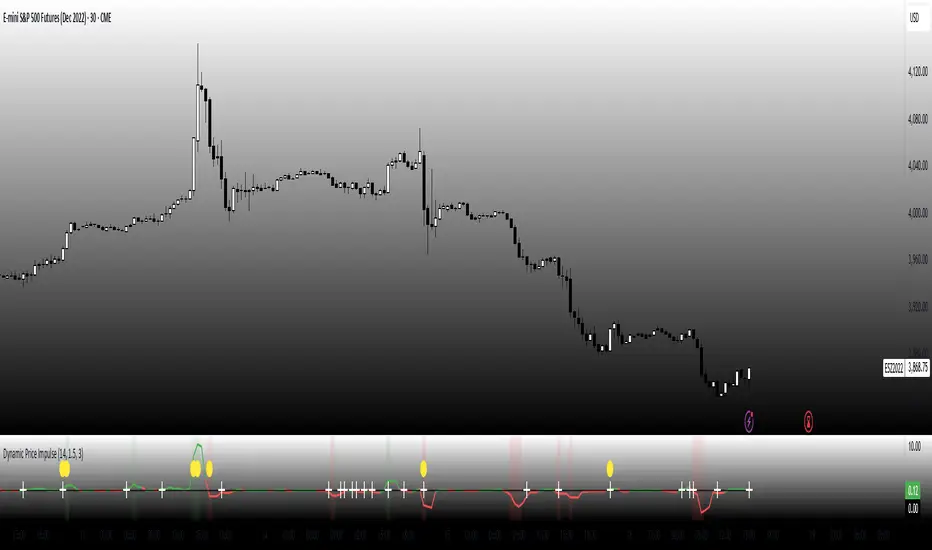

Dynamic Price ImpulseThis indicator is designed to capture price momentum without the lag typically found in traditional oscillators.

Core Mechanics

Instead of using simple price differences, the indicator normalizes changes relative to the average true range (ATR), making it adaptive to different volatility regimes.

By squaring the normalized change while preserving its sign, the indicator responds more aggressively to stronger price moves while remaining sensitive to smaller ones.

The indicator identifies periods when volatility is expanding, which often precede significant price movements.

Trading Strategy Applications

1. Momentum Signals:

o When the indicator crosses above zero, look for long entries

o When it crosses below zero, look for short entries

o The stronger the impulse (farther from zero), the stronger the signal

2. Early Trend Detection:

o Volatility expansion markers (yellow circles) often appear at the beginning of new trends

o Use these as early warning signals to prepare for potential entries

3. Trend Continuation:

o Strong readings in the direction of the trend suggest continuation

o Weakening readings suggest the trend may be losing steam

4. Counter-Trend Opportunities:

o Look for divergences between price and the indicator for potential reversals

o When price makes a new high but the indicator doesn't, consider potential shorts (and vice versa)

Fine-Tuning

• Length (14): Controls the lookback period for ATR calculation. Lower values make it more responsive but noisier.

• Threshold (1.5): Determines how much volatility needs to expand to trigger the volatility expansion signal.

• Smoothing (3): Reduces noise in the signal. Higher values reduce false signals but introduce more lag.

Volatility

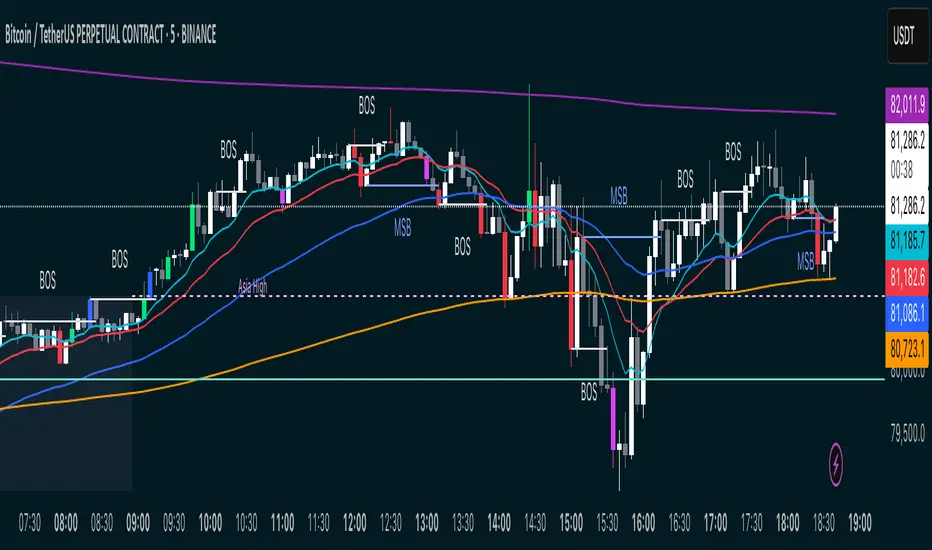

MSB BOS Market Structure [FTB]Track Market Structure Breaks (MSB) and Breaks of Structure (BOS) on your charts. This indicator does exactly that without clutter and with easy-to-spot.

🔑 Features:

MSB (Market Structure Break): Shows when price flips and breaks the previous high/low — possible start of a new trend.

BOS (Break of Structure): Highlights key structural breakouts in line with the existing trend.

✅ Pivot-Based Analysis (Body Focused)

Uses candle body-based pivot highs and lows to find clean market structure points (no wicks confusion here!).

Adjustable pivot strength — control how many candles you want on either side to define a swing.

✅ Clean Visual Markings

MSB and BOS lines with optional labels so you see exactly where breaks happen.

Customizable line style (Solid, Dashed, Dotted) to match your chart aesthetic.

Optional pivot markers to show minor swing highs/lows.

✅ Alerts Ready

Set alerts for any MSB or BOS, or filter to specific bullish/bearish breaks — never miss a key level again

💡 How to Use This Indicator:

Identify Trend Shifts: Use MSB to spot early trend reversals — when a previous structure breaks against the trend.

Catch Continuations: Watch for BOS to confirm trend continuation — great for riding the trend!

⚙️ Settings You Can Adjust:

Pivot Strength: How many candles to look back and forward for swing points (default: 3).

Show Pivots: Optional — highlight swing highs and lows for extra clarity.

FTB Smart Trader System — Market Maker Levels, EMAs & VectorsThe FTB Trade Engine is an indicator suite I built for myself as a crypto trader. It's designed specifically for trading Institution levels, EMAs, PVSRA Volume Candles, and Session Timings. It helps me spot high probability trade setups without overcomplicating things.

🔑 Features of this Indicator

📌 🔥 Key Session Levels (extend lines in settings as needed)

✅ Weekly High & Low (HOW/LOW) — Automatically plots the previous week's high and low

✅ Daily High & Low (HOD/LOD) — Marks the prior day's range

✅ Asia Session High & Low — Plots the Asian session’s high and low, helping you detect potential breakouts or fakeouts, as Asia often sets the initial high and low of the day.

✅ 50% Asia Level — Automatically calculates and displays the midpoint between Asia’s high and low, an important level for intraday trading.

📌 🔥 Advanced EMA Suite

✅ Includes 10, 20, 50, 200, and 800 EMAs — providing key zones of support, resistance, and trend direction.

👀 Good to know: the break of the 50EMA WITH a vector candle is significant for reversals.

📌 🔥 PVSRA Candles

(👀 IMPORTANT: To properly view PVSRA candles, make sure to UNCHECK all default candle settings — Color Bars, Body, Borders, and Wick — in your chart's candle settings.)

✅ Price, Volume, Support & Resistance Analysis (PVSRA) Candles — These special candles combine price action with volume analysis, color-coded to highlight areas potentially influenced by market makers, institutions, and large players. Perfect for identifying key volume zones and quickly analyzing any coin or pair without switching tools.

Candle Colors Explained:

Bullish Candles:

🟢 Green — 200% increase in volume on bullish moves (strong buyer presence).

🔵 Blue — 150% increase in bullish volume, but may also indicate fatigue or possible reversal.

⚪ White — Normal bullish volume (standard green candles).

Bearish Candles:

🔴 Red — 200% increase in bearish volume compared to the last 10 candles (strong selling).

🟣 Magenta — 150% increase in bearish volume, signaling possible continuation or exhaustion.

⚫ Gray — Normal bearish volume (standard red candles).

Triple Doji SequenceThe Triple Doji Sequence indicator helps traders identify consecutive Doji candlestick patterns, allowing them to choose between spotting single, double, or triple Dojis. A Doji is detected when the candle's body is small relative to its wicks, with either the upper or lower wick being significantly larger. Users can customize their own Doji criteria by adjusting the body size and wick dominance settings. The indicator ensures that consecutive Dojis align in the same direction before confirming a valid pattern, making it easier to identify market indecision or potential trend reversals.

