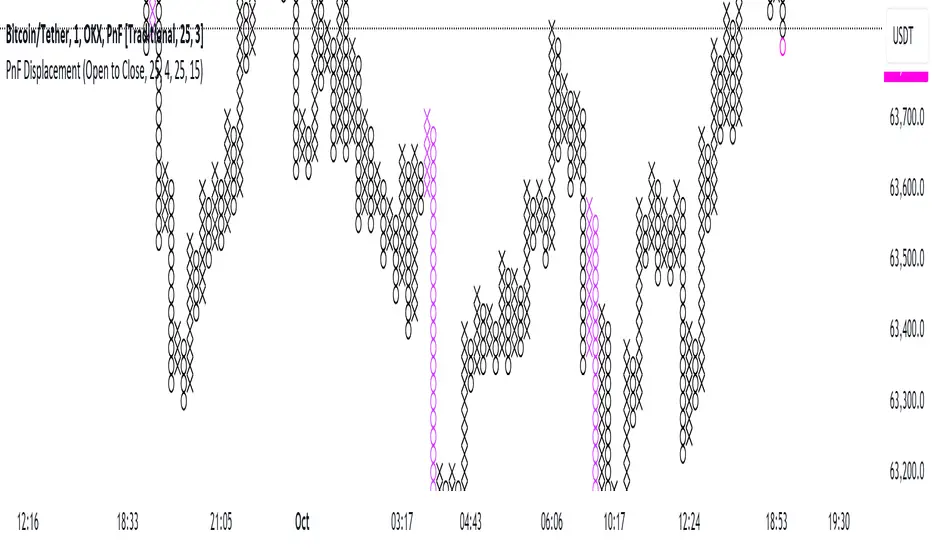

Point and Figure Displacement IndicatorThe PnF Displacement indicator is my custom script for TradingView, designed to analyze Point and Figure (PnF) charts with displacement features.

Key components of the script include:

User Inputs:

Require FVG: A boolean input to determine if a Fair Value Gap (FVG) is required for displacement calculations.

Displacement Type: Allows users to choose between "Open to Close" and "High to Low" for column range calculations.

Displacement Length: Defines how far back to look for calculating the standard deviation of the column range.

Displacement Strength: Multiplier for the standard deviation to adjust sensitivity.

Box Size: Sets the size of each box in the PnF chart.

Number of Boxes for Minimum Displacement: Specifies how many boxes to consider for calculating the minimum displacement.

Displacement Logic:

The script calculates the column range based on the selected displacement type.

It computes a standard deviation of the candle range and determines a minimum displacement based on user-defined box size and count.

The displacement condition combines the FVG check and the column range against the calculated minimum.

Visual Representation:

The bars are colored based on displacement conditions, enhancing visual analysis on the chart.

This indicator aids traders in identifying significant price movements in PnF charts while incorporating user customization options for better analysis.

Volume

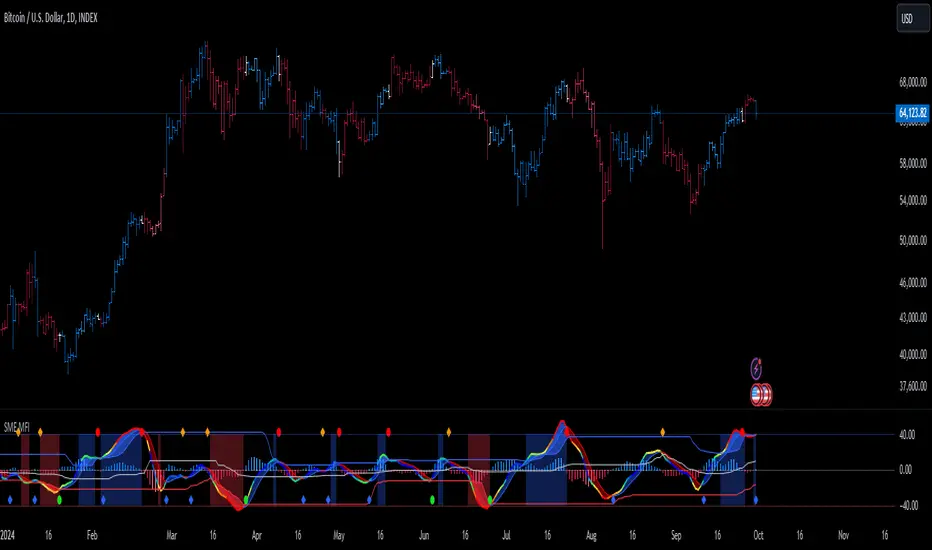

SMI Ergodic Indicator/Oscillator of Money Flow Index▮ Introduction

The Stochastic Momentum Index Ergodic (SMII) indicator is a technical analysis tool designed to predict trend reversals in the price of an asset.

It functions as a momentum oscillator, measuring the ratio of the smoothed price change to the smoothed absolute price change over a given number of previous periods.

The Ergodic SMI is based on the True Strength Index (TSI) and integrates a signal line, which is an exponential moving average (EMA) of the SMI indicator itself.

The Ergodic SMI oscillator provides a clearer picture of market trends than the traditional stochastic oscillator by incorporating the concept of 'ergodicity', which helps remove market noise.

On ther other hand, MFI (Money Flow Index) is a technical analysis indicator used to measure the inflow of money into an asset and thus help identify buying and selling pressure in a given financial instrument.

When these two indicators are combined, they can provide a more comprehensive view of price direction and market strength.

▮ Motivation: why another indicator?

By combining SMII with MFI, we can gain even more insights into the market.

One way to do this is to use the MFI as an input to the SMII, rather than just using price.

This means we are measuring momentum based on buying and selling pressure rather than just price.

Furthermore, there is the possibility of making several fine adjustments to both the calculation and visualization parameters that are not present in other indicators.

▮ What to look for

When using the SMII MFI indicator, there are a few things to look out for.

First, look at the SMII signal line.

When the line crosses above -40, it is considered a buy signal, while the crossing below +40 is considered a sell signal.

Also, pay attention to divergences between the SMII and the price.

If price is rising but the SMII is showing negative divergence, it could indicate that momentum is waning and a reversal could be in the offing.

Likewise, if price is falling but the SMII is showing positive divergence, this could indicate that momentum is building and a reversal could also be in the offing.

Divergences can be considered in both indicator and/or histogram.

Examples:

▮ Notes

The indicator presented here offers both the 'SMII' and the 'SMIO', that is, the 'Stochastic Momentum Index Ergodic Indicator' together with the 'Stochastic Momentum Index Ergodic Oscillator' (histogram), as per the documentation described in reference links.

