India VIX TableThis indicator gives you the India Vix value in real time on your chart. You can change the position on the chart as per your preference.

Volatility

ADX EMA's DistanceIt is well known to technical analysts that the price of the most volatile and traded assets do not tend to stay in the same place for long. A notable observation is the recurring pattern of moving averages that tend to move closer together prior to a strong move in some direction to initiate the trend, it is precisely that distance that is measured by the blue ADX EMA's Distance lines on the chart, normalized and each line being the distance between 2, 3 or all 4 moving averages, with the zero line being the point where the distance between them is zero, but it is also necessary to know the direction of the movement, and that is where the modified ADX will be useful.

This is the well known Directional Movement Indicator (DMI), where the +DI and -DI lines of the ADX will serve to determine the direction of the trend.

(FVC) Fractal Volatility Compression (DAFE) (FVC) Fractal Volatility Compression

See the Market’s Volatility DNA.

The Fractal Volatility Compression (FVC) is a next-generation tool for traders who want to see volatility compression and expansion across multiple timeframes and volatility engines—not just price, but the very structure of volatility itself.

What Makes FVC Unique?

Dual-Engine Volatility:

Plots both classic price-based (Stdev) and meta-volatility (VoVix) compression/expansion, so you can see when the market is “coiling” or “exploding” on multiple levels.

Fractal, Multi-Timeframe Analysis:

Measures volatility on short, medium, and long timeframes, then normalizes each as a Z-score. The result: a true “coiled spring” detector that works on any asset, any timeframe.

Threshold Lines You Control:

Yellow center line: Your neutral baseline.

Green compression line: When crossed, the market is “spring-loading.”

Red expansion line: When crossed, volatility is breaking out.

All lines are solid, clean, and end before the dashboard for a professional look.

Agreement Fill: When both engines agree (both above or both below the center line), a bright fill highlights the zone—red for expansion, green for compression.

Signature Dashboard & Info Line:

Dashboard (right-middle) shows all Z-scores and FVC values, color-coded for instant clarity.

Compact info label for mobile or minimalist users.

Inputs & Customization

Thresholds: Set the yellow, green, and red lines to match your asset, timeframe, and risk tolerance.

Timeframes & Lengths: Tune the short, medium, and long volatility windows for your style.

Toggle Lines: Show/hide Stdev or VoVix FVC lines independently.

Dashboard & Info Line: Toggle for your workflow and screen size.

How to Use

Compression (below green): Market is “coiling” across timeframes—watch for explosive moves.

Expansion (above red): Volatility is breaking out—expect regime shifts or trend acceleration.

Agreement Fill: When both lines agree, the signal is strongest.

Not a Buy/Sell Signal: These are regime and structure signals—combine with your own

strategy and risk management.

Why should you use FVC?

See what others can’t:

Most tools show only one dimension of volatility. FVC reveals the fractal DNA of market compression and expansion. Works on any asset, any timeframe. Professional, clean, and fully customizable.

Fractal Volatility Compression (FVC):

Because the next big move is born in the market’s hidden compression.

For educational purposes only. Not financial advice. Always use proper risk management

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

ADR, ATR & VOL OverlayThis is a combined version of 2 of my other indicators:

ADR / ATR Overlay

VOL / AVG Overlay

This indicator will display the following as an overlay on your chart:

ADR

% of ADR

ADR % of Price

ATR

% of ATR

ATR % of Price

Custom Session Volume

Average For Selected Session

Volume Percentage Comparison

Description:

ADR : Average Day Range

% of ADR : Percentage that the current price move has covered its average.

ADR % of Price : The percentage move implied by the average range.

ATR : Average True Range

% of ATR : Percentage that the current price move has covered its average.

ATR % of Price : The percentage move implied by the average true range.

Custom Session Volume : User chosen time frame to monitor volume

Average For Selected Session : Average for the custom session volume

Volume Percentage Comparison : Current session compared to the average (calculated at session close)

Options:

ADR/ATR:

Time Frame

Length

Smoothing

Volume:

Set Custom Time Frame For Calculations

Set Custom Time Frame For Average Comparison

Set Custom Time Zone

Table:

Enable / Disable Each Value

Change Text Color

Change Background Color

Change Table location

Add/Remove extra row for placement

ADR / ATR Example:

The ADR and ATR can be used to provide information about average price moves to help set targets, stop losses, entries and exits based on the potential average moves.

Example: If the "% of ADR" is reading 100%, then 100% of the asset's average price range has been covered, suggesting that an additional move beyond the range has a lower probability.

Example: "ADR % of Price" provides potential price movement in percentage which can be used to asses R/R for asset.

Example: ADR (D) reading is 100% at market close but ATR (D) is at 70% at close. This suggests that there is a potential (coverage) move of 30% in Pre/Post market as suggested by averages.

Custom Volume Session Example:

Set indicator to 30 period average. Set custom time frame to 9:30am to 10:30am Eastern/New York.

When the time frame for the calculation is closed, the indicator will provide a comparison of the current days volume compared to the average of 30 previous days for that same time frame and display it as a percentage in the table.

In this example you could compare how the first hour of the trading day compares to the previous 30 day's average, aiding in evaluating the potential volume for the remainder of the day.

Notes:

Times must be entered in 24 hour format. (1pm = 13:00 etc.)

Volume indicator is for Intra-day time frames, not > Day.

How I use these values:

I use these calculations to determine if a ticker symbol has the necessary range to achieve target gains, to determine if the price oscillation is within "normal" ranges to determine if the trading day will be choppy, and to determine placement of stops and targets within average ranges in combination with support, resistance and retracement levels.

(MVD) Meta-Volatility Divergence (DAFE) Meta-Volatility Divergence (MVD)

Reveal the Hidden Tension in Volatility.

The Meta-Volatility Divergence (MVD) indicator is a next-generation tool designed to expose the disagreement between multiple volatility measures—helping you spot when the market’s “volatility engines” are out of sync, and a regime shift or volatility event may be brewing.

What Makes MVD Unique?

Multi-Source Volatility Analysis:

Unlike traditional volatility indicators that rely on a single measure, MVD fuses four distinct volatility signals:

ATR (Average True Range): Captures the average range of price movement.

Stdev (Standard Deviation): Measures the dispersion of closing prices.

Range: The average difference between high and low.

VoVix: A proprietary “volatility of volatility” metric, quantifying the difference between fast and slow ATR, normalized by ATR’s own volatility.

Divergence Engine:

The core MVD line (yellow) represents the mean absolute deviation (MAD) of these volatility measures from their average. When the line is flat, all volatility measures are in agreement. When the line rises, it means the market’s volatility signals are diverging—often a precursor to regime shifts, volatility expansions, or hidden stress.

Dynamic Z-Score Normalization:

The MVD line is normalized as a Z-score, so you can easily spot when current divergence is rare or extreme compared to recent history.

Visual Clarity:

Yellow center line: Tracks the real-time divergence of volatility measures.

Green dashed thresholds: Mark the ±2.00 Z-score levels, highlighting when divergence is unusually high and action may be warranted.

Dashboard: Toggleable panel shows all key metrics (ATR, Stdev, VoVix, MVD Z) and your custom branding.

Compact Info Label : For mobile or minimalist users, a single-line summary keeps you informed without clutter.

What Makes The MVD line move?

- The MVD line rises when the included volatility measures (ATR, Stdev, Range, VoVix) are moving in different directions or at different magnitudes. For example, if ATR is rising but Stdev is falling, the line will move up, signaling disagreement.

- The line falls or flattens when all volatility measures are in sync, indicating a consensus in the market’s volatility regime.

- VoVix adds a unique dimension, making the indicator especially sensitive to sudden changes in volatility structure that most tools miss.

Inputs & Settings

ATR Length: Sets the lookback for ATR calculation. Shorter = more sensitive, longer = smoother.

Stdev Length: Sets the lookback for standard deviation. Adjust for your asset’s volatility.

