Volume Zones IndicatorVolume Zones Indicator — VWAP with Dynamic Monthly Volume Zones

This indicator is an enhanced version of the classic VWAP (Volume Weighted Average Price), designed to create clear monthly zones around VWAP based on average price range (ATR) and volume activity.

The core idea is to highlight key zones where price is more likely to reverse or consolidate, based on where significant trading volume occurs.

How does it work?

VWAP is calculated over the last N days (set by the lookbackPeriod input).

Four zones are plotted above and below VWAP, spaced using a multiple of ATR.

Each zone has its own color for clarity:

Blue — closest to VWAP

Red — second band

Green — third band

Orange — outer band (potential breakout or exhaustion zone)

If the current volume exceeds the moving average of volume, it is highlighted directly on the chart. This helps detect accumulation or distribution moments more easily.

What does the trader see?

You see horizontal colored bands on the chart that update at the start of each new month. These zones:

Remain fixed throughout the month

Automatically adjust based on recent volume and volatility

Act as dynamic support/resistance levels

Best used for:

Mean reversion strategies — identifying pullbacks toward value areas

Support and resistance mapping — automatic SR zones based on price/volume behavior

Breakout filtering — when price reaches zone 3 or 4, trend continuation or reversal is likely

Adding volume context to price action — works well with candlestick and pattern analysis

Settings

Lookback Period (Days): VWAP and volume smoothing length

Volume Area Threshold %: Reserved for future functionality

Works on any timeframe; best suited for 4H timeframe.

Zones are calculated and fixed monthly for clean visual context

Combines price structure with actual volume flow for more reliable decision-making

Volume Weighted Average Price (VWAP)

SHA Multi Pivot Points -v1.0.0🔎Using Pivot Points in Trading

Traders use PPs to help determine predefined support and resistance levels to guide their trading strategies. In addition, traders identify potential price reversals, trend direction, and breakout opportunities:

Trend identification: PPs act as a reference level to gauge market sentiment. If the price opens above the PP and remains above it, traders interpret this as an uptrend. Conversely, if the price opens below the pivot point and stays below, it suggests a downtrend.

Support and resistance determination: Pivot levels are natural barriers where price reactions frequently occur. Traders may enter long positions near support levels, expecting a price bounce, or if the price approaches resistance levels, traders may consider shorting the asset.

Breakout trading: When the price breaks above resistance or support, it may indicate strong momentum for further movement.

Reversal identification: Traders also look for failed breakouts or price rejections at pivot levels to anticipate reversals.

Trading strategy combinations: Traders can improve accuracy by combining PPs with other technical analysis indicators.

1. Camarilla Pivot Points

📌 Overview:

Developed by Nick Scott in 1989, Camarilla Pivot Points are designed for short-term, intraday trading. Unlike traditional pivots, Camarilla levels are tighter and more responsive, making them useful in volatile markets.

📐 Key Levels:

It generates eight levels:

- Resistance: Initial Level (R1), Mid-range Level (R2), Sell Reversal Level (R3), Breakout Level (R4)

- Support: Initial Level (S1), Mid-range Level (S2), Buy Reversal Level (S3), Breakout Level (S4)

✅ How to Use:

- S1/R1 + RSI or volume divergence to confirm weak momentum and early reversals.

- S2/R2 with price action patterns to enter early on major moves before L3/H3 get tested.

- S3/R3: Mean-reversion zones → price often reverses.

- Break of S4/R4: Strong breakout → trend-following signal.

- Combine with volume or candlestick confirmation for entries.

🔹 2. Floor (Standard) Pivot Points

📌 Overview:

This is the most traditional pivot method, widely used by floor traders. It’s symmetrical and provides a clear central pivot point with equally spaced support and resistance levels.

📐 Key Levels:

- Povit Points : Average price (PPs)

- Resistance : First price ceiling (R1), Stronger ceiling (R2), Extreme resistance (R3)

- Support : First price floor (S1), Stronger floor (S2), Extreme support (S3)

✅ How to Use:

- Above PPs = bullish bias; Below PPs = bearish bias.

