High Volatility and Big Price Change ScannerThis Pine Script scans for high volatility and significant price changes on the chart. It uses Average True Range (ATR) to measure volatility and calculates the percentage change in price over a specified lookback period. When both conditions—high volatility (ATR above a threshold) and a significant price change (greater than the set percentage threshold)—are met, a signal is plotted below the bar. Additionally, an alert condition is included for notifications when these conditions are satisfied.

This script is useful for identifying stocks with large price movements and increased volatility, which may indicate potential trading opportunities.

Volatility

VWAP with ADX Buy/Sell Signals and 50 MA BackgroundThis Pine Script combines several technical indicators to create a comprehensive chart with buy and sell signals based on the ADX and VWAP, as well as background color changes depending on the price relative to the 50-period simple moving average (SMA). Here's a breakdown of what each part of the code does:

1. VWAP Settings

Anchor Period: You can select different periods such as "Session", "Week", "Month", etc. to define the anchor period for the VWAP.

Source: The source for VWAP is set to the typical price (hlc3).

Offset: Allows for shifting the VWAP by a specified amount.

2. ADX Settings

ADX Length: The period used to calculate the ADX.

ADX Smoothing: Used to smooth the ADX for better clarity.

ADX Threshold: Used to filter out weak trends (i.e., signals when ADX > 20).

3. ADX and VWAP Calculation

The ADX values are calculated using ta.dmi(), which returns the +DI, -DI, and ADX lines.

VWAP is calculated using ta.vwap(), based on the selected price source.

4. Buy/Sell Conditions

Buy Signal: A buy signal is generated when:

The +DI crosses above the -DI (indicating an uptrend).

The ADX is above 20 (indicating a strong trend).

The closing price is above the VWAP (indicating bullish market sentiment).

Sell Signal: A sell signal occurs when:

The -DI crosses above the +DI (indicating a downtrend).

The ADX is above 20 (indicating a strong trend).

The closing price is below the VWAP (indicating bearish market sentiment).

5. VWAP Bands

The standard deviation of the price is calculated using ta.stdev(), and the bands are plotted at multiples of the standard deviation (1, 2, and 3).

These bands are used to highlight possible overbought or oversold conditions.

6. 50-period SMA and Background Color

The script calculates a 50-period Simple Moving Average (SMA).

The background color is then changed based on whether the price is above or below the 50-period SMA. If the price is above the SMA, the background is green (bullish), and if it’s below, it’s red (bearish).

7. Plots

The script includes plots for the VWAP line, the ADX and DI lines (optional), and the upper and lower bands.

The buy and sell signals are plotted as shapes with text labels ("BUY" and "SELL") that appear below or above the price bars.

Final Notes:

Band Plots: Three levels of bands (green, olive, teal) are plotted using standard deviation multipliers (1, 2, and 3 times the standard deviation).

Background Color: The background color changes depending on whether the price is above or below the 50 SMA, giving a visual cue for bullish or bearish market conditions.

This indicator aims to offer a multi-faceted view of the market with trend-following signals (via ADX), VWAP for intraday support/resistance, and background coloring to indicate the current trend strength based on the 50 SMA.

ATR Impact CandlesATR Impact Candles: Simplify Your Trading with Pure Price Action

You don’t need dozens of cluttered indicators to catch what really matters. With ATR Impact Candles, you get a powerful, single-tool solution that cuts through the noise by focusing on what truly drives the market: price action and volatility. This indicator highlights only those candlesticks that pack a punch—showing you when the market’s range is exceptionally strong relative to its recent behavior. Whether you’re a scalper or a swing trader, ATR Impact Candles empowers you to time your entries and exits with confidence, letting you trade based on real market momentum.

⸻

Indicator Overview

The indicator is designed for TradingView and is implemented in Pine Script (version 5). Its primary purpose is to highlight specific candles that meet a defined volatility condition based on the Average True Range (ATR). Instead of modifying every candle’s appearance, the indicator only changes the color of those “signal” candles that exceed a user-defined multiple of the ATR. The rest of the candles remain in their traditional black and white appearance—preserving the classic candlestick chart look.

⸻

Key Features

1. ATR-Based Signal Identification:

• ATR Calculation:

The indicator calculates the ATR using a configurable lookback period (default is 14 periods). The ATR is a common volatility measure that reflects the average range of price movement.

• Threshold Condition:

A candle is flagged as a signal if its range (high minus low) meets or exceeds a specified multiple (the “ATR Factor”) of the ATR. By default, this factor is set to 2, meaning any candle whose range is at least twice the ATR is considered significant.

2. Dynamic Candle Coloring:

• Signal Candles:

• When a candle meets the ATR threshold condition:

• Up Candles: are colored green.

• Down Candles: are colored red.

• Non-Signal Candles:

• Candles that do not meet the threshold condition retain their classic appearance:

• Up candles are white.

• Down candles are black.

3. User Configurability:

• ATR Period:

Traders can adjust the ATR period to tailor the volatility measure to different markets or timeframes.

• ATR Factor:

The multiple of the ATR that defines a signal candle is also configurable, giving flexibility to experiment with different thresholds for what constitutes “significant” price movement.

• Overlay Display:

The indicator runs in overlay mode on the chart, meaning it directly affects the appearance of the candlestick bars without interfering with other chart elements.

4. Additional Visual Aid:

• Threshold Line Plot:

The script optionally plots a line representing the ATR multiplied by the chosen factor. This line serves as a visual benchmark on the chart, allowing traders to see at what level the ATR threshold lies relative to the price action.

⸻

How It Works

1. ATR Calculation:

The indicator first calculates the Average True Range (ATR) for the defined period. This value is updated for each new candle.

2. Range Comparison:

For each candle, the indicator calculates the range (high - low) and compares it to the threshold, which is the ATR multiplied by the user-defined factor.

3. Conditional Coloring:

• If the Candle’s Range ≥ (ATR * Factor):

• The candle is marked as a “signal candle.”

• Its color is set to green if it is an up candle (close is greater than or equal to open) or red if it is a down candle.

• Otherwise:

• The candle retains its classic look, with up candles in white and down candles in black.

4. Chart Display:

By applying these rules to every candle, the indicator visually emphasizes those moments when the market shows unusually large price movements relative to its recent average volatility. This helps traders quickly spot potential breakouts or reversals.

⸻

Practical Applications

• Volatility Breakouts:

Identify candles that may signal the start of a breakout or strong reversal.

• Risk Management:

Adjust stop-loss levels or position sizes when unusually volatile candles are detected.

• Signal Confirmation:

Combine with other technical indicators or chart patterns to reinforce entry or exit decisions.

⸻

ATR Impact Candles is your essential, no-nonsense tool for filtering out market noise and focusing solely on significant price action. Simplify your trading decisions and harness the power of volatility with one clear, effective indicator.

ROC + SMI Auto Adjust

This indicator combines the Rate of Change (ROC) and the Stochastic Momentum Index (SMI) with automatically adjusted parameters for different time frames (short, medium, long). It normalizes the ROC to match the SMI levels, displays the ROC as a histogram and the SMI as lines, highlights overbought/oversold zones and includes a settings table. Ideal for analyzing momentum on different time frames.

Key Features:

Automatic Parameter Adjustment:

The script detects the current chart time frame (e.g. 1-minute, 1-hour, daily) and adjusts the parameters for the ROC and SMI accordingly.

Parameters such as ROC length, SMI length and smoothing periods are optimized for short, medium and long term time frames.

Rate of Change (ROC):

ROC measures the percentage change in price over a specified period.

The script normalizes the ROC values to match the SMI range, making it easier to compare the two indicators on the same scale.

The ROC is displayed as a histogram, where positive values are colored green and negative values are colored red.

Stochastic Momentum Index (SMI):

SMI is a momentum oscillator that identifies overbought and oversold conditions.

The script calculates the SMI and its signal line, plotting them on the chart.

Overbought and oversold levels are displayed as dotted lines for convenience.

SMI and SMI Signal Crossover:

When the main SMI crosses the signal line from below upwards, it may be a buy signal (bullish signal).

When the SMI crosses the signal line from above downwards, it may be a sell signal (bearish signal).

Configurable Inputs:

Users can use the automatically adjusted settings or manually override the parameters (e.g. ROC length, SMI length, smoothing periods).

Overbought and oversold levels for SMI are also configurable.

Parameter Table:

A table is displayed on the chart showing the current parameters (e.g. timeframe, ROC length, SMI length) for transparency and debugging.

The position of the table is configurable (e.g. top left, bottom right).

How it works:

The script first detects the chart timeframe and classifies it as short-term (e.g. 1M, 5M), medium-term (e.g. 1H, 4H) or long-term (e.g. D1, W1).

Based on the timeframe, it sets default values for the ROC and SMI parameters.

ROC and SMI are calculated and normalized so that they can be compared on the same scale.

ROC is displayed as a histogram, while SMI and its signal line are displayed as lines.

Overbought and oversold levels are displayed as horizontal lines.

Use cases:

Trend identification: ROC helps to identify the strength of the trend, while SMI indicates overbought/oversold conditions.