Range Length: Sets the lookback for the average high-low range.

MVD Lookback: Controls the window for Z-score normalization. Higher values = more historical context, lower = more responsive.

Show Dashboard: Toggle the full dashboard panel on/off.

Show Compact Info Label: Toggle the mobile-friendly info line on/off.

Tip:

Adjust these settings to match your asset’s volatility and your trading timeframe. There is no “one size fits all”—tuning is key to extracting the most value from MVD.

How to make MVD work for you:

Threshold Crosses: When the MVD line crosses above or below the green dashed thresholds (±2.00), it signals that volatility measures are diverging more than usual. This is a heads-up that a volatility event, regime shift, or hidden market stress may be developing.

Not a Buy/Sell Signal: A threshold cross is not a direct buy or sell signal. It is an indication that the market’s volatility structure is changing. Use it as a filter, confirmation, or alert in combination with your own strategy and risk management.

Dashboard & Info Line: Use the dashboard for a full view of all metrics, or the info label for a quick glance—especially useful on mobile.

Chart: MNQ! on 5min frames

ATR: 14

StDev L: 11

Range L: 13

MDV LB: 13

Important Note

MVD is a market structure and volatility regime tool.

It is designed to alert you to potential changes in market conditions, not to provide direct trade entries or exits. Always combine with your own analysis and risk management.

Meta-Volatility Divergence:

See the market’s hidden tension. Anticipate the next wave.

For educational purposes only. Not financial advice. Always use proper risk management.

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

Horizontal ATR LinesDisclaimer:

This script was generated using OpenAI’s ChatGPT. I take no responsibility for the correctness, performance, or financial impact of this indicator. Use it at your own risk and discretion.

This indicator draws horizontal ATR-based levels from the last closed candle on a user-selected timeframe. It is designed for traders who want to visualize realistic volatility zones for setting dynamic support/resistance, take-profit, or stop-loss levels.

What it does:

Calculates the Average True Range (ATR) using a customizable period and timeframe.

Plots four horizontal lines:

+1 ATR and –1 ATR from the last closed candle’s close

+X ATR and –X ATR, where X is a second custom multiplier

Each level includes a compact label showing:

The price of the level

The percentage distance from the close price

Use cases:

Identify realistic intraday or swing price movement boundaries

Build volatility-aware take-profit and stop-loss zones

Visually track market compression or expansion in context

Customization:

ATR period and timeframe

Two independent ATR multipliers

Custom color settings for each group of levels

Trend Volatility Index (TVI)Trend Volatility Index (TVI)

A robust nonparametric oscillator for structural trend volatility detection

⸻

What is this?

TVI is a volatility oscillator designed to measure the strength and emergence of price trends using nonparametric statistics.

It calculates a U-statistic based on the Gini mean difference across multiple simple moving averages.

This allows for objective, robust, and unbiased quantification of trend volatility in tick-scale values.

⸻

What can it do?

• Quantify trend strength as a continuous value aligned with tick price scale

• Detect trend breakouts and volatility expansions

• Identify range-bound market states

• Detect early signs of new trends with minimal lag

⸻

What can’t it do?

• Predict future price levels

• Predict trend direction before confirmation

⸻

How it works

TVI computes a nonparametric dispersion metric (Gini mean difference) from multiple SMAs of different lengths.

As this metric shares the same dimension as price ticks, it can be directly interpreted on the chart as a volatility gauge.

The output is plotted using candlestick-style charts to enhance visibility of change rate and trend behavior.

⸻

Disclaimer

TVI does not predict price. It is a structural indicator designed to support discretionary judgment.

Trading carries inherent risk, and this tool does not guarantee profitability. Use at your own discretion.

⸻

Innovation

This indicator introduces a novel approach to trend volatility by applying U-statistics over time series

to produce a nonparametric, unbiased, and robust estimate of structural volatility.

日本語要約

Trend Volatility Index (TVI) は、ノンパラメトリックなU統計量(Gini平均差)を使ってトレンドの強度を客観的に測定することを目的に開発されたボラティリティ・オシレーターです。

ティック単位で連続的に変化し、トレンドのブレイク・レンジ・初動の予兆を定量的に検出します。

未来の価格や方向は予測せず、現在の構造的ばらつきだけをロバストに評価します。

Retail Pain Index (RPIx) (RPIx) Retail Pain Index (DAFE)

See the Market’s Pain. Trade the Edge.

The Retail Pain Index (RPIx) is a next-generation volatility and sentiment tool designed to reveal the hidden moments when retail traders are most likely being squeezed, stopped out, or forced to capitulate. This is not just another oscillator—it’s a behavioral market scanner that quantifies “pain” as price rips away from the average entry zone, often marking the fuel for the next big move.

Why is RPIx so Unique?

Behavioral Volatility Engine:

RPIx doesn’t just track price or volume. It measures how far price is moving away from where the crowd has recently entered (using a rolling VWAP average), then normalizes this “distance” into a Z-score. The result? You see when the market is inflicting maximum pain on the most participants.

Dynamic, Intuitive Coloring:

The main RPIx line is purple in normal conditions, but instantly turns red when pain is extreme to the upside (+2.00 or higher) and green when pain is extreme to the downside (-2.00 or lower). This makes it visually obvious when the market is entering a “max pain” regime.

Threshold Lines for Clarity:

Dashed red and green lines at +2.00 and -2.00 Z-score levels make it easy to spot rare, high-pain events at a glance.

Signature Dashboard & Info Line:

Dashboard: A compact, toggleable panel in the top right of the indicator pane shows the current Z-score, threshold, and status—perfect for desktop users who want a quick read on market stress.

Info Line: For mobile or minimalist traders, a single-line info label gives you the essentials without cluttering your screen.

Inputs & Customization

Entry Cluster Lookback: Adjusts how many bars are used to calculate the “entry zone” (VWAP average). A higher value smooths the signal, a lower value makes it more responsive.

Pain Z-Score Threshold:

Sets the sensitivity for what counts as “extreme pain.” Default is ±2.00, but you can fine-tune this to match your asset’s volatility or your own risk appetite.

Show Dashboard / Show Compact Info Label:

Toggle these features on or off to fit your workflow and screen size.

How to utilize RPIx's awesomeness:

Extreme Readings = Opportunity:

When RPIx spikes above +2.00 (red) or below -2.00 (green), the market is likely running stops, liquidating weak hands, or forcing retail traders to capitulate. These moments often precede sharp reversals, trend accelerations, or volatility expansions.

Combine with Price Action:

Use RPIx as a confirmation tool for your existing strategy, or as a standalone alert for “pain points” where the crowd is most vulnerable.

Visual Edge:

The color-coded line and threshold levels make it easy to spot regime shifts and rare events—no more squinting at numbers or guessing when the market is about to snap.

Why RPIx?

Works on Any Asset, Any Timeframe:

Stocks, futures, crypto, forex—if there’s a crowd, there’s pain, and RPIx will find it.

Behavioral Alpha:

Most indicators lag. RPIx quantifies the psychological stress in the market, giving you a real-time edge over the herd.

Customizable, Clean, and Powerful:

Designed for both power users and mobile traders, with toggles for every workflow.

See the pain. Trade the edge.

Retail Pain Index: Because the market’s next move is written in the crowd’s discomfort.

For educational purposes only. Not financial advice. Always use proper risk management

Use with discipline. Trade your edge.

— Dskyz , for DAFE Trading Systems, for DAFE Trading Systems

Stop Cascade Detector Stop Cascade Detector (DAFE)

Unlock the Hidden Triggers of Market Momentum!

The Stop Cascade Detector (Bull & Bear, Info Bubble) is a next-generation tool designed for traders who want to see what the crowd can’t: the precise moments when clusters of stop orders are being triggered, unleashing explosive moves in either direction. The reason for this is traders taking there position too early. We on the other hand will take our positions once the less informed traders have been liquidated.

What Makes This Indicator Unique?

