Convergence [by Oberlunar]

The Convergence Indicator by Oberlunar is a multi-timeframe analysis tool that identifies and visualizes trend convergence across up to 10 configurable timeframes using advanced customizable moving averages, including Hull, OberX (a Hull mod), THMA, EMA, and SMA, with an optional pseudo-Hilbert Transform.

It provides a clear visual overlay through gradual fill areas that highlight bullish and bearish trends while offering a fully configurable dynamic table to monitor live trend states across all selected timeframes with user-defined colors and positioning.

This tool is designed for traders who seek to pinpoint multi-timeframe convergence points to enhance their decision-making process in trend-following and breakout strategies.

Oberlunar 👁️⭐

Volatilty

PRO Investing - ATR Quant.algo by proinvesting.coATR Quant.algo by PROInvesting.co

A powerful and visually intuitive trend-following system designed to capture high-momentum moves and avoid market chop.

Quant.algo combines a dynamic trend-following EMA with multi-level ATR volatility zones to provide a complete trading framework with clear entry signals, stop-loss levels, and take-profit targets.

Key Features:

Dynamic Trend EMA: A thick baseline that turns Green for uptrends and Red for downtrends. Only trade in the direction of the trend.

Multi-Level ATR Zones: Automatically adapting channels that define ideal zones for entries, stops, and profit-taking.

Volatility Filter: A smart filter that tints the background when volatility is expanding, helping you avoid sideways markets and only trade when the market is ready to move.

Pullback Entry Signals: Clear BUY and SELL arrows appear after a pullback to the EMA, providing high-probability entry points.

Simple Trading Rules:

Go LONG: When the baseline is Green, wait for a Green BUY arrow, and aim for the upper TP Zone. Place your stop below the orange Stop Zone line.

Go SHORT: When the baseline is Red, wait for a Red SELL arrow, and aim for the lower TP Zone. Place your stop above the orange Stop Zone line.

Best For:

Traders: Swing Traders & Position Traders.

Timeframes: 4-Hour (H4) and Daily (D1).

Assets: Trending markets (Indices, Forex, Crypto).

Kelly Optimal Leverage IndicatorThe Kelly Optimal Leverage Indicator mathematically applies Kelly Criterion to determine optimal position sizing based on market conditions.

This indicator helps traders answer the critical question: "How much capital should I allocate to this trade?"

Note that "optimal position sizing" does not equal the position sizing that you should have. The Optima position sizing given by the indicator is based on historical data and cannot predict a crash, in which case, high leverage could be devastating.

Originally developed for gambling scenarios with known probabilities, the Kelly formula has been adapted here for financial markets to dynamically calculate the optimal leverage ratio that maximizes long-term capital growth while managing risk.

Key Features

Kelly Position Sizing: Uses historical returns and volatility to calculate mathematically optimal position sizes

Multiple Risk Profiles: Displays Full Kelly (aggressive), 3/4 Kelly (moderate), 1/2 Kelly (conservative), and 1/4 Kelly (very conservative) leverage levels

Volatility Adjustment: Automatically recommends appropriate Kelly fraction based on current market volatility

Return Smoothing: Option to use log returns and smoothed calculations for more stable signals

Comprehensive Table: Displays key metrics including annualized return, volatility, and recommended exposure levels

How to Use

Interpret the Lines: Each colored line represents a different Kelly fraction (risk tolerance level). When above zero, positive exposure is suggested; when below zero, reduce exposure. Note that this is based on historical returns. I personally like to increase my exposure during market downturns, but this is hard to illustrate in the indicator.

Monitor the Table: The information panel provides precise leverage recommendations and exposure guidance based on current market conditions.

Follow Recommended Position: Use the "Recommended Position" guidance in the table to determine appropriate exposure level.

Select Your Risk Profile: Conservative traders should follow the Half Kelly or Quarter Kelly lines, while more aggressive traders might consider the Three-Quarter or Full Kelly lines.

Adjust with Volatility: During high volatility periods, consider using more conservative Kelly fractions as recommended by the indicator.

Mathematical Foundation

The indicator calculates the optimal leverage (f*) using the formula:

f* = μ/σ²

Where:

μ is the annualized expected return

σ² is the annualized variance of returns

This approach balances potential gains against risk of ruin, offering a scientific framework for position sizing that maximizes long-term growth rate.

Notes

The Full Kelly is theoretically optimal for maximizing long-term growth but can experience significant drawdowns. You should almost never use full kelly.

Most practitioners use fractional Kelly strategies (1/2 or 1/4 Kelly) to reduce volatility while capturing most of the growth benefits

This indicator works best on daily timeframes but can be applied to any timeframe

Negative Kelly values suggest reducing or eliminating market exposure

The indicator should be used as part of a complete trading system, not in isolation

Enjoy the indicator! :)

P.S. If you are really geeky about the Kelly Criterion, I recommend the book The Kelly Capital Growth Investment Criterion by Edward O. Thorp and others.

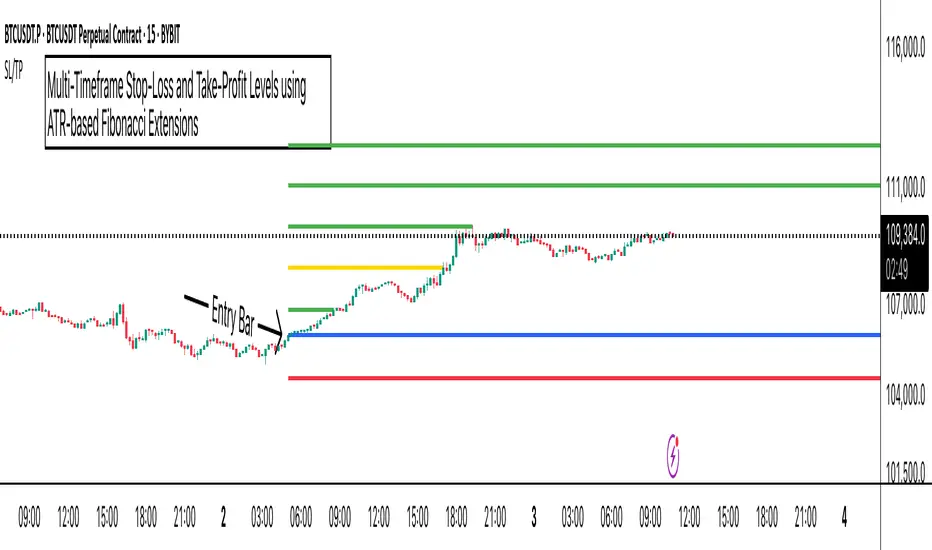

ATR Stop-Loss with Fibonacci Take-Profit [jpkxyz]ATR Stop-Loss with Fibonacci Take-Profit Indicator

This comprehensive indicator combines Average True Range (ATR) volatility analysis with Fibonacci extensions to create dynamic stop-loss and take-profit levels. It's designed to help traders set precise risk management levels and profit targets based on market volatility and mathematical ratios.

Two Operating Modes

Default Mode (Rolling Levels)

In default mode, the indicator continuously plots evolving stop-loss and take-profit levels based on real-time price action. These levels update dynamically as new bars form, creating rolling horizontal lines across the chart. I use this mode primarily to plot the rolling ATR-Level which I use to trail my Stop-Loss into profit.

Characteristics:

Levels recalculate with each new bar

All selected Fibonacci levels display simultaneously

Uses plot() functions with trackprice=true for price tracking

Custom Anchor Mode (Fixed Levels)

This is the primary mode for precision trading. You select a specific timestamp (typically your entry bar), and the indicator locks all calculations to that exact moment, creating fixed horizontal lines that represent your actual trade levels.

Characteristics:

Entry line (blue) marks your anchor point

Stop-loss calculated using ATR from the anchor bar

Fibonacci levels projected from entry-to-stop distance

Lines terminate when price breaks through them

Includes comprehensive alert system

Core Calculation Logic

ATR Stop-Loss Calculation:

Stop Loss = Entry Price ± (ATR × Multiplier)

Long positions: SL = Entry - (ATR × Multiplier)

Short positions: SL = Entry + (ATR × Multiplier)

ATR uses your chosen smoothing method (RMA, SMA, EMA, or WMA)

Default multiplier is 1.5, adjustable to your risk tolerance

Fibonacci Take-Profit Projection:

The distance from entry to stop-loss becomes the base unit (1.0) for Fibonacci extensions:

TP Level = Entry + (Entry-to-SL Distance × Fibonacci Ratio)

Available Fibonacci Levels:

Conservative: 0.618, 1.0, 1.618

Extended: 2.618, 3.618, 4.618

Complete range: 0.0 to 4.764 (23 levels total)

Multi-Timeframe Functionality

One of the indicator's most powerful features is timeframe flexibility. You can analyze on one timeframe while using stop-loss and take-profit calculations from another.

