Dual Keltner Channels Strategy [Eastgate3194]This strategy utilised 2 Keltner Channels to perform counter trade.

The strategy have 2 steps:

Long Position:

Step 1. Close price must cross under Outer Lower band of Keltner Channel.

Step 2. Close price cross over Inner Lower band of Keltner Channel.

Short Position:

Step 1. Close price must cross over Outer Upper band of Keltner Channel.

Step 2. Close price cross under Inner Upper band of Keltner Channel.

Volatility

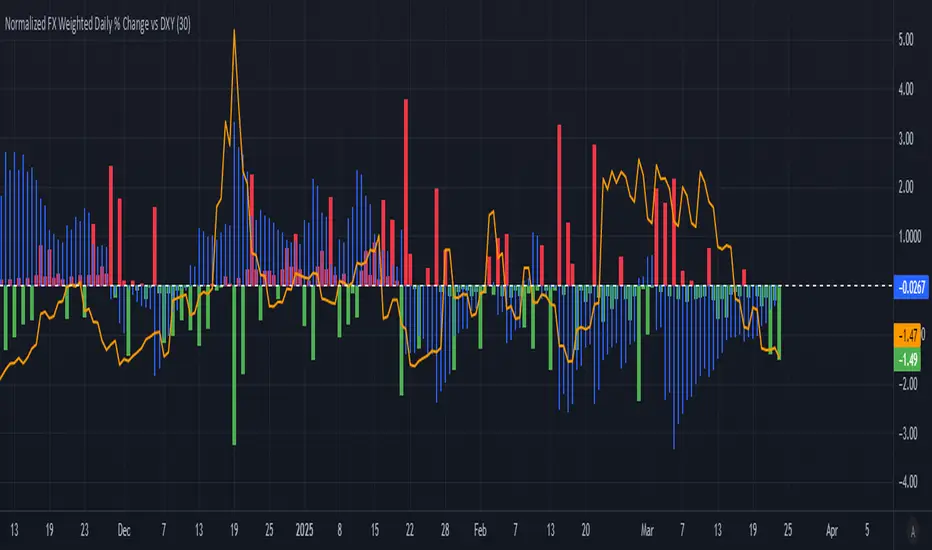

Normalized FX Weighted Daily % Change vs DXYThis indicator tracks international liquidity flows by measuring the USD’s relative strength against major currencies—EUR, CNY, JPY, GBP, and CAD. It calculates the weighted percentage change of each pair over a specified interval. A positive reading means the USD is weakening (liquidity flowing out of the US), while a negative reading indicates the USD is strengthening (liquidity flowing in). Additionally, the indicator incorporates the DXY index and VIX, with all components normalized using Z-scores for clear, comparable insights into market dynamics.

Fib BB on VWMA*ATRThis TradingView Pine Script is designed to plot Fibonacci Bollinger Bands on a Volume Weighted Moving Average (VWMA) using the Average True Range (ATR). The script takes a higher timeframe (HTF) approach, allowing traders to analyze price action and volatility from a broader market perspective.

🔹 How It Works

Higher Timeframe Data Integration

Users can select a specific timeframe to calculate the VWMA and ATR.

This allows for a more macro perspective, avoiding the noise of lower timeframes.

Volume Weighted Moving Average (VWMA)

Unlike the Simple Moving Average (SMA), VWMA gives higher weight to price movements with larger volume.

Calculation Formula:

𝑉𝑊𝑀𝐴=∑(𝐶𝑙𝑜𝑠𝑒×𝑉𝑜𝑙𝑢𝑚𝑒) / ∑𝑉𝑜𝑙𝑢𝑚𝑒

Since VWMA accounts for volume, it is more reactive to price zones with high buying or selling activity, making it useful for identifying liquidity zones.

ATR-Based Fibonacci Bollinger Bands

The Average True Range (ATR) is used to measure market volatility.

Instead of standard deviation-based Bollinger Bands, Fibonacci multipliers (2.618, 3.0, 3.414) are applied to ATR.

These bands adjust dynamically with market volatility.

🔹 Key Findings from Exploration

Through testing and analysis, this indicator seems to effectively detect supply and demand zones, particularly at the Fibonacci levels of 2.618 to 3.414.

Price frequently reacts at these bands, indicating that they capture key liquidity zones.

Potential Order Block Detection:

The ends of the Fibonacci Bollinger Bands (especially at 2.618, 3.0, and 3.414) tend to align with order blocks—areas where institutional traders previously accumulated or distributed positions.

This is particularly useful for order flow traders who focus on unfilled institutional orders.

🔹 How to Use This Indicator?

Identifying Order Blocks

When price reaches the upper or lower bands, check if there was a strong reaction (rejection or consolidation).

If price rapidly moves away from a band, that level might be an order block.

Spotting Liquidity Pools

VWMA’s nature enhances liquidity detection since it emphasizes high-volume price action.

If a price level repeatedly touches the band without breaking through, it suggests institutional orders may be absorbing liquidity there.

Trend Confirmation

If VWMA is trending upwards and price keeps rejecting the lower bands, it confirms a strong bullish trend.

Conversely, constant rejection from the upper bands suggests a bearish market.

This script is designed for open-source publication and offers traders a refined approach to detecting order blocks and liquidity zones using Fibonacci-based volatility bands.

📌 한글 설명 (상세 설명)

이 트레이딩뷰 파인스크립트는 거래량 가중 이동평균(VWMA)과 평균 실제 범위(ATR)를 활용하여 피보나치 볼린저 밴드를 표시하는 지표입니다.

또한, 고차 타임프레임(HTF) 데이터를 활용하여 시장의 큰 흐름을 분석할 수 있도록 설계되었습니다.

🔹 지표 작동 방식

고차 타임프레임(HTF) 데이터 적용

사용자가 원하는 타임프레임을 선택하여 VWMA와 ATR을 계산할 수 있습니다.

이를 통해 더 큰 시장 흐름을 분석할 수 있으며, 저타임프레임의 노이즈를 줄일 수 있습니다.

거래량 가중 이동평균(VWMA) 적용

VWMA는 단순 이동평균(SMA)보다 거래량이 많은 가격 움직임에 더 큰 가중치를 부여합니다.

계산 공식:

𝑉𝑊𝑀𝐴=∑(𝐶𝑙𝑜𝑠𝑒×𝑉𝑜𝑙𝑢𝑚𝑒) / ∑𝑉𝑜𝑙𝑢𝑚𝑒

거래량이 많이 발생한 가격 구간을 강조하는 특성이 있어, 시장의 유동성 구간을 더 정확히 포착할 수 있습니다.

ATR 기반 피보나치 볼린저 밴드 생성

ATR(Average True Range)를 활용하여 변동성을 측정합니다.

기존의 표준편차 기반 볼린저 밴드 대신, 피보나치 계수(2.618, 3.0, 3.414)를 ATR에 곱하여 밴드를 생성합니다.

이 밴드는 시장 변동성에 따라 유동적으로 조정됩니다.

🔹 탐구 결과: 매물대 및 오더블록 감지

테스트를 통해 Fibonacci 2.618 ~ 3.414 구간에서 매물대 및 오더블록을 포착하는 경향이 있음을 확인했습니다.

가격이 피보나치 밴드(특히 2.618, 3.0, 3.414)에 닿을 때 반응하는 경우가 많음

VWMA의 특성을 통해 오더블록을 감지할 가능성이 높음

🔹 오더블록(Order Block) 감지 원리

Fibonacci 밴드 끄트머리(2.618 ~ 3.414)에서 가격이 강하게 반응

이 영역에서 가격이 강하게 튀어 오르거나(매수 압력) 급락하는(매도 압력) 경우,

→ 기관들이 포지션을 청산하거나 추가 매집하는 구간일 가능성이 큼.

과거에 대량 주문이 체결된 가격 구간(= 오더블록)일 수 있음.

VWMA를 통한 유동성 감지

VWMA는 거래량이 집중된 가격을 기준으로 이동하기 때문에, 기관 주문이 많이 들어온 가격대를 강조하는 특징이 있음.

따라서 VWMA와 피보나치 밴드가 만나는 지점은 유동성이 높은 핵심 구간이 될 가능성이 큼.

매물대 및 청산 구간 분석

가격이 밴드에 도달했을 때 강한 반등이 나오는지를 확인 → 오더블록 가능성

가격이 밴드를 여러 번 테스트하면서 돌파하지 못한다면, 해당 지점은 강한 매물대일 가능성

🔹 활용 방법

✅ 오더블록 감지:

가격이 밴드(2.618~3.414)에 닿고 강하게 튕긴다면, 오더블록 가능성

해당 지점에서 거래량 증가 및 강한 반등 발생 시 매수 고려

✅ 유동성 풀 확인:

VWMA와 피보나치 밴드가 만나는 구간에서 반복적으로 거래량이 터진다면, 해당 지점은 기관 유동성 구간일 가능성

✅ 추세 확인:

VWMA가 상승하고 가격이 밴드 하단(지지선)에서 튕긴다면 강한 상승 추세

VWMA가 하락하고 가격이 밴드 상단(저항선)에서 거부당하면 하락 추세 지속

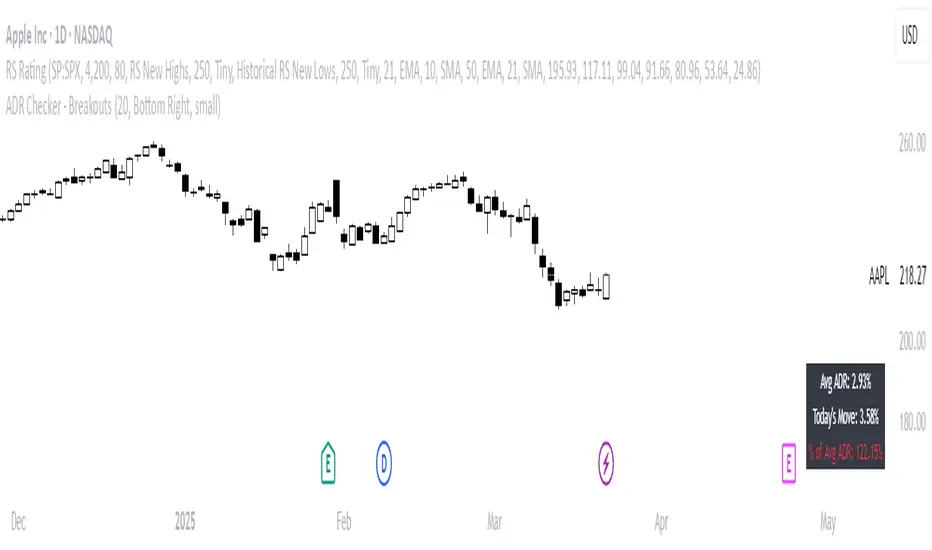

ADR Checker - Breakouts📈 ADR Checker – Breakouts

Gain the edge by knowing when a stock has already made its move.

