Anomalous Holonomy Field Theory🌌 Anomalous Holonomy Field Theory (AHFT) - Revolutionary Quantum Market Analysis

Where Theoretical Physics Meets Trading Reality

A Groundbreaking Synthesis of Differential Geometry, Quantum Field Theory, and Market Dynamics

🔬 THEORETICAL FOUNDATION - THE MATHEMATICS OF MARKET REALITY

The Anomalous Holonomy Field Theory represents an unprecedented fusion of advanced mathematical physics with practical market analysis. This isn't merely another indicator repackaging old concepts - it's a fundamentally new lens through which to view and understand market structure .

1. HOLONOMY GROUPS (Differential Geometry)

In differential geometry, holonomy measures how vectors change when parallel transported around closed loops in curved space. Applied to markets:

Mathematical Formula:

H = P exp(∮_C A_μ dx^μ)

Where:

P = Path ordering operator

A_μ = Market connection (price-volume gauge field)

C = Closed price path

Market Implementation:

The holonomy calculation measures how price "remembers" its journey through market space. When price returns to a previous level, the holonomy captures what has changed in the market's internal geometry. This reveals:

Hidden curvature in the market manifold

Topological obstructions to arbitrage

Geometric phase accumulated during price cycles

2. ANOMALY DETECTION (Quantum Field Theory)

Drawing from the Adler-Bell-Jackiw anomaly in quantum field theory:

Mathematical Formula:

∂_μ j^μ = (e²/16π²)F_μν F̃^μν

Where:

j^μ = Market current (order flow)

F_μν = Field strength tensor (volatility structure)

F̃^μν = Dual field strength

Market Application:

Anomalies represent symmetry breaking in market structure - moments when normal patterns fail and extraordinary opportunities arise. The system detects:

Spontaneous symmetry breaking (trend reversals)

Vacuum fluctuations (volatility clusters)

Non-perturbative effects (market crashes/melt-ups)

3. GAUGE THEORY (Theoretical Physics)

Markets exhibit gauge invariance - the fundamental physics remains unchanged under certain transformations:

Mathematical Formula:

A'_μ = A_μ + ∂_μΛ

This ensures our signals are gauge-invariant observables , immune to arbitrary market "coordinate changes" like gaps or reference point shifts.

4. TOPOLOGICAL DATA ANALYSIS

Using persistent homology and Morse theory:

Mathematical Formula:

β_k = dim(H_k(X))

Where β_k are the Betti numbers describing topological features that persist across scales.

🎯 REVOLUTIONARY SIGNAL CONFIGURATION

Signal Sensitivity (0.5-12.0, default 2.5)

Controls the responsiveness of holonomy field calculations to market conditions. This parameter directly affects the threshold for detecting quantum phase transitions in price action.

Optimization by Timeframe:

Scalping (1-5min): 1.5-3.0 for rapid signal generation

Day Trading (15min-1H): 2.5-5.0 for balanced sensitivity

Swing Trading (4H-1D): 5.0-8.0 for high-quality signals only

Score Amplifier (10-200, default 50)

Scales the raw holonomy field strength to produce meaningful signal values. Higher values amplify weak signals in low-volatility environments.

Signal Confirmation Toggle

When enabled, enforces additional technical filters (EMA and RSI alignment) to reduce false positives. Essential for conservative strategies.

Minimum Bars Between Signals (1-20, default 5)

Prevents overtrading by enforcing quantum decoherence time between signals. Higher values reduce whipsaws in choppy markets.

👑 ELITE EXECUTION SYSTEM

Execution Modes:

Conservative Mode:

Stricter signal criteria

Higher quality thresholds

Ideal for stable market conditions

Adaptive Mode:

Self-adjusting parameters

Balances signal frequency with quality

Recommended for most traders

Aggressive Mode:

Maximum signal sensitivity

Captures rapid market moves

Best for experienced traders in volatile conditions

Dynamic Position Sizing:

When enabled, the system scales position size based on:

Holonomy field strength

Current volatility regime

Recent performance metrics

Advanced Exit Management:

Implements trailing stops based on ATR and signal strength, with mode-specific multipliers for optimal profit capture.

🧠 ADAPTIVE INTELLIGENCE ENGINE

Self-Learning System:

The strategy analyzes recent trade outcomes and adjusts:

Risk multipliers based on win/loss ratios

Signal weights according to performance

Market regime detection for environmental adaptation

Learning Speed (0.05-0.3):

Controls adaptation rate. Higher values = faster learning but potentially unstable. Lower values = stable but slower adaptation.

Performance Window (20-100 trades):

Number of recent trades analyzed for adaptation. Longer windows provide stability, shorter windows increase responsiveness.

🎨 REVOLUTIONARY VISUAL SYSTEM

1. Holonomy Field Visualization

What it shows: Multi-layer quantum field bands representing market resonance zones

How to interpret:

Blue/Purple bands = Primary holonomy field (strongest resonance)

Band width = Field strength and volatility

Price within bands = Normal quantum state

Price breaking bands = Quantum phase transition

Trading application: Trade reversals at band extremes, breakouts on band violations with strong signals.

2. Quantum Portals

What they show: Entry signals with recursive depth patterns indicating momentum strength

How to interpret:

Upward triangles with portals = Long entry signals

Downward triangles with portals = Short entry signals

Portal depth = Signal strength and expected momentum

Color intensity = Probability of success

Trading application: Enter on portal appearance, with size proportional to portal depth.

3. Field Resonance Bands

What they show: Fibonacci-based harmonic price zones where quantum resonance occurs

How to interpret:

Dotted circles = Minor resonance levels

Solid circles = Major resonance levels

Color coding = Resonance strength

Trading application: Use as dynamic support/resistance, expect reactions at resonance zones.

4. Anomaly Detection Grid

What it shows: Fractal-based support/resistance with anomaly strength calculations

How to interpret:

Triple-layer lines = Major fractal levels with high anomaly probability

Labels show: Period (H8-H55), Price, and Anomaly strength (φ)

⚡ symbol = Extreme anomaly detected

● symbol = Strong anomaly

○ symbol = Normal conditions

Trading application: Expect major moves when price approaches high anomaly levels. Use for precise entry/exit timing.

5. Phase Space Flow

What it shows: Background heatmap revealing market topology and energy

How to interpret:

Dark background = Low market energy, range-bound

Purple glow = Building energy, trend developing

Bright intensity = High energy, strong directional move

Trading application: Trade aggressively in bright phases, reduce activity in dark phases.

📊 PROFESSIONAL DASHBOARD METRICS

Holonomy Field Strength (-100 to +100)

What it measures: The Wilson loop integral around price paths

>70: Strong positive curvature (bullish vortex)

<-70: Strong negative curvature (bearish collapse)

Near 0: Flat connection (range-bound)

Anomaly Level (0-100%)

What it measures: Quantum vacuum expectation deviation

>70%: Major anomaly (phase transition imminent)

30-70%: Moderate anomaly (elevated volatility)

<30%: Normal quantum fluctuations

Quantum State (-1, 0, +1)

What it measures: Market wave function collapse

+1: Bullish eigenstate |↑⟩

0: Superposition (uncertain)

-1: Bearish eigenstate |↓⟩

Signal Quality Ratings

LEGENDARY: All quantum fields aligned, maximum probability

EXCEPTIONAL: Strong holonomy with anomaly confirmation

STRONG: Good field strength, moderate anomaly

MODERATE: Decent signals, some uncertainty

WEAK: Minimal edge, high quantum noise

Performance Metrics

Win Rate: Rolling performance with emoji indicators

Daily P&L: Real-time profit tracking

Adaptive Risk: Current risk multiplier status

Market Regime: Bull/Bear classification

🏆 WHY THIS CHANGES EVERYTHING

Traditional technical analysis operates on 100-year-old principles - moving averages, support/resistance, and pattern recognition. These work because many traders use them, creating self-fulfilling prophecies.

AHFT transcends this limitation by analyzing markets through the lens of fundamental physics:

Markets have geometry - The holonomy calculations reveal this hidden structure

Price has memory - The geometric phase captures path-dependent effects

Anomalies are predictable - Quantum field theory identifies symmetry breaking

Everything is connected - Gauge theory unifies disparate market phenomena

This isn't just a new indicator - it's a new way of thinking about markets . Just as Einstein's relativity revolutionized physics beyond Newton's mechanics, AHFT revolutionizes technical analysis beyond traditional methods.