Not Just Another Volatility Tool:

This script doesn’t just measure volatility or volume. It detects the chain reactions that occur when price and volume spikes combine to trigger stop-loss clusters—events that often precede the most powerful surges and reversals in any market.

Directional Intelligence:

Unlike generic “spike” detectors, this tool distinguishes between bullish stop cascades (green, above the bar) and bearish stop cascades (red, below the bar), giving you instant clarity on which side of the market is being liquidated.

Visual Precision:

Each event is marked with a color-coded info bubble and a triangle, clearly separated from the price bars for maximum readability. No more guessing where the action is—see it, trade it, and stay ahead.

Universal Application:

Works on any asset, any timeframe, and in any market—futures, stocks, crypto, forex. If there are stops, this indicator will find the cascade.

What makes it work?

Momentum + Volume Spike:

The detector identifies bars where both price momentum and volume are simultaneously extreme (using Z-scores). This combination is a classic signature of stop runs and forced liquidations.

Bull & Bear Detection:

Bull Stop Cascade : Price plunges downward with a volume spike—likely longs getting stopped out.

Bear Stop Cascade: Price surges upward with a volume spike—likely shorts getting stopped out.

Info Bubbles:

Each event is labeled with the exact Z-scores for momentum and volume, so you can gauge the intensity of the cascade at a glance.

What will it do for you?

Front-Run the Crowd:

Most traders react after the move. This tool helps you spot the cause of the move—giving you a tactical edge to fade exhaustion, ride momentum, or avoid getting trapped.

Perfect for Scalpers, Day Traders, and Swing Traders:

Whether you’re looking for high-probability reversals or want to ride the wave, knowing when stops are being triggered is a game-changer.

No More Blind Spots:

Stop cascades are the hidden fuel behind many of the market’s biggest moves. Now you can see them in real time.

How to Use

Red Bubble Above Bar: Bear stop cascade detected—watch for possible trend acceleration or reversal.

Green Bubble Below Bar: Bull stop cascade detected—watch for possible trend acceleration or reversal.

Combine with Your Strategy : Use as a confirmation tool, a reversal signal, or a filter for high-volatility environments. Level up your trading. See the market’s hidden triggers.

Stop Cascade Detector: Because the real edge is knowing what sets the market on fire.

For educational purposes only. Not financial advice. Always use proper risk management.

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

Gap Reversal Signal with Indicators🔍 Gap Reversal Signal with Indicators — 結合 KD、MACD、SAR 與背離分析的多功能指標

🔍 Gap Reversal Signal with Indicators — A Multi-Tool Signal Indicator Combining KD, MACD, SAR, and Divergence Analysis

中文說明:

本指標結合多種常用技術分析工具,包括 KD 隨機指標、MACD 動能交叉、SAR 趨勢方向、以及 MACD 背離偵測,用以辨識潛在的價格反轉區域。適用於日內交易與波段操作,支援各類市場,如加密貨幣、股票與外匯等。

English Description:

This indicator combines several popular technical tools: Stochastic KD, MACD momentum crossovers, SAR trend direction, and MACD divergence detection. It helps traders identify potential reversal areas and is ideal for both intraday and swing trading. Works well on crypto, stocks, and forex markets.

🧠 功能特點 | Key Features

✅ KD指標(慢速隨機指標)檢測超買超賣並提供%K與%D交叉訊號

✅ Stochastic KD (slow) to detect overbought/oversold zones and crossover signals

✅ MACD金叉/死叉與零軸突破捕捉趨勢轉變與動能反轉

✅ MACD Crossovers + Zero-Line Breaks to capture trend changes and momentum reversals

✅ SAR指標即時顯示多空方向

✅ Parabolic SAR for real-time trend direction indication

✅ MACD背離偵測協助辨識潛在反轉區域

✅ MACD Divergence Detection for identifying hidden trend reversals

✅ 圖形提示與標籤提示可視化呈現各類訊號

✅ Visual Alerts and Labels for easy and quick signal recognition

📈 支援市場 | Supported Markets

📊 台股 / 美股 / 外匯 / 加密貨幣

📊 Taiwan Stocks / US Stocks / Forex / Cryptocurrencies (e.g. BTC, ETH)

🔧 推薦用法 | Recommended Use

搭配缺口策略與支撐壓力位使用

Use with gap-trading strategies and support/resistance zones

用於盤整末期或趨勢反轉的提示

Helpful for end-of-consolidation signals or trend reversals

支援短線與波段交易風格

Suitable for scalping and swing trading styles

💡 把這個指標加入你的圖表,立即體驗多重技術分析所帶來的交易優勢!

💡 Add this indicator to your chart now and experience the power of multi-tool technical analysis!

Macd, Wt Cross & HVPMacd Wt Cross & HVP – Advanced Multi-Signal Indicator

This script is a custom-designed multi-signal indicator that brings together three proven concepts to provide a complete view of market momentum, reversals, and volatility build-ups. It is built for traders who want to anticipate key market moves, not just react to them.

Why This Combination ?

While each tool has its strengths, their combined use creates powerful signal confluence.

Instead of juggling multiple indicators separately, this script synchronizes three key perspectives into a single, intuitive display—helping you trade with greater clarity and confidence.

1. MACD Histogram – Momentum and Trend Clarity

At the core of the indicator is the MACD histogram, calculated as the difference between two exponential moving averages (EMAs).

Color-coded bars represent momentum direction and intensity:

Green / blue bars: bullish momentum

Red / pink bars: bearish momentum

Color intensity shows acceleration or weakening of trend.

This visual makes it easy to detect trend shifts and momentum divergence at a glance.

2. WT Cross Signals – Early Reversal Detection

Overlaid on the histogram are green and red dots, based on the logic of the WaveTrend oscillator cross:

Green dots = potential bullish cross (buy signal)

Red dots = potential bearish cross (sell signal)

These signals are helpful for identifying reversal points during both trending and ranging phases.

3. Historical Volatility Percentile (HVP) – Volatility Compression Zones

Behind the histogram, purple vertical zones highlight periods of low historical volatility, based on the HVP:

When volatility compresses below a specific threshold, these zones appear.

Such periods are often followed by explosive price moves, making them prime areas for pre-breakout positioning.

By integrating HVP, the script doesn’t just tell you where the trend is—it tells you when the trend is likely to erupt.

How to Use This Script

Use the MACD histogram to confirm the dominant trend and its strength.

Watch for WT Cross dots as potential entry/exit signals in alignment or divergence with the MACD.

Monitor HVP purple zones as warnings of incoming volatility expansions—ideal moments to prepare for breakout trades.

Best results occur when all three elements align, offering a high-probability trade setup.

What Makes This Script Original?

Unlike many mashups, this script was not created by simply merging indicators. Each component was carefully integrated to serve a specific, complementary purpose:

MACD detects directional bias

WT Cross adds precision timing

HVP anticipates volatility-based breakout timing

This results in a strategic tool for traders, useful on multiple timeframes and adaptable to different trading styles (trend-following, breakout, swing).

Anchored Probability Cone by TenozenFirst of all, credit to @nasu_is_gaji for the open source code of Log-Normal Price Forecast! He teaches me alot on how to use polylines and inverse normal distribution from his indicator, so check it out!

What is this indicator all about?

This indicator draws a probability cone that visualizes possible future price ranges with varying levels of statistical confidence using Inverse Normal Distribution , anchored to the start of a selected timeframe (4h, W, M, etc.)

Feutures:

Anchored Cone: Forecasts begin at the first bar of each chosen higher timeframe, offering a consistent point for analysis.

Drift & Volatility-Based Forecast: Uses log returns to estimate market volatility (smoothed using VWMA) and incorporates a trend angle that users can set manually.

Probabilistic Price Bands: Displays price ranges with 5 customizable confidence levels (e.g., 30%, 68%, 87%, 99%, 99,9%).

Dynamic Updating: Recalculates and redraws the cone at the start of each new anchor period.