So it is important to highlight the differences in relation to my other indicator, the 'Stochastic Momentum Index (SMI) of Money Flow Index (MFI)':

This last one is purely based on the SMI , which is implemented using SMA smoothing for the relative range and the high/low range.

Although they may seem the same in some situations, the calculation is actually different. The TSI tends to be more responsive at the expense of being noisier, while the SMI tends to be smoother. Which of these two indicators is best depends on the situation, the context, and the analyst's personal preference.

Please refer to reference links to more info.

▮ References

SMI documentation

SMII documentation

SMIO documentation

MFI documentation

Bubbles Volume [BigBeluga]The Bubbles Volume indicator is an innovative visualization tool designed to represent trading volume in a more intuitive and visually appealing manner. By displaying volume as bubbles of varying sizes and colors on the price chart, this indicator helps traders quickly identify significant volume levels and potential areas of interest.

Important Note:

For correct visual representation of indicator, layout it to front:

🔵 KEY FEATURES

● Volume Bubbles

Represents trading volume as bubbles on the price chart

Bubble size increases with higher volume levels

Color intensity changes based on volume significance

Provides an intuitive visual representation of volume distribution

● Heatmap Coloring

Optional feature to color bubbles based on volume intensity

Uses a color gradient from cool (low volume) to hot (high volume) colors

Helps quickly identify extremely high volume areas

● Significant Volume Levels

Option to display horizontal lines at significant volume levels

Shows volume amount as labels for highly significant levels

Helps identify potential support/resistance areas based on volume

Volume Levels:

Levels with HeatMap:

Levels without Volume Bubles:

● Normalized Volume Calculation

Uses normalized volume to account for overall market volume trends

Provides a more accurate representation of volume significance

🔵 HOW TO USE

● Volume Analysis

Larger bubbles indicate higher trading volume

Clusters of large bubbles may suggest areas of high interest or potential reversals

Use in conjunction with price action to identify potential breakouts or fakeouts

● Trend Confirmation

Strong trends often show increasing bubble sizes in the trend direction

Diminishing bubble sizes might indicate weakening trends

● Support and Resistance

Significant volume levels (displayed as lines) can act as potential support/resistance

Pay attention to price reactions at these levels for trading opportunities

● Divergences

Look for divergences between price action and bubble sizes

Price making new highs/lows with smaller bubbles might indicate weakening momentum

● Volatility Assessment

Periods with consistently large bubbles indicate high volatility

Can be used to adjust trading strategies or position sizing

🔵 CUSTOMIZATION

The Bubbles Volume indicator offers several customization options:

Toggle bubble display on/off

Adjust volume threshold for filtering low volume bubbles

Enable/disable heatmap coloring for enhanced visual analysis

Show/hide significant volume levels

Adjust the number of significant levels displayed

Customize colors to suit personal preferences

By fine-tuning these settings, traders can adapt the indicator to various market conditions and personal analysis preferences.

The Bubbles Volume indicator provides a unique and intuitive way to visualize trading volume directly on the price chart. This approach allows traders to quickly identify areas of significant trading activity and potential price levels of interest without the need for a separate volume sub-chart.

This tool can be particularly useful for traders focusing on volume analysis, breakout strategies, or those looking to confirm price action with volume. The visual nature of the bubbles makes it easy to spot volume patterns and anomalies at a glance, potentially leading to faster and more informed trading decisions.

As with all technical indicators, it's recommended to use the Bubbles Volume indicator in conjunction with other forms of analysis and within the context of a well-defined trading strategy. While this indicator provides valuable volume insights, it should be considered alongside other factors such as overall market trends, price patterns, and fundamental analysis when making trading decisions.

Theoretical price by volumeThis code is used to calculate a theoretical price range based on volume and price change and display it on the chart. Specifically, it calculates the “theoretical price volatility” based on price changes and volume, from which the upper and lower price limits are derived.

The price volatility is calculated by dividing the price change by the volume as the change unit volume.

Based on this volatility, we calculate the theoretical variation relative to the current price (“Theoretical Variance Difference”).

Based on the results, **Theoretical High Price (p_price) and Theoretical Low Price (m_price)** are calculated.

The chart displays the upper and lower bounds of these theoretical prices in color, and also calculates their mean and standard deviation (in the form of a Bollinger band) and plots them.

The background color on the chart indicates whether the price is within the theoretical price range, and at the same time, the mean and standard deviation of the theoretical prices are used to visualize price movements in more detail.

This indicator helps traders understand the impact of volume on price movements and helps them determine if prices are staying within the theoretical range or if there are unusual movements.

Volume to Shares Outstanding Ratio IndicatorDescription:

This indicator shows the ratio of trading volume to the total number of shares outstanding.

Formula:

Volume to Shares Outstanding Ratio = (Trading Volume / Shares Outstanding) * 100

説明:

このインジケーターは、出来高を発行済株式数で割った比率を表示します。

式:

出来高の割合 = (出来高 / 発行済株式数) × 100

Dynamic Supply and Demand Zones [AlgoAlpha]Introducing the Dynamic Supply and Demand Zones by AlgoAlpha. This indicator is designed to automatically identify and visualize dynamic supply and demand zones on your chart, helping traders pinpoint potential reversal areas and assess market sentiment with enhanced clarity. It adapts to market conditions using a dynamic look-back mechanism, making it more responsive to recent price movements. 📈💡

Key Features

📊 Dynamic Look-Back : Automatically adjusts the look-back period based on the most recent pivot point, ensuring the most relevant data is analyzed.

🎯 Pivot Point Detection : Utilizes a user-defined period to detect significant pivot highs and lows, marking potential reversal points with precision.

🛠 Customizable Parameters : Offers extensive customization options including look-back period, pivot detection sensitivity, resolution, and zone tolerance.

🗺 Visual Display : Shows supply and demand zones as boxes on the chart, with optional profiles and background highlighting to differentiate between bullish and bearish zones.

🖍 Color-Coded Zones : Zones are color-coded for easy identification: green for bullish, red for bearish, and gray for neutral levels.

🔔 Alert Conditions : Triggers alerts when new pivot points are detected, ensuring you never miss a key market movement.

How to Use

🚀 Adding the Indicator : Press the star icon and add the indicator to favorites. Add it to your chart and adjust settings to fit your trading strategy.

🔍 Zone Analysis : Observe the color-coded zones on the chart. Bullish zones indicate potential support areas, while bearish zones suggest resistance. Monitor price interactions with these zones for potential entry and exit signals.

🔔 Alerts : Activate alert conditions for new pivot detections to stay ahead of market reversals.