When the chosen Doji sequence is detected, the indicator plots a star (*) above bearish Dojis (upper wick dominant) and below bullish Dojis (lower wick dominant). It also sends alerts when a valid sequence is confirmed at the close of the bar. This tool helps traders refine their strategy by spotting repeated Doji formations, which may indicate key turning points or continuation patterns in price action.

How to Use the Triple Doji Sequence Indicator?

Apply the Indicator:

Add the Triple Doji Sequence indicator to your TradingView chart.

It will automatically scan for Doji patterns based on your settings.

Customize Your Doji Criteria:

Adjust the body size and wick dominance settings to define what qualifies as a Doji.

Choose whether to detect single, double, or triple Doji sequences.

Interpret the Signals:

A star (*) above a candle signals a bearish Doji (upper wick dominant).

A star (*) below a candle signals a bullish Doji (lower wick dominant).

Set Up Alerts:

Enable alerts to receive notifications when a Doji sequence is confirmed at bar close.

Choose alert frequency based on your trading strategy (e.g., once per bar, once per bar close).

Use in Trading Strategy:

Doji sequences can indicate trend reversals or market indecision.

Combine this indicator with support/resistance levels, volume, or other indicators to confirm signals.

PS: Good luck in finding a Triple Doji :)

Volatility BandsThe Volatility Bands script is a custom indicator designed to help traders visualize volatility levels in the market. It calculates dynamic bands around a central moving average, providing insights into potential support and resistance levels based on recent price action.

The script calculates multiple volatility bands (u0, u1, u2, d0, d1, d2) that adjust based on recent price movements. The outer bands (u2 and d2) represent extreme volatility levels, while the inner bands (u0, u1, d0, d1) indicate more immediate support and resistance.

Look for price reactions at the band levels. A touch of the upper bands may indicate overbought conditions, while a touch of the lower bands may indicate oversold conditions.

Central Moving Average: A smoothed moving average that adapts to price changes, providing a clear trend direction.

The script has no input parameters.

Script Functions:

erf(x): Calculates the error function for a given input x. Used in the calculation of the smoothing factor for the UMA.

uma(input): Provides a smoothed average that adapts to recent price changes, reducing lag compared to traditional moving averages.

dev(input, mu): Used to calculate the volatility bands around the central moving average.

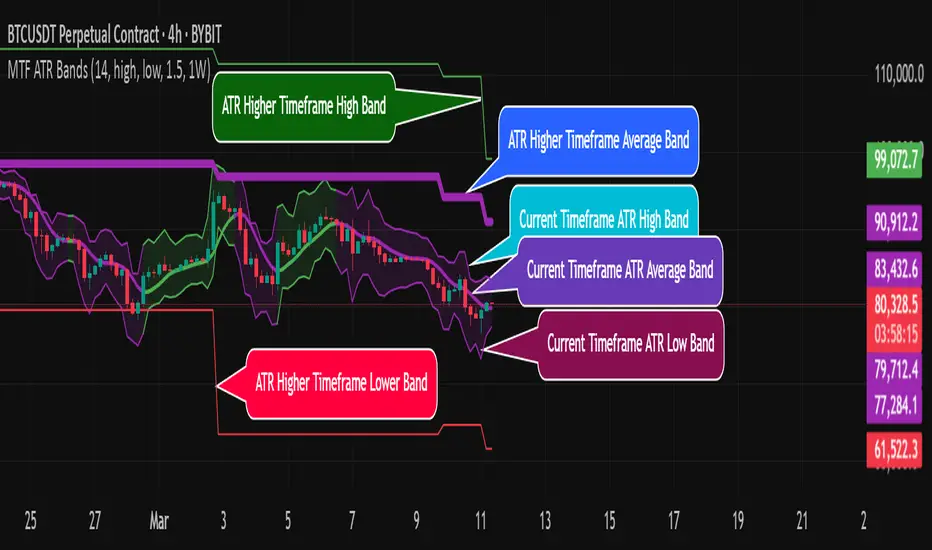

MTF ATR BandsA simple but effective MTF ATR bands indicator.

The script calculate and display ATR bands low and high of the current timeframe using high, low inputs and an RMA moving average, adding to it ATR of the period multiplied with the user multiplier, default is set to 1.5.

Than is calculated a smoothed average of the range and the color of it based on its slope, same color is used to fill the atr bands.

Than the higher timeframe bands are calculated and displayed on the chart.

How can be used ?

The higher timeframe average and bands can give you long term direction of the trend and the current timeframes moving average and filling short term trend, for example using the 15 min chart with a 4h HTF bands, or an 1h with a daily, or a daily with an weekly or weekly with bi-monthly atr bands.

Also can be used as a stop loss indicator.

Hope you will like it, any question send me a PM.

Clustering Volatility (ATR-ADR-ChaikinVol) [Sam SDF-Solutions]The Clustering Volatility indicator is designed to evaluate market volatility by combining three widely used measures: Average True Range (ATR), Average Daily Range (ADR), and the Chaikin Oscillator.

Each indicator is normalized using one of the available methods (MinMax, Rank, or Z-score) to create a unified metric called the Score. This Score is further smoothed with an Exponential Moving Average (EMA) to reduce noise and provide a clearer view of market conditions.

Key Features:

Multi-Indicator Integration: Combines ATR, ADR, and the Chaikin Oscillator into a single Score that reflects overall market volatility.

Flexible Normalization: (Supports three normalization methods)

MinMax: Scales values between the observed minimum and maximum.

Rank: Normalizes based on the relative rank within a moving window.

Z-score: Standardizes values using mean and standard deviation.

Dynamic Window Selection: Offers an automatic window selection option based on a specified lookback period, or a fixed window size can be used.

Customizable Weights: Allows the user to assign individual weights to ATR, ADR, and the Chaikin Oscillator. Optionally, weights can be normalized to sum to 1.

Score Smoothing: Applies an EMA to the computed Score to smooth out short-term fluctuations and reduce market noise.

Cluster Visualization: Divides the smoothed Score into a number of clusters, each represented by a distinct color. These colors can be applied to the price bars (if enabled) for an immediate visual indication of the current volatility regime.

How It Works:

Input & Window Setup: Users set parameters for indicator periods, normalization methods, weights, and window size. The indicator can automatically determine the analysis window based on the number of lookback days.

Calculation of Metrics: The indicator computes the ATR, ADR (as the average of bar ranges), and the Chaikin Oscillator (based on the difference between short and long EMAs of the Accumulation/Distribution line).

Normalization & Scoring: Each indicator’s value is normalized and then weighted to form a raw Score. This raw Score is scaled to a range using statistics from the chosen window.

Smoothing & Clustering: The raw Score is smoothed using an EMA. The resulting smoothed Score is then multiplied by the number of clusters to assign a cluster index, which is used to choose a color for visual signals.

Visualization: The smoothed Score is plotted on the chart with a color that changes based on its value (e.g., lime for low, red for high, yellow for intermediate values). Optionally, the price bars are colored according to the assigned cluster.

_____________

This indicator is ideal for traders seeking a quick and clear assessment of market volatility. By integrating multiple volatility measures into one comprehensive Score, it simplifies analysis and aids in making more informed trading decisions.

For more detailed instructions, please refer to the guide here:

Clustering & Divergences (RSI-Stoch-CCI) [Sam SDF-Solutions]The Clustering & Divergences (RSI-Stoch-CCI) indicator is a comprehensive technical analysis tool that consolidates three popular oscillators—Relative Strength Index (RSI), Stochastic, and Commodity Channel Index (CCI)—into one unified metric called the Score. This Score offers traders an aggregated view of market conditions, allowing them to quickly identify whether the market is oversold, balanced, or overbought.

Functionality:

Oscillator Clustering: The indicator calculates the values of RSI, Stochastic, and CCI using user-defined periods. These oscillator values are then normalized using one of three available methods: MinMax, Z-Score, or Z-Bins.

Score Calculation: Each normalized oscillator value is multiplied by its respective weight (which the user can adjust), and the weighted values are summed to generate an overall Score. This Score serves as a single, interpretable metric representing the combined oscillator behavior.

Market Clustering: The indicator performs clustering on the Score over a configurable window. By dividing the Score range into a set number of clusters (also configurable), the tool visually represents the market’s state. Each cluster is assigned a unique color so that traders can quickly see if the market is trending toward oversold, balanced, or overbought conditions.