🔧 OPTIMAL SETTINGS FOR MNQ 10-MINUTE

For the Micro E-mini Nasdaq-100 on 10-minute timeframe:

Signal Sensitivity: 2.5-3.5

Score Amplifier: 50-70

Execution Mode: Adaptive

Min Bars Between: 3-5

Theme: Quantum Nebula or Dark Matter

💭 THE JOURNEY - FROM IMPOSSIBLE THEORY TO TRADING REALITY

Creating AHFT was a mathematical odyssey that pushed the boundaries of what's possible in Pine Script. The journey began with a seemingly impossible question: Could the profound mathematical structures of theoretical physics be translated into practical trading tools?

The Theoretical Challenge:

Months were spent diving deep into differential geometry textbooks, studying the works of Chern, Simons, and Witten. The mathematics of holonomy groups and gauge theory had never been applied to financial markets. Translating abstract mathematical concepts like parallel transport and fiber bundles into discrete price calculations required novel approaches and countless failed attempts.

The Computational Nightmare:

Pine Script wasn't designed for quantum field theory calculations. Implementing the Wilson loop integral, managing complex array structures for anomaly detection, and maintaining computational efficiency while calculating geometric phases pushed the language to its limits. There were moments when the entire project seemed impossible - the script would timeout, produce nonsensical results, or simply refuse to compile.

The Breakthrough Moments:

After countless sleepless nights and thousands of lines of code, breakthrough came through elegant simplifications. The realization that market anomalies follow patterns similar to quantum vacuum fluctuations led to the revolutionary anomaly detection system. The discovery that price paths exhibit holonomic memory unlocked the geometric phase calculations.

The Visual Revolution:

Creating visualizations that could represent 4-dimensional quantum fields on a 2D chart required innovative approaches. The multi-layer holonomy field, recursive quantum portals, and phase space flow representations went through dozens of iterations before achieving the perfect balance of beauty and functionality.

The Balancing Act:

Perhaps the greatest challenge was maintaining mathematical rigor while ensuring practical trading utility. Every formula had to be both theoretically sound and computationally efficient. Every visual had to be both aesthetically pleasing and information-rich.

The result is more than a strategy - it's a synthesis of pure mathematics and market reality that reveals the hidden order within apparent chaos.

📚 INTEGRATED DOCUMENTATION

Once applied to your chart, AHFT includes comprehensive tooltips on every input parameter. The source code contains detailed explanations of the mathematical theory, practical applications, and optimization guidelines. This published description provides the overview - the indicator itself is a complete educational resource.

⚠️ RISK DISCLAIMER

While AHFT employs advanced mathematical models derived from theoretical physics, markets remain inherently unpredictable. No mathematical model, regardless of sophistication, can guarantee future results. This strategy uses realistic commission ($0.62 per contract) and slippage (1 tick) in all calculations. Past performance does not guarantee future results. Always use appropriate risk management and never risk more than you can afford to lose.

🌟 CONCLUSION

The Anomalous Holonomy Field Theory represents a quantum leap in technical analysis - literally. By applying the profound insights of differential geometry, quantum field theory, and gauge theory to market analysis, AHFT reveals structure and opportunities invisible to traditional methods.

From the holonomy calculations that capture market memory to the anomaly detection that identifies phase transitions, from the adaptive intelligence that learns and evolves to the stunning visualizations that make the invisible visible, every component works in mathematical harmony.

This is more than a trading strategy. It's a new lens through which to view market reality.

Trade with the precision of physics. Trade with the power of mathematics. Trade with AHFT.

I hope this serves as a good replacement for Quantum Edge Pro - Adaptive AI until I'm able to fix it.

— Dskyz, Trade with insight. Trade with anticipation.

Volatility

BB Oscillator - Price Relative to Bollinger BandsThis Bollinger Band Oscillator visualizes where the current price sits relative to its Bollinger Bands, scaled between 0 and 100. It helps identify overbought and oversold conditions based on the price’s position within the bands and provides dynamic signals when momentum shifts occur.

Features

Price Relative to Bollinger Bands

The main oscillator plots the price’s relative position within the Bollinger Bands on a scale from 0 (lower band) to 100 (upper band), giving an intuitive view of where price stands.

Customizable Moving Average Overlay

An optional moving average (SMA or EMA) smooths the oscillator for trend analysis, with adjustable length and color options.

Crossover & Crossunder Signals

Alerts and background highlights trigger when the oscillator crosses over or under its moving average, signaling potential momentum shifts or trend changes.

Fully Customizable Colors

Choose your preferred colors for the oscillator line, moving average and crossover signals to match your charting style.

This tool offers a unique oscillator view of Bollinger Bands, combining volatility context with momentum signals for clearer decision-making.

Toolbar-FrenToolbar-Fren is a comprehensive, data-rich toolbar designed to present a wide array of key metrics in a compact and intuitive format. The core philosophy of this indicator is to maximize the amount of relevant, actionable data available to the trader while occupying minimal chart space. It leverages a dynamic color-coded system to provide at-a-glance insights into market conditions, instantly highlighting positive/negative values, trend strength, and proximity to important technical levels.

Features and Data Displayed

The toolbar displays a vertical column of critical data points, primarily calculated on the Daily timeframe to give a broader market context. Each cell is color-coded for quick interpretation.

DAY:

The percentage change of the current price compared to the previous day's close. The cell is colored green for a positive change and red for a negative one.

LOD:

The current price's percentage distance from the Low of the Day.

HOD

The current price's percentage distance from the High of the Day.

MA Distances (9/21 or 10/20, 50, 200)

These cells show how far the current price is from key Daily moving averages (MAs).

The values are displayed either as a percentage distance or as a multiple of the Average Daily Range (ADR), which can be toggled in the settings.

The cells are colored green if the price is above the corresponding MA (bullish) and red if it is below (bearish).

ADR

Shows the 14-period Average Daily Range as a percentage of the current price. The cell background uses a smooth gradient from green (low volatility) to red (high volatility) to visualize the current daily range expansion.

ADR%/50: A unique metric showing the distance from the Daily 50 SMA, measured in multiples of the 14-period Average True Range (ATR). This helps quantify how extended the price is from its mean. The cell is color-coded from green (close to the mean) to red (highly extended).

RSI

The standard 14-period Relative Strength Index calculated on the Daily timeframe. The background color changes to indicate potentially overbought (orange/red) or oversold (green) conditions.

ADX

The 14-period Average Directional Index (ADX) from the Daily timeframe, which measures trend strength. The cell is colored to reflect the strength of the trend (e.g., green for a strong trend, red for a weak/non-trending market). An arrow (▲/▼) is also displayed to indicate if the ADX value is sloping up or down.

User Customization

The indicator offers several options for personalization to fit your trading style and visual preferences:

MA Type

Choose between using Exponential Moving Averages (EMA 9/21) or Simple Moving Averages (SMA 10/20) for the primary MA calculations.

MA Distance Display

Toggle the display of moving average distances between standard percentage values and multiples of the Average Daily Range (ADR).

Display Settings

Fully customize the on-chart appearance by selecting the table's position (e.g., Top Right, Bottom Left) and the text size. An option for a larger top margin is also available.

Colors

Personalize the core Green, Yellow, Orange, and Red colors used throughout the indicator to match your chart's theme.

Technical Parameters

Fine-tune the length settings for the ADX and DI calculations.

VWAP %BVWAP %B - Volume Weighted Average Price Percent B

The VWAP %B indicator combines the reliability of VWAP (Volume Weighted Average Price) with the analytical power of %B oscillators, similar to Bollinger Bands %B but using volume-weighted statistics.

## How It Works

This indicator calculates where the current price sits relative to VWAP-based standard deviation bands, expressed as a percentage from 0 to 1:

• **VWAP Calculation**: Uses volume-weighted average price as the center line

• **Standard Deviation Bands**: Creates upper and lower bands using standard deviation around VWAP

• **%B Formula**: %B = (Price - Lower Band) / (Upper Band - Lower Band)

## Key Levels & Interpretation

• **Above 1.0**: Price is trading above the upper VWAP band (strong bullish momentum)

• **0.8 - 1.0**: Overbought territory, potential resistance

• **0.5**: Price exactly at VWAP (equilibrium)

• **0.2 - 0.0**: Oversold territory, potential support

• **Below 0.0**: Price is trading below the lower VWAP band (strong bearish momentum)

## Trading Applications

**Trend Following**: During strong trends, breaks above 1.0 or below 0.0 often signal continuation rather than reversal.

**Mean Reversion**: In ranging markets, extreme readings (>0.8 or <0.2) may indicate potential reversal points.

**Volume Context**: Unlike traditional %B, this incorporates volume weighting, making it more reliable during high-volume periods.