How It Works

The indicator starts by detecting pivot highs and lows over a specified period. These pivots serve as reference points for determining the analysis range. If the Dynamic Look-Back feature is enabled, the look-back range dynamically adjusts from the most recent pivot to the current bar. Otherwise, a fixed look-back period is used. The price range is divided into multiple bins based on a specified resolution, and each bin’s volume is calculated by accumulating the volume of candles that fall within its price range. A zone is defined as significant if its volume is less than the adjacent bins, and the difference meets the Zone Tolerance criteria, indicating a potential area of support or resistance. These zones are then plotted on the chart as boxes. Bullish zones are shown in green, and bearish zones in red, helping traders visually identify key levels where supply and demand imbalances may cause price reversals.

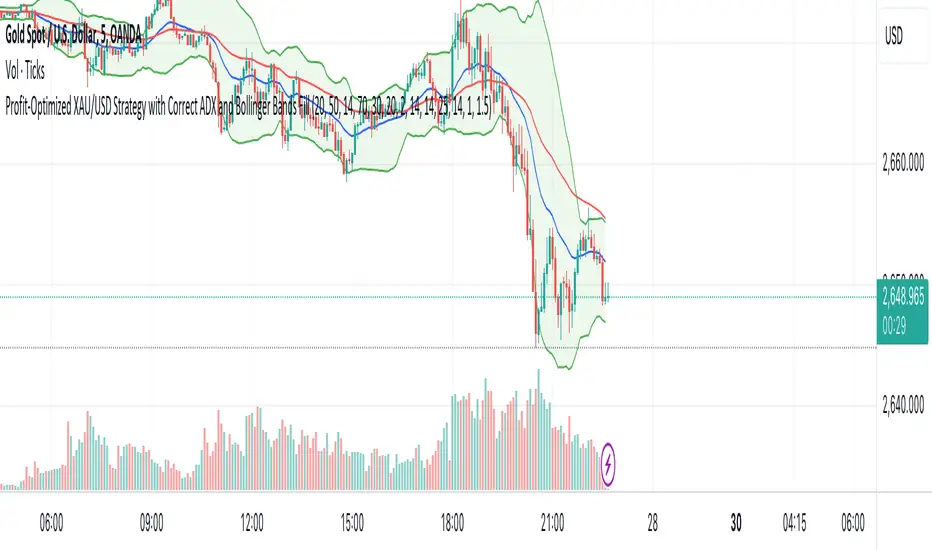

XAU/USD Strategy with Correct ADX and Bollinger Bands Fill1. *Indicators Used*:

- *Exponential Moving Averages (EMAs)*: Two EMAs (20-period and 50-period) are used to identify the trend direction and potential entry points based on crossovers.

- *Relative Strength Index (RSI)*: A momentum oscillator that measures the speed and change of price movements. It identifies overbought and oversold conditions.

- *Bollinger Bands*: These consist of a middle line (simple moving average) and two outer bands (standard deviations away from the middle). They help to identify price volatility and potential reversal points.

- *Average Directional Index (ADX)*: This indicator quantifies trend strength. It's derived from the Directional Movement Index (DMI) and helps confirm the presence of a strong trend.

- *Average True Range (ATR)*: Used to calculate position size based on volatility, ensuring that trades align with the trader's risk tolerance.

2. *Entry Conditions*:

- *Long Entry*:

- The 20 EMA crosses above the 50 EMA (indicating a potential bullish trend).

- The RSI is below the oversold level (30), suggesting the asset may be undervalued.

- The price is below the lower Bollinger Band, indicating potential price reversal.

- The ADX is above a specified threshold (25), confirming that there is sufficient trend strength.

- *Short Entry*:

- The 20 EMA crosses below the 50 EMA (indicating a potential bearish trend).

- The RSI is above the overbought level (70), suggesting the asset may be overvalued.

- The price is above the upper Bollinger Band, indicating potential price reversal.

- The ADX is above the specified threshold (25), confirming trend strength.

3. *Position Sizing*:

- The script calculates the position size dynamically based on the trader's risk per trade (expressed as a percentage of the total capital) and the ATR. This ensures that the trader does not risk more than the specified percentage on any single trade, adjusting the position size according to market volatility.

4. *Exit Conditions*:

- The strategy uses a trailing stop-loss mechanism to secure profits as the price moves in the trader's favor. The trailing stop is set at a percentage (1.5% by default) below the highest price reached since entry for long positions and above the lowest price for short positions.

- Additionally, if the RSI crosses back above the overbought level while in a long position or below the oversold level while in a short position, the position is closed to prevent losses.

5. *Alerts*:

- Alerts are set to notify the trader when a buy or sell condition is met based on the strategy's rules. This allows for timely execution of trades.

### Summary

This strategy aims to capture significant price movements in the XAU/USD market by combining trend-following (EMAs, ADX) and momentum indicators (RSI, Bollinger Bands). The dynamic position sizing based on ATR helps manage risk effectively. By implementing trailing stops and alert mechanisms, the strategy enhances the trader's ability to act quickly on opportunities while mitigating potential losses.

VR1 DEMA - Liquidity IdentifierThis custom Pine Script indicator, titled "VR1 DEMA - Liquidity Identifier", is designed to help traders identify periods of significant resistance to price movement, often indicating high liquidity areas where the market may encounter difficulty moving in one direction. The indicator analyzes the relationship between volume and price range, combined with bar volume conditions, to provide enhanced signals of potential liquidity buildup.

Key Features:

Customizable EMA Lengths:

Users can define the lengths of both the fast and slow Exponential Moving Averages (EMAs), with default values of 5 for the fast EMA and 13 for the slow EMA. These EMAs are calculated from the ratio of volume to price range, smoothing the data to detect trends in liquidity.

Dynamic Fast EMA Color:

The fast EMA changes color based on its relationship to the slow EMA:

Red when the fast EMA is above the slow EMA, signaling stronger resistance or greater liquidity.

White when the fast EMA is below the slow EMA, indicating potentially weaker resistance.

Liquidity Signal with Multiplier Condition:

The background of the chart changes to white when the volume-to-price ratio exceeds 1.5 times the fast EMA. This highlights potential areas of liquidity buildup where price movement may encounter stronger resistance. The 1.5 multiplier is adjustable, allowing for sensitivity customization.

Volume Condition for Enhanced Signals:

A new condition is added that requires the actual bar volume to exceed 1.2 times the 5-period EMA of average bar volume. This ensures that the background color only changes when there is not only increased liquidity but also significantly higher trading volume. The 1.2 multiplier is user-adjustable for further refinement.