Best Practices:

Identify your entry point on execution timeframe

Enable "Custom Anchor" mode

Set anchor timestamp to your entry bar

Select appropriate analysis timeframe

Choose relevant Fibonacci levels

Enable alerts for automated notifications

Example Scenario:

Analyse trend on 4-hour chart

Execute entry on 5-minute chart for precision

Set custom anchor to your 5-minute entry bar

Configure timeframe setting to "4h" for swing-level targets

Select appropriate Fibonacci Extension levels

Result: Precise entry with larger timeframe risk management

Visual Intelligence System

Line Behaviour in Custom Anchor Mode:

Active levels: Lines extend to the right edge

Hit levels: Lines terminate at the breaking bar

Entry line: Always visible in blue

Stop-loss: Red line, terminates when hit

Take-profits: Green lines (1.618 level in gold for emphasis)

Customisation Options:

Line width (1-4 pixels)

Show/hide individual Fibonacci levels

ATR length and smoothing method

ATR multiplier for stop-loss distance

Ticker Pulse Meter + Fear EKG StrategyDescription

The Ticker Pulse Meter + Fear EKG Strategy is a technical analysis tool designed to identify potential entry and exit points for long positions based on price action relative to historical ranges. It combines two proprietary indicators: the Ticker Pulse Meter (TPM), which measures price positioning within short- and long-term ranges, and the Fear EKG, a VIX-inspired oscillator that detects extreme market conditions. The strategy is non-repainting, ensuring signals are generated only on confirmed bars to avoid false positives. Visual enhancements, such as optional moving averages and Bollinger Bands, provide additional context but are not core to the strategy's logic. This script is suitable for traders seeking a systematic approach to capturing momentum and mean-reversion opportunities.

How It Works

The strategy evaluates price action using two key metrics:

Ticker Pulse Meter (TPM): Measures the current price's position within short- and long-term price ranges to identify momentum or overextension.

Fear EKG: Detects extreme selling pressure (akin to "irrational selling") by analyzing price behavior relative to historical lows, inspired by volatility-based oscillators.

Entry signals are generated when specific conditions align, indicating potential buying opportunities. Exits are triggered based on predefined thresholds or partial position closures to manage risk. The strategy supports customizable lookback periods, thresholds, and exit percentages, allowing flexibility across different markets and timeframes. Visual cues, such as entry/exit dots and a position table, enhance usability, while optional overlays like moving averages and Bollinger Bands provide additional chart context.

Calculation Overview

Price Range Calculations:

Short-Term Range: Uses the lowest low (min_price_short) and highest high (max_price_short) over a user-defined short lookback period (lookback_short, default 50 bars).

Long-Term Range: Uses the lowest low (min_price_long) and highest high (max_price_long) over a user-defined long lookback period (lookback_long, default 200 bars).

Percentage Metrics:

pct_above_short: Percentage of the current close above the short-term range.

pct_above_long: Percentage of the current close above the long-term range.

Combined metrics (pct_above_long_above_short, pct_below_long_below_short) normalize price action for signal generation.

Signal Generation:

Long Entry (TPM): Triggered when pct_above_long_above_short crosses above a user-defined threshold (entryThresholdhigh, default 20) and pct_below_long_below_short is below a low threshold (entryThresholdlow, default 40).

Long Entry (Fear EKG): Triggered when pct_below_long_below_short crosses under an extreme threshold (orangeEntryThreshold, default 95), indicating potential oversold conditions.

Long Exit: Triggered when pct_above_long_above_short crosses under a profit-taking level (profitTake, default 95). Partial exits are supported via a user-defined percentage (exitAmt, default 50%).

Non-Repainting Logic: Signals are calculated using data from the previous bar ( ) and only plotted on confirmed bars (barstate.isconfirmed), ensuring reliability.

Visual Enhancements:

Optional moving averages (SMA, EMA, WMA, VWMA, or SMMA) and Bollinger Bands can be enabled for trend context.

A position table displays real-time metrics, including open positions, Fear EKG, and Ticker Pulse values.

Background highlights mark periods of high selling pressure.

Entry Rules

Long Entry:

TPM Signal: Occurs when the price shows strength relative to both short- and long-term ranges, as defined by pct_above_long_above_short crossing above entryThresholdhigh and pct_below_long_below_short below entryThresholdlow.

Fear EKG Signal: Triggered by extreme selling pressure, when pct_below_long_below_short crosses under orangeEntryThreshold. This signal is optional and can be toggled via enable_yellow_signals.

Entries are executed only on confirmed bars to prevent repainting.

Exit Rules

Long Exit: Triggered when pct_above_long_above_short crosses under profitTake.

Partial exits are supported, with the strategy closing a user-defined percentage of the position (exitAmt) up to four times per position (exit_count limit).

Exits can be disabled or adjusted via enable_short_signal and exitPercentage settings.

Inputs

Backtest Start Date: Defines the start of the backtesting period (default: Jan 1, 2017).

Lookback Periods: Short (lookback_short, default 50) and long (lookback_long, default 200) periods for range calculations.

Resolution: Timeframe for price data (default: Daily).

Entry/Exit Thresholds:

entryThresholdhigh (default 20): Threshold for TPM entry.

entryThresholdlow (default 40): Secondary condition for TPM entry.

orangeEntryThreshold (default 95): Threshold for Fear EKG entry.

profitTake (default 95): Exit threshold.

exitAmt (default 50%): Percentage of position to exit.

Visual Options: Toggle for moving averages and Bollinger Bands, with customizable types and lengths.

Notes

The strategy is designed to work across various timeframes and assets, with data sourced from user-selected resolutions (i_res).

Alerts are included for long entry and exit signals, facilitating integration with TradingView's alert system.

The script avoids repainting by using confirmed bar data and shifted calculations ( ).

Visual elements (e.g., SMA, Bollinger Bands) are inspired by standard Pine Script practices and are optional, not integral to the core logic.

Usage

Apply the script to a chart, adjust input settings to suit your trading style, and use the visual cues (entry/exit dots, position table) to monitor signals. Enable alerts for real-time notifications.

Designed to work best on Daily timeframe.

ATR Buy, Target, Stop + OverlayATR Buy, Target, Stop + Overlay

This tool is to assist traders with precise trade planning using the Average True Range (ATR) as a volatility-based reference.

This script plots buy, target, and stop-loss levels on the chart based on a user-defined buy price and ATR-based multipliers, allowing for objective and adaptive trade management.

*NOTE* In order for the indicator to initiate plotted lines and table values a non-zero number must be entered into the settings.

What It Does:

Buy Price Input: Users enter a manual buy price (e.g., an executed or planned trade entry).

ATR-Based Target and Stop: The script calculates:

Target Price = Buy + (ATR × Target Multiplier)

Stop Price = Buy − (ATR × Stop Multiplier)

Customizable Timeframe: Optionally override the ATR timeframe (e.g., use daily ATR on a 1-hour chart).

Visual Overlay: Lines are drawn directly on the price chart for the Buy, Target, and Stop levels.

Interactive Table: A table is displayed with relevant levels and ATR info.

Customization Options:

Line Settings:

Adjust color, style (solid/dashed/dotted), and width for Buy, Target, and Stop lines.

Choose whether to extend lines rightward only or in both directions.

Table Settings:

Choose position (top/bottom, left/right).

Toggle individual rows for Buy, Target, Stop, ATR Timeframe, and ATR Value.

Customize text color and background transparency.

How to Use It for Trading:

Plan Your Trade: Enter your intended buy price when planning a trade.

Assess Risk/Reward: The script immediately visualizes the potential stop-loss and target level, helping assess R:R ratios.

Adapt to Volatility: Use ATR-based levels to scale stop and target dynamically depending on current market volatility.

Higher Timeframe ATR: Select a different timeframe for the ATR calculation to smooth noise on lower timeframe charts.

On-the-Chart Reference: Visually track trade zones directly on the price chart—ideal for live trading or strategy backtesting.

Ideal For:

Swing traders and intraday traders

Risk management and trade planning

Traders using ATR-based exits or scaling

Visualizing asymmetric risk/reward setups

How I Use This:

After entering a trade, adding an entry price will plot desired ATR target and stop level for visualization.

Adjusting ATR multiplier values assists in evaluating and planning trades.

Visualization assists in comparing ATR multiples to recent support and resistance levels.

Session Range ProjectionsSession Range Projections

Purpose & Concept:

Session Range Projections is a comprehensive trading tool that identifies and analyzes price ranges during user-defined time periods. The indicator visualizes high-probability reversal zones and profit targets by projecting Fibonacci levels from custom session ranges, making it ideal for traders who focus on time-based market structure analysis.