## Parameters

• **Length (20)**: Period for standard deviation calculation

• **Standard Deviation Multiplier (2.0)**: Controls band width

• **Source (close)**: Price input for calculations

## Visual Features

• Reference lines at key levels (0, 0.2, 0.5, 0.8, 1.0)

• Background highlighting for extreme breaks

• Real-time values table

• Clean oscillator format below price chart

Perfect for intraday traders and swing traders who want to combine volume analysis with momentum oscillators.

Approximate Entropy Zones [PhenLabs]Version: PineScript™ v6

Description

This indicator identifies periods of market complexity and randomness by calculating the Approximate Entropy (ApEn) of price action. As the movement of the market becomes complex, it means the current trend is losing steam and a reversal or consolidation is likely near. The indicator plots high-entropy periods as zones on your chart, providing a graphical suggestion to anticipate a potential market direction change. This indicator is designed to help traders identify favorable times to get in or out of a trade by highlighting when the market is in a state of disarray.

Points of Innovation

Advanced Complexity Analysis: Instead of relying on traditional momentum or trend indicators, this tool uses Approximate Entropy to quantify the unpredictability of price movements.

Dynamic Zone Creation: It automatically plots zones on the chart during periods of high entropy, providing a clear and intuitive visual guide.

Customizable Sensitivity: Users can fine-tune the ‘Entropy Threshold’ to adjust how frequently zones appear, allowing for calibration to different assets and timeframes.

Time-Based Zone Expiration: Zones can be set to expire after a specific time, keeping the chart clean and relevant.

Built-in Zone Size Filter: Excludes zones that form on excessively large candles, filtering out noise from extreme volatility events.

On-Chart Calibration Guide: A persistent note on the chart provides simple instructions for adjusting the entropy threshold, making it easy for users to optimize the indicator’s performance.

Core Components

Approximate Entropy (ApEn) Calculation: The core of the indicator, which measures the complexity or randomness of the price data.

Zone Plotting: Creates visual boxes on the chart when the calculated ApEn value exceeds a user-defined threshold.

Dynamic Zone Management: Manages the lifecycle of the zones, from creation to expiration, ensuring the chart remains uncluttered.

Customizable Settings: A comprehensive set of inputs that allow users to control the indicator’s sensitivity, appearance, and time-based behavior.

Key Features

Identifies Potential Reversals: The high-entropy zones can signal that a trend is nearing its end, giving traders an early warning.

Works on Any Timeframe: The indicator can be applied to any chart timeframe, from minutes to days.

Customizable Appearance: Users can change the color and transparency of the zones to match their chart’s theme.

Informative Labels: Each zone can display the calculated entropy value and the direction of the candle on which it formed.

Visualization

Entropy Zones: Shaded boxes that appear on the chart, highlighting candles with high complexity.

Zone Labels: Text within each zone that displays the ApEn value and a directional arrow (e.g., “0.525 ↑”).

Calibration Note: A small table in the top-right corner of the chart with instructions for adjusting the indicator’s sensitivity.

Usage Guidelines

Entropy Analysis

Source: The price data used for the ApEn calculation. (Default: close)

Lookback Length: The number of bars used in the ApEn calculation. (Default: 20, Range: 10-50)

Embedding Dimension (m): The length of patterns to be compared; a standard value for financial data. (Default: 2)

Tolerance Multiplier (r): Adjusts the tolerance for pattern matching; a larger value makes matching more lenient. (Default: 0.2)

Entropy Threshold: The ApEn value that must be exceeded to plot a zone. Increase this if too many zones appear; decrease it if too few appear. (Default: 0.525)

Time Settings

Analysis Timeframe: How long a zone remains on the chart after it forms. (Default: 1D)

Custom Period (Bars): The zone’s lifespan in bars if “Analysis Timeframe” is set to “Custom”. (Default: 1000)

Zone Settings

Zone Fill Color: The color of the entropy zones. (Default: #21f38a with 80% transparency)

Maximum Zone Size %: Filters out zones on candles that are larger than this percentage of their low price. (Default: 0.5)

Display Options

Show Entropy Label: Toggles the visibility of the text label inside each zone. (Default: true)

Label Text Position: The horizontal alignment of the text label. (Default: Right)

Show Calibration Note: Toggles the visibility of the calibration note in the corner of the chart. (Default: true)

Best Use Cases

Trend Reversal Trading: Identifying when a strong trend is likely to reverse or pause.

Breakout Confirmation: Using the absence of high entropy to confirm the strength of a breakout.

Ranging Market Identification: Periods of high entropy can indicate that a market is transitioning into a sideways or choppy phase.

Limitations

Not a Standalone Signal: This indicator should be used in conjunction with other forms of analysis to confirm trading signals.

Lagging Nature: Like all indicators based on historical data, ApEn is a lagging measure and does not predict future price movements with certainty.

Calibration Required: The effectiveness of the indicator is highly dependent on the “Entropy Threshold” setting, which needs to be adjusted for different assets and timeframes.

What Makes This Unique

Quantifies Complexity: It provides a numerical measure of market complexity, offering a different perspective than traditional indicators.

Clear Visual Cues: The zones make it easy to see when the market is in a state of high unpredictability.

User-Friendly Design: With features like the on-chart calibration note, the indicator is designed to be easy to use and optimize.

How It Works

Calculate Standard Deviation: The indicator first calculates the standard deviation of the source price data over a specified lookback period.

Calculate Phi: It then calculates a value called “phi” for two different pattern lengths (embedding dimensions ‘m’ and ‘m+1’). This involves comparing sequences of data points to see how many are “similar” within a certain tolerance (determined by the standard deviation and the ‘r’ multiplier).

Calculate ApEn: The Approximate Entropy is the difference between the two phi values. A higher ApEn value indicates greater irregularity and unpredictability in the data.

Plot Zones: If the calculated ApEn exceeds the user-defined ‘Entropy Threshold’, a zone is plotted on the chart.

Note: The “Entropy Threshold” is the most important setting to adjust. If you see too many zones, increase the threshold. If you see too few, decrease it.

ADR Pivot LevelsThe ADR (Average Daily Range) indicator shows the average range of price movement over a trading day. The ADR is used to estimate volatility and to determine target levels. It helps to set Take-Profit and Stop-Loss orders. It is suitable for intraday trading on lower time frames.

The “ADR Pivot Levels” produces a sequence of horizontal line levels above and below the Center Line (reference level). They are sized based on the instrument's volatility, representing the average historical price movement on a selected higher timeframe using the average daily range (ADR) indicator.

TitanGrid L/S SuperEngineTitanGrid L/S SuperEngine

Experimental Trend-Aligned Grid Signal Engine for Long & Short Execution

🔹 Overview

TitanGrid is an advanced, real-time signal engine built around a tactical grid structure.

It manages Long and Short trades using trend-aligned entries, layered scaling, and partial exits.

Unlike traditional strategy() -based scripts, TitanGrid runs as an indicator() , but includes its own full internal simulation engine.

This allows it to track capital, equity, PnL, risk exposure, and trade performance bar-by-bar — effectively simulating a custom backtest, while remaining compatible with real-time alert-based execution systems.

The concept was born from the fusion of two prior systems:

Assassin’s Grid (grid-based execution and structure) + Super 8 (trend-filtering, smart capital logic), both developed under the AssassinsGrid framework.

🔹 Disclaimer

This is an experimental tool intended for research, testing, and educational use.

It does not provide guaranteed outcomes and should not be interpreted as financial advice.

Use with demo or simulated accounts before considering live deployment.

🔹 Execution Logic

Trend direction is filtered through a custom SuperTrend engine. Once confirmed:

• Long entries trigger on pullbacks, exiting progressively as price moves up

• Short entries trigger on rallies, exiting as price declines

Grid levels are spaced by configurable percentage width, and entries scale dynamically.

🔹 Stop Loss Mechanism

TitanGrid uses a dual-layer stop system:

• A static stop per entry, placed at a fixed percentage distance matching the grid width

• A trend reversal exit that closes the entire position if price crosses the SuperTrend in the opposite direction

Stops are triggered once per cycle, ensuring predictable and capital-aware behavior.

🔹 Key Features

• Dual-side grid logic (Long-only, Short-only, or Both)

• SuperTrend filtering to enforce directional bias

• Adjustable grid spacing, scaling, and sizing

• Static and dynamic stop-loss logic

• Partial exits and reset conditions

• Webhook-ready alerts (browser-based automation compatible)

• Internal simulation of equity, PnL, fees, and liquidation levels

• Real-time dashboard for full transparency

🔹 Best Use Cases

TitanGrid performs best in structured or mean-reverting environments.