🚀 What It Does:

The ADR Checker - Breakouts is a powerful yet simple visual tool that helps traders instantly assess whether a stock has already exceeded its Average Daily Range (ADR) for the day — a critical piece of information for momentum traders, swing traders, and especially those following breakout, VCP, or CANSLIM strategies.

Using a customizable on-screen table that always stays in view (regardless of zoom or chart scaling), this script shows:

✅ Average ADR% – 20-day average range, calculated in %.

📊 Today’s Move – how much the stock has moved today.

🔥 % of Avg ADR – today's move relative to its historical average, with live color feedback:

🟥 Over 100% (Overextended – danger!)

🟧 70-100% (Caution zone)

🟩 Below 70% (Room to move)

💡 Why It Matters:

One of the most overlooked mistakes by breakout traders is entering a trade after the move has already happened. If a stock has already moved more than its typical daily range, the odds of further continuation sharply decrease, while the risk of pullback or chop increases.

With this tool, you can:

🚫 Avoid chasing extended breakouts

🎯 Time entries before the real move

⚠️ Quickly assess risk/reward potential intraday

🧠 Example Use Case:

Imagine you're watching a classic VCP setup or flat base breakout. The stock breaks out on volume—but when you check this indicator, you see:

Today’s Move: 7.2%

Avg ADR: 5.3%

% of ADR: 135% 🟥

This tells you the stock is already well beyond its average daily range. While it may continue higher, odds now favor a consolidation, shakeout, or pullback. This is your cue to wait for a better entry or pass entirely.

On the flip side, if the breakout just started and the % of ADR is still under 50%, you have confirmation that there’s room to run — giving you more confidence to enter early.

⚙️ Fully Customizable:

Choose position on screen (top/bottom left/right)

Customize text color, background, and size

🔧 Install This Tool and:

✅ Stop chasing extended moves

✅ Add discipline to your entries

✅ Improve your breakout win rate

Perfect for VCP, CANSLIM, and BREAKOUT traders who want a clean, edge-enhancing visual guide.

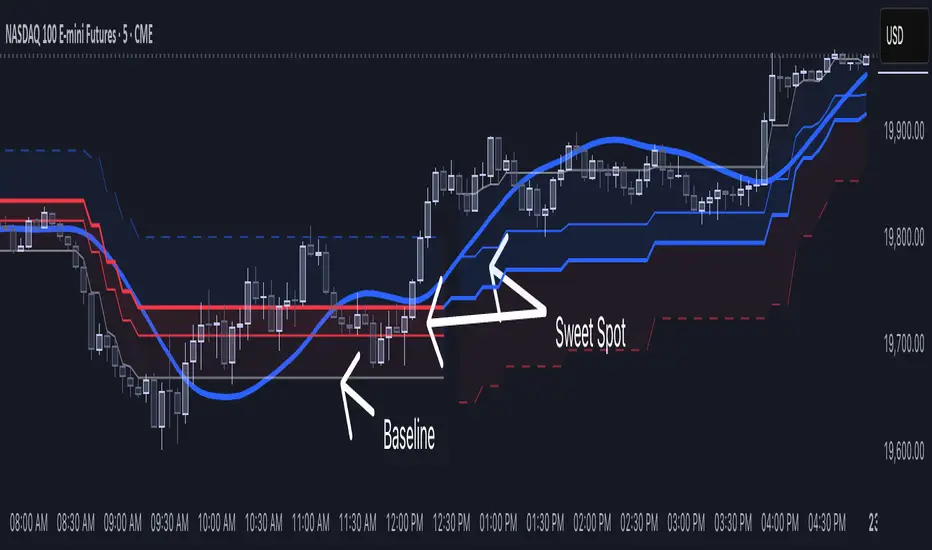

[NLR] - SweetSpot ZonesThe Sweet Spot Zone helps you find the best spots to enter a trade, inspired by the " Follow Line Indicator " by Dreadblitz (big thanks to him!). It draws a colored zone on your chart to show ideal entry points, with a Base Point to keep you on track.

What It Does

Blue Zone: Uptrend—buy when the price dips into the zone.

Red Zone: Downtrend—sell or short when the price climbs into the zone.

Base Point: A gray line showing the key level the zone is built on.

How to Use It

Look for the colored zone:

- Blue: Buy if the price dips into the zone but stays above the Base Point.

- Red: Sell/short if the price climbs into the zone but stays below the Base Point.

Important: Avoid entering trade beyond base point - you might see low returns and face big drawdowns.

Confirm with other signals (like RSI/MACD) before entering.

Settings

ATR Length (10): How far back it looks to calculate price movement.

ATR Multiplier (2.5): How wide the zone is.

Error Margin (5.0): Keeps the zone steady during small price wiggles.

Uptrend/Downtrend Colors: Change the zone colors if you’d like!

Credits

Inspired by the "Follow Line Indicator" by Dreadblitz—check out his work for more great ideas!

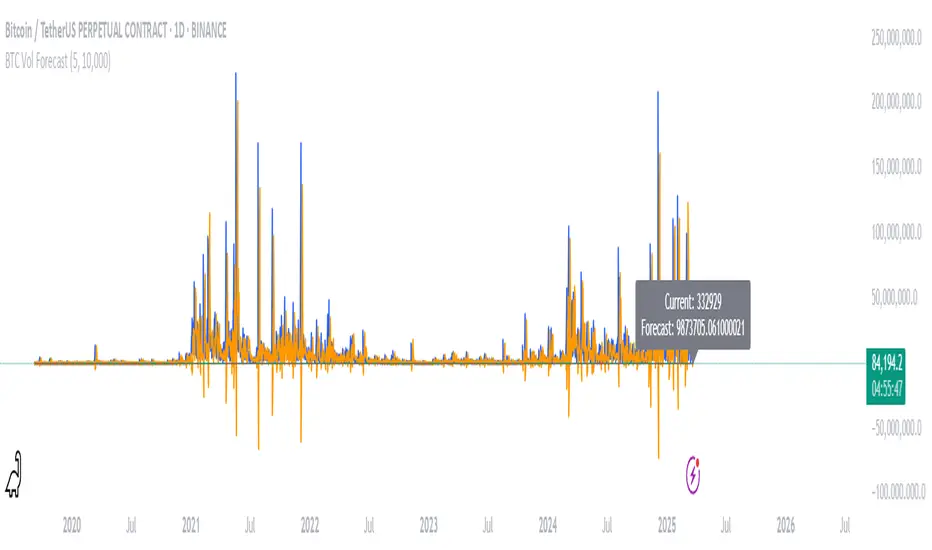

BTC Volatility ForecastThe "BTC Volatility Forecast" indicator is designed to help traders anticipate Bitcoin (BTC) price volatility by analyzing historical daily price ranges and projecting future fluctuations. Inspired by advanced volatility forecasting studies, it calculates an approximate realized variance using the squared difference between each day’s high and low prices. By applying a simple linear regression model over the past five days of variance data (customizable via the "Lag Period" input), the indicator provides a forecast for the next day’s volatility. This makes it a valuable tool for BTC traders looking to gauge potential market turbulence and adjust their strategies accordingly.

On the chart, the indicator displays two lines: a blue solid line representing the current realized variance and an orange line showing the forecasted volatility for the upcoming day. Traders can set a "Volatility Threshold" to trigger alerts when the forecast exceeds a specified level, aiding in risk management or trade planning. A debug label on the last bar also shows the exact current and forecasted values for quick reference. While this version uses daily data for simplicity, it captures the essence of volatility prediction and can be a starting point for understanding BTC market dynamics—perfect for both novice and experienced traders on TradingView.

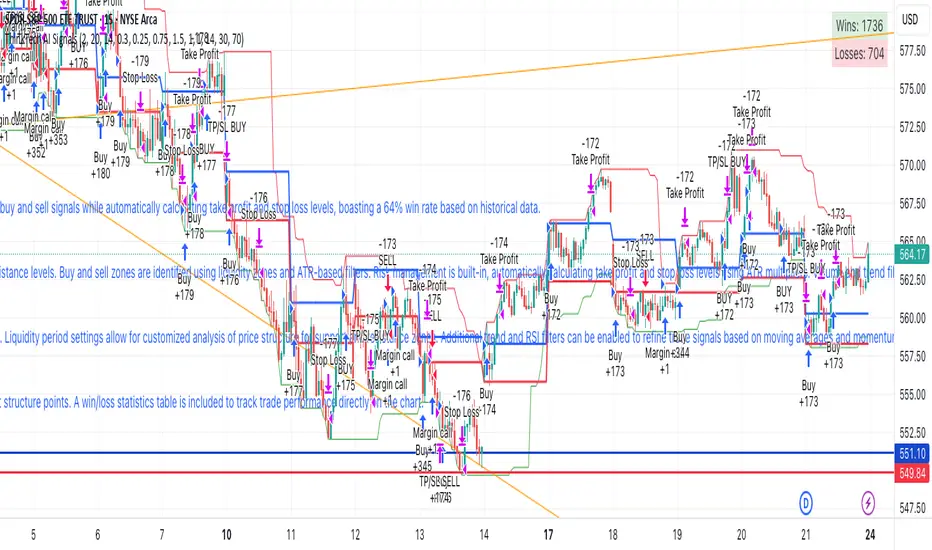

ThinkTech AI SignalsThink Tech AI Strategy

The Think Tech AI Strategy provides a structured approach to trading by integrating liquidity-based entries, ATR volatility thresholds, and dynamic risk management. This strategy generates buy and sell signals while automatically calculating take profit and stop loss levels, boasting a 64% win rate based on historical data.