How to use:

Choose the Anchored Timeframe (PineScript only be able to forecast 500 bars in the future, so if it doesn't plot, try adjusting to a lower anchored period).

You can set the Model Length, 100 sample is the default. The higher the sample size, the higher the bias towards the overall volatility. So better set the sample size in a balanced manner.

If the market is inside the 30% conifidence zone (gray color), most likely the market is sideways. If it's outside the 30% confidence zone, that means it would tend to trend and reach the other probability levels.

Always follow the trend, don't ever try to trade mean reversions if you don't know what you're doing, as mean reversion trades are riskier.

That's all guys! I hope this indicator helps! If there's any suggestions, I'm open for it! Thanks and goodluck on your trading journey!

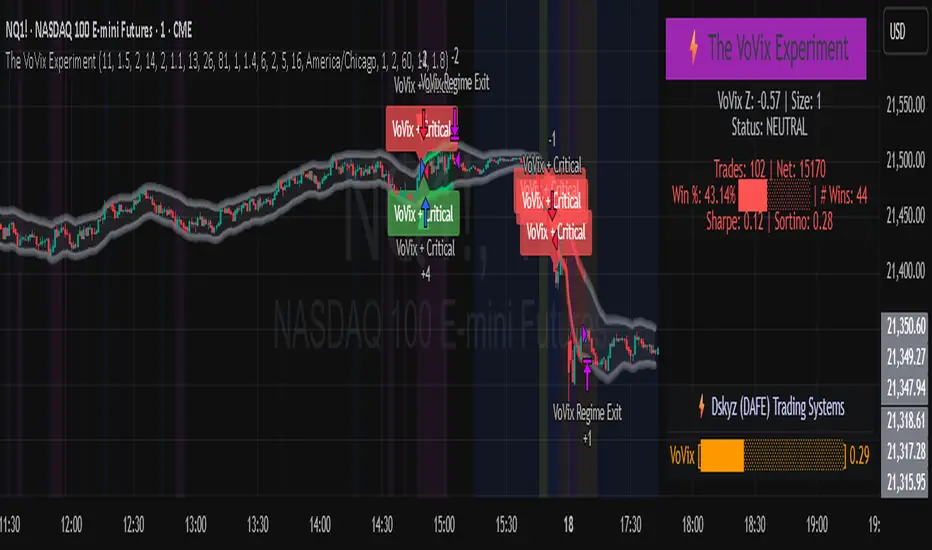

The VoVix Experiment The VoVix Experiment

The VoVix Experiment is a next-generation, regime-aware, volatility-adaptive trading strategy for futures, indices, and more. It combines a proprietary VoVix (volatility-of-volatility) anomaly detector with price structure clustering and critical point logic, only trading when multiple independent signals align. The system is designed for robustness, transparency, and real-world execution.

Logic:

VoVix Regime Engine: Detects pre-move volatility anomalies using a fast/slow ATR ratio, normalized by Z-score. Only trades when a true regime spike is detected, not just random volatility.

Cluster & Critical Point Filters: Price structure and volatility clustering must confirm the VoVix signal, reducing false positives and whipsaws.

Adaptive Sizing: Position size scales up for “super-spikes” and down for normal events, always within user-defined min/max.

Session Control: Trades only during user-defined hours and days, avoiding illiquid or high-risk periods.

Visuals: Aurora Flux Bands (From another Original of Mine (Options Flux Flow): glow and change color on signals, with a live dashboard, regime heatmap, and VoVix progression bar for instant insight.

Backtest Settings

Initial capital: $10,000

Commission: Conservative, realistic roundtrip cost:

15–20 per contract (including slippage per side) I set this to $25

Slippage: 3 ticks per trade

Symbol: CME_MINI:NQ1!

Timeframe: 15 min (but works on all timeframes)

Order size: Adaptive, 1–2 contracts

Session: 5:00–15:00 America/Chicago (default, fully adjustable)

Why these settings?

These settings are intentionally strict and realistic, reflecting the true costs and risks of live trading. The 10,000 account size is accessible for most retail traders. 25/contract including 3 ticks of slippage are on the high side for MNQ, ensuring the strategy is not curve-fit to perfect fills. If it works here, it will work in real conditions.

Forward Testing: (This is no guarantee. I've provided these results to show that executions perform as intended. Test were done on Tradovate)

ALL TRADES

Gross P/L: $12,907.50

# of Trades: 64

# of Contracts: 186

Avg. Trade Time: 1h 55min 52sec

Longest Trade Time: 55h 46min 53sec

% Profitable Trades: 59.38%

Expectancy: $201.68

Trade Fees & Comm.: $(330.95)

Total P/L: $12,576.55

Winning Trades: 59.38%

Breakeven Trades: 3.12%

Losing Trades: 37.50%

Link: www.dropbox.com

Inputs & Tooltips

VoVix Regime Execution: Enable/disable the core VoVix anomaly detector.

Volatility Clustering: Require price/volatility clusters to confirm VoVix signals.

Critical Point Detector: Require price to be at a statistically significant distance from the mean (regime break).

VoVix Fast ATR Length: Short ATR for fast volatility detection (lower = more sensitive).

VoVix Slow ATR Length: Long ATR for baseline regime (higher = more stable).

VoVix Z-Score Window: Lookback for Z-score normalization (higher = smoother, lower = more reactive).

VoVix Entry Z-Score: Minimum Z-score for a VoVix spike to trigger a trade.

VoVix Exit Z-Score: Z-score below which the regime is considered decayed (exit).

VoVix Local Max Window: Bars to check for local maximum in VoVix (higher = stricter).

VoVix Super-Spike Z-Score: Z-score for “super” regime events (scales up position size).

Min/Max Contracts: Adaptive position sizing range.

Session Start/End Hour: Only trade between these hours (exchange time).

Allow Weekend Trading: Enable/disable trading on weekends.

Session Timezone: Timezone for session filter (e.g., America/Chicago for CME).

Show Trade Labels: Show/hide entry/exit labels on chart.

Flux Glow Opacity: Opacity of Aurora Flux Bands (0–100).

Flux Band EMA Length: EMA period for band center.

Flux Band ATR Multiplier: Width of bands (higher = wider).

Compliance & Transparency

* No hidden logic, no repainting, no pyramiding.

* All signals, sizing, and exits are fully explained and visible.

* Backtest settings are stricter than most real accounts.

* All visuals are directly tied to the strategy logic.

* This is not a mashup or cosmetic overlay; every component is original and justified.

Disclaimer

Trading is risky. This script is for educational and research purposes only. Do not trade with money you cannot afford to lose. Past performance is not indicative of future results. Always test in simulation before live trading.

Proprietary Logic & Originality Statement

This script, “The VoVix Experiment,” is the result of original research and development. All core logic, algorithms, and visualizations—including the VoVix regime detection engine, adaptive execution, volatility/divergence bands, and dashboard—are proprietary and unique to this project.

1. VoVix Regime Logic

The concept of “volatility of volatility” (VoVix) is an original quant idea, not a standard indicator. The implementation here (fast/slow ATR ratio, Z-score normalization, local max logic, super-spike scaling) is custom and not found in public TradingView scripts.

2. Cluster & Critical Point Logic

Volatility clustering and “critical point” detection (using price distance from a rolling mean and standard deviation) are general quant concepts, but the way they are combined and filtered here is unique to this script. The specific logic for “clustered chop” and “critical point” is not a copy of any public indicator.

3. Adaptive Sizing

The adaptive sizing logic (scaling contracts based on regime strength) is custom and not a standard TradingView feature or public script.

4. Time Block/Session Control

The session filter is a common feature in many strategies, but the implementation here (with timezone and weekend control) is written from scratch.

5. Aurora Flux Bands (From another Original of Mine (Options Flux Flow)

The “glowing” bands are inspired by the idea of volatility bands (like Bollinger Bands or Keltner Channels), but the visual effect, color logic, and integration with regime signals are original to this script.