Key Features & Calculations:

1. Custom Time Range Analysis

- Define any time period for range calculation - from traditional sessions (Asian, London, NY) to custom periods like opening ranges, hourly ranges, or 4-hour blocks

- Automatically captures the highest and lowest prices within your specified timeframe

- Supports multiple timezone selections for global market analysis

- Flexible enough for intraday scalping ranges or longer-term swing trading setups

2. Premium & Discount Zones

- Automatically divides the range into premium (above 50%) and discount (below 50%) zones

- Visual differentiation helps identify institutional buying and selling areas

- Color-coded boxes clearly mark these critical price zones

3. Optimal Trade Entry (OTE) Zones

- Highlights the 79-89% retracement zone in premium territory

- Highlights the 11-21% retracement zone in discount territory

- These zones represent high-probability reversal areas based on institutional order flow concepts

4. Fibonacci Projections

- Projects 11 customizable Fibonacci extension levels from the range extremes

- Levels extend both above and below the range for symmetrical analysis

- Each level can be individually toggled and color-customized

- Default levels include common retracement ratios: -0.5, -1.0, -2.0, -2.33, -2.5, -3.0, -4.0, -4.5, -6.0, -7.0, -8.0

How to Use:

Set Your Time Range: Input your desired session start and end times (24-hour format)

Select Timezone: Choose the appropriate timezone for your trading session

Customize Display: Toggle various visual elements based on your preferences

Monitor Price Action: Watch for reactions at projected levels and OTE zones

Set Alerts: Configure sweep alerts for when price breaks above/below range extremes

Input Parameters Explained:

Time Range Settings

Range Start/End Hour & Minute: Define your analysis period

Time Zone: Ensure accurate session timing across different markets

Visual Settings

Range Box: Toggle the premium/discount zone visualization

Horizontal Lines: Customize high/low line appearance

Internal Range Levels: Show/hide equilibrium and OTE zones

Labels: Configure text display for key levels

Fibonacci Projections: Enable/disable extension levels

Display Settings

Historical Ranges: Show up to 10 previous session ranges

Alert Type: Choose between high sweep, low sweep, or both

Trading Applications:

Session-Based Trading: Analyze specific market sessions (Asian, London, New York, opening ranges, hourly ranges)

Reversal Trading: Identify high-probability reversal zones at OTE levels

Breakout/Reversal Trading: Monitor range breaks/reversals with built-in sweep alerts

Risk Management: Use Fibonacci projections as profit targets or rejection areas

Multi-Timeframe Analysis: Apply to any timeframe for various trading styles

Important Notes:

This indicator is for educational purposes only and should not be considered financial advice

Past performance does not guarantee future results

Always use proper risk management when trading

The indicator automatically manages historical data to maintain chart performance

Volatility Quality [Alpha Extract]The Alpha-Extract Volatility Quality (AVQ) Indicator provides traders with deep insights into market volatility by measuring the directional strength of price movements. This sophisticated momentum-based tool helps identify overbought and oversold conditions, offering actionable buy and sell signals based on volatility trends and standard deviation bands.

🔶 CALCULATION

The indicator processes volatility quality data through a series of analytical steps:

Bar Range Calculation: Measures true range (TR) to capture price volatility.

Directional Weighting: Applies directional bias (positive for bullish candles, negative for bearish) to the true range.

VQI Computation: Uses an exponential moving average (EMA) of weighted volatility to derive the Volatility Quality Index (VQI).

vqiRaw = ta.ema(weightedVol, vqiLen)

Smoothing: Applies an additional EMA to smooth the VQI for clearer signals.

Normalization: Optionally normalizes VQI to a -100/+100 scale based on historical highs and lows.

Standard Deviation Bands: Calculates three upper and lower bands using standard deviation multipliers for volatility thresholds.

vqiStdev = ta.stdev(vqiSmoothed, vqiLen)

upperBand1 = vqiSmoothed + (vqiStdev * stdevMultiplier1)

upperBand2 = vqiSmoothed + (vqiStdev * stdevMultiplier2)

upperBand3 = vqiSmoothed + (vqiStdev * stdevMultiplier3)

lowerBand1 = vqiSmoothed - (vqiStdev * stdevMultiplier1)

lowerBand2 = vqiSmoothed - (vqiStdev * stdevMultiplier2)

lowerBand3 = vqiSmoothed - (vqiStdev * stdevMultiplier3)

Signal Generation: Produces overbought/oversold signals when VQI reaches extreme levels (±200 in normalized mode).

Formula:

Bar Range = True Range (TR)

Weighted Volatility = Bar Range × (Close > Open ? 1 : Close < Open ? -1 : 0)

VQI Raw = EMA(Weighted Volatility, VQI Length)

VQI Smoothed = EMA(VQI Raw, Smoothing Length)

VQI Normalized = ((VQI Smoothed - Lowest VQI) / (Highest VQI - Lowest VQI) - 0.5) × 200

Upper Band N = VQI Smoothed + (StdDev(VQI Smoothed, VQI Length) × Multiplier N)

Lower Band N = VQI Smoothed - (StdDev(VQI Smoothed, VQI Length) × Multiplier N)

🔶 DETAILS

Visual Features:

VQI Plot: Displays VQI as a line or histogram (lime for positive, red for negative).

Standard Deviation Bands: Plots three upper and lower bands (teal for upper, grayscale for lower) to indicate volatility thresholds.

Reference Levels: Horizontal lines at 0 (neutral), +100, and -100 (in normalized mode) for context.

Zone Highlighting: Overbought (⋎ above bars) and oversold (⋏ below bars) signals for extreme VQI levels (±200 in normalized mode).

Candle Coloring: Optional candle overlay colored by VQI direction (lime for positive, red for negative).

Interpretation:

VQI ≥ 200 (Normalized): Overbought condition, strong sell signal.

VQI 100–200: High volatility, potential selling opportunity.

VQI 0–100: Neutral bullish momentum.

VQI 0 to -100: Neutral bearish momentum.

VQI -100 to -200: High volatility, strong bearish momentum.

VQI ≤ -200 (Normalized): Oversold condition, strong buy signal.

🔶 EXAMPLES

Overbought Signal Detection: When VQI exceeds 200 (normalized), the indicator flags potential market tops with a red ⋎ symbol.

Example: During strong uptrends, VQI reaching 200 has historically preceded corrections, allowing traders to secure profits.

Oversold Signal Detection: When VQI falls below -200 (normalized), a lime ⋏ symbol highlights potential buying opportunities.

Example: In bearish markets, VQI dropping below -200 has marked reversal points for profitable long entries.

Volatility Trend Tracking: The VQI plot and bands help traders visualize shifts in market momentum.

Example: A rising VQI crossing above zero with widening bands indicates strengthening bullish momentum, guiding traders to hold or enter long positions.

Dynamic Support/Resistance: Standard deviation bands act as dynamic volatility thresholds during price movements.

Example: Price reversals often occur near the third standard deviation bands, providing reliable entry/exit points during volatile periods.

🔶 SETTINGS

Customization Options:

VQI Length: Adjust the EMA period for VQI calculation (default: 14, range: 1–50).

Smoothing Length: Set the EMA period for smoothing (default: 5, range: 1–50).

Standard Deviation Multipliers: Customize multipliers for bands (defaults: 1.0, 2.0, 3.0).

Normalization: Toggle normalization to -100/+100 scale and adjust lookback period (default: 200, min: 50).

Display Style: Switch between line or histogram plot for VQI.

Candle Overlay: Enable/disable VQI-colored candles (lime for positive, red for negative).

The Alpha-Extract Volatility Quality Indicator empowers traders with a robust tool to navigate market volatility. By combining directional price range analysis with smoothed volatility metrics, it identifies overbought and oversold conditions, offering clear buy and sell signals. The customizable standard deviation bands and optional normalization provide precise context for market conditions, enabling traders to make informed decisions across various market cycles.

Approximate Entropy Zones [PhenLabs]Version: PineScript™ v6

Description

This indicator identifies periods of market complexity and randomness by calculating the Approximate Entropy (ApEn) of price action. As the movement of the market becomes complex, it means the current trend is losing steam and a reversal or consolidation is likely near. The indicator plots high-entropy periods as zones on your chart, providing a graphical suggestion to anticipate a potential market direction change. This indicator is designed to help traders identify favorable times to get in or out of a trade by highlighting when the market is in a state of disarray.

Points of Innovation

Advanced Complexity Analysis: Instead of relying on traditional momentum or trend indicators, this tool uses Approximate Entropy to quantify the unpredictability of price movements.

Dynamic Zone Creation: It automatically plots zones on the chart during periods of high entropy, providing a clear and intuitive visual guide.