Divergence Detection: The script automatically identifies both Regular and Hidden divergences between the price action and the Score. By using pivot detection on both price and Score data, the indicator marks potential reversal signals on the chart with labels and connecting lines. This helps in pinpointing moments when the price and the underlying oscillator dynamics diverge.

Customization Options: Users have full control over the indicator’s behavior. They can adjust:

The periods for each oscillator (RSI, Stochastic, CCI).

The weights applied to each oscillator in the Score calculation.

The normalization method and its manual boundaries.

The number of clusters and whether to invert the cluster order.

Parameters for divergence detection (such as pivot sensitivity and the minimum/maximum bar distance between pivots).

Visual Enhancements:

Depending on the user’s preference, either the Score or the Cluster Index (derived from the clustering process) is plotted on the chart. Additionally, the script changes the color of the price bars based on the identified cluster, providing an at-a-glance visual cue of the current market regime.

Logic & Methodology:

Input Parameters: The script starts by accepting user inputs for clustering settings, oscillator periods, weights, divergence detection, and manual boundary definitions for normalization.

Oscillator Calculation & Normalization: It computes RSI, Stochastic, and CCI values from the price data. These values are then normalized using either the MinMax method (scaling between a lower and upper band) or the Z-Score method (standardizing based on mean and standard deviation), or using Z-Bins for an alternative scaling approach.

Score Computation: Each normalized oscillator is multiplied by its corresponding weight. The sum of these products results in the overall Score that represents the combined oscillator behavior.

Clustering Algorithm: The Score is evaluated over a moving window to determine its minimum and maximum values. Using these values, the script calculates a cluster index that divides the Score into a predefined number of clusters. An option to invert the cluster calculation is provided to adjust the interpretation of the clustering.

Divergence Analysis: The indicator employs pivot detection (using left and right bar parameters) on both the price and the Score. It then compares recent pivot values to detect regular and hidden divergences. When a divergence is found, the script plots labels and optional connecting lines to highlight these key moments on the chart.

Plotting: Finally, based on the user’s selection, the indicator plots either the Score or the Cluster Index. It also overlays manual boundary lines (for the chosen normalization method) and adjusts the bar colors according to the cluster to provide clear visual feedback on market conditions.

_________

By integrating multiple oscillator signals into one cohesive tool, the Clustering & Divergences (RSI-Stoch-CCI) indicator helps traders minimize subjective analysis. Its dynamic clustering and automated divergence detection provide a streamlined method for assessing market conditions and potentially enhancing the accuracy of trading decisions.

For further details on using this indicator, please refer to the guide available at:

AI Adaptive Oscillator [PhenLabs]📊 Algorithmic Adaptive Oscillator

Version: PineScript™ v6

📌 Description

The AI Adaptive Oscillator is a sophisticated technical indicator that employs ensemble learning and adaptive weighting techniques to analyze market conditions. This innovative oscillator combines multiple traditional technical indicators through an AI-driven approach that continuously evaluates and adjusts component weights based on historical performance. By integrating statistical modeling with machine learning principles, the indicator adapts to changing market dynamics, providing traders with a responsive and reliable tool for market analysis.

🚀 Points of Innovation:

Ensemble learning framework with adaptive component weighting

Performance-based scoring system using directional accuracy

Dynamic volatility-adjusted smoothing mechanism

Intelligent signal filtering with cooldown and magnitude requirements

Signal confidence levels based on multi-factor analysis

🔧 Core Components

Ensemble Framework : Combines up to five technical indicators with performance-weighted integration

Adaptive Weighting : Continuous performance evaluation with automated weight adjustment

Volatility-Based Smoothing : Adapts sensitivity based on current market volatility

Pattern Recognition : Identifies potential reversal patterns with signal qualification criteria

Dynamic Visualization : Professional color schemes with gradient intensity representation

Signal Confidence : Three-tiered confidence assessment for trading signals

🔥 Key Features

The indicator provides comprehensive market analysis through:

Multi-Component Ensemble : Integrates RSI, CCI, Stochastic, MACD, and Volume-weighted momentum

Performance Scoring : Evaluates each component based on directional prediction accuracy

Adaptive Smoothing : Automatically adjusts based on market volatility

Pattern Detection : Identifies potential reversal patterns in overbought/oversold conditions

Signal Filtering : Prevents excessive signals through cooldown periods and minimum change requirements

Confidence Assessment : Displays signal strength through intuitive confidence indicators (average, above average, excellent)

🎨 Visualization

Gradient-Filled Oscillator : Color intensity reflects strength of market movement

Clear Signal Markers : Distinct bullish and bearish pattern signals with confidence indicators

Range Visualization : Clean representation of oscillator values from -6 to 6

Zero Line : Clear demarcation between bullish and bearish territory

Customizable Colors : Color schemes that can be adjusted to match your chart style

Confidence Symbols : Intuitive display of signal confidence (no symbol, +, or ++) alongside direction markers

📖 Usage Guidelines

⚙️ Settings Guide

Color Settings

Bullish Color

Default: #2b62fa (Blue)

This setting controls the color representation for bullish movements in the oscillator. The color appears when the oscillator value is positive (above zero), with intensity indicating the strength of the bullish momentum. A brighter shade indicates stronger bullish pressure.

Bearish Color

Default: #ce9851 (Amber)

This setting determines the color representation for bearish movements in the oscillator. The color appears when the oscillator value is negative (below zero), with intensity reflecting the strength of the bearish momentum. A more saturated shade indicates stronger bearish pressure.

Signal Settings

Signal Cooldown (bars)

Default: 10

Range: 1-50

This parameter sets the minimum number of bars that must pass before a new signal of the same type can be generated. Higher values reduce signal frequency and help prevent overtrading during choppy market conditions. Lower values increase signal sensitivity but may generate more false positives.

Min Change For New Signal

Default: 1.5

Range: 0.5-3.0

This setting defines the minimum required change in oscillator value between consecutive signals of the same type. It ensures that new signals represent meaningful changes in market conditions rather than minor fluctuations. Higher values produce fewer but potentially higher-quality signals, while lower values increase signal frequency.

AI Core Settings

Base Length

Default: 14

Minimum: 2

This fundamental setting determines the primary calculation period for all technical components in the ensemble (RSI, CCI, Stochastic, etc.). It represents the lookback window for each component’s base calculation. Shorter periods create a more responsive but potentially noisier oscillator, while longer periods produce smoother signals with potential lag.

Adaptive Speed

Default: 0.1

Range: 0.01-0.3

Controls how quickly the oscillator adapts to new market conditions through its volatility-adjusted smoothing mechanism. Higher values make the oscillator more responsive to recent price action but potentially more erratic. Lower values create smoother transitions but may lag during rapid market changes. This parameter directly influences the indicator’s adaptiveness to market volatility.

Learning Lookback Period

Default: 150

Minimum: 10

Determines the historical data range used to evaluate each ensemble component’s performance and calculate adaptive weights. This setting controls how far back the AI “learns” from past performance to optimize current signals. Longer periods provide more stable weight distribution but may be slower to adapt to regime changes. Shorter periods adapt more quickly but may overreact to recent anomalies.

Ensemble Size

Default: 5

Range: 2-5

Specifies how many technical components to include in the ensemble calculation.

Understanding The Interaction Between Settings

Base Length and Learning Lookback : The base length determines the reactivity of individual components, while the lookback period determines how their weights are adjusted. These should be balanced according to your timeframe - shorter timeframes benefit from shorter base lengths, while the lookback should generally be 10-15 times the base length for optimal learning.

Adaptive Speed and Signal Cooldown : These settings control sensitivity from different angles. Increasing adaptive speed makes the oscillator more responsive, while reducing signal cooldown increases signal frequency. For conservative trading, keep adaptive speed low and cooldown high; for aggressive trading, do the opposite.

Ensemble Size and Min Change : Larger ensembles provide more stable signals, allowing for a lower minimum change threshold. Smaller ensembles might benefit from a higher threshold to filter out noise.

Understanding Signal Confidence Levels

The indicator provides three distinct confidence levels for both bullish and bearish signals:

Average Confidence (▲ or ▼) : Basic signal that meets the minimum pattern and filtering criteria. These signals indicate potential reversals but with moderate confidence in the prediction. Consider using these as initial alerts that may require additional confirmation.

Above Average Confidence (▲+ or ▼+) : Higher reliability signal with stronger underlying metrics. These signals demonstrate greater consensus among the ensemble components and/or stronger historical performance. They offer increased probability of successful reversals and can be traded with less additional confirmation.