It is especially well-suited to assets with the behavioral profile of ETH — reactive, trend-intraday, and prone to clean pullback formations.

While adaptable to multiple timeframes, it shows strongest performance on the 15-minute chart , offering a balance of signal frequency and directional clarity.

🔹 License

Published under the Mozilla Public License 2.0 .

You are free to study, adapt, and extend this script.

🔹 Panel Reference

The real-time dashboard displays performance metrics, capital state, and position behavior:

• Asset Type – Automatically detects the instrument class (e.g., Crypto, Stock, Forex) from symbol metadata

• Equity – Total simulated capital: realized PnL + floating PnL + remaining cash

• Available Cash – Capital not currently allocated to any position

• Used Margin – Capital locked in open trades, based on position size and leverage

• Net Profit – Realized gain/loss after commissions and fees

• Raw Net Profit – Gross result before trading costs

• Floating PnL – Unrealized profit or loss from active positions

• ROI – Return on initial capital, including realized and floating PnL. Leverage directly impacts this metric, amplifying both gains and losses relative to account size.

• Long/Short Size & Avg Price – Open position sizes and volume-weighted average entry prices

• Leverage & Liquidation – Simulated effective leverage and projected liquidation level

• Hold – Best-performing hold side (Long or Short) over the session

• Hold Efficiency – Performance efficiency during holding phases, relative to capital used

• Profit Factor – Ratio of gross profits to gross losses (realized)

• Payoff Ratio – Average profit per win / average loss per loss

• Win Rate – Percent of profitable closes (including partial exits)

• Expectancy – Net average result per closed trade

• Max Drawdown – Largest recorded drop in equity during the session

• Commission Paid – Simulated trading costs: maker, taker, funding

• Long / Short Trades – Count of entry signals per side

• Time Trading – Number of bars spent in active positions

• Volume / Month – Extrapolated 30-day trading volume estimate

• Min Capital – Lowest equity level recorded during the session

🔹 Reference Ranges by Strategy Type

Use the following metrics as reference depending on the trading style:

Grid / Mean Reversion

• Profit Factor: 1.2 – 2.0

• Payoff Ratio: 0.5 – 1.2

• Win Rate: 50% – 70% (based on partial exits)

• Expectancy: 0.05% – 0.25%

• Drawdown: Moderate to high

• Commission Impact: High

Trend-Following

• Profit Factor: 1.5 – 3.0

• Payoff Ratio: 1.5 – 3.5

• Win Rate: 30% – 50%

• Expectancy: 0.3% – 1.0%

• Drawdown: Low to moderate

Scalping / High-Frequency

• Profit Factor: 1.1 – 1.6

• Payoff Ratio: 0.3 – 0.8

• Win Rate: 80% – 95%

• Expectancy: 0.01% – 0.05%

• Volume / Month: Very high

Breakout Strategies

• Profit Factor: 1.4 – 2.2

• Payoff Ratio: 1.2 – 2.0

• Win Rate: 35% – 60%

• Expectancy: 0.2% – 0.6%

• Drawdown: Can be sharp after failed breakouts

🔹 Note on Performance Simulation

TitanGrid includes internal accounting of fees, slippage, and funding costs.

While its logic is designed for precision and capital efficiency, performance is naturally affected by exchange commissions.

In frictionless environments (e.g., zero-fee simulation), its high-frequency logic could — in theory — extract substantial micro-edges from the market.

However, real-world conditions introduce limits, and all results should be interpreted accordingly.

COV Bands ~ C H I P ACOV Bands ~ C H I P A is a custom volatility and trend identification tool designed to capture directional shifts using the Coefficient of Variation (COV), calculated from standard deviation relative to a mean price baseline.

Key features include:

A configurable SMA-based mean baseline to anchor volatility measurements clearly.

Adjustable upper and lower band multipliers to independently calibrate sensitivity and responsiveness for bullish or bearish breakouts.

Dynamic bands derived from price-relative volatility (COV), enabling adaptive identification of significant price deviations.

User-controlled standard deviation length to manage sensitivity and smoothness of volatility signals.

Direct candle coloring, providing immediate visual feedback using vibrant electric blue for bullish momentum and bright red for bearish momentum.

This indicator is particularly useful for detecting meaningful price movements, breakout signals, and potential reversals when the market moves significantly beyond its typical volatility boundaries.

Note: This indicator has not undergone formal robustness or optimization testing. Therefore, future performance in live trading environments isn't guaranteed.

Candle Range % vs 8-Candle AvgCandle % Indicator – Measure Candle Strength by Range %

**Overview:**

The *Candle % Indicator* helps traders visually and analytically gauge the strength or significance of a price candle relative to its recent historical context. This is particularly useful for detecting breakout moves, volatility shifts, or overextended candles that may signal exhaustion.

**What It Does:**

* Calculates the **percentage range** of the current candle compared to the **average range of the past N candles**.

* Highlights candles that exceed a user-defined threshold (e.g., 150% of the average range).

* Useful for **filtering out extreme candles** that might represent anomalies or unsustainable moves.

* Can be combined with other strategies (like EMA crossovers, support/resistance breaks, etc.) to improve signal quality.

**Use Case Examples:**

***Filter out fakeouts** in breakout strategies by ignoring candles that are overly large and may revert.

***Volatility control**: Avoid entries when market conditions are erratic.

**Confluence**: Combine with EMA or RSI signals for refined entries.

**How to Read:**

* If a candle is larger than the average range by more than the set percentage (default 150%), it's flagged (e.g., no entry signal or optional visual marker).

* Ideal for intraday, swing, or algorithmic trading setups.

**Customizable Inputs:**

**Lookback Period**: Number of previous candles to calculate the average range.

**% Threshold**: Maximum percentage a candle can exceed the average before being filtered or marked.

ATR RopeATR Rope is inspired by DonovanWall's "Range Filter". It implements a similar concept of filtering out smaller market movements and adjusting only for larger moves. In addition, this indicator goes one step deeper by producing actionable zones to determine market state. (Trend vs. Consolidation)

> Background

When reading up on the Range Filter indicator, it reminded me exactly of a Rope stabilization drawing tool in a program I use frequently. Rope stabilization essentially attaches a fixed length "rope" to your cursor and an anchor point (Brush). As you move your cursor, you are pulling the brush behind it. The cursor (of course) will not pull the brush until the rope is fully extended, this behavior filters out jittery movements and is used to produce smoother drawing curves.

If compared visually side-by-side, you will notice that this indicator bears striking resemblance to its inspiration.

> Goal

Other than simply distinguishing price movements between meaningful and noise, this indicator strives to create a rigid structure to frame market movements and lack-there-of, such as when to anticipate trend, and when to suspect consolidation.

Since the indicator works based on an ATR range, the resulting ATR Channel does well to get reactions from price at its extremes. Naturally, when consolidating, price will remain within the channel, neither pushing the channel significantly up or down. Likewise, when trending, price will continue to push the channel in a single direction.

With the goal of keeping it quick and simple, this indicator does not do any smoothing of data feeds, and is simply based on the deviation of price from the central rope. Adjusting the rope when price extends past the threshold created by +/- ATR from the rope.

> Features & Behaviors

- ATR Rope

ATR Rope is displayed as a 3 color single line.

This can be considered the center line, or the directional line, whichever you'd prefer.

The main point of the Rope display is to indicate direction, however it also is factually the center of the current working range.

- ATR Rope Color

When the rope's value moves up, it changes to green (uptrend), when down, red (downtrend).

When the source crosses the rope, it turns blue (flat).

With these simple rules, we've formed a structure to view market movements.

- Consolidation Zones

Consolidation Zones generate from "Flat" areas, and extend into subsequent trend areas. Consolidation is simply areas where price has crossed the Rope and remains inside the range. Over these periods, the upper and lower values are accumulated and averaged together to form the "Consolidation Zone" values. These zones are draw live, so values are averaged as the flat areas progress and don't repaint, so all values seen historically are as they would appear live.

- ATR Channel

ATR Channel displays the upper and lower bounds of the working range.

When the source moves beyond this range, the rope is adjusted based on the distance from the source to the channel. This range can be extremely useful to view, but by default it is hidden.

> Application

This indicator is not created to provide signals, or serve as a "complete" system.

(People who didn't read this far will still comment for signals. :) )

This is created to be used alongside manual interpretation and intuition. This indicator is not meant to constrain any users into a box, and I would actually encourage an open mind and idea generation, as the application of this indicator can take various forms.