Momentum analysis: The combination of ROC and SMI provides insight into both price momentum and potential reversals.

Time frame flexibility: The auto-adjustment feature makes the script suitable for scalping (short-term), swing trading (medium-term) and long-term investing.

Liquidity Zones [ActiveQuants]The Liquidity Zones indicator detects price areas where high trading volume coincides with below-average volatility , critical zones where large players often accumulate or distribute positions. Ideal for spotting potential reversal points and strategic liquidity pools.

Core Detection Formula

Liquidity Zone = (Volume > SMA(Volume, Length) × Multiplier) AND (Short-Term Volatility < 0.5 × Average Volatility)

Volume Surge Detection

Compares current volume to its SMA (user-defined length).

Multiplies threshold with " Volume Threshold Multiplier " parameter.

Volatility Contraction Filter

Calculates 5-bar volatility (standard deviation of closes).

Compares to average volatility over " Price Std. Dev. Length " period.

Requires short-term volatility < 50% of average.

█ KEY FEATURES

Merging Consecutive Zones

If the " Merge Consecutive Zones " option is enabled, the indicator will:

Calculate the number of consecutive bars that meet the liquidity zone criteria.

Sum the volume of these consecutive bars.

Display only the most recent label for the merged zone (previous labels in the sequence are removed).

Displays volume in either

Raw units (" Units ").

Dollar-equivalent (" Currency Value ") using closing price.

Alerts

An alert condition is built into the script. Traders can selectively enable alerts via TradingView’s alert system. Whenever a liquidity zone is detected, an alert is triggered with the message: " High-volume and low-volatility zone detected! ".

█ USER INPUTS

- Liquidity Zones Color

Sets the background color for liquidity zones.

Default: Orange (with 70 transparency).

- Volume SMA Length

Determines the number of bars over which the volume simple moving average is calculated.

Default: 20 bars.

- Volume Threshold Multiplier

Multiplies the volume SMA to establish a threshold. A bar’s volume must exceed this product to be considered high volume.

Default: 2.0.

- Price Std. Dev. Length

The period used to calculate the standard deviation of the closing prices. This is the basis for measuring average volatility.

Default: 14 bars.

- Zone Volume

A toggle to display a label with the volume value on liquidity zones.

Allows you to choose how the volume is displayed: Units (shows raw volume) or Currency Value (multiplies volume by the current closing price).

Allows you to choose the font size of the volume label.

- Merge Consecutive Zones

When enabled, volumes from consecutive liquidity zones are summed into a single total, and only the most recent label is displayed (previous labels in the sequence are removed).

Default: Enabled.

- Show Last

Specifies the number of bars back that the indicator will evaluate and plot liquidity zones.

Default: 500 bars.

- Timeframe

Analysis period.

Default: Chart.

█ CONCLUSION

The Liquidity Zones indicator is a powerful tool for traders seeking to identify key areas on the chart where liquidity is concentrated, characterized by high volume and low volatility . With customizable settings for volume analysis and volatility measurement , this indicator can be integrated into a wide range of trading strategies. It not only highlights these zones visually but also provides volume data labels and alerts for timely decision-making.

█ IMPORTANT NOTES

⚠ Volume and Volatility Settings: Adjust the Volume SMA Length , Volume Threshold Multiplier , and Price Std. Dev. Length to suit the typical trading volume and volatility of the asset you are analyzing.

⚠ Confirmed Bars Only: Signals are generated only on confirmed bars. This minimizes false signals due to intra-bar noise and also prevents indicator repainting .

⚠ Risk Management: Liquidity zones may signal areas of potential accumulation or distribution, but they should be used in conjunction with other technical analysis tools (e.g., support/resistance levels, trendlines, or momentum indicators). Trading involves risk, and it is recommended to combine this indicator with proper risk management techniques.

█ RISK DISCLAIMER

Trading involves substantial risk of loss. Liquidity zones indicate potential interest areas but don't guarantee price reactions. Always confirm with additional analysis and proper risk management. Past performance is not indicative of future results.

📈 Happy trading! 🚀

iD EMARSI on ChartSCRIPT OVERVIEW

The EMARSI indicator is an advanced technical analysis tool that maps RSI values directly onto price charts. With adaptive scaling capabilities, it provides a unique visualization of momentum that flows naturally with price action, making it particularly valuable for FOREX and low-priced securities trading.

KEY FEATURES

1 PRICE MAPPED RSI VISUALIZATION

Unlike traditional RSI that displays in a separate window, EMARSI plots the RSI directly on the price chart, creating a flowing line that identifies momentum shifts within the context of price action:

// Map RSI to price chart with better scaling

mappedRsi = useAdaptiveScaling ?

median + ((rsi - 50) / 50 * (pQH - pQL) / 2 * math.min(1.0, 1/scalingFactor)) :

down == pQL ? pQH : up == pQL ? pQL : median - (median / (1 + up / down))

2 ADAPTIVE SCALING SYSTEM

The script features an intelligent scaling system that automatically adjusts to different market conditions and price levels:

// Calculate adaptive scaling factor based on selected method

scalingFactor = if scalingMethod == "ATR-Based"

math.min(maxScalingFactor, math.max(1.0, minTickSize / (atrValue/avgPrice)))

else if scalingMethod == "Price-Based"

math.min(maxScalingFactor, math.max(1.0, math.sqrt(100 / math.max(avgPrice, 0.01))))

else // Volume-Based

math.min(maxScalingFactor, math.max(1.0, math.sqrt(1000000 / math.max(volume, 100))))

3 MODIFIED RSI CALCULATION

EMARSI uses a specially formulated RSI calculation that works with an adaptive base value to maintain consistency across different price ranges:

// Adaptive RSI Base based on price levels to improve flow

adaptiveRsiBase = useAdaptiveScaling ? rsiBase * scalingFactor : rsiBase

// Calculate RSI components with adaptivity

up = ta.rma(math.max(ta.change(rsiSourceInput), adaptiveRsiBase), emaSlowLength)

down = ta.rma(-math.min(ta.change(rsiSourceInput), adaptiveRsiBase), rsiLengthInput)

// Improved RSI calculation with value constraint

rsi = down == 0 ? 100 : up == 0 ? 0 : 100 - (100 / (1 + up / down))

4 MOVING AVERAGE CROSSOVER SYSTEM

The indicator creates a smooth moving average of the RSI line, enabling a crossover system that generates trading signals:

// Calculate MA of mapped RSI

rsiMA = ma(mappedRsi, emaSlowLength, maTypeInput)

// Strategy entries

if ta.crossover(mappedRsi, rsiMA)

strategy.entry("RSI Long", strategy.long)

if ta.crossunder(mappedRsi, rsiMA)

strategy.entry("RSI Short", strategy.short)

5 VISUAL REFERENCE FRAMEWORK

The script includes visual guides that help interpret the RSI movement within the context of recent price action:

// Calculate pivot high and low

pQH = ta.highest(high, hlLen)

pQL = ta.lowest(low, hlLen)

median = (pQH + pQL) / 2

// Plotting

plot(pQH, "Pivot High", color=color.rgb(82, 228, 102, 90))

plot(pQL, "Pivot Low", color=color.rgb(231, 65, 65, 90))

med = plot(median, style=plot.style_steplinebr, linewidth=1, color=color.rgb(238, 101, 59, 90))

6 DYNAMIC COLOR SYSTEM

The indicator uses color fills to clearly visualize the relationship between the RSI and its moving average:

// Color fills based on RSI vs MA

colUp = mappedRsi > rsiMA ? input.color(color.rgb(128, 255, 0), '', group= 'RSI > EMA', inline= 'up') :

input.color(color.rgb(240, 9, 9, 95), '', group= 'RSI < EMA', inline= 'dn')

colDn = mappedRsi > rsiMA ? input.color(color.rgb(0, 230, 35, 95), '', group= 'RSI > EMA', inline= 'up') :

input.color(color.rgb(255, 47, 0), '', group= 'RSI < EMA', inline= 'dn')

fill(rsiPlot, emarsi, mappedRsi > rsiMA ? pQH : rsiMA, mappedRsi > rsiMA ? rsiMA : pQL, colUp, colDn)

7 REAL TIME PARAMETER MONITORING

A transparent information panel provides real-time feedback on the adaptive parameters being applied:

// Information display

var table infoPanel = table.new(position.top_right, 2, 3, bgcolor=color.rgb(0, 0, 0, 80))

if barstate.islast

table.cell(infoPanel, 0, 0, "Current Scaling Factor", text_color=color.white)

table.cell(infoPanel, 1, 0, str.tostring(scalingFactor, "#.###"), text_color=color.white)

table.cell(infoPanel, 0, 1, "Adaptive RSI Base", text_color=color.white)

table.cell(infoPanel, 1, 1, str.tostring(adaptiveRsiBase, "#.####"), text_color=color.white)

BENEFITS FOR TRADERS

INTUITIVE MOMENTUM VISUALIZATION

By mapping RSI directly onto the price chart, traders can immediately see the relationship between momentum and price without switching between different indicator windows.