Usage

The strategy can be used to identify key breakout and retest opportunities. Liquidity-based zones act as potential accumulation and distribution areas and may serve as future support or resistance levels. Buy and sell zones are identified using liquidity zones and ATR-based filters. Risk management is built-in, automatically calculating take profit and stop loss levels using ATR multipliers. Volume and trend filtering options help confirm directional bias using a 50 EMA and RSI filter. The strategy also allows for session-based trading, limiting trades to key market hours for higher probability setups.

Settings

The risk/reward ratio can be adjusted to define the desired stop loss and take profit calculations. The ATR length and threshold determine ATR-based breakout conditions for dynamic entries. Liquidity period settings allow for customized analysis of price structure for support and resistance zones. Additional trend and RSI filters can be enabled to refine trade signals based on moving averages and momentum conditions. A session filter is included to restrict trade signals to specific market hours.

Style

The strategy includes options to display liquidity lines, showing key support and resistance areas. The first 15-minute candle breakout zones can also be visualized to highlight critical market structure points. A win/loss statistics table is included to track trade performance directly on the chart.

This strategy is intended for descriptive analysis and should be used alongside other confluence factors. Optimize your trading process with Think Tech AI today!

Trapped Traders Order BlocksHow It Works

The Trapped Traders Order Blocks indicator identifies specific price action patterns that suggest large market participants ("big money") have been trapped in losing positions after significant price sweeps, creating potential opportunities for reversals. The indicator detects both "bullish trap blocks" (where bearish traders are trapped) and "bearish trap blocks" (where bullish traders are trapped). Here’s the step-by-step process for each:

Bullish Trap Block (Bears Trapped):

A bearish candle (Candle A) must sweep the high of the previous candle (Candle B), meaning its high exceeds the high of the prior candle.

This bearish candle must have a longer upper wick than its lower wick, indicating rejection of higher prices.

The candle must not be a doji (i.e., it must have a significant body, defined as the body being at least 10% of the candle's range).

The next candle (Candle C) must close above the body of the bearish candle (Candle A), suggesting that price has immediately moved against the bearish sweep, potentially trapping bearish traders who entered short positions expecting a downward move.

The body of the bearish candle (Candle A) is marked as a "bullish trap block." A box is drawn around this candle's body, and a label ("Bullish Trap") is placed below it.

Bearish Trap Block (Bulls Trapped):

A bullish candle (Candle A) must sweep the low of the previous candle (Candle B), meaning its low is below the low of the prior candle.

This bullish candle must have a longer lower wick than its upper wick, indicating rejection of lower prices.

The candle must not be a doji.

The next candle (Candle C) must close below the body of the bullish candle (Candle A), suggesting that price has immediately moved against the bullish sweep, potentially trapping bullish traders who entered long positions expecting an upward move.

The body of the bullish candle (Candle A) is marked as a "bearish trap block." A box is drawn around this candle's body, and a label ("Bearish Trap") is placed above it.

Dynamic Box Extension:

For both bullish and bearish trap blocks, the box extends dynamically to the current bar unless it exceeds a user-defined age (default is 52 bars), at which point it stops at the maximum age.

Sweep Detection:

Bullish Sweep (of any trap block, bullish or bearish):

The current candle's open is above the top of the box.

The low is below the top of the box.

The close is above the top of the box.

The lower wick is longer than the upper wick (indicating rejection of lower prices).

The close is above 50% of the candle's range (ensuring a strong bullish bias).

When a bullish sweep occurs, a label ("Bullish Sweep") is placed at the low of the candle, pointing upward, and an alert is triggered.

Bearish Sweep (of any trap block, bullish or bearish):

The current candle's open is below the bottom of the box.

The high is above the bottom of the box.

The close is below the bottom of the box.

The upper wick is longer than the lower wick (indicating rejection of higher prices).

The close is below 50% of the candle's range (ensuring a strong bearish bias).

When a bearish sweep occurs, a label ("Bearish Sweep") is placed at the high of the candle, pointing downward, and an alert is triggered.

When to Be Used

The Trapped Traders Order Blocks indicator is best used in the following scenarios:

Reversal Trading:

Use this indicator to identify potential reversal points in the market. Bullish trap blocks suggest that trapped bears may unwind their short positions, leading to a potential bullish move. Bearish trap blocks suggest that trapped bulls may unwind their long positions, leading to a potential bearish move.

Look for sweeps of these blocks as confirmation of a directional move. A bullish sweep indicates a potential upward move, while a bearish sweep indicates a potential downward move.

Range-Bound Markets:

In sideways or ranging markets, trapped blocks can highlight key levels where large players have been caught off-guard. These levels often act as support or resistance, and a sweep of the block can signal a breakout or continuation in the direction of the sweep.

Confluence with Other Indicators:

Combine the trapped blocks with other technical analysis tools, such as support/resistance levels, Fibonacci retracements, or volume analysis, to increase the probability of a successful trade. For example, a bullish trap block near a strong support level with a bullish sweep can provide a high-probability setup for a long position, while a bearish trap block near a strong resistance level with a bearish sweep can signal a short opportunity.

Timeframes:

The indicator is most effective on higher timeframes such as 1-day (1D), 1-week (1W), and 1-month (1M) charts. These timeframes are more likely to capture significant moves involving large market participants, reducing noise and false signals compared to lower timeframes. While it can be used on lower timeframes (e.g., 1-hour or 4-hour), the signals may be less reliable due to increased market noise.

Logic Behind It

The logic behind the Trapped Traders Order Blocks indicator is rooted in market psychology and the behavior of large market participants ("big money"). When a large sweep candle occurs where price spikes in one direction but then quickly reverses it often indicates that traders have entered positions in the direction of the sweep, expecting a continuation. However, if the price immediately moves against them, these traders are now trapped in losing positions.

Bullish Trap Block (Bears Trapped):

A large bearish sweep candle (spiking upward but closing lower) suggests that bearish traders (bears) have entered short positions at the top of the move, expecting a downward continuation. If the next candle closes above the bearish candle's body, these bears are trapped in losing positions.

The body of the bearish candle becomes a "bullish trap block" because the trapped bears are likely to have placed their stop-loss orders or break-even exit orders just above the high of the sweep candle or within the body of the candle. As price revisits this level in the future, these trapped traders may attempt to unwind their positions by buying back their shorts, which can drive the price higher. This unwinding process often attracts new buyers, leading to a potential bullish reversal or continuation.

The bullish sweep conditions (e.g., close > box top, longer lower wick, and close above 50% of the range) ensure that the price action at the block level shows strong bullish momentum and rejection of lower prices, confirming the potential for a move higher.

Bearish Trap Block (Bulls Trapped):

A large bullish sweep candle (spiking downward but closing higher) suggests that bullish traders (bulls) have entered long positions at the bottom of the move, expecting an upward continuation. If the next candle closes below the bullish candle's body, these bulls are trapped in losing positions.

The body of the bullish candle becomes a "bearish trap block" because the trapped bulls are likely to have placed their stop-loss orders or break-even exit orders just below the low of the sweep candle or within the body of the candle. As price revisits this level in the future, these trapped traders may attempt to unwind their positions by selling their longs, which can drive the price lower. This unwinding process often attracts new sellers, leading to a potential bearish reversal or continuation.

The bearish sweep conditions (e.g., close < box bottom, longer upper wick, and close below 50% of the range) ensure that the price action at the block level shows strong bearish momentum and rejection of higher prices, confirming the potential for a move lower.

Summary

Bullish Trap Block: Occurs when bears get trapped after a bearish sweep candle is immediately followed by a bullish candle, indicating a potential reversal as trapped bears may unwind their positions.

Bearish Trap Block: Occurs when bulls get trapped after a bullish sweep candle is immediately followed by a bearish candle, indicating a potential bearish reversal.

Use Case: Ideal for identifying reversal opportunities, especially in range-bound markets or at key support/resistance levels on higher timeframes like 1D, 1W, and 1M, and can be combined with other indicators for confluence.

Logic: Large sweep candles followed by an immediate reversal suggest that big money has been trapped, and these traders may unwind their positions at break-even in the near future, driving price in the opposite direction of their initial trade.

This indicator provides a visual and actionable way to identify these trapped trader scenarios, with customizable settings for box display, sweep visuals, and alerts to help traders capitalize on these opportunities, particularly on higher timeframes where the signals are most reliable.

Hourly Volatility Explorer📊 Hourly Volatility Explorer: Master The Market's Pulse

Unlock the hidden rhythms of price action with this sophisticated volatility analysis tool. The Hourly Volatility Explorer reveals the most potent trading hours across multiple time zones, giving you a strategic edge in timing your trades.

🌟 Key Features:

⏰ Multi-Timezone Analysis

• GMT (UTC+0)

• EST (UTC-5) - New York

• BST (UTC+1) - London

• JST (UTC+9) - Tokyo

• AEST (UTC+10) - Sydney

Perfect for tracking major market sessions and their overlaps!