Excellent Confidence (▲++ or ▼++) : Highest quality signals with exceptional underlying metrics. These signals show strong agreement across oscillator components, excellent historical performance, and optimal signal strength. These represent the indicator’s highest conviction trade opportunities and can be prioritized in your trading decisions.

Confidence assessment is calculated through a multi-factor analysis including:

Historical performance of ensemble components

Degree of agreement between different oscillator components

Relative strength of the signal compared to historical thresholds

✅ Best Use Cases:

Identify potential market reversals through oscillator extremes

Filter trade signals based on AI-evaluated component weights

Monitor changing market conditions through oscillator direction and intensity

Confirm trade signals from other indicators with adaptive ensemble validation

Detect early momentum shifts through pattern recognition

Prioritize trading opportunities based on signal confidence levels

Adjust position sizing according to signal confidence (larger for ++ signals, smaller for standard signals)

⚠️ Limitations

Requires sufficient historical data for accurate performance scoring

Ensemble weights may lag during dramatic market condition changes

Higher ensemble sizes require more computational resources

Performance evaluation quality depends on the learning lookback period length

Even high confidence signals should be considered within broader market context

💡 What Makes This Unique

Adaptive Intelligence : Continuously adjusts component weights based on actual performance

Ensemble Methodology : Combines strength of multiple indicators while minimizing individual weaknesses

Volatility-Adjusted Smoothing : Provides appropriate sensitivity across different market conditions

Performance-Based Learning : Utilizes historical accuracy to improve future predictions

Intelligent Signal Filtering : Reduces noise and false signals through sophisticated filtering criteria

Multi-Level Confidence Assessment : Delivers nuanced signal quality information for optimized trading decisions

🔬 How It Works

The indicator processes market data through five main components:

Ensemble Component Calculation :

Normalizes traditional indicators to consistent scale

Includes RSI, CCI, Stochastic, MACD, and volume components

Adapts based on the selected ensemble size

Performance Evaluation :

Analyzes directional accuracy of each component

Calculates continuous performance scores

Determines adaptive component weights

Oscillator Integration :

Combines weighted components into unified oscillator

Applies volatility-based adaptive smoothing

Scales final values to -6 to 6 range

Signal Generation :

Detects potential reversal patterns

Applies cooldown and magnitude filters

Generates clear visual markers for qualified signals

Confidence Assessment :

Evaluates component agreement, historical accuracy, and signal strength

Classifies signals into three confidence tiers (average, above average, excellent)

Displays intuitive confidence indicators (no symbol, +, ++) alongside direction markers

💡 Note:

The AI Adaptive Oscillator performs optimally when used with appropriate timeframe selection and complementary indicators. Its adaptive nature makes it particularly valuable during changing market conditions, where traditional fixed-weight indicators often lose effectiveness. The ensemble approach provides a more robust analysis by leveraging the collective intelligence of multiple technical methodologies. Pay special attention to the signal confidence indicators to optimize your trading decisions - excellent (++) signals often represent the most reliable trade opportunities.

IU Gap Fill StrategyThe IU Gap Fill Strategy is designed to capitalize on price gaps that occur between trading sessions. It identifies gaps based on a user-defined percentage threshold and executes trades when the price fills the gap within a day. This strategy is ideal for traders looking to take advantage of market inefficiencies that arise due to overnight or session-based price movements. An ATR-based trailing stop-loss is incorporated to dynamically manage risk and lock in profits.

USER INPUTS

Percentage Difference for Valid Gap - Defines the minimum gap size in percentage terms for a valid trade setup. ( Default is 0.2 )

ATR Length - Sets the lookback period for the Average True Range (ATR) calculation. (default is 14 )

ATR Factor - Determines the multiplier for the trailing stop-loss, helping in risk management. ( Default is 2.00 )

LONG CONDITION

A gap-up occurs, meaning the current session opens above the previous session’s close.

The price initially dips below the previous session's close but then recovers and closes above it.

The gap meets the valid percentage threshold set by the user.

The bar is not the first or last bar of the session to avoid false signals.

SHORT CONDITION

A gap-down occurs, meaning the current session opens below the previous session’s close.

The price initially moves above the previous session’s close but then closes below it.

The gap meets the valid percentage threshold set by the user.

The bar is not the first or last bar of the session to avoid false signals.

LONG EXIT

An ATR-based trailing stop-loss is set below the entry price and dynamically adjusts upwards as the price moves in favor of the trade.

The position is closed when the trailing stop-loss is hit.

SHORT EXIT

An ATR-based trailing stop-loss is set above the entry price and dynamically adjusts downwards as the price moves in favor of the trade.

The position is closed when the trailing stop-loss is hit.

WHY IT IS UNIQUE

Precision in Identifying Gaps - The strategy focuses on real price gaps rather than minor fluctuations.

Dynamic Risk Management - Uses ATR-based trailing stop-loss to secure profits while allowing the trade to run.

Versatility - Works on stocks, indices, forex, and any market that experiences session-based gaps.

Optimized Entry Conditions - Ensures entries are taken only when the price attempts to fill the gap, reducing false signals.

HOW USERS CAN BENEFIT FROM IT

Enhance Trade Timing - Captures high-probability trade setups based on market inefficiencies caused by gaps.

Minimize Risk - The ATR trailing stop-loss helps protect gains and limit losses.

Works in Different Market Conditions - Whether markets are trending or consolidating, the strategy adapts to potential gap fill opportunities.

Fully Customizable - Users can fine-tune gap percentage, ATR settings, and stop-loss parameters to match their trading style.

Liquidity Market Seeking SwiftEdgeThis indicator is designed to identify potential liquidity levels on the chart by detecting swing highs and lows, which are often areas where stop-loss orders or significant orders accumulate. It visualizes these levels with horizontal lines and labels on the right side of the chart, color-coded based on volume to help traders understand where the market might seek liquidity.

How It Works

Swing Highs and Lows: The indicator uses the ta.pivothigh and ta.pivotlow functions to identify significant swing points over a user-defined lookback period (Swing Length). These points are considered potential liquidity levels where stop-loss orders might be placed.

Volume Analysis: The indicator compares the volume at each swing point to the average volume over a specified period (Volume Average Length). Levels with above-average volume are colored red, indicating higher liquidity, while levels with below-average volume are colored green.

Liquidity Visualization: Horizontal dashed lines are drawn at each identified level, extending across the chart. Labels on the right side display the estimated liquidity amount (simulated based on volume and a multiplier, Volume Multiplier for Liquidity).

Sell Signal: A "SELL NOW" label appears when the price approaches a liquidity level after an uptrend (detected using a simple moving average crossover). This suggests a potential reversal as the market may target liquidity at that level.

Strategy Concept: Market Seeking Liquidity

The indicator is based on the concept that markets often move toward areas of high liquidity, such as clusters of stop-loss orders or significant order accumulations. These liquidity pools are typically found around swing highs and lows, where traders place their stop-losses or large orders. By identifying these levels and highlighting those with higher volume (red lines), the indicator aims to show where the market might move to "grab" this liquidity. For example, after an uptrend, the market may reverse at a swing high to take out stop-losses above that level, providing liquidity for larger players to enter or exit positions.

Settings

Swing Length: The number of bars to look back for detecting swing highs and lows. Default is 20.

Liquidity Threshold: The price threshold for merging nearby levels to avoid duplicates. Default is 0.001.

Volume Average Length: The period for calculating the average volume to compare against. Default is 20.

Volume Multiplier for Liquidity: A multiplier to scale the volume into a simulated liquidity amount (displayed as "K"). Default is 1000.

Usage Notes

Use this indicator on any timeframe, though it may be more effective on higher timeframes (e.g., 1H, 4H) where swing points are more significant.

Red lines indicate levels with higher volume, suggesting stronger liquidity pools that the market might target.

Green lines indicate levels with lower volume, which may be less significant.

The "SELL NOW" signal is a basic example of how to use liquidity levels for trading decisions. It appears when the price approaches a liquidity level after an uptrend, but it should be used in conjunction with other analysis.

Adjust the Volume Multiplier for Liquidity to scale the displayed liquidity amounts based on your instrument (e.g., forex pairs may need a higher multiplier than indices).