ADAPTIVE TO ANY MARKET CONDITION

The three scaling methods (ATR-Based, Price-Based, and Volume-Based) ensure the indicator performs consistently across different market conditions, volatility regimes, and price levels.

PREVENTS EXTREME VALUES

The adaptive scaling system prevents the RSI from generating extreme values that exceed chart boundaries when trading low-priced securities or during high volatility periods.

CLEAR TRADING SIGNALS

The RSI and moving average crossover system provides clear entry signals that are visually reinforced through color changes, making it easy to identify potential trading opportunities.

SUITABLE FOR MULTIPLE TIMEFRAMES

The indicator works effectively across multiple timeframes, from intraday to daily charts, making it versatile for different trading styles and strategies.

TRANSPARENT PARAMETER ADJUSTMENT

The information panel provides real-time feedback on how the adaptive system is adjusting to current market conditions, helping traders understand why the indicator is behaving as it is.

CUSTOMIZABLE VISUALIZATION

Multiple visualization options including Bollinger Bands, different moving average types, and customizable colors allow traders to adapt the indicator to their personal preferences.

CONCLUSION

The EMARSI indicator represents a significant advancement in RSI visualization by directly mapping momentum onto price charts with adaptive scaling. This approach makes momentum shifts more intuitive to identify and helps prevent the scaling issues that commonly affect RSI-based indicators when applied to low-priced securities or volatile markets.

Adaptive Trend FinderAdaptive Trend Finder - The Ultimate Trend Detection Tool

Introducing Adaptive Trend Finder, the next evolution of trend analysis on TradingView. This powerful indicator is an enhanced and refined version of Adaptive Trend Finder (Log), designed to offer even greater flexibility, accuracy, and ease of use.

What’s New?

Unlike the previous version, Adaptive Trend Finder allows users to fully configure and adjust settings directly within the indicator menu, eliminating the need to modify chart settings manually. A major improvement is that users no longer need to adjust the chart's logarithmic scale manually in the chart settings; this can now be done directly within the indicator options, ensuring a smoother and more efficient experience. This makes it easier to switch between linear and logarithmic scaling without disrupting the analysis. This provides a seamless user experience where traders can instantly adapt the indicator to their needs without extra steps.

One of the most significant improvements is the complete code overhaul, which now enables simultaneous visualization of both long-term and short-term trend channels without needing to add the indicator twice. This not only improves workflow efficiency but also enhances chart readability by allowing traders to monitor multiple trend perspectives at once.

The interface has been entirely redesigned for a more intuitive user experience. Menus are now clearer, better structured, and offer more customization options, making it easier than ever to fine-tune the indicator to fit any trading strategy.

Key Features & Benefits

Automatic Trend Period Selection: The indicator dynamically identifies and applies the strongest trend period, ensuring optimal trend detection with no manual adjustments required. By analyzing historical price correlations, it selects the most statistically relevant trend duration automatically.

Dual Channel Display: Traders can view both long-term and short-term trend channels simultaneously, offering a broader perspective of market movements. This feature eliminates the need to apply the indicator twice, reducing screen clutter and improving efficiency.

Fully Adjustable Settings: Users can customize trend detection parameters directly within the indicator settings. No more switching chart settings – everything is accessible in one place.

Trend Strength & Confidence Metrics: The indicator calculates and displays a confidence score for each detected trend using Pearson correlation values. This helps traders gauge the reliability of a given trend before making decisions.

Midline & Channel Transparency Options: Users can fine-tune the visibility of trend channels, adjusting transparency levels to fit their personal charting style without overwhelming the price chart.

Annualized Return Calculation: For daily and weekly timeframes, the indicator provides an estimate of the trend’s performance over a year, helping traders evaluate potential long-term profitability.

Logarithmic Adjustment Support: Adaptive Trend Finder is compatible with both logarithmic and linear charts. Traders who analyze assets like cryptocurrencies, where log scaling is common, can enable this feature to refine trend calculations.

Intuitive & User-Friendly Interface: The updated menu structure is designed for ease of use, allowing quick and efficient modifications to settings, reducing the learning curve for new users.

Why is this the Best Trend Indicator?

Adaptive Trend Finder stands out as one of the most advanced trend analysis tools available on TradingView. Unlike conventional trend indicators, which rely on fixed parameters or lagging signals, Adaptive Trend Finder dynamically adjusts its settings based on real-time market conditions. By combining automatic trend detection, dual-channel visualization, real-time performance metrics, and an intuitive user interface, this indicator offers an unparalleled edge in trend identification and trading decision-making.

Traders no longer have to rely on guesswork or manually tweak settings to identify trends. Adaptive Trend Finder does the heavy lifting, ensuring that users are always working with the strongest and most reliable trends. The ability to simultaneously display both short-term and long-term trends allows for a more comprehensive market overview, making it ideal for scalpers, swing traders, and long-term investors alike.

With its state-of-the-art algorithms, fully customizable interface, and professional-grade accuracy, Adaptive Trend Finder is undoubtedly one of the most powerful trend indicators available.

Try it today and experience the future of trend analysis.

This indicator is a technical analysis tool designed to assist traders in identifying trends. It does not guarantee future performance or profitability. Users should conduct their own research and apply proper risk management before making trading decisions.

// Created by Julien Eche - @Julien_Eche

Range Breakout Signals [AlgoAlpha]OVERVIEW

This script detects range-bound market conditions and breakout signals using a combination of volatility compression and volume imbalance analysis. It identifies zones where price consolidates within a defined range and highlights potential breakout points with visual markers. Traders can use this to spot market transitions from ranging to trending phases, aiding in decision-making for breakout strategies.

CONCEPTS

The script measures volatility by comparing the ratio of the simple moving average (SMA) of price movements to their median value. When volatility drops below a threshold, the script assumes a range-bound market. It then tracks the cumulative volume of buying and selling pressure to assess breakout strength. The approach is based on the idea that market consolidation often precedes strong moves, and volume distribution can provide clues on the breakout direction.

FEATURES

Range Detection : Uses a volatility filter to identify low-volatility zones and marks them on the chart with shaded boxes.

Volume Imbalance Analysis : Evaluates cumulative up and down volume over a confirmation period to assess directional bias.

Breakout Signals : When price exits a detected range, the script plots breakout markers. A ▲ symbol indicates a bullish breakout, and a ▼ symbol indicates a bearish breakout. Additional "+" markers indicate strong volume imbalance favoring the breakout direction.

Adaptive Timeframe Volume Analysis : The script dynamically adjusts its volume calculation based on the chart’s timeframe, ensuring reliable signal generation across different trading conditions.

Alerts : Notifies traders when a new range is detected or when a breakout occurs, allowing for automated monitoring.

USAGE

Traders can use this script to identify potential trade setups by entering positions when price breaks out of a detected range. For breakout confirmation, traders can look at volume imbalance cues—bullish breakouts with strong buying volume may indicate sustained moves, while weak volume breakouts may lead to false signals. This script is particularly useful for breakout traders, range traders seeking to fade breakouts, and those looking to automate trade alerts in volatile markets.

Parabolic SAR Deviation [BigBeluga]Parabolic SAR + Deviation is an enhanced Parabolic SAR indicator designed to detect trends while incorporating deviation levels and trend change markers for added depth in analyzing price movements.

🔵 Key Features:

> Parabolic SAR with Optimized Settings:

Built on the classic Parabolic SAR, this version uses predefined default settings to enhance its ability to detect and confirm trends.

Clear trend direction is indicated by smooth trend lines, allowing traders to easily visualize market movements.

Trend Change Markers:

When a trend change occurs based on the SAR, the indicator plots a triangle at the trend change point.

The triangle is accompanied by the price value of the trend change, allowing traders to identify key reversal points instantly.

> Deviation Levels:

Four deviation levels are automatically plotted when a trend change occurs (up or down).

Uptrend: Deviation levels are positioned above the entry point.

Downtrend: Deviation levels are positioned below the entry point.

Levels are labeled with numbers 1 to 4, representing increasing degrees of deviation.

> Dynamic Level Updates:

When the price crosses a deviation level, the level becomes dashed and its label changes to display the volume at the breakout point.

This volume information helps traders assess the strength of the breakout and the potential for trend continuation or reversal.

> Volume Analysis at Breakpoints:

The volume displayed at crossed deviation levels provides insight into the strength of the price movement.

High volume at a breakout may indicate strong momentum, while low volume could signal potential exhaustion or a false breakout.

🔵 Usage:

Identify Trends: Use the trend change triangles and smooth SAR trend lines to confirm whether the market is trending up or down.

Analyze Deviation Levels: Monitor deviation levels **1–4** to identify potential breakout points and assess the degree of price deviation from the entry point.

Observe Trend Change Points: Utilize the triangles and price labels to quickly spot significant trend changes.

Volume Insights: Evaluate the volume displayed at crossed levels to determine the strength of the breakout and assess the likelihood of trend continuation or reversal.

Risk Management: Use deviation levels as potential stop-loss or take-profit zones, depending on the strength of the trend and volume conditions.

Parabolic SAR + Deviation is an essential tool for traders seeking a straightforward yet powerful method to identify trends, analyze price deviations, and gain insights into volume dynamics at critical breakout and trend change levels.