Combined Liquidity and Volume Filtering:

Both conditions (volume-to-price ratio and actual volume) must be met for the background color to change. This double-filtering helps traders spot moments of unusual market activity more accurately.

Optional Volume/Price Range Visualization:

An optional plot of the volume-to-price ratio is included, providing a visual representation of how volume interacts with price movement in real-time. This can be enabled or disabled based on user preference.

User-Friendly Customization:

The script includes inputs for adjusting the fast and slow EMA lengths, as well as the multipliers for the volume-to-price ratio and actual volume conditions. These customizable parameters allow traders to tailor the indicator to their specific market strategies.

Use Case:

This indicator is particularly useful for identifying periods of high liquidity and resistance in the market, where price movement may stall or reverse. By combining volume-to-price ratio analysis with actual volume conditions, the indicator provides more reliable signals for detecting potential breakouts, reversals, or consolidation periods. The color-coded fast EMA and background shading make it easy to spot key moments of increased market activity and liquidity.

Dynamic Sentiment RSI [UAlgo]The Dynamic Sentiment RSI is a technical analysis tool that combines the classic RSI (Relative Strength Index) concept with dynamic sentiment analysis, offering traders enhanced insights into market conditions. Unlike the traditional RSI, this indicator integrates volume weighting, sentiment factors, and smoothing features to provide a more nuanced view of momentum and potential market reversals. It is designed to assist traders in detecting overbought/oversold conditions, momentum shifts, and to generate potential buy or sell signals using crossover and crossunder techniques. By dynamically adjusting based on sentiment and volume factors, this RSI offers better adaptability to varying market conditions, making it suitable for different trading styles and timeframes.

This tool is particularly helpful for traders who wish to explore not only price movement but also the underlying market sentiment, offering a more comprehensive approach to momentum analysis. The sentiment factor amplifies the RSI's sensitivity to price shifts, making it easier to detect early signals of market reversals or the continuation of a trend.

🔶 Key Features

Dynamic Sentiment Calculation: The indicator incorporates a "Sentiment Factor" that adjusts the RSI length dynamically based on a multiplier, helping traders better understand market sentiment at different time intervals.

Volume Weighting: When enabled, the RSI calculations are weighted by volume, allowing traders to give more importance to price movements with higher trading volume, which may provide more accurate signals.

Smoothing Feature: A customizable smoothing period is applied to the RSI to help filter out noise and make the signal smoother. This feature is particularly useful for traders who prefer to focus on long-term trends while minimizing false signals.

Step Size Customization: A "Step Size" input allows users to round the sentiment RSI to predefined intervals, making the results easier to interpret and act upon. This feature allows you to focus on significant sentiment changes and ignore minor fluctuations.

Crossover/Crossunder Alerts: The indicator includes crossover and crossunder signals on the zero-line, helping traders identify potential buy and sell opportunities as the smoothed RSI crosses these levels.

The indicator offers a clear visual display with multiple color-coded lines and areas:

Sentiment RSI: Plotted as an area chart, color-coded based on sentiment strength.

Raw RSI: A purple line representing the raw adjusted RSI.

Smoothed RSI: A dynamic line, color-coded aqua or orange based on its position relative to the zero line.

Buy/Sell Signals: Triangle shapes are plotted at crossovers and crossunders, providing clear entry and exit points.

🔶 Interpreting the Indicator

Sentiment RSI

-This line represents the sentiment-adjusted RSI, where the higher the value, the stronger the bullish sentiment, and the lower the value, the stronger the bearish sentiment. It is rounded to step intervals, making it easier to detect significant shifts in sentiment.

- A positive sentiment RSI (above 0) suggests bullish market conditions, while a negative sentiment RSI (below 0) suggests bearish conditions.

Smoothed RSI

The smoothed RSI helps reduce noise and shows the trend more clearly.

Crossovers of the zero line are significant:

- Crossover above zero: Indicates that bullish momentum is building, potentially signaling a buying opportunity.

- Crossunder below zero: Signals a shift towards bearish momentum, potentially indicating a sell signal.

Traders should look for these crossovers in conjunction with other signals for more accurate entry/exit points.

Raw RSI (Adjusted)

The raw adjusted RSI offers a less smoothed, more responsive version of the RSI. While it may be noisier, it provides early signals of market reversals and trends.

Crossover/Crossunder Signals

- When the smoothed RSI crosses above the zero line, a "Signal Up" triangle appears, indicating a potential buying opportunity.

- When the smoothed RSI crosses below the zero line, a "Signal Down" triangle appears, signaling a potential sell opportunity.

These signals help traders time their entries and exits by identifying momentum shifts.

Volume Weighting (Optional)

- If volume weighting is enabled, the RSI will give more weight to periods of higher trading volume, making the signals more reliable when the market is highly active.

Strong Up/Down Levels (40/-40)

- These dotted lines represent extreme sentiment levels. When the sentiment RSI reaches 40 or -40, the market may be nearing an overbought or oversold condition, respectively. This could be a signal for traders to prepare for potential reversals or shifts in momentum.

By combining the various components of this indicator, traders can gain a comprehensive view of market sentiment and price action, helping them make more informed trading decisions. The combination of sentiment factors, volume weighting, and smoothing makes this indicator highly flexible and suitable for a variety of trading strategies.

🔶 Disclaimer

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

Price vs 200 EMA IndicatorPurpose :

The Price vs. 200 MA (EMA) Indicator measures the deviation of the current price from its 200-period Exponential Moving Average (EMA). Instead of merely plotting the raw difference, the indicator calculates a standardized difference (similar to a z-score), which quantifies the deviation in terms of standard deviations over time. This helps traders understand how extreme the price is relative to its long-term average and its typical volatility.

Use Cases :

Trend Analysis:

Traders can use the standardized difference to assess how extreme the current price is relative to its long-term trend (200 EMA) while normalizing for volatility.

When the z-score approaches extreme levels (e.g., above 2 or below -2), it may indicate that the asset is overextended in either direction.

Mean Reversion Strategy:

Since the indicator identifies when the price deviates far from the 200 EMA (in terms of standard deviations), traders can use it to time mean-reversion trades, buying when the price is below -2 (oversold) and selling when it’s above +2 (overbought).

Trend Continuation or Exhaustion:

If the price continues to stay above +2 for extended periods, it could indicate a strong trend, whereas a reversion toward the EMA after reaching +2 or -2 could signal trend exhaustion or reversal.

