Support and Resistance levels - DMI - DI trailing stop linesThis can be used to compliment the Directional Movement Index if used as a standalone trading system. In addition to using the ADX and DI lines, a trailing stop can be used when the DI lines cross. If the plus line is above to show a buy signal, then the low of the price of when which the cross took place is used as a trailing stop. If the minus line is above to show a sell signal, then the high of the price of when which the cross took place is used as a trailing stop. This helps cut losses sooner whenever the price would end up going through these trailing stops or support/resistance levels yet the DMI system would show an upward or downward move.

Volatility Stop

Dual Volatility StopThis merges Volatility Stop & its MTF version both published by u/TradingView . Background is colored green or red when both the current timeframe Vstop and higher timeframe Vstop point in same direction. Aim is to take the standard Vstop script which differentiates market from only uptrend/downtrend to uptrend/downtrend/sideways. There is a tradeoff with this, that there is no need for the Vstop to be always in a position which reduces trade time & frees up capital. However this leads to situations where it takes slightly more time to catch on to a trend after a reversal.

Green Background = Buy

Red Background = Sell

No Background = Flat

Buurmans TutorialA little Script as part of a Tutorial using Monday as entries and Friday as exits/shorts, with option to Long-Only and a rudimentary Stoploss.

outlined in detail here

can't find a better fitting Category, so bear with me

Stop ATR BuyStop ATR focused on Bull Trend Following, therefore it is plotted only as ATR subtracted from the prices. This indicator has the correct calculation of the ATR formula.

SwingArm ATR Trend IndicatorThe general idea of using SwingArms is to provide a visual confirmation of a trend change.

Green for bullish (BUY)

Red for bearish (SELL)

A color-coded system providing an easy way for a novice to understand.

Converted to TradingView based on the work of Jose Azcarate.

I hope you guys enjoy.

Loro Vola StopThis indicator is a variation of a chandelier volatility stop using an average true range. The indicator draws a green support line in an uptrend and a red resistance line in a downtrend. The signals normally should be used as exit triggers.

Volatility Stop Flow [AR]The indicator is designed to scan cross multiple timeframes and display the Volatility Stop Value.

Guppy Count Back LineThe Guppy Count Back Line was created by Daryl Guppy and is essentially a trailing stop indicator. I have color coded the indicator to tell you if you should go long or short.

This was a special request so let me know if you would like me to write more scripts for other indicators!

vstop5 (RA)Upgrade standart Volatility Stop with 5 fixed values for selected tickers.

When switching between tickers - VStop multiplier will be changed to desired fixed value for fixed tickers.

If nothing mached - will be used standart value

See the example of setting here

As You can see on screenshot 5 different VStops can be set up for different tickers.

and as a result:

Доработка стандартного индикатора VStop, но с возможностью зафиксировать для 5-ти разных инструментов свое значение мультипликатора.

Далее при переключении с одного инструмента на другой - значение Мультипликатора VStop будет меняться в соответствии с сохраненными привязанными настройками. для всех НЕ привязанных инструментов - будет использовано значение Мультипликатора по умолчанию, которое также задается в Настройках.

Пример настроек тут

ST0PST0P is a kind of a TRAILING STOP LOSS INDICATOR in which users can set up LONG or SHORT trade versions and also can set up a STOP LOSS level by percent % or unit difference.

It tries to solve the problem of stop loss indicators' default BUY or SELL settings and non adjustable stop levels of % and difference change in price levels.

(Will try to make updates to add user defined start bars.)

Kıvanç Özbilgiç

Trailing SL Alerts [QuantNomad]It's alerts version of my Trailing SL strategy:

Use "Once Per Bar" param when creating alerts.

Trailing SL Strategy [QuantNomad]I'm a big fan of simple strategies.

This one is a very simple one. So it consists only from one Trailing SL. When SL is hit, the position is reversed and SL is tracked for a new position.

You can choose one of 3 types of SL:

% of your price

ATR - it is calculated as current ATR * multiplier

Absolute

As you can see even this simple strategy can show pretty good results.

ATR Stoploss Lines - Minimize Risk | Maximize ProfitThe ATR Stoploss is best used as a trailing stop. While actively managing your trades, move your stops up as price increases/decreases.

There is an offset of 1 candle, so the ATR will only be based on closed candles. This prevents you from moving your stop's when you really shouldn't.

The top lines are used for short positions and the bottom lines are used for long positions.

You can adjust the distance of the ATR lines from your candles by changing the multiplier in the settings.

You may want to increase the multiplier to 2-3 on less volatile assets, and keep it ~1.75 for volatile assets like BTC.

Feel free to reach out if you need any tips or more help with using these. Just remember, this indicator should only be used to manage your trades, not enter them.

Volatility Stop MTFThis is a multi-timeframe version of our Volatility Stop , an ATR-based trend detector that can be used as a stop.

► Timeframe selection

The higher timeframe can be selected using 3 different ways:

• By steps (60 min., 1D, 3D, 1W, 1M, 1Y).

• As a multiple of the current chart's resolution, which can be fractional, so 3.5 will work.

• Fixed.