Risk MeterRisk Meter Indicator for TradingView

The Risk Meter is a powerful market risk assessment tool designed to help traders evaluate the current risk environment using a simple, data-driven score. By analyzing four critical market factors—VIX (volatility index), market breadth, trailing volatility, and credit spreads—the indicator generates a risk score between 0 and 4. This score empowers traders to make informed decisions about hedging, exiting positions, or re-entering the market, with clear visual cues and alerts for intraday monitoring.

What It Does

Calculates a Risk Score: Assigns a score from 0 to 4, where each point reflects an active risk condition based on four market indicators.

Identifies Risk Levels:

A score of 3 or higher indicates a high-risk environment, suggesting traders consider hedging or reducing exposure.

A score of 2 or lower for at least two consecutive days signals a potential opportunity to re-enter the market.

Provides Visual Feedback: Uses color-coded Columns, threshold markers, and a component table for quick interpretation.

Supports Decision-Making: Offers a structured approach to managing risk and timing trades.

How It Works

The Risk Meter aggregates four key risk conditions, each contributing 1 point to the total score when triggered:

Elevated and Rising VIX (Risk 1)

Condition: The VIX is above 18 and higher than it was 20 days ago.

Purpose: Detects increasing market fear or uncertainty.

Market Breadth Dropping (Risk 2)

Condition: Either:

Fewer than 50% of S&P 500 stocks are above their 200-day moving average and fewer than 70% are above their 50-day moving average, or

The 3-day EMA of the 200-day breadth falls below 80% of its 20-day SMA.

Purpose: Identifies weakening participation across the market.

Trailing Volatility (Risk 3)

Condition: The 30-day annualized volatility of the equal-weight S&P 500 (RSP) exceeds 35%.

Purpose: Highlights periods of heightened price instability.

Credit Spreads (Risk 4)

Condition: The price ratio of high-yield bonds (HYG) to Treasuries (TLT or IEF) is lower than it was 20 days ago, indicating widening credit spreads.

Purpose: Signals potential stress in credit markets.

The total risk score is the sum of these conditions (0 to 4). Additionally, the indicator tracks consecutive days with a score of 2 or lower to generate re-entry signals.

How to Read It Intraday

The Risk Meter is built on daily data but can be monitored intraday for real-time insights. Here’s how traders can interpret it:

Risk Score Plot:

Displayed as a step line ranging from 0 to 4.

Colors:

Red: High risk (score ≥ 3) – caution advised.

Green: Re-entry signal – score ≤ 2 for at least two consecutive days (triggered when the count increments from 1 to 2).

Blue: Neutral or low risk (score < 3 without a re-entry signal).

Threshold Lines:

Dashed Gray Line at 3: Marks the high-risk threshold.

Dotted Gray Line at 2: Indicates the low-risk threshold for re-entry signals.

Risk Component Table:

Located in the top-right corner, it lists:

VIX, Breadth, Volatility, and Credit Spreads.

Status: Shows "" (warning, red) if the risk condition is met, or "✓" (safe, blue) if not.

Helps traders pinpoint which factors are driving the score.

Alerts:

High Risk Alert: Triggers when the score moves from < 3 to ≥ 3.

Re-entry Signal Alert: Triggers when the score ≤ 2 for two consecutive days.

Intraday Usage Tips

Check the indicator throughout the day for early signs of risk shifts, especially if the score is near a threshold (e.g., 2 or 3).

Combine with other intraday tools (e.g., price action, volume) since the Risk Meter updates daily but reflects broader market conditions.

How Traders Can Use It

High-Risk Signal (Score ≥ 3):

Consider hedging positions (e.g., with options) or reducing equity exposure to protect against potential downturns.

Re-entry Signal (Score ≤ 2 for 2+ Days):

Look to re-enter the market or increase exposure, as it suggests stabilizing conditions.

Daily Risk Management:

Use the score and table to assess overall market health and adjust strategies accordingly.

Alert-Driven Trading:

Set up alerts to stay notified of critical risk changes without constant monitoring.

Why Use the Risk Meter?

This indicator offers a systematic, multi-factor approach to risk assessment, blending volatility, breadth, and credit market data into an easy-to-read score. Whether you’re an intraday trader or a longer-term investor, the Risk Meter helps you stay proactive, avoid surprises, and time your trades with greater confidence.

Financial Risk Disclaimer for the Risk Meter Tool

Important Notice: The Risk Meter is a market risk assessment tool designed to provide insights into current market conditions based on historical data and predefined indicators. It is intended for informational and educational purposes only and should not be considered financial advice, a recommendation to buy or sell any securities, or a guarantee of future market performance.

Key Considerations

No Guarantee of Accuracy: While the Risk Meter utilizes reliable data sources and established financial metrics, the creators do not guarantee the accuracy, completeness, or timeliness of the information provided. Financial markets are complex and subject to rapid, unpredictable changes, and the tool’s output may not fully reflect all market dynamics.

Market Risks: Trading and investing in financial markets carry significant risks, including the potential loss of principal. Market volatility, economic shifts, and other factors can lead to unexpected outcomes. Past performance is not a reliable indicator of future results, and the Risk Meter’s assessments are based on historical data, not future predictions.

Not a Substitute for Professional Advice: The Risk Meter is not intended to replace personalized financial guidance. Users are strongly encouraged to consult a qualified financial advisor, perform their own research, and evaluate their personal financial situation, risk tolerance, and investment objectives before making any trading or investment decisions.

Limitation of Liability: The creators of the Risk Meter, including any affiliates, developers, or contributors, are not liable for any direct, indirect, incidental, or consequential losses or damages arising from the use of this tool. This includes, but is not limited to, financial losses, missed opportunities, or decisions based on the tool’s output.

User Responsibility: By using the Risk Meter, you accept full responsibility for your trading and investment decisions. You acknowledge that you use the tool at your own risk and that the creators bear no responsibility for any outcomes resulting from its use.

Final Note

The Risk Meter is a supplementary tool designed to enhance your understanding of market risk. It is not a comprehensive solution for investment management. Approach trading and investing with caution, ensuring your decisions align with your personal financial strategy.

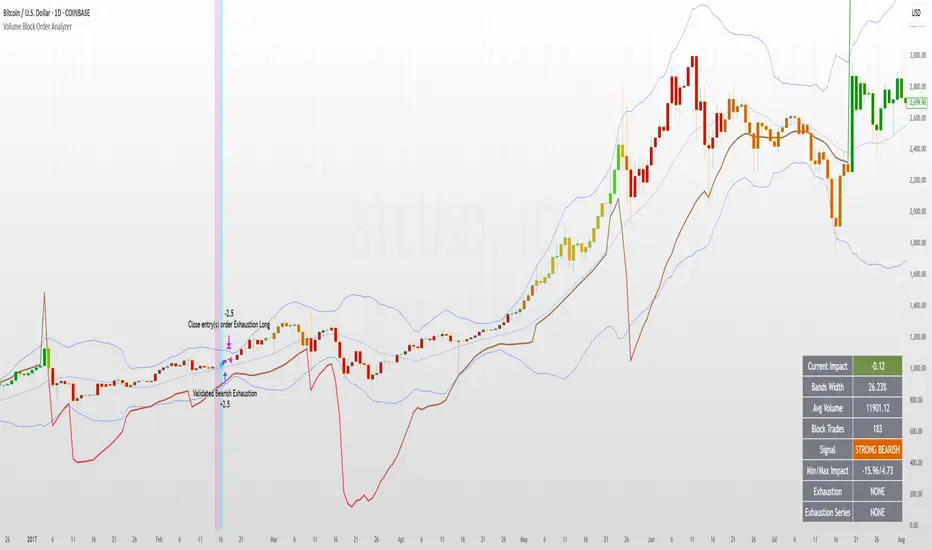

Volume Block Order AnalyzerCore Concept

The Volume Block Order Analyzer is a sophisticated Pine Script strategy designed to detect and analyze institutional money flow through large block trades. It identifies unusually high volume candles and evaluates their directional bias to provide clear visual signals of potential market movements.

How It Works: The Mathematical Model

1. Volume Anomaly Detection

The strategy first identifies "block trades" using a statistical approach:

```

avgVolume = ta.sma(volume, lookbackPeriod)

isHighVolume = volume > avgVolume * volumeThreshold

```

This means a candle must have volume exceeding the recent average by a user-defined multiplier (default 2.0x) to be considered a significant block trade.

2. Directional Impact Calculation

For each block trade identified, its price action determines direction:

- Bullish candle (close > open): Positive impact

- Bearish candle (close < open): Negative impact

The magnitude of impact is proportional to the volume size:

```

volumeWeight = volume / avgVolume // How many times larger than average

blockImpact = (isBullish ? 1.0 : -1.0) * (volumeWeight / 10)

```

This creates a normalized impact score typically ranging from -1.0 to 1.0, scaled by dividing by 10 to prevent excessive values.