6. Dashboard, Watermark, and Metrics

The dashboard, real-time Sharpe/Sortino, and VoVix progression bar are all custom code, not copied from any public script.

What is “standard” or “common quant practice”?

Using ATR, EMA, and Z-score are standard quant tools, but the way they are combined, filtered, and visualized here is unique. The structure and logic of this script are original and not a mashup of public code.

This script is 100% original work. All logic, visuals, and execution are custom-coded for this project. No code or logic is directly copied from any public or private script.

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

Dskyz (DAFE) GENESIS Dskyz (DAFE) GENESIS: Adaptive Quant, Real Regime Power

Let’s be honest: Most published strategies on TradingView look nearly identical—copy-paste “open-source quant,” generic “adaptive” buzzwords, the same shallow explanations. I’ve even fallen into this trap with my own previously posted strategies. Not this time.

What Makes This Unique

GENESIS is not a black-box mashup or a pre-built template. It’s the culmination of DAFE’s own adaptive, multi-factor, regime-aware quant engine—built to outperform, survive, and visualize live edge in anything from NQ/MNQ to stocks and crypto.

True multi-factor core: Volume/price imbalances, trend shifts, volatility compression/expansion, and RSI all interlock for signal creation.

Adaptive regime logic: Trades only in healthy, actionable conditions—no “one-size-fits-all” signals.

Momentum normalization: Uses rolling, percentile-based fast/slow EMA differentials, ALWAYS normalized, ALWAYS relevant—no “is it working?” ambiguity.

Position sizing that adapts: Not fixed-lot, not naive—not a loophole for revenge trading.

No hidden DCA or pyramiding—what you see is what you trade.

Dashboard and visual system: Directly connected to internal logic. If it’s shown, it’s used—and nothing cosmetic is presented on your chart that isn’t quantifiable.

📊 Inputs and What They Mean (Read Carefully)

Maximum Raw Score: How many distinct factors can contribute to regime/trade confidence (default 4). If you extend the quant logic, increase this.

RSI Length / Min RSI for Shorts / Max RSI for Longs: Fine-tunes how “overbought/oversold” matters; increase the length for smoother swings, tighten floors/ceilings for more extreme signals.

⚡ Regime & Momentum Gates

Min Normed Momentum/Score (Conf): Raise to demand only the strongest trends—your filter to avoid algorithmic chop.

🕒 Volatility & Session

ATR Lookback, ATR Low/High Percentile: These control your system’s awareness of when the market is dead or ultra-volatile. All sizing and filter logic adapts in real time.

Trading Session (hours): Easy filter for when entries are allowed; default is regular trading hours—no surprise overnight fills.

📊 Sizing & Risk

Max Dollar Risk / Base-Max Contracts: All sizing is adaptive, based on live regime and volatility state—never static or “just 1 contract.” Control your max exposures and real $ risk. ATR will effect losses in high volatility times.

🔄 Exits & Scaling

Stop/Trail/Scale multipliers: You choose how dynamic/flexible risk controls and profit-taking need to be. ATR-based, so everything auto-adjusts to the current market mode.

Visuals That Actually Matter

Dashboard (Top Right): Shows only live, relevant stats: scoring, status, position size, win %, win streak, total wins—all from actual trade engine state (not “simulated”).

Watermark (Bottom Right): Momentum bar visual is always-on, regime-aware, reflecting live regime confidence and momentum normalization. If the bar is empty, you’re truly in no-momentum. If it glows lime, you’re riding the strongest possible edge.

*No cosmetics, no hidden code distractions.

Backtest Settings

Initial capital: $10,000

Commission: Conservative, realistic roundtrip cost:

15–20 per contract (including slippage per side) I set this to $25

Slippage: 3 ticks per trade

Symbol: CME_MINI:NQ1!

Timeframe: 1 min (but works on all timeframes)

Order size: Adaptive, 1–3 contracts

No pyramiding, no hidden DCA

Why these settings?

These settings are intentionally strict and realistic, reflecting the true costs and risks of live trading. The 10,000 account size is accessible for most retail traders. 25/contract including 3 ticks of slippage are on the high side for NQ, ensuring the strategy is not curve-fit to perfect fills. If it works here, it will work in real conditions.

Why It Wins

While others put out “AI-powered” strategies with little logic or soul, GENESIS is ruthlessly practical. It is built around what keeps traders alive:

- Context-aware signals, not just patterns

- Tight, transparent risk

- Inputs that adapt, not confuse

- Visuals that clarify, not distract

- Code that runs clean, efficient, and with minimal overfitting risk (try it on QQQ, AMD, SOL, etc. out of the box)

Disclaimer (for TradingView compliance):

Trading is risky. Futures, stocks, and crypto can result in significant losses. Do not trade with funds you cannot afford to lose. This is for educational and informational purposes only. Use in simulation/backtest mode before live trading. No past performance is indicative of future results. Always understand your risk and ownership of your trades.

This will not be my last—my goal is to keep raising the bar until DAFE is a brand or I’m forced to take this private.

Use with discipline, use with clarity, and always trade smarter.

— Dskyz , powered by DAFE Trading Systems.

REVELATIONS (VoVix - PoC) REVELATIONS (VoVix - POC): True Regime Detection Before the Move

Let’s not sugarcoat it: Most strategies on TradingView are recycled—RSI, MACD, OBV, CCI, Stochastics. They all lag. No matter how many overlays you stack, every one of these “standard” indicators fires after the move is underway. The retail crowd almost always gets in late. That’s never been enough for my team, for DAFE, or for anyone who’s traded enough to know the real edge vanishes by the time the masses react.

How is this different?

REVELATIONS (VoVix - POC) was engineered from raw principle, structured to detect pre-move regime change—before standard technicals even light up. We built, tested, and refined VoVix to answer one hard question:

What if you could see the spike before the trend?

Here’s what sets this system apart, line-by-line:

o True volatility-of-volatility mathematics: It’s not just "ATR of ATR" or noise smoothing. VoVix uses normalized, multi-timeframe v-vol spikes, instantly detecting orderbook stress and "outlier" market events—before the chart shows them as trends.

o Purist regime clustering: Every trade is enabled only during coordinated, multi-filter regime stress. No more signals in meaningless chop.

o Nonlinear entry logic: No trade is ever sent just for a “good enough” condition. Every entry fires only if every requirement is aligned—local extremes, super-spike threshold, regime index, higher timeframe, all must trigger in sync.

o Adaptive position size: Your contracts scale up with event strength. Tiny size during nominal moves, max leverage during true regime breaks—never guesswork, never static exposure.

o All exits governed by regime decay logic: Trades are closed not just on price targets but at the precise moment the market regime exhausts—the hardest part of systemic trading, now solved.

How this destroys the lag:

Standard indicators (RSI, MACD, OBV, CCI, and even most “momentum” overlays) simply tell you what already happened. VoVix triggers as price structure transitions—anyone running these generic scripts will trade behind the move while VoVix gets in as stress emerges. Real alpha comes from anticipation, not confirmation.

The visuals only show what matters:

Top right, you get a live, live quant dashboard—regime index, current position size, real-time performance (Sharpe, Sortino, win rate, and wins). Bottom right: a VoVix "engine bar" that adapts live with regime stress. Everything you see is a direct function of logic driving this edge—no cosmetics, no fake momentum.

Inputs/Signals—explained carefully for clarity:

o ATR Fast Length & ATR Slow Length:

These are the heart of VoVix’s regime sensing. Fast ATR reacts to sharp volatility; Slow ATR is stability baseline. Lower Fast = reacts to every twitch; higher Slow = requires more persistent, “real” regime shifts.

Tip: If you want more signals or faster markets, lower ATR Fast. To eliminate noise, raise ATR Slow.

o ATR StdDev Window: Smoothing for volatility-of-volatility normalization. Lower = more jumpy, higher = only the cleanest spikes trigger.