> Examples

As you would probably already know, price movement can be fast impulses, and movement can be slow bleeds. In the screenshot below, we are using movements from and to consolidation zones to classify weak trend and strong trend. As you can see, there are also areas of consolidation which get broken out of and confirmed for the larger moves.

Author's Note: In each of these examples, I have outlined the start and end of each session. These examples come from 1 Min Future charts, and have specifically been framed with day trading in mind.

"Breakout Retest" or "Support/Resistance Flips" or "Structure Retests" are all generally the same thing, with different traders referring to them by different names, all of which can be seen throughout these examples.

In the next example, we have a day which started with an early reversal leading into long, slow, trend. Notice how each area throughout the trend essentially moves slightly higher, then consolidates while holding support of the previous zone. This day had a few sharp movements, however there was a large amount of neutrality throughout this day with continuous higher lows.

In contrast to the previous example, next up, we have a very choppy day. Throughout which we see a significant amount of retests before fast directional movements. We also see a few examples of places where previous zones remained relevant into the future. While the zones only display into the resulting trend area, they do not become immediately meaningless once they stop drawing.

> Abstract

In the screenshot below, I have stacked 2 of these indicators, using the high as the source for one and the low as the source for the other. I've hidden lines of the high and low channels to create a 4 lined channel based on the wicks of price.

This is not necessary to use the indicator, but should help provide an idea of creative ways the simple indicator could be used to produce more complicated analysis.

If you've made it this far, I would hope it's clear to you how this indicator could provide value to your trading.

Thank you to DonovonWall for the inspiration.

Enjoy!

Donchian x WMA Crossover (2025 Only, Adjustable TP, Real OHLC)Short Description:

Long-only breakout system that goes long when the Donchian Low crosses up through a Weighted Moving Average, and closes when it crosses back down (with an optional take-profit), restricted to calendar year 2025. All signals use the instrument’s true OHLC data (even on Heikin-Ashi charts), start with 1 000 AUD of capital, and deploy 100 % equity per trade.

Ideal parameters configured for Temple & Webster on ASX 30 minute candles. Adjust parameter to suit however best to download candle interval data and have GPT test the pine script for optimum parameters for your trading symbol.

Detailed Description

1. Strategy Concept

This strategy captures trend-driven breakouts off the bottom of a Donchian channel. By combining the Donchian Low with a WMA filter, it aims to:

Enter when volatility compresses and price breaks above the recent Donchian Low while the longer‐term WMA confirms upward momentum.

Exit when price falls back below that same WMA (i.e. when the Donchian Low crosses back down through WMA), but only if the WMA itself has stopped rising.

Optional Take-Profit: you can specify a profit target in decimal form (e.g. 0.01 = 1 %).

2. Timeframe & Universe

In-sample period: only bars stamped between Jan 1 2025 00:00 UTC and Dec 31 2025 23:59 UTC are considered.

Any resolution (e.g. 30 m, 1 h, D, etc.) is supported—just set your preferred timeframe in the TradingView UI.

3. True-Price Execution

All indicator calculations (Donchian Low, WMA, crossover checks, take-profit) are sourced from the chart’s underlying OHLC via request.security(). This guarantees that:

You can view Heikin-Ashi or other styled candles, but your strategy will execute on the real OHLC bars.

Chart styling never suppresses or distorts your backtest results.

4. Position Sizing & Equity

Initial capital: 1 000 AUD

Size per trade: 100 % of available equity

No pyramiding: one open position at a time

5. Inputs (all exposed in the “Inputs” tab):

Input Default Description

Donchian Length 7 Number of bars to calculate the Donchian channel low

WMA Length 62 Period of the Weighted Moving Average filter

Take Profit (decimal) 0.01 Exit when price ≥ entry × (1 + take_profit_perc)

6. How It Works

Donchian Low: ta.lowest(low, DonchianLength) over the specified look-back.

WMA: ta.wma(close, WMALength) applied to true closes.

Entry: ta.crossover(DonchianLow, WMA) AND barTime ∈ 2025.

Exit:

Cross-down exit: ta.crossunder(DonchianLow, WMA) and WMA is not rising (i.e. momentum has stalled).

Take-profit exit: price ≥ entry × (1 + take_profit_perc).

Calendar exit: barTime falls outside 2025.

7. Usage Notes

After adding to your chart, open the Strategy Tester tab to review performance metrics, list of trades, equity curve, etc.

You can toggle your chart to Heikin-Ashi for visual clarity without affecting execution, thanks to the real-OHLC calls.

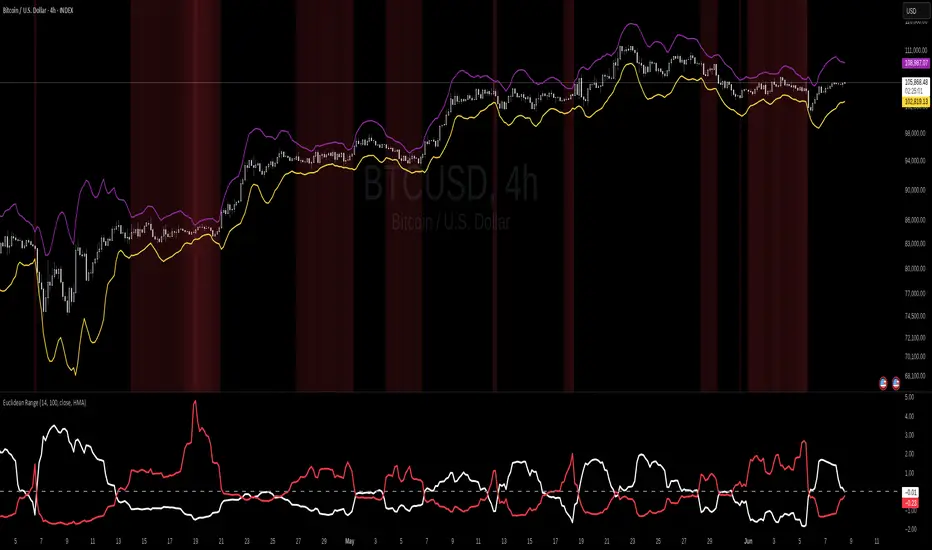

Euclidean Range [InvestorUnknown]The Euclidean Range indicator visualizes price deviation from a moving average using a geometric concept Euclidean distance. It helps traders identify trend strength, volatility shifts, and potential overextensions in price behavior.

Euclidean Distance

Euclidean distance is a fundamental concept in geometry and machine learning. It measures the "straight-line distance" between two points in space. In time series analysis, it can be used to measure how far one sequence deviates from another over a fixed window.

euclidean_distance(src, ref, len) =>

var float sum_sq_diff = na

sum_sq_diff := 0.0

for i = 0 to len - 1

diff = src - ref

sum_sq_diff += diff * diff

math.sqrt(sum_sq_diff)

In this script, we calculate the Euclidean distance between the price (source) and a smoothed average (reference) over a user-defined window. This gives us a single scalar that reflects the overall divergence between price and trend.

How It Works

Moving Average Calculation: You can choose between SMA, EMA, or HMA as your reference line. This becomes the "baseline" against which the actual price is compared.

Distance Band Construction: The Euclidean distance between the price and the reference is calculated over the Window Length. This value is then added to and subtracted from the average to form dynamic upper and lower bands, visually framing the range of deviation.

Distance Ratios and Z-Scores: Two distance ratios are computed: dist_r = distance / price (sensitivity to volatility); dist_v = price / distance (sensitivity to compression or low-volatility states)

Both ratios are normalized using a Z-score to standardize their behavior and allow for easier interpretation across different assets and timeframes.

Z-Score Plots: Z_r (white line) highlights instances of high volatility or strong price deviation; Z_v (red line) highlights low volatility or compressed price ranges.

Background Highlighting (Optional): When Z_v is dominant and increasing, the background is colored using a gradient. This signals a possible build-up in low volatility, which may precede a breakout.

Use Cases

Detect volatile expansions and calm compression zones.

Identify mean reversion setups when price returns to the average.

Anticipate breakout conditions by observing rising Z_v values.

Use dynamic distance bands as adaptive support/resistance zones.

Notes

The indicator is best used with liquid assets and medium-to-long windows.

Background coloring helps visually filter for squeeze setups.

Disclaimer

This indicator is provided for speculative analysis and educational purposes only. It is not financial advice. Always backtest and evaluate in a simulated environment before live trading.

