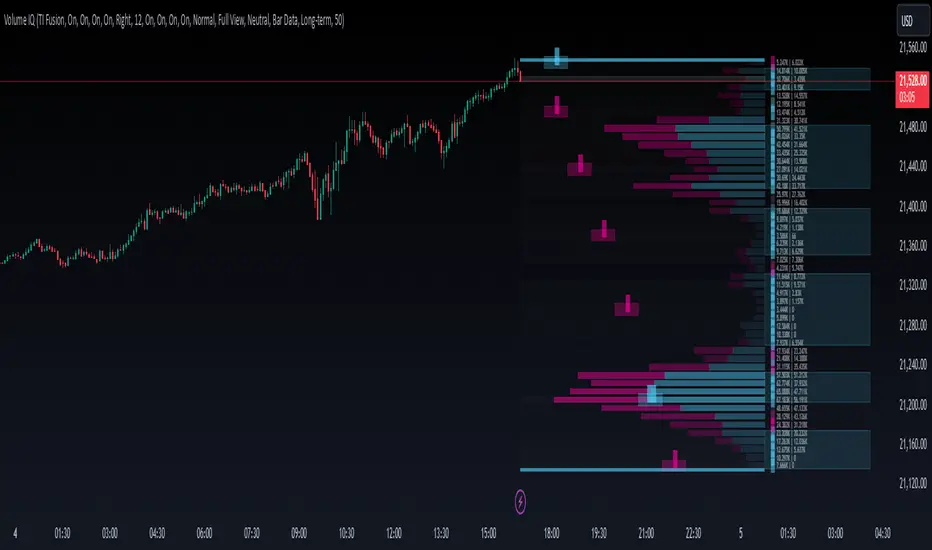

Volume IQOverview

Volume IQ is meant to be the ‘intelligent volume distribution analyzer’ that takes much of the work of interpreting volume profiles off of your shoulders. It attempts to ‘do the technical analysis’ of volume data for you, with its capstone feature being "Trading Action Zones": ranges on the chart whose placement are determined by high and low volume nodes and sentiment analysis, and their adapting range affected by current volatility. These zones are meant to offer practical levels for potential entries, exits, targets, and stops while trading. These zones are the cherry on top of other useful and original features like visuals for grouping areas of similar buy/sell bias.

Originality and Usefulness

Volume IQ stands out for its originality by offering a data-driven approach to interpreting volume profiles and presenting its analysis on the chart. Unlike traditional volume profiles, Volume IQ automates much of the volume analysis process, helping traders identify potential opportunities and key trading areas with minimal effort. Its unique "Trading Action Zones" leverage high and low volume nodes, sentiment analysis, and current volatility to highlight practical levels for entries, exits, targets, and stops. Additionally, the tool provides grouped bias visuals, gradient coloring, and flexible customization options, allowing traders to gain a clearer understanding of market sentiment and structure. By simplifying complex volume data into actionable insights, Volume IQ provides a valuable and efficient resource for charting on TradingView.

The ‘Capstone’ Feature:

Trading ‘Action Zones’: Potential areas to take trading action based on built-in interpretations of high-volume nodes, low-volume nodes, and overarching chart sentiment (whose calculation is described below), and their interplay. Categorized by tiers - with Tier 2 zones intended as potential entry areas, and Tier 1 zones for exits or adds. These zones can also present logical areas to consider targets and stops, for example placing a stop loss in a Tier 1 sell zone below price where there is a series of low-volume nodes and potentially not much support. These zones help you quickly identify potential areas on the chart to ‘take action’.

Key Features:

Level and Block Biases: By estimating buying and selling volume, as well as leveraging intrabar data, the Volume IQ profile provides detailed buy/sell sentiment at individual price levels. It then groups together consecutive price levels with the same bias into what we call ‘Block Biases’ making it easy to determine larger price areas with distinct buying or selling pressure.