Tip: Shorten for “jumpy” assets, raise for indices/futures.

o Base Spike Threshold: Think of this as your “minimum event strength.” If the current move isn’t volatile enough (normalized), no signal.

Tip: Higher = only biggest moves matter. Lower for more signals but more potential noise.

o Super Spike Multiplier: The “are you sure?” test—entry only when the current spike is this multiple above local average.

Tip: Raise for ultra-selective/swing-trading; lower for more active style.

Regime & MultiTF:

o Regime Window (Bars):

How many bars to scan for regime cluster “events.” Short for turbo markets, long for big swings/trends only.

o Regime Event Count: Only trade when this many spikes occur within the Regime Window—filters for real stress, not isolated ticks.

Tip: Raise to only ever trade during true breakouts/crashes.

o Local Window for Extremes:

How many bars to check that a spike is a local max.

Tip: Raise to demand only true, “clearest” local regime events; lower for early triggers.

o HTF Confirm:

Higher timeframe regime confirmation (like 45m on an intraday chart). Ensures any event you act on is visible in the broader context.

Tip: Use higher timeframes for only major moves; lower for scalping or fast regimes.

Adaptive Sizing:

o Max Contracts (Adaptive): The largest size your system will ever scale to, even on extreme event.

Tip: Lower for small accounts/conservative risk; raise on big accounts or when you're willing to go big only on outlier events.

o Min Contracts (Adaptive): The “toe-in-the-water.” Smallest possible trade.

Tip: Set as low as your broker/exchange allows for safety, or higher if you want to always have meaningful skin in the game.

Trade Management:

o Stop %: Tightness of your stop-loss relative to entry. Lower for tighter/safer, higher for more breathing room at cost of greater drawdown.

o Take Profit %: How much you'll hold out for on a win. Lower = more scalps. Higher = only run with the best.

o Decay Exit Sensitivity Buffer: Regime index must dip this far below the trading threshold before you exit for “regime decay.”

Tip: 0 = exit as soon as stress fails, higher = exits only on stronger confirmation regime is over.

o Bars Decay Must Persist to Exit: How long must decay be present before system closes—set higher to avoid quick fades and whipsaws.

Backtest Settings

Initial capital: $10,000

Commission: Conservative, realistic roundtrip cost:

15–20 per contract (including slippage per side) I set this to $25

Slippage: 3 ticks per trade

Symbol: CME_MINI:NQ1!

Timeframe: 1 min (but works on all timeframes)

Order size: Adaptive, 1–3 contracts

No pyramiding, no hidden DCA

Why these settings?

These settings are intentionally strict and realistic, reflecting the true costs and risks of live trading. The 10,000 account size is accessible for most retail traders. 25/contract including 3 ticks of slippage are on the high side for NQ, ensuring the strategy is not curve-fit to perfect fills. If it works here, it will work in real conditions.

Tip: Set to 1 for instant regime exit; raise for extra confirmation (less whipsaw risk, exits held longer).

________________________________________

Bottom line: Tune the sensitivity, selectivity, and risk of REVELATIONS by these inputs. Raise thresholds and windows for only the best, most powerful signals (institutional style); lower for activity (scalpers, fast cryptos, signals in constant motion). Sizing is always adaptive—never static or martingale. Exits are always based on both price and regime health. Every input is there for your control, not to sell “complexity.” Use with discipline, and make it your own.

This strategy is not just a technical achievement: It’s a statement about trading smarter, not just more.

* I went back through the code to make sure no the strategy would not suffer from repainting, forward looking, or any frowned upon loopholes.

Disclaimer:

Trading is risky and carries the risk of substantial loss. Do not use funds you aren’t prepared to lose. This is for research and informational purposes only, not financial advice. Backtest, paper trade, and know your risk before going live. Past performance is not a guarantee of future results.

Expect more: We’ll keep pushing the standard, keep evolving the bar until “quant” actually means something in the public code space.

Use with clarity, use with discipline, and always trade your edge.

— Dskyz , for DAFE Trading Systems

Deviation over Deviation (DoD) (DAFE) Deviation over Deviation (DoD)

Let’s call it out: The vast majority of “volatility” tools on TradingView are just new wrappers on old math—ATR, bands, and basic deviation, all chasing the same tired after-the-fact moves. They’re built to describe the aftermath, not the ignition. If you’re still relying on these, you’re trading in the rearview mirror while the real edge is already gone. That’s not our game, and it shouldn’t be yours.

Deviation over Deviation (DoD) is built for one purpose:

To expose the hidden regime shifts—the moments when volatility itself becomes volatile, when the market’s “normal” deviation is no longer normal, and when the next move is about to erupt. This isn’t just another overlay. This is a quant-grade anomaly detector, engineered to show you the probability surface before the crowd even knows it’s changed.

What sets this apart:

Deviation over Deviation (DoD):

Not just “how much did price move,” but “how unusual is the current volatility compared to its own history?” This is the Z-score of Z-scores—a true rarity detector for market stress, lull, or impending breakout.

VoVix Integration:

Select VoVix as your source and you’re not just tracking price, but the volatility of volatility—the same math that powers institutional regime models. This is the edge that front-runs the move, not follows it.

Multi-Timeframe Comparative Engine:

Instantly compare current and higher timeframe DoD Z-scores. See when the micro and macro regimes align—or when they’re about to collide.

Professional, Adaptive Dashboard:

No cosmetic fluff, always showing you the real quant state: current DoD Z, HTF DoD Z, and regime warnings. Every color, every plot, every signal is a direct function of the logic—no distractions, no lag.

How this destroys the lag:

Standard deviation, ATR, and “volatility bands” are always late. They tell you what just happened. DoD and VoVix show you when the nature of volatility itself is changing—when the market is about to leave the old regime behind. This is the difference between trading the past and trading the future.

Inputs/Signals—explained for clarity:

Deviation Lookback & DoD Lookback:

Control the sensitivity and selectivity of the regime detector. Shorter = more signals, longer = only the rarest events.

Source Selection:

Choose from price, volume, volatility, or VoVix. Each source gives you a different lens on market stress. VoVix is for those who want to see the “regime quake” before the aftershocks.

HTF (Comparative Timeframe):

Set your higher timeframe for macro regime confirmation. When both DoD Z-scores align, you’re seeing a true market inflection.

VoVix Parameters:

Fine-tune the volatility-of-volatility engine for your market. Lower ATR Fast = more responsive; higher ATR Slow = more selective. Adjust for your asset, your timeframe, your edge.

Bottom line:

This isn’t just another “volatility” script. This is a regime anomaly detector, built for traders who want to anticipate, not react. Every input is there for a reason. Every plot is a direct readout of the quant logic. Use it to filter your entries, to time your exits, or to simply see the market’s hidden structure in real time.

Disclaimer:

Trading is risky. This script is for research and informational purposes only, not financial advice. Backtest, paper trade, and know your risk before going live. Past performance is not a guarantee of future results.

*Updated the Dashboard/Metrics Display for better visibility

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

(DAFE) DEVMA - Crossover (Deviation Moving Average) (DAFE) DEVMA - Crossover (Deviation Moving Average)

Let’s keep pushing the edge. After the breakthrough of Deviation over Deviation (DoD)—which gave traders a true lens into volatility’s hidden regime shifts—many asked: “What’s next?” The answer is DEVMA: a crossover engine built not on price, but on the heartbeat of the market itself.

Why is this different?

DEVMA isn’t just a moving average crossover. It’s a regime detector that tracks the expansion and contraction of deviation—giving you a real-time readout of when the market’s energy is about to shift. This is the next step for anyone who wants to anticipate volatility, not just react to it.

What sets DEVMA apart:

Volatility-First Logic:Both fast and slow lines are moving averages of deviation, not price. You’re tracking the market’s “energy,” not just its direction. This is the quant edge that most scripts miss.