3. Cumulative Impact with Time Decay

The key innovation is the cumulative impact calculation with decay:

```

cumulativeImpact := cumulativeImpact * impactDecay + blockImpact

```

This mathematical model has important properties:

- Recent block trades have stronger influence than older ones

- Impact gradually "fades" at rate determined by decay factor (default 0.95)

- Sustained directional pressure accumulates over time

- Opposing pressure gradually counteracts previous momentum

Trading Logic

Signal Generation

The strategy generates trading signals based on momentum shifts in institutional order flow:

1. Long Entry Signal: When cumulative impact crosses from negative to positive

```

if ta.crossover(cumulativeImpact, 0)

strategy.entry("Long", strategy.long)

```

*Logic: Institutional buying pressure has overcome selling pressure, indicating potential upward movement*

2. Short Entry Signal: When cumulative impact crosses from positive to negative

```

if ta.crossunder(cumulativeImpact, 0)

strategy.entry("Short", strategy.short)

```

*Logic: Institutional selling pressure has overcome buying pressure, indicating potential downward movement*

3. Exit Logic: Positions are closed when the cumulative impact moves against the position

```

if cumulativeImpact < 0

strategy.close("Long")

```

*Logic: The original signal is no longer valid as institutional flow has reversed*

Visual Interpretation System

The strategy employs multiple visualization techniques:

1. Color Gradient Bar System:

- Deep green: Strong buying pressure (impact > 0.5)

- Light green: Moderate buying pressure (0.1 < impact ≤ 0.5)

- Yellow-green: Mild buying pressure (0 < impact ≤ 0.1)

- Yellow: Neutral (impact = 0)

- Yellow-orange: Mild selling pressure (-0.1 < impact ≤ 0)

- Orange: Moderate selling pressure (-0.5 < impact ≤ -0.1)

- Red: Strong selling pressure (impact ≤ -0.5)

2. Dynamic Impact Line:

- Plots the cumulative impact as a line

- Line color shifts with impact value

- Line movement shows momentum and trend strength

3. Block Trade Labels:

- Marks significant block trades directly on the chart

- Shows direction and volume amount

- Helps identify key moments of institutional activity

4. Information Dashboard:

- Current impact value and signal direction

- Average volume benchmark

- Count of significant block trades

- Min/Max impact range

Benefits and Use Cases

This strategy provides several advantages:

1. Institutional Flow Detection: Identifies where large players are positioning themselves

2. Early Trend Identification: Often detects institutional accumulation/distribution before major price movements

3. Market Context Enhancement: Provides deeper insight than simple price action alone

4. Objective Decision Framework: Quantifies what might otherwise be subjective observations

5. Adaptive to Market Conditions: Works across different timeframes and instruments by using relative volume rather than absolute thresholds

Customization Options

The strategy allows users to fine-tune its behavior:

- Volume Threshold: How unusual a volume spike must be to qualify

- Lookback Period: How far back to measure average volume

- Impact Decay Factor: How quickly older trades lose influence

- Visual Settings: Labels and line width customization

This sophisticated yet intuitive strategy provides traders with a window into institutional activity, helping identify potential trend changes before they become obvious in price action alone.

ATR Stop Loss & 3 TP FinderATR Stop Loss & 3 TP Finder - By SeehraSingh

This indicator is designed to help traders automate Stop Loss (SL) and Take Profit (TP) placement based on the Average True Range (ATR). It dynamically calculates:

Stop Loss (SL): Set based on a user-defined ATR multiplier.

Three Take Profit (TP) levels: Configurable ATR multipliers for TP1, TP2, and TP3.

Customizable Price Sources: Allows traders to choose different price sources (Open, High, Low, Close, HL2, HLC3, OHLC4, HLCC4) for both SL and TP calculations.

Visual Representation: Plots dashed lines for Entry, SL, TP1, TP2, and TP3.

Table Display: Provides an easy-to-read table at the bottom showing SL, TP1, TP2, and TP3 values.

How It Works:

Select ATR length and smoothing type (RMA, SMA, EMA, WMA).

Set ATR multipliers for SL and TP levels.

Choose the price source for SL and TP calculations.

The indicator automatically plots entry, SL, and three TP levels on the chart.

Ideal For:

Traders who use ATR-based dynamic Stop Loss and Take Profit strategies.

Those who want to avoid fixed SL/TP placements and prefer volatility-based risk management.

Scalpers, Swing Traders, and Position Traders looking for automated SL/TP visualization.

Disclaimer

⚠️ Trading involves risk. This indicator is for educational purposes only and should not be considered financial advice. Always conduct your own analysis before entering any trade. The author is not responsible for any financial losses incurred while using this tool. Past performance does not guarantee future results.

Adaptive Fibonacci Volatility Bands (AFVB)

**Adaptive Fibonacci Volatility Bands (AFVB)**

### **Overview**

The **Adaptive Fibonacci Volatility Bands (AFVB)** indicator enhances standard **Fibonacci retracement levels** by dynamically adjusting them based on market **volatility**. By incorporating **ATR (Average True Range) adjustments**, this indicator refines key **support and resistance zones**, helping traders identify **more reliable entry and exit points**.

**Key Features:**

- **ATR-based adaptive Fibonacci levels** that adjust to changing market volatility.

- **Buy and Sell signals** based on price interactions with dynamic support/resistance.

- **Toggleable confirmation filter** for refining trade signals.

- **Customizable color schemes** and alerts.

---

## **How This Indicator Works**

The **AFVB** operates in three main steps:

### **1️⃣ Detecting Key Fibonacci Levels**

The script calculates **swing highs and swing lows** using a user-defined lookback period. From this, it derives **Fibonacci retracement levels**:

- **0% (High)**

- **23.6%**

- **38.2%**

- **50% (Mid-Level)**

- **61.8%**

- **78.6%**

- **100% (Low)**

### **2️⃣ Adjusting for Market Volatility**

Instead of using **fixed retracement levels**, this indicator incorporates an **ATR-based adjustment**:

- **Resistance levels** shift **upward** based on ATR.

- **Support levels** shift **downward** based on ATR.

- This makes levels more **responsive** to price action.

### **3️⃣ Generating Buy & Sell Signals**

AFVB provides **two types of signals** based on price interactions with key levels:

✔ **Buy Signal**:

Occurs when price **dips below** a support level (78.6% or 100%) and **then closes back above it**.

- **Optionally**, a confirmation buffer can be enabled to require price to close **above an additional threshold** (based on ATR).

✔ **Sell Signal**:

Triggered when price **breaks above a resistance level** (0% or 23.6%) and **then closes below it**.

📌 **Important:**

- The **buy threshold setting** allows traders to **fine-tune** entry conditions.

- Turning this setting **off** generates **more frequent** buy signals.

- Keeping it **on** reduces false signals but may result in **fewer trade opportunities**.

---

## **How to Use This Indicator in Trading**

### 🔹 **Entry Strategy (Buying)**

1️⃣ Look for **buy signals** at the **78.6% or 100% Fibonacci levels**.

2️⃣ Ensure price **closes above** the support level before entering a long trade.

3️⃣ **Enable or disable** the buy threshold filter depending on desired trade strictness.

### 🔹 **Exit Strategy (Selling)**

1️⃣ Watch for **sell signals** at the **0% or 23.6% Fibonacci levels**.

2️⃣ If price **breaks above resistance and then closes below**, consider exiting long positions.

3️⃣ Can be used **alone** or **combined with trend confirmation tools** (e.g., moving averages, RSI).

### 🔹 **Using the Toggleable Buy Threshold**

- **ON**: Buy signal requires **extra confirmation** (reduces false signals but fewer trades).

- **OFF**: Buy triggers as soon as price **closes back above support** (more signals, but may include weaker setups).

---

## **User Inputs**

### **🔧 Customization Options**

- **ATR Length**: Defines the period for **ATR calculation**.

- **Swing Lookback**: Determines how far back to find **swing highs and lows**.

- **ATR Multiplier**: Adjusts the size of **volatility-based modifications**.

- **Buy/Sell Threshold Factor**: Fine-tunes the **entry signal strictness**.

- **Show Level Labels**: Enables/disables **Fibonacci level annotations**.

- **Color Settings**: Customize **support/resistance colors**.

### **📢 Alerts**

AFVB includes built-in **alert conditions** for:

- **Buy Signals** ("AFVB BUY SIGNAL - Possible reversal at support")

- **Sell Signals** ("AFVB SELL SIGNAL - Possible reversal at resistance")

- **Any Signal Triggered** (Useful for automated alerts)

---

## **Who Is This Indicator For?**

✅ **Scalpers & Day Traders** – Helps identify **short-term reversals**.

✅ **Swing Traders** – Useful for **buying dips** and **selling rallies**.

✅ **Trend Traders** – Can be combined with **momentum indicators** for confirmation.

**Best Timeframes:**

⏳ **15-minute, 1-hour, 4-hour, Daily charts** (works across multiple assets).

---

## **Limitations & Considerations**

🚨 **Important Notes**:

- **No indicator guarantees profits**. Always **combine** it with **risk management strategies**.

- Works best **in trending & mean-reverting markets**—may generate false signals in **choppy conditions**.

- Performance may vary across **different assets & timeframes**.