Customizable Sensitivity: Users can fine-tune the ‘Entropy Threshold’ to adjust how frequently zones appear, allowing for calibration to different assets and timeframes.

Time-Based Zone Expiration: Zones can be set to expire after a specific time, keeping the chart clean and relevant.

Built-in Zone Size Filter: Excludes zones that form on excessively large candles, filtering out noise from extreme volatility events.

On-Chart Calibration Guide: A persistent note on the chart provides simple instructions for adjusting the entropy threshold, making it easy for users to optimize the indicator’s performance.

Core Components

Approximate Entropy (ApEn) Calculation: The core of the indicator, which measures the complexity or randomness of the price data.

Zone Plotting: Creates visual boxes on the chart when the calculated ApEn value exceeds a user-defined threshold.

Dynamic Zone Management: Manages the lifecycle of the zones, from creation to expiration, ensuring the chart remains uncluttered.

Customizable Settings: A comprehensive set of inputs that allow users to control the indicator’s sensitivity, appearance, and time-based behavior.

Key Features

Identifies Potential Reversals: The high-entropy zones can signal that a trend is nearing its end, giving traders an early warning.

Works on Any Timeframe: The indicator can be applied to any chart timeframe, from minutes to days.

Customizable Appearance: Users can change the color and transparency of the zones to match their chart’s theme.

Informative Labels: Each zone can display the calculated entropy value and the direction of the candle on which it formed.

Visualization

Entropy Zones: Shaded boxes that appear on the chart, highlighting candles with high complexity.

Zone Labels: Text within each zone that displays the ApEn value and a directional arrow (e.g., “0.525 ↑”).

Calibration Note: A small table in the top-right corner of the chart with instructions for adjusting the indicator’s sensitivity.

Usage Guidelines

Entropy Analysis

Source: The price data used for the ApEn calculation. (Default: close)

Lookback Length: The number of bars used in the ApEn calculation. (Default: 20, Range: 10-50)

Embedding Dimension (m): The length of patterns to be compared; a standard value for financial data. (Default: 2)

Tolerance Multiplier (r): Adjusts the tolerance for pattern matching; a larger value makes matching more lenient. (Default: 0.2)

Entropy Threshold: The ApEn value that must be exceeded to plot a zone. Increase this if too many zones appear; decrease it if too few appear. (Default: 0.525)

Time Settings

Analysis Timeframe: How long a zone remains on the chart after it forms. (Default: 1D)

Custom Period (Bars): The zone’s lifespan in bars if “Analysis Timeframe” is set to “Custom”. (Default: 1000)

Zone Settings

Zone Fill Color: The color of the entropy zones. (Default: #21f38a with 80% transparency)

Maximum Zone Size %: Filters out zones on candles that are larger than this percentage of their low price. (Default: 0.5)

Display Options

Show Entropy Label: Toggles the visibility of the text label inside each zone. (Default: true)

Label Text Position: The horizontal alignment of the text label. (Default: Right)

Show Calibration Note: Toggles the visibility of the calibration note in the corner of the chart. (Default: true)

Best Use Cases

Trend Reversal Trading: Identifying when a strong trend is likely to reverse or pause.

Breakout Confirmation: Using the absence of high entropy to confirm the strength of a breakout.

Ranging Market Identification: Periods of high entropy can indicate that a market is transitioning into a sideways or choppy phase.

Limitations

Not a Standalone Signal: This indicator should be used in conjunction with other forms of analysis to confirm trading signals.

Lagging Nature: Like all indicators based on historical data, ApEn is a lagging measure and does not predict future price movements with certainty.

Calibration Required: The effectiveness of the indicator is highly dependent on the “Entropy Threshold” setting, which needs to be adjusted for different assets and timeframes.

What Makes This Unique

Quantifies Complexity: It provides a numerical measure of market complexity, offering a different perspective than traditional indicators.

Clear Visual Cues: The zones make it easy to see when the market is in a state of high unpredictability.

User-Friendly Design: With features like the on-chart calibration note, the indicator is designed to be easy to use and optimize.

How It Works

Calculate Standard Deviation: The indicator first calculates the standard deviation of the source price data over a specified lookback period.

Calculate Phi: It then calculates a value called “phi” for two different pattern lengths (embedding dimensions ‘m’ and ‘m+1’). This involves comparing sequences of data points to see how many are “similar” within a certain tolerance (determined by the standard deviation and the ‘r’ multiplier).

Calculate ApEn: The Approximate Entropy is the difference between the two phi values. A higher ApEn value indicates greater irregularity and unpredictability in the data.

Plot Zones: If the calculated ApEn exceeds the user-defined ‘Entropy Threshold’, a zone is plotted on the chart.

Note: The “Entropy Threshold” is the most important setting to adjust. If you see too many zones, increase the threshold. If you see too few, decrease it.

Heikin-Ashi Mean Reversion Oscillator [Alpha Extract]The Heikin-Ashi Mean Reversion Oscillator combines the smoothing characteristics of Heikin-Ashi candlesticks with mean reversion analysis to create a powerful momentum oscillator. This indicator applies Heikin-Ashi transformation twice - first to price data and then to the oscillator itself - resulting in smoother signals while maintaining sensitivity to trend changes and potential reversal points.

🔶 CALCULATION

Heikin-Ashi Transformation: Converts regular OHLC data to smoothed Heikin-Ashi values

Component Analysis: Calculates trend strength, body deviation, and price deviation from mean

Oscillator Construction: Combines components with weighted formula (40% trend strength, 30% body deviation, 30% price deviation)

Double Smoothing: Applies EMA smoothing and second Heikin-Ashi transformation to oscillator values

Signal Generation: Identifies trend changes and crossover points with overbought/oversold levels

Formula:

HA Close = (Open + High + Low + Close) / 4

HA Open = (Previous HA Open + Previous HA Close) / 2

Trend Strength = Normalized consecutive HA candle direction

Body Deviation = (HA Body - Mean Body) / Mean Body * 100

Price Deviation = ((HA Close - Price Mean) / Price Mean * 100) / Standard Deviation * 25

Raw Oscillator = (Trend Strength * 0.4) + (Body Deviation * 0.3) + (Price Deviation * 0.3)

Final Oscillator = 50 + (EMA(Raw Oscillator) / 2)

🔶 DETAILS Visual Features:

Heikin-Ashi Candlesticks: Smoothed oscillator representation using HA transformation with vibrant teal/red coloring

Overbought/Oversold Zones: Horizontal lines at customizable levels (default 70/30) with background highlighting in extreme zones

Moving Averages: Optional fast and slow EMA overlays for additional trend confirmation

Signal Dashboard: Real-time table showing current oscillator status (Overbought/Oversold/Bullish/Bearish) and buy/sell signals

Reference Lines: Middle line at 50 (neutral), with 0 and 100 boundaries for range visualization

Interpretation:

Above 70: Overbought conditions, potential selling opportunity

Below 30: Oversold conditions, potential buying opportunity

Bullish HA Candles: Green/teal candles indicate upward momentum

Bearish HA Candles: Red candles indicate downward momentum

MA Crossovers: Fast EMA above slow EMA suggests bullish momentum, below suggests bearish momentum

Zone Exits: Price moving out of extreme zones (above 70 or below 30) often signals trend continuation

🔶 EXAMPLES

Mean Reversion Signals: When the oscillator reaches extreme levels (above 70 or below 30), it identifies potential reversal points where price may revert to the mean.

Example: Oscillator reaching 80+ levels during strong uptrends often precedes short-term pullbacks, providing profit-taking opportunities.

Trend Change Detection: The double Heikin-Ashi smoothing helps identify genuine trend changes while filtering out market noise.

Example: When oscillator HA candles change from red to teal after oversold readings, this confirms potential trend reversal from bearish to bullish.

Moving Average Confirmation: Fast and slow EMA crossovers on the oscillator provide additional confirmation of momentum shifts.

Example: Fast EMA crossing above slow EMA while oscillator is rising from oversold levels provides strong bullish confirmation signal.

Dashboard Signal Integration: The real-time dashboard combines oscillator status with directional signals for quick decision-making.

Example: Dashboard showing "Oversold" status with "BUY" signal when HA candles turn bullish provides clear entry timing.

🔶 SETTINGS

Customization Options:

Calculation: Oscillator period (default 14), smoothing factor (1-50, default 2)

Levels: Overbought threshold (50-100, default 70), oversold threshold (0-50, default 30)

Moving Averages: Toggle display, fast EMA length (default 9), slow EMA length (default 21)

Visual Enhancements: Show/hide signal dashboard, customizable table position

Alert Conditions: Oversold bounce, overbought reversal, bullish/bearish MA crossovers

The Heikin-Ashi Mean Reversion Oscillator provides traders with a sophisticated momentum tool that combines the smoothing benefits of Heikin-Ashi analysis with mean reversion principles. The double transformation process creates cleaner signals while the integrated dashboard and multiple confirmation methods help traders identify high-probability entry and exit points during both trending and ranging market conditions.