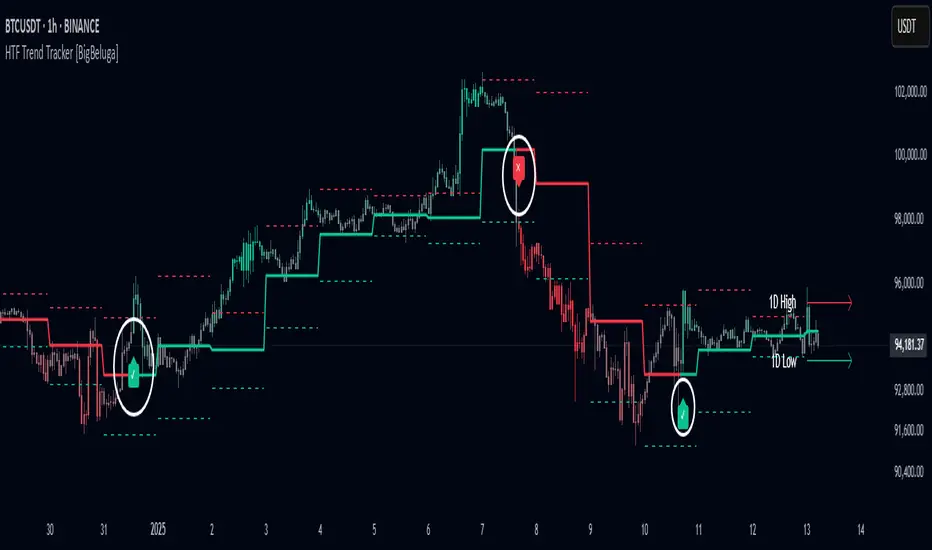

HTF Trend Tracker [BigBeluga]HTF Trend Tracker is a higher timeframe (HTF) trend tracking indicator designed to help traders identify significant trends, key levels, and market sentiment. The indicator dynamically adapts to the current price action, using HTF highs and lows to display trend direction and strength with detailed visuals.

🔵 Key Features:

Dynamic Trend Detection:

Uptrend is identified when the price closes above the HTF high.

Downtrend is detected when the price closes below the HTF low.

Midline changes color dynamically based on the trend direction:

Bullish Green: Indicates an uptrend.

Bearish Red: Indicates a downtrend.

Historical and Active HTF Levels:

Historic HTF highs and lows are displayed as dotted lines.

Current active HTF high and low levels are shown as solid lines.

Timeframe labels (e.g., "1D High" or "1D Low") mark the active levels for clarity.

Trend Change Signals:

A green checkmark (✓) is plotted when an uptrend starts.

A red cross (✕) appears when a downtrend begins.

Trend-Based Candle Coloring:

Candle colors change dynamically based on the trend and the price's distance from the midline:

Intense Bullish Green: Price is far above the midline during an uptrend.

Intense Bearish Red: Price is far below the midline during a downtrend.

Neutral Gray: Price is near the midline.

Users can customize the colors to suit their preferences.

🔵 Usage:

Identify uptrends and downtrends using the midline's color and the position of the close relative to the HTF levels.

Use solid lines and timeframe labels to track current HTF high and low levels.

Observe dotted lines for historical HTF levels to understand past price behavior.

Watch for checkmark (✓) and cross (✕) signals to spot trend changes and key market shifts.

Monitor candle colors to gauge trend intensity and proximity to the midline:

Intense colors signal strong trends, while neutral gray indicates consolidation near the midline.

HTF Trend Tracker is an essential tool for traders aiming to follow higher timeframe trends, identify key levels, and make data-driven decisions based on price dynamics and trend strength. Its customizable features allow for flexible integration into any trading strategy.

Ehlers Instantaneous Trendline ATR LevelsOverview

This sophisticated technical analysis tool merges John Ehlers' cutting-edge Instantaneous Trendline methodology with a dynamic ATR-based bands system. The indicator is designed to provide traders with a comprehensive view of market trends while accounting for volatility, making it suitable for both trending and ranging markets. Works on all timeframes and chart types.

Key Features in Detail

1. Ehlers Instantaneous Trendline Implementation

- Advanced algorithm that reduces lag typically associated with moving averages

- Built-in volatility filtering system to minimize false signals

- Adaptive to market conditions through dynamic calculations

- Real-time trend direction identification

2. Multi-layered ATR Band System

- Hierarchical band structure with 18 total bands (9 upper, 9 lower)

- Color-coded visualization system:

Upper bands: Red gradient (darker = further from trendline)

Lower bands: Green gradient (darker = further from trendline)

Central trendline: Yellow for optimal visibility

- Customizable multipliers for each band level

- Independent visibility controls for each band

Configuration Options

Trendline Settings:

- Lower values: More responsive to price changes and faster reacting to break in ATR filter

- Higher values: Smoother trendline with less noise and slower reacting to break in ATR filter

ATR Configuration:

Period: Customizable from 1 to any positive integer

- Longer periods: More stable volatility measurement

- Shorter periods: More reactive to recent volatility changes

Filter Multiplier: Fine-tune volatility filtering

- Higher values: More filtered signals leading to less shift in bands

- Lower values: More sensitive to price movements leading to more band shifts

Practical Applications

1. Trend Analysis

Use the central trendline for primary trend direction

Monitor band crossovers for trend strength confirmation

Track price position relative to bands for trend context

2. Volatility Assessment

Band spacing indicates current market volatility

Width between bands helps identify consolidation vs. expansion phases

Price Extremes

3. Support and Resistance

Each band acts as a dynamic support/resistance level

Multiple timeframe analysis possible adjusting for different timeframe ATR

TJR SEEK AND DESTROYTJR SEEK AND DESTROY – Intraday ICT Trading Tool

Built for day traders, TJR SEEK AND DESTROY combines Smart Money concepts like order blocks, fair value gaps, and liquidity sweeps with structure breaks and daily bias to pinpoint high-probability trades during US market hours (9:30–16:00). Ideal for scalping or intraday strategies on stocks, futures, or forex.

What Makes It Unique?

Unlike standalone ICT indicators, this script integrates:

Order Blocks with volume and range filters for precise support/resistance zones.

Fair Value Gaps (FVG) to spot pre-market price imbalances.

Break of Structure (BOS) and Liquidity Sweeps for trend and reversal signals.

A 1H MA-based Bias to align trades with the day’s direction.

BUY/SELL Labels triggered only when bias, BOS, and sweeps align, reducing noise.

How Does It Work?

Order Blocks: Marks zones with high volume (>1.5x 20-period SMA) and low range (<0.5x ATR20) as teal boxes—potential reversal points.

Fair Value Gap: Compares the prior day’s close to the current open (pre- or post-9:30), shown as a purple line and label (e.g., "FVG: 0.005").

Pivot Point: Calculates (prevHigh + prevLow + prevClose) / 3 from the prior day, plotted as an orange line for equilibrium.

Break of Structure: Detects crossovers of 5-bar highs/lows (gray lines), marked with red triangles.

Liquidity Sweeps: Tracks breaches of the prior day’s high/low (yellow lines), marked with yellow triangles.

Daily Bias: Uses 1H close vs. 20-period MA (blue line) for bullish (green background), bearish (red), or neutral (gray) context.

Signals: BUY (green label) when bias is bullish, price breaks up, and sweeps the prior high; SELL (red label) when bias is bearish, price breaks down, and sweeps the prior low.

How to Use It

Setup: Apply to 1M–15M charts for US session trading (9:30–16:00 EST).

Trading:

Wait for a BUY label after a yellow sweep triangle above the prior day’s high in a green (bullish) background.

Wait for a SELL label after a yellow sweep triangle below the prior day’s low in a red (bearish) background.

Use order blocks (teal boxes) as support/resistance for stop-loss or take-profit.

Markets: Best for SPY, ES futures, or forex pairs with US session volatility.

Underlying Concepts

Order Blocks: High-volume, low-range bars suggest institutional activity.

FVG: Gaps between close and open indicate imbalance to be filled.

BOS & Sweeps: Price breaking key levels signals momentum or stop-hunting.

Bias: 1H MA filters trades by broader trend.

Chart Setup

Displays order blocks (teal boxes), pivot (orange), open (purple), bias (colored background), BOS/sweeps (triangles), and signals (labels). Keep other indicators off for clarity.

BBVOL SwiftEdgeBBVOL SwiftEdge – Precision Scalping with Volume and Trend Filtering

Optimized for scalping and short-term trading on fast-moving markets (e.g., 1-minute charts), BBVOL SwiftEdge combines Bollinger Bands, Heikin Ashi smoothing, volume momentum, and EMA trend alignment to deliver actionable buy/sell signals with visual trend cues. Ideal for forex, crypto, and stocks.

What Makes BBVOL SwiftEdge Unique?