Chart Sentiment Analysis: A ‘continuously optimizing algorithm’ configured to find high average runups after a sentiment switch powers what we call ‘bias guidelines’ which border the Volume IQ profile and influence the determination of Action Zones. This algorithm is based on comparing many combinations of volume-weighted trends, largely based on smoothed volume weighted moving averages, on each bar, to ensure that the approach with the highest average runup amongst the combinations is used.

Zones of Control: A gradient-coloring approach to the profile highlighst areas of influence at a glance, making it easier to focus on key price levels.

Broad Compatibility: Works across all chart timeframes and market types - so long as volume data and OHLC candle data is available.

Highly Customizable: Configure features to align with your trading preferences and workflow. Show them all, or pick and choose the ones you want.

Settings

Use a Color Theme: Toggle between our predefined color themes or customize your own.

Style: Select your preferred color theme (e.g., "TI Fusion").

Colors (When Not Using a Theme): Customize primary, secondary, and background colors for your own non-theme styling.

Gradient Coloring: Enable or disable gradient shading of the profile for visual enhancement of zones with high control and low control.

Action Zones: Turn trading action zones on or off to highlight key trading levels.

Time Staggering: Enabling this option will simply ‘stagger’ the display of action zones horizontally. Zones closer to price will be placed leftwards, and as they become more distant from price, they will be ‘staggered out’ rightwards, to give an intuitive feel for the time it may take for price to reach these zones.

Tier Labels: Enable or disable the ‘tier labels’ (1 square for Tier 1, 2 squares for Tier 2) for action zones.

Bias Blocks: Toggle the display of grouped buy/sell bias blocks.

Extend: Choose how the bias blocks are displayed: “Left” to stretch them from the end to the beginning of the histogram, “Right” to extend from the end outwards, and “Across” to extend from the beginning to outwards past the end, enveloping the bias and volume count labels.

Opacity: Adjust the transparency level of bias blocks (0–100).

Level Bias Labels: Turn on/off labels for individual price level biases.

Bias Guidelines: Enable the visual guidelines for bias levels which border the profile.

Volume Counts: Toggle volume count labels for each of the profile’s price levels.

Split Buy/Sell Volume: Enable separate display of buy and sell volume for each level (buy volume on the left, sell volume on the right).

Font Size: Adjust the font size for these labels.

Histogram Display: Choose the display option for the histogram bars of the profile themselves: "Full View" will display the profile, and “None” will hide it.

BG Shading Logic: Adjust the background shading logic for the display: “Neutral” will use the ‘Neutral Color’ from your color theme to put some emphasis around high and low volume nodes, while “None” will remove any background shading.

Detail: This option allows you to set the granularity of the volume data used: “Bar Data” will simply use the bar data from the chart timeframe, while “Intrabar Data” will attempt to use bar data from a lower timeframe. Please note that using intrabar data may not be available with your TradingView subscription on some timeframes, and also that using intrabar data may increase calculation time.

Data Request: Choose the lookback for the volume distribution: "Long-term" will look back 500 bars, and “Short-Term” will halve this.

# of Levels: Specify the number of levels/rows to display for visualizing the distribution.

Volatilityrange

Fixed Volatility OscillatorA fixed volatility plotter set to a 0-100 range - Plots the current volatility % using the formula to calculate volatility and stdev (standard deviation) based on the candle lookback.

The indicator is Fixed, which means that regardless of the chart, the volatility will be plotted on a percentage of 0% - 100% with a 101% threshold set to indicate a volatility reset. While the volume of volatility will change depending on the chart, the volatility will ALWAYS stay within this range.

if a plot exceeds 100% it should be marked as volatility reset - not an expansion

and should also be noted that the volatility spikes are also very inconsistent in volume and vary greatly.

The candle lookbacks on standard are organized be from 10 candles to 100 candles. I found the best results using the 50 candles lookback, and therefore have set it as the default value. These different values can be used to pull the information from the # of candles on the selected option - and therefore the volatility will be calculated from the number of candles selected.

// note for other people versed in pinescript

While this indicator may be useful in trading or strategies, it is more meant to incorporated into other scripts or used as a basis that can be further expanded on. The visuals are not built at all - for that purpose.

