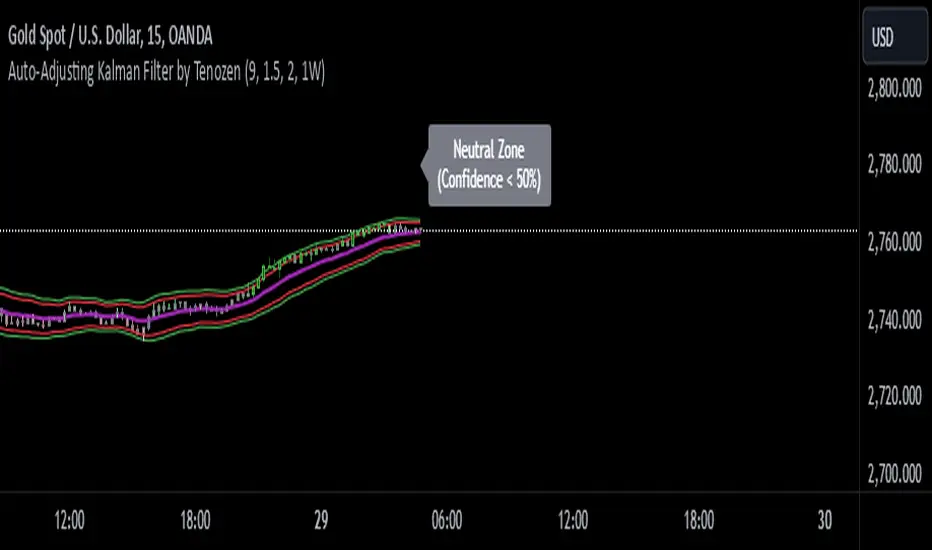

Auto-Adjusting Kalman Filter by TenozenNew year, new indicator! Auto-Adjusting Kalman Filter is an indicator designed to provide an adaptive approach to trend analysis. Using the Kalman Filter (a recursive algorithm used in signal processing), this algo dynamically adjusts to market conditions, offering traders a reliable way to identify trends and manage risk! In other words, it's a remaster of my previous indicator, Kalman Filter by Tenozen.

What's the difference with the previous indicator (Kalman Filter by Tenozen)?

The indicator adjusts its parameters (Q and R) in real-time using the Average True Range (ATR) as a measure of market volatility. This ensures the filter remains responsive during high-volatility periods and smooth during low-volatility conditions, optimizing its performance across different market environments.

The filter resets on a user-defined timeframe, aligning its calculations with dominant trends and reducing sensitivity to short-term noise. This helps maintain consistency with the broader market structure.

A confidence metric, derived from the deviation of price from the Kalman filter line (measured in ATR multiples), is visualized as a heatmap:

Green : Bullish confidence (higher values indicate stronger trends).

Red : Bearish confidence (higher values indicate stronger trends).

Gray : Neutral zone (low confidence, suggesting caution).

This provides a clear, objective measure of trend strength.

How it works?

The Kalman Filter estimates the "true" price by filtering out market noise. It operates in two steps, that is, prediction and update. Prediction is about projection the current state (price) forward. Update is about adjusting the prediction based on the latest price data. The filter's parameters (Q and R) are scaled using normalized ATR, ensuring adaptibility to changing market conditions. So it means that, Q (Process Noise) increases during high volatility, making the filter more responsive to price changes and R (Measurement Noise) increases during low volatility, smoothing out the filter to avoid overreacting to minor fluctuations. Also, the trend confidence is calculated based on the deviation of price from the Kalman filter line, measured in ATR multiples, this provides a quantifiable measure of trend strength, helping traders assess market conditions objectively.

How to use?

Use the Kalman Filter line to identify the prevailing trend direction. Trade in alignment with the filter's slope for higher-probability setups.

Look for pullbacks toward the Kalman Filter line during strong trends (high confidence zones)

Utilize the dynamic stop-loss and take-profit levels to manage risk and lock in profits

Confidence Heatmap provides an objective measure of market sentiment, helping traders avoid low-confidence (neutral) zones and focus on high-probability opportunities

Guess that's it! I hope this indicator helps! Let me know if you guys got some feedback! Ciao!

Volatilty

Market Pressure Index [AlgoAlpha]The Market Pressure Index is a cutting-edge trading tool designed to measure and visualize bullish and bearish momentum through a unique blend of volatility analysis and dynamic smoothing techniques. This indicator provides traders with an intuitive understanding of market pressure, making it easier to identify trend shifts, breakout opportunities, and key moments to take profit. Perfect for scalpers and swing traders looking for a strategic edge in volatile markets.

Key Features:

🔎 Bullish and Bearish Volatility Separation : Dynamically calculates and displays bullish and bearish momentum separately, helping traders assess market direction with precision.

🎨 Customizable Appearance: Set your preferred colors for bullish and bearish signals to match your chart's theme.

📊 Deviation-Based Upper Band : Tracks extreme volatility levels using a configurable deviation multiplier, highlighting potential breakout points.

📈 Real-Time Signal Alerts : Provides alerts for bullish and bearish crossovers, as well as take-profit signals, ensuring you never miss key market movements.

⚡ Gradient-Based Visualization : Uses color gradients to depict the intensity of market pressure, making it easy to spot changes in momentum at a glance.

How to Use:

Add the Indicator : Add the Market Pressure Index to your TradingView chart by clicking the star icon. Customize inputs like the pressure lookback period, deviation settings, and colors to fit your trading style.

Interpret the Signals : Monitor the bullish and bearish momentum columns to gauge market direction. Look for crossovers to signal potential trend changes.

Take Action : Use alerts for breakouts above the upper band or for take-profit levels to enhance your trade execution.

How It Works:

The Market Pressure Index separates bullish and bearish momentum by analyzing price movement (close vs. open) and volatility. These values are smoothed using Hull Moving Averages (HMA) to highlight trends while minimizing noise. A deviation-based upper band dynamically tracks market extremes, signaling breakout zones. Color gradients depict the intensity of momentum, offering a clear, visually intuitive representation of market pressure. Alerts are triggered when significant crossovers or take-profit conditions occur, giving traders actionable insights without constant chart monitoring.

Sharpe and Sortino Ratios with Date RangeThis indicator calculates the Sharpe and Sortino ratios using a chart symbol's periodic price returns.

I added the ability to calculate SORTINO and Sharpe based on CUSTOM DATES within the option menu.

It builds on the script here: by adding this feature.

A little about the Sortino Ratio.

www.nasdaq.com

I want equity market returns, but I don’t want equity market volatility. This is the sentiment many investors naturally feel. This sentiment often grows stronger as one approaches or is in the phase where they desire distributions from their savings to improve lifestyle. This is why there is a need for active management in the investment arena. The desire to control downside volatility, but also participate in the upside growth is a very fundamental human desire. The Sortino Ratio measures how well a particular investment meets this fundamental human desire.

There is the old adage, “volatility is the price you pay for returns.” However, what if we could measure the historical performance of an investment and see if it has given above average returns compared to the downside volatility. This is a simple division problem. It will tell us if the volatility “price we are paying for returns” is good. We can then compare that to other investments to see how they compare.

Let us take the return and subtract the risk-free interest rate and then simply divide that by the downside movement from the average. A basic division problem yielding a number that measures a very basic human desire: How well did this investment do compared to the downside risk it experienced.

In the world of financial analysis and investment management, ratios are abundant. There are many ratios that are truly important to a particular analysis. However, the sheer abundance of ratios that are available often overwhelms the casual investor, leading them to disregard ratios altogether. I would argue for those investors that desire a way to rank an investment by its ability to satisfy this very fundamental human desire, the Sortino Ratio is the number they need to consider.

Disappointing in the marketplace for research, the Sortino Ratio is not featured prominently. It is much easier to find the inflows a particular ETF has experienced than the Sortino Ratio. Inflows are important. They measure how much people are investing into an ETF. However, they are mostly only important to the fund manager, not the investor. What investors care about is the Risk-Adjusted Return. This is the Sortino Ratio.