Regime-Colored Lines:

The fast and slow DEVMA lines change color in real time—green/aqua for expansion, maroon/orange for contraction—so you can see regime shifts at a glance.

Quant-Pro Visuals:

Subtle glow, clean cross markers, and a minimalist dashboard keep your focus on what matters: the regime, not the noise.

Static Regime Thresholds:

Reference lines at 1.5 and 0.5 (custom colors) give you instant context for “normal” vs. “extreme” volatility states.

No Price Chasing:

This isn’t about following price. It’s about anticipating the next volatility regime—before the crowd even knows what’s coming.

How this builds on DoD:

DoD showed you when volatility itself was about to change. DEVMA takes that insight and turns it into a crossover engine—so you can see, filter, and act on regime shifts in real time. If DoD was the radar, DEVMA is the navigation system.

Inputs/Signals—explained for clarity:

Deviation Lookback:

Controls the sensitivity of the regime detector. Shorter = more signals, longer = only the rarest events.

Fast/Slow DEVMA Lengths:

Fine-tune how quickly the regime lines react. Fast for scalping, slow for swing trading.

Source Selection:

Choose from price, volume, volatility, or VoVix. Each source gives you a different lens on market stress. VoVix is for those who want to see the “regime quake” before the aftershocks.

VoVix Parameters:

Fine-tune the volatility-of-volatility engine for your market. Lower ATR Fast = more responsive; higher ATR Slow = more selective.

Bottom line:

DEVMA is for those who want to see the market’s heartbeat, not just its shadow. Use it to filter your trades, time your entries, or simply understand the market’s true rhythm. Every input is there for a reason. Every plot is a direct readout of the quant logic. Use with discipline, and make it your own.

Disclaimer:

Trading is risky. This script is for research and informational purposes only, not financial advice. Backtest, paper trade, and know your risk before going live. Past performance is not a guarantee of future results.

*Updated the Dashboard/Metrics Display for better visibility

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

Harmony in Havoc - The Entropy of VoVix Harmony in Havoc – The Entropy of VoVix

There are moments in the market when chaos and order are not opposites, but partners in a dance.

Harmony in Havoc is not just an indicator—it’s a window into that dance.

Most tools try to tame the market by smoothing it, boxing it in, or chasing after what’s already happened. This script does the opposite: it listens for the music beneath the noise, the rare moments when volatility and unpredictability align, and the market’s next movement is about to begin.

What is Harmony in Havoc?

VoVix Spike:

The pulse of volatility-of-volatility. Not just how much the market is moving, but how violently its own heartbeat is changing.

Entropy:

A real-time measure of surprise. When entropy is high, the market is not just moving—it’s breaking its own patterns, rewriting its own rules.

Progression Bar & Status:

The yellow bar is your visual gauge of tension. As it fills, the market is winding up.

Wait: The world is calm.

Get ready!: The storm is building.

Take Action!!: The probability of a regime eruption is at its peak.

Yellow Background:

When the background glows, the market is at its most unstable—this is not a buy or sell signal, but a quant alert.

How does it work?

Every tick, Harmony in Havoc measures the distance between the market’s current volatility and its own unpredictability. When the VoVix spike approaches or exceeds the entropy threshold, the system knows:

“This is the moment when the improbable becomes possible.”

Why is this different?

It doesn’t tell you what to do.

It doesn’t chase price.

It doesn’t care about trends, bands, or the past.

Instead, it gives you a quantitative sense of anticipation—a way to see when the market is most likely to break from its own history, and when the edge is at its sharpest.

How to use it:

Watch for the yellow background and “Take Action!!” status.

Use it as a regime filter, a volatility dashboard, or a warning system for your own strategies.

Tune the inputs for your asset and timeframe—make it your own.

Inputs—explained for you:

VoVix Fast/Slow ATR & Stdev:

Control how sensitive the system is to volatility shocks. Lower = more signals, higher = only the rarest events.

Entropy Window & Bins:

Control how “surprised” the entropy engine is by current volatility. Shorter window = more responsive, more bins = finer detail.

Show/Hide Controls:

Toggle the VoVix spike, entropy line, and their glows to customize your visual experience.

Bottom line:

This is not a buy or sell script.

This is a quant regime detector for those who want to feel the market’s tension—to sense when harmony and havoc are about to collide.

Disclaimer:

Trading is risky. This script is for research and informational purposes only, not financial advice. Backtest, paper trade, and know your risk before going live. Past performance is not a guarantee of future results.

*I've only tested this on 1 and 5 min frames.

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

3 days ago

Release Notes

* Now mobile friendly. I've added a toggle to switch the dashboard on/off, and added a mobile information line that shows the same information on the dashboard. This is to allow the script to stay visually in balance and this also has a toggle.

* Background color added that coresponds with Buy or Sell areas.

SuperTrend: Silent Shadow 🕶️ SuperTrend: Silent Shadow — Operate in trend. Vanish in noise.

Overview

SuperTrend: Silent Shadow is an enhanced trend-following system designed for traders who demand clarity in volatile markets and silence during indecision.

It combines classic Supertrend logic with a proprietary ShadowTrail engine and an adaptive Silence Protocol to filter noise and highlight only the cleanest signals.

Key Features

✅ Core Supertrend Logic

Built on Average True Range (ATR), this trend engine identifies directional bias with visual clarity. Lines adjust dynamically with price action and flip when meaningful reversals occur.

✅ ShadowTrail: Stepped Counter-Barrier

ShadowTrail doesn’t predict reversals — it reinforces structure.

When price is trending, ShadowTrail forms a stepped ceiling in downtrends and a stepped floor in uptrends. This visual containment zone helps define the edges of price behavior and offers a clear visual anchor for stop-loss placement and trade containment.

✅ Silence Protocol: Adaptive Noise Filtering

During low-volatility zones, the system enters “stealth mode”:

• Trend lines turn white to indicate reduced signal quality

• Fill disappears to reduce distraction

This helps avoid choppy entries and keeps your focus sharp when the market isn’t.

✅ Visual Support & Stop-Loss Utility

When trendlines flatten or pause, they naturally highlight price memory zones. These flat sections often align with:

• Logical stop-loss levels

• Prior support/resistance areas

• Zones of reduced volatility where price recharges or rejects

✅ Custom Styling

Full control over line colors, width, transparency, fill visibility, and silence behavior. Tailor it to your strategy and visual preferences.

How to Use

• Use Supertrend color to determine bias — flips mark momentum shifts

• ShadowTrail mirrors the primary trend as a structural ceiling/floor

• Use flat segments of both lines to identify consolidation zones or place stops

• White lines = low-quality signal → stand by

• Combine with RSI, volume, divergence, or your favorite tools for confirmation

Recommended For:

• Traders seeking clearer trend signals

• Avoiding false entries in sideways or silent markets

• Identifying key support/resistance visually

• Structuring stops around real market containment levels

• Scalping, swing, or position trading with adaptive clarity

Built by Sherlock Macgyver

Forged for precision. Designed for silence.

When the market speaks, you listen.

When it doesn’t — you wait in the shadows.