📢 **Backtesting is recommended** before using it for live trading.

Advanced Adaptive Grid Trading StrategyThis strategy employs an advanced grid trading approach that dynamically adapts to market conditions, including trend, volatility, and risk management considerations. The strategy aims to capitalize on price fluctuations in both rising (long) and falling (short) markets, as well as during sideways movements. It combines multiple indicators to determine the trend and automatically adjusts grid parameters for more efficient trading.

How it Works:

Trend Analysis:

Short, long, and super long Moving Averages (MA) to determine the trend direction.

RSI (Relative Strength Index) to identify overbought and oversold levels, and to confirm the trend.

MACD (Moving Average Convergence Divergence) to confirm momentum and trend direction.

Momentum indicator.

The strategy uses a weighted scoring system to assess trend strength (strong bullish, moderate bullish, strong bearish, moderate bearish, sideways).

Grid System:

The grid size (the distance between buy and sell levels) changes dynamically based on market volatility, using the ATR (Average True Range) indicator.

Grid density also adapts to the trend: in a strong trend, the grid is denser in the direction of the trend.

Grid levels are shifted depending on the trend direction (upwards in a bear market, downwards in a bull market).

Trading Logic:

The strategy opens long positions if the trend is bullish and the price reaches one of the lower grid levels.

It opens short positions if the trend is bearish and the price reaches one of the upper grid levels.

In a sideways market, it can open positions in both directions.

Risk Management:

Stop Loss for every position.

Take Profit for every position.

Trailing Stop Loss to protect profits.

Maximum daily loss limit.

Maximum number of positions limit.

Time-based exit (if the position is open for too long).

Risk-based position sizing (optional).

Input Options:

The strategy offers numerous settings that allow users to customize its operation:

Timeframe: The chart's timeframe (e.g., 1 minute, 5 minutes, 1 hour, 4 hours, 1 day, 1 week).

Base Grid Size (%): The base size of the grid, expressed as a percentage.

Max Positions: The maximum number of open positions allowed.

Use Volatility Grid: If enabled, the grid size changes dynamically based on the ATR indicator.

ATR Length: The period of the ATR indicator.

ATR Multiplier: The multiplier for the ATR to fine-tune the grid size.

RSI Length: The period of the RSI indicator.

RSI Overbought: The overbought level for the RSI.

RSI Oversold: The oversold level for the RSI.

Short MA Length: The period of the short moving average.

Long MA Length: The period of the long moving average.

Super Long MA Length: The period of the super long moving average.

MACD Fast Length: The fast period of the MACD.

MACD Slow Length: The slow period of the MACD.

MACD Signal Length: The period of the MACD signal line.

Stop Loss (%): The stop loss level, expressed as a percentage.

Take Profit (%): The take profit level, expressed as a percentage.

Use Trailing Stop: If enabled, the strategy uses a trailing stop loss.

Trailing Stop (%): The trailing stop loss level, expressed as a percentage.

Max Loss Per Day (%): The maximum daily loss, expressed as a percentage.

Time Based Exit: If enabled, the strategy exits the position after a certain amount of time.

Max Holding Period (hours): The maximum holding time in hours.

Use Risk Based Position: If enabled, the strategy calculates position size based on risk.

Risk Per Trade (%): The risk per trade, expressed as a percentage.

Max Leverage: The maximum leverage.

Important Notes:

This strategy does not guarantee profits. Cryptocurrency markets are volatile, and trading involves risk.

The strategy's effectiveness depends on market conditions and settings.

It is recommended to thoroughly backtest the strategy under various market conditions before using it live.

Past performance is not indicative of future results.

ST_HTF_EMA### **ST_HTF_EMA – Higher Timeframe EMA Overlay**

#### **Description:**

The **ST_HTF_EMA** indicator plots a **21-period Exponential Moving Average (EMA)** from a **higher timeframe** onto the current chart. This allows traders to track key trend levels from a larger perspective while trading on a lower timeframe.

#### **Features:**

- **Customizable Timeframe:** The EMA is sourced from a user-defined timeframe (default: **5-minute**).

- **EMA Calculation:** Uses the **21-period EMA** for smoothing price action and identifying trend direction.

- **Envelope Bands (Optional):** A **0.75% envelope** can be toggled on to create upper and lower bands around the EMA for potential dynamic support/resistance zones.

- **Overlay on Chart:** The EMA and envelope bands are plotted directly on the price chart for easy visibility.

#### **How to Use:**

- Use the **EMA as a trend guide**—price above the EMA suggests bullish momentum, while price below indicates bearish momentum.

- Enable the **envelope bands** (if needed) to spot price deviations from the mean for possible reversal or continuation trades.

#### **Customization:**

- Modify the **timeframe** to adapt the EMA to different market structures.

- Adjust the **envelope percentage** to fine-tune sensitivity.

#### **Visuals:**

- The **EMA is plotted in yellow** for clear visibility.

- **Envelope bands (if enabled)** appear in yellow, with a subtle background highlight.

This indicator is ideal for traders who rely on **higher timeframe trend confirmation** while making decisions on lower timeframes. 🚀

BTC: Open InterestThis indicator tracks the 7-day (default) percentage change in open interest (OI), providing insights into market participation trends. It includes customizable periods and colors, allowing traders to adjust settings for better visualization.

Open interest (OI) is the total number of active contracts (futures or options) that haven’t been closed or settled. It represents the total open positions in the market.

Thus when OI increases, more traders are entering new positions, signaling growing market interest. Conversely, when OI decreases, positions are being closed, suggesting lower trader participation or liquidation.

Attributes & Features:

Open Interest Percentage Change – Measures the 7-day % change in open interest to track market participation.

Customizable Calculation Period – Users can adjust the period (default: 7 days) for more flexible analysis.

Adjustable Colors – Allows modification of colors for better visualization.

Trend Identification – Highlights rising vs. falling open interest trends.

Works Across Assets – Can be used for cryptos, stocks, and futures with open interest data.

Overlay or Separate Panel – Can be plotted on price chart or as a separate indicator.

How It Works:

Fetches Open Interest Data – Retrieves open interest values for each day for USD, USDT, and USDC Bitcoin Perpetual Derivitives.

Calculates Percentage Change – Compares current open interest to its value X days ago (Default = 7 days).

Standard Deviation – Applies standard deviation ranging from -2 to +2 deviations to identify large shifts in OI.

Visual Alerts – Can highlight extreme increases or decreases signaling potential market shifts.

NOTE: THE INDICATOR DATA ONLY GOES BACK TO START OF 2022

Higher Timeframe Support/ResistanceMulti-Timeframe Support/Resistance Indicator

This TradingView indicator helps you monitor important support and resistance levels based on the previous candle’s high, low, and close from a higher timeframe. By default, it uses a daily timeframe, but you can adjust this to any timeframe you want.

Key Features:

- Previous Candle High (PCH) and Previous Candle Low (PCL):

These levels are plotted on your chart (if enabled) and can act as potential support and

resistance zones. You can toggle the visibility of these levels.

- Pivot, Resistance (R1), and Support (S1):

The script calculates Pivot, R1 (Resistance), and S1 (Support) levels based on the previous

candle's price action from the selected higher timeframe.

These levels are displayed on your chart and can be used to identify potential breakout or

reversal points.

- Alert Feature:

Alerts are triggered when the price approaches any of these key levels (PCH, PCL, Pivot, R1,

or S1) within a specified threshold (e.g., 0.5%).

This helps traders react quickly to potential price movements near critical levels.

- Visual Representation:

The script visually fills the areas between Pivot and R1 (Resistance-Pivot Zone) and Pivot and

S1 (Support-Pivot Zone) with color for easy identification of key price zones.

Combined ATR + VolumeOverview

The Combined ATR + Volume indicator (C-ATR+Vol) is designed to measure both price volatility and market participation by merging the Average True Range (ATR) and trading volume into a single normalized value. This provides traders with a more comprehensive tool than ATR alone, as it highlights not only how much price is moving, but also whether there is sufficient volume behind those moves.

Originality & Utility

Two Key Components

ATR (Average True Range): Measures price volatility by analyzing the range (high–low) over a specified period. A higher ATR often indicates larger price swings.

Volume: Reflects how actively traders are participating in the market. High volume typically indicates strong buying or selling interest.

Normalized Combination

Both ATR and volume are independently normalized to a 0–100 range.

The final output (C-ATR+Vol) is the average of these two normalized values. This makes it easy to see when both volatility and market participation are relatively high.

Practical Use

Above 80: Signifies elevated volatility and strong volume. Markets may experience significant moves.

Around 50–80: Indicates moderate activity. Price swings and volume are neither extreme nor minimal.

Below 50: Suggests relatively low volatility and lower participation. The market may be ranging or consolidating.

This combined approach can help filter out situations where volatility is high but volume is absent—or vice versa—providing a more reliable context for potential breakouts or trend continuations.

Indicator Logic

ATR Calculation

Uses Pine Script’s built-in ta.tr(true) function to measure true range, then smooths it with a user-selected method (RMA, SMA, EMA, or WMA).

Key Input: ATR Length (default 14).