Vix_Fix Enhanced MTF [Cometreon]The VIX Fix Enhanced is designed to detect market bottoms and spikes in volatility, helping traders anticipate major reversals with precision. Unlike standard VIX Fix tools, this version allows you to control the standard deviation logic, switch between chart styles, customize visual outputs, and set up advanced alerts — all with no repainting.

🧠 Logic and Calculation

This indicator is based on Larry Williams' VIX Fix and integrates features derived from community requests/advice, such as inverse VIX logic.

It calculates volatility spikes using a customizable standard deviation of the lows and compares it to a moving high to identify potential reversal points.

All moving average logic is based on Cometreon's proprietary library, ensuring accurate and optimized calculations on all 15 moving average types.

🔷 New Features and Improvements

🟩 Custom Visual Styles

Choose how you want your VIX data displayed:

Line

Step Line

Histogram

Area

Column

You can also flip the orientation (bottom-up or top-down), change the source ticker, and tailor the display to match your charting preferences.

🟩 Multi-MA Standard Deviation Calculation

Customize the standard deviation formula by selecting from 15 different moving averages:

SMA (Simple Moving Average)

EMA (Exponential Moving Average)

WMA (Weighted Moving Average)

RMA (Smoothed Moving Average)

HMA (Hull Moving Average)

JMA (Jurik Moving Average)

DEMA (Double Exponential Moving Average)

TEMA (Triple Exponential Moving Average)

LSMA (Least Squares Moving Average)

VWMA (Volume-Weighted Moving Average)

SMMA (Smoothed Moving Average)

KAMA (Kaufman’s Adaptive Moving Average)

ALMA (Arnaud Legoux Moving Average)

FRAMA (Fractal Adaptive Moving Average)

VIDYA (Variable Index Dynamic Average)

This gives you fine control over how volatility is measured and allows tuning the sensitivity for different market conditions.

🟩 Full Control Over Percentile and Deviation Conditions

You can enable or disable lines for standard deviation and percentile conditions, and define whether you want to trigger on over or under levels — adapting the indicator to your exact logic and style.

🟩 Chart Type Selection

You're no longer limited to candlestick charts! Now you can use Vix_Fix with different chart formats, including:

Candlestick

Heikin Ashi

Renko

Kagi

Line Break

Point & Figure

🟩 Multi-Timeframe Compatibility Without Repainting

Use a different timeframe from your chart with confidence. Signals remain stable and do not repaint. Perfect for spotting long-term reversal setups on lower timeframes.

🟩 Alert System Ready

Configure alerts directly from the indicator’s panel when conditions for over/under signals are met. Stay informed without needing to monitor the chart constantly.

🔷 Technical Details and Customizable Inputs

This indicator includes full control over the logic and appearance:

1️⃣ Length Deviation High - Adjusts the lookback period used to calculate the high deviation level of the VIX logic. Shorter values make it more reactive; longer values smooth out the signal.

2️⃣ Ticker - Choose a different chart type for the calculation, including Heikin Ashi, Renko, Kagi, Line Break, and Point & Figure.

3️⃣ Style VIX - Change the visual style (Line, Histogram, Column, etc.), adjust line width, and optionally invert the display (bottom-to-top).

📌 Fill zones for deviation and percentile are active only in Line and Step Line modes

4️⃣ Use Standard Deviation Up / Down - Enable the overbought and oversold zone logic based on upper and lower standard deviation bands.

5️⃣ Different Type MA (for StdDev) - Choose from 15 different moving averages to define the calculation method for standard deviation (SMA, EMA, HMA, JMA, etc.), with dedicated parameters like Phase, Sigma, and Offset for optimized responsiveness.

6️⃣ BB Length & Multiplier - Adjust the period and multiplier for the standard deviation bands, similar to how Bollinger Bands work.

7️⃣ Show StdDev Up / Down Line - Enable or disable the visibility of upper and lower standard deviation boundaries.

8️⃣ Use Percentile & Length High - Activate the percentile-based logic to detect extreme values in historical volatility using a customizable lookback length.

9️⃣ Highest % / Lowest % - Set the high and low percentile thresholds (e.g., 85 for high, 99 for low) that will be used to trigger over/under signals.

🔟 Show High / Low Percentile Line - Toggle the visual display of the percentile boundaries directly on the chart for clearer signal reference.

1️⃣1️⃣ Ticker Settings – Customize parameters for special chart types such as Renko, Heikin Ashi, Kagi, Line Break, and Point & Figure, adjusting reversal, number of lines, ATR length, etc.

1️⃣2️⃣ Timeframe – Enables using SuperTrend on a higher timeframe.

1️⃣3️⃣ Wait for Timeframe Closes -

✅ Enabled – Displays Vix_Fix smoothly with interruptions.

❌ Disabled – Displays Vix_Fix smoothly without interruptions.

☄️ If you find this indicator useful, leave a Boost to support its development!

Every feedback helps to continuously improve the tool, offering an even more effective trading experience. Share your thoughts in the comments! 🚀🔥

Symbol vs Benchmark Performance & Volatility TableThis tool puts the current symbol’s performance and volatility side-by-side with any benchmark —NASDAQ, S&P 500, NIFTY or a custom index of your choice.

A quick glance shows whether the stock is outperforming, lagging, or just moving with the market.

⸻

Features

• ✅ Returns over 1W, 1M, 3M, 6M, 12M

• 🔄 Benchmark comparison with optional difference row

• ⚡ Volatility snapshot (20D, 60D, or 252D)

• 🎛️ Fully customizable:

• Show/hide rows and timeframes

• Switch between default or custom benchmarks

• Pick position, size, and colors

Built to answer a simple, everyday question — “How’s this really doing compared to the broader market?”

Thanks to @BeeHolder, whose performance table originally inspired this.

Hope it makes your analysis a little easier and quicker.

Navier-Cauchy Market Elasticity [PhenLabs]📊 Navier-Cauchy Market Elasticity

Version: PineScript™ v6

📌 Description

The Navier-Cauchy Market Elasticity (NCME) indicator takes a new step into technical analysis by applying materials science principles to financial markets. Similar to last weeks release utilizing Navier-Stokes dynamics equation this indicator focuses on the elastic interaction of virtual “solids”. Based on elasticity theory used in engineering, NCME treats price movements as material deformations, calculating market stress and strain using proven physics formulas. This unique approach reveals hidden market dynamics invisible to traditional indicators.

By implementing Lamé parameters and Young’s modulus calculations, NCME identifies critical stress points where markets exhibit extreme tension or compression. These zones often precede significant price movements, providing traders with advanced warning of potential reversals or breakouts.

🚀 Points of Innovation

• First indicator to apply Navier-Cauchy elasticity equations to market analysis

• Dynamic stress tensor calculations adapted for one-dimensional price movements

• Real-time Poisson ratio adjustments for market-specific elasticity modeling

• Gradient-based coloring system that visualizes stress intensity variations

• Advanced display modes with customizable visual layers for professional analysis

• Physics-based volatility normalization using Young’s modulus principles

🔧 Core Components

• Elasticity Engine: Calculates market elasticity using volatility-adjusted Young’s modulus

• Stress Tensor System: Computes normal stress values using Lamé parameters (λ and μ)

• Strain Measurement: Tracks price displacement relative to historical movement patterns

• Dynamic Bands: Statistical deviation bands that adapt to market elasticity changes

🔥 Key Features

• Four Display Modes: Choose between Histogram, Line, Both, or Advanced visualization

• Five Color Schemes: Modern, Classic, Neon, Ocean, and Fire themes with gradient support

• Background Stress Zones: Five distinct zones showing market stress levels visually

• Customizable Smoothing: Adjustable period for noise reduction without signal lag

• Extreme Value Detection: Automatic marking of critical stress points with visual alerts

• Advanced Mode Options: Glow effects, momentum ribbon, and extreme dots toggles

🎨 Visualization

• Stress Line: Primary indicator showing real-time market stress with gradient coloring

• Histogram Bars: Normalized stress values with dynamic opacity based on magnitude

• Reference Bands: Primary and secondary deviation bands for context

• Background Zones: Color-coded regions indicating stress intensity levels

• Signal Dots: Markers appearing at extreme stress points for easy identification

📖 Usage Guidelines

Display Settings

• Display Style

○ Default: Advanced

○ Options: Histogram, Line, Both, Advanced

○ Description: Controls visual presentation mode. Advanced offers the most comprehensive view with multiple layers

