sessions

bool sessionFilterApproval = view.sess.is_bar_included()

You can visualize the result by drawing the background of the bars that are outside the given session:

bgcolor(color = sessionFilterApproval ? na : color.new(color.red, 90), offset = 1, title = 'Session Filter')

In case you want to visualize multiple session ranges you can create a SessionView object like that:

var view = SessionView.new().init(SessionDays.new().from_sess_string('2345'), array.from(SessionTimeRange.new().from_sess_string('0800-1600'), SessionTimeRange.new().from_sess_string('1300-2200')), array.from('London', 'New York'), array.from(color.blue, color.orange))

and then call the draw method of the SessionView object like that:

view.draw()

🏋️♂️ Please refer to the "EXAMPLE DATETIME WINDOW FILTER" and "EXAMPLE SESSION FILTER" regions of the script for more advanced code examples of how to utilize the full potential of this library, including user input settings and advanced visualization!

⚠️ Caveats

As I mentioned in the description there are some cases that the prediction of the next bar is not accurate. A wrong prediction will affect the outcome of the filtering. The main reasons this could happen are the following:

Public holidays when the market is closed

Half trading days usually before public holidays

Change in the daylight saving time (DST)

A data anomaly of the chart, where there are missing and/or inconsistent data.

A bug in this library (Please report by PM sending the symbol, timeframe, and settings)

Special thanks to @robbatt and @skinra for the constructive feedback 🏆. Without them, the exposed API of this library would be very lengthy and complicated to use. Thanks to them, now the user of this library will be able to get the most, with only a few lines of code!

SessionVolumeProfileLibrary "SessionVolumeProfile"

Analyzes price & volume during regular trading hours to provide a session volume profile analysis. The primary goal of this library is to provide the developer with three values: the value area high, low and the point of control. The library also provides methods for rendering the value areas and histograms. To learn more about this library and how you can use it, click on the website link in my profile where you will find a blog post with detailed information.

debug(vp, position)

Helper function to write some information about the supplied SVP object to the screen in a table.

Parameters:

vp (Object) : The SVP object to debug

position (string) : The position.* to place the table. Defaults to position.bottom_center

getLowerTimeframe()

Depending on the timeframe of the chart, determines a lower timeframe to grab volume data from for the analysis

Returns: The timeframe string to fetch volume for

get(volumeProfile, lowerTimeframeHigh, lowerTimeframeLow, lowerTimeframeVolume)

Populated the provided SessionVolumeProfile object with vp data on the session.

Parameters:

volumeProfile (Object) : The SessionVolumeProfile object to populate

lowerTimeframeHigh (float ) : The lower timeframe high values

lowerTimeframeLow (float ) : The lower timeframe low values

lowerTimeframeVolume (float ) : The lower timeframe volume values

drawPriorValueAreas(todaySessionVolumeProfile, extendYesterdayOverToday, showLabels, labelSize, pocColor, pocStyle, pocWidth, vahlColor, vahlStyle, vahlWidth, vaColor)

Given a SessionVolumeProfile Object, will render the historical value areas for that object.

Parameters:

todaySessionVolumeProfile (Object) : The SessionVolumeProfile Object to draw

extendYesterdayOverToday (bool) : Defaults to true

showLabels (bool) : Defaults to true

labelSize (string) : Defaults to size.small

pocColor (color) : Defaults to #e500a4

pocStyle (string) : Defaults to line.style_solid

pocWidth (int) : Defaults to 1

vahlColor (color) : The color of the value area high/low lines. Defaults to #1592e6

vahlStyle (string) : The style of the value area high/low lines. Defaults to line.style_solid

vahlWidth (int) : The width of the value area high/low lines. Defaults to 1

vaColor (color) : The color of the value area background. Defaults to #00bbf911)

drawHistogram(volumeProfile, bgColor, showVolumeOnHistogram)

Given a SessionVolumeProfile object, will render the histogram for that object.

Parameters:

volumeProfile (Object) : The SessionVolumeProfile object to draw

bgColor (color) : The baseline color to use for the histogram. Defaults to #00bbf9

showVolumeOnHistogram (bool) : Show the volume amount on the histogram bars. Defaults to false.

Object

Fields:

numberOfRows (series__integer)

valueAreaCoverage (series__integer)

trackDevelopingVa (series__bool)

valueAreaHigh (series__float)

pointOfControl (series__float)

valueAreaLow (series__float)

startTime (series__integer)

endTime (series__integer)

dayHigh (series__float)

dayLow (series__float)

step (series__float)

pointOfControlLevel (series__integer)

valueAreaHighLevel (series__integer)

valueAreaLowLevel (series__integer)

volumeRows (array__float)

priceLevelRows (array__float)

ltfSessionHighs (array__float)

ltfSessionLows (array__float)

ltfSessionVols (array__float)

CalendarCadLibrary "CalendarCad"

This library provides date and time data of the important events on CAD. Data source is csv exported from www.fxstreet.com and transformed into perfered format by C# script.

HighImpactNews2015To2023()

CAD high impact news date and time from 2015 to 2023

CalendarEurLibrary "CalendarEur"

This library provides date and time data of the important events on EUR. Data source is csv exported from www.fxstreet.com and transformed into perfered format by C# script.

HighImpactNews2015To2019()

EUR high impact news date and time from 2015 to 2019

HighImpactNews2020To2023()

EUR high impact news date and time from 2020 to 2023

CalendarGbpLibrary "CalendarGbp"

This library provides date and time data of the important events on GBP. Data source is csv exported from www.fxstreet.com and transformed into perfered format by C# script.

HighImpactNews2015To2019()

GBP high impact news date and time from 2015 to 2019

HighImpactNews2020To2023()

GBP high impact news date and time from 2020 to 2023