Volume Calculation

Smooths the built-in volume variable using the same selectable smoothing methods.

Key Input: Volume Length (default 14).

Normalization

For each metric (ATR and Volume), the script finds the lowest and highest values over the lookback period and converts them into a 0–100 scale:

normalized value

=(current value−min)(max−min)×100

normalized value= (max−min)(current value−min) ×100

Combined Score

The final plot is the average of Normalized ATR and Normalized Volume. This single value simplifies the process of identifying high-volatility, high-volume conditions.

How to Use

Setup

Add the indicator to your chart.

Adjust ATR Length, Volume Length, and Smoothing to match your preferred time horizon or chart style.

Interpretation

High Values (above 80): The market is experiencing significant price movement with high participation. Potential for strong trends or breakouts.

Moderate Range (50–80): Conditions are active but not extreme. Trend setups may be forming.

Low Values (below 50): Indicates quieter markets with reduced liquidity. Expect ranging or less decisive moves.

Strategy Integration

Use C-ATR+Vol alongside other trend or momentum indicators (e.g., Moving Averages, RSI, MACD) to confirm potential entries/exits.

Combine it with support/resistance or price action analysis for a broader market view.

Important Notes

This script is open-source and intended as a community contribution.

No Future Guarantee: Past market behavior does not guarantee future results. Always use proper risk management and validate signals with additional tools.

The indicator’s performance may vary depending on timeframes, asset classes, and market conditions.

Adjust inputs as needed to suit different instruments or personal trading styles.

By adhering to TradingView’s publishing rules, this script is provided with sufficient detail on what it does, how it’s unique, and how traders can use it. Feel free to customize the settings and experiment with other technical indicators to develop a trading methodology that fits your objectives.

🔹 Combined ATR + Volume (C-ATR+Vol) 지표 설명

이 인디케이터는 ATR(Average True Range)와 거래량(Volume)을 결합하여 시장의 변동성과 유동성을 동시에 측정하는 지표입니다.

ATR은 가격 변동성의 크기를 나타내며, 거래량은 시장 참여자의 활동 수준을 반영합니다. 보통 높은 ATR은 가격 변동이 크다는 의미이고, 높은 거래량은 시장에서 적극적인 거래가 이루어지고 있음을 나타냅니다.

이 두 지표를 각각 0~100 범위로 정규화한 후, 평균을 구하여 "Combined ATR + Volume (C-ATR+Vol)" 값을 계산합니다.

이를 통해 단순한 가격 변동성뿐만 아니라 거래량까지 고려하여, 더욱 신뢰성 있는 변동성 판단을 할 수 있도록 도와줍니다.

📌 핵심 개념

1️⃣ ATR (Average True Range)란?

시장의 변동성을 측정하는 지표로, 일정 기간 동안의 고점-저점 변동폭을 기반으로 계산됩니다.

ATR이 높을수록 가격 변동이 크며, 낮을수록 횡보장이 지속될 가능성이 큽니다.

하지만 ATR은 방향성을 제공하지 않으며, 단순히 변동성의 크기만을 나타냅니다.

2️⃣ 거래량 (Volume)의 역할

거래량은 시장 참여자의 관심과 유동성을 반영하는 중요한 요소입니다.

높은 거래량은 강한 매수 또는 매도세가 존재함을 의미하며, 낮은 거래량은 시장 참여가 적거나 관심이 줄어들었음을 나타냅니다.

3️⃣ ATR + 거래량의 결합 (C-ATR+Vol)

단순한 ATR 값만으로는 변동성이 커도 거래량이 부족할 수 있으며, 반대로 거래량이 많아도 변동성이 낮을 수 있습니다.

이를 해결하기 위해 ATR과 거래량을 각각 0~100으로 정규화하여 균형 잡힌 변동성 지표를 만들었습니다.

두 지표의 평균값을 계산하여, 가격 변동과 거래량이 동시에 높은지를 측정할 수 있도록 설계되었습니다.

📊 사용법 및 해석

80 이상 → 강한 변동성 구간

가격 변동성이 크고 거래량도 높은 상태

강한 추세가 진행 중이거나 큰 변동이 일어날 가능성이 큼

상승/하락 방향성을 확인한 후 트렌드를 따라가는 전략이 유리

50~80 구간 → 보통 수준의 변동성

가격 움직임이 일정하며, 거래량도 적절한 수준

점진적인 추세 형성이 이루어질 가능성이 있음

시장이 점진적으로 상승 혹은 하락할 가능성이 크므로, 보조지표를 활용하여 매매 타이밍을 결정하는 것이 중요

50 이하 → 낮은 변동성 및 유동성 부족

가격 변동이 적고, 거래량도 낮은 상태

시장이 횡보하거나 조정 기간에 들어갈 가능성이 큼

박스권 매매(지지/저항 활용) 또는 돌파 전략을 고려할 수 있음

💡 활용 방법 및 전략

✅ 1. 트렌드 판단 보조지표로 활용

단독으로 사용하는 것보다는 RSI, MACD, 이동평균선(MA) 등의 지표와 함께 활용하는 것이 효과적입니다.

예를 들어, MACD가 상승 신호를 주고, C-ATR+Vol 값이 80을 초과하면 강한 상승 추세로 해석할 수 있습니다.

✅ 2. 변동성 돌파 전략에 활용

C-ATR+Vol이 80 이상인 구간에서 가격이 특정 저항선을 돌파한다면, 강한 추세의 시작을 의미할 수 있습니다.

반대로, C-ATR+Vol이 50 이하에서 가격이 저항선에 가까워지면 돌파 가능성이 낮아질 수 있습니다.

✅ 3. 시장 참여도와 변동성 확인

단순히 ATR만 높아서는 신뢰하기 어려운 경우가 많습니다. 예를 들어, 급등 후 거래량이 급감하면 상승 지속 가능성이 낮아질 수도 있습니다.

하지만 C-ATR+Vol을 사용하면 거래량이 함께 증가하는지를 확인하여 보다 신뢰할 수 있는 분석이 가능합니다.

🚀 결론

🔹 Combined ATR + Volume (C-ATR+Vol) 인디케이터는 단순한 ATR이 아니라 거래량까지 고려하여 변동성을 측정하는 강력한 도구입니다.

🔹 시장이 큰 움직임을 보일 가능성이 높은 구간을 찾는 데 유용하며, 80 이상일 경우 강한 변동성이 있음을 나타냅니다.

🔹 단독으로 사용하기보다는 보조지표와 함께 활용하여, 트렌드 분석 및 돌파 전략 등에 효과적으로 적용할 수 있습니다.

📌 주의사항

변동성이 크다고 해서 반드시 가격이 급등/급락한다는 보장은 없습니다.

특정한 매매 전략 없이 단순히 이 지표만 보고 매수/매도를 결정하는 것은 위험할 수 있습니다.

시장 상황에 따라 변동성의 의미가 다르게 작용할 수 있으므로, 반드시 다른 보조지표와 함께 활용하는 것이 중요합니다.

🔥 이 지표를 활용하여 시장의 변동성과 거래량을 보다 효과적으로 분석해보세요! 🚀

IU BBB(Big Body Bar) StrategyDESCRIPTION

The IU BBB (Big Body Bar) Strategy is a price action-based trading strategy that identifies high-momentum candles with significantly larger body sizes compared to the average. It enters trades when a strong bullish or bearish move occurs and manages risk using an ATR-based trailing stop-loss system.

USER INPUTS:

- Big Body Threshold – Defines how many times larger the candle body should be compared to the average body ( default is 4 ).

- ATR Length – The period for the Average True Range (ATR) used in the trailing stop-loss calculation ( default is 14 ).

- ATR Factor – Multiplier for ATR to determine the trailing stop distance ( default is 2 ).

LONG CONDITION:

- The current candle’s body is greater than the average body size multiplied by the Big Body Threshold.

- The closing price is higher than the opening price (bullish candle).

SHORT CONDITION:

- The current candle’s body is greater than the average body size multiplied by the Big Body Threshold.

- The closing price is lower than the opening price (bearish candle).

LONG EXIT:

- ATR-based trailing stop-loss dynamically adjusts, locking in profits as the price moves higher.

SHORT EXIT:

- ATR-based trailing stop-loss dynamically adjusts, securing profits as the price moves lower.

WHY IT IS UNIQUE:

- Unlike traditional momentum strategies, this system adapts to volatility by filtering trades based on relative candle size.

- It incorporates an ATR-based trailing stop-loss, ensuring risk management and profit protection.

- The strategy avoids choppy market conditions by only trading when significant momentum is present.

HOW USERS CAN BENEFIT FROM IT:

- Catch Strong Price Moves – The strategy helps traders enter trades when the market shows decisive momentum.

- Effective Risk Management – The ATR-based trailing stop ensures that winning trades remain profitable.

- Works Across Markets – Can be applied to stocks, forex, crypto, and indices with proper optimization.

- Fully Customizable – Users can adjust sensitivity settings to match their trading style and time frame.

Supertrend with RSI FilterThis indicator is an enhanced version of the classic Supertrend, incorporating an RSI (Relative Strength Index) filter to refine trend signals. Here is a detailed explanation of its functionality and key advantages over the traditional Supertrend.