• Smoothing Period

○ Default: 3

○ Range: 1-50

○ Description: Moving average periods for noise reduction. Higher values create smoother signals but may introduce lag

Elasticity Parameters

• Displacement Length

○ Default: 14

○ Range: 1-100

○ Description: Lookback period for strain calculation. Shorter periods detect rapid stress changes

• Elasticity Length

○ Default: 30

○ Range: 1-200

○ Description: Period for volatility-based elasticity calculation. Longer periods provide more stable readings

• Poisson Ratio

○ Default: 0.3

○ Range: 0-0.5

○ Description: Theoretical elasticity ratio. 0.3 works well for most markets; adjust for specific asset classes

✅ Best Use Cases

• Identifying market tension before major breakouts

• Detecting compression zones during accumulation phases

• Confirming trend strength through stress persistence

• Timing reversals at extreme stress levels

• Multi-timeframe stress analysis for comprehensive market view

⚠️ Limitations

• Requires sufficient price history for accurate elasticity calculations

• May produce false signals during unprecedented market events

• Works best in liquid markets with consistent volume

• Not suitable as a standalone trading system

💡 What Makes This Unique

• Physics-Based Foundation: First indicator to properly implement elasticity theory

• Academic Rigor: Based on proven Navier-Cauchy equations from materials science

• Visual Innovation: Multiple display modes with professional-grade aesthetics

• Adaptive Technology: Self-adjusting parameters based on market conditions

🔬 How It Works

1. Strain Calculation:

• Measures price displacement over specified period

• Normalizes displacement relative to price level

2. Elasticity Determination:

• Calculates Young’s modulus using inverse volatility

• Updates Lamé parameters based on Poisson ratio

3. Stress Computation:

• Applies elasticity theory formula: σ = (λ + 2μ) × ε

• Scales result for visual clarity

• Applies smoothing to reduce noise

💡 Note: NCME represents a breakthrough in applying physics principles to market analysis. While based on proven scientific formulas, remember that markets are complex systems influenced by human psychology and external factors. Use NCME as part of a comprehensive trading strategy with proper risk management.

PhenLabs - Market Fluid Dynamics📊 Market Fluid Dynamics -

Version: PineScript™ v6

📌 Description

The Market Fluid Dynamics - Phen indicator is a new thinking regarding market analysis by modeling price action, volume, and volatility using a fluid system. It attempts to offer traders control over more profound market forces, such as momentum (speed), resistance (thickness), and buying/selling pressure. By visualizing such dynamics, the script allows the traders to decide on the prevailing market flow, its power, likely continuations, and zones of calmness and chaos, and thereby allows improved decision-making.

This measure avoids the usual difficulty of reconciling multiple, often contradictory, market indications by including them within a single overarching model. It moves beyond traditional binary indicators by providing a multi-dimensional view of market behavior, employing fluid dynamic analogs to describe complex interactions in an accessible manner.

🚀 Points of Innovation

Integrated Fluid Dynamics Model: Combines velocity, viscosity, pressure, and turbulence into a single indicator.

Normalized Metrics: Uses ATR and other normalization techniques for consistent readings across different assets and timeframes.

Dynamic Flow Visualization: Main flow line changes color and intensity based on direction and strength.

Turbulence Background: Visually represents market stability with a gradient background, from calm to turbulent.

Comprehensive Dashboard: Provides an at-a-glance summary of key fluid dynamic metrics.

Multi-Layer Smoothing: Employs several layers of EMA smoothing for a clearer, more responsive main flow line.

🔧 Core Components

Velocity Component: Measures price momentum (first derivative of price), normalized by ATR. It indicates the speed and direction of price changes.

Viscosity Component: Represents market resistance to price changes, derived from ATR relative to its historical average. Higher viscosity suggests it’s harder for prices to move.

Pressure Component: Quantifies the force created by volume and price range (close - open), normalized by ATR. It reflects buying or selling pressure.

Turbulence Detection: Calculates a Reynolds number equivalent to identify market stability, ranging from laminar (stable) to turbulent (chaotic).

Main Flow Indicator: Combines the above components, applying sensitivity and smoothing, to generate a primary signal of market direction and strength.

🔥 Key Features

Advanced Smoothing Algorithm: Utilizes multiple EMA layers on the raw flow calculation for a fluid and responsive main flow line, reducing noise while maintaining sensitivity.

Gradient Flow Coloring: The main flow line dynamically changes color from light to deep blue for bullish flow and light to deep red for bearish flow, with intensity reflecting flow strength. This provides an immediate visual cue of market sentiment and momentum.

Turbulence Level Background: The chart background changes color based on calculated turbulence (from calm gray to vibrant orange), offering an intuitive understanding of market stability and potential for erratic price action.

Informative Dashboard: A customizable on-screen table displays critical metrics like Flow State, Flow Strength, Market Viscosity, Turbulence, Pressure Force, Flow Acceleration, and Flow Continuity, allowing traders to quickly assess current market conditions.

Configurable Lookback and Sensitivity: Users can adjust the base lookback period for calculations and the sensitivity of the flow to viscosity, tailoring the indicator to different trading styles and market conditions.

Alert Conditions: Pre-defined alerts for flow direction changes (positive/negative crossover of zero line) and detection of high turbulence states.

🎨 Visualization

Main Flow Line: A smoothed line plotted below the main chart, colored blue for bullish flow and red for bearish flow. The intensity of the color (light to dark) indicates the strength of the flow. This line crossing the zero line can signal a change in market direction.

Zero Line: A dotted horizontal line at the zero level, serving as a baseline to gauge whether the market flow is positive (bullish) or negative (bearish).

Turbulence Background: The indicator pane’s background color changes based on the calculated turbulence level. A calm, almost transparent gray indicates low turbulence (laminar flow), while a more vibrant, semi-transparent orange signifies high turbulence. This helps traders visually assess market stability.

Dashboard Table: An optional table displayed on the chart, showing key metrics like ‘Flow State’, ‘Flow Strength’, ‘Market Viscosity’, ‘Turbulence’, ‘Pressure Force’, ‘Flow Acceleration’, and ‘Flow Continuity’ with their current values and qualitative descriptions (e.g., ‘Bullish Flow’, ‘Laminar (Stable)’).

📖 Usage Guidelines

Setting Categories

Show Dashboard - Default: true; Range: true/false; Description: Toggles the visibility of the Market Fluid Dynamics dashboard on the chart. Enable to see key metrics at a glance.

Base Lookback Period - Default: 14; Range: 5 - (no upper limit, practical limits apply); Description: Sets the primary lookback period for core calculations like velocity, ATR, and volume SMA. Shorter periods make the indicator more sensitive to recent price action, while longer periods provide a smoother, slower signal.

Flow Sensitivity - Default: 0.5; Range: 0.1 - 1.0 (step 0.1); Description: Adjusts how much the market viscosity dampens the raw flow. A lower value means viscosity has less impact (flow is more sensitive to raw velocity/pressure), while a higher value means viscosity has a greater dampening effect.

Flow Smoothing - Default: 5; Range: 1 - 20; Description: Controls the length of the EMA smoothing applied to the main flow line. Higher values result in a smoother flow line but with more lag; lower values make it more responsive but potentially noisier.

Dashboard Position - Default: ‘Top Right’; Range: ‘Top Right’, ‘Top Left’, ‘Bottom Right’, ‘Bottom Left’, ‘Middle Right’, ‘Middle Left’; Description: Determines the placement of the dashboard on the chart.

Header Size - Default: ‘Normal’; Range: ‘Tiny’, ‘Small’, ‘Normal’, ‘Large’, ‘Huge’; Description: Sets the text size for the dashboard header.

Values Size - Default: ‘Small’; Range: ‘Tiny’, ‘Small’, ‘Normal’, ‘Large’; Description: Sets the text size for the metric values in the dashboard.

✅ Best Use Cases

Trend Identification: Identifying the dominant market flow (bullish or bearish) and its strength to trade in the direction of the prevailing trend.

Momentum Confirmation: Using the flow strength and acceleration to confirm the conviction behind price movements.

Volatility Assessment: Utilizing the turbulence metric to gauge market stability, helping to adjust position sizing or avoid choppy conditions.

Reversal Spotting: Watching for divergences between price and flow, or crossovers of the main flow line above/below the zero line, as potential reversal signals, especially when combined with changes in pressure or viscosity.

Swing Trading: Leveraging the smoothed flow line to capture medium-term market swings, entering when flow aligns with the desired trade direction and exiting when flow weakens or reverses.

Intraday Scalping: Using shorter lookback periods and higher sensitivity to identify quick shifts in flow and turbulence for short-term trading opportunities, particularly in liquid markets.

⚠️ Limitations

Lagging Nature: Like many indicators based on moving averages and lookback periods, the main flow line can lag behind rapid price changes, potentially leading to delayed signals.