Bands Vision-XBands Vision-X (BB-Vision-X) – Full Description

Description:

Bands Vision-X is an indicator based on dynamic bands constructed from customizable moving averages and standard deviation, allowing you to visualize potential support and resistance zones, volatility, and market conditions. It uses an adjustable moving average (with multiple options such as SMA, EMA, WMA, JMA, LSMA, DEMA, and TEMA) to define the central line, and upper and lower bands calculated by standard deviation multiplied by an adjustable factor. The bands are smoothed by a Hull Moving Average (HMA) to reduce noise and improve clarity.

How to Use

The bands indicate potential support and resistance levels.

The central line serves as a dynamic price reference.

The distance between bands reflects market volatility.

Touches or breakouts of the bands may signal entry or exit opportunities.

Parameters

Parameter Description Default

Standard Error Band Period Period for moving average and standard deviation 20

Moving Average Type Type of moving average (SMA, EMA, etc.) SMA

Standard Deviation Multiplier Multiplier for standard deviation 2.0

Band Lines Smoothing Period Period for smoothing the bands (HMA) 5

Technical Notes

The JMA function used is not the original Jurik version but an approximate and open implementation based on publicly available TradingView community code.

Developed in Pine Script v6 with optimized and clean code.

Recommendations

Ideal for traders seeking a clear view of volatility and dynamic support/resistance levels.

Should not be used in isolation; it is recommended to combine with volume analysis, price action, or other technical indicators.

Adjust the period and multiplier according to the asset and timeframe for better effectiveness.

Candle Body Strength CounterThis indicator measures the total bullish and bearish candle body strength over a user-defined lookback period. For each bar, it sums the absolute body sizes of bullish candles (where close > open) and bearish candles (where close < open) within the lookback window. The result is two lines: one for bullish body strength and one for bearish body strength, making it easy to spot shifts in market momentum and bias.

Adjustable lookback period (default: 20 bars)

Green line: cumulative bullish body strength

Red line: cumulative bearish body strength

Use this tool to quickly assess which side (bulls or bears) has been stronger over your chosen timeframe.

ICT Directional FVG Indicator (Buffered SL)This is the first indicator I have ever made, and I am very new to Pine Script. I’ve tried my best to create this as a strategy, but I’m still learning, so please be kind and constructive with your feedback!

ICT Directional FVG Indicator (Buffered SL)

This indicator is designed for traders who follow ICT (Inner Circle Trader) concepts, focusing on Fair Value Gaps (FVGs), liquidity sweeps, and session-based trading. It automatically detects bullish and bearish FVGs, highlights them on the chart, and identifies liquidity sweep events. The indicator features three customizable Kill Zones (London, New York, and Asia sessions), each with independent toggles and color-coded backgrounds for clear visual separation.

Key features:

Fair Value Gap Detection: Highlights bullish and bearish FVGs in real time.

Liquidity Sweep Alerts: Marks potential liquidity sweep events for both highs and lows.

Session Kill Zones: Toggle each Kill Zone (London, New York, Asia) independently; background color changes only in enabled zones.

Trade Signal Visualization: Plots entry, stop loss, and take profit levels based on FVG and sweep logic, with a user-defined stop loss buffer.

Customizable Display: Easily enable or disable FVGs, sweeps, trade levels, and each Kill Zone to suit your strategy.

This tool is ideal for ICT-based traders who want a clear, automated view of FVGs, sweeps, and session activity, with full control over which sessions and signals are displayed.

Langlands-Operadic Möbius Vortex (LOMV)Langlands-Operadic Möbius Vortex (LOMV)

Where Pure Mathematics Meets Market Reality

A Revolutionary Synthesis of Number Theory, Category Theory, and Market Dynamics

🎓 THEORETICAL FOUNDATION

The Langlands-Operadic Möbius Vortex represents a groundbreaking fusion of three profound mathematical frameworks that have never before been combined for market analysis:

The Langlands Program: Harmonic Analysis in Markets

Developed by Robert Langlands (Fields Medal recipient), the Langlands Program creates bridges between number theory, algebraic geometry, and harmonic analysis. In our indicator:

L-Function Implementation:

- Utilizes the Möbius function μ(n) for weighted price analysis

- Applies Riemann zeta function convergence principles

- Calculates quantum harmonic resonance between -2 and +2

- Measures deep mathematical patterns invisible to traditional analysis

The L-Function core calculation employs:

L_sum = Σ(return_val × μ(n) × n^(-s))

Where s is the critical strip parameter (0.5-2.5), controlling mathematical precision and signal smoothness.

Operadic Composition Theory: Multi-Strategy Democracy

Category theory and operads provide the mathematical framework for composing multiple trading strategies into a unified signal. This isn't simple averaging - it's mathematical composition using:

Strategy Composition Arity (2-5 strategies):

- Momentum analysis via RSI transformation

- Mean reversion through Bollinger Band mathematics

- Order Flow Polarity Index (revolutionary T3-smoothed volume analysis)

- Trend detection using Directional Movement

- Higher timeframe momentum confirmation

Agreement Threshold System: Democratic voting where strategies must reach consensus before signal generation. This prevents false signals during market uncertainty.

Möbius Function: Number Theory in Action

The Möbius function μ(n) forms the mathematical backbone:

- μ(n) = 1 if n is a square-free positive integer with even number of prime factors

- μ(n) = -1 if n is a square-free positive integer with odd number of prime factors

- μ(n) = 0 if n has a squared prime factor

This creates oscillating weights that reveal hidden market periodicities and harmonic structures.

🔧 COMPREHENSIVE INPUT SYSTEM

Langlands Program Parameters

Modular Level N (5-50, default 30):

Primary lookback for quantum harmonic analysis. Optimized by timeframe:

- Scalping (1-5min): 15-25

- Day Trading (15min-1H): 25-35

- Swing Trading (4H-1D): 35-50

- Asset-specific: Crypto 15-25, Stocks 30-40, Forex 35-45

L-Function Critical Strip (0.5-2.5, default 1.5):

Controls Riemann zeta convergence precision:

- Higher values: More stable, smoother signals

- Lower values: More reactive, catches quick moves

- High frequency: 0.8-1.2, Medium: 1.3-1.7, Low: 1.8-2.3

Frobenius Trace Period (5-50, default 21):

Galois representation lookback for price-volume correlation:

- Measures harmonic relationships in market flows

- Scalping: 8-15, Day Trading: 18-25, Swing: 25-40

HTF Multi-Scale Analysis:

Higher timeframe context prevents trading against major trends:

- Provides market bias and filters signals

- Improves win rates by 15-25% through trend alignment

Operadic Composition Parameters

Strategy Composition Arity (2-5, default 4):

Number of algorithms composed for final signal:

- Conservative: 4-5 strategies (higher confidence)

- Moderate: 3-4 strategies (balanced approach)

- Aggressive: 2-3 strategies (more frequent signals)

Category Agreement Threshold (2-5, default 3):

Democratic voting minimum for signal generation:

- Higher agreement: Fewer but higher quality signals

- Lower agreement: More signals, potential false positives

Swiss-Cheese Mixing (0.1-0.5, default 0.382):

Golden ratio φ⁻¹ based blending of trend factors:

- 0.382 is φ⁻¹, optimal for natural market fractals

- Higher values: Stronger trend following

- Lower values: More contrarian signals

OFPI Configuration:

- OFPI Length (5-30, default 14): Order Flow calculation period

- T3 Smoothing (3-10, default 5): Advanced exponential smoothing

- T3 Volume Factor (0.5-1.0, default 0.7): Smoothing aggressiveness control

Unified Scoring System

Component Weights (sum ≈ 1.0):

- L-Function Weight (0.1-0.5, default 0.3): Mathematical harmony emphasis

- Galois Rank Weight (0.1-0.5, default 0.2): Market structure complexity

- Operadic Weight (0.1-0.5, default 0.3): Multi-strategy consensus

- Correspondence Weight (0.1-0.5, default 0.2): Theory-practice alignment

Signal Threshold (0.5-10.0, default 5.0):

Quality filter producing:

- 8.0+: EXCEPTIONAL signals only

- 6.0-7.9: STRONG signals

- 4.0-5.9: MODERATE signals

- 2.0-3.9: WEAK signals

🎨 ADVANCED VISUAL SYSTEM

Multi-Dimensional Quantum Aura Bands

Five-layer resonance field showing market energy:

- Colors: Theme-matched gradients (Quantum purple, Holographic cyan, etc.)