Summary :

The Price vs. 200 MA (EMA) Indicator calculates the standardized difference (z-score) between the price and its 200-period EMA, giving traders a normalized measure of how far the price is from its long-term average, relative to typical price volatility. The color-coded plot provides a clear visual representation of potential overbought/oversold conditions and highlights when the price has deviated significantly from the 200 EMA in either direction.

Auto Anchored Swing VWAP'sThe Auto Anchored Swing VWAP's indicator automatically anchors Volume-Weighted Average Price (VWAP) lines to recent swing highs and swing lows. VWAPs often act as key support or resistance levels because they represent the average price at which the majority of trading volume has occurred over a given time.

What is VWAP? VWAP is an essential tool in trading, representing the average price of a security over a specific period, weighted by volume. It helps traders identify the average price at which most trades have been executed, providing a balanced view of price action over time.

Anchored VWAPs: Unlike traditional VWAPs, which start from the beginning of the day, anchored VWAPs allow traders to "anchor" the calculation to a specific point in time or a pivot on the chart, in this case a swing high and swing low. This version of VWAP follows the price action from a selected point forward.

When the price is above the VWAP, it indicates that the majority of traders have paid less for the asset, creating a potential support zone as buyers may step in at or near this level. On the other hand, when the price is below the VWAP, it suggests that most traders have paid a higher price, which can lead to a resistance level where sellers may appear to defend their positions.

Anchored VWAPs, in particular, provide more precise support and resistance levels by starting from a specific swing high, swing low, or other significant point on the chart. This allows traders to track how price interacts with these levels after a certain bar.

The selectable pivot lookback length in this indicator defines the number of bars to the left and right of a potential swing high or swing low that must be lower (for a swing high) or higher (for a swing low) in order to confirm the pivot. In other words, it controls how many surrounding bars need to validate a local price extreme before it is considered a true swing point.

For example, if the lookback length is set to 9, a swing high is identified when there are 9 bars to the left and 9 bars to the right that all have lower highs than the current bar. The same logic applies for swing lows, where the price must be lower than the highs of the bars to the left and right for it to be considered a swing low.

This parameter allows traders to control the sensitivity of the swing points used to anchor VWAPs. A smaller lookback value will identify more frequent and short-term swing highs and lows, making the VWAPs more responsive to recent price action. Conversely, a larger lookback value will result in fewer but more significant swing points.

Pine Script

Utilization of Pine Script’s Enum Feature: This indicator leverages Pine Script's new enum feature for the selection of the VWAP lines (solid, dashed, or dotted) style.

Nifty IT VolumeHello everyone,

Here I present Nifty IT index volumes calculated based on weighted volumes of all constituents.

A simple formula for calculation:

constituent1.volume*weightage + constituent2.volume*weightage + ....

You can change color and code if there is a change in constituents of the index from NSE. I will share other index volumes soon.

Enjoy!

TechniTrend: Strong Candles DetectorTechniTrend: Strong Candles Detector

Description:

The TechniTrend: Strong Candles Detector indicator is designed to identify strong candlestick patterns based on customizable thresholds of candle strength, volume, and price volatility. By detecting significant candles that have a high proportion of body relative to total range, the indicator helps traders identify potential shifts in market direction, making it a useful tool for trend analysis and reversal spotting.

Key Features:

Candle Strength Detection: The indicator calculates the strength of a candle based on the ratio of its body (difference between open and close) to its total range (high minus low). If the body size exceeds a user-defined threshold, the candle is flagged as strong. This helps traders quickly identify key candles that may signal market movements.

Volume Confirmation (Optional): An optional volume confirmation allows the indicator to only flag candles as "strong" if the trading volume during the candle exceeds the average volume over a customizable period. This can help validate that a candle’s movement is backed by significant market participation.

Volatility Body Confirmation (Optional): Users can further refine the detection by requiring that the body of a strong candle exceed the average body size (volatility) of previous candles. This ensures that candles with greater price movement are prioritized.

Customizable Inputs:

Strength Threshold: Defines the minimum ratio of body to total range for a candle to be considered strong.

Moving Average Type: Choose from SMA, EMA, or WMA for calculating the moving average of volume or body volatility.

Volume and Body Confirmation: Adjust the percentage thresholds for the difference between the current volume/body size and their average values.

Visual Alerts: The indicator marks strong bullish candles with green upward labels below the candle, and strong bearish candles with red downward labels above the candle. Additionally, strong candles can be highlighted with a customizable background color for easier visualization.

How It Works:

Strength Ratio:

The core of this indicator is the calculation of the strength ratio, which is defined as the body size (open-close) divided by the total range (high-low). If the body size is larger relative to the total range and exceeds the user-defined threshold, the candle is flagged as strong.

Volume and Volatility Confirmation:

For traders seeking additional confirmation, the indicator can be configured to only mark candles if the current volume or body volatility exceeds the average by a user-defined percentage. These confirmations can be toggled on or off to suit different trading strategies.

Customization Options:

Strength Threshold (0-1):

Sets the minimum strength required for a candle to be flagged. A higher value will result in fewer but more significant candles being marked.

Volume Confirmation:

Toggle on to require a higher volume compared to the average volume for a candle to be confirmed as strong.

Volatility Body Confirmation:

Toggle on to require a larger candle body compared to the average body size for further confirmation.

Candle Color:

Choose the background color used to highlight strong candles.

Recommended Settings:

Strength Threshold: 0.7 (for a good balance between body and range)

Volume Difference: 0.05 (5% above the average volume)

Body Volatility Difference: 0.05 (5% above the average body size)

Length: 14 (for volume and volatility moving averages)

Conclusion: The TechniTrend: Strong Candles Detector is an easy-to-use yet powerful tool for traders who want to identify key candles that signal potential market trends. Its customizable settings allow for fine-tuning to fit different trading styles, whether looking for high-volume breakouts or significant price movements. The indicator offers both a visual and configurable alert system to help traders make more informed decisions.

TechniTrend: Relative Volume IndexRelative Volume Index (RVI)

Short Description:

Relative Volume Index (RVI) with customizable volume bands, moving averages, and alerts for high and low volume thresholds. Includes options for displaying daily and weekly relative volume for enhanced analysis.

Full Description:

The Relative Volume Index is a powerful and versatile tool designed to help traders easily identify volume trends and anomalies in the market. By comparing the current volume to its moving average, this indicator highlights significant increases or decreases in relative volume, allowing traders to catch potential breakouts, breakdowns, or volume spikes early on.

Key Features:

Relative Volume Comparison : Compares the current volume to the moving average volume over a customizable period, highlighting overbought and oversold conditions.

Volume Alerts : Customizable alert thresholds for high and low relative volume to quickly notify traders when volume exceeds predefined limits.