1. Indicator Functionality

The indicator uses ATR (Average True Range) to calculate the Supertrend line, just like the classic version. However, it introduces an additional condition based on RSI to strengthen or weaken the Supertrend color based on market momentum.

2. Interpretation of Colors

The indicator displays the Supertrend line with dynamic colors based on trend direction and RSI strength:

- Uptrend (Supertrend in buy mode):

- Dark green (Teal): RSI above the defined threshold (default 50) → Strong bullish confirmation.

- Light gray: RSI below the threshold → Indicates a weaker uptrend or lack of confirmation.

- Downtrend (Supertrend in sell mode):

- Dark red: RSI below the threshold → Strong bearish confirmation.

- Light gray: RSI above the threshold → Indicates a weaker downtrend or lack of confirmation.

The opacity of the color dynamically adjusts based on how far RSI is from its threshold. The greater the difference, the more vivid the color, signaling a stronger trend.

3. Key Advantages Over the Classic Supertrend

- Filters out false signals: The RSI integration helps reduce false signals by only validating trends when RSI aligns with the Supertrend direction.

- Weakens uncertain signals: When RSI is close to its threshold, the color becomes more transparent, alerting traders to a less reliable trend.

- Classic mode available: The 'Use Classic Supertrend' option allows switching to a standard Supertrend display (fixed red/green) without the RSI effect.

4. Customizable Parameters

- ATR Length & ATR Factor: Define the sensitivity of the Supertrend.

- RSI Period & RSI Threshold: Allow refining the RSI filter based on market volatility.

- Classic mode: Enables/disables the RSI filtering to revert to the original Supertrend.

This indicator is especially valuable for traders looking to refine their trend signals based on market momentum measured by RSI.

This indicator is for informational purposes only and should not be considered financial advice. Trading involves risks, and past performance does not guarantee future results. Always conduct your own analysis before making any trading decisions.

BBr1 Candle Range Volitility Gap IndicatorModified Candle Range Volatility Gap Indicator

1. Useful to analyze bars body and wicks and volatility of security.

2. Added a Percentage Option - easier to analyze across different securities.

2. Added a Standard Deviation ("1 std dev= 68.2%, 2 std dev=95.4%, 3 std dev=99.7%, etc") based upon user defined lookback period.

3. Added the ability to include Gaps in Analysis. (Gaps are when the prior closing cost does not equal opening price)

4. Possible Uses setting up stop losses, trailing entries/exits (inside range or outside range).

5. Use it with other indicators in determining if to make an entry or close entry.

Reposted Original Description by © ka66 Kamal Advani

Visually shows the Body Range (open to close) and Candle Range (high to low).

Semi-transparent overlapping area is the full Candle Range, and fully-opaque smaller area is the Body Range. For aesthetics and visual consistency, Candle Range follows the direction of the Body Range, even though technically it's always positive (high - low).

The different plots for each range type also means the UI will allow deselecting one or the other as needed. For example, some strategies may care only about the Body Range, rather than the entire Candle Range, so the latter can be hidden to reduce noise.

Threshold horizontal lines are plotted, so the trader can modify these high and low levels as needed through the user interface. These need to be configured to match the instrument's price range levels for the timeframe. The defaults are pretty arbitrary for +/- 0.0080 (80 pips in a 4-decimal place forex pair). Where a range reaches or exceeds a threshold, it's visually marked as well with a shape at the Body or Candle peak, to assist with quicker visual potential setup scanning, for example, to anticipate a following reversal or continuation.

Sharpe Ratio ScreenerThe original code was created by tim_amblard , and the modifications were made by Mr_Rakun for the purpose of adapting the script into a screener format.

The Sharpe ratio is a popular metric used to measure the risk-adjusted return of an asset or portfolio, which allows traders and investors to assess whether the returns they are receiving are worth the risk they are taking. In this script, the Sharpe ratio is calculated over a 180-day period (approximately 6 months), and several valuation zones are defined based on the ratio to help assess whether an asset is overvalued, undervalued, or critically undervalued.

Key Features:

1. Risk-Free Rate Input: The user can define the risk-free rate (usually the return of government bonds or a similar safe asset) for Sharpe ratio calculation.

2. Lookback Period (180 Days): The default lookback period is set to 180 days (approximately 6 months) to calculate the mean and standard deviation of the asset’s daily returns.

3. Valuation Zones:

• Overvalued Zone: If the Sharpe ratio is greater than 5.

• Undervalued Zone: If the Sharpe ratio is between -1 and 5.

• Critically Undervalued Zone: If the Sharpe ratio is below -3.

• Neutral Zone: If the Sharpe ratio does not meet any of the above conditions.

4. Table View: The script pulls a list of symbols from the user (e.g., cryptocurrency or stock tickers) and displays their latest price, Sharpe ratio, and whether they are in an overvalued, undervalued, or neutral zone in a table format.

5. Custom Symbol Input: The user can input a list of symbols (separated by commas) to track.

6. Daily Timeframe Check: The script warns the user to ensure they are using a daily timeframe, as this indicator is designed specifically for it.

How It Works:

• The script calculates the daily returns for each symbol over the specified lookback period.

• It then calculates the mean and standard deviation of the returns to derive the Sharpe ratio.

• The Sharpe ratio is annualized, and it’s compared to the defined thresholds to categorize the symbol into different valuation zones.

• A table is generated on the chart to show the symbols, their current prices, and their Sharpe ratios, with color-coded background to easily identify whether they are overvalued (red), undervalued (green), or critically undervalued (blue).

This tool is useful for screening multiple assets for their Sharpe ratio to find investment opportunities with optimal risk-adjusted returns.

Original code credit: This code was originally written by tim_amblard and modified by Mr_Rakun for use as a screener.

Türkçe Açıklama:

Orijinal kod tim_amblard tarafından yazılmıştır ve Mr_Rakun tarafından, bu script’in tarayıcı formatına dönüştürülmesi amacıyla değiştirilmiştir.

Sharpe oranı, bir varlığın veya portföyün risk düzeltilmiş getirisini ölçmek için yaygın olarak kullanılan bir metriktir. Bu metrik, yatırımcıların aldıkları risk karşılığında aldıkları getirinin ne kadar verimli olduğunu değerlendirmelerine olanak tanır. Bu script’te, Sharpe oranı 180 günlük bir periyot (yaklaşık 6 ay) boyunca hesaplanır ve oranı baz alarak varlıkların değerleme bölgeleri tanımlanır: aşırı değerli, değerli ve kritik şekilde değersiz.

Ana Özellikler:

1. Risk-Free Rate (Risk-Free Oranı) Girişi: Kullanıcı, Sharpe oranı hesaplaması için risk-free (risksiz) oranı (genellikle devlet tahvilleri veya benzeri güvenli bir varlık getirisi) tanımlayabilir.

2. Lookback (Geribildirim) Periyodu (180 Gün): Varsayılan geribildirim periyodu, varlığın günlük getirilerinin ortalama ve standart sapmalarını hesaplamak için 180 gün (yaklaşık 6 ay) olarak ayarlanmıştır.

3. Değerleme Bölgeleri:

• Aşırı Değerli Bölge: Sharpe oranı 5’ten büyükse.

• Değerli Bölge: Sharpe oranı -1 ile 5 arasında ise.

• Kritik Derecede Değersiz Bölge: Sharpe oranı -3’ten küçükse.

• Nötr Bölge: Sharpe oranı yukarıdaki hiçbir koşulu karşılamıyorsa.

4. Tablo Görünümü: Script, kullanıcıdan alınan semboller listesine göre (örneğin, kripto para veya hisse senedi sembolleri) her bir sembolün son fiyatını, Sharpe oranını ve değerleme bölgesini tablo şeklinde gösterir.

5. Özel Sembol Girişi: Kullanıcı, izlemek istediği semboller listesini (virgülle ayrılmış) girebilir.

6. Günlük Zaman Çerçevesi Kontrolü: Script, kullanıcının doğru sonuçlar almak için günlük zaman çerçevesinde işlem yapması gerektiğini hatırlatır.

Nasıl Çalışır:

• Script, her sembol için belirtilen geribildirim periyodu boyunca günlük getirileri hesaplar.

• Ardından, getirilerin ortalama ve standart sapmasını hesaplayarak Sharpe oranını çıkarır.

• Sharpe oranı yıllıklaştırılır ve tanımlanan eşiklerle karşılaştırılarak sembol, farklı değerleme bölgelerine kategorize edilir.

• Grafik üzerinde, semboller, mevcut fiyatları ve Sharpe oranları gösteren bir tablo oluşturulur. Bu tablo, hangi sembollerin aşırı değerli (kırmızı), değerli (yeşil) veya kritik derecede değersiz (mavi) olduğunu kolayca görmek için renk kodlu arka planlar kullanır.

Bu araç, yatırım fırsatlarını daha verimli bir şekilde değerlendirebilmek için risk düzeltilmiş getiri açısından optimal fırsatları bulmak için birden fazla varlığın Sharpe oranlarını taramak için kullanışlıdır.