Unlike traditional Bollinger Bands scripts that focus solely on price volatility, BBVOL SwiftEdge enhances signal precision by:

Using Heikin Ashi to filter out noise and confirm trend direction, reducing false signals in choppy markets.

Incorporating volume analysis to ensure signals align with significant buying or selling pressure (customizable thresholds).

Adding an EMA overlay to keep trades in sync with the short-term trend.

Coloring candlesticks (green for bullish, red for bearish, purple for consolidation) to visually highlight market conditions at a glance.

How Does It Work?

Buy Signal: Triggers when price crosses above the lower Bollinger Band, Heikin Ashi shows bullish momentum (close > open), buy volume exceeds your set threshold (default 30%), and price is above the EMA. A green triangle appears below the candle.

Sell Signal: Triggers when price crosses below the upper Bollinger Band, Heikin Ashi turns bearish (close < open), sell volume exceeds the threshold (default 30%), and price is below the EMA. A red triangle appears above the candle.

Trend Visualization: Candles turn green when price is significantly above the Bollinger Bands’ basis (indicating a bullish trend), red when below (bearish trend), or purple when near the basis (consolidation), based on a customizable threshold (default 10% of BB width).

Risk Management: Each signal calculates a stop-loss (10% beyond the opposite band) and take-profit (opposite band), plotted for reference.

How to Use It

Timeframe: Best on 1-minute to 5-minute charts for scalping; test higher timeframes for swing trading.

Markets: Works well in volatile markets like forex pairs (e.g., EUR/USD), crypto (e.g., BTC/USD), or liquid stocks.

Customization: Adjust Bollinger Bands length (default 10), multiplier (default 1.2), volume thresholds (default 30%), EMA length (default 3), and consolidation threshold (default 0.1%) to match your strategy.

Interpretation: Look for green/red triangles as entry signals, confirmed by candle colors. Purple candles suggest caution—wait for a breakout. Use stop-loss/take-profit levels for trade management.

Underlying Concepts

Bollinger Bands: Measures volatility and identifies overbought/oversold zones.

Heikin Ashi: Smooths price action to emphasize trend direction.

Volume Momentum: Calculates cumulative buy/sell volume percentages to confirm market strength (e.g., buyVolPercent = buyVolume / totalVolume * 100).

EMA: A fast-moving average (default length 3) ensures signals align with the immediate trend.

Chart Setup

The chart displays Bollinger Bands (orange), Heikin Ashi close (green circles), EMA (purple), and volume-scaled lines (lime/red). Signals are marked with triangles, and candle colors reflect trend state. Keep the chart clean by focusing on these outputs for clarity.

VIX/VIX3M Ratio計算並顯示 CBOE:VIX 和 CBOE:VIX3M 的比率,幫助交易者評估市場的波動性。

當比率超過設定的高水平或低於低水平時,指標將顯示為紅色,提示潛在的市場異常情況。

Calculates and displays the ratio of CBOE:VIX to CBOE:VIX3M, helping traders assess market volatility.

When the ratio exceeds the set high level or falls below the low level, the indicator will be displayed in red, signaling potential market anomalies.

Bollinger Bands + Supertrend by XoediacBollinger Bands with Supertrend Indicator by Xeodiac

This script combines two powerful technical analysis tools — Bollinger Bands and the Supertrend Indicator — to provide traders with a comprehensive view of market volatility and trend direction.

Bollinger Bands: These bands consist of a middle band (the simple moving average, or SMA) and two outer bands (calculated as standard deviations away from the middle). The upper and lower bands act as dynamic support and resistance levels, expanding during high volatility and contracting during low volatility.

Supertrend Indicator: The Supertrend is a trend-following indicator that uses the Average True Range (ATR) to calculate an adaptive threshold, indicating whether the market is in an uptrend or downtrend. The indicator changes color based on the trend direction, providing clear buy and sell signals.

Features of the Script:

Volatility-based Signals : By incorporating the Bollinger Bands, the script adjusts to market volatility. Traders can identify periods of high and low volatility, helping to gauge potential price breakouts or reversals.

Trend Confirmation: The Supertrend helps confirm the trend direction, ensuring that trades are aligned with the overall market trend. Green Supertrend signals indicate an uptrend, while red signals indicate a downtrend.

Enhanced Decision-making: By using both indicators together, traders can make more informed decisions. For instance, buying opportunities are validated when the price is near the lower Bollinger Band, and the Supertrend is in a bullish phase, and vice versa for selling.

Customizable Parameters: The script allows users to customize the settings for both the Bollinger Bands and the Supertrend, enabling fine-tuning based on trading preferences or market conditions.

Ideal Use Cases:

Identifying trend reversals or continuation patterns in trending markets.

Monitoring price action during periods of low volatility for breakout opportunities.

Filtering out false signals by combining volatility with trend strength.

ReadyFor401ks Just Tell Me When!ReadyFor401ks Just Tell Me When!

LET ME START BY SAYING. NO INDICATOR WILL HELP YOU NAIL THE PERFECT ENTRY/EXIT ON A TRADE. YOU SHOULD ALWAYS EDUCATE YOURSELF AND HAVE A BASIC UNDERSTANDING OF INVESTING, TRADING, CHART ANALYSIS, AND THE RISKS INVOLVED WITH. THAT BEING SAID, WITH THE RIGHT ADJUSTMENTS, IT'S PRETTY D*$N CLOSE TO PERFECTION!

This indicator is designed to help traders identify t rend direction, continuation signals, and potential exits based on a dynamic blend of moving averages, ATR bands, and price action filters. Whether you’re an intraday trader scalping the 5-minute chart or a swing trader analyzing the weekly timeframe for LEAPS , this tool provides a clear, rule-based system to help guide your trading decisions.

⸻

Key Features & Benefits

🔹 Customizable Trend Power (Baseline) Calculation

• Choose from JMA, EMA, HMA, TEMA, DEMA, SMA, VAMA, and WMA for defining your baseline trend direction.

• The baseline helps confirm whether the market is in a bullish or bearish phase.

🔹 ATR-Based Trend Continuation & Volatility Measurement

• ATR bands dynamically adjust to market conditions, helping you spot breakouts and fakeouts.

• The indicator detects when price violates ATR range , which often signals impulse moves.

🔹 Clear Entry & Exit Signals

• Uses a Continuation MA (SSL2) to confirm trends.

• Includes a separate Exit MA (SSL3) that provides crossover signals to indicate when to exit trades or reverse positions .

• Plots trend continuation circles when ATR conditions align with trend signals.

🔹 Keltner Channel Baseline for Market Structure

• A modified Keltner Channel is integrated into the baseline to help filter out choppy conditions .

• If price remains inside the baseline, the market is in consolidation , while breakouts beyond the bands indicate strong trends .

🔹 Adaptive Color Coding for Market Conditions

• Bars change color based on momentum, making trend direction easy to read.

• Green = Bullish Trend, Red = Bearish Trend, Gray = Neutral/Chop.

🔹 Flexible Alerts for Trade Management

• Get real-time alerts when the Exit MA crosses price , helping you l ock in profits or switch directions .

⸻

How to Use This Indicator for Different Trading Styles

🟢 For Intraday Trading (5-Minute Chart Setup)

• Faster MA settings help react quickly to momentum shifts.

• Ideal for scalping breakouts, trend continuation setups, and intraday reversals.

• Watch for ATR violations and price interacting with the baseline/Keltner Channel for entries.

--------------------------------

My Settings for Intraday Trading on 5min Chart

ATR Period: 15

ATR Multi: 1

ATR Smoothing: WMA

Trend Power based off of: JMA

Trend Power Period: 30

Continuation Type: JMA

Continuation Length: 20

Calculate Exit of what MA?: HMA

Calculate Exit off what Period? 30

Source of Exit Calculation: close

JMA Phase *APPLIES TO JMA ONLY: 3

JMA Power *APPLIES TO JMA ONLY: 3

Volatility Lookback Period *APPLIES TO VAMA ONLY 30

Use True Range for Channel? Checked

Base Channel Multiplier: 0.4

ATR Continuation Criteria: 1.1

----------------------------------

🔵 For Swing Trading & LEAPS (Weekly Chart Setup - Default Settings)

• Slower MAs provide a broader view of trend structure.

• Helps capture multi-week trend shifts and confirm entry points for longer-term trades.

• Weekly ATR bands highlight when stocks are entering overextended conditions.

💡 Example:

Let’s say you’re looking at TSLA on a Weekly Chart using the default settings. You notice that price crosses above the continuation MA (SSL2) while remaining above the baseline (trend power MA). The bar turns green, and price breaks above ATR resistance, signaling a strong bullish continuation. This could be a great opportunity to enter a long-term swing trade or LEAPS options position.