Whipsaws in Ranging Markets: During periods of low volatility or sideways price action (high viscosity, low flow strength), the indicator might produce frequent buy/sell signals (whipsaws) as the flow oscillates around the zero line.

Not a Standalone System: While comprehensive, it should be used in conjunction with other forms of analysis (e.g., price action, support/resistance levels, other indicators) and not as a sole basis for trading decisions.

Subjectivity in Interpretation: While the dashboard provides quantitative values, the interpretation of “strong” flow, “high” turbulence, or “significant” acceleration can still have a subjective element depending on the trader’s strategy and risk tolerance.

💡 What Makes This Unique

Fluid Dynamics Analogy: Its core strength lies in translating complex market interactions into an intuitive fluid dynamics framework, making concepts like momentum, resistance, and pressure easier to visualize and understand.

Market View: Instead of focusing on a single aspect (like just momentum or just volatility), it integrates multiple factors (velocity, viscosity, pressure, turbulence) to provide a more comprehensive picture of market conditions.

Adaptive Visualization: The dynamic coloring of the flow line and the turbulence background provide immediate, adaptive visual feedback that changes with market conditions.

🔬 How It Works

Price Velocity Calculation: The indicator first calculates price velocity by measuring the rate of change of the closing price over a given ‘lookback’ period. The raw velocity is then normalized by the Average True Range (ATR) of the same lookback period. Normalization enables comparison of momentum between assets or timeframes by scaling for volatility. This is the direction and speed of initial price movement.

Viscosity Calculation: Market ‘viscosity’ or resistance to price movement is determined by looking at the current ATR relative to its longer-term average (SMA of ATR over lookback * 2). The further the current ATR is above its average, the lower the viscosity (less resistance to price movement), and vice-versa. The script inverts this relationship and bounds it so that rising viscosity means more resistance.

Pressure Force Measurement: A ‘pressure’ variable is calculated as a function of the ratio of current volume to its simple moving average, multiplied by the price range (close - open) and normalized by ATR. This is designed to measure the force behind price movement created by volume and intraday price thrusts. This pressure is smoothed by an EMA.

Turbulence State Evaluation: A equivalent ‘Reynolds number’ is calculated by dividing the absolute normalized velocity by the viscosity. This is the proclivity of the market to move in a chaotic or orderly fashion. This ‘reynoldsValue’ is smoothed with an EMA to get the ‘turbulenceState’, which indicates if the market is laminar (stable), transitional, or turbulent.

Main Flow Derivation: The ‘rawFlow’ is calculated by taking the normalized velocity, dampening its impact based on the ‘viscosity’ and user-input ‘sensitivity’, and orienting it by the sign of the smoothed ‘pressureSmooth’. The ‘rawFlow’ is then put through multiple layers of exponential moving average (EMA) smoothing (with ‘smoothingLength’ and derived values) to reach the final ‘mainFlow’ line. The extensive smoothing is designed to give a smooth and clear visualization of the overall market direction and magnitude.

Dashboard Metrics Compilation: Additional metrics like flow acceleration (derivative of mainFlow), and flow continuity (correlation between close and volume) are calculated. All primary components (Flow State, Strength, Viscosity, Turbulence, Pressure, Acceleration, Continuity) are then presented in a user-configurable dashboard for ease of monitoring.

💡 Note:

The “Market Fluid Dynamics - Phen” indicator is designed to offer a unique perspective on market behavior by applying principles from fluid dynamics. It’s most effective when used to understand the underlying forces driving price rather than as a direct buy/sell signal generator in isolation. Experiment with the settings, particularly the ‘Base Lookback Period’, ‘Flow Sensitivity’, and ‘Flow Smoothing’, to find what best suits your trading style and the specific asset you are analyzing. Always combine its insights with robust risk management practices.

Anchored Probability Cone by TenozenFirst of all, credit to @nasu_is_gaji for the open source code of Log-Normal Price Forecast! He teaches me alot on how to use polylines and inverse normal distribution from his indicator, so check it out!

What is this indicator all about?

This indicator draws a probability cone that visualizes possible future price ranges with varying levels of statistical confidence using Inverse Normal Distribution , anchored to the start of a selected timeframe (4h, W, M, etc.)

Feutures:

Anchored Cone: Forecasts begin at the first bar of each chosen higher timeframe, offering a consistent point for analysis.

Drift & Volatility-Based Forecast: Uses log returns to estimate market volatility (smoothed using VWMA) and incorporates a trend angle that users can set manually.

Probabilistic Price Bands: Displays price ranges with 5 customizable confidence levels (e.g., 30%, 68%, 87%, 99%, 99,9%).

Dynamic Updating: Recalculates and redraws the cone at the start of each new anchor period.

How to use:

Choose the Anchored Timeframe (PineScript only be able to forecast 500 bars in the future, so if it doesn't plot, try adjusting to a lower anchored period).

You can set the Model Length, 100 sample is the default. The higher the sample size, the higher the bias towards the overall volatility. So better set the sample size in a balanced manner.

If the market is inside the 30% conifidence zone (gray color), most likely the market is sideways. If it's outside the 30% confidence zone, that means it would tend to trend and reach the other probability levels.

Always follow the trend, don't ever try to trade mean reversions if you don't know what you're doing, as mean reversion trades are riskier.

That's all guys! I hope this indicator helps! If there's any suggestions, I'm open for it! Thanks and goodluck on your trading journey!

Disparity Index with Volatility ZonesDisparity Index with Volatility Zones

is a momentum oscillator that measures the percentage difference between the current price and its simple moving average (SMA). This allows traders to identify overbought/oversold conditions, assess momentum strength, and detect potential trend reversals or continuations.

🔍 Core Concept:

The Disparity Index (DI) is calculated as:

DI = 100 × (Price − SMA) / SMA

A positive DI indicates the price is trading above its moving average (potential bullish sentiment), while a negative DI suggests the price is below the average (potential bearish sentiment).

This version of the Disparity Index introduces a dual-zone volatility framework, offering deeper insight into the market's current state.

🧠 What Makes This Version Unique?

1. High Volatility Zones

When DI crosses above +1.0% or below –1.0%, it often indicates the start or continuation of a strong trend.

Sustained readings beyond these thresholds typically align with trending phases, offering opportunities for momentum-based entries.

A reversal back within ±1.0% after exceeding these levels can suggest a shift in momentum — similar to how RSI exits the overbought/oversold zones before reversals.

These thresholds act as dynamic markers for breakout confirmation and potential trend exhaustion.

2. Low Volatility Zones

DI values between –0.5% and +0.5% define the low-volatility zone, shaded for visual clarity.

This area typically indicates market indecision, sideways price action, or consolidation.

Trading within this range may favor range-bound or mean-reversion strategies, as trend momentum is likely limited.

The logic is similar to interpreting a flat ADX, tight Bollinger Bands, or contracting Keltner Channels — all suggesting consolidation.

⚙️ Features:

Customizable moving average length and input source

Adjustable thresholds for overbought/oversold and low-volatility zones

Optional visual fill between low-volatility bounds

Clean and minimal chart footprint (non-essential plots hidden by default)

📈 How to Use:

1. Trend Confirmation:

A break above +1.0% can be used as a bullish continuation signal.

A break below –1.0% may confirm bearish strength.

Long periods above/below these thresholds support trend-following entries.

2. Reversal Detection:

If DI returns below +1.0% after exceeding it, bullish momentum may be fading.

If DI rises above –1.0% after falling below, bearish pressure may be weakening.

These shifts resemble overbought/oversold transitions in oscillators like RSI or Stochastic, and can be paired with divergence, volume, or price structure analysis for higher reliability.

3. Sideways Market Detection:

DI values within ±0.5% indicate low volatility or a non-trending environment.

Traders may avoid breakout entries during these periods or apply range-trading tactics instead.

Observing transitions out of the low-volatility zone can help anticipate breakouts.

4. Combine with Other Indicators:

DI signals can be enhanced using tools like MACD, Volume Oscillators, or Moving Averages.

For example, a DI breakout beyond ±1.0% supported by a MACD crossover or volume spike can help validate trend initiation.

This indicator is especially powerful when paired with Bollinger Bands:

A simultaneous price breakout from the Bollinger Band and DI moving beyond ±1.0% can help identify early trend inflection points.

This combination supports entering positions early in a developing trend, improving the efficiency of trend-following strategies and enhancing decision-making precision.

It also helps filter false breakouts when DI fails to confirm the move outside the band.

This indicator is designed for educational and analytical purposes and works across all timeframes and asset classes.

It is particularly useful for traders seeking a clear framework to identify momentum strength, filter sideways markets, and improve entry timing within a larger trading system.