- S1/R1 are most used for intraday targets.

- S2–S3/R2–R3 indicate potential extreme moves.

- Often used in combination with momentum indicators.

🔹 3. Woodie Pivot Points

📌 Overview:

Woodie’s pivot formula gives double weight to the closing price, emphasizing the most recent session's sentiment.

📐 Key Levels:

- Povit Points : Weighted average (PPs)

- Resistance : First price ceiling (R1), Stronger resistance (R2)

- Support : First price floor (S1), Stronger support (S2)

✅ How to Use:

- Works best in fast-moving markets.

- PPs acts as a momentum-based balance level.

- Good for scalpers and momentum traders.

🔹 4. Fusion Pivot Points

📌 Overview:

This method differs significantly — it calculates only one support and one resistance level, adjusting based on the relationship between the open and close.

📐 Key Levels:

- Povit Points : Single directional (PPs)

- Resistance : Potential ceiling (R)

- Support : Potential floor (S)

✅ How to Use:

- Not symmetrical → more responsive to price behavior.

- Best for breakout or reversal strategies.

- Use when you're expecting directional momentum.

🔹 5. Classic Pivot Points (Traditional)

📌 Overview:

Also known as Standard or Traditional Pivot Points, this is the default method used by most charting platforms. It offers a balanced and simple framework.

📐 Key Levels:

- Povit Points : Central price level (PPs)

- Resistance : First ceiling (R1), Stronger resistance (R2), Extreme resistance (R3)

- Support : First floor (S1), Stronger floor (S2), Extreme support (S3)

✅ How to Use:

- PPs is the market’s equilibrium point.

- Helps define market structure, bias, and trade zones.

- Combine with order blocks, RSI, or MACD for confirmation.

📊 Summary Comparison :

1. Camarilla Pivot Points

- Focus : Mean Reversion & Breakouts

- Best Use : Scalping, Day Trading

2. Floor Pivot Points

- Focus : General Support/Resistance

- Best Use : Intraday, Swing

3. Woodie Pivot Points

- Focus : Recent Close Emphasis

- Best Use : Momentum Trading

4. Fusion Pivot Points

- Focus : Trend/Breakout

- Best Use : Directional Breakouts

5. Classic Povit Points

- Focus : Market Structure

- Best Use : General Use

⚠️ Disclaimer

The information and tools provided in this script are for educational and informational purposes only. They do not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instrument.

Trading in the financial markets involves risk of loss and is not suitable for every investor. You are solely responsible for your trading decisions. Always do your own research, use proper risk management, and consult a licensed financial advisor before making any financial decisions.

Mark4ex vWapMark4ex VWAP is a precision session-anchored Volume Weighted Average Price (VWAP) indicator crafted for intraday traders who want clean, reliable VWAP levels that reset daily to match a specific market session.

Unlike the built-in continuous VWAP, this version anchors each day to your chosen session start and end time, most commonly aligned with the New York Stock Exchange Open (9:30 AM EST) through the market close (4:00 PM EST). This ensures your VWAP reflects only intraday price action within your active trading window — filtering out irrelevant overnight moves and providing clearer mean-reversion signals.

Key Features:

Fully configurable session start & end times — adapt it for NY session or any other market.

Anchored VWAP resets daily for true session-based levels.

Built for the New York Open Range Breakout strategy: see how price interacts with VWAP during the volatile first 30–60 minutes of the US market.

Plots a clean, dynamic line that updates tick-by-tick during the session and disappears outside trading hours.

Designed to help you spot real-time support/resistance, intraday fair value zones, and liquidity magnets used by institutional traders.

How to Use — NY Open Range Breakout:

During the first hour of the New York session, institutional traders often define an “Opening Range” — the high and low formed shortly after the bell. The VWAP in this zone acts as a dynamic pivot point:

When price is above the session VWAP, bulls are in control — the level acts as a support floor for pullbacks.