Custom Moving Averages : Choose from various moving average types (SMA, EMA, WMA) to calculate the average volume over a given length.

Volume Normalization : For better readability, volumes greater than 1000 are divided by 1000 and displayed with a 'K' suffix (thousands).

Volume Bands : Configurable high, average, and low volume bands for visual reference.

Daily Relative Volume : Option to display the daily relative volume in comparison to its daily average.

Weekly Average Volume : Option to display the weekly average volume for broader market trends.

Customization Options:

Length : Customize the period for calculating the moving average.

Volume Moving Average : Toggle to show/hide the volume moving average (normalized in 'K').

Alerts : Set thresholds for high and low volume alerts and configure alerts for immediate notification.

Volume Bands : Toggle to show/hide volume bands for easy visual identification of volume zones.

Daily/Weekly Relative Volume : Optional display of relative volume data on a daily and weekly basis.

This indicator provides traders with a more intuitive view of market volume dynamics, making it easier to spot significant volume changes and take action accordingly.

Recommended Settings:

High Volume Alert Threshold: 2.0

Low Volume Alert Threshold: 0.5

Length for Moving Average Calculation: 14

Show Weekly Average Volume: On for broader trend insights

Use this indicator to stay ahead of market moves by monitoring volume trends with precision.

Alerts:

High Volume Alert : Get notified when relative volume exceeds your high threshold.

Low Volume Alert : Get notified when relative volume drops below your low threshold.

Thrax - Intraday Market Pressure ZonesTHRAX - INTRADAY MARKET PRESSURE ZONES

This indicator identifies potential support and resistance zones based on areas of significant market pressure. It dynamically plots these zones and adjusts their visibility based on real-time price action and user-defined thresholds. The indicator is useful for traders seeking to understand intraday market pressure, visualize zones of potential price reversals, and analyze volume imbalances at critical levels.

1. Support/Resistance Zones: Wherever the price retraces significantly from its high a support zone is drawn and when it retraces significantly from it low a resistance zone is drawn. The significant retracing is measured by the wick threshold percentage. For instance, if set to 75%, it implies price retracement of 75% either from high or from low for a particular candel

Volume delat: Displays volume delta information where the zones are formed. This can be used by trader to consider only those zones where delta is significant.

2. Breakout Detection: Monitors for price breakouts beyond established zones, deleting zones that are invalidated by price movement. when the price breaks a given zone with the threshold, it is considered to be mitigated and chances of trend continuation is decent.

Candle Coloring: Uses color codes (green, red, and yellow) to represent bullish, bearish, and indecisive (doji) candles, aiding quick visual assessment.

INPUTS

1. Wick Threshold (%) : Sets the minimum wick percentage required for a candle to be considered a support or resistance candidate.

2. Breakout Threshold (%) : Determines the percentage above or below a support or resistance zone that defines a breakout condition. if breaks a zone with the set threshold then the zone will be considered mititgated.

3. Max Number of Support/Resistance Zones : Limits the maximum number of support/resistance zones displayed on the chart, ranging from 1 to 5.

4. Show Wick Percentage Labels : Toggles the display of percentage values for upper and lower wicks on each candle.

TRADE SETUP

Identifying Entry Points: Look for the formation of support or resistance zones. Wait for price to retrace to these zones. if you are willing to take risk, you can consider even zones with low delta. If you want to be more cautious you should consider zones with high delta.

Volume Confirmation: Use the volume information to confirm the strength of the zone. Strong volume differences (displayed as labels) can indicate significant market pressure at these levels.

Breakout Trades: If price breaks through a support/resistance zone by more than the breakout threshold, consider this a signal for a potential trend continuation in the breakout direction.

Risk Management: Set stop-loss levels slightly outside of the identified zones to minimize risk in case of false breakouts. This can be set in input setting for breakout threshold.

Bonus Tip : Mark your significant highs and lows from where prices have retraced multiple times in the near past and if the zone is near these levels it can serve s a strong candidate of support or resistance

Therefore, in conclusion monitor the zones, based on delta and volume presence filter out the zone, wait for price retracement to the zone, intiate the trade with stop loss below zone with a set percentage.

MM Relative Volume (RVOL)What this script does:

This script shows you the "Relative Volume" (RVOL) value up to the current minute. RVOL is the volume from market open up to the current minute today, compared to the average of the same over the last n (30 by default) days.

How this script works:

There are a lot of indicators out there for RVOL, but they all take shortcuts that result in sub-par data. This indicator goes the distance to store data for every minute for the last n days for the current chart, then in sums the volume up to the current minute today along with the average of the same up-to-the-minute data from the prior n days to calculate the relative volume of the stock. It's super important to get this data up to the current minute, because most traders use this information primarily during the first 90 minutes of trading, and need to know if this value is going up or down.

How to use this script:

Relative volume can be used to gauge how "In Play" a stock is. If RVOL is less than 1 it is not "In Play" on this trading day and you might not want to trade it. If RVOL is above 2, it is "In Play" and you may want to trade it. When stocks are very "In Play", you can see an RVOL of 5 and above. The higher the RVOL the more "In Play" the stock is. You can also used RVOL for position sizing. If RVOL is <1 you may decide not to take a large position in the name. If RVOL is >3, this may give you more confidence to take a larger position as more reward and more liquidity should be present.

What makes this script original:

This particular implementation of RVOL has never been done before on TradingView to my knowledge. Most other indicators use a rolling average of the prior 30 days which is much easier to do, but this doesn't actually work properly because instead of getting large volume spikes from prior days filtered out correctly, it takes a LOT longer for those to even out as the rolling average eventually smooths down. Instead, with this indicator, any large/small volume days will truly drop off after the moving average length and the calculated average daily volume (ADV) will be accurate up to the minute. For more details on the original concept behind this indicator, check out the blog linked on my profile.

Price Action Volumetric Breaker Blocks [UAlgo]The Price Action Volumetric Breaker Blocks indicator is designed to identify and visualize significant price levels in the market. It combines concepts of price action, volume analysis, and market structure to provide traders with a comprehensive view of potential support and resistance areas. This indicator identifies "breaker blocks," which are price zones where the market has shown significant interest in the past.

These blocks are created based on swing highs and lows, and are further analyzed using volume data to determine their strength. The indicator also tracks market structure shifts, providing additional context to price movements.

By visualizing these key levels and market structure changes, traders can gain insights into potential areas of price reversal or continuation, helping them make more informed trading decisions.

🔶 Key Features

Dynamic Breaker Block Identification: The indicator automatically detects and draws breaker blocks based on swing highs and lows. These blocks represent areas of potential support and resistance.