This script has not been listed as a library for the fact that it can be used as an actual indicator within a strategy - hope you enjoy.

Lots / Leverage / Margin [JoseMetal]============

ENGLISH

============

- Description:

This is a utility indicator, it prints a table with ATR, Volatility, Lotage and Margin for 3 custom timeframes, using the ATR of basis, it calculates volatility (%) and a recommended lotage depending on your risk settings.

A few months ago i fled from crypto exchanges to regulated brokers, and working with lots instead of plain margin was a bit of headache, i also trade with crypto, currencies, metals and indexes, each with different volatility, leverage... so this tool was a MUST for me to code.

So basically, this tool allows to keep the same RISK for every single asset, no matter if they have different volatility.

- Visual:

The indicator shows a table with all the info explained, ATR, Volatility...

For each timeframe it also prints 3 periods, short, long and average, you can show/hide timeframes and the different periods.

- Customization:

Colors in the table are custom, as well as the font size.

The risk management settings start with the margin you want to use as average, then you can customize your asset leverage, the risk (which is a value you HAVE to keep the same for all assets to balance the results correctly) and units per lot.

You can increase/decrease risk if you want to, i personally take DAILY values with a 18-20 risk to trade on a 4H chart.

For the "units per lot" take in mind that usually that value is ONE, but in some assets with really low value like currencies or some crypto your broker can set 1 lot to xxxx units, that's why you have that option.

- Usage and recommendations:

As i said i trade from 4H to daily, that's why my risk setting is 18-20, i use the lots plotted in the table on DAILY.

If you're more a scalper, just adjust the timeframes to your needs :)

Enjoy!

============

INGLÉS

============

- Descripción:

Este es un indicador de utilidad, imprime una tabla con ATR, Volatilidad, Lotaje y Margen para 3 temporalidades personalizadas, usando el ATR de base, calcula la volatilidad (%) y un lotaje recomendado dependiendo de tu configuración de riesgo.

Hace unos meses cambié de intercambios crypto (exchanges) a brokers regulados, y trabajar con lotes en lugar de margen simple era un poco dolor de cabeza, también tradeo con crypto, divisas, metales e índices, cada uno con diferente volatilidad, apalancamiento... así que esta herramienta era IMPRESCINDIBLE para mí de programar.

Básicamente, esta herramienta permite mantener el mismo RIESGO para cada activo, sin importar si tienen diferente volatilidad.

- Visual:

El indicador muestra una tabla con toda la información explicada, ATR, Volatilidad...

Para cada temporalidad también imprime 3 períodos, corto, largo y medio, puedes mostrar/ocultar los marcos temporales y los diferentes periodos.

- Personalización:

Los colores de la tabla son personalizados, así como el tamaño de la fuente.

La configuración de la gestión del riesgo comienza con el margen que deseas utilizar como promedio, a continuación, puedes personalizar el apalancamiento del activo, el riesgo (que es un valor que TIENE que mantener igual para todos los activos para equilibrar los resultados correctamente) y las unidades por lote.

Puedes aumentar/disminuir el riesgo si quieres, yo personalmente tomo valores DIARIOS con un riesgo de 18-20 para operar en un gráfico de 4H.

Para las "unidades por lote" ten en cuenta que normalmente ese valor es UNO, pero en algunos activos con valor realmente bajo como divisas o algunas criptomonedas tu broker puede poner 1 lote a xxxx unidades, por eso agrego esa opción.

- Uso y recomendaciones:

Como dije yo opero de 4H a diario, por eso mi ajuste de riesgo es de 18-20, uso los lotes graficados en la tabla en DIARIO.

Si eres más un scalper, sólo tienes que ajustar las temporalidades a tus necesidades :)

¡Que lo disfrutes!

Highs/Lows difference [OrganicPunch]Highs/Lows difference indicator

To visually evaluate the difference between highs and lows of a price range.

This handsome indicator shows:

difference between highs of 2 candles by displaying it in green histogram

difference between lows of 2 candles by displaying it in red histogram

difference between both highs and lows by displaying a circle at the level of the difference

To read the numerical value, point at the circle of the relevant bar you are interested in, and see the scale.