Note that you can also use this indicator without the higher timeframe functionality. It will then behave as our normal Volatility Stop would.

► Stop breaches

Two modes of stop-breaching logic can be selected.

• In the default, Early Breach mode, the stop is considered breached when a bar at the chart's current resolution breaches the higher timeframe stop.

• You may also choose to calculate breaches on the higher timeframe information only.

Choosing the Early Breach mode has the advantage of generating faster exits. It will create a state of limbo where the stop has been breached but the Volatility Stop trend has not yet reversed. The impact of detecting earlier exits to minimize losses comes, as is usually the case, at the cost of a compromise: if the stop is breached early in a long trend, the indicator will then spend most of that trend in limbo. Sizeable portions of a trend can thus be missed.

A few options are provided when you use Early Breach mode:

• A red triangle can identify early breaches (default).

• You can color bars or the background to identify limbo states.

When in limbo, the color used to plot the indicator's line or shapes will always be darker.

► Alerts

Five pre-defined alerts are supplied:

• #1: On any trend change.

• #2: On changes into an uptrend.

• #3: On changes into a downtrend.

• #4: Only on breaches of the uptrend by the chart's bars (Early Breach mode). Will not trigger on a trend change.

• #5: Only on breaches of the downtrend by the chart's bars (Early Breach mode). Will not trigger on a trend change.

As usual, alerts should be configured to trigger Once Per Bar Close . When creating alerts, you will see a warning to the effect that potentially repainting code is used, even if the indicator's default non-repainting mode is active. The warning is normal.

► Other features

• You can color bars using the indicator's up/down state. When bars are colored, up bars are more brightly colored.

• The HTF line is non-repainting by default, but you can allow it to repaint.

• You can confirm the higher timeframe used by displaying it at a selectable distance from the last bar on the chart.

• Choice of 2 color themes.

• Choice of display as a line, circles, diamonds or arrows. The line can be used with the other shapes. If no line is required, set its thickness to zero.

Enjoy!

Look first. Then leap.

Volatility StopThis is a new version of the classic Volatility Stop originally published in 2014 by admin and written in Pine v1. While the code has evolved, its logic is identical. It is an ATR-based trend detector that can also be used as a stop. It belongs to the same family of indicators as:

• Charles Le Beau's Chandelier Exit ,

• Olivier Seban's Super Trend , and

• Sylvain Vervoort's Average True Range Trailing Stop .

Unlike the Chandelier Exit , Volatility Stop will not move against the trend.

This new version is written in Pine v4. The indicator can be used as a chart overlay, like the original. The calculations have been functionalized for easier reuse, so it is now easier to lift the logic out of the script and use it in others.

Features

• Choice of 2 color themes.

• Choice of display as a line, circles, diamonds or arrows. The line can be used with the other shapes. If no line is required, set its thickness to zero.

• Same default of length=20 and ATR factor=2 used in the original Volatility Stop.

• 3 alerts: on any trend change, or on changes into up or downtrends only. Alerts should be configured to trigger Once Per Bar Close .

Original version:

Look first. Then leap.

BEST Trailing Stop StrategyHello traders

Here we go again.... with the second strategy snippet.

Reminder: the first snipper was a Trailing Profit strategy script

What's on the menu?

A trailing stop is designed to protect gains by enabling a trade to remain open and continue to profit as long as the price is moving in the investor's favor.

The order closes the trade if the price changes direction by a specified percentage or dollar amount.

Trigger me I'm famous

I developed many trading strategies in my career and often I've been asked to trigger a trailing-stop once a certain % move has been made.

On the screenshot below, the SL trigger is plotted in maroon.

Once the price goes past that level for the first time, I'll start trailing the trailing stop level.

In other words, when we see a price makes an interesting move in percentage value - we decide to trail the stop for at least not losing any more

All the BEST

Dave

Stop ATRStop based on price volatitlty.

It uses ATR indicator multiplied by a factor as a reference for protective stop.

Guppy CBLThis is the Count Back Line script from the book Guppy Trading by Daryl Guppy.

It is usually used as a stop loss line, but can also be used to find entries.

Hope someone finds it usefull, if you find anything that is wrong with it, please let me know and I will try to fix it.

This is my first PineScript, hope it is working as intended.

Market Adaptive Stop-LossI realized that the zone changes in the stoploss remained slow, so I couldn't make enough use of the characteristics of technical indicators when opening positions.

This pushed me to keep stop-loss under the influence of a dependent variable.

This script helped me a lot (everget) :

I've redesigned the stop-loss to be affected by intersections.

Therefore, this script is also suitable for adaptive moving averages, fractional periods.

Script features:

1.You can select calculation methods created by using various technical analysis methods from the scripts' settings:

-Moving Average Convergence Divergence ( Macd )

-Stochastic Oscillator ( Stoch )

-Stochastic Relative Strength Index (StochRSI)

-Stochastic Money Flow Index (StochMFI ) (More info : )

-Know Sure Thing ( KST )

-OBV ( On Balance Volume )

-SMA ( Simple Moving Average )

-EMA ( Exponential Moving Average )

-FISHERTRANSFORM ( Fisher Transform )

-AWESOMEOSCILLATOR( Awesome Oscillator )

-PSAR ( Parabolic Stop and Reverse - Parabolic SAR )

-HULLMA( Hull Moving Average )

-VWMA ( Volume Weighted Moving Average )

-RMA (Moving Average using in Relative Strength Index calculations.)