On the flip side, if price reverses below the Exit MA (SSL3) and turns red while breaking the lower ATR band, it might signal a good time to exit longs or enter a short trade.

⸻

Final Thoughts

The ReadyFor401ks Just Tell Me When! indicator is an all-in-one trading system that simplifies trend-following, volatility measurement, and trade management. By integrating multiple moving average types, ATR filters, and clear visual cues, it allows traders to stay disciplined and remove emotions from their trading decisions.

✅ Perfect for scalpers, day traders, and swing traders alike!

🔔 Set up alerts for automated trade signals and never miss a key move!

💬 If you find this indicator useful, leave a comment and share how you use it in your trading! 🚀

Range%This indicator displays the range of each candle i.e. High minus Low as a percentage of the previous closing price. It does not account for gaps, making it particularly useful for intraday trading. By tracking the volatility cycle of candles, this indicator helps identify periods of increased or decreased market volatility, allowing traders to pinpoint the best days to execute trades.

If the Range% is below low line candles will turn White and If Range% is above the High Line Candles will turn Red.

Dual SuperTrend w VIX Filter - Strategy [presentTrading]Hey everyone! Haven't been here for a long time. Been so busy again in the past 2 months. I recently started working on analyzing the combination of trend strategy and VIX, but didn't get outstanding results after a few tries. Sharing this tool with all of you in case you have better insights.

█ Introduction and How it is Different

The Dual SuperTrend with VIX Filter Strategy combines traditional trend following with market volatility analysis. Unlike conventional SuperTrend strategies that focus solely on price action, this experimental system incorporates VIX (Volatility Index) as an adaptive filter to create a more context-aware trading approach. By analyzing where current volatility stands relative to historical norms, the strategy adjusts to different market environments rather than applying uniform logic across all conditions.

BTCUSD 6hr Long Short Performance

█ Strategy, How it Works: Detailed Explanation

🔶 Dual SuperTrend Core

The strategy uses two SuperTrend indicators with different sensitivity settings:

- SuperTrend 1: Length = 13, Multiplier = 3.5

- SuperTrend 2: Length = 8, Multiplier = 5.0

The SuperTrend calculation follows this process:

1. ATR = Average of max(High-Low, |High-PreviousClose|, |Low-PreviousClose|) over 'length' periods

2. UpperBand = (High+Low)/2 - (Multiplier * ATR)

3. LowerBand = (High+Low)/2 + (Multiplier * ATR)

Trend direction is determined by:

- If Close > previous LowerBand, Trend = Bullish (1)

- If Close < previous UpperBand, Trend = Bearish (-1)

- Otherwise, Trend = previous Trend

🔶 VIX Analysis Framework

The core innovation lies in the VIX analysis system:

1. Statistical Analysis:

- VIX Mean = SMA(VIX, 252)

- VIX Standard Deviation = StdDev(VIX, 252)

- VIX Z-Score = (Current VIX - VIX Mean) / VIX StdDev

2. **Volatility Bands:

- Upper Band 1 = VIX Mean + (2 * VIX StdDev)

- Upper Band 2 = VIX Mean + (3 * VIX StdDev)

- Lower Band 1 = VIX Mean - (2 * VIX StdDev)

- Lower Band 2 = VIX Mean - (3 * VIX StdDev)

3. Volatility Regimes:

- "Very Low Volatility": VIX < Lower Band 1

- "Low Volatility": Lower Band 1 ≤ VIX < Mean

- "Normal Volatility": Mean ≤ VIX < Upper Band 1

- "High Volatility": Upper Band 1 ≤ VIX < Upper Band 2

- "Extreme Volatility": VIX ≥ Upper Band 2

4. VIX Trend Detection:

- VIX EMA = EMA(VIX, 10)

- VIX Rising = VIX > VIX EMA

- VIX Falling = VIX < VIX EMA

Local performance:

🔶 Entry Logic Integration

The strategy combines trend signals with volatility filtering:

Long Entry Condition:

- Both SuperTrend 1 AND SuperTrend 2 must be bullish (trend = 1)

- AND selected VIX filter condition must be satisfied

Short Entry Condition:

- Both SuperTrend 1 AND SuperTrend 2 must be bearish (trend = -1)

- AND selected VIX filter condition must be satisfied

Available VIX filter rules include:

- "Below Mean + SD": VIX < Lower Band 1

- "Below Mean": VIX < VIX Mean

- "Above Mean": VIX > VIX Mean

- "Above Mean + SD": VIX > Upper Band 1

- "Falling VIX": VIX < VIX EMA

- "Rising VIX": VIX > VIX EMA

- "Any": No VIX filtering

█ Trade Direction

The strategy allows testing in three modes:

1. **Long Only:** Test volatility effects on uptrends only

2. **Short Only:** Examine volatility's impact on downtrends only

3. **Both (Default):** Compare how volatility affects both trend directions

This enables comparative analysis of how volatility regimes impact bullish versus bearish markets differently.

█ Usage

Use this strategy as an experimental framework:

1. Form a hypothesis about how volatility affects trend reliability

2. Configure VIX filters to test your specific hypothesis

3. Analyze performance across different volatility regimes

4. Compare results between uptrends and downtrends

5. Refine your volatility filtering approach based on results

6. Share your findings with the trading community

This framework allows you to investigate questions like:

- Are uptrends more reliable during rising or falling volatility?

- Do downtrends perform better when volatility is above or below its historical average?

- Should different volatility filters be applied to long vs. short positions?

█ Default Settings

The default settings serve as a starting point for exploration:

SuperTrend Parameters:

- SuperTrend 1 (Length=13, Multiplier=3.5): More responsive to trend changes

- SuperTrend 2 (Length=8, Multiplier=5.0): More selective filter requiring stronger trends

VIX Analysis Settings:

- Lookback Period = 252: Establishes a full market cycle for volatility context

- Standard Deviation Bands = 2 and 3 SD: Creates statistically significant regime boundaries

- VIX Trend Period = 10: Balances responsiveness with noise reduction

Default VIX Filter Selection:

- Long Entry: "Above Mean" - Tests if uptrends perform better during above-average volatility

- Short Entry: "Rising VIX" - Tests if downtrends accelerate when volatility is increasing

Feel Free to share your insight below!!!

Volatility-Enhanced Williams %R [AIBitcoinTrend]👽 Volatility-Enhanced Williams %R (AIBitcoinTrend)

The Volatility-Enhanced Williams %R takes the classic Williams %R oscillator to the next level by incorporating volatility-adaptive smoothing, making it significantly more responsive to market dynamics. Unlike the traditional version, which uses a fixed calculation method, this indicator dynamically adjusts its smoothing factor based on market volatility, helping traders capture trends more effectively while filtering out noise.

Additionally, the indicator includes real-time divergence detection and an ATR-based trailing stop system, providing traders with enhanced risk management tools and early reversal signals.

👽 What Makes the Volatility-Enhanced Williams %R Unique?

Unlike the standard Williams %R, which applies a simple lookback-based formula, this version integrates adaptive smoothing and volatility-based filtering to refine its signals and reduce false breakouts.

✅ Volatility-Adaptive Smoothing – Adjusts dynamically based on standard deviation, enhancing signal accuracy.

✅ Real-Time Divergence Detection – Identifies bullish and bearish divergences for early trend reversal signals.

✅ Crossovers & Trailing Stops – Implements Williams %R crossovers with ATR-based trailing stops for intelligent trade management.

👽 The Math Behind the Indicator

👾 Volatility-Adaptive Smoothing

The indicator smooths the Williams %R calculation by applying an adaptive filtering mechanism, which adjusts its responsiveness based on market conditions. This helps to eliminate whipsaws and makes trend-following strategies more reliable.

The smoothing function is defined as:

clamp(x, lo, hi) => math.min(math.max(x, lo), hi)

adaptive(src, prev, len, divisor, minAlpha, maxAlpha) =>

vol = ta.stdev(src, len)

alpha = clamp(vol / divisor, minAlpha, maxAlpha)

prev + alpha * (src - prev)

Where:

Volatility Factor (vol) measures price dispersion using standard deviation.

Adaptive Alpha (alpha) dynamically adjusts smoothing strength.

Clamped Output ensures that the smoothing factor remains within a stable range.

👽 How Traders Can Use This Indicator

👾 Divergence Trading Strategy

Bullish Divergence Setup:

Price makes a lower low, while Williams %R forms a higher low.

Buy signal is confirmed when Williams %R reverses upward.