📈 Dynamic Visualization

• Color-gradient hourly bars for instant pattern recognition

• Real-time volatility comparison

• Interactive data table with comprehensive statistics

• Automatic highlighting of peak volatility periods

🎯 Strategic Applications:

Day Trading:

• Identify optimal trading windows

• Avoid low-liquidity periods

• Capitalize on session overlaps

• Fine-tune entry/exit timing

Risk Management:

• Set appropriate stop losses based on hourly volatility

• Adjust position sizes for different market hours

• Optimize risk-reward ratios

• Plan around high-impact hours

Global Market Analysis:

• Track volatility across all major sessions

• Spot institutional trading patterns

• Identify quiet vs. active periods

• Monitor 24/7 market dynamics

💡 Perfect For:

• Forex traders navigating global sessions

• Crypto traders in 24/7 markets

• Day traders optimizing execution times

• Algorithmic traders fine-tuning strategies

• Risk managers calibrating exposure

📊 Advanced Features:

• Rolling 3-month analysis for reliable patterns

• Precise pip movement calculations

• Sample size tracking for statistical validity

• Real-time current hour comparison

• Color-coded visual system for instant insights

⚡ Pro Trading Tips:

• Use during major session overlaps for maximum opportunity

• Compare patterns across different instruments

• Combine with volume analysis for deeper insights

• Track seasonal variations in hourly patterns

• Build trading schedules around peak hours

🎓 Educational Value:

• Understand market microstructure

• Learn global market dynamics

• Master timezone relationships

• Develop timing intuition

🛠️ Customization:

• Adjustable lookback period

• Flexible pip multiplier

• Multiple timezone options

• Visual preference settings

Whether you're scalping the 1-minute chart or managing longer-term positions, the Hourly Volatility Explorer provides the precise timing intelligence needed for today's global markets.

Transform your trading schedule from guesswork to science. Know exactly when markets move, why they move, and how to position yourself for maximum opportunity.

#TechnicalAnalysis #Trading #Volatility #MarketTiming #DayTrading #Forex #Crypto #TradingView #PineScript #MarketAnalysis #TradingStrategy #RiskManagement #GlobalMarkets #FinancialMarkets #TradingTools #MarketStructure #PriceAction #Scalping #SwingTrading #AlgoTrading

Percentage ChangeThis is a very simple script. It calculations the percentage the stocks price has changed with 3 different metrics over the configured lookback period.

- Close to Open: calculates the percentage difference between the opening bar at the beginning of the lookback period to the closing current bar.

- Low to High: calculates the percentage difference between the lowest low to the highest high over the period.

- High to Low: calculates the percentage difference between the highest high to the lowest low over the period.

This indicator is used to call out especially volatile periods allowing traders to target spikes up or down.

Nef33 Forex & Crypto Trading Signals PRO

1. Understanding the Indicator's Context

The indicator generates signals based on confluence (trend, volume, key zones, etc.), but it does not include predefined SL or TP levels. To establish them, we must:

Use dynamic or static support/resistance levels already present in the script.

Incorporate volatility (such as ATR) to adjust the levels based on market conditions.

Define a risk/reward ratio (e.g., 1:2).

2. Options for Determining SL and TP

Below, I provide several ideas based on the tools available in the script:

Stop Loss (SL)

The SL should protect you from adverse movements. You can base it on:

ATR (Volatility): Use the smoothed ATR (atr_smooth) multiplied by a factor (e.g., 1.5 or 2) to set a dynamic SL.

Buy: SL = Entry Price - (atr_smooth * atr_mult).

Sell: SL = Entry Price + (atr_smooth * atr_mult).

Key Zones: Place the SL below a support (for buys) or above a resistance (for sells), using Order Blocks, Fair Value Gaps, or Liquidity Zones.

Buy: SL below the nearest ob_lows or fvg_lows.

Sell: SL above the nearest ob_highs or fvg_highs.

VWAP: Use the daily VWAP (vwap_day) as a critical level.

Buy: SL below vwap_day.

Sell: SL above vwap_day.

Take Profit (TP)

The TP should maximize profits. You can base it on:

Risk/Reward Ratio: Multiply the SL distance by a factor (e.g., 2 or 3).

Buy: TP = Entry Price + (SL Distance * 2).

Sell: TP = Entry Price - (SL Distance * 2).

Key Zones: Target the next resistance (for buys) or support (for sells).

Buy: TP at the next ob_highs, fvg_highs, or liq_zone_high.

Sell: TP at the next ob_lows, fvg_lows, or liq_zone_low.

Ichimoku: Use the cloud levels (Senkou Span A/B) as targets.

Buy: TP at senkou_span_a or senkou_span_b (whichever is higher).

Sell: TP at senkou_span_a or senkou_span_b (whichever is lower).

3. Practical Implementation

Since the script does not automatically draw SL/TP, you can:

Calculate them manually: Observe the chart and use the levels mentioned.

Modify the code: Add SL/TP as labels (label.new) at the moment of the signal.

Here’s an example of how to modify the code to display SL and TP based on ATR with a 1:2 risk/reward ratio:

Modified Code (Signals Section)

Find the lines where the signals (trade_buy and trade_sell) are generated and add the following:

pinescript

// Calculate SL and TP based on ATR

atr_sl_mult = 1.5 // Multiplier for SL

atr_tp_mult = 3.0 // Multiplier for TP (1:2 ratio)

sl_distance = atr_smooth * atr_sl_mult

tp_distance = atr_smooth * atr_tp_mult

if trade_buy

entry_price = close

sl_price = entry_price - sl_distance

tp_price = entry_price + tp_distance

label.new(bar_index, low, "Buy: " + str.tostring(math.round(bull_conditions, 1)), color=color.green, textcolor=color.white, style=label.style_label_up, size=size.tiny)

label.new(bar_index, sl_price, "SL: " + str.tostring(math.round(sl_price, 2)), color=color.red, textcolor=color.white, style=label.style_label_down, size=size.tiny)

label.new(bar_index, tp_price, "TP: " + str.tostring(math.round(tp_price, 2)), color=color.blue, textcolor=color.white, style=label.style_label_up, size=size.tiny)

if trade_sell

entry_price = close

sl_price = entry_price + sl_distance

tp_price = entry_price - tp_distance

label.new(bar_index, high, "Sell: " + str.tostring(math.round(bear_conditions, 1)), color=color.red, textcolor=color.white, style=label.style_label_down, size=size.tiny)

label.new(bar_index, sl_price, "SL: " + str.tostring(math.round(sl_price, 2)), color=color.red, textcolor=color.white, style=label.style_label_up, size=size.tiny)

label.new(bar_index, tp_price, "TP: " + str.tostring(math.round(tp_price, 2)), color=color.blue, textcolor=color.white, style=label.style_label_down, size=size.tiny)

Code Explanation

SL: Calculated by subtracting/adding sl_distance to the entry price (close) depending on whether it’s a buy or sell.

TP: Calculated with a double distance (tp_distance) for a 1:2 risk/reward ratio.

Visualization: Labels are added to the chart to display SL (red) and TP (blue).

4. Practical Strategy Without Modifying the Code

If you don’t want to modify the script, follow these steps manually:

Entry: Take the trade_buy or trade_sell signal.

SL: Check the smoothed ATR (atr_smooth) on the chart or calculate a fixed level (e.g., 1.5 times the ATR). Also, review nearby key zones (OB, FVG, VWAP).

TP: Define a target based on the next key zone or multiply the SL distance by 2 or 3.

Example:

Buy at 100, ATR = 2.

SL = 100 - (2 * 1.5) = 97.

TP = 100 + (2 * 3) = 106.

5. Recommendations

Test in Demo: Apply this logic in a demo account to adjust the multipliers (atr_sl_mult, atr_tp_mult) based on the market (forex or crypto).

Combine with Zones: If the ATR-based SL is too wide, use the nearest OB or FVG as a reference.

Risk/Reward Ratio: Adjust the TP based on your tolerance (1:1, 1:2, 1:3)

Deviation ChannelsIndicator Name: Deviation Channels (Dev Chan)

Why Use This Indicator?

Visualize Volatility Ranges:

The indicator plots Keltner Channels at four levels above and below an average line, letting you easily see how far price has deviated from a typical range. Each “dev” line highlights potential support or resistance during pullbacks or surges.

Color-Coded Clarity:

Each band shifts color intensity depending on whether the current price is trading above or below it, letting you spot breakouts and rejections at a glance. Meanwhile, the Fast SMA (default 10) also changes color – green if price is above, red if below – adding a quick momentum read.

Adjustable Source & Length:

Choose your input source (open, close, ohlc4, or hlc3) and set your Keltner length to suit different asset classes or timeframes. Whether you want a tighter, more reactive channel or a smoother, longer-term reading, the script adapts with minimal effort.

A Simple Trading Approach

Identify Trend with Fast SMA:

If the Fast SMA (default length 10) is green (price above it), treat that as a bullish environment. If it’s red (price below), favor bearish or neutral stances.

Wait for Price to Reach Lower/Upper Deviations:

In a bullish setup (Fast SMA green), watch for price to dip into one of the lower channels (e.g., -1 Dev or -2 Dev). Such pullbacks can become potential “buy the dip” zones if price stabilizes and resumes upward momentum.

Conversely, if the Fast SMA is red, watch for price to test the upper channels (1 Dev or 2 Dev). That might be a short opportunity or a place to close out any remaining longs before a deeper correction.

Manage Risk with Channel Levels:

Place stop-losses just beyond the next “dev” band to protect against volatility. For example, if you enter on a bounce at -1 Dev, consider placing a stop near -2 Dev or -3 Dev, depending on your risk tolerance.

Take Profits Gradually:

In an uptrend, you might scale out of positions as price moves toward higher lines (e.g., 1 Dev or 2 Dev). Conversely, if price fails to hold above the Fast SMA or repeatedly closes below a key band, it might be time to exit.

Disclaimer: No single indicator is foolproof. Always combine with sound risk management, observe multiple timeframes, and consider fundamental factors before making trading decisions. Experiment with the Keltner length and Fast SMA fastLength to find the sweet spot for your market and time horizon.