-COG (Center of Gravity )

-ACC-DIST ( Accumulation / Distribution Index )

2 - The region is determined according to the above calculation methods and if it is larger or smaller than the previous stop loss level.

And if the price in the negative zone is lower than the stoploss, it is the exact signal and is shown with more highlighted colors.

And, in the positive zone, where the price is greater than the stoploss, the trade zones are certain.

Shown with more highlighted colors.

If the zones are correct but stop-loss is not suitable for opening positions:

In other words, if the stop-loss is above/under the highest-lowest levels in the positive zone or if the stop loss is located in the lower zone in the negative zone, these zones are shown to be darker and dimmed so that they do not cause false movements.

*** SUMMARY : As a result, you can use this script with support and resistances,and trend lines to get good results.

I hope it helps in your analyzes. Best regards.

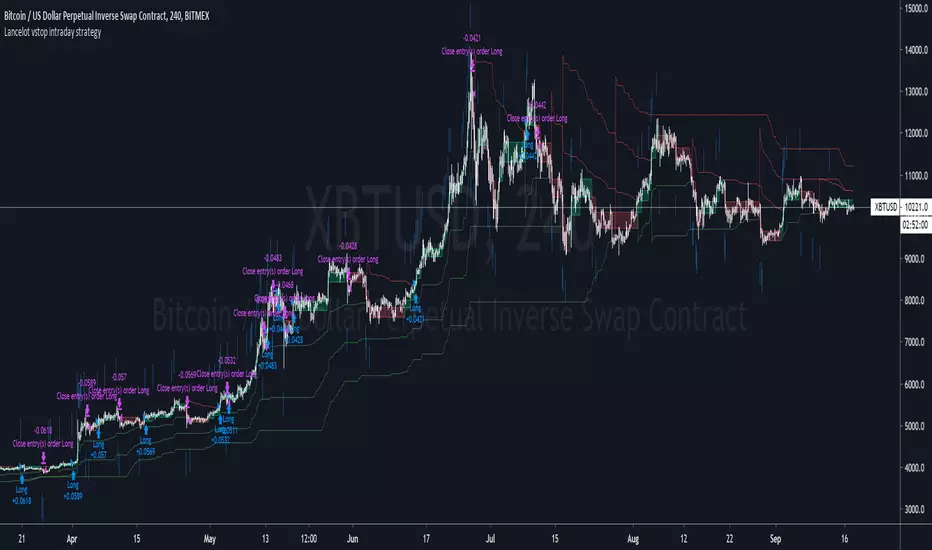

Lancelot vstop intraday trending strategyDear all,

Free strategy again.

I found using 3 volatility stop with different settings could be very helpful when trading an intraday trending market.

With the ATR setting or 5, 10, 15, we can weed out many false break.

Vstop setting is OHLC4.

On the other hand, this strategy also utilize Renko as part of the strategy, so you could say this strategy is mainly an intraday break out trend following strategy.

Works well on BTCUSD XBTUSD, as well as other major liquid alt Pairs.

And lastly,

Save Hong Kong, the revolution of our times.

Alert-QuarryLake Indicator Map - ATR Trend Following Strategy A lot of times I don't like my chart crowding with indicators, thus the reason for creating this script for my strategy QuarryLake.

This script also comes with alert.

Below is the explanation for QuarryLake

I have also updated the script in version 4.

This strategy consists of 3 indicators that I found works quite well together.

Keltner Channel, Waddah Attah Explosion, and Volatility Stop.

You can find WAE here

KC Period = 200

KCATR = 5

Vstop Period = 3

Vstop Mult = 1.5

Long when close > KC, close > Vstop, WAE trendUp

Short when close < KC, close < Vstop, WAE trendDown

Works well on BTCUSD XBTUSD, as well as other major liquid Pair.

Feel free to follow me on Twitter @Lancelot_Auger for more free Alpha.

Please acknowledge my effort by like and follow.

And lastly,

Save Hong Kong, the revolution of our times.

CloudRest ATR based cloudThis is an indicator I have been working on for the past 2 years, developed specifically for cryptocurrency.

It is primarily a trend following indicator with great success and it performs the best in 4hrs to the weekly chart.

There are two components of this indicator.

The baseline from Ichimoku cloud and volatility stop .

baseline period = 26

volatility stop = 1.5ATR, 3

You can view this as the main component of a trend following system but you will need other confirmation indicators to confirm your entry.

Feel free to modify the script for your own system.

Feel free to follow me on twitter @Lancelot_Auger

I will be posting more content in the future, stay tuned.

And lastly,

Free hong kong, the revolution of our time!

ATR ChannelsATR Channels help you to identify where to place your stop-loss or trailing stop-loss based on price volatility, according to the Average True Range (ATR).