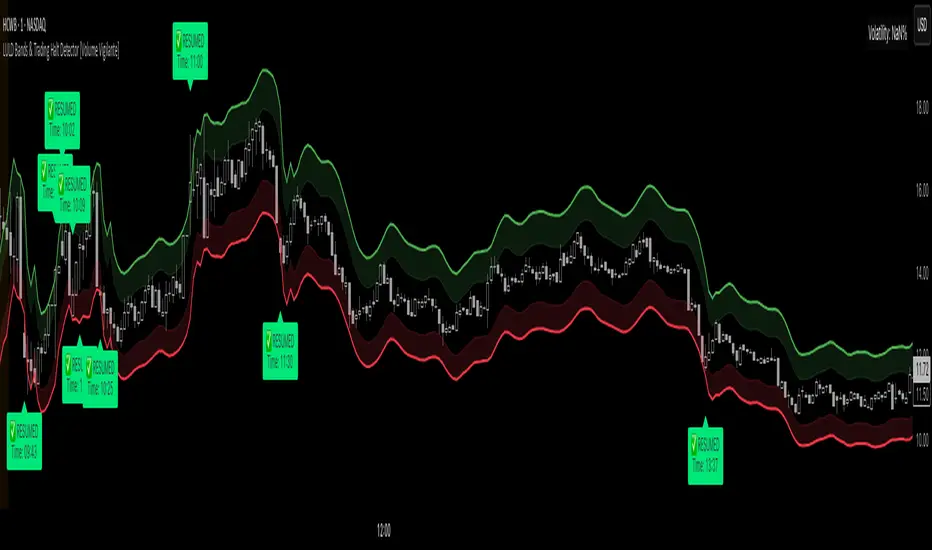

LULD Bands & Trading Halt Detector [Volume Vigilante]📖 LULD Bands & Trading Halt Detector

This advanced tool visualizes official Limit Up / Limit Down (LULD) price bands and detects regulatory trading halts and resumptions based on SEC and NASDAQ rules. It is engineered for high accuracy by anchoring all calculations to the 1-minute timeframe, ensuring reliable signals across any chart resolution.

📌 What Does This Script Do?

- Draws real-time LULD price band estimations and optional buffer (caution) zones directly on the chart.

- Detects trading halt resumptions by monitoring time gaps between candles and other regulatory criteria. (Note: Due to Pine Script limitations, halts cannot be detected in real-time, only resumptions after they occur.)

- Triggers real-time alerts for:

- Trading Resumptions (Limit Up & Limit Down)

- LULD Zone Entries (Caution Zone)

- Band Breaches (Limit Up and Limit Down)

- Plots historical halt resumption markers to analyse past events.

📐 How It Works:

- Implements official SEC/NASDAQ LULD rules for Tier 1 and Tier 2 securities.

- Applies special band adjustments for the final 25 minutes of trading (after 3:35 PM ET).

- Anchors all logic to the 1-minute timeframe for precise calculations, even on higher timeframe charts.

- Includes adjustable volume and volatility filters to eliminate false signals (ghost halts) on low-- liquidity assets, especially Tier 2 securities when TradingView fails to print candles.

⚙️ How to Use It:

1.) Apply the script to any asset or timeframe.

2.) Adjust Volume and Volatility Filters to reduce noise. (Recommended: 500,000+ volume, 10%+ volatility.)

3.) Enable or disable visual components like bands, buffer zones, and halt resumption labels.

4.) Configure alerts directly from the script settings panel.

5.) Apply alerts to individual assets via "Add Alert On..." or to entire watchlists using "Add Alert on the List."

🧩 What Makes This Script Unique?

- True 1-Minute Anchored Calculations: Ensures alerts and visuals match official trading halt criteria regardless of chart timeframe.

- Customisable Buffered Zones: Visualise proximity to regulatory price limits and avoid volatility traps.

- Combines halt resumption detection, limit up/down band visualisation, and real-time alerts into one clean, modular tool.

📚 Disclaimer:

This script is for educational purposes only and does not constitute financial advice. Use at your own discretion and consult a licensed financial advisor before making trading decisions based on it.

Official Resources:

- NASDAQ LULD Regulations (FAQ):

www.nasdaqtrader.com

Current Nasdaq Trading Halts:

www.nasdaqtrader.com

ATR ComboA Collection of three ATRs.

The whole idea of this indicator is to easily visualise the relationship of volatility to the current price action.

The default settings are:

5 Moving Average (Pink)

50 Moving Average (Blue)

1000 Moving Average (Yellow)

Using the default settings, the Yellow line represents the larger-scale volatility average.

the Blue line represents more recent volatility and the Pink lien represents the very recent average.

Using this indicator is possible in a number of ways:

If volatility is high and directional, you will see a sharp increase in the Pink line.

If volatility is high and choppy, the Pink line will be well above the Blue line and will oscillate up and down.

If volatility is starting to cool down, the Pink line will approach the Blue and Yellow lines.

Disparity Index with Volatility ZonesDisparity Index with Volatility Zones

is a momentum oscillator that measures the percentage difference between the current price and its simple moving average (SMA). This allows traders to identify overbought/oversold conditions, assess momentum strength, and detect potential trend reversals or continuations.

🔍 Core Concept:

The Disparity Index (DI) is calculated as:

DI = 100 × (Price − SMA) / SMA

A positive DI indicates the price is trading above its moving average (potential bullish sentiment), while a negative DI suggests the price is below the average (potential bearish sentiment).

This version of the Disparity Index introduces a dual-zone volatility framework, offering deeper insight into the market's current state.

🧠 What Makes This Version Unique?

1. High Volatility Zones

When DI crosses above +1.0% or below –1.0%, it often indicates the start or continuation of a strong trend.

Sustained readings beyond these thresholds typically align with trending phases, offering opportunities for momentum-based entries.

A reversal back within ±1.0% after exceeding these levels can suggest a shift in momentum — similar to how RSI exits the overbought/oversold zones before reversals.

These thresholds act as dynamic markers for breakout confirmation and potential trend exhaustion.

2. Low Volatility Zones

DI values between –0.5% and +0.5% define the low-volatility zone, shaded for visual clarity.

This area typically indicates market indecision, sideways price action, or consolidation.

Trading within this range may favor range-bound or mean-reversion strategies, as trend momentum is likely limited.

The logic is similar to interpreting a flat ADX, tight Bollinger Bands, or contracting Keltner Channels — all suggesting consolidation.

⚙️ Features:

Customizable moving average length and input source

Adjustable thresholds for overbought/oversold and low-volatility zones

Optional visual fill between low-volatility bounds

Clean and minimal chart footprint (non-essential plots hidden by default)

📈 How to Use:

1. Trend Confirmation:

A break above +1.0% can be used as a bullish continuation signal.

A break below –1.0% may confirm bearish strength.

Long periods above/below these thresholds support trend-following entries.

2. Reversal Detection:

If DI returns below +1.0% after exceeding it, bullish momentum may be fading.

If DI rises above –1.0% after falling below, bearish pressure may be weakening.

These shifts resemble overbought/oversold transitions in oscillators like RSI or Stochastic, and can be paired with divergence, volume, or price structure analysis for higher reliability.

3. Sideways Market Detection:

DI values within ±0.5% indicate low volatility or a non-trending environment.

Traders may avoid breakout entries during these periods or apply range-trading tactics instead.

Observing transitions out of the low-volatility zone can help anticipate breakouts.

4. Combine with Other Indicators:

DI signals can be enhanced using tools like MACD, Volume Oscillators, or Moving Averages.

For example, a DI breakout beyond ±1.0% supported by a MACD crossover or volume spike can help validate trend initiation.

This indicator is especially powerful when paired with Bollinger Bands:

A simultaneous price breakout from the Bollinger Band and DI moving beyond ±1.0% can help identify early trend inflection points.

This combination supports entering positions early in a developing trend, improving the efficiency of trend-following strategies and enhancing decision-making precision.

It also helps filter false breakouts when DI fails to confirm the move outside the band.

This indicator is designed for educational and analytical purposes and works across all timeframes and asset classes.

It is particularly useful for traders seeking a clear framework to identify momentum strength, filter sideways markets, and improve entry timing within a larger trading system.

VOID Directional Spike MarkerThis indicator highlights significant directional moves on the $VOID chart (NYSE USI:UVOL − DERIBIT:DVOL ) using simple visual cues:

🔼 Green up arrows when the candle closes significantly higher than it opens

🔽 Red down arrows when the candle closes significantly lower than it opens

Threshold is fully customizable (default: 15,000,000)

Ideal for spotting explosive internal shifts on the 5-minute chart during key market moments

Alerts included for both up and down spikes

Use this to track aggressive buying or selling pressure across NYSE internals and time your entries on NQ, ES, or YM with stronger conviction.