Indicator is useful in creating strategies where you want to filter out consolidations/ranges (or to locate them), e.g. "Open trade when H/L difference is larger than 200", or "Look for candles with H/L difference lesser than 50".

The exact value of needed H/L difference can be found using this indicator.

Volatility Risk Premium GOLD & SILVER 1.0ENGLISH

This indicator (V-R-P) calculates the (one month) Volatility Risk Premium for GOLD and SILVER.

V-R-P is the premium hedgers pay for over Realized Volatility for GOLD and SILVER options.

The premium stems from hedgers paying to insure their portfolios, and manifests itself in the differential between the price at which options are sold (Implied Volatility) and the volatility GOLD and SILVER ultimately realize (Realized Volatility).

I am using 30-day Implied Volatility (IV) and 21-day Realized Volatility (HV) as the basis for my calculation, as one month of IV is based on 30 calendaristic days and one month of HV is based on 21 trading days.

At first, the indicator appears blank and a label instructs you to choose which index you want the V-R-P to plot on the chart. Use the indicator settings (the sprocket) to choose one of the precious metals (or both).

Together with the V-R-P line, the indicator will show its one year moving average within a range of +/- 15% (which you can change) for benchmarking purposes. We should consider this range the “normalized” V-R-P for the actual period.

The Zero Line is also marked on the indicator.

Interpretation

When V-R-P is within the “normalized” range, … well... volatility and uncertainty, as it’s seen by the option market, is “normal”. We have a “premium” of volatility which should be considered normal.

When V-R-P is above the “normalized” range, the volatility premium is high. This means that investors are willing to pay more for options because they see an increasing uncertainty in markets.

When V-R-P is below the “normalized” range but positive (above the Zero line), the premium investors are willing to pay for risk is low, meaning they see decreasing uncertainty and risks in the market, but not by much.

When V-R-P is negative (below the Zero line), we have COMPLACENCY. This means investors see upcoming risk as being lower than what happened in the market in the recent past (within the last 30 days).

CONCEPTS :

Volatility Risk Premium

The volatility risk premium (V-R-P) is the notion that implied volatility (IV) tends to be higher than realized volatility (HV) as market participants tend to overestimate the likelihood of a significant market crash.

This overestimation may account for an increase in demand for options as protection against an equity portfolio. Basically, this heightened perception of risk may lead to a higher willingness to pay for these options to hedge a portfolio.

In other words, investors are willing to pay a premium for options to have protection against significant market crashes even if statistically the probability of these crashes is lesser or even negligible.

Therefore, the tendency of implied volatility is to be higher than realized volatility, thus V-R-P being positive.

Realized/Historical Volatility

Historical Volatility (HV) is the statistical measure of the dispersion of returns for an index over a given period of time.

Historical volatility is a well-known concept in finance, but there is confusion in how exactly it is calculated. Different sources may use slightly different historical volatility formulas.

For calculating Historical Volatility I am using the most common approach: annualized standard deviation of logarithmic returns, based on daily closing prices.

Implied Volatility

Implied Volatility (IV) is the market's forecast of a likely movement in the price of the index and it is expressed annualized, using percentages and standard deviations over a specified time horizon (usually 30 days).

IV is used to price options contracts where high implied volatility results in options with higher premiums and vice versa. Also, options supply and demand and time value are major determining factors for calculating Implied Volatility.

Implied Volatility usually increases in bearish markets and decreases when the market is bullish.

For determining GOLD and SILVER implied volatility I used their volatility indices: GVZ and VXSLV (30-day IV) provided by CBOE.

Warning

Please be aware that because CBOE doesn’t provide real-time data in Tradingview, my V-R-P calculation is also delayed, so you shouldn’t use it in the first 15 minutes after the opening.

This indicator is calibrated for a daily time frame.

----------------------------------------------------------------------

ESPAŇOL

Este indicador (V-R-P) calcula la Prima de Riesgo de Volatilidad (de un mes) para GOLD y SILVER.