Volume-Weighted Strength Analysis: Each breaker block is analyzed using volume data to determine its bullish and bearish strength. This is visually represented by the proportion of green (bullish) and red (bearish) coloring within each block.

Market Structure Break (MSB) and Break of Structure (BOS): The indicator identifies and labels Market Structure Breaks (MSB) and Break of Structure (BOS) events, providing context to larger market trends.

Customizable Settings:

- Adjustable swing length for identifying pivot points

- Option to show a specific number of recent breaker blocks

- Choice between wick or close price for violation checks

- Toggle to hide overlapping blocks for cleaner analysis

Violation Detection: Automatically detects when a breaker block has been violated (broken through), either by wick or close price, depending on user settings.

Overlap Control: Provides an option to hide overlapping order blocks, ensuring that the chart remains clean and easy to read when multiple blocks are detected in close proximity.

🔶 Interpreting Indicator

Breaker Blocks:

Breaker blocks are key areas where the price moves through and invalidates a previously identified order block. The indicator detects a breaker block when the price violates an order block by exceeding its high or low (depending on whether it's a bullish or bearish block). This violation is determined by either the wick or the close of a candle, depending on the user's selection in the "Violation Check" setting. When a breaker block is detected, the indicator removes the violated order block from the chart, signaling that the zone is no longer relevant for future price action.

Bullish Breaker Block: This occurs when a bearish order block (red) is violated by the price closing above the block’s top boundary or when the wick surpasses this level. It signals that a prior bearish structure has been invalidated, and the market may shift to a bullish trend.

Bearish Breaker Block: This occurs when a bullish order block (teal) is violated by the price closing below the block’s bottom boundary or when the wick drops below it. It suggests that a previous bullish structure has been broken, indicating potential bearish momentum.

Market Structure Labels:

"MSB" (Market Structure Break) labels indicate a potential change in trend direction.

"BOS" (Break of Structure) labels confirm the continuation of the current trend after breaking a significant level.

Block Strength:

A block with more green indicates stronger bullish interest.

A block with more red indicates stronger bearish interest.

The relative sizes of the green and red portions show the balance of power between buyers and sellers at that level.

🔶 Disclaimer

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

Liquidity Zones [BigBeluga]This indicator is designed to detect liquidity zones on the chart by identifying significant pivot highs and lows filtered by volume strength. It plots these zones as boxes, highlighting areas where liquidity is likely to accumulate. The indicator also draws lines extending from these boxes, marking the levels where price may "grab" this liquidity. The size of these boxes can be dynamic, adjusting based on the volume size, offering a visual representation of market areas where traders might expect significant price reactions.

🔵 IDEA

The idea behind the Liquidity Zones indicator is to help traders identify key market levels where liquidity accumulates. Liquidity zones are areas where there are enough buy or sell orders that can potentially lead to significant price movements. By focusing on pivot points filtered by volume strength, the indicator aims to provide a clearer picture of where large players may have positioned their orders. This insight allows traders to anticipate potential market reactions, such as reversals or breakouts, when the price reaches these zones. The option for dynamic box height further refines the visualization, showing the extent of liquidity based on the volume's intensity.

🔵 KEY FEATURES & USAGE

◉ Volume-Filtered Pivot Highs and Lows:

The indicator scans for pivot highs and lows on the chart, filtering these points based on the volume strength setting (Low, Mid, High). This ensures that only the most significant liquidity zones, backed by notable trading volume, are highlighted. Traders can adjust the filter to focus on different levels of market activity, from small fluctuations to major volume spikes.

Low:

Mid:

High:

◉ Dynamic and Static Liquidity Zones:

Liquidity zones are plotted as boxes around pivot points, with an optional dynamic mode that adjusts the box height based on the normalized volume. This dynamic adjustment reflects the liquidity carried by the volume, making it easier to gauge the significance of each zone. In static mode, the boxes have a fixed height, providing a consistent visual reference for the zones.

◉ Color Intensity Based on Volume:

The indicator adjusts the color intensity of the liquidity zones based on the volume strength. Higher volume zones will be displayed with more intense colors, giving a visual cue to the strength of the liquidity present in that area. This makes it easier to differentiate between zones of varying importance at a glance, allowing traders to quickly identify where the market has the highest concentration of liquidity.

◉ Liquidity Grab Detection and Red Circles:

When the price interacts with a liquidity zone, the indicator detects whether liquidity has been "grabbed" at these levels. If the price moves into a zone and crosses a level, the box label changes to "Liquidity Grabbed," and the line marking the level becomes dashed.

Reversal Points:

The beginning of a trend:

Additionally marks these "liquidity grabs" with red circles, indicating both recent and past liquidity grabs. This feature helps traders identify areas where liquidity has been absorbed by the market, which may signal potential reversals or shifts in market direction.

◉ Dashboard Display:

A dashboard in the upper right corner of the chart provides an overview of the indicator's settings and status. It shows the number of plotted zones, as set in the input settings, and whether the dynamic mode is active. This quick reference helps traders stay informed about the indicator's configuration without needing to open the settings panel.

🔵 CUSTOMIZATION

Length & Zones Amount: Set the length for pivot detection and the maximum number of zones to be displayed on the chart. This allows you to control how many liquidity zones you want to monitor at any given time.

Volume Strength Filter: Adjust the filter to Low, Mid, or High to control the strength of volume required for a pivot to be considered a significant liquidity zone. Higher settings focus on zones with greater volume, indicating stronger liquidity.

Dynamic Distance Mode: Enable or disable the dynamic mode, which adjusts the box height based on the volume size. When dynamic mode is off, the boxes have a fixed height based on the ATR, offering a consistent visualization regardless of the volume size.

The Liquidity Zones indicator is a versatile tool for identifying areas of significant market activity, offering a clear view of where liquidity is likely to reside. By filtering these zones through volume strength and providing dynamic or static visualization options, it equips traders with insights into potential market reaction points, enhancing their ability to anticipate and respond to market movements. The varying color intensity based on volume further aids in quickly recognizing the most critical liquidity zones on the chart.

China's stock market volume ratio1. Introduction to Volume Ratio:

In China's stock market, the volume ratio is an indicator used to measure relative trading volume. It compares the average volume per minute after the market opens to the average volume per minute over the past five trading days.

2. Application of Volume Ratio:

When there is a sudden surge in volume, the volume ratio chart will show a sharp upward break, indicating an increase in trading volume (initial market movements can be disregarded). Conversely, when volume contracts, the volume ratio will move downward.

If the volume ratio is greater than 1, it indicates that the average trading volume per minute for the current day is higher than the average over the past five days, signifying increased trading activity.