- Expansion: Dynamic based on score intensity and volatility

- Function: Multi-timeframe support/resistance zones

Morphism Flow Portals

Category theory visualization showing market topology:

- Green/Cyan Portals: Bullish mathematical flow

- Red/Orange Portals: Bearish mathematical flow

- Size/Intensity: Proportional to signal strength

- Recursion Depth (1-8): Nested patterns for flow evolution

Fractal Grid System

Dynamic support/resistance with projected L-Scores:

- Multiple Timeframes: 10, 20, 30, 40, 50-period highs/lows

- Smart Spacing: Prevents level overlap using ATR-based minimum distance

- Projections: Estimated signal scores when price reaches levels

- Usage: Precise entry/exit timing with mathematical confirmation

Wick Pressure Analysis

Rejection level prediction using candle mathematics:

- Upper Wicks: Selling pressure zones (purple/red lines)

- Lower Wicks: Buying pressure zones (purple/green lines)

- Glow Intensity (1-8): Visual emphasis and line reach

- Application: Confluence with fractal grid creates high-probability zones

Regime Intensity Heatmap

Background coloring showing market energy:

- Black/Dark: Low activity, range-bound markets

- Purple Glow: Building momentum and trend development

- Bright Purple: High activity, strong directional moves

- Calculation: Combines trend, momentum, volatility, and score intensity

Six Professional Themes

- Quantum: Purple/violet for general trading and mathematical focus

- Holographic: Cyan/magenta optimized for cryptocurrency markets

- Crystalline: Blue/turquoise for conservative, stability-focused trading

- Plasma: Gold/magenta for high-energy volatility trading

- Cosmic Neon: Bright neon colors for maximum visibility and aggressive trading

📊 INSTITUTIONAL-GRADE DASHBOARD

Unified AI Score Section

- Total Score (-10 to +10): Primary decision metric

- >5: Strong bullish signals

- <-5: Strong bearish signals

- Quality ratings: EXCEPTIONAL > STRONG > MODERATE > WEAK

- Component Analysis: Individual L-Function, Galois, Operadic, and Correspondence contributions

Order Flow Analysis

Revolutionary OFPI integration:

- OFPI Value (-100% to +100%): Real buying vs selling pressure

- Visual Gauge: Horizontal bar chart showing flow intensity

- Momentum Status: SHIFTING, ACCELERATING, STRONG, MODERATE, or WEAK

- Trading Application: Flow shifts often precede major moves

Signal Performance Tracking

- Win Rate Monitoring: Real-time success percentage with emoji indicators

- Signal Count: Total signals generated for frequency analysis

- Current Position: LONG, SHORT, or NONE with P&L tracking

- Volatility Regime: HIGH, MEDIUM, or LOW classification

Market Structure Analysis

- Möbius Field Strength: Mathematical field oscillation intensity

- CHAOTIC: High complexity, use wider stops

- STRONG: Active field, normal position sizing

- MODERATE: Balanced conditions

- WEAK: Low activity, consider smaller positions

- HTF Trend: Higher timeframe bias (BULL/BEAR/NEUTRAL)

- Strategy Agreement: Multi-algorithm consensus level

Position Management

When in trades, displays:

- Entry Price: Original signal price

- Current P&L: Real-time percentage with risk level assessment

- Duration: Bars in trade for timing analysis

- Risk Level: HIGH/MEDIUM/LOW based on current exposure

🚀 SIGNAL GENERATION LOGIC

Balanced Long/Short Architecture

The indicator generates signals through multiple convergent pathways:

Long Entry Conditions:

- Score threshold breach with algorithmic agreement

- Strong bullish order flow (OFPI > 0.15) with positive composite signal

- Bullish pattern recognition with mathematical confirmation

- HTF trend alignment with momentum shifting

- Extreme bullish OFPI (>0.3) with any positive score

Short Entry Conditions:

- Score threshold breach with bearish agreement

- Strong bearish order flow (OFPI < -0.15) with negative composite signal

- Bearish pattern recognition with mathematical confirmation

- HTF trend alignment with momentum shifting

- Extreme bearish OFPI (<-0.3) with any negative score

Exit Logic:

- Score deterioration below continuation threshold

- Signal quality degradation

- Opposing order flow acceleration

- 10-bar minimum between signals prevents overtrading

⚙️ OPTIMIZATION GUIDELINES

Asset-Specific Settings

Cryptocurrency Trading:

- Modular Level: 15-25 (capture volatility)

- L-Function Precision: 0.8-1.3 (reactive to price swings)

- OFPI Length: 10-20 (fast correlation shifts)

- Cascade Levels: 5-7, Theme: Holographic

Stock Index Trading:

- Modular Level: 25-35 (balanced trending)

- L-Function Precision: 1.5-1.8 (stable patterns)

- OFPI Length: 14-20 (standard correlation)

- Cascade Levels: 4-5, Theme: Quantum

Forex Trading:

- Modular Level: 35-45 (smooth trends)

- L-Function Precision: 1.6-2.1 (high smoothing)

- OFPI Length: 18-25 (disable volume amplification)

- Cascade Levels: 3-4, Theme: Crystalline

Timeframe Optimization

Scalping (1-5 minute charts):

- Reduce all lookback parameters by 30-40%

- Increase L-Function precision for noise reduction

- Enable all visual elements for maximum information

- Use Small dashboard to save screen space

Day Trading (15 minute - 1 hour):

- Use default parameters as starting point

- Adjust based on market volatility

- Normal dashboard provides optimal information density

- Focus on OFPI momentum shifts for entries

Swing Trading (4 hour - Daily):

- Increase lookback parameters by 30-50%

- Higher L-Function precision for stability

- Large dashboard for comprehensive analysis

- Emphasize HTF trend alignment

🏆 ADVANCED TRADING STRATEGIES

The Mathematical Confluence Method

1. Wait for Fractal Grid level approach

2. Confirm with projected L-Score > threshold

3. Verify OFPI alignment with direction

4. Enter on portal signal with quality ≥ STRONG

5. Exit on score deterioration or opposing flow

The Regime Trading System

1. Monitor Aether Flow background intensity

2. Trade aggressively during bright purple periods

3. Reduce position size during dark periods

4. Use Möbius Field strength for stop placement

5. Align with HTF trend for maximum probability

The OFPI Momentum Strategy

1. Watch for momentum shifting detection

2. Confirm with accelerating flow in direction

3. Enter on immediate portal signal

4. Scale out at Fibonacci levels

5. Exit on flow deceleration or reversal

⚠️ RISK MANAGEMENT INTEGRATION

Mathematical Position Sizing

- Use Galois Rank for volatility-adjusted sizing

- Möbius Field strength determines stop width

- Fractal Dimension guides maximum exposure

- OFPI momentum affects entry timing

Signal Quality Filtering

- Trade only STRONG or EXCEPTIONAL quality signals

- Increase position size with higher agreement levels

- Reduce risk during CHAOTIC Möbius field periods

- Respect HTF trend alignment for directional bias

🔬 DEVELOPMENT JOURNEY

Creating the LOMV was an extraordinary mathematical undertaking that pushed the boundaries of what's possible in technical analysis. This indicator almost didn't happen. The theoretical complexity nearly proved insurmountable.

The Mathematical Challenge

Implementing the Langlands Program required deep research into:

- Number theory and the Möbius function

- Riemann zeta function convergence properties

- L-function analytical continuation

- Galois representations in finite fields

The mathematical literature spans decades of pure mathematics research, requiring translation from abstract theory to practical market application.

The Computational Complexity

Operadic composition theory demanded:

- Category theory implementation in Pine Script

- Multi-dimensional array management for strategy composition

- Real-time democratic voting algorithms

- Performance optimization for complex calculations

The Integration Breakthrough

Bringing together three disparate mathematical frameworks required:

- Novel approaches to signal weighting and combination

- Revolutionary Order Flow Polarity Index development

- Advanced T3 smoothing implementation

- Balanced signal generation preventing directional bias

Months of intensive research culminated in breakthrough moments when the mathematics finally aligned with market reality. The result is an indicator that reveals market structure invisible to conventional analysis while maintaining practical trading utility.