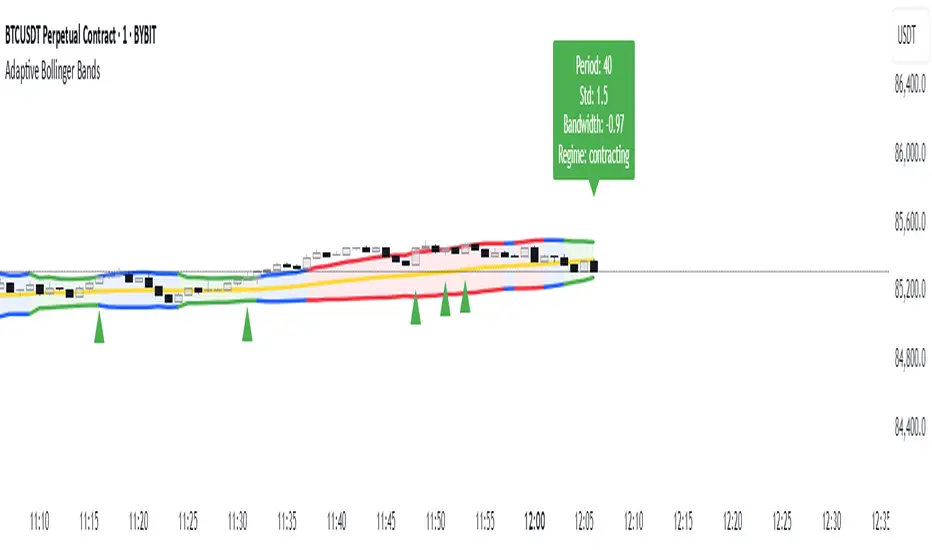

Adaptive Bollinger BandsAdaptive Bollinger Bands

This indicator displays Bollinger Bands with parameters that dynamically adjust based on market volatility. Unlike standard Bollinger Bands with fixed parameters, this version adaptively modifies both the period and standard deviation multiplier in real-time based on measured market conditions.

Key Features

Dynamic adjustment of period and standard deviation based on normalized volatility

Color-coded visualization of current volatility regime (expanding, normal, contracting)

Integration with Keltner Channels for band refinement

Bandwidth analysis for volatility regime identification

Optional on-chart parameter labels showing current settings

Band cross alerts and visual markers

Volatility Visualization

The indicator uses color-coding to display different volatility regimes:

Red: Expanding volatility regime (higher measured volatility)

Blue: Normal volatility regime (average measurements)

Green: Contracting volatility regime (lower measured volatility)

Technical Information

The indicator calculates volatility by analyzing price returns over a configurable lookback period (default 50 bars). The standard deviation of returns is normalized against historical extremes to create an adaptive scaling factor.

Band adaptation occurs through two primary mechanisms:

1. Period adjustment: Higher volatility uses shorter periods (more responsive), while lower volatility uses longer periods (more stable)

2. Standard deviation multiplier adjustment: Higher volatility increases the multiplier (wider bands), while lower volatility decreases it (tighter bands)

The middle band uses a simple moving average with the adaptive period. Additional refinement occurs through Keltner Channel integration, which can tighten bands when contained within Keltner boundaries.

Volatility regimes are determined by analyzing Bollinger Bandwidth relative to its recent history, providing contextual information about the current market state.

Settings Customization

The indicator provides extensive customization options:

- Base parameters (period and standard deviation)

- Adaptive range limits (min/max period and standard deviation)

- Keltner Channel parameters for band refinement

- Bandwidth analysis settings

- Display options for visual elements

Limitations and Considerations

All technical indicators have inherent limitations and should not be used in isolation

Past performance does not guarantee future results

The indicator requires sufficient historical data for proper volatility normalization

Smaller timeframes may produce more noise in the adaptive calculations

Parameters may require adjustment for different markets and trading styles

Band crosses are not trading signals on their own and should be evaluated with other factors

This indicator is designed to provide objective information about market volatility conditions and potential support/resistance zones. Always combine with other analysis methods within a comprehensive trading approach.

FlexATRFlexATR: A Dynamic Multi-Timeframe Trading Strategy

Overview: FlexATR is a versatile trading strategy that dynamically adapts its key parameters based on the timeframe being used. It combines technical signals from exponential moving averages (EMAs) and the Relative Strength Index (RSI) with volatility-based risk management via the Average True Range (ATR). This approach helps filter out false signals while adjusting to varying market conditions — whether you’re trading on a daily chart, intraday charts (30m, 60m, or 5m), or even on higher timeframes like the 4-hour or weekly charts.

How It Works:

Multi-Timeframe Parameter Adaptation: FlexATR is designed to automatically adjust its indicator settings depending on the timeframe:

Daily and Weekly: On higher timeframes, the strategy uses longer periods for the fast and slow EMAs and standard periods for RSI and ATR to capture more meaningful trend confirmations while minimizing noise.

Intraday (e.g., 30m, 60m, 5m, 4h): The parameters are converted from “days” into the corresponding number of bars. For instance, on a 30-minute chart, a “day” might equal 48 bars. The preset values for a 30-minute chart have been slightly reduced (e.g., a fast EMA is set at 0.35 days instead of 0.4) to improve reactivity while maintaining robust filtering.

Signal Generation:

Entry Signals: The strategy enters long positions when the fast EMA crosses above the slow EMA and the RSI is above 50, and it enters short positions when the fast EMA crosses below the slow EMA with the RSI below 50. This dual confirmation helps ensure that signals are reliable.

Risk Management: The ATR is used to compute dynamic levels for stop loss and profit target:

Stop Loss: For a long position, the stop loss is placed at Price - (ATR × Stop Loss Multiplier). For a short position, it is at Price + (ATR × Stop Loss Multiplier).

Profit Target: The profit target is similarly set using the ATR multiplied by a designated profit multiplier.

Dynamic Trailing Stop: FlexATR further incorporates a dynamic trailing stop (if enabled) that adjusts according to the ATR. This trailing stop follows favorable price movements at a distance defined by a multiplier, locking in gains as the trend develops. The use of a trailing stop helps protect profits without requiring a fixed exit point.

Capital Allocation: Each trade is sized at 10% of the total equity. This percentage-based position sizing allows the strategy to scale with your account size. While the current setup assumes no leverage (a 1:1 exposure), the inherent design of the strategy means you can adjust the leverage externally if desired, with risk metrics scaling accordingly.

Visual Representation: For clarity and accessibility (especially for those with color vision deficiencies), FlexATR employs a color-blind friendly palette (the Okabe-Ito palette):

EMA Fast: Displayed in blue.

EMA Slow: Displayed in orange.

Stop Loss Levels: Rendered in vermilion.

Profit Target Levels: Shown in a distinct azzurro (light blue).

Benefits and Considerations:

Reliability: By requiring both EMA crossovers and an RSI confirmation, FlexATR filters out a significant amount of market noise, which reduces false signals at the expense of some delayed entries.

Adaptability: The automatic conversion of “day-based” parameters into bar counts for intraday charts means the strategy remains consistent across different timeframes.

Risk Management: Using the ATR for both fixed and trailing stops allows the strategy to adapt to changing market volatility, helping to protect your capital.

Flexibility: The strategy’s inputs are customizable via the input panel, allowing traders to fine-tune the parameters for different assets or market conditions.

Conclusion: FlexATR is designed as a balanced, adaptive strategy that emphasizes reliability and robust risk management across a variety of timeframes. While it may sometimes enter trades slightly later due to its filtering mechanism, its focus on confirming trends helps reduce the likelihood of false signals. This makes it particularly attractive for traders who prioritize a disciplined, multi-timeframe approach to capturing market trends.

Elastic Volume-Weighted Student-T TensionOverview

The Elastic Volume-Weighted Student-T Tension Bands indicator dynamically adapts to market conditions using an advanced statistical model based on the Student-T distribution. Unlike traditional Bollinger Bands or Keltner Channels, this indicator leverages elastic volume-weighted averaging to compute real-time dispersion and location parameters, making it highly responsive to volatility changes while maintaining robustness against price fluctuations.

This methodology is inspired by incremental calculation techniques for weighted mean and variance, as outlined in the paper by Tony Finch:

📄 "Incremental Calculation of Weighted Mean and Variance" .

Key Features

✅ Adaptive Volatility Estimation – Uses an exponentially weighted Student-T model to dynamically adjust band width.

✅ Volume-Weighted Mean & Dispersion – Incorporates real-time volume weighting, ensuring a more accurate representation of market sentiment.

✅ High-Timeframe Volume Normalization – Provides an option to smooth volume impact by referencing a higher timeframe’s cumulative volume, reducing noise from high-variability bars.

✅ Customizable Tension Parameters – Configurable standard deviation multipliers (σ) allow for fine-tuned volatility sensitivity.

✅ %B-Like Oscillator for Relative Price Positioning – The main indicator is in form of a dedicated oscillator pane that normalizes price position within the sigma ranges, helping identify overbought/oversold conditions and potential momentum shifts.

✅ Robust Statistical Foundation – Utilizes kurtosis-based degree-of-freedom estimation, enhancing responsiveness across different market conditions.

How It Works

Volume-Weighted Elastic Mean (eμ) – Computes a dynamic mean price using an elastic weighted moving average approach, influenced by trade volume, if not volume detected in series, study takes true range as replacement.

Dispersion (eσ) via Student-T Distribution – Instead of assuming a fixed normal distribution, the bands adapt to heavy-tailed distributions using kurtosis-driven degrees of freedom.

Incremental Calculation of Variance – The indicator applies Tony Finch’s incremental method for computing weighted variance instead of arithmetic sum's of fixed bar window or arrays, improving efficiency and numerical stability.

Tension Calculation – There are 2 dispersion custom "zones" that are computed based on the weighted mean and dynamically adjusted standard student-t deviation.

%B-Like Oscillator Calculation – The oscillator normalizes the price within the band structure, with values between 0 and 1:

* 0.00 → Price is at the lower band (-2σ).

* 0.50 → Price is at the volume-weighted mean (eμ).

* 1.00 → Price is at the upper band (+2σ).

* Readings above 1.00 or below 0.00 suggest extreme movements or possible breakouts.

Recommended Usage

For scalping in lower timeframes, it is recommended to use the fixed α Decay Factor, it is in raw format for better control, but you can easily make a like of transformation to N-bar size window like in EMA-1 bar dividing 2 / decayFactor or like an RMA dividing 1 / decayFactor.