If the volume ratio is less than 1, it means that today's trading volume is lower than the average of the past five days, indicating decreased trading activity.

3. Volume Ratio Calculation:

The formula for calculating the volume ratio is:

Volume Ratio=Current Total Volume/(Average Volume per Minute over the Last 5 Days * Accumulated Market Open Time (in minutes))

Custom Buy BID StrategyThis Pine Script strategy is designed to identify and capitalize on upward trends in the market using the Average True Range (ATR) as a core component of the analysis. The script provides the following features:

Customizable ATR Calculation: Users can switch between different methods of ATR calculation (traditional or simple moving average).

Adjustable Parameters: The strategy allows for adjustable ATR periods, ATR multipliers, and custom time windows for executing trades.

Buy Signal Alerts: The strategy generates buy signals when the market shifts from a downtrend to an uptrend, based on ATR and price action.

Profit and Stop-Loss Management: Built-in take profit and stop-loss conditions are calculated as a percentage of the entry price, allowing for automatic position management.

Visual Enhancements: The script highlights the uptrend with green lines and optionally colors bars to help visualize market direction.

Flexible Timeframe: Users can configure a specific date range to activate the strategy, offering more control over when trades are executed.

This strategy is ideal for traders looking to automate their buy entries and manage risk with a straightforward trend-following approach. By utilizing customizable settings, it adapts to various market conditions and timeframes.

Advanced Volume-Driven Breakout SignalsThe "Advanced Volume-Driven Breakout Signals" indicator is a cutting-edge tool designed to help traders identify high-potential trading opportunities through sophisticated volume analysis techniques. This indicator integrates volume flow analysis, moving averages, and Relative Volume (RVOL) to provide a comprehensive view of market conditions, going beyond traditional Volume Spread Analysis (VSA) methods.

Key Features:

Volume Flow Analysis: Distinguishes bullish and bearish volume flows with distinct colors, making it easier to visualize market sentiment and potential breakout points.

Volume Flow Moving Averages: Calculates moving averages for volume using various methods (SMA, EMA, WMA, HMA, VWMA), accommodating different trading strategies. This includes settings for adjusting the type of moving average and its period, as well as thresholds for high, medium, and low volume levels.

Volume Spikes Detection: Identifies significant volume spikes based on user-defined multipliers and moving averages, highlighting unusual trading activity.

Volume MA Cloud Settings: Computes general moving averages of volume to track trends and detect deviations. This feature includes options to select different moving average types and adjust thresholds for detecting high volume activity.

Relative Volume (RVOL): Measures current volume relative to historical averages, triggering signals when RVOL exceeds predefined thresholds, indicating notable changes in trading activity.

Entry Conditions: Provides clear long and short entry signals based on combined volume flow conditions and RVOL, offering actionable trading opportunities.

Volume Visualization:

— Bullish Volume Flow: Light and dark green bars indicate bullish volume flow.

— Bearish Volume Flow: Light and dark red bars denote bearish volume flow.

— High Volume Bars: Highlighted in yellow, and extreme volume bars in orange for additional context. These bars are plotted for visual aid and do not directly influence trade signals, focusing instead on the quality and strength of the volume flow.

Alerts: Allows users to create alert notifications for long and short entry signals when the criteria are met, enabling traders to respond promptly to trading opportunities.

Usage:

Overlay: Apply the indicator directly to your price chart to visualise real-time signals and volume conditions.

Customisable: Adjust settings for moving averages, RVOL, and other parameters to match your trading strategy and preferences.

Comparison to VSA Scripts: The "Advanced Volume-Driven Breakout Signals" indicator extends beyond traditional VSA scripts by incorporating a wider range of analytical features. While VSA primarily focuses on volume spread patterns and price action, this indicator offers enhanced functionality with advanced RVOL metrics, customizable moving averages, and detailed volume spike detection, making it a more versatile tool for identifying breakout opportunities and managing trades. It is particularly effective when used alongside key levels and order blocks.

Acknowledgements: Special thanks to @oh92 and @goofoffgoose for their invaluable scripts, which served as inspiration in the development of this advanced trading indicator.

Notes: The script is continually evolving, with ongoing refinements aimed at enhancing accuracy and performance.

EMA Volume [MacroGlide]EMA Volume is a versatile tool designed to track and analyze market volumes by calculating the Exponential Moving Averages (EMAs) of total, bullish, and bearish volumes. This indicator helps traders visualize volume dynamics, identify buying and selling pressure, and make informed trading decisions based on volume activity.

Key Features:

• Volume EMAs: The indicator calculates the EMAs of total, bullish, and bearish volumes, allowing users to observe how volume trends evolve over time. This helps identify shifts in market sentiment and potential reversals.

• Separation of Bullish and Bearish Volumes: By separating bullish and bearish volumes, the indicator provides a clear view of buying versus selling activity. This distinction is valuable for understanding the market's underlying momentum and direction.

• Customizable Visuals: Users can customize the line style and color for each volume type, allowing them to tailor the display of the indicator to their personal preferences and enhance the visual interpretation of the data.

How to Use:

• Add the indicator to your chart and adjust the EMA settings and display parameters according to your needs.

• Use the difference between bullish and bearish volumes to assess current market sentiment and analyze potential trend changes.

• Monitor the EMA of total volume to identify overall volume trends that can serve as additional signals for entering or exiting positions.

Methodology:

The indicator calculates the EMAs for total, bullish, and bearish volumes based on the trading volumes associated with price increases or decreases. This tool helps evaluate the strength of buying and selling at different times, making it especially useful for volume and market dynamics analysis.

Originality and Usefulness:

EMA Volume stands out for its ability to separate buying and selling volumes and present them in a clear visual format, significantly simplifying the analysis of market activity and decision-making in trading.

Charts:

The indicator displays clean and clear charts, where each type of volume is represented by its own line and color, making visual interpretation easier. The charts focus solely on key information for analysis: EMAs of total, bullish, and bearish volumes. These features make the charts highly useful for quick analysis and trading decision-making.

Enjoy the game!

Volume PACustom volume histogram that visually represents trading volume in relation to the price action of the current bar. The histogram is colored based on whether the current bar is bullish or bearish, and it greys out when the current volume is lower than the volumes of the previous specified number of bars.

Customizable Bar Count: Users can specify how many previous bars to compare against for determining if the current volume is lower.

Default color-coded histogram:

Green: Indicates a bullish bar (closing price is greater than opening price).

Red: Indicates a bearish bar (closing price is less than opening price).

Grey: Indicates that the current volume is lower than the volumes of the previous specified number of bars.