When price is below the session VWAP, bears dominate — the level acts as resistance against bounces.

Breakouts from the opening range often test the VWAP for confirmation or rejection.

Traders use this to time entries for breakouts, retests, or mean-reversion scalps with greater confidence.

⚙️ Recommended Settings:

Default: 9:30 AM to 4:00 PM New York time — standard US equities session.

Adjust hours/minutes to match your target market’s open and close.

👤 Who is it for?

Scalpers, day traders, prop traders, and anyone trading the NY Open, indices like the S&P 500, or highly liquid stocks during US cash hours.

🚀 Why use Mark4ex VWAP?

Because a properly anchored VWAP is a trader’s real-time institutional fair value, giving you better context than static moving averages. It adapts live to volume shifts and helps you follow smart money footprints.

This indicator will reconfigure every day, anchored to the New York Open, it will also leave historical NY Open VWAP for study purpose.

Volume Weighted Average Price Dynamic Slope [sgbpulse]VWAP Dynamic Slope: A Comprehensive Indicator for Trend Identification and Smart Trading

Introducing VWAP Dynamic Slope, an innovative TradingView indicator that harnesses the power of Volume Weighted Average Price (VWAP) and enhances it with immediate visual feedback. The indicator colors the VWAP line based on its slope, allowing you to quickly and easily identify the direction and strength of the current trend for the asset, providing advanced tools for in-depth analysis.

What is VWAP and Why is it so Important?

VWAP (Volume Weighted Average Price) is an indicator that represents the average price at which an asset has traded, weighted by the volume traded at each price level. Unlike a simple moving average, VWAP gives greater weight to trades executed with high volume, making it a reliable measure of the asset's "true" or "fair" price within a given period. Many institutional traders use VWAP as a central reference point for evaluating the effectiveness of entries and exits. An asset trading above its VWAP is considered to have bullish momentum, and below it – bearish momentum.

How it Works: Dynamic VWAP Slope Analysis

VWAP Dynamic Slope analyzes the inclination of the VWAP line and displays it using an intuitive color scheme:

Positive Slope (Uptrend): When the VWAP points upwards, signaling positive momentum, the default color will be green.

Negative Slope (Downtrend): When the VWAP points downwards, signaling negative momentum, the default color will be orange.

Trend Change (CHG): When a change in the VWAP's trend direction occurs, a "CHG" label will be displayed. The label's color will be green if the change is to an uptrend, and orange if the change is to a downtrend.

Identifying Steep Slopes for Increased Momentum:

The indicator's uniqueness lies in its ability to identify "steep" slopes – rapid and particularly strong changes in the VWAP's direction. This indicates exceptionally strong momentum:

Steep Positive Slope: The VWAP color will change to dark green, indicating significant buying pressure.

Steep Negative Slope: The VWAP color will change to dark red, indicating significant selling pressure.

Dynamic Momentum Strength Label: In situations of steep slope (positive or negative), a dynamic label will be displayed with the change value of the VWAP at that point. This label allows you to monitor momentum strength, intensification, or weakening in real-time.

Advanced Analytical Tools for Complete Control

VWAP Dynamic Slope provides you with unprecedented flexibility through a variety of customizable tools:

Multiple VWAP Anchors and Visual Marking:

Common Time Anchors: Choose whether the VWAP resets at the beginning of each Session (daily), Week, Month, Quarter, Year, Decade, or Century.

Advanced Intraday Anchors: Within the Session, you can choose to calculate VWAP specifically for Pre-Market, Regular Hours, and Post-Market hours. This option is particularly crucial for intraday traders.

Important Event Anchors: The indicator allows for VWAP resets at significant milestones such as Earnings, Dividends, and Splits, for analyzing the market's immediate reaction.

Visual Anchor Marking: To enhance clarity and orientation, a Label ⚓ can be displayed at each