The HTF selector catch quite well Higher Time Frame analysis, for example using a Daily chart and using as HTF the 200-day timeframe, weekly or monthly.

Suitable for trend confirmation, breakout detection, and mean reversion plays.

The %B-like oscillator helps gauge momentum strength and detect divergences in price action if user prefer a clean chart without bands, this thanks to pineScript v6 force overlay feature.

Ideal for markets with volume-driven momentum shifts (e.g., futures, forex, crypto).

Customization Parameters

Fixed α Decay Factor – Controls the rate of volume weighting influence for an approximation EWMA approach instead of using sum of series or arrays, making the code lightweight & computing fast O(1).

HTF Volume Smoothing – Instead of a fixed denominator for computing α , a volume sum of the last 2 higher timeframe closed candles are used as denominator for our α weight factor. This is useful to review mayor trends like in daily, weekly, monthly.

Tension Multipliers (±σ) – Adjusts sensitivity to dispersion sigma parameter (volatility).

Oscillator Zone Fills – Visual cues for price positioning within the cloud range.

Posible Interpretations

As market within indicators relay on each individual edge, this are just some key ideas to glimpse how the indicator could be interpreted by the user:

📌 Price inside bands – Market is considered somehow "stable"; price is like resting from tension or "charging batteries" for volume spike moves.

📌 Price breaking outer bands – Potential breakout or extreme movement; watch for reversals or continuation from strong moves. Market is already in tension or generating it.

📌 Narrowing Bands – Decreasing volatility; expect contraction before expansion.

📌 Widening Bands – Increased volatility; prepare for high probability pull-back moves, specially to the center location of the bands (the mean) or the other side of them.

📌 Oscillator is just the interpretation of the price normalized across the Student-T distribution fitting "curve" using the location parameter, our Elastic Volume weighted mean (eμ) fixed at 0.5 value.

Final Thoughts

The Elastic Volume-Weighted Student-T Tension indicator provides a powerful, volume-sensitive alternative to traditional volatility bands. By integrating real-time volume analysis with an adaptive statistical model, incremental variance computation, in a relative price oscillator that can be overlayed in the chart as bands, it offers traders an edge in identifying momentum shifts, trend strength, and breakout potential. Think of the distribution as a relative "tension" rubber band in which price never leave so far alone.

DISCLAIMER:

The Following indicator/code IS NOT intended to be a formal investment advice or recommendation by the author, nor should be construed as such. Users will be fully responsible by their use regarding their own trading vehicles/assets.

The following indicator was made for NON LUCRATIVE ACTIVITIES and must remain as is, following TradingView's regulations. Use of indicator and their code are published for work and knowledge sharing. All access granted over it, their use, copy or re-use should mention authorship(s) and origin(s).

WARNING NOTICE!

THE INCLUDED FUNCTION MUST BE CONSIDERED FOR TESTING. The models included in the indicator have been taken from open sources on the web and some of them has been modified by the author, problems could occur at diverse data sceneries, compiler version, or any other externality.

ETH/USDT EMA Crossover Strategy - OptimizedStrategy Name: EMA Crossover Strategy for ETH/USDT

Description:

This trading strategy is designed for the ETH/USDT pair and is based on exponential moving average (EMA) crossovers combined with momentum and volatility indicators. The strategy uses multiple filters to identify high-probability signals in both bullish and bearish trends, making it suitable for traders looking to trade in trending markets.

Strategy Components

EMAs (Exponential Moving Averages):

EMA 200: Used to identify the primary trend. If the price is above the EMA 200, it is considered a bullish trend; if below, a bearish trend.

EMA 50: Acts as an additional filter to confirm the trend.

EMA 20 and EMA 50 Short: These short-term EMAs generate entry signals through crossovers. A bullish crossover (EMA 20 crosses above EMA 50 Short) is a buy signal, while a bearish crossover (EMA 20 crosses below EMA 50 Short) is a sell signal.

RSI (Relative Strength Index):

The RSI is used to avoid overbought or oversold conditions. Long trades are only taken when the RSI is above 30, and short trades when the RSI is below 70.

ATR (Average True Range):

The ATR is used as a volatility filter. Trades are only taken when there is sufficient volatility, helping to avoid false signals in quiet markets.

Volume:

A volume filter is used to confirm sufficient market participation in the price movement. Trades are only taken when volume is above average.

Strategy Logic

Long Trades:

The price must be above the EMA 200 (bullish trend).

The EMA 20 must cross above the EMA 50 Short.

The RSI must be above 30.

The ATR must indicate sufficient volatility.

Volume must be above average.

Short Trades:

The price must be below the EMA 200 (bearish trend).

The EMA 20 must cross below the EMA 50 Short.

The RSI must be below 70.

The ATR must indicate sufficient volatility.

Volume must be above average.

How to Use the Strategy

Setup:

Add the script to your ETH/USDT chart on TradingView.

Adjust the parameters according to your preferences (e.g., EMA periods, RSI, ATR, etc.).

Signals:

Buy and sell signals will be displayed directly on the chart.

Long trades are indicated with an upward arrow, and short trades with a downward arrow.

Risk Management:

Use stop-loss and take-profit orders in all trades.

Consider a risk-reward ratio of at least 1:2.

Backtesting:

Test the strategy on historical data to evaluate its performance before using it live.

Advantages of the Strategy

Trend-focused: The strategy is designed to trade in trending markets, increasing the probability of success.

Multiple filters: The use of RSI, ATR, and volume reduces false signals.

Adaptability: It can be adjusted for different timeframes, although it is recommended to test it on 5-minute and 15-minute charts for ETH/USDT.

Warnings

Sideways markets: The strategy may generate false signals in markets without a clear trend. It is recommended to avoid trading in such conditions.

Optimization: Make sure to optimize the parameters according to the market and timeframe you are using.

Risk management: Never trade without stop-loss and take-profit orders.

Author

Jose J. Sanchez Cuevas

Version

v1.0

MLB Momentum IndicatorMLB Momentum Indicator is a no‐lookahead technical indicator designed to signal intraday trend shifts and potential reversal points. It combines several well‐known technical components—Moving Averages, MACD, RSI, and optional ADX & Volume filters—to deliver high‐probability buy/sell signals on your chart.

Below is an overview of how it works and what each part does:

1. Moving Average Trend Filter

The script uses two moving averages (fast and slow) to determine the primary trend:

isUpTrend if Fast MA > Slow MA

isDownTrend if Fast MA < Slow MA

You can select the MA method—SMA, EMA, or WMA—and customize lengths.

Why it matters: The indicator only gives bullish signals if the trend is up, and bearish signals if the trend is down, helping avoid trades that go against the bigger flow.

2. MACD Confirmation (Momentum)

Uses MACD (with user‐defined Fast, Slow, and Signal lengths) to check momentum:

macdBuySignal if the MACD line crosses above its signal line (bullish)

macdSellSignal if the MACD line crosses below its signal line (bearish)

Why it matters: MACD crossovers confirm an emerging momentum shift, aligning signals with actual price acceleration rather than random fluctuation.

3. RSI Overbought/Oversold Filter

RSI (Relative Strength Index) is calculated with a chosen length, plus Overbought & Oversold thresholds:

For long signals: the RSI must be below the Overbought threshold (e.g. 70).

For short signals: the RSI must be above the Oversold threshold (e.g. 30).

Why it matters: Prevents buying when price is already overbought or shorting when price is too oversold, filtering out possible poor‐risk trades.

4. Optional ADX Filter (Trend Strength)

If enabled, ADX must exceed a chosen threshold (e.g., 20) for a signal to be valid:

This ensures you’re only taking trades in markets that have sufficient directional momentum.

Why it matters: It weeds out choppy, sideways conditions where signals are unreliable.

5. Optional Volume Filter (High‐Participation Moves)

If enabled, the indicator checks whether current volume is above a certain multiple of its moving average (e.g., 1.5× average volume).

Why it matters: High volume often indicates stronger institutional interest, validating potential breakouts or reversals.

6. ATR & Chandelier (Visual Reference)

For reference only, the script can display ATR‐based stop levels or a Chandelier Exit line:

ATR (Average True Range) helps gauge volatility and can inform stop‐loss distances.

Chandelier Exit is a trailing stop technique that adjusts automatically as price moves.

Why it matters: Though this version of the script doesn’t execute trades, these lines help you see how far to place stops or how to ride a trend.

7. Final Bullish / Bearish Signal

When all conditions (trend, MACD, RSI, optional ADX, optional Volume) line up for a long, a green “Long” arrow appears.

When all conditions line up for a short, a red “Short” arrow appears.

Why it matters: You get a clear, on‐chart signal for each potential entry, rather than needing to check multiple indicators manually.

8. Session & Date Filtering

The script allows choosing a start/end date and an optional session window (e.g. 09:30–16:00).

Why it matters: Helps limit signals to a specific historical backtest range or trading hours, which can be crucial for day traders (e.g., stock market hours only).

Putting It All Together

Primary Trend → ensures you trade in line with the bigger direction.

MACD & RSI → confirm momentum and avoid overbought/oversold extremes.

ADX & Volume → optional filters for strong trend strength & genuine interest.

Arrows → each potential buy (Long) or sell (Short) signal is clearly shown on your chart.

Use Cases

5‐Minute Scalping: Shorter RSI/MACD lengths to catch small, frequent intraday moves.

Swing Trading: Larger MAs, bigger RSI thresholds, and using ADX to filter only major trends.

Cautious Approach: Enable volume & ADX filters to reduce false signals in choppy markets.

Benefits & Limitations

Benefits:

Consolidates multiple indicators into one overlay.

Clear buy/sell signals with optional dynamic volatility references.

Flexible user inputs adapt to different trading styles/timeframes.

Limitations:

Like all technical indicators, it can produce false signals in sideways or news‐driven markets.

Success depends heavily on user settings and the particular market’s behavior.