V-R-P es la prima que pagan los hedgers sobre la Volatilidad Realizada para las opciones de GOLD y SILVER.

La prima proviene de los hedgers que pagan para asegurar sus carteras y se manifiesta en el diferencial entre el precio al que se venden las opciones (Volatilidad Implícita) y la volatilidad que finalmente se realiza en el ORO y la PLATA (Volatilidad Realizada).

Estoy utilizando la Volatilidad Implícita (IV) de 30 días y la Volatilidad Realizada (HV) de 21 días como base para mi cálculo, ya que un mes de IV se basa en 30 días calendario y un mes de HV se basa en 21 días de negociación.

Al principio, el indicador aparece en blanco y una etiqueta le indica que elija qué índice desea que el V-R-P represente en el gráfico. Use la configuración del indicador (la rueda dentada) para elegir uno de los metales preciosos (o ambos).

Junto con la línea V-R-P, el indicador mostrará su promedio móvil de un año dentro de un rango de +/- 15% (que puede cambiar) con fines de evaluación comparativa. Deberíamos considerar este rango como el V-R-P "normalizado" para el período real.

La línea Cero también está marcada en el indicador.

Interpretación

Cuando el V-R-P está dentro del rango "normalizado",... bueno... la volatilidad y la incertidumbre, como las ve el mercado de opciones, es "normal". Tenemos una “prima” de volatilidad que debería considerarse normal.

Cuando V-R-P está por encima del rango "normalizado", la prima de volatilidad es alta. Esto significa que los inversores están dispuestos a pagar más por las opciones porque ven una creciente incertidumbre en los mercados.

Cuando el V-R-P está por debajo del rango "normalizado" pero es positivo (por encima de la línea Cero), la prima que los inversores están dispuestos a pagar por el riesgo es baja, lo que significa que ven una disminución, pero no pronunciada, de la incertidumbre y los riesgos en el mercado.

Cuando V-R-P es negativo (por debajo de la línea Cero), tenemos COMPLACENCIA. Esto significa que los inversores ven el riesgo próximo como menor que lo que sucedió en el mercado en el pasado reciente (en los últimos 30 días).

CONCEPTOS :

Prima de Riesgo de Volatilidad

La Prima de Riesgo de Volatilidad (V-R-P) es la noción de que la Volatilidad Implícita (IV) tiende a ser más alta que la Volatilidad Realizada (HV) ya que los participantes del mercado tienden a sobrestimar la probabilidad de una caída significativa del mercado.

Esta sobreestimación puede explicar un aumento en la demanda de opciones como protección contra una cartera de acciones. Básicamente, esta mayor percepción de riesgo puede conducir a una mayor disposición a pagar por estas opciones para cubrir una cartera.

En otras palabras, los inversores están dispuestos a pagar una prima por las opciones para tener protección contra caídas significativas del mercado, incluso si estadísticamente la probabilidad de estas caídas es menor o insignificante.

Por lo tanto, la tendencia de la Volatilidad Implícita es de ser mayor que la Volatilidad Realizada, por lo cual el V-R-P es positivo.

Volatilidad Realizada/Histórica

La Volatilidad Histórica (HV) es la medida estadística de la dispersión de los rendimientos de un índice durante un período de tiempo determinado.

La Volatilidad Histórica es un concepto bien conocido en finanzas, pero existe confusión sobre cómo se calcula exactamente. Varias fuentes pueden usar fórmulas de Volatilidad Histórica ligeramente diferentes.

Para calcular la Volatilidad Histórica, utilicé el enfoque más común: desviación estándar anualizada de rendimientos logarítmicos, basada en los precios de cierre diarios.

Volatilidad Implícita

La Volatilidad Implícita (IV) es la previsión del mercado de un posible movimiento en el precio del índice y se expresa anualizada, utilizando porcentajes y desviaciones estándar en un horizonte de tiempo específico (generalmente 30 días).

IV se utiliza para cotizar contratos de opciones donde la alta Volatilidad Implícita da como resultado opciones con primas más altas y viceversa. Además, la oferta y la demanda de opciones y el valor temporal son factores determinantes importantes para calcular la Volatilidad Implícita.