Bearish Divergence Setup:

Price makes a higher high, while Williams %R forms a lower high.

Sell signal is confirmed when Williams %R reverses downward.

👾 Trailing Stop & Signal-Based Trading

Bullish Setup:

✅ Williams %R crosses above trigger level → Buy signal.

✅ A bullish trailing stop is placed at Low - (ATR × Multiplier).

✅ Exit if price crosses below the stop.

Bearish Setup:

✅ Williams %R crosses below trigger level → Sell signal.

✅ A bearish trailing stop is placed at High + (ATR × Multiplier).

✅ Exit if price crosses above the stop.

👽 Why It’s Useful for Traders

Adaptive Filtering Mechanism – Avoids excessive noise while maintaining responsiveness.

Real-Time Divergence Alerts – Helps traders anticipate market reversals before they occur.

ATR-Based Risk Management – Stops dynamically adjust based on market volatility.

Multi-Market Compatibility – Works effectively across stocks, forex, crypto, and futures.

👽 Indicator Settings

Smoothing Factor – Controls how aggressively the indicator adapts to volatility.

Enable Divergence Analysis – Activates real-time divergence detection.

Lookback Period – Defines the number of bars for detecting pivot points.

Enable Crosses Signals – Turns on Williams %R crossover-based trade signals.

ATR Multiplier – Adjusts trailing stop sensitivity.

Disclaimer: This indicator is designed for educational purposes and does not constitute financial advice. Please consult a qualified financial advisor before making investment decisions.

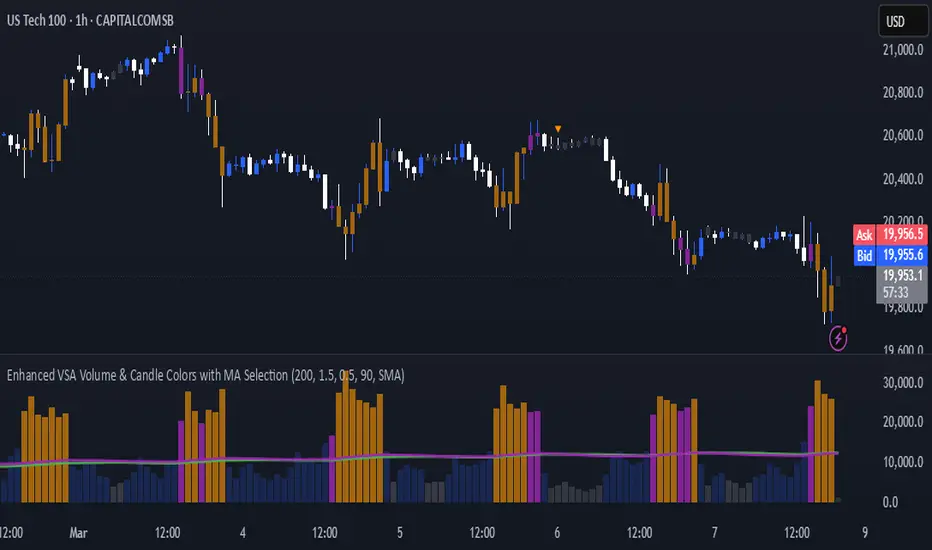

Enhanced VSA Volume & Candle Colors with MA SelectionOverview:

This script aims to enhance the visualization of volume spikes and price action by coloring volume bars and price candles dynamically based on the volume behavior. It allows traders to customize the type of volume moving average (SMA, EMA, or VWMA) used and apply various color schemes to highlight high, low, and extreme volume conditions. Additionally, alerts are generated when extreme or low-volume conditions occur.

---------------------------------------------------------------------------------------------------------------------

Key Features:

Customizable Volume Lookback Period:

The script allows users to define the period for calculating the moving average of volume (default: 200).

Volume Multiplier Settings:

High and low volume thresholds are defined using multipliers. Users can adjust these to customize how volume is categorized (default multipliers: 1.5 for high volume, 0.5 for low volume).

Percentile-Based Extreme Volume Detection:

The script calculates a percentile threshold for extreme volume (default: 90th percentile) based on the volume data, highlighting exceptionally high volume spikes.

Moving Average Selection:

Users can choose between Simple Moving Average (SMA), Exponential Moving Average (EMA), or Volume Weighted Moving Average (VWMA) to track volume trends over the selected lookback period.

Volume-Based Price Bar Coloring:

Price bars can be colored according to the volume conditions (high, low, or extreme). This feature can be toggled on or off.

Dynamic Transparency and Color Customization:

The script allows users to set custom colors for different volume conditions (high, low, neutral, extreme) and adjusts the transparency of volume bars based on the relative size of the volume.

Alerts:

Alerts can be set for when extreme volume spikes or low volume conditions are detected.

---------------------------------------------------------------------------------------------------------------------

Script Components:

Volume Histogram Plot:

Displays the volume bars with dynamic coloring based on the volume condition (high, low, or extreme). The color of the bars adjusts for clarity, with transparency based on volume levels.

Moving Average Plot:

Plots the selected volume moving average (SMA, EMA, or VWMA) to visualize the trend of volume over the chosen lookback period.

Smoothed Average Volume (EMA of Volume):

A smoothed EMA line is plotted to provide a clear representation of volume trends over time.

Price Bar Coloring:

If enabled, price bars are colored according to the current volume condition, providing immediate visual feedback to the trader.

---------------------------------------------------------------------------------------------------------------------

How It Can Be Used:

Volume Analysis for Entry/Exit Points: Traders can use the volume conditions (high, low, and extreme) to identify potential entry or exit points. High-volume bars often signal strong market activity, while low-volume bars may indicate consolidation or indecision.

Volume Confirmation for Trend Reversal: Extreme volume spikes can sometimes precede significant price movements. Traders can monitor these spikes for potential trend reversal signals.

Customizing Alerts: Alerts based on volume conditions help traders stay updated on important volume events without constantly monitoring the chart.

Color-Coded Price Action: The dynamic coloring of price bars makes it easier to identify periods of strong or weak market participation, allowing traders to make informed decisions quickly.

---------------------------------------------------------------------------------------------------------------------

Compliance with TradingView's House Rules:

No Promotion of Financial Products: The script does not promote any specific financial instruments or products, ensuring compliance with TradingView’s content guidelines.

Clear Functionality: The script provides clear, functional analysis tools without making unsupported claims about predicting market movements.

No Automated Trading: The script does not include any automated trading or order execution features, which complies with TradingView’s policy on non-automated scripts.

This breakdown ensures clarity on the script’s purpose, features, and how it might be used by traders. It's written in a way that fits TradingView's content guidelines, keeping the focus on providing valuable analytical tools rather than making promises or promoting any financial product.

Whale Buy Activity Detector (Real-Time)Whale Buy Activity Detector (Real-Time)

This indicator helps to identify abnormal spikes in the volume of purchases, which may indicate the activity of large players ("whales"). It analyzes the volume of purchases and compares it with the average volume over a certain period of time. If the volume of purchases exceeds a set threshold, the indicator marks this as potential whale activity.

Basic parameters:

Volume Threshold (x Average): The coefficient by which the current purchase volume must exceed the average volume in order to be considered abnormal. The default value is 2.0, which means that the purchase volume should be 2 times the average volume for the selected time period. This parameter can be adjusted in the range from 1.0 and higher in increments of 0.1.

Example: If you set the value to 1.5, the indicator will mark situations when the volume of purchases exceeds the average volume by 1.5 times.

Lookback Period: The time period used to calculate the average purchase volume. The default value is 20, which means that the average purchase volume will be calculated for the last 20 candles. This parameter can be set in the range from 1 and above.Example: If you set the value to 10, the average purchase volume will be calculated for the last 10 candles.

How to use:

Buy Volume: Shows the volume of purchases on each candle. This is the volume that was sold at a price higher than the opening price of the candle.

Average Buy Volume: The average volume of purchases over a given time period (Lookback Period). This parameter helps to determine the "normal" level of purchase volume.

Whale Buy: Notes abnormal spikes in the volume of purchases, which may indicate the activity of "whales". The indicator draws a mark on the top of the candle when the purchase volume exceeds the threshold set by the Volume Threshold parameter.

Notifications:

The indicator can send notifications when an abnormal volume of purchases is detected. You can set up notifications via the TradingView menu to receive real-time alerts.

Usage example:

If you are trading in a highly volatile market, you can increase the Volume Threshold to filter out small volume spikes.

If you trade in a low-volatility market, you can reduce the Volume Threshold to capture even small anomalies.