🎯 PRACTICAL IMPLEMENTATION

Getting Started

1. Apply indicator with default settings

2. Select appropriate theme for your markets

3. Observe dashboard metrics during different market conditions

4. Practice signal identification without trading

5. Gradually adjust parameters based on observations

Signal Confirmation Process

- Never trade on score alone - verify quality rating

- Confirm OFPI alignment with intended direction

- Check fractal grid level proximity for timing

- Ensure Möbius field strength supports position size

- Validate against HTF trend for bias confirmation

Performance Monitoring

- Track win rate in dashboard for strategy assessment

- Monitor component contributions for optimization

- Adjust threshold based on desired signal frequency

- Document performance across different market regimes

🌟 UNIQUE INNOVATIONS

1. First Integration of Langlands Program mathematics with practical trading

2. Revolutionary OFPI with T3 smoothing and momentum detection

3. Operadic Composition using category theory for signal democracy

4. Dynamic Fractal Grid with projected L-Score calculations

5. Multi-Dimensional Visualization through morphism flow portals

6. Regime-Adaptive Background showing market energy intensity

7. Balanced Signal Generation preventing directional bias

8. Professional Dashboard with institutional-grade metrics

📚 EDUCATIONAL VALUE

The LOMV serves as both a practical trading tool and an educational gateway to advanced mathematics. Traders gain exposure to:

- Pure mathematics applications in markets

- Category theory and operadic composition

- Number theory through Möbius function implementation

- Harmonic analysis via L-function calculations

- Advanced signal processing through T3 smoothing

⚖️ RESPONSIBLE USAGE

This indicator represents advanced mathematical research applied to market analysis. While the underlying mathematics are rigorously implemented, markets remain inherently unpredictable.

Key Principles:

- Use as part of comprehensive trading strategy

- Implement proper risk management at all times

- Backtest thoroughly before live implementation

- Understand that past performance does not guarantee future results

- Never risk more than you can afford to lose

The mathematics reveal deep market structure, but successful trading requires discipline, patience, and sound risk management beyond any indicator.

🔮 CONCLUSION

The Langlands-Operadic Möbius Vortex represents a quantum leap forward in technical analysis, bringing PhD-level pure mathematics to practical trading while maintaining visual elegance and usability.

From the harmonic analysis of the Langlands Program to the democratic composition of operadic theory, from the number-theoretic precision of the Möbius function to the revolutionary Order Flow Polarity Index, every component works in mathematical harmony to reveal the hidden order within market chaos.

This is more than an indicator - it's a mathematical lens that transforms how you see and understand market structure.

Trade with mathematical precision. Trade with the LOMV.

*"Mathematics is the language with which God has written the universe." - Galileo Galilei*

*In markets, as in nature, profound mathematical beauty underlies apparent chaos. The LOMV reveals this hidden order.*

— Dskyz, Trade with insight. Trade with anticipation.

Fear-Greed ThermometerFear-Greed Thermometer

This indicator measures market sentiment between fear and greed by combining three key factors: volatility, average volume, and percentage price change. Each factor is normalized and averaged to produce an index ranging from 0 to 100 that reflects the overall level of market fear or greed.

How to use:

Index above 50: Indicates greed dominance. The market tends to be more optimistic, signaling potential bullish conditions or overbought levels.

Index below 50: Indicates fear dominance. The market is more cautious or pessimistic, pointing to potential bearish conditions or oversold levels.

Neutral line (50): Acts as a reference for transitions between fear and greed phases.

Features:

Dynamic background: The chart background changes color according to sentiment — green for greed, red for fear — making it easy to visually gauge the index.

Customizable: Adjust the calculation periods for volatility, volume, and price change to fit your analysis style.

Tips:

Use alongside other technical tools to confirm entry and exit points.

Watch for divergences between the index and price to anticipate possible reversals.

Monitoring extreme levels can help identify market turning points.

This indicator is not a buy or sell recommendation but an additional tool to help understand the overall market sentiment.

Adaptive MACD Deluxe [AlgoAlpha]OVERVIEW

This script is an advanced rework of the classic MACD indicator, designed to be more adaptive, visually informative, and customizable. It enhances the original MACD formula using a dynamic feedback loop and a correlation-based weighting system that adjusts in real-time based on how deterministic recent price action is. The signal line is flexible, offering several smoothing types including Heiken Ashi, while the histogram is color-coded with gradients to help users visually identify momentum shifts. It also includes optional normalization by volatility, allowing MACD values to be interpreted as relative percentage moves, making the indicator more consistent across different assets and timeframes.

CONCEPTS

This version of MACD introduces a deterministic weight based on R-squared correlation with time, which modulates how fast or slow the MACD adapts to price changes. Higher correlation means smoother, slower MACD responses, and low correlation leads to quicker reaction. The momentum calculation blends traditional EMA math with feedback and damping components to create a smoother, less noisy series. Heiken Ashi is optionally used for signal smoothing to better visualize short-term trend bias. When normalization is enabled, the MACD is scaled by an EMA of the high-low range, converting it into a bounded, volatility-relative indicator. This makes extreme readings more meaningful across markets.

FEATURES

The script offers six distinct options for signal line smoothing: EMA, SMA, SMMA (RMA), WMA, VWMA, and a custom Heiken Ashi mode based on the MACD series. Each option provides a different response speed and smoothing behavior, allowing traders to match the indicator’s behavior to their strategy—whether it's faster reaction or reduced noise.

Normalization is another key feature. When enabled, MACD values are scaled by a volatility proxy, converting the indicator into a relative percentage. This helps standardize the MACD across different assets and timeframes, making overbought and oversold readings more consistent and easier to interpret.

Threshold zones can be customized using upper and lower boundaries, with inner zones for early warnings. These zones are highlighted on the chart with subtle background fills and directional arrows when MACD enters or exits key levels. This makes it easier to spot strong or weak reversals at a glance.

Lastly, the script includes multiple built-in alerts. Users can set alerts for MACD crossovers, histogram flips above or below zero, and MACD entries into strong or weak reversal zones. This allows for hands-free monitoring and quick decision-making without staring at the chart.

USAGE

To use this script, choose your preferred signal smoothing type, enable normalization if you want MACD values relative to volatility, and adjust the threshold zones to fit your asset or timeframe. Use the colored histogram to detect changes in momentum strength—brighter colors indicate rising strength, while faded colors imply weakening. Heiken Ashi mode smooths out noise and provides clearer signals, especially useful in choppy conditions. Use alert conditions for crossover and reversal detection, or monitor the arrow markers for entries into potential exhaustion zones. This setup works well for trend following, momentum trading, and reversal spotting across all market types.

Choppiness ZONE OverlayPurpose

This script overlays choppiness zones directly onto the price chart to help traders identify whether the market is trending or ranging. It is designed to filter out low-probability trades during high choppiness conditions.

How It Works

Calculates the Choppiness Index over a user-defined period using ATR and price range.

Divides choppiness into four zones:

30 to 40: Low choppiness, possible trend initiation, shown in yellow.

40 to 50: Moderate choppiness, transition zone, shown in orange.

50 to 60: High choppiness, weakening momentum, shown in red.

60 and above: Extreme choppiness, avoid trading, shown in purple.

Highlights each zone with customizable color fills between the high and low of the selected range.

Triggers a real-time alert when choppiness exceeds 60.

Features

Customizable choppiness zones and color settings.

Real-time alert when market becomes extremely choppy (choppiness ≥ 60).

Visual zone overlay on the price chart.

Compatible with all timeframes.

Lightweight and responsive for scalping, intraday, or swing trading.

Tip

Use this tool as a volatility or trend filter. Combine it with momentum or trend-following indicators to improve trade selection.

Golden Key: Opening Channel DashboardGolden Key: Opening Channel Dashboard

Complementary to the original Golden Key – The Frequency

Upgrade of 10 Monday's 1H Avg Range + 30-Day Daily Range

This indicator provides a structured dashboard to monitor the opening channel range and related metrics on 15m and 5m charts. Built to work alongside the Golden Key methodology, it focuses on pip precision, average volatility, and SL sizing.

What It Does

Detects first 4 candles of the session:

15m chart → first 4 Monday candles (1 hour)

5m chart → first 4 candles of each day (20 minutes)

Calculates pip range of the opening move

Stores and averages the last 10 such ranges

Calculates daily range average over 10 or 30 days

Generates SL size based on your multiplier setting

Auto-adjusts for FX, JPY, and XAUUSD pip sizes

Displays all values in a clean table in the top-right

How to Use It

Add to a 15m or 5m chart

Compare the current opening range to the average

Use the daily average to assess broader volatility

Define SL size using the opening range x multiplier

Customize display colors per table row

About This Script

This is not a visual box-style indicator. It is designed to complement the original “Golden Key – The Frequency” by focusing on metric output. It is also an upgraded version of the earlier "10 Monday’s 1H Avg Range" script, now supporting multi-timeframe logic and additional customization.

Disclaimer

This is a technical analysis tool. It does not provide trading advice. Use it in combination with your own research and strategy.

VWAP Supply & Demand Zones PRO**Overview:**