La Volatilidad Implícita generalmente aumenta en los mercados bajistas y disminuye cuando el mercado es alcista.

Para determinar la Volatilidad Implícita de GOLD y SILVER utilicé sus índices de volatilidad: GVZ y VXSLV (30 días IV) proporcionados por CBOE.

Precaución

Tenga en cuenta que debido a que CBOE no proporciona datos en tiempo real en Tradingview, mi cálculo de V-R-P también se retrasa, y por este motivo no se recomienda usar en los primeros 15 minutos desde la apertura.

Este indicador está calibrado para un marco de tiempo diario.

TTrail| Trade Trail‴What does it do?

This indicator suggests buy and sell signals with a third indicator as a confirmation indicator.

What is it composed of?

This indicator has three buy or sell signals:

SAR (Stop And Reverse): dotted line above and below the candles;

VR (Volatility Range): green and red line above and below the candles;

SR (Spread Range) ): blue and pink line above and below the candles.

How does it work?

The SAR indicator is a tracker and confirms the movement of VR and SR. The VR indicator is a more conservative Buy/Sell flag, tolerating more price fluctuation. The SR indicator is a less conservative Buy/Sell flag, not tolerating much price fluctuation. The balanced use of these 3 indicators helps the trader to be more coherent in making a decision to open or close a trade.

Some of the characteristics of this indicator are:

it is possible to change the colors of the signaling lines and box;

it is possible to adjust the greater or lesser tolerance of the 3 indicators according to the volatility of the asset;

it is possible to activate/deactivate the indicators and their attributes;

the respective gray boxes refer to countertrend Buy/Sell signals (open/close position against MA20).

How to get access to it?

If you wish to lease this indicator, please contact me by DM, do not use the comment area.

H/V/Q Volatility Index v2.0This is a standalone version of the volatility calculation used in QuantRsi. It is a relatively complex volatility-specific filtering calculation designed to give deeper insight into volatility trends for any asset class.

Use with Log scaling on the indicator's value scalar.

This tool offers an alternative model for volatility calculation. Experience using this tool proves that it extends the efficacy of volatility prediction techniques, and allows deeper technical analysis within volatility moves.

Use alongside conventional volatility indices to find opportunities within option chains to long or short volatility when HVQ provides evidence for volatility reversal that other options value models have not priced in.

Use as part of a predictive based risk management strategy.

Use alongside QuantRsi and HeffaeClouds as a complete trading suite, sans volume analysis, and gain insight not offered by any other indicator set.

SETTINGS:

TimeFrame settings:

Chart/Custom timeframe inputs are carried over from HeffaeClouds and QuantRsi indicators. Allows you to assign any non-chart timeframe to the indicator:

"ChartTF" follows your chart's selected resolution / TimeFrame

"Non-Chart TimeFrame" is an integer for your custom TimeFrame, the setting below:

"Non-Chart TimeFrame" selects "Minutes, Hours, Days" that corresponds to the above setting for a custom TimeFrame.

More Settings:

"Invert Output switch" will invert the volatility chart scale. Useful for visualizing some trends on assets that regularly correlate large volatility spikes with disorderly selloffs.

"Show High/Low Volt range" switch (experimental) shows the high/low extremes of alternate volatility window calculations. There is insight to be gained from large differences v.s. all ranges trending near the same values.

"Relative value switch" (experimental) divides the HVQ values by the hl2 candle price, per candle. This is a unique way to filter the output, visualize the volatility value per asset value.

"Range Multiplier" adjusts the average window length HVQ uses for calculations. This has been finely tuned so that the value of "10" corresponds to the best average fitting of all assets and timeframes. In most situations TimeFrame should be used to alter the real window periods and this should be left at default. Instead you can change this to find better fitting if you'd like.

If there is a feature you would like, question answered, or a bug to report, visit the TradingView SNOW_CITY public chat-room; link in my signature

Use the pastebin link below for indicator access information and pricing