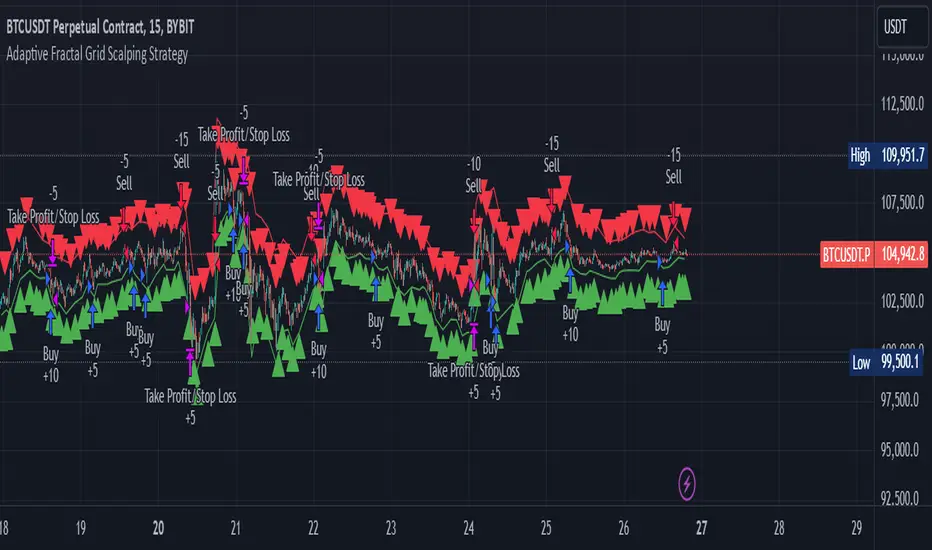

Adaptive Fractal Grid Scalping StrategyThis Pine Script v6 component implements an "Adaptive Fractal Grid Scalping Strategy" with an added volatility threshold feature.

Here's how it works:

Fractal Break Detection: Uses ta.pivothigh and ta.pivotlow to identify local highs and lows.

Volatility Clustering: Measures volatility using the Average True Range (ATR).

Adaptive Grid Levels: Dynamically adjusts grid levels based on ATR and user-defined multipliers.

Directional Bias Filter: Uses a Simple Moving Average (SMA) to determine trend direction.

Volatility Threshold: Introduces a new input to specify a minimum ATR value required to activate the strategy.

Trade Execution Logic: Places limit orders at grid levels based on trend direction and fractal levels, but only when ATR exceeds the volatility threshold.

Profit-Taking and Stop-Loss: Implements profit-taking at grid levels and a trailing stop-loss based on ATR.

How to Use

Inputs: Customize the ATR length, SMA length, grid multipliers, trailing stop multiplier, and volatility threshold through the input settings.

Visuals: The script plots fractal points and grid levels on the chart for easy visualization.

Trade Signals: The strategy automatically places buy/sell orders based on the detected fractals, trend direction, and volatility threshold.

Profit and Risk Management: The script includes logic for taking profits and setting stop-loss levels to manage trades effectively.

This strategy is designed to capitalize on micro-movements during high volatility and avoid overtrading during low-volatility trends. Adjust the input parameters to suit your trading style and market conditions.

RSI Volatility Suppression Zones [BigBeluga]RSI Volatility Suppression Zones is an advanced indicator that identifies periods of suppressed RSI volatility and visualizes these suppression zones on the main chart. It also highlights breakout dynamics, giving traders actionable insights into potential market momentum.

🔵 Key Features:

Detection of Suppression Zones:

Identifies periods where RSI volatility is suppressed and marks these zones on the main price chart.

Breakout Visualization:

When the price breaks above the suppression zone, the box turns aqua, and an upward label is drawn to indicate a bullish breakout.

If the price breaks below the zone, the box turns purple, and a downward label is drawn for a bearish breakout.

Breakouts accompanied by a "+" label represent strong moves caused by short-lived, tight zones, signaling significant momentum.

Wave Labels for Consolidation:

If the suppression zone remains unbroken, a "wave" label is displayed within the gray box, signifying continued price stability within the range.

Gradient Intensity Below RSI:

A gradient strip below the RSI line increases in intensity based on the duration of the suppressed RSI volatility period.

This visual aid helps traders gauge how extended the low volatility phase is.

🔵 Usage:

Identify Breakouts: Use color-coded boxes and labels to detect breakouts and their direction, confirming potential trend continuation or reversals.

Evaluate Market Momentum: Leverage "+" labels for strong breakout signals caused by short suppression phases, indicating significant market moves.

Monitor Price Consolidation: Observe gray boxes and wave labels to understand ongoing consolidation phases.

Analyze RSI Behavior: Utilize the gradient strip to measure the longevity of suppressed volatility phases and anticipate breakout potential.

RSI Volatility Suppression Zones provides a powerful visual representation of RSI volatility suppression, breakout signals, and price consolidation, making it a must-have tool for traders seeking to anticipate market movements effectively.

Trendilo ARTrendilo AR is a custom trading indicator designed to identify market trends using advanced techniques such as the Arnaud Legoux Moving Average (ALMA), volume confirmations, and dynamic volatility bands. This indicator provides a clear visualization of trends, including significant changes and custom alerts.

Review of Indicators Used

1. ALMA

Description:

ALMA is a moving average that applies an advanced filter to smooth price data, reducing noise and focusing on actual trends.

Usage in the Indicator:

Used to calculate the smoothed percentage price change and determine trend direction. Customizable parameters include:

- Length: Defines the number of bars to consider.

- Offset: Adjusts sensitivity toward recent prices.

- Sigma: Controls the degree of smoothing.

Advantages:

- Reduced lag in trend detection.

- Resistance to market noise.

2. ATR

Description:

ATR measures the market’s average volatility by considering the range between high and low prices over a given period.

Usage in the Indicator:

ATR is used to calculate "dynamic smoothing", adjusting the indicator’s sensitivity based on current market volatility.

Advantages:

- Adapts to high or low volatility conditions.

- Helps define dynamic support and resistance levels.

3. SMA

Description:

SMA calculates the average of prices or volume over a specific time period.

Usage in the Indicator:

Used to calculate the volume moving average (Volume SMA) to confirm whether the current volume supports the detected trend.

Advantages:

- Easy to understand and calculate.

- Provides volume-based trend confirmation.

4. RMS Bands

Description:

RMS Bands calculate the standard deviation of percentage price changes, creating upper and lower levels that act as overbought and oversold indicators.

Usage in the Indicator:

- Define the range within which the market is considered neutral.

- Crosses above or below the bands indicate trend changes.

Advantages:

- Visual identification of strong trends.

- Helps filter false signals.

Colors and Visuals Used in the Indicator

1. ALMA Line

Colors:

- Green: Indicates a confirmed uptrend (with sufficient volume).

- Red: Indicates a confirmed downtrend (with sufficient volume).

- Gray: Indicates a neutral phase or insufficient volume to confirm a trend.

2. RMS Bands

- Upper and Lower Lines:

- Purple (with transparency): These lines represent the RMS bands (upper and lower) and

adjust opacity based on trend strength.

- Stronger trends result in less transparency (more solid colors).

3. Highlighted Background (Strong Trends)

- Color:

- Light Green (transparent): Highlights a strong trend when the smoothed percentage change (ALMA) exceeds 1.5 times the RMS.

4. Horizontal Lines

- Baseline (0):

- Dark Gray: Serves as a central reference to identify the directionality of percentage changes.

- Additional Line (0.1):

- Blue: A customizable line to mark user-defined key levels.

5. Bar Colors

- Bar Colors:

- Green: When the price is in a confirmed uptrend.

- Red: When the price is in a confirmed downtrend.

- No color: When there is insufficient volume or no clear trend.

How to Use the Indicator

1. Initial Setup

1. Add the Indicator to Your Chart: Copy the code into the Pine Editor on TradingView and apply it to your chart.

2. Customize Parameters: Adjust values based on your trading strategy:

- Smoothing: Controls the level of smoothing for percentage changes.

- Lookback Length: Defines the observation period for calculations.

- Band Multiplier: Adjusts the width of RMS bands.

2. Signal Interpretation

1. Indicator Colors:

- Green: Confirmed uptrend.

- Red: Confirmed downtrend.

- Gray: No clear trend or insufficient volume.

2. RMS Bands:

- If the ALMA line (smoothed percentage change) crosses above the upper RMS band, it signals a potential uptrend.

- If it crosses below the lower RMS band, it signals a potential downtrend.

3. Volume Confirmation:

- The indicator's color activates only if the current volume exceeds the Volume SMA.

3. Alerts and Decisions

1. Trend Change Alerts:

- The indicator automatically triggers alerts when an uptrend or downtrend is detected.

- Configure these alerts to receive real-time notifications.

2. Strong Trend Signals:

- When the magnitude of the percentage change exceeds 1.5 times the RMS, the chart background highlights the strong trend.

4. Trading Strategies

1. Buy:

- Enter long positions when:

- The indicator turns green.

- Volume confirms the trend.

- Consider placing a stop-loss just below the lower RMS band.

2. Sell:

- Enter short positions when:

- The indicator turns red.

- Volume confirms the trend.

- Consider placing a stop-loss just above the upper RMS band.

3. Neutral:

- Avoid trading when the indicator is gray, as no clear trend or insufficient volume is present.

Disclaimer: As this is my first published indicator, please use it with caution. Feedback is highly appreciated to improve its performance.

Happy Trading!

EWMA Volatility Bands

The EWMA Volatility Bands indicator combines an Exponential Moving Average (EMA) and Exponentially Weighted Moving Average (EWMA) of volatility to create dynamic upper and lower price bands. It helps traders identify trends, measure market volatility, and spot extreme conditions. Key features include:

Centerline (EMA): Tracks the trend based on a user-defined period.

Volatility Bands: Adjusted by the square root of volatility, representing potential price ranges.

Percentile Rank: Highlights extreme volatility (e.g., >99% or <1%) with shaded areas between the bands.

This tool is useful for trend-following, risk assessment, and identifying overbought/oversold conditions.

HV-RV Oscillator by DINVESTORQ(PRABIR DAS)Description:

The HV-RV Oscillator is a powerful tool designed to help traders track and compare two types of volatility measures: Historical Volatility (HV) and Realized Volatility (RV). This indicator is useful for identifying periods of market volatility and can be employed in various trading strategies. It plots both volatility measures on a normalized scale (0 to 100) to allow easy comparison and analysis.

How It Works:

Historical Volatility (HV):

HV is calculated by taking the log returns of the closing prices and finding the standard deviation over a specified period (default is 14 periods).

The value is then annualized assuming 252 trading days in a year.

Realized Volatility (RV):

RV is based on the True Range, which is the maximum of the current high-low range, the difference between the high and the previous close, and the difference between the low and the previous close.

Like HV, the standard deviation of the True Range over a specified period is calculated and annualized.

Normalization:

Both HV and RV values are normalized to a 0-100 scale, making it easy to see their relative magnitude over time.

The highest and lowest values within the period are used to normalize the data, which smooths out short-term volatility spikes.

Smoothing:

The normalized values of both HV and RV are then smoothed using a Simple Moving Average (SMA) to reduce noise and provide a clearer trend.

Crossover Signals:

Buy Signal : When the Normalized HV crosses above the Normalized RV, it indicates that the historical volatility is increasing relative to the realized volatility, which could be interpreted as a buy signal.

Sell Signal : When the Normalized HV crosses below the Normalized RV, it suggests that the historical volatility is decreasing relative to the realized volatility, which could be seen as a sell signal.

Features:

Two Volatility Lines: The blue line represents Normalized HV, and the orange line represents Normalized RV.

Neutral Line: A gray dashed line at the 50 level indicates a neutral state between the two volatility measures.

Buy/Sell Markers: Green upward arrows are shown when the Normalized HV crosses above the Normalized RV, and red downward arrows appear when the Normalized HV crosses below the Normalized RV.

Inputs:

HV Period: The number of periods used to calculate Historical Volatility (default = 14).

RV Period: The number of periods used to calculate Realized Volatility (default = 14).

Smoothing Period: The number of periods used for smoothing the normalized values (default = 3).

How to Use:

This oscillator is designed for traders who want to track the relationship between Historical Volatility and Realized Volatility.

Buy signals occur when HV increases relative to RV, which can indicate increased market movement or potential breakout conditions.

Sell signals occur when RV is greater than HV, signaling reduced volatility or potential trend exhaustion.

Example Use Cases:

Breakout/Trend Strategy: Use the oscillator to identify potential periods of increased volatility (when HV crosses above RV) for breakout trades.

Mean Reversion: Use the oscillator to detect periods of low volatility (when RV crosses above HV) that might signal a return to the mean or consolidation.

This tool can be used on any asset class such as stocks, forex, commodities, or indices to help you make informed decisions based on the comparison of volatility measures.

NOTE: FOR INTRDAY PURPOSE USE 30/7/9 AS SETTING AND FOR DAY TRADE USE 14/7/9

Catalyst TrendCatalyst Trend – A Comprehensive Trend and Regime Analyzer

The Catalyst Trend indicator was designed to dynamically and intuitively merge various classic analytical techniques. The goal is to filter out short-term market noise and reveal reliable trend phases or potential turning points. Below is a detailed explanation of its core elements and practical usage.

1. Concept and Idea

Multidimensional Trend Detection

This indicator goes beyond a simple momentum or volatility focus. It factors in multiple measurements to provide a more well-rounded market perspective.

Versatile Indicator Fusion

Linear Regression (LinReg): Multiple LinReg calculations are combined to smooth out price fluctuations and produce a robust trendline—known here as the “Cycle Reduced Line.”

ADX (Average Directional Index): Measures trend strength.

RSI (Relative Strength Index): Flags potential overbought or oversold conditions, in both the current timeframe and a higher timeframe.

ATR (Average True Range): Assesses volatility; used to dynamically adjust calculation lengths.

By weaving these elements together, the indicator adds value beyond simply stacking multiple indicators. It adapts to real-time market conditions, aiming to highlight genuine trends and reduce false signals.

2. Key Functions and Calculations

Dynamic Length & Smoothing

A blend of volatility (ATR), ADX values, and RSI inputs determines how many candles are used in the LinReg calculations and how heavily the data is smoothed.

This allows the indicator to respond promptly during periods of high volatility, while automatically adjusting to filter out unnecessary noise in quieter phases.c

Cycle Reduced Line

The script averages several offset LinReg calculations to produce a cleaner overall signal. Random outliers are thus minimized, making the trend path more visually consistent.

An additional EMA smoothing (“Final Smoothing”) further stabilizes this trendline, reducing the impact of minor price fluctuations.

Channel Bands (Optional)

These bands are derived from the standard deviation of the price residual (the difference between the smoothed price and the trendline).

They highlight potential over-extension zones: the upper band can mark short-term overbought areas, while the lower band might indicate oversold conditions.

Trend and Sideways Determination

Slope Calculation: The slope of the trendline (comparing the current bar to the previous one) helps identify short-term directional shifts.

DX Threshold: Once the ADX surpasses a user-defined threshold and the slope is positive, it may indicate a developing uptrend. Similarly, if the slope is negative and ADX > threshold, it could signal a potential downtrend.

Multi-Level Color Coding

Original Mode: Interpolated colors reflect uptrends, downtrends, and sideways phases, factoring in metrics like ADX and RSI.

Single Color: For a neutral look, the indicator can be displayed in one uniform color.

HTF RSI: This mode uses the higher-timeframe RSI to color the trendline (Long/Short/Neutral), offering a quick gauge of overarching market pressure.

3. Use Cases and Interpretation

Timeframes & Markets

The indicator is versatile and adapts well to different intervals, from 5-minute charts to weekly views.

It can be applied to various markets—crypto, forex, stocks—since volatility and trend strength are universal concepts.

Signal Recognition

Color Swings into a more pronounced upward hue (e.g., green) may signal mounting strength.

Neutral or mixed tones often point to sideways phases, which breakout traders might watch for potential price surges.

A shift to downward colors (e.g., red) may indicate a growing bearish trend.

Channel Bands & Volatility

When the bands spread widely, it’s wise to proceed with caution: abrupt spikes above the upper band or below the lower band can flag rapid short-term extremes.

These bands are more of a reference for potential overextension than a strict buy or sell trigger.

Additional Confirmations

Not a standalone panacea: The Catalyst Trend indicator is an analytical tool, best used alongside other methods such as volume analysis or price action (candlestick patterns, support/resistance levels) to bolster confidence in trading decisions.

4. Practical Tips

Parameter Adjustments

Depending on the market—crypto vs. traditional currency pairs—different ADX, RSI, or smoothing periods may be more effective. Experiment with the settings to tailor the indicator to your preferred timeframe.

Strategic Integration

Trailing Stops: For those riding a trend, the trendline or the channel bands may serve as a reference to trail stop-loss orders.

Trend Confirmation: Using RSI and ADX filters can help traders avoid sideways markets or stay the course when the trend is strong.

5. Important Final Notes

No Guarantee of Profits

No indicator can predict the future. Markets are inherently volatile and often unpredictable.

Responsible Risk Management

Test the indicator in a demo environment or with smaller positions before committing to large trades.

300-Candle Weighted Average Zones w/50 EMA SignalsThis indicator is designed to deliver a more nuanced view of price dynamics by combining a custom, weighted price average with a volatility-based zone and a trend filter (in this case, a 50-period exponential moving average). The core concept revolves around capturing the overall price level over a relatively large lookback window (300 candles) but with an intentional bias toward recent market activity (the most recent 20 candles), thereby offering a balance between long-term context and short-term responsiveness. By smoothing this weighted average and establishing a “zone” of standard deviation bands around it, the indicator provides a refined visualization of both average price and its recent volatility envelope. Traders can then look for confluence with a standard trend filter, such as the 50 EMA, to identify meaningful crossover signals that may represent trend shifts or opportunities for entry and exit.

What the Indicator Does:

Weighted Price Average:

Instead of using a simple or exponential moving average, this indicator calculates a custom weighted average price over the past 300 candles. Most historical candles receive a base weight of 1.0, but the most recent 20 candles are assigned a higher weight (for example, a weight of 2.0). This weighting scheme ensures that the calculation is not simply a static lookback average; it actively emphasizes current market conditions. The effect is to generate an average line that is more sensitive to the most recent price swings while still maintaining the historical context of the previous 280 candles.

Smoothing of the Weighted Average:

Once the raw weighted average is computed, an exponential smoothing function (EMA) is applied to reduce noise and produce a cleaner, more stable average line. This smoothing helps traders avoid reacting prematurely to minor price fluctuations. By stabilizing the average line, traders can more confidently identify actual shifts in market direction.

Volatility Zone via Standard Deviation Bands:

To contextualize how far price can deviate from this weighted average, the indicator uses standard deviation. Standard deviation is a statistical measure of volatility—how spread out the price values are around the mean. By adding and subtracting one standard deviation from the smoothed weighted average, the indicator plots an upper band and a lower band, creating a zone or channel. The area between these bands is filled, often with a semi-transparent color, highlighting a volatility corridor within which price and the EMA might oscillate.

This zone is invaluable in visualizing “normal” price behavior. When the 50 EMA line and the weighted average line are both within this volatility zone, it indicates that the market’s short- to mid-term trend and its average pricing are aligned well within typical volatility bounds.

Incorporation of a 50-Period EMA:

The inclusion of a commonly used trend filter, the 50 EMA, adds another layer of context to the analysis. The 50 EMA, being a widely recognized moving average length, is often considered a baseline for intermediate trend bias. It reacts faster than a long-term average (like a 200 EMA) but is still stable enough to filter out the market “chop” seen in very short-term averages.

By overlaying the 50 EMA on this custom weighted average and the surrounding volatility zone, the trader gains a dual-dimensional perspective:

Trend Direction: If the 50 EMA is generally above the weighted average, the short-term trend is gaining bullish momentum; if it’s below, the short-term trend has a bearish tilt.

Volatility Normalization: The bands, constructed from standard deviations, provide a sense of whether the price and the 50 EMA are operating within a statistically “normal” range. If the EMA crosses the weighted average within this zone, it signals a potential trend initiation or meaningful shift, as opposed to a random price spike outside normal volatility boundaries.

Why a Trader Would Want to Use This Indicator:

Contextualized Price Level:

Standard MAs may not fully incorporate the most recent price dynamics in a large lookback window. By weighting the most recent candles more heavily, this indicator ensures that the trader is always anchored to what the market is currently doing, not just what it did 100 or 200 candles ago.

Reduced Whipsaw with Smoothing:

The smoothed weighted average line reduces noise, helping traders filter out inconsequential price movements. This makes it easier to spot genuine changes in trend or sentiment.

Visual Volatility Gauge:

The standard deviation bands create a visual representation of “normal” price movement. Traders can quickly assess if a breakout or breakdown is statistically significant or just another oscillation within the expected volatility range.

Clear Trade Signals with Confirmation:

By integrating the 50 EMA and designing signals that trigger only when the 50 EMA crosses above or below the weighted average while inside the zone, the indicator provides a refined entry/exit criterion. This avoids chasing breakouts that occur in abnormal volatility conditions and focuses on those crossovers likely to have staying power.

How to Use It in an Example Strategy:

Imagine you are a swing trader looking to identify medium-term trend changes. You apply this indicator to a chart of a popular currency pair or a leading tech stock. Over the past few days, the 50 EMA has been meandering around the weighted average line, both confined within the standard deviation zone.

Bullish Example:

Suddenly, the 50 EMA crosses decisively above the weighted average line while both are still hovering within the volatility zone. This might be your cue: you interpret this crossover as the 50 EMA acknowledging the recent upward shift in price dynamics that the weighted average has highlighted. Since it occurred inside the normal volatility range, it’s less likely to be a head-fake. You place a long position, setting an initial stop just below the lower band to protect against volatility.

If the price continues to rise and the EMA stays above the average, you have confirmation to hold the trade. As the price moves higher, the weighted average may follow, reinforcing your bullish stance.

Bearish Example:

On the flip side, if the 50 EMA crosses below the weighted average line within the zone, it suggests a subtle but meaningful change in trend direction to the downside. You might short the asset, placing your protective stop just above the upper band, expecting that the statistically “normal” level of volatility will contain the price action. If the price does break above those bands later, it’s a sign your trade may not work out as planned.

Other Indicators for Confluence:

To strengthen the reliability of the signals generated by this weighted average zone approach, traders may want to combine it with other technical studies:

Volume Indicators (e.g., Volume Profile, OBV):

Confirm that the trend crossover inside the volatility zone is supported by volume. For instance, an uptrend crossover combined with increasing On-Balance Volume (OBV) or volume spikes on up candles signals stronger buying pressure behind the price action.

Momentum Oscillators (e.g., RSI, Stochastics):

Before taking a crossover signal, check if the RSI is above 50 and rising for bullish entries, or if the Stochastics have turned down from overbought levels for bearish entries. Momentum confirmation can help ensure that the trend change is not just an isolated random event.

Market Structure Tools (e.g., Pivot Points, Swing High/Low Analysis):

Identify if the crossover event coincides with a break of a previous pivot high or low. A bullish crossover inside the zone aligned with a break above a recent swing high adds further strength to your conviction. Conversely, a bearish crossover confirmed by a breakdown below a previous swing low can make a short trade setup more compelling.

Volume-Weighted Average Price (VWAP):

Comparing where the weighted average zone lies relative to VWAP can provide institutional insight. If the bullish crossover happens while the price is also holding above VWAP, it can mean that the average participant in the market is in profit and that the trend is likely supported by strong hands.

This indicator serves as a tool to balance long-term perspective, short-term adaptability, and volatility normalization. It can be a valuable addition to a trader’s toolkit, offering enhanced clarity and precision in detecting meaningful shifts in trend, especially when combined with other technical indicators and robust risk management principles.

Visual ATR StopThis indicator uses the Average True Range (ATR) to display a visual range for stop placement. Two multiplier values (example, 1 and 3) can be set to create a filled area below the price. This area represents the range between the two ATR levels, adjusted by subtracting the current price, providing a simple way to visualize stop-loss placement based on volatility.

The indicator is customizable; for example, negative values can place the area above the price for short positions. The filled color can also be removed, which allows precise levels to be marked above and below.

GapDetectGap Severity Analysis Library

This library, GapDetect , simplifies the identification and evaluation of overnight gaps by leveraging statistical metrics such as standard deviation and percentage moves. It is ideal for detecting large abnormal gaps which may be used to modify how strategies may decide to enter or exit.

Key Features:

Overnight Gap Detection

Provides two core functions:

today : Computes the value of today's overnight gap.

todayPercent : Computes the percentage change for today's overnight gap.

Volatility Analysis

Includes functions for statistical gap analysis:

normal : Calculates the normal daily standard deviation of the overnight gap, filtering outliers using customizable thresholds.

normalPercent : Similar to normal , but for percentage-based gap moves.

Gap Severity Metric

severity : a positive or negative value that represents the ratio of the current overnight move compared to the standard deviation of previous ones.

Customizable Parameters

Supports custom session specifications, resolutions, and outlier thresholds.

HMA Gaussian Volatility AdjustedOverview

The "HMA Gaussian Volatility Adjusted" indicator introduces a unique combination of HMA smoothing with a Gaussian filter and two components to measure volatility (Average True Range (ATR) and Standard Deviation (SD)). This tool provides traders with a stable and accurate measure of price trends by integrating a Gaussian Filter smoothed using HMA with a customized calculation of volatility. This innovative approach allows for enhanced sensitivity to market fluctuations while filtering out short-term price noise.

Technical Composition and Calculation

The "HMA Gaussian Volatility Adjusted" indicator incorporates HMA smoothing and dynamic standard deviation calculations to build upon traditional volatility measures.

HMA & Gaussian Smoothing:

HMA Calculation (HMA_Length): The script applies a Hull Moving Average (HMA) to smooth the price data over a user-defined period, reducing noise and helping focus on broader market trends.

Gaussian Filter Calculation (Length_Gaussian): The smoothed HMA data is further refined by putting it into a Gaussian filter to incorporate a normal distribution.

Volatility Measurement:

ATR Calculation (ATR_Length, ATR_Factor): The indicator incorporates the Average True Range (ATR) to measure market volatility. The user-defined ATR multiplier is applied to this value to calculate upper and lower trend bands around the Gaussian, providing a dynamic measure of potential price movement based on recent volatility.

Standard Deviation Calculation (SD_Length): The script calculates the standard deviation of the price over a user-defined length, providing another layer of volatility measurement. The upper and lower standard deviation bands (SDD, SDU) act as additional indicators of price extremes.

Momentum Calculation & Scoring

When the indicator signals SHORT:

Diff = Price - Upper Boundary of the Standard Deviation (calculated on a Gaussian filter).

When the indicator signals LONG:

Diff = Price - Upper Boundary of the ATR (calculated on a Gaussian filter).

The calculated Diff signals how close the indicator is to changing trends. An EMA is applied to the Diff to smooth the data. Positive momentum occurs when the Diff is above the EMA, and negative momentum occurs when the Diff is below the EMA.

Trend Detection

Trend Logic: The indicator uses the calculated bands to identify whether the price is moving within or outside the standard deviation and ATR bands. Crosses above or below these bands, combined with positive/negative momentum, signals potential uptrends or downtrends, offering traders a clear view of market direction.

Features and User Inputs

The "HMA Gaussian Volatility Adjusted" script offers a variety of user inputs to customize the indicator to suit traders' styles and market conditions:

HMA Length: Allows traders to adjust the sensitivity of the HMA smoothing to control the amount of noise filtered from the price data.

Gaussian Length: Users can define the length at which the Gaussian filter is applied.

ATR Length and Multiplier: These inputs let traders fine-tune the ATR calculation, affecting the size of the dynamic upper and lower bands to adjust for price volatility.

Standard Deviation Length: Controls how the standard deviation is calculated, allowing further customization in detecting price volatility.

EMA Confluence: This input lets traders determine the length of the EMA used to calculate price momentum.

Type of Plot Setting: Allows users to determine how the indicator signal is plotted on the chart (Background color, Trend Lines, BOTH (backgroung color and Trend Lines)).

Transparency: Provides users with customization of the background color's transparency.

Color Long/Short: Offers users the option to choose their preferred colors for both long and short signals.

Summary and Usage Tips

The "HMA Gaussian Volatility Adjusted" indicator is a powerful tool for traders looking to refine their analysis of market trends and volatility. Its combination of HMA smoothing, Gaussian filtering, and standard deviation analysis provides a nuanced view of market movements by incorporating various metrics to determine direction, momentum, and volatility. This helps traders make better-informed decisions. It's recommended to experiment with the various input parameters to optimize the indicator for specific needs.

FRAMA Channel [BigBeluga]This is a trend-following indicator that utilizes the Fractal Adaptive Moving Average (FRAMA) to create a dynamic channel around the price. The FRAMA Channel helps identify uptrends, downtrends, and ranging markets by examining the relationship between the price and the channel's boundaries. It also marks trend changes with arrows, optionally displaying either price values or average volume at these key points.

🔵 IDEA

The core idea behind the FRAMA Channel indicator is to use the fractal nature of markets to adapt to different market conditions. By creating a channel around the FRAMA line, it not only tracks price trends but also adapts its sensitivity based on market volatility. When the price crosses the upper or lower bands of the channel, it signals a potential shift in trend direction. If the price remains within the channel and crosses over the upper or lower bands without a breakout, the market is likely in a ranging phase with low momentum. This adaptive approach makes the FRAMA Channel effective in both trending and ranging market environments.

🔵 KEY FEATURES & USAGE

◉ Dynamic FRAMA Channel with Trend Signals:

The FRAMA Channel uses a fractal-based moving average to create an adaptive channel around the price. When the price crosses above the upper band, it signals an uptrend and plots an upward arrow with the price (or average volume) value. Conversely, when the price crosses below the lower band, it signals a downtrend and marks the point with a downward arrow. This dynamic adaptation to market conditions helps traders identify key trend shifts effectively.

◉ Ranging Market Detection:

If the price remains within the channel, and only the high crosses the upper band or the low crosses the lower band, the indicator identifies a ranging market with low momentum. In this case, the channel turns gray, signaling a neutral trend. This is particularly useful for avoiding false signals during periods of market consolidation.

◉ Color-Coded Candles and Channel Bands:

Candles and channel bands are color-coded to reflect the current trend direction. Green indicates an upward trend, blue shows a downward trend, and gray signals a neutral or ranging market. This visual representation makes it easy to identify the market condition at a glance, helping traders make informed decisions quickly.

◉ Customizable Display of Price or Average Volume:

On trend change signals, the indicator allows users to choose whether to display the price at the point of trend change or the average volume of 10 bars. This flexibility enables traders to focus on the information that is most relevant to their strategy, whether it's the exact price entery or the volume context of the market shift. Displaying the average volume allows to see the strength of the trend change.

Price Data:

Average Volume of points:

🔵 CUSTOMIZATION

Length & Bands Distance: Adjust the length for the FRAMA calculation to control the sensitivity of the channel. A shorter length makes the channel more reactive to price changes, while a longer length smooths it out. The Bands Distance setting determines how far the bands are from the FRAMA line, helping to define the breakout and ranging conditions.

Signals Data: Choose between displaying the price or the average volume on trend change arrows. This allows traders to focus on either the exact price level of trend change or the market volume context.

Color Settings: Customize the colors for upward momentum, downward momentum, and neutral states to suit your charting preferences. You can also toggle whether to color the candles based on the momentum for a clearer visual of the trend direction.

The FRAMA Channel indicator adapts to market conditions, providing a versatile tool for identifying trends and ranging markets with clear visual cues.

Volatility % (Standard Deviation of Returns)This script takes closing prices of candles to measure the Standard Deviation (σ) which is then used to calculate the volatility by taking the stdev of the last 30 candles and multiplying it by the root of the trading days in a year, month and week. It then multiplies that number by 100 to show a percentage.

Default settings are annual volatility (252 candles, red), monthly volatility (30 candles, blue) and weekly volatility (5 candles, green) if you use daily candles. It is open source so you can increase the number of candles with which the stdev is calculated, and change the number of the root that multiplies the stdev.

Multifactor Buy/Sell Strategy V2 | RSI, MACD, ATR, EMA, Boll.BITGET:1INCHUSDT

This Pine Script code for TradingView is a multifactor Buy/Sell indicator that combines several technical factors to generate trading signals based on trend, volatility, and volume conditions. Here’s a breakdown of the main components and functionality:

Indicator Name

- Multifactor Buy/Sell Strategy V2 — an overlay indicator applied directly on the price chart.

### Input Parameters

The script includes multiple customizable parameters:

- RSI, EMA, MACD parameters — for setting periods and signals of MACD and RSI.

- ATR and Bollinger Bands — used for volatility analysis and level determination.

- Minimum Volatility Threshold — sets a minimum Bollinger Band width threshold for determining high volatility.

Core Indicators

1. RSI — calculated to identify oversold (below 30) and overbought (above 70) conditions.

2. EMA and MACD — calculates exponential moving averages and MACD histogram to determine trend direction.

3. ATR and Bollinger Bands — used to assess current volatility and establish dynamic upper and lower bands.

Volatility and Volume Analysis

- Determines the current ATR level and Bollinger Band width to evaluate high volatility.

- Calculates the volume moving average to track periods of increased volume during high volatility.

Trend Analysis

The script uses the difference between fast and slow EMAs to define strong trends:

- Uptrend — when the fast EMA is above the slow EMA, the price is above the fast EMA, and the trend is strong.

- Downtrend — when the fast EMA is below the slow EMA, the price is below the fast EMA, and the trend is strong.

Momentum Filter

- Based on the price change over the last three bars and compared against the minimum volatility threshold to identify strong momentum.

Buy and Sell Signal Generation

- Buy Signal: Uptrend with RSI oversold, positive MACD histogram, high volatility and volume, strong momentum, and sufficient Bollinger Band width.

- Sell Signal: Downtrend with RSI overbought, negative MACD histogram, high volatility and volume, strong momentum, and sufficient Bollinger Band width.

Visualization

- Buy and sell signals are displayed as green and red triangles on the chart.

- Plots for fast and slow EMAs, upper and lower bands, and Bollinger Bands.

Alerts

The script includes alert conditions for buy and sell signals, allowing notifications to be sent via email or mobile app.

Information Panel

A small table on the chart displays current volatility dataThis Pine Script code for TradingView is a multifactor Buy/Sell indicator that combines several technical factors to generate trading signals based on trend, volatility, and volume conditions. Here’s a breakdown of the main components and functionality:

Indicator Name

- Multifactor Buy/Sell Strategy V2 — an overlay indicator applied directly on the price chart.

Input Parameters

The script includes multiple customizable parameters:

- **RSI, EMA, MACD parameters** — for setting periods and signals of MACD and RSI.

- **ATR and Bollinger Bands** — used for volatility analysis and level determination.

- **Minimum Volatility Threshold** — sets a minimum Bollinger Band width threshold for determining high volatility.

Core Indicators

1. RSI — calculated to identify oversold (below 30) and overbought (above 70) conditions.

2. EMA and MACD — calculates exponential moving averages and MACD histogram to determine trend direction.

3. ATR and Bollinger Bands — used to assess current volatility and establish dynamic upper and lower bands.

Volatility and Volume Analysis

- Determines the current ATR level and Bollinger Band width to evaluate high volatility.

- Calculates the volume moving average to track periods of increased volume during high volatility.

Trend Analysis

The script uses the difference between fast and slow EMAs to define strong trends:

- Uptrend — when the fast EMA is above the slow EMA, the price is above the fast EMA, and the trend is strong.

- Downtrend — when the fast EMA is below the slow EMA, the price is below the fast EMA, and the trend is strong.

Momentum Filter

- Based on the price change over the last three bars and compared against the minimum volatility threshold to identify strong momentum.

Buy and Sell Signal Generation

- Buy Signal: Uptrend with RSI oversold, positive MACD histogram, high volatility and volume, strong momentum, and sufficient Bollinger Band width.

- Sell Signal: Downtrend with RSI overbought, negative MACD histogram, high volatility and volume, strong momentum, and sufficient Bollinger Band width.

Visualization

- Buy and sell signals are displayed as green and red triangles on the chart.

- Plots for fast and slow EMAs, upper and lower bands, and Bollinger Bands.

Alerts

The script includes alert conditions for buy and sell signals, allowing notifications to be sent via email or mobile app.

Information Panel

A small table on the chart displays current volatility

- Volatility Status — indicates high or low volatility.

- Bollinger Band Width — current width as a percentage.

- ATR Ratio — ratio of current ATR to long-term average ATR.

This script is suitable for trading in high-volatility conditions, combining multiple filters and factors to generate precise buy and sell signals.

Rolling ATR Bands | Flux Charts💎 GENERAL OVERVIEW

Introducing the Rolling ATR Bands indicator! This indicator overlays adaptive bands around the price, using the Average True Range (ATR) to define dynamic support and resistance levels. The Rolling ATR Bands are color-coded to visually indicate potential trend strength, shifting between bearish, neutral, and bullish colors. This tool can help traders interpret price volatility, as well as identify probable trend changes, continuations, or reversals. For more information about the process, check the "HOW DOES IT WORK ?" section.

Features of the new Rolling ATR Bands:

ATR Bands With Customizable ATR Length & Multiplier

Smooth Trend Strength With Adjustable Smoothing Options

Color-coded bands Representing Bearish, Neutral, or Bullish Trends

Alerts for Retests & Breaks

Customizable Visuals

📌 HOW DOES IT WORK?

The Rolling ATR Bands indicator calculates the ATR based on the specified length and multiplier to form upper and lower bands around the price. These bands adapt with market volatility, widening during high volatility and contracting during lower volatility periods.

In addition, the indicator calculates a "trend strength" score by combining an interpolated RSI, Supertrend, and EMA crossover. This score is smoothed with a customizable length, and a color gradient is applied to visually denote the strength of bearish, neutral, or bullish conditions.

Here's how to interpret the bands:

Upper Band: Acts as dynamic resistance; when price approaches or touches it, this often suggests potential overbought conditions.

Lower Band: Acts as dynamic support; touching or nearing this band might indicate potential oversold conditions.

Color Shifts: Color changes indicate shifts in trend direction. For example, a green color suggests a bullish trend, while red hints at bearish tendencies.

🚩 UNIQUENESS

What sets the Rolling ATR Bands apart is the combined use of interpolated RSI, Supertrend, and EMA cross values, creating a weighted trend strength score. This integration allows for nuanced, color-coded visual cues that respond quickly to trend changes without excessive noise, offering traders an intuitive view of both trend direction and potential momentum. You can also set up alerts for retest & alerts for upper and lower bands to get informed of potential movements.

⚙️ SETTINGS

1. General Configuration

ATR Length : Controls the ATR calculation length for the bands.

Smoothing: Adjusts the trend strength smoothing to control sensitivity to trend changes.

ATR Multiplier : Sets the width of the bands by multiplying the ATR value.

Trend Smoothing : Higher settings will result in longer periods of time required for trend to change direction from bullish to bearish and vice versa.

Relative Measured Volatility (RMV) – Spot Tight Entry ZonesTitle: Relative Measured Volatility (RMV) – Spot Tight Entry Zones

Introduction

The Relative Measured Volatility (RMV) indicator is designed to highlight tight price consolidation zones , making it an ideal tool for traders seeking optimal entry points before potential breakouts. By focusing on tightness rather than general volatility, RMV offers traders a practical way to detect consolidation phases that often precede significant market moves.

How RMV Works

The RMV calculates short-term tightness by averaging three ATR (Average True Range) values over different lookback periods and then normalizing them within a specified lookback window. The result is a percentage-based scale from 0 to 100, indicating how tight the current price range is compared to recent history.

Here’s the breakdown:

Three ATR values are computed using user-defined short lookback periods to represent short-term price movements. An average of the ATRs provides a smoothed measure of current tightness. The RMV normalizes this average against the highest and lowest values over the defined lookback period, scaling it from 0 to 100.

This approach helps traders identify consolidation zones that are more likely to lead to breakouts.

Key Features of RMV

Multi-Period ATR Calculation : Uses three ATR values to effectively capture market tightness over the short term. Normalization : Converts the tightness measure to a 0-100 scale for easy interpretation. Dynamic Histogram and Background Colors : The RMV indicator uses a color-coded system for clarity.

How to Use the RMV Indicator

Identify Tight Consolidation Zones:

a - RMV values between 0-10 indicate very tight price ranges, making this the most optimal zone for potential entries before breakouts.

b - RMV values between 11-20 suggest moderate tightness, still favorable for entries.

Monitor Potential Breakout Areas:

As RMV moves from 21-30 , tightness reduces, signaling expanding volatility that may require wider stops or more flexible entry strategies.

Adjust Trading Strategies:

Use RMV values to identify tight zones for entering trades, especially in trending markets or at key support/resistance levels.

Customize the Indicator:

a - Adjust the short-term ATR lookback periods to control sensitivity.

b - Modify the lookback period to match your trading horizon, whether short-term or long-term.

Color-Coding Guide for RMV

ibb.co

How to Add RMV to Your Chart

Open your chart on TradingView.

Go to the “Indicators” section.

Search for "Relative Measured Volatility (RMV)" in the Community Scripts section.

Click on the indicator to add it to your chart.

Customize the input parameters to fit your trading strategy.

Input Parameters

Lookback Period : Defines the period over which tightness is measured and normalized.

Short-term ATR Lookbacks (1, 2, 3) : Control sensitivity to short-term tightness.

Histogram Threshold : Sets the threshold for differentiating between bright (tight) and dim (less tight) histogram colors.

Conclusion

The Relative Measured Volatility (RMV) is a versatile tool designed to help traders identify tight entry zones by focusing on market consolidation. By highlighting narrow price ranges, the RMV guides traders toward potential breakout setups while providing clear visual cues for better decision-making. Add RMV to your trading toolkit today and enhance your ability to identify optimal entry points!

Supertrend StrategyThe Supertrend Strategy was created based on the Supertrend and Relative Strength Index (RSI) indicators, widely respected tools in technical analysis. This strategy combines these two indicators to capture market trends with precision and reliability, looking for optimizing exit levels at oversold or overbought price levels.

The Supertrend indicator identifies trend direction based on price and volatility by using the Average True Range (ATR). The ATR measures market volatility by calculating the average range between an asset’s high and low prices over a set period. It provides insight into price fluctuations, with higher ATR values indicating increased volatility and lower values suggesting stability. The Supertrend Indicator plots a line above or below the price, signaling potential buy or sell opportunities: when the price closes above the Supertrend line, an uptrend is indicated, while a close below the line suggests a downtrend. This line shifts as price movements and volatility levels change, acting as both a trailing stop loss and trend confirmation.

To enhance the Supertrend strategy, the Relative Strength Index (RSI) has been added as an exit criterion. As a momentum oscillator, the RSI indicates overbought (usually above 70) or oversold (usually below 30) conditions. This integration allows trades to close when the asset is overbought or oversold, capturing gains before a possible reversal, even if the percentage take profit level has not been reached. This mechanism aims to prevent losses due to market reversals before the Supertrend signal changes.

### Key Features

1. **Entry criteria**:

- The strategy uses the Supertrend indicator calculated by adding or subtracting a multiple of the ATR from the closing price, depending on the trend direction.

- When the price crosses above the Supertrend line, the strategy signals a long (buy) entry. Conversely, when the price crosses below, it signals a short (sell) entry.

- The strategy performs a reversal if there is an open position and a change in the direction of the supertrend occurs

2. **Exit criteria**:

- Take profit of 30% (default) on the average position price.

- Oversold (≤ 5) or overbought (≥ 95) RSI

- Reversal when there is a change in direction of the Supertrend

3. **No Repainting**:

- This strategy is not subject to repainting, as long as the timeframe configured on your chart is the same as the supertrend timeframe .

4. **Position Sizing by Equity and risk management**:

- This strategy has a default configuration to operate with 35% of the equity. At the time of opening the position, the supertrend line is typically positioned at about 12 to 16% of the entry price. This way, the strategy is putting at risk about 16% of 35% of equity, that is, around 5.6% of equity for each trade. The percentage of equity can be adjusted by the user according to their risk management.

5. **Backtest results**:

- This strategy was subjected to deep backtesting and operations in replay mode, including transaction fees of 0.12%, and slippage of 5 ticks.

- The past results in deep backtest and replay mode were compatible and profitable (Variable results depending on the take profit used, supertrend and RSI parameters). However, it should be noted that few operations were evaluated, since the currency in question has been created for a short time and the frequency of operations is relatively small.

- Past results are no guarantee of future results. The strategy's backtest results may even be due to overfitting with past data.

Default Settings

Chart timeframe: 2h

Supertrend Factor: 3.42

ATR period: 14

Supertrend timeframe: 2 h

RSI timeframe: 15 min

RSI Lenght: 5 min

RSI Upper limit: 95

RSI Lower Limit: 5

Take Profit: 30%

BYBIT:1000000MOGUSDT.P

Relative VolatilityRelative Volatility is a technical indicator designed to assess changes in market volatility by comparing fast and slow Average True Range (ATR) values. It operates by subtracting a slower ATR (e.g., 50-period ATR) from a faster ATR (e.g., 20-period ATR) and visualizing the result as a histogram. This enables traders to determine whether volatility is increasing or decreasing over time.

This indicator can help traders recognize volatility trends, which can inform decisions related to trade entries, exits, and risk management.

Interpreting Volatility Changes

Increasing Volatility: When the histogram is above zero, it indicates that the fast ATR is greater than the slow ATR, signifying an increase in short-term volatility compared to the long-term average. This may suggest heightened market activity and potential trading opportunities.

Decreasing Volatility: When the histogram is below zero, it shows that the fast ATR is less than the slow ATR, indicating a decrease in short-term volatility relative to the long-term average. This may suggest consolidating markets or reduced trading activity.

Relative Volatility assists traders in monitoring and analyzing changes in market volatility, providing insights that can enhance trading strategies and decision-making processes.

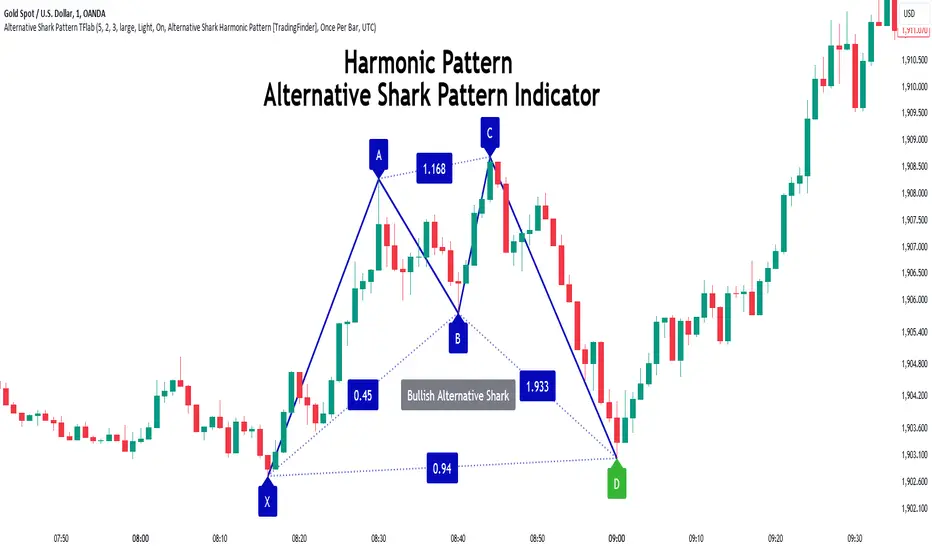

Alternative Shark Harmonic Pattern [TradingFinder] ALT Shark🔵 Introduction

The Alternative Shark harmonic pattern, similar to the original Shark harmonic pattern introduced by Scott Carney, is a powerful tool in technical analysis used to identify potential reversal zones (PRZ) in financial markets.

These harmonic patterns help traders spot key turning points in market trends by relying on specific Fibonacci ratios. The Alternative Shark pattern is particularly unique due to its distinct Fibonacci retracements within the PRZ, which differentiate it from the standard Shark pattern and provide traders with more precise entry and exit signals.

By focusing on harmonic patterns and utilizing tools like the Harmonic Pattern Indicator, traders can easily identify both the Shark and Alternative Shark patterns, making it easier to find PRZs and capture potential trend reversals. This enhanced detection of potential reversal zones allows for better trade optimization and improved risk management.

Incorporating the Alternative Shark pattern into your technical analysis strategy enables you to enhance your trading performance by identifying market reversals with greater accuracy, improving the timing of your trades, and reducing risks associated with sudden market shifts.

🟣 Understanding the Types of Alternative Shark Pattern

The Alternative Shark harmonic pattern, much like the original Shark pattern, forms at the end of price trends and is divided into two types: Bullish and Bearish Alternative Shark patterns.

Bullish Alternative Shark Pattern :

This pattern typically forms at the end of a downtrend, signaling a potential reversal into an uptrend. Traders can use this pattern to identify buy entry points. The image below illustrates the core components of the Bullish Alternative Shark Pattern.

Bearish Alternative Shark Pattern :

Conversely, the Bearish Alternative Shark Pattern appears at the end of an uptrend and signals a potential reversal to a downtrend. This variation allows traders to adjust their strategies for selling. The image below outlines the characteristics of the Bearish Alternative Shark Pattern.

🟣 Differences Between Shark and Alternative Shark Patterns

Although both patterns share similar structures and serve as tools for identifying price reversals, there is one key difference between them :

AB to XA Ratio : In the Shark pattern, the AB leg retraces between 1 and 2 of the XA leg, whereas in the Alternative Shark pattern, this retracement is reduced to 0.382 to 0.618 of the XA leg. This difference in the retracement ratio leads to slightly different trade signals and can affect the timing of entry and exit points.

Other ratios and reversal signals remain consistent between the two patterns, but this difference in the AB to XA ratio provides traders with more nuanced opportunities to optimize their trades.

🔵 How to Use

🟣 Trading with the Bullish Alternative Shark Pattern

The Bullish Alternative Shark Pattern functions similarly to the traditional Bullish Shark, acting as a reversal pattern that helps traders recognize the end of a downtrend and the beginning of an uptrend.

The main distinction lies in the reduced AB retracement, which can offer more refined entry signals. Once the pattern completes, traders can look to enter buy trades and place a stop-loss below the lowest point of the pattern for effective risk management.

🟣 Trading with the Bearish Alternative Shark Pattern

The Bearish Alternative Shark Pattern operates much like the Bearish Shark pattern but with the adjusted AB to XA ratio. This difference provides traders with unique entry points for sell trades. Once the pattern is fully identified, traders can enter short positions, placing a stop-loss above the highest point of the pattern to safeguard against market fluctuations.

🔵 Setting

🟣 Logical Setting

ZigZag Pivot Period : You can adjust the period so that the harmonic patterns are adjusted according to the pivot period you want. This factor is the most important parameter in pattern recognition.

Show Valid Forma t: If this parameter is on "On" mode, only patterns will be displayed that they have exact format and no noise can be seen in them. If "Off" is, the patterns displayed that maybe are noisy and do not exactly correspond to the original pattern.

Show Formation Last Pivot Confirm : if Turned on, you can see this ability of patterns when their last pivot is formed. If this feature is off, it will see the patterns as soon as they are formed. The advantage of this option being clear is less formation of fielded patterns, and it is accompanied by the latest pattern seeing and a sharp reduction in reward to risk.

Period of Formation Last Pivot : Using this parameter you can determine that the last pivot is based on Pivot period.

🟣 Genaral Setting

Show : Enter "On" to display the template and "Off" to not display the template.

Color : Enter the desired color to draw the pattern in this parameter.

LineWidth : You can enter the number 1 or numbers higher than one to adjust the thickness of the drawing lines. This number must be an integer and increases with increasing thickness.

LabelSize : You can adjust the size of the labels by using the "size.auto", "size.tiny", "size.smal", "size.normal", "size.large" or "size.huge" entries.

🟣 Alert Setting

Alert : On / Off

Message Frequency : This string parameter defines the announcement frequency. Choices include: "All" (activates the alert every time the function is called), "Once Per Bar" (activates the alert only on the first call within the bar), and "Once Per Bar Close" (the alert is activated only by a call at the last script execution of the real-time bar upon closing). The default setting is "Once per Bar".

Show Alert Time by Time Zone : The date, hour, and minute you receive in alert messages can be based on any time zone you choose. For example, if you want New York time, you should enter "UTC-4". This input is set to the time zone "UTC" by default.

🔵 Conclusion

The Alternative Shark harmonic pattern, despite its structural similarity to the traditional Shark pattern, introduces a key difference in the AB to XA ratio, making it a valuable addition to the trader’s toolkit. This subtle variation enables traders to pinpoint reversal points with greater accuracy and fine-tune their trading strategies.

As with any technical pattern, it is crucial to use the Alternative Shark pattern in combination with other technical indicators and strong risk management practices. Incorporating this pattern into a broader trading strategy can help traders enhance their ability to detect and capitalize on market reversals more effectively.

ATR Range Pivot LinesDescription:

This Pine Script calculates and plots pivot lines based on ATR (Average True Range) value and closing price. It uses the previous trading day's ATR value to set static pivot levels for the current trading day. These pivot lines help traders identify potential support and resistance levels based on historical volatility. The script includes two main pivot lines—ATR High and ATR Low —and two midpoint lines between them for additional context. Labels are added to show the exact pivot values, with options to customize label positions.

Intended Use:

The script is designed to help traders forecast potential price ranges for the current trading day based on the previous day’s volatility. By adding and subtracting the previous day's ATR from the prior close, the script identifies key levels where price action may encounter support or resistance. It is useful for setting realistic price targets or entry/exit points. Since the ATR-based pivot lines are static for the entire day, they provide a reliable range for intraday trading strategies.

Disclosure:

This script was generated using AI. It is recommended to review and test the script thoroughly before applying it in live trading scenarios.

The Bar Counter Trend Reversal Strategy [TradeDots]Overview

The Bar Counter Trend Reversal Strategy is designed to identify potential counter-trend reversal points in the market after a series of consecutive rising or falling bars.

By analyzing price movements in conjunction with optional volume confirmation and channel bands (Bollinger Bands or Keltner Channels), this strategy aims to detect overbought or oversold conditions where a trend reversal may occur.

🔹How it Works

Consecutive Price Movements

Rising Bars: The strategy detects when there are a specified number of consecutive rising bars (No. of Rises).

Falling Bars: Similarly, it identifies a specified number of consecutive falling bars (No. of Falls).

Volume Confirmation (Optional)

When enabled, the strategy checks for increasing volume during the consecutive price movements, adding an extra layer of confirmation to the potential reversal signal.

Channel Confirmation (Optional)

Channel Type: Choose between Bollinger Bands ("BB") or Keltner Channels ("KC").

Channel Interaction: The strategy checks if the price interacts with the upper or lower channel lines: For short signals, it looks for price moving above the upper channel line. For long signals, it looks for price moving below the lower channel line.

Customization:

No. of Rises/Falls: Set the number of consecutive bars required to trigger a signal.

Volume Confirmation: Enable or disable volume as a confirmation factor.

Channel Confirmation: Enable or disable channel bands as a confirmation factor.

Channel Settings: Adjust the length and multiplier for the Bollinger Bands or Keltner Channels.

Visual Indicators:

Entry Signals: Triangles plotted on the chart indicate potential entry points:

Green upward triangle for long entries.

Red downward triangle for short entries.

Channel Bands: The upper and lower bands are plotted for visual reference.

Strategy Parameters:

Initial Capital: $10,000.

Position Sizing: 80% of equity per trade.

Commission: 0.01% per trade to simulate realistic trading costs.

🔹Usage

Set up the number of Rises/Falls and choose whether if you want to use channel indicators and volume as the confirmation.

Monitor the chart for triangles indicating potential entry points.

Consider the context of the overall market trend and other technical factors.

Backtesting and Optimization:

Use TradingView's Strategy Tester to evaluate performance.

Adjust parameters to optimize results for different market conditions.

🔹 Considerations and Recommendations

Risk Management:

The strategy does not include built-in stop-loss or take-profit levels. It's recommended to implement your own risk management techniques.

Market Conditions:

Performance may vary in different market environments. Testing and adjustments are advised when applying the strategy to new instruments or timeframes.

No Guarantee of Future Results:

Past performance is not indicative of future results. Always perform due diligence and consider the risks involved in trading.