Summary

The MLB Momentum Indicator combines a trend filter (MAs), momentum check (MACD), overbought/oversold gating (RSI), and optional ADX/Volume filters to create clear buy/sell arrows on your chart. This approach encourages trading in sync with both trend and momentum, and helps avoid suboptimal entries when volume or trend strength is lacking. It can be tailored to scalp micro‐moves on lower timeframes or used for higher‐timeframe swing trading by adjusting the input settings.

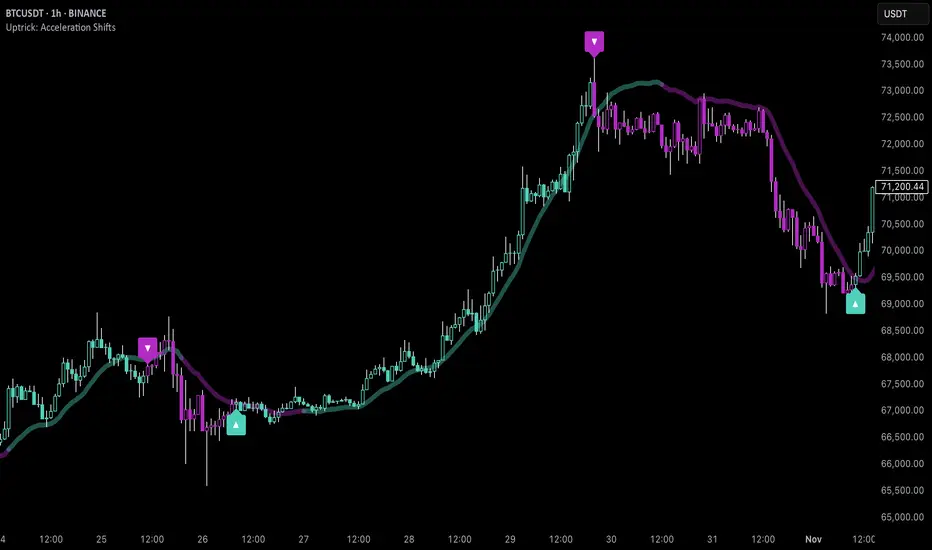

Uptrick: Acceleration ShiftsIntroduction

Uptrick: Acceleration Shifts is designed to measure and visualize price momentum shifts by focusing on acceleration —the rate of change in velocity over time. It uses various moving average techniques as a trend filter, providing traders with a clearer perspective on market direction and potential trade entries or exits.

Purpose

The main goal of this indicator is to spot strong momentum changes (accelerations) and confirm them with a chosen trend filter. It attempts to distinguish genuine market moves from noise, helping traders make more informed decisions. The script can also trigger multiple entries (smart pyramiding) within the same trend, if desired.

Overview

By measuring how quickly price velocity changes (acceleration) and comparing it against a smoothed average of itself, this script generates buy or sell signals once the acceleration surpasses a given threshold. A trend filter is added for further validation. Users can choose from multiple smoothing methods and color schemes, and they can optionally enable a small table that displays real-time acceleration values.

Originality and Uniqueness

This script offers an acceleration-based approach, backed by several different moving average choices. The blend of acceleration thresholds, a trend filter, and an optional extra-entry (pyramiding) feature provides a flexible toolkit for various trading styles. The inclusion of multiple color themes and a slope-based coloring of the trend line adds clarity and user customization.

Inputs & Features

1. Acceleration Length (length)

This input determines the number of bars used when calculating velocity. Specifically, the script computes velocity by taking the difference in closing prices over length bars, and then calculates acceleration based on how that velocity changes over an additional length. The default is 14.

2. Trend Filter Length (smoothing)

This sets the lookback period for the chosen trend filter method. The default of 50 results in a moderately smooth trend line. A higher smoothing value will create a slower-moving trend filter.

3. Acceleration Threshold (threshold)

This multiplier determines when acceleration is considered strong enough to trigger a main buy or sell signal. A default value of 2.5 means the current acceleration must exceed 2.5 times the average acceleration before signaling.

4. Smart Pyramiding Strength (pyramidingThreshold)

This lower threshold is used for additional (pyramiding) entries once the main trend has already been identified. For instance, if set to 0.5, the script looks for acceleration crossing ±0.5 times its average acceleration to add extra positions.

5. Max Pyramiding Entries (maxPyramidingEntries)

This sets a limit on how many extra positions can be opened (beyond the first main signal) in a single directional trend. The default of 3 ensures traders do not become overexposed.

6. Show Acceleration Table (showTable)

When enabled, a small table displaying the current acceleration and its average is added to the top-right corner of the chart. This table helps monitor real-time momentum changes.

7. Smart Pyramiding (enablePyramiding)

This toggle decides whether additional entries (buy or sell) will be generated once a main signal is active. If enabled, these extra signals act as filtered entries, only firing when acceleration re-crosses a smaller threshold (pyramidingThreshold). These signals have a '+' next to their signal on the label.

8. Select Color Scheme (selectedColorScheme)

Allows choosing between various pre-coded color themes, such as Default, Emerald, Sapphire, Golden Blaze, Mystic, Monochrome, Pastel, Vibrant, Earth, or Neon. Each theme applies a distinct pair of colors for bullish and bearish conditions.

9. Trend Filter (TrendFilter)

Lets the user pick one of several moving average approaches to determine the prevailing trend. The options include:

Short Term (TEMA)

EWMA

Medium Term (HMA)

Classic (SMA)

Quick Reaction (DEMA)

Each method behaves differently, balancing reactivity and smoothness.

10. Slope Lookback (slopeOffset)

Used to measure the slope of the trend filter over a set number of bars (default is 10). This slope then influences the coloring of the trend filter line, indicating bullish or bearish tilt.

Note: The script refers to this as the "Massive Slope Index," but it effectively serves as a Trend Slope Calculation, measuring how the chosen trend filter changes over a specified period.

11. Alerts for Buy/Sell and Pyramiding Signals

The script includes built-in alert conditions that can be enabled or configured. These alerts trigger whenever the script detects a main Buy or Sell signal, as well as extra (pyramiding) signals if Smart Pyramiding is active. This feature allows traders to receive immediate notifications or automate a trading response.

Calculation Methodology

1. Velocity and Acceleration

Velocity is derived by subtracting the closing price from its value length bars ago. Acceleration is the difference in velocity over an additional length period. This highlights how quickly momentum is shifting.

2. Average Acceleration

The script smooths raw acceleration with a simple moving average (SMA) using the smoothing input. Comparing current acceleration against this average provides a threshold-based signal mechanism.

3. Trend Filter

Users can pick one of five moving average types to form a trend baseline. These range from quick-reacting methods (DEMA, TEMA) to smoother options (SMA, HMA, EWMA). The script checks whether the price is above or below this filter to confirm trend direction.

4. Buy/Sell Logic

A buy occurs when acceleration surpasses avgAcceleration * threshold and price closes above the trend filter. A sell occurs under the opposite conditions. An additional overbought/oversold check (based on a longer SMA) refines these signals further.

When price is considered oversold (i.e., close is below a longer-term SMA), a bullish acceleration signal has a higher likelihood of success because it indicates that the market is attempting to reverse from a lower price region. Conversely, when price is considered overbought (close is above this longer-term SMA), a bearish acceleration signal is more likely to be valid. This helps reduce false signals by waiting until the market is extended enough that a reversal or continuation has a stronger chance of following through.

5. Smart Pyramiding

Once a main buy or sell signal is triggered, additional (filtered) entries can be taken if acceleration crosses a smaller multiplier (pyramidingThreshold). This helps traders scale into strong moves. The script enforces a cap (maxPyramidingEntries) to limit risk.

6. Visual Elements

Candles can be recolored based on the active signal. Labels appear on the chart whenever a main or pyramiding entry signal is triggered. An optional table can show real-time acceleration values.

Color Schemes

The script includes a variety of predefined color themes. For bullish conditions, it might use turquoise or green, and for bearish conditions, magenta or red—depending on which color scheme the user selects. Each scheme aims to provide clear visual differentiation between bullish and bearish market states.

Why Each Indicator Was Part of This Component

Acceleration is employed to detect swift changes in momentum, capturing shifts that may not yet appear in more traditional measures. To further adapt to different trading styles and market conditions, several moving average methods are incorporated:

• TEMA (Triple Exponential Moving Average) is chosen for its ability to reduce lag more effectively than a standard EMA while still reacting swiftly to price changes. Its construction layers exponential smoothing in a way that can highlight sudden momentum shifts without sacrificing too much smoothness.

• DEMA (Double Exponential Moving Average) provides a faster response than a single EMA by using two layers of exponential smoothing. It is slightly less smoothed than TEMA but can alert traders to momentum changes earlier, though with a higher risk of noise in choppier markets.

• HMA (Hull Moving Average) is known for its balance of smoothness and reduced lag. Its weighted calculations help track trend direction clearly, making it useful for traders who want a smoother line that still reacts fairly quickly.

• SMA (Simple Moving Average) is the classic baseline for smoothing price data. It offers a clear, stable perspective on long-term trends, though it reacts more slowly than other methods. Its simplicity can be beneficial in lower-volatility or more stable market environments.

• EWMA (Exponentially Weighted Moving Average) provides a middle ground by emphasizing recent price data while still retaining some degree of smoothing. It typically responds faster than an SMA but is less aggressive than DEMA or TEMA.

Alongside these moving average techniques, the script employs a slope calculation (referred to as the “Massive Slope Index”) to visually indicate whether the chosen filter is sloping upward or downward. This adds an extra layer of clarity to directional analysis. The indicator also uses overbought/oversold checks, based on a longer-term SMA, to help filter out signals in overstretched markets—reducing the likelihood of false entries in conditions where the price is already extensively extended.

Additional Features

Alerts can be set up for both main signals and additional pyramiding signals, which is helpful for automated or semi-automated trading. The optional acceleration table offers quick reference values, making momentum monitoring more intuitive. Including explicit alert conditions for Buy/Sell and Pyramiding ensures traders can respond promptly to market movements or integrate these triggers into automated strategies.