MA Dispersion+MA Dispersion+ — read the “breathing space” between your moving-averages

Get instant feedback on trend strength, volatility expansion and mean-reversion — across any timeframe.

MA Dispersion+ turns the humble moving-average stack into a single, easy-to-read oscillator that tells you at a glance whether price is coiling or fanning out.

🧩 What it does

Plugs into your favourite MA setup

• Pick the classic 5 / 20 / 50 / 200 lengths or disable any combination with one click.

• Choose the MA engine you trust — SMA, EMA, RMA, VWMA or WMA.

• Works on any timeframe thanks to TradingView’s security() engine.

Measures “spread”

For every bar it calculates the absolute distance of each selected MA from their average.

The tighter the stack, the lower the value; the wider the fan, the higher the value.

Adds professional-grade controls

• Weighting — let short-term MAs dominate (Inverse Length), keep everything equal, or dial in your own custom weights.

• Normalisation — convert the raw distance into a percentage of price, ATR multiples, or scale by the MAs’ own mean so you can compare symbols of any price or volatility.

🔍 How traders use it

Trend confirmation – rising dispersion while price breaks out = momentum is genuine.

Volatility squeeze – dispersion parking near zero warns that a big move is loading.

Multi-TF outlook – drop one pane per timeframe (e.g. 5 m, 1 h, 1 D) and see which layer of the market is driving.

Mean-reversion plays – spikes that fade quickly often coincide with exhaustion and snap-backs.

⚙️ Quick-start

Add MA Dispersion+ to your chart.

Set the pane’s timeframe in the first input.

Tick the MA lengths you actually use.

(Optional) Pick a weighting scheme and a normaliser.

Repeat the indicator for as many timeframes as you like — each instance keeps its own settings.

✨ Why you’ll love it

Zero clutter – one orange line tells you what four separate MAs whisper.

Configurable yet bullet-proof – all lengths are hard-coded constants, so Pine never complains.

Context aware – normalisation lets you compare BTC’s $60 000 chaos with EURUSD’s four--decimals calm.

Lightweight – no labels, no drawings, no background processing — perfect for mobile and multi-pane layouts.

Give MA Dispersion+ a try and let your charts breathe — you’ll never look at moving-average ribbons the same way again.

Happy trading!

BTC vs ALT Lag Detector [MEXC Overlay]This indicator monitors the price movement of Bitcoin (BTC) and compares it in real time to a customizable list of major altcoins on the MEXC exchange.

It helps you identify lagging altcoins — tokens that are underperforming or overperforming BTC’s price action over a selected timeframe. These temporary deviations can offer profitable entry or rotation opportunities, especially for scalpers, day traders, and arbitrage-style strategies.

Key Features:

- Real-time deviation detection between BTC and altcoins

- Customizable comparison timeframe: 1m, 6m, 12m, 30m, 1h, 4h, or 1d

- Deviation threshold alert: Highlights coins that lag BTC by more than 0.5%, 1%, 2%, or 3%

- Compact stats table embedded in the price chart

- Fully adjustable layout: Table position (Top/Bottom/Center + Left/Right), Font size (Tiny, Small, Medium)

- Built-in alert system when deviation exceeds your chosen threshold

How to Use It:

Set your desired timeframe for comparison (e.g., 1 hour).

Select a deviation threshold (e.g., 1.0%).

The table will show:

Each altcoin’s % change

BTC’s % change

The delta (deviation) vs BTC

Red highlights indicate alts whose deviation exceeded the threshold.

When at least one alt lags beyond your threshold, the indicator can trigger an alert — helping you capitalize on potential catch-up trades.

Please provide any feedback on it.

Market Structure Confluence [AlgoAlpha]OVERVIEW

This script is called "Market Structure Confluence" and it combines classic market structure analysis with a dynamic volatility-based band system to detect shifts in trend and momentum more reliably. It tracks key swing points (higher highs, higher lows, lower highs, lower lows) to define the trend, then overlays a basis and ATR-smoothed volatility bands to catch rejection signals and highlight potential inflection points in the market.

CONCEPTS

Market structure is the foundation of price action trading, focusing on the relationship between successive highs and lows to understand trend conditions. Break of Structure (BOS) and Change of Character (CHoCH) events are important because they signal when a market might be shifting direction. This script enhances traditional structure by integrating volatility bands, which act like dynamic support/resistance zones based on ATR, allowing it to capture momentum surges and rejections beyond just structural shifts.

FEATURES

Swing Detection: It detects and labels Higher Highs (HH), Higher Lows (HL), Lower Highs (LH), and Lower Lows (LL) based on user-defined time horizons, helping traders quickly spot the trend direction.

BOS and CHoCH Lines: When a previous swing point is broken, the script automatically plots a Break of Structure (BOS) line. If the break represents a major trend reversal (a CHoCH), it is marked differently to separate simple breakouts from real trend changes.

Rejection Signals: Special arrows plot when price pierces a band and then pulls back, suggesting a potential trap move or rejection signal in the direction of the new structure.

Alerts: Built-in alerts for structure breaks, CHoCHs, swing points, rejections at bands, and trend flips make it easy to automate setups without manually watching the chart.

USAGE

Set your preferred swing detection size depending on your timeframe and trading style — smaller numbers for intraday, larger numbers for swing trading. Choose whether you want BOS/CHoCH confirmed by candle closes or by wick breaks. Use the volatility band settings to fine-tune how tightly or loosely the bands hug the price, adjusting sensitivity based on market conditions. When a BOS or CHoCH occurs, or when a rejection happens at the bands, the script will highlight it clearly and optionally trigger alerts. Watch for combinations where both structure breaks and volatility band rejections happen together — those are high-quality trade signals. This setup works best when used with basic trend filtering and higher timeframe confirmation.

Machine Learning | Adaptive Trend Signals [Bitwardex]⚙️🧠Machine Learning | Adaptive Trend Signals

🔷Overview

Machine Learning | Adaptive Trend Signals is a Pine Script™ v6 indicator designed to visualize market trends and generate signals through a combination of volatility clustering, Gaussian smoothing, and adaptive trend calculations. Built as an overlay indicator, it integrates advanced techniques inspired by machine learning concepts, such as K-Means clustering, to adapt to changing market conditions. The script is highly customizable, includes a backtesting module, and supports alert conditions, making it suitable for traders exploring trend-based strategies and developers studying volatility-driven indicator design.

🔷Functionality

The indicator performs the following core functions:

• Volatility Clustering: Uses K-Means clustering to categorize market volatility into high, medium, and low states, adjusting trend sensitivity accordingly.

• Trend Calculation: Computes adaptive trend lines (SmartTrend) based on volatility-adjusted standard deviation, smoothed RSI, and ADX filters.

• Signal Generation: Identifies potential buy and sell points through trend line crossovers and directional confirmation.

• Backtesting Module: Tracks trade outcomes based on the SmartTrend3 value, displaying win rate and total trades.

• Visualization: Plots trend lines with gradient colors and optional signal markers (bullish 🐮 and bearish 🐻).

• Alerts: Provides configurable alerts for trend shifts and volatility state changes.

🔷Technical Methodology

Volatility Clustering with K-Means

The indicator employs a K-Means clustering algorithm to classify market volatility, measured via the Average True Range (ATR), into three distinct clusters:

• Data Collection: Gathers ATR values over a user-defined training period (default: 100 bars).

• Centroid Initialization: Sets initial centroids at the highest, lowest, and midpoint ATR values within the training period.

• Iterative Clustering: Assigns ATR data points to the nearest centroid, recalculates centroid means, and repeats until convergence.

• Dynamic Adjustment: Assigns a volatility state (high, medium, or low) based on the closest centroid, adjusting the trend factor (e.g., tighter for high volatility, wider for low volatility).

This approach allows the indicator to adapt its sensitivity to varying market conditions, providing a data-driven foundation for trend calculations.

🔷Gaussian Smoothing

To enhance signal clarity and reduce noise, the indicator applies Gaussian kernel smoothing to:

• RSI: Smooths the Relative Strength Index (calculated from OHLC4) to filter short-term fluctuations.

• SmartTrend: Smooths the primary trend line for a more stable output.

The Gaussian kernel uses a sigma value derived from the user-defined smoothing length, ensuring mathematically consistent noise reduction.

🔷SmartTrend Calculation

The pineSmartTrend function is the core of the indicator, producing three trend lines:

• SmartTrend: The primary trend line, calculated using a volatility-adjusted standard deviation, smoothed RSI, and ADX conditions.

• SmartTrend2: A secondary trend line with a wider factor (base factor * 1.382) for signal confirmation.

SmartTrend3: The average of SmartTrend and SmartTrend2, used for plotting and backtesting.

Key components of the calculation include: