Dynamic Trading Strategy with Key Levels, Entry/Exit Managementjust a strategy tester i dont have any copy right of this indicator

Volume

Ichimoku + RSI + MACD Strategy1. Relative Strength Index (RSI)

Overview:

The Relative Strength Index (RSI) is a momentum oscillator that measures the speed and change of price movements. It ranges from 0 to 100 and is typically used to identify overbought or oversold conditions in a market.

How to Use with Ichimoku:

Long Entry: Look for RSI to be above 30 (indicating it is not oversold) when the price is above the Ichimoku Cloud.

Short Entry: Look for RSI to be below 70 (indicating it is not overbought) when the price is below the Ichimoku Cloud.

2. Moving Average Convergence Divergence (MACD)

Overview:

The MACD is a trend-following momentum indicator that shows the relationship between two moving averages of a security’s price. It consists of the MACD line, signal line, and histogram.

How to Use with Ichimoku:

Long Entry: Enter a long position when the MACD line crosses above the signal line while the price is above the Ichimoku Cloud.

Short Entry: Enter a short position when the MACD line crosses below the signal line while the price is below the Ichimoku Cloud.

Combined Strategy Example

Here’s a brief outline of how to structure a trading strategy using Ichimoku, RSI, and MACD:

Long Entry Conditions:

Price is above the Ichimoku Cloud.

RSI is above 30.

MACD line crosses above the signal line.

Short Entry Conditions:

Price is below the Ichimoku Cloud.

RSI is below 70.

MACD line crosses below the signal line.

Exit Conditions:

Exit long when MACD line crosses below the signal line.

Exit short when MACD line crosses above the signal line.

MFI Strategy with Oversold Zone Exit and AveragingThis strategy is based on the Money Flow Index (MFI) and aims to enter a long position when the MFI exits an oversold zone, with specific rules for limit orders, stop-loss, and take-profit settings. Here's a detailed breakdown:

Key Components

1. **Money Flow Index (MFI)**: The strategy uses the MFI, a volume-weighted indicator, to gauge whether the market is in an oversold condition (default threshold of MFI < 20). Once the MFI rises above the oversold threshold, it signals a potential buying opportunity.

2. **Limit Order for Long Entry**: Instead of entering immediately after the oversold condition is cleared, the strategy places a limit order at a price slightly below the current price (by a user-defined percentage). This helps achieve a better entry price.

3. **Stop-Loss and Take-Profit**:

- **Stop-Loss**: A stop-loss is set to protect against significant losses, calculated as a percentage below the entry price.

- **Take-Profit**: A take-profit target is set as a percentage above the entry price to lock in gains.

4. **Order Cancellation**: If the limit order isn’t filled within a specific number of bars (default is 5 bars), it’s automatically canceled to avoid being filled at a potentially suboptimal price as market conditions change.

Strategy Workflow

1. **Identify Oversold Zone**: The strategy checks if the MFI falls below a defined oversold level (default is 20). Once this condition is met, the flag `inOversoldZone` is set to `true`.

2. **Wait for Exit from Oversold Zone**: When the MFI rises back above the oversold level, it’s considered a signal that the market is potentially recovering, and the strategy prepares to enter a position.

3. **Place Limit Order**: Upon exiting the oversold zone, the strategy places a limit order for a long position at a price below the current price, defined by the `Long Entry Percentage` parameter.

4. **Monitor Limit Order**: A counter (`barsSinceEntryOrder`) starts counting the bars since the limit order was placed. If the order isn’t filled within the specified number of bars, it’s canceled automatically.

5. **Set Stop-Loss and Take-Profit**: Once the order is filled, a stop-loss and take-profit are set based on user-defined percentages relative to the entry price.

6. **Exit Strategy**: The trade will close automatically when either the stop-loss or take-profit level is hit.

Advantages

- **Risk Management**: With configurable stop-loss and take-profit, the strategy ensures losses are limited while capturing profits at pre-defined levels.

- **Controlled Entry**: The use of a limit order below the current price helps secure a better entry point, enhancing risk-reward.

- **Oversold Exit Trigger**: Using the exit from an oversold zone as an entry condition can help catch reversals.

Disadvantages

- **Missed Entries**: If the limit order isn’t filled due to insufficient downward movement after the oversold signal, potential opportunities may be missed.

- **Dependency on MFI Sensitivity**: As the MFI is sensitive to both price and volume, its fluctuations might not always accurately represent oversold conditions.

Overall Purpose

The strategy is suited for traders who want to capture potential reversals after oversold conditions in the market, with a focus on precise entries, risk management, and an automated exit plan.

MT Enhanced Trend Reversal StrategyThis strategy, called **"Enhanced Trend Reversal Strategy with Take Profit,"** is designed to identify trend reversal points based on several indicators: **Exponential Moving Averages (EMA), MACD**, and **RSI**. The strategy also includes **take-profit levels** to provide traders with suggested profit-taking points.

Key Components of the Strategy

1. **Exponential Moving Averages (EMA)**:

- The strategy uses **20 and 50-period EMAs** to determine trend direction. The shorter period (EMA 20) reacts more quickly to price changes, while the longer period (EMA 50) smooths out fluctuations.

- An **uptrend** (bullish market) is indicated when the EMA 20 is above the EMA 50. In this case, the main trend line is colored green.

- A **downtrend** (bearish market) is indicated when the EMA 20 is below the EMA 50, in which case the trend line is colored red.

- This visual indication simplifies analysis and allows traders to quickly assess the market condition.

2. **MACD (Moving Average Convergence Divergence)**:

- MACD is an oscillator that shows the difference between two EMAs (with periods 6 and 13) and a **signal line** with a period of 5.

- A **buy signal** is generated when the MACD line crosses above the signal line, indicating a potential bullish trend.

- A **sell signal** is generated when the MACD line crosses below the signal line, indicating a possible bearish trend.

- Shorter MACD periods make the strategy more sensitive to price changes, allowing for more frequent trading signals.

3. **RSI (Relative Strength Index)**:

- RSI measures the speed and magnitude of directional price movements to determine if an asset is overbought or oversold.

- The strategy uses a standard RSI period of 14, but with relaxed levels for more signals.

- **For buy entries**, RSI should be above 40, signaling the start of a bullish impulse without indicating overbought conditions.

- **For sell entries**, RSI should be below 60, signaling potential bearish movement without being oversold.

Entry Conditions

- **Buy Signal**:

- The MACD line crosses above the signal line.

- EMA 20 is above EMA 50 (uptrend).

- RSI is above 40, indicating a potential rise without overbought conditions.

- When these conditions are met, the strategy enters a **long position**.

- **Sell Signal**:

- The MACD line crosses below the signal line.

- EMA 20 is below EMA 50 (downtrend).

- RSI is below 60, indicating a possible decline without being oversold.

- When these conditions are met, the strategy enters a **short position**.

Take-Profit Levels

- **Take Profit** is calculated at 1.5% of the entry price:

- **For long positions**, take profit is set at a level 1.5% above the entry price.

- **For short positions**, take profit is set at a level 1.5% below the entry price.

- This take-profit level is displayed as a blue line on the chart, giving traders a clear idea of the target profit point for each trade.

Visualization and Colors

- The main trend line (EMA 20) changes to green in an uptrend and red in a downtrend. This provides a clear visual indicator of the current trend direction.

- Take-profit levels are displayed as blue lines, helping traders follow targets and lock in profits at recommended levels.

Usage Recommendations

- **Timeframe**: The strategy is optimized for a 30-minute timeframe. At this interval, signals are frequent enough without being overly sensitive to noise.

- **Applicability**: The strategy works well for assets with moderate to high volatility, such as stocks, cryptocurrencies, and currency pairs.

- **Risk Management**: In addition to take profit, a stop loss at around 1-2% is recommended to minimize losses in case of sudden trend reversals.

Conclusion

This strategy is designed for more frequent signals by using faster indicators and relaxed RSI conditions. It is suitable for traders seeking quick trade opportunities and clearly defined take-profit levels.

Velocity/Volatility/Volume StrategyThe "Vel/Vty/Vol Strategy" is a momentum-based trading approach designed to take advantage of strong price movements that are confirmed by both volatility and volume (if enabled). It provides a high level of customization, allowing traders to adjust various settings based on market conditions and individual preferences. By combining three critical indicators—velocity, volatility (measured through Bollinger Band Width), and an optional volume filter—the strategy generates trade signals for both long and short positions. Here’s a comprehensive explanation of how the strategy works, how the parameters can be customized, and how those adjustments benefit users.

At its core, the strategy focuses on velocity, which measures the speed at which price is changing over time. This is a key indicator of momentum, with a "StrongUp" signal indicating bullish momentum and a "StrongDown" signal suggesting bearish momentum. In addition to velocity, the strategy factors in acceleration, which helps gauge whether momentum is building or weakening. The second essential component is Bollinger Band Width (BBW), which measures volatility in the market. When the BBW expands, it signals increasing volatility, a condition that must be met in combination with a velocity signal to generate a trade. Lastly, the strategy includes an optional Volume Oscillator to filter trades. When this volume filter is enabled, trades will only be executed if there’s an increase in volume, further validating market activity.

The strategy generates long and short trade signals based on specific conditions. A long trade is triggered when there is a strong upward velocity, accompanied by an increase in Bollinger Band Width, indicating both momentum and heightened volatility. If the volume filter is toggled on, a rise in volume must also confirm the signal. Similarly, a short trade is initiated when a strong downward velocity is detected, again paired with an increase in volatility and, optionally, a volume rise. This ensures that trades occur during periods of heightened market activity, reducing the likelihood of false signals.

To help manage risk, the strategy includes several customizable tools. Users can set take profit levels to automatically close positions and lock in gains once a predefined profit percentage is reached. For example, if a 2% take profit is set, a long position will be closed once the price has risen by 2%. Additionally, a trailing take profit option can be enabled, allowing the strategy to dynamically adjust the take-profit target as the market moves in the user’s favor. This ensures that profits are locked in as long as the market continues to trend positively, while providing protection in case of a reversal. The strategy also includes a trailing stop-loss feature, which adjusts the stop price as the market moves in favor of the trade, helping to minimize losses and protect gains.

The strategy offers a variety of parameters that can be customized to suit different trading styles and market conditions. The velocity lookback period controls how far back the strategy looks to calculate velocity. A shorter lookback makes the strategy more sensitive to recent price changes, generating more signals, which can benefit day traders or those seeking to capture short-term price swings. Conversely, a longer lookback smooths out the velocity calculation, reducing false signals and making the strategy more suitable for traders seeking to capture larger trends. Similarly, the Bollinger Band Width (BBW) length can be adjusted to control how far back the strategy looks to calculate volatility. A shorter BBW length makes the strategy more sensitive to volatility spikes, useful in rapidly changing markets. In contrast, a longer BBW length filters out short-term noise and focuses on more sustainable volatility shifts, better suited for slower, more stable markets.

The volume filter is another powerful feature that can be toggled on or off. When turned on, the strategy will only execute trades if there is an increase in volume alongside velocity and volatility signals. This helps filter out false signals in low-volume markets, ensuring that price movements are supported by actual market activity. If the volume filter is turned off, the strategy focuses purely on price and volatility changes, which can be useful in markets where volume data is unreliable or less relevant.

The take profit percentage can be adjusted to define how aggressively or conservatively profits are locked in. A lower take profit percentage allows traders to capture smaller, quicker profits, which can be advantageous in volatile markets. A higher take profit percentage suits traders who prefer to capture larger moves, allowing them to stay in trades longer to benefit from extended trends. Similarly, the trailing take profit percentage determines how tightly the strategy follows market prices as they move in favor of the trade. A tighter trailing percentage ensures that profits are locked in quickly, while a wider trailing percentage gives trades more room to run, ideal for capturing large trends.

The stop loss percentage is another key setting that controls how much risk a trader is willing to take before the position is closed. A tighter stop loss minimizes losses but may result in more frequent stop-outs, particularly in volatile markets. A wider stop loss provides more room for trades to develop, which is useful for traders aiming to capture longer trends despite short-term fluctuations. Additionally, the velocity thresholds can be adjusted to set how sensitive the strategy is to price movements. Lower thresholds increase sensitivity, generating more signals in fast-moving markets, while higher thresholds filter out weaker signals, focusing on larger momentum shifts.

The strategy also allows users to define a time range during which it is active, offering flexibility in backtesting and optimizing for specific market conditions. By limiting the strategy to certain periods, users can tailor it to seasonal trends or historical data that matches their current trading environment.

The flexibility of this strategy makes it suitable for a wide range of traders. Day traders can benefit from adjusting the velocity and BBW lookback periods, tightening take profit and stop loss settings to capture short, fast price movements in highly volatile markets. Trend traders can lengthen the lookback periods and widen the velocity thresholds to capture larger, sustained moves while riding out short-term volatility. Traders with a lower risk tolerance can enable the volume filter and tighten stop losses to reduce false signals and minimize losses. On the other hand, aggressive traders can widen the take profit and trailing stop percentages to allow trades to develop fully, maximizing potential gains in trending markets.

Central Pivot Point Cross & Retrace Strategy // AlgoFyreThe Central Pivot Point Cross & Retrace Strategy uses pivot points for trend identification and trade entry. It combines accumulation/distribution indicators with pivot point levels to generate signals. The strategy incorporates dynamic position sizing based on a fixed risk amount and allows for both long and short positions with customizable stop-loss levels.

TABLE OF CONTENTS

🔶 ORIGINALITY

🔸Pivot Point-Based Trading

🔸Accumulation/Distribution

🔸Dynamic Position Sizing

🔸Customizable Risk Management

🔶 FUNCTIONALITY

🔸Indicators

🞘 Pivot Points

🞘 Accumulation/Distribution

🔸Conditions

🞘 Long Entry

🞘 Short Entry

🞘 Take Profit

🞘 Stop Loss

🔶 INSTRUCTIONS

🔸Adding the Strategy to the Chart

🔸Configuring the Strategy

🔸Backtesting and Practice

🔸Market Awareness

🔸Visual Customization

🔶 CONCLUSION

▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅▅

🔶 ORIGINALITY The Central Pivot Point Cross & Retrace Strategy uniquely combines pivot point analysis with accumulation/distribution indicators to identify optimal entry and exit points. It employs dynamic position sizing based on a fixed risk amount, ensuring consistent risk management across trades. This approach allows traders to adapt to varying market conditions by adjusting position sizes according to predefined risk parameters, enhancing both flexibility and control in trading decisions. The strategy's integration of customizable stop-loss levels further refines its risk management capabilities.

🔸Pivot Point-Based Trading This strategy utilizes daily pivot points to identify key support and resistance levels, providing a framework for trend identification and trade entry. The central pivot point serves as the intraday point of balance between buyers and sellers, with the largest amount of trading volume assumed to take place in this area.

🔸Accumulation/Distribution The strategy incorporates the Accumulation/Distribution (A/D) line, an underrated volume-based indicator, to establish the main trend. The A/D line is used in conjunction with a trend based indicator like the 200-period Exponential Moving Average (EMA) to confirm trend direction and strength.

🔸Dynamic Position Sizing Position sizes are calculated dynamically based on a fixed risk amount, allowing traders to maintain consistent risk exposure across trades.

🔸Customizable Risk Management Traders can set flexible risk-reward ratios and adjust stop-loss and take-profit levels, tailoring the strategy to their risk tolerance and market conditions. The strategy recommends taking partial profits at S1 or R1 levels and moving the stop-loss to break-even for remaining positions.

🔶 FUNCTIONALITY The Central Pivot Point Cross & Retrace Strategy leverages pivot points and accumulation/distribution indicators to identify optimal trading opportunities. This strategy is designed to capitalize on price movements around key pivot levels by dynamically adjusting position sizes based on predefined risk parameters. It allows traders to manage risk effectively while taking advantage of both long and short positions.

🔸Indicators 🞘 Pivot Points: Calculates daily pivot points (PP, R1, R2, S1, S2) to identify key support and resistance levels. The central pivot point is crucial for determining market bias and entry points.

🞘 Accumulation/Distribution: Uses the A/D line and with a trend based indicator like the 200 EMA to determine market direction and trend strength. This combination helps eliminate noise and provides more reliable trend signals. We recommend using the Adaptive MAs (Hurst, CVaR, Fractal) // AlgoFyre , but any moving average could be used.

🔸Conditions 🞘 Long Entry: Initiates a long position when the price crosses above the central pivot point (PP), retraces back to it and the A/D line is above its 200 EMA, indicating an uptrend. A limit entry order is set at the PP for entering the long trade.

🞘 Short Entry: Initiates a short position when the price crosses below the central pivot point (PP), retraces back to it and the A/D line is below its 200 EMA, indicating a downtrend. A limit entry order is set at the PP for entering the short trade.

🞘 Take Profit: 50% of the position is closed as profit when R1 for Longs and S1 for Shorts is reached. The position is fully closed when R2 for Longs and S2 for Shorts is reached.

🞘 Stop Loss: Stop loss is set via strategy settings. When the first 50% take profit for both long and shorts is taken, stop loss for both will be moved to break-even/entry.

🔶 INSTRUCTIONS

The Central Pivot Point Cross & Retrace Strategy can be set up by adding it to your TradingView chart and configuring parameters such as the accumulation/distribution source, stop-loss percentage, and risk management settings. This strategy is designed to capitalize on price movements around key pivot levels by dynamically adjusting position sizes based on predefined risk parameters. Enhance the accuracy of signals by combining this strategy with additional indicators like trend-following or momentum-based tools. Adjust settings to better manage risk and optimize entry and exit points.

🔸Adding the Strategy to the Chart Go to your TradingView chart.

Click on the "Pine Editor" button at the bottom of the chart.

Copy and paste the strategy code into the Pine Editor.

Click "Add to Chart" to apply the strategy.

Add the technical indicator "Accumulation/Distribution" to the chart.

Add the trend indicator " Adaptive MAs (Hurst, CVaR, Fractal) // AlgoFyre " or any other MA to the chart and move it to the "Accumulation/Distribution" pane.

Set the source of your trend indicator to "Accumulation/Distribution".

🔸Configuring the Strategy Open the strategy settings by clicking on the gear icon next to its name on the chart.

Accumulation/Distribution Source: Select the source for the accumulation/distribution indicator.

Accumulation/Distribution EMA Source: Select the source for the trend indicator.

Stop Loss Percentage: Set the stop loss distance from the pivot point as a percentage.

Risk Amount: Define the fixed risk amount for position sizing.

Base Order Size: Set the base order size for position calculations.

Number of Positions: Specify the maximum number of positions allowed.

Time Frame: Adjust the time frame based on the currency pair or asset being traded (e.g., 15-minute for EUR/USD, 30-minute for GBP/USD).

🔸Backtesting and Practice Backtest the strategy on historical data to understand how it performs in various market environments.

Practice using the strategy on a demo account before implementing it in live trading.

Test different time frames and asset pairs to find the most suitable combinations.

🔸Market Awareness Keep an eye on market news and events that might cause extreme price movements. The strategy reacts to price data and might not account for news-driven events that can cause large deviations.

Remember that this strategy is not recommended for stocks due to the A/D line's inability to account for gaps in its calculation.

🔸Visual Customization Visualization Settings: Customize the display of entry price, take profit, and stop loss levels.

Color Settings: Switch to the AlgoFyre theme or set custom colors for bullish, bearish, and neutral states.

Table Settings: Enable or disable the information table and adjust its position.

🔶 CONCLUSION

The Central Pivot Point Cross & Retrace Strategy provides a robust framework for capitalizing on price movements around key pivot levels by combining pivot point analysis with accumulation/distribution indicators. This strategy leverages pivot point crossovers to identify entry points and utilizes the A/D line crossover with its 200 EMA for trend confirmation, ensuring trades align with prevailing market conditions. By incorporating dynamic position sizing based on a fixed risk amount, traders can effectively manage risk and adapt to varying market conditions. The strategy's focus on trading around the central pivot point and its customizable stop-loss and take-profit levels further enhance its risk management capabilities, making it a versatile tool for both trending and ranging markets. With its strategic blend of technical indicators and risk management, the Central Pivot Point Cross & Retrace Strategy offers traders a comprehensive approach to optimizing trade execution and maximizing potential returns across various currency pairs and commodities.

ML Supply Zone Strategy - ETHOverview

The ML (Machine Learning) Supply Zone Strategy for ETH is an advanced trading tool designed for traders looking to capitalize market movements in Ethereum (ETH). This strategy employs sophisticated machine learning techniques to identify supply zones by analyzing historical price data and calculating the statistical likelihood of price movements in specific directions. Our proprietary Python scripts perform monthly analyses to update these probabilities, ensuring the strategy adapts to evolving market conditions.

Key Features

Machine Learning-Derived Supply Zones-

Data-Driven Identification: Utilizes ML algorithms to process extensive historical price data of ETH, pinpointing supply zones where significant price reversals or continuations are statistically probable.

Probability Assessment: Breaks down the percentage chance of the price moving up or down upon reaching these zones, based on patterns recognized by the ML (machine learning) models.

Monthly Updates: Refreshes supply zones and probabilities every month through new data analysis, keeping the strategy current with market trends.

Proprietary Python Script Integration-

Advanced Algorithms: Our custom Python scripts employ clustering algorithms (e.g., K-means, DBSCAN) and statistical analysis to detect meaningful patterns in ETH price action.

Seamless Strategy Integration: The outputs from the Python analysis are directly incorporated into the trading script, providing actionable insights without the need for external tools.

Comprehensive Risk Management-

Precise Entry and Exit Points: Based on ML-derived supply zones and associated probabilities, the strategy sets exact entry and exit points to optimize trade outcomes.

Risk-to-Reward Optimization: Implements stop-loss and take-profit levels designed to achieve a favorable risk-to-reward ratio, typically aiming for 1:3 (0.7% SL / 2.1% TP).

Versatility Across Timeframes: While the strategy works well across various timeframes, it performs particularly effectively on the 1-minute timeframe, capturing short-term market movements.

How the Strategy Works

Data Collection and ML Analysis-

Historical Price Data Processing: The proprietary Python scripts analyze large datasets of historical ETH price movements, focusing on identifying zones where supply exceeds demand, leading to potential price drops.

Feature Extraction: ML models extract features such as price levels, volume spikes, and volatility measures that influence supply zone formations.

Probability Calculation-

Statistical Modeling: Uses statistical techniques to calculate the probability of price moving in a particular direction after reaching a supply zone.

Pattern Recognition: Identifies recurring patterns and correlations that have historically led to significant price movements.

Integration into Trading Script-

Supply Zone Mapping: The identified supply zones and their associated probabilities are embedded into the trading script as key levels.

Signal Generation:

Entry Signals: Triggered when the current price approaches a supply zone with a high probability of a downward move.

Choppiness Index (CI) and Volume Filtering-

Trade Quality Enhancement: To prevent excessive trading on determined supply zones, the strategy incorporates the Choppiness Index and volume filters.

Market Condition Assessment: The CI helps determine whether the market is trending or ranging, ensuring trades are taken in optimal conditions.

Liquidity Confirmation: Volume filters ensure that trades are only executed when there is sufficient market activity, improving execution and reliability.

Setup and Configuration

Access the Strategy: Add the ML Supply Zone Probability Strategy for ETH to your TradingView chart.

Select the Correct Chart: Apply it to the Pionex ETH/USDT Perpetual chart for optimal performance.

Select Timeframe: For best results, use the 1-minute timeframe (although almost all timeframes work).

Customize Settings: Adjust parameters such as risk tolerance, position sizing, and probability thresholds to suit your trading preferences.

Backtesting Recommendations

Sufficient Trade Sample Size: To generate around 100+ trades in backtesting, it is recommended to extend the backtesting period to at least three months.

Statistical Significance: A larger number of trades provides a more reliable assessment of the strategy's performance, enhancing confidence in its effectiveness.

XAU/USD Strategy with Correct ADX and Bollinger Bands Fill1. *Indicators Used*:

- *Exponential Moving Averages (EMAs)*: Two EMAs (20-period and 50-period) are used to identify the trend direction and potential entry points based on crossovers.

- *Relative Strength Index (RSI)*: A momentum oscillator that measures the speed and change of price movements. It identifies overbought and oversold conditions.

- *Bollinger Bands*: These consist of a middle line (simple moving average) and two outer bands (standard deviations away from the middle). They help to identify price volatility and potential reversal points.

- *Average Directional Index (ADX)*: This indicator quantifies trend strength. It's derived from the Directional Movement Index (DMI) and helps confirm the presence of a strong trend.

- *Average True Range (ATR)*: Used to calculate position size based on volatility, ensuring that trades align with the trader's risk tolerance.

2. *Entry Conditions*:

- *Long Entry*:

- The 20 EMA crosses above the 50 EMA (indicating a potential bullish trend).

- The RSI is below the oversold level (30), suggesting the asset may be undervalued.

- The price is below the lower Bollinger Band, indicating potential price reversal.

- The ADX is above a specified threshold (25), confirming that there is sufficient trend strength.

- *Short Entry*:

- The 20 EMA crosses below the 50 EMA (indicating a potential bearish trend).

- The RSI is above the overbought level (70), suggesting the asset may be overvalued.

- The price is above the upper Bollinger Band, indicating potential price reversal.

- The ADX is above the specified threshold (25), confirming trend strength.

3. *Position Sizing*:

- The script calculates the position size dynamically based on the trader's risk per trade (expressed as a percentage of the total capital) and the ATR. This ensures that the trader does not risk more than the specified percentage on any single trade, adjusting the position size according to market volatility.

4. *Exit Conditions*:

- The strategy uses a trailing stop-loss mechanism to secure profits as the price moves in the trader's favor. The trailing stop is set at a percentage (1.5% by default) below the highest price reached since entry for long positions and above the lowest price for short positions.

- Additionally, if the RSI crosses back above the overbought level while in a long position or below the oversold level while in a short position, the position is closed to prevent losses.

5. *Alerts*:

- Alerts are set to notify the trader when a buy or sell condition is met based on the strategy's rules. This allows for timely execution of trades.

### Summary

This strategy aims to capture significant price movements in the XAU/USD market by combining trend-following (EMAs, ADX) and momentum indicators (RSI, Bollinger Bands). The dynamic position sizing based on ATR helps manage risk effectively. By implementing trailing stops and alert mechanisms, the strategy enhances the trader's ability to act quickly on opportunities while mitigating potential losses.

Custom Buy BID StrategyThis Pine Script strategy is designed to identify and capitalize on upward trends in the market using the Average True Range (ATR) as a core component of the analysis. The script provides the following features:

Customizable ATR Calculation: Users can switch between different methods of ATR calculation (traditional or simple moving average).

Adjustable Parameters: The strategy allows for adjustable ATR periods, ATR multipliers, and custom time windows for executing trades.

Buy Signal Alerts: The strategy generates buy signals when the market shifts from a downtrend to an uptrend, based on ATR and price action.

Profit and Stop-Loss Management: Built-in take profit and stop-loss conditions are calculated as a percentage of the entry price, allowing for automatic position management.

Visual Enhancements: The script highlights the uptrend with green lines and optionally colors bars to help visualize market direction.

Flexible Timeframe: Users can configure a specific date range to activate the strategy, offering more control over when trades are executed.

This strategy is ideal for traders looking to automate their buy entries and manage risk with a straightforward trend-following approach. By utilizing customizable settings, it adapts to various market conditions and timeframes.

Nifty scalping 3 minutes options on Dhan

Strategy Description for Publishing: Nifty Scalping 3 Minutes Options on Dhan

Overview:

The Nifty Scalping 3 Minutes Options on Dhan strategy is an enhanced version tailored for trading Nifty Options, building on the core logic used in the previously published Nifty Scalping 3 Minutes Strategy. This strategy provides automated order execution via JSON alerts for seamless integration with the Dhan platform, enabling hands-free options trading.

This system is designed to capture short-term market moves using a combination of technical indicators like the Jurik Moving Average (JMA), Exponential Moving Average (EMA), and Bollinger Bands, while also allowing traders to manage risk effectively with custom inputs for maximum loss per lot and partial profit booking.

For more details on the core logic and performance of the strategy, please refer to our earlier published strategy:

Nifty Scalping 3 Minutes Strategy

Key Features:

JMA and EMA Crossovers: Trades are executed when the Jurik Moving Average (JMA) crosses over (for long trades) or under (for short trades) the Exponential Moving Average (EMA), signaling trend direction.

Price-Volume Spike Detection: Ensures that trades are executed only when significant market activity is detected, avoiding low-momentum conditions. Price-volume relationships are monitored to confirm the strength of market movements.

Bollinger Band Noise Filter: Filters out low-volatility periods by executing trades only when prices break through the upper or lower Bollinger Bands, confirming high volatility.

Customizable Risk Management: Traders can set their own maximum risk per lot (e.g., ₹650), and the strategy adjusts the stop-loss accordingly to ensure that no trade exceeds this threshold.

Partial Profit Booking: A predefined percentage (e.g., 60%) of the position can be booked as profit once the first profit target is reached, with the remaining position trailed using an ATR-based stop.

STBT/BTST Support: The strategy offers the flexibility to carry trades overnight, supporting Sell Today, Buy Tomorrow (STBT) and Buy Today, Sell Tomorrow (BTST).

Time-Based Exit: The strategy automatically closes any open positions by 3:20 PM to avoid the volatile end-of-day market conditions.

Inputs for Traders:

Option Quantity: Select the number of contracts to trade (e.g., 10).

Maximum Risk Per Lot: Set your maximum allowable loss per lot (e.g., ₹650), ensuring that your risk is managed effectively.

Partial Profit Booking Percentage: Define what percentage of your position to book as profit (e.g., 60%) when the first target is hit.

STBT/BTST Option: Choose whether to allow positions to be carried overnight.

Alert Secret Key: Input your secret key for the Dhan platform to trigger automated orders via JSON alerts.

Option Expiry Date: Specify the expiry date for the options being traded.

Trade Logic:

Long Trades: Triggered when JMA crosses above EMA, supported by filters like price-volume spikes and Bollinger Band breakouts. The strategy waits for momentum confirmation before entering long trades, with stop-loss and profit-taking mechanisms in place.

Short Trades: Triggered when JMA crosses below EMA, with confirmation through additional filters to ensure strong market trends before entering short positions.

Risk Management:

Stop-Loss: A dynamic stop-loss is placed for each trade based on the trader's maximum risk per lot. The stop-loss adapts to market conditions using ATR trailing stops to capture further gains as the trade progresses.

Partial Profit Booking: Once the first profit target is hit (2.1x risk for long trades and 2.5x risk for short trades), a percentage of the position is booked as profit, and the remainder is trailed using an ATR stop.

Automation via JSON Alerts:This strategy sends automated JSON alerts to the Dhan platform for seamless execution of orders. The alerts support multi-leg orders for both entry and exit, ensuring that trades are executed efficiently without manual intervention.

Why Use This Strategy?

The Nifty Scalping 3 Minutes Options on Dhan strategy is perfect for traders who want to capitalize on quick market moves in options, backed by strong risk management and automation. With automated alerts, customizable inputs, and advanced technical filters, this strategy is ideal for traders looking to engage in high-probability options trades with minimal effort.

For more detailed information about the underlying logic, you can refer to the previously published Nifty Scalping 3 Minutes Strategy here.

Disclaimer:

This strategy is provided as an educational tool, and we are not affiliated with or sponsored by Dhan. The strategy integrates with the Dhan platform for automated trading, but there is no formal relationship between this strategy and Dhan.

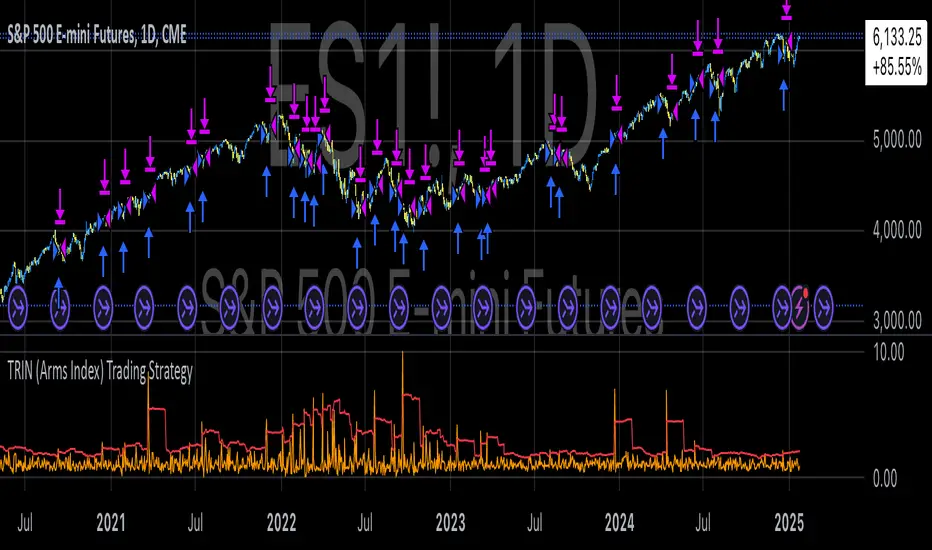

TRIN (Arms Index) Trading StrategyThe TRIN (Arms Index), also known as the Short-Term Trading Index, is a technical indicator designed to gauge the internal strength or weakness of the market. It compares the number of advancing and declining stocks to the advancing and declining volume (AD Volume). A TRIN value above 1.0 generally indicates bearish market conditions, while a value below 1.0 suggests bullish market sentiment.

Strategy Rules:

Entry Condition (Long Position): When the TRIN value is above 1.0, the strategy enters a long position, indicating that the market may be oversold, and a potential reversal could occur.

Exit Condition: The strategy exits the long position when the closing price is higher than the previous day’s high, signaling a potential rebound in the market.

This strategy aims to capitalize on short-term market inefficiencies by entering trades during periods of potential market weakness and exiting when signs of recovery appear.

How the TRIN Index Works:

The TRIN is calculated as follows:

TRIN=Advancing Issues / Declining IssuesAdvancing Volume / Declining Volume

TRIN=Advancing Volume / Declining VolumeAdvancing Issues / Declining Issues

A TRIN value above 1.0 indicates that the market is potentially oversold (more declining stocks with higher volume), while a value below 1.0 suggests the market may be overbought (more advancing stocks with higher volume) .

Empirical Evidence:

Market Sentiment Indicator: The TRIN has been widely used as a sentiment indicator. Research by Zweig (1997) suggests that extreme TRIN values can serve as a contrarian signal, indicating potential turning points in the market. For instance, a TRIN above 2.0 is often considered a sign of panic selling, which can precede a market bottom .

Overbought/Oversold Conditions: Studies have shown that indicators like TRIN, which measure market breadth and volume, can be effective in identifying overbought and oversold conditions. According to Fama and French (1988), market sentiment indicators that consider both price and volume data can offer insights into future price movements .

Risks and Limitations:

False Signals:

One of the primary risks of using the TRIN-based strategy is the possibility of false signals. A TRIN value above 1.0 does not always guarantee a market rebound, especially in sustained bearish trends. In such cases, the strategy might enter long positions prematurely, leading to losses.

Research by Brock, Lakonishok, and LeBaron (1992) found that while market indicators like TRIN can be useful, they are not foolproof and can generate multiple false positives, particularly in volatile markets .

Market Regimes:

The effectiveness of the TRIN index can vary depending on the market regime. In strongly trending markets, either bullish or bearish, the TRIN may not provide reliable reversal signals, and relying on it could result in trades that go against the prevailing trend. For instance, during strong bear markets, the TRIN may frequently remain above 1.0, leading to multiple losing trades as the market continues to decline.

Short-Term Focus:

The TRIN strategy is inherently short-term focused, aiming to capture quick market reversals. This makes it sensitive to market noise and less effective for longer-term investors. Moreover, short-term trading strategies often require more frequent adjustments and can incur higher transaction costs, which may erode profitability over time.

Liquidity and Execution Risk:

Since the TRIN strategy requires entering and exiting trades based on short-term market movements, it is vulnerable to liquidity and execution risks. In fast-moving markets, the execution of trades may be delayed, leading to slippage and potentially unfavorable entry or exit points.

Conclusion:

The TRIN (Arms Index) Trading Strategy can be an effective tool for traders looking to capitalize on short-term market inefficiencies and potential reversals. However, it is important to recognize the risks associated with this strategy, including false signals, sensitivity to market regimes, and execution risks. Traders should employ proper risk management techniques and consider combining the TRIN with other indicators to improve the robustness of the strategy.

While the TRIN provides valuable insights into market sentiment, it is not a standalone solution and should be used in conjunction with a broader trading plan that takes into account both technical and fundamental analysis.

References:

Arms, Richard W. "Volume Adjusted Moving Averages." Technical Analysis of Stocks & Commodities, 1993.

Zweig, Martin. Winning on Wall Street. Warner Books, 1997.

Fama, Eugene F., and Kenneth R. French. "Permanent and Temporary Components of Stock Prices." Journal of Political Economy, 1988.

Brock, William, Josef Lakonishok, and Blake LeBaron. "Simple Technical Trading Rules and the Stochastic Properties of Stock Returns." Journal of Finance, 1992.

Nifty scalping 3 minutesOverview:

The "Nifty Scalping 3 Minutes" strategy is a uniquely tailored trading system for Nifty Futures traders, with a clear focus on capital preservation, dynamic risk management, and high-probability trade entries. This strategy uses unique combination of standard technical indicators like Jurik Moving Average (JMA), Exponential Moving Average (EMA), and Bollinger Bands, but it truly stands out through its Price-Volume Spike Detection system—a unique mechanism designed to trigger trades only during periods of high momentum and market participation. The strategy also incorporates robust risk management, ensuring that traders minimize losses while maximizing profits. in complete back test range max drawdown is less than 1%

Scalping Approach and Requirements:

The strategy focuses on quick in and out trades, aiming to capture small, quick profits during periods of heightened market activity. For optimal performance, traders should have ₹2,00,000 or more in capital available per trade. The dynamic lot calculation and risk controls require this level of capital to function effectively.

Small, frequent trades are the focus, and the strategy is ideal for traders comfortable with high-frequency executions. Traders with insufficient capital or those not comfortable with frequent trades may find this strategy unsuitable.

Default Properties for Publication:

Initial Capital: ₹2,000,000

Lot Size: 25 contracts (adjusted dynamically based on available margin)

Stop-Loss: Risk per trade capped at 1% of equity.

Slippage and Commission: Realistic values are factored into the backtesting.

Key Feature: Price-Volume Spike Detection

1. Condition: Trades are executed only when there is a significant price spike confirmed by a volume spike. The candle width is calculated by multiplying the price change (difference between the candle's open and close) by the volume, and this result is compared to a 126-period average of both price and volume.

A trade is triggered when the current price-volume spike exceeds this average by a preset volume multiplier (default set at 3). This ensures that both the price change and volume are unusually strong compared to normal market behavior.

2. Reasoning: Many traders fail to incorporate the relationship between price movement and volume effectively. By using this Price-Volume Spike Detection mechanism, the strategy ensures that it only enters trades during periods of strong market momentum when both price and volume confirm a real market move, not just noise or small fluctuations.

The 126-period moving average of volume is chosen specifically because it represents a complete trading session on the 3-minute chart. This ensures that the volume spike is compared against a realistic baseline of daily activity, making the detection more robust and reliable.

The volume multiplier allows flexibility in determining the threshold for a significant spike, enabling users to fine-tune the strategy according to their risk tolerance and market conditions.

Trade Placement Logic:

1. Trend Confirmation with JMA and EMA:

Condition: The strategy will only consider entering a trade when JMA crosses above EMA for a long trade or JMA crosses below EMA for a short trade.

Reasoning: The JMA is used for its low lag and responsiveness, allowing it to capture early trends, while the EMA adds a level of confirmation by weighing recent price action more heavily. This dual confirmation ensures that trades are entered only when a solid trend is in place.

2. Bollinger Bands for Volatility Breakouts:

Condition: In addition to the JMA-EMA crossover, the price must break outside the Bollinger Bands—above the upper band for long trades, or below the lower band for short trades.

Reasoning: Bollinger Bands are a volatility indicator. By requiring a price breakout beyond the bands, the strategy ensures that trades are placed during periods of high volatility, avoiding low-momentum, sideways markets.

3. Volume and Price Confirmation (Price-Volume Spike Detection):

Condition: A trade is only triggered if the price-volume spike condition is met. This ensures that the market move is backed by strong volume and that the price change is significant relative to the recent average activity.

Reasoning: This condition filters out low-volume environments where price movements are more likely to reverse or stall. By waiting for a spike in both price and volume, the strategy ensures that it enters trades during high-momentum periods, where follow-through is more likely.

Exit Logic and Risk Management:

1. Stop-Loss (SL) Placement:

Condition: Upon entering a trade, an initial stop-loss is placed below the candle low for long trades or above the candle high for short trades. This is adjusted if the risk exceeds 1% of total capital.

Reasoning: The stop-loss is placed at a logical level that accounts for recent price action, ensuring that the trade is given room to develop while protecting capital from unexpected market reversals.

2. Profit Target and Partial Profit Booking:

Condition: The first profit target is set at 2.1x the initial risk for long trades, and 2.5x the initial risk for short trades.

Reasoning: The 2.1x risk-reward ratio for long trades provides a solid return while maintaining a conservative risk profile. For short trades, the strategy uses a higher 2.5x risk-reward ratio because market falls tend to be sharper and quicker than rises, allowing for larger profit targets to be reached more reliably.

Partial Profit Booking: Once the first target is hit, 60% of the position is closed to lock in profits. The remaining 40% is left to run with a trailing stop.

3. ATR-Based Trailing Stop:

Condition: Once the first target is hit, the ATR (Average True Range) trailing stop is applied to the remaining position. This dynamically adjusts the stop-loss as the trade moves in a favorable direction.

Reasoning: The trailing stop allows the trade to capture further gains if the trend continues, while protecting profits if the momentum weakens. The ATR ensures that the stop adjusts according to the market's current volatility, providing flexibility and protection.

4. Time-Based Exit:

Condition: If a trade is still open by 3:20 PM, it is automatically closed to avoid end-of-day volatility.

Reasoning: The time-based exit ensures that trades are not held into the often-volatile closing minutes of the market, reducing the risk of unexpected price swings.

Capital and Risk Management:

1. Lot Size Calculation:

Condition: The strategy calculates the number of lots dynamically based on the available margin. It uses only 10% of total equity for each trade, and ensures that the maximum risk per trade does not exceed 1% of total capital.

Reasoning: This ensures that traders are not over-leveraged and that the risk is controlled for each trade. Capital protection is at the core of the strategy, ensuring that even during adverse market conditions, the trader’s capital is preserved.

2. Stop-Loss Protection:

Condition: The stop-loss is designed to ensure that no more than 1% of capital is at risk in any trade.

Reasoning: By limiting risk exposure, the strategy focuses on long-term capital preservation while still allowing for profitable trades in favorable market conditions.

STBT/BTST Facilitation:

1. Feature: The strategy allows traders the option to hold positions overnight, facilitating STBT (Sell Today Buy Tomorrow) and BTST (Buy Today Sell Tomorrow) trades.

Reasoning: Backtests show that holding positions overnight when all trade conditions are still valid can lead to beneficial outcomes. This feature allows traders to take advantage of overnight market movements, providing flexibility beyond intraday trades.

Why This Strategy Stands Out:

Price-Volume Spike Detection: Unlike traditional strategies, this one uniquely focuses on Price-Volume Spike Detection to filter out low-probability trades. By ensuring that both price and volume spikes are present, the strategy guarantees that trades are placed only when there is significant market momentum.

Risk Management with Capital Protection: The strategy strictly limits the risk per trade to 1% of capital, ensuring long-term capital preservation. This is especially important for traders who wish to avoid large drawdowns and prefer a sustainable approach to trading.

2.5x Risk-Reward for Short Trades: Recognizing the sharpness of market declines, the strategy employs a 2.5x risk-reward ratio for short trades, maximizing profits during bearish trends.

Dynamic Exit Strategy: With partial profit booking and ATR-based trailing stops, the strategy is designed to capture gains efficiently while protecting capital through dynamic exit conditions.

Summary of Execution:

Entry: Triggered when JMA crosses EMA, combined with Bollinger Band breakouts and Price-Volume Spike Detection.

Capital Management: Trades are executed with 10% of available capital, and the risk per trade is capped at 1%.

Exit: Trades exit when stop-loss, ATR trailing stop, or time-based exit conditions are met.

Profit Booking: 60% of the position is closed at the first target, with the remainder trailed using an ATR-based stop.

Price-Volume w Trendline - Strategy [presentTrading]█ Introduction and How it is Different

The Price-Volume with Trendline Strategy is an innovative strategy that combines volume profile analysis, price-based Z-scores, and dynamic trendline filtering to identify optimal entry and exit points in the market. What sets this strategy apart is the integration of volume concentration (Point of Control or PoC) with dynamic volatility thresholds. Additionally, this strategy introduces a multi-step take profit (TP) mechanism that adjusts based on predefined levels, allowing traders to exit trades progressively while capitalizing on market momentum.

BTCUSD 6hr LS Performance

█ Strategy, How it Works: Detailed Explanation

The combination of multiple indicators and methodologies serves to create a more robust and reliable trading system. Each element is carefully chosen for its complementary role in providing accurate signals while minimizing false entries and exits. Here’s why the different components were chosen and how they work together:

- PoC and Z-Scores: The volume profile identifies key price areas, while the Z-score measures deviations from the mean. Together, they highlight points where the market is likely to react. For example, when the Z-score indicates an oversold condition near a PoC support level, it increases the probability of a reversal, providing a clear entry signal.

- Trendlines and Z-Scores: Trendlines serve as a secondary filter to ensure that price deviations identified by Z-scores align with broader market trends. This ensures that trades are only entered when the price has both deviated from its average and broken through a significant trendline level, reducing the likelihood of false signals.

- Multi-Step TP and Risk Management: Finally, the multi-step take profit logic works in tandem with the entry signals generated by the PoC, Z-scores, and trendlines. As the price moves in favor of the trade, profits are gradually locked in, ensuring the trader captures gains while still leaving room for further upside.

🔶 Point of Control (PoC) and Volume Profile Analysis

The PoC identifies the price level with the highest volume concentration within a specified lookback period. This price level represents where the most trading activity has occurred, often acting as a strong support or resistance. By breaking down the range into several rows (bins), the strategy identifies how much volume was traded at each price level.

🔶 Z-Score Calculation

The Z-score is a statistical metric that measures how far the current price is from its mean, expressed in terms of standard deviations. This is calculated both for price deviation and PoC-based deviation.

🔶 Trendline Breakout Filtering

The trendline filtering is a crucial aspect that refines entry signals by confirming trend continuation or reversals. It calculates trendlines based on pivot highs and lows using the selected method (e.g., ATR or standard deviation).

🔶 Multi-Step Take Profit

The multi-step take profit mechanism allows the strategy to take partial profits at several predefined levels. For example, when the price reaches 3%, 8%, 14%, or 21% above (or below) the entry price, it exits portions of the position. This is a useful technique for locking in profits as the market moves favorably.

Local

█ Usage

The Price-Volume with Trendline Strategy can be applied to various asset classes, including stocks, cryptocurrencies, and commodities. It is particularly effective in volatile markets where price deviations and volume concentrations signal potential reversals or trend continuations. By adjusting the settings for volatility and the lookback period, this strategy can be tailored to both short-term intraday trades and longer-term swing trades.

█ Default Settings

The default settings in the strategy play a vital role in shaping its performance.

- POC_lookbackLength (144): This defines the number of bars used to calculate the PoC. A longer lookback captures more data, leading to a more stable PoC, but may result in delayed signals. A shorter lookback increases responsiveness but may introduce noise.

- priceDeviationLength (200): This determines the period for calculating the standard deviation of price. A higher length smooths out the volatility, reducing the likelihood of false signals. Shorter lengths make the strategy more sensitive to sudden price movements.

- TL_length (14): Controls the swing detection period for trendline calculation. A shorter length will generate more frequent trendline breakouts, while a longer length captures only significant moves.

- Stop Loss and Take Profit: The strategy offers both fixed and SuperTrend-based stop losses. SuperTrend is adaptive to volatility, while fixed stop losses provide simpler risk control. The multi-step take profit ensures that profits are secured progressively, which can improve performance in trending markets by reducing the risk of full reversals.

Each of these settings can significantly affect the strategy’s risk-reward balance. For instance, increasing the stop loss level or the take profit percentages allows the strategy to stay in trades longer, potentially increasing profit per trade but at the cost of larger drawdowns. Conversely, tighter stops and smaller profit targets result in more frequent trades with lower average profit per trade.

PVT Crossover Strategy**Release Notes**

**Strategy Name**: PVT Crossover Strategy

**Purpose**: This strategy aims to capture entry and exit points in the market using the Price-Volume Trend (PVT) and its Exponential Moving Average (EMA). It specifically uses the crossover of PVT with its EMA as signals to identify changes in market trends.

**Uniqueness and Usefulness**

**Uniqueness**: This strategy is unique in its use of the PVT indicator, which combines price changes with trading volume to track trends. The filtering with EMA reduces noise and provides more accurate signals compared to other indicators.

**Usefulness**: This strategy is effective for traders looking to detect trend changes early. The signals based on PVT and its EMA crossover work particularly well in markets where volume fluctuations are significant.

**Entry Conditions**

**Long Entry**:

- **Condition**: A crossover occurs where PVT crosses above its EMA.

- **Signal**: A buy signal is generated, indicating a potential uptrend.

**Short Entry**:

- **Condition**: A crossunder occurs where PVT crosses below its EMA.

- **Signal**: A sell signal is generated, indicating a potential downtrend.

**Exit Conditions**

**Exit Strategy**:

- The strategy does not explicitly program exit conditions beyond the entry signals, but traders are encouraged to close positions manually based on signals or apply their own risk management strategy.

**Risk Management**

This strategy does not include default risk management rules, so traders should implement their own. Consider using trailing stops or fixed stop losses to manage risk.

**Account Size**: ¥100,000

**Commissions and Slippage**: 94 pips per trade for commissions and 1 pip for slippage

**Risk per Trade**: 10% of account equity

**Configurable Options**

**Configurable Options**:

- **EMA Length**: The length of the EMA used to calculate the EMA of PVT (default is 20).

- **Signal Display Control**: The option to turn the display of signals on or off.

**Adequate Sample Size**

To ensure the robustness and reliability of this strategy, it is recommended to backtest it with a sufficiently long period of historical data, especially across different market conditions.

**Credits**

**Acknowledgments**:

This strategy is based on the concept of the PVT indicator and its application in strategy design, drawing on contributions from technical analysis and the trading community.

**Clean Chart Description**

**Chart Appearance**:

This strategy is designed to maintain a clean and simple chart by turning off the plot of PVT, its EMA, and entry signals. This reduces clutter and allows for more effective trend analysis.

**Addressing the House Rule Violations**

**Omissions and Unrealistic Claims**

**Clarification**:

This strategy does not make unrealistic or unsupported claims about its performance, and all signals are for educational purposes only, not guaranteeing future results. It is important to understand that past performance does not guarantee future outcomes.

Innocent Heikin Ashi Ethereum StrategyHello there, im back!

If you are familiar with my previous scripts, this one will seem like the future's nostalgia!

Functionality:

As you can see, all candles are randomly colored. This has no deeper meaning, it should remind you to switch to Heikin Ashi. The Strategy works on standard candle stick charts, but should be used with Heikin Ashi to see the actual results. (Regular OHLC calculations are included.)

Same as in my previous scripts we import our PVSRA Data from @TradersReality open source Indicator.

With this data and the help of moving averages, we have got an edge in the market.

Signal Logic:

When a "violently green" candle appears (high buy volume + tick speed) above the 50 EMA indicates a change in trend and sudden higher prices. Depending on OHLC of the candle itself and volume, Take Profit and Stop Loss is calculated. (The price margin is the only adjustable setting). Additionally, to make this script as simple and easily useable as possible, all other adjustable variables have been already set to the best suitable value and the chart was kept plain, except for the actual entries and exits.

Basic Settings and Adjustables:

Main Input 1: TP and SL combined price range. (Double, Triple R:R equally.)

Trade Inputs: All standard trade size and contract settings for testing available.

Special Settings:

Checkbox 1: Calculate Signal in Heikin Ashi chart, including regular candle OHLC („Open, High, Low, Close“)

Checkbox 2/3: Calculate by order fill or every tick.

Checkbox 4: Possible to fill orders on bar close.

Timeframe and practical usage:

Made for the 5 Minute to 1 hour timeframe.

Literally ONLY works on Ethereum and more or less on Bitcoin.

EVERY other asset has absolute 0% profitability.

Have fun and share with your friends!

Thanks for using!

Example Chart:

Rsi Long-Term Strategy [15min]Hello, I would like to present to you The "RSI Long-Term Strategy" for 15min tf

The "RSI Long-Term Strategy " is designed for traders who prefer a combination of momentum and trend-following techniques. The strategy focuses on entering long positions during significant market corrections within an overall uptrend, confirmed by both RSI and volume. The use of long-term SMAs ensures that trades are made in line with the broader market trend. The stop-loss feature provides risk management by limiting losses on trades that do not perform as expected. This strategy is particularly well-suited for longer-term traders who monitor 15-minute charts but look for substantial trend reversals or continuations.

Indicators and Parameters:

Relative Strength Index (RSI):

- The RSI is calculated using a 10-period length. It measures the magnitude of recent price changes to evaluate overbought or oversold conditions. The script defines oversold conditions when the RSI is at or below 30 and overbought conditions when the RSI is at or above 70.

Volume Condition:

-The strategy incorporates a volume condition where the current volume must be greater than 2.5 times the 20-period moving average of volume. This is used to confirm the strength of the price movement.

Simple Moving Averages (SMA):

- The strategy uses two SMAs: SMA1 with a length of 250 periods and SMA2 with a length of 500 periods. These SMAs help identify long-term trends and generate signals based on their crossover.

Strategy Logic:

Entry Logic:

A long position is initiated when all the following conditions are met:

The RSI indicates an oversold condition (RSI ≤ 30).

SMA1 is above SMA2, indicating an uptrend.

The volume condition is satisfied, confirming the strength of the signal.

Exit Logic:

The strategy closes the long position when SMA1 crosses under SMA2, signaling a potential end of the uptrend (a "Death Cross").

Stop-Loss:

A stop-loss is set at 5% below the entry price to manage risk and limit potential losses.

Buy and sell signals are highlighted with circles below or above bars:

Green Circle : Buy signal when RSI is oversold, SMA1 > SMA2, and the volume condition is met.

Red Circle : Sell signal when RSI is overbought, SMA1 < SMA2, and the volume condition is met.

Black Cross: "Death Cross" when SMA1 crosses under SMA2, indicating a potential bearish signal.

to determine the level of stop loss and target point I used a piece of code by RafaelZioni, here is the script from which a piece of code was taken

I hope the strategy will be helpful, as always, best regards and safe trades

;)

Gann + Laplace Smoothed Hybrid Volume Spread AnalysisThe Gann + Laplace Smoothed Hybrid Volume Spread Analysis ( GannLSHVSA ) Strategy/Indicator is an trading tool designed to fuse volume analysis with trend detection, offering traders a view of market dynamics.

This Strategy/Indicator stands apart by integrating the principles of the upgraded Discrete Fourier Transform (DFT), the Laplace Stieltjes Transform and volume spread analysis, enhanced with a layer of Fourier smoothing to distill market noise and highlight trend directions with unprecedented clarity.

The length of EMA and Strategy Entries are modified with the Gann swings .

This smoothing process allows traders to discern the true underlying patterns in volume and price action, stripped of the distractions of short-term fluctuations and noise.

The core functionality of the GannLSHVSA revolves around the innovative combination of volume change analysis, spread determination (calculated from the open and close price difference), and the strategic use of the EMA (default 10) to fine-tune the analysis of spread by incorporating volume changes.

Trend direction is validated through a moving average (MA) of the histogram, which acts analogously to the Volume MA found in traditional volume indicators. This MA serves as a pivotal reference point, enabling traders to confidently engage with the market when the histogram's movement concurs with the trend direction, particularly when it crosses the Trend MA line, signalling optimal entry points.

It returns 0 when MA of the histogram and EMA of the Price Spread are not align.

WHAT IS GannLSHVSA INDICATOR:

The GannLSHVSA plots a positive trend when a positive Volume smoothed Spread and EMA of Volume smoothed price is above 0, and a negative when negative Volume smoothed Spread and EMA of Volume smoothed price is below 0. When this conditions are not met it plots 0.

HOW TO USE THE STRATEGY:

Here you fine-tune the inputs until you find a combination that works well on all Timeframes you will use when creating your Automated Trade Algorithmic Strategy. I suggest 4h, 12h, 1D, 2D, 3D, 4D, 5D, 6D, W and M.

ORIGINALITY & USEFULNESS:

The GannLSHVSA Strategy is unique because it applies upgraded DFT, the Laplace Stieltjes Transform for data smoothing, effectively filtering out the minor fluctuations and leaving traders with a clear picture of the market's true movements. The DFT's ability to break down market signals into constituent frequencies offers a granular view of market dynamics, highlighting the amplitude and phase of each frequency component. This, combined with the strategic application of Ehler's Universal Oscillator principles via a histogram, furnishes traders with a nuanced understanding of market volatility and noise levels, thereby facilitating more informed trading decisions. The Gann swing strategy is developed by meomeo105, this Gann high and low algorithm forms the basis of the EMA modification.

DETAILED DESCRIPTION:

My detailed description of the indicator and use cases which I find very valuable.

What is the meaning of price spread?

In finance, a spread refers to the difference between two prices, rates, or yields. One of the most common types is the bid-ask spread, which refers to the gap between the bid (from buyers) and the ask (from sellers) prices of a security or asset.

We are going to use Open-Close spread.

What is Volume spread analysis?

Volume spread analysis (VSA) is a method of technical analysis that compares the volume per candle, range spread, and closing price to determine price direction.

What does this mean?

We need to have a positive Volume Price Spread and a positive Moving average of Volume price spread for a positive trend. OR via versa a negative Volume Price Spread and a negative Moving average of Volume price spread for a negative trend.

What if we have a positive Volume Price Spread and a negative Moving average of Volume Price Spread?

It results in a neutral, not trending price action.

Thus the Indicator/Strategy returns 0 and Closes all long and short positions.

I suggest using "Close all" input False when fine-tuning Inputs for 1 TimeFrame. When you export data to Excel/Numbers/GSheets I suggest using "Close all" input as True, except for the lowest TimeFrame. I suggest using 100% equity as your default quantity for fine-tune purposes. I have to mention that 100% equity may lead to unrealistic backtesting results. Be avare. When backtesting for trading purposes use Contracts or USDT.

Fine-tune Inputs: Gann + Laplace Smooth Volume Zone OscillatorUse this Strategy to Fine-tune inputs for the GannLSVZ0 Indicator.

Strategy allows you to fine-tune the indicator for 1 TimeFrame at a time; cross Timeframe Input fine-tuning is done manually after exporting the chart data.

I suggest using "Close all" input False when fine-tuning Inputs for 1 TimeFrame. When you export data to Excel/Numbers/GSheets I suggest using "Close all" input as True, except for the lowest TimeFrame.

MEANINGFUL DESCRIPTION:

The Volume Zone oscillator breaks up volume activity into positive and negative categories. It is positive when the current closing price is greater than the prior closing price and negative when it's lower than the prior closing price. The resulting curve plots through relative percentage levels that yield a series of buy and sell signals, depending on level and indicator direction.

The Gann Laplace Smoothed Volume Zone Oscillator GannLSVZO is a refined version of the Volume Zone Oscillator, enhanced by the implementation of the upgraded Discrete Fourier Transform, the Laplace Stieltjes Transform. Its primary function is to streamline price data and diminish market noise, thus offering a clearer and more precise reflection of price trends.

By combining the Laplace with Gann Swing Entries and with Ehler's white noise histogram, users gain a comprehensive perspective on volume-related market conditions.

HOW TO USE THE INDICATOR:

The default period is 2 but can be adjusted after backtesting. (I suggest 5 VZO length and NoiceR max length 8 as-well)

The VZO points to a positive trend when it is rising above the 0% level, and a negative trend when it is falling below the 0% level. 0% level can be adjusted in setting by adjusting VzoDifference. Oscillations rising below 0% level or falling above 0% level result in a natural trend.

HOW TO USE THE STRATEGY:

Here you fine-tune the inputs until you find a combination that works well on all Timeframes you will use when creating your Automated Trade Algorithmic Strategy. I suggest 4h, 12h, 1D, 2D, 3D, 4D, 5D, 6D, W and M.

When Indicator/Strategy returns 0 or natural trend, Strategy Closes All it's positions.

ORIGINALITY & USFULLNESS:

Personal combination of Gann swings and Laplace Stieltjes Transform of a price which results in less noise Volume Zone Oscillator.

The Laplace Stieltjes Transform is a mathematical technique that transforms discrete data from the time domain into its corresponding representation in the frequency domain. This process involves breaking down a signal into its individual frequency components, thereby exposing the amplitude and phase characteristics inherent in each frequency element.

This indicator utilizes the concept of Ehler's Universal Oscillator and displays a histogram, offering critical insights into the prevailing levels of market noise. The Ehler's Universal Oscillator is grounded in a statistical model that captures the erratic and unpredictable nature of market movements. Through the application of this principle, the histogram aids traders in pinpointing times when market volatility is either rising or subsiding.

The Gann swing strategy is developed by meomeo105, this Gann high and low algorithm forms the basis of the EMA modification.

DETAILED DESCRIPTION:

My detailed description of the indicator and use cases which I find very valuable.

What is oscillator?

Oscillators are chart indicators that can assist a trader in determining overbought or oversold conditions in ranging (non-trending) markets.

What is volume zone oscillator?

Price Zone Oscillator measures if the most recent closing price is above or below the preceding closing price.

Volume Zone Oscillator is Volume multiplied by the 1 or -1 depending on the difference of the preceding 2 close prices and smoothed with Exponential moving Average.

What does this mean?

If the VZO is above 0 and VZO is rising. We have a bullish trend. Most likely.

If the VZO is below 0 and VZO is falling. We have a bearish trend. Most likely.

Rising means that VZO on close is higher than the previous day.

Falling means that VZO on close is lower than the previous day.

What if VZO is falling above 0 line?

It means we have a high probability of a bearish trend.

Thus the indicator returns 0 and Strategy closes all it's positions when falling above 0 (or rising bellow 0) and we combine higher and lower timeframes to gauge the trend.

What is approximation and smoothing?

They are mathematical concepts for making a discrete set of numbers a

continuous curved line.

Laplace Stieltjes Transform approximation of a close price are taken from aprox library.

Key Features:

You can tailor the Indicator/Strategy to your preferences with adjustable parameters such as VZO length, noise reduction settings, and smoothing length.

Volume Zone Oscillator (VZO) shows market sentiment with the VZO, enhanced with Exponential Moving Average (EMA) smoothing for clearer trend identification.

Noise Reduction leverages Euler's White noise capabilities for effective noise reduction in the VZO, providing a cleaner and more accurate representation of market dynamics.

Choose between the traditional Fast Laplace Stieltjes Transform (FLT) and the innovative Double Discrete Fourier Transform (DTF32) soothed price series to suit your analytical needs.

Use dynamic calculation of Laplace coefficient or the static one. You may modify those inputs and Strategy entries with Gann swings.

I suggest using "Close all" input False when fine-tuning Inputs for 1 TimeFrame. When you export data to Excel/Numbers/GSheets I suggest using "Close all" input as True, except for the lowest TimeFrame. I suggest using 100% equity as your default quantity for fine-tune purposes. I have to mention that 100% equity may lead to unrealistic backtesting results. Be avare. When backtesting for trading purposes use Contracts or USDT.

AsianRange, KillZones, RSI Bars, and Supertrend Strategy by VKombinacija AsianRange, KillZones, RSI Bars, and Supertrend Strategy

zavaUnni-bitcoin signals(1day)

📌 This strategy predicts price movements based on trading volume and enters positions accordingly. It calculates the expected price increase based on bullish volume and the expected price decrease based on bearish volume to determine the direction of the position.

Top predicted price based on declining bullish volume: top_ifpricebull

Bottom predicted price based on declining bearish volume: top_ifpricebear

Top predicted price based on increasing bullish volume: bot_ifpricebull

Bottom predicted price based on increasing bearish volume: bot_ifpricebear

Using these four values, the strategy calculates the final maxprice and minprice based on volume. If the price settles above the max value, it indicates an upward trend; if it settles below the min value, it indicates a downward trend.

📌 The indicator does not solely rely on the maxprice and minprice conditions. It incorporates complex and sophisticated analysis by considering average volume and candle size.

During a decline, if the average volume and spread of bullish candles exceed those of bearish candles and the price settles above the max value, a long position is entered.

During a rise, if the average volume and spread of bearish candles exceed those of bullish candles and the price settles below the min value, a short position is entered.