Summary

This script serves as a comprehensive momentum-based trading framework, leveraging acceleration metrics and multiple moving average filters to identify potential shifts in market direction. By combining overbought/oversold checks with threshold-based triggers, it aims to reduce the noise that commonly plagues purely reactive indicators. The flexibility of Smart Pyramiding, customizable color schemes, and built-in alerts allows users to tailor their experience and respond swiftly to valid signals, potentially enhancing trading decisions across various market conditions.

Disclaimer

All trading involves significant risk, and users should apply their own judgment, risk management, and broader analysis before making investment decisions.

Volume Predictor [PhenLabs]📊 Volume Predictor

Version: PineScript™ v6

📌 Description

The Volume Predictor is an advanced technical indicator that leverages machine learning and statistical modeling techniques to forecast future trading volume. This innovative tool analyzes historical volume patterns to predict volume levels for upcoming bars, providing traders with valuable insights into potential market activity. By combining multiple prediction algorithms with pattern recognition techniques, the indicator delivers forward-looking volume projections that can enhance trading strategies and market analysis.

🚀 Points of Innovation:

Machine learning pattern recognition using Lorentzian distance metrics

Multi-algorithm prediction framework with algorithm selection

Ensemble learning approach combining multiple prediction methods

Real-time accuracy metrics with visual performance dashboard

Dynamic volume normalization for consistent scale representation

Forward-looking visualization with configurable prediction horizon

🔧 Core Components

Pattern Recognition Engine : Identifies similar historical volume patterns using Lorentzian distance metrics

Multi-Algorithm Framework : Offers five distinct prediction methods with configurable parameters

Volume Normalization : Converts raw volume to percentage scale for consistent analysis

Accuracy Tracking : Continuously evaluates prediction performance against actual outcomes

Advanced Visualization : Displays actual vs. predicted volume with configurable future bar projections

Interactive Dashboard : Shows real-time performance metrics and prediction accuracy

🔥 Key Features

The indicator provides comprehensive volume analysis through:

Multiple Prediction Methods : Choose from Lorentzian, KNN Pattern, Ensemble, EMA, or Linear Regression algorithms

Pattern Matching : Identifies similar historical volume patterns to project future volume

Adaptive Predictions : Generates volume forecasts for multiple bars into the future

Performance Tracking : Calculates and displays real-time prediction accuracy metrics

Normalized Scale : Presents volume as a percentage of historical maximums for consistent analysis

Customizable Visualization : Configure how predictions and actual volumes are displayed

Interactive Dashboard : View algorithm performance metrics in a customizable information panel

🎨 Visualization

Actual Volume Columns : Color-coded green/red bars showing current normalized volume

Prediction Columns : Semi-transparent blue columns representing predicted volume levels

Future Bar Projections : Forward-looking volume predictions with configurable transparency

Prediction Dots : Optional white dots highlighting future prediction points

Reference Lines : Visual guides showing the normalized volume scale

Performance Dashboard : Customizable panel displaying prediction method and accuracy metrics

📖 Usage Guidelines

History Lookback Period

Default: 20

Range: 5-100

This setting determines how many historical bars are analyzed for pattern matching. A longer period provides more historical data for pattern recognition but may reduce responsiveness to recent changes. A shorter period emphasizes recent market behavior but might miss longer-term patterns.

🧠 Prediction Method

Algorithm

Default: Lorentzian

Options: Lorentzian, KNN Pattern, Ensemble, EMA, Linear Regression

Selects the algorithm used for volume prediction:

Lorentzian: Uses Lorentzian distance metrics for pattern recognition, offering excellent noise resistance

KNN Pattern: Traditional K-Nearest Neighbors approach for historical pattern matching

Ensemble: Combines multiple methods with weighted averaging for robust predictions

EMA: Simple exponential moving average projection for trend-following predictions

Linear Regression: Projects future values based on linear trend analysis

Pattern Length

Default: 5

Range: 3-10

Defines the number of bars in each pattern for machine learning methods. Shorter patterns increase sensitivity to recent changes, while longer patterns may identify more complex structures but require more historical data.

Neighbors Count

Default: 3

Range: 1-5

Sets the K value (number of nearest neighbors) used in KNN and Lorentzian methods. Higher values produce smoother predictions by averaging more historical patterns, while lower values may capture more specific patterns but could be more susceptible to noise.

Prediction Horizon

Default: 5

Range: 1-10

Determines how many future bars to predict. Longer horizons provide more forward-looking information but typically decrease accuracy as the prediction window extends.

📊 Display Settings

Display Mode

Default: Overlay

Options: Overlay, Prediction Only

Controls how volume information is displayed:

Overlay: Shows both actual volume and predictions on the same chart

Prediction Only: Displays only the predictions without actual volume

Show Prediction Dots

Default: false

When enabled, adds white dots to future predictions for improved visibility and clarity.

Future Bar Transparency (%)

Default: 70

Range: 0-90

Controls the transparency of future prediction bars. Higher values make future bars more transparent, while lower values make them more visible.

📱 Dashboard Settings

Show Dashboard

Default: true

Toggles display of the prediction accuracy dashboard. When enabled, shows real-time accuracy metrics.

Dashboard Location

Default: Bottom Right

Options: Top Left, Top Right, Bottom Left, Bottom Right

Determines where the dashboard appears on the chart.

Dashboard Text Size

Default: Normal

Options: Small, Normal, Large

Controls the size of text in the dashboard for various display sizes.

Dashboard Style

Default: Solid

Options: Solid, Transparent

Sets the visual style of the dashboard background.

Understanding Accuracy Metrics

The dashboard provides key performance metrics to evaluate prediction quality:

Average Error

Shows the average difference between predicted and actual values

Positive values indicate the prediction tends to be higher than actual volume

Negative values indicate the prediction tends to be lower than actual volume

Values closer to zero indicate better prediction accuracy

Accuracy Percentage

A measure of how close predictions are to actual outcomes

Higher percentages (>70%) indicate excellent prediction quality

Moderate percentages (50-70%) indicate acceptable predictions

Lower percentages (<50%) suggest weaker prediction reliability

The accuracy metrics are color-coded for quick assessment:

Green: Strong prediction performance

Orange: Moderate prediction performance

Red: Weaker prediction performance

✅ Best Use Cases

Anticipate upcoming volume spikes or drops

Identify potential volume divergences from price action

Plan entries and exits around expected volume changes

Filter trading signals based on predicted volume support

Optimize position sizing by forecasting market participation

Prepare for potential volatility changes signaled by volume predictions

Enhance technical pattern analysis with volume projection context

⚠️ Limitations

Volume predictions become less accurate over longer time horizons

Performance varies based on market conditions and asset characteristics

Works best on liquid assets with consistent volume patterns

Requires sufficient historical data for pattern recognition

Sudden market events can disrupt prediction accuracy

Volume spikes may be muted in predictions due to normalization

💡 What Makes This Unique

Machine Learning Approach : Applies Lorentzian distance metrics for robust pattern matching

Algorithm Selection : Offers multiple prediction methods to suit different market conditions

Real-time Accuracy Tracking : Provides continuous feedback on prediction performance

Forward Projection : Visualizes multiple future bars with configurable display options

Normalized Scale : Presents volume as a percentage of maximum volume for consistent analysis

Interactive Dashboard : Displays key metrics with customizable appearance and placement

🔬 How It Works

The Volume Predictor processes market data through five main steps:

1. Volume Normalization:

Converts raw volume to percentage of maximum volume in lookback period

Creates consistent scale representation across different timeframes and assets

Stores historical normalized volumes for pattern analysis

2. Pattern Detection:

Identifies similar volume patterns in historical data

Uses Lorentzian distance metrics for robust similarity measurement

Determines strength of pattern match for prediction weighting

3. Algorithm Processing:

Applies selected prediction algorithm to historical patterns

For KNN/Lorentzian: Finds K nearest neighbors and calculates weighted prediction

For Ensemble: Combines multiple methods with optimized weighting

For EMA/Linear Regression: Projects trends based on statistical models

4. Accuracy Calculation:

Compares previous predictions to actual outcomes

Calculates average error and prediction accuracy

Updates performance metrics in real-time

5. Visualization:

Displays normalized actual volume with color-coding

Shows current and future volume predictions

Presents performance metrics through interactive dashboard

💡 Note:

The Volume Predictor performs optimally on liquid assets with established volume patterns. It’s most effective when used in conjunction with price action analysis and other technical indicators. The multi-algorithm approach allows adaptation to different market conditions by switching prediction methods. Pay special attention to the accuracy metrics when evaluating prediction reliability, as sudden market changes can temporarily reduce prediction quality. The normalized percentage scale makes the indicator consistent across different assets and timeframes, providing a standardized approach to volume analysis.

Custom Time Alert with Vertical Line📌 Detailed Explanation of the Custom Time Alert with Vertical Line in Pine Script v5

This script is a time-based alert system designed for TradingView. It allows traders to set a specific hour and minute for alerts and provides visual indicators on the chart, including a marker when the alert triggers and a vertical line at the alert time.

🔹 Main Features

Custom Alert Time → Users can specify the exact hour and minute for an alert.

Time Zone Offset Support → Users can manually adjust their local UTC offset to ensure alerts trigger at the correct time.

Real-Time Alert Condition → When the market reaches the set time, an alert notification is triggered.

Chart Visualization → A red marker appears when the alert is activated, and a blue vertical line is drawn at the alert time.

Automated Calculation → The script adjusts the alert time based on the user’s time zone settings.

🛠️ How It Works

User Input for Alert Time

The script allows users to enter their desired alert hour (0-23) and minute (0-59).

This ensures the alert triggers at the exact specified time.

Time Zone Offset Handling

Users enter their UTC offset (e.g., New York is -5, Tokyo is +9).

This ensures alerts work correctly regardless of the user’s location.

Time Calculation

The script adjusts the TradingView time by adding the time zone offset in milliseconds.

This converts the UTC-based TradingView time into the user’s local time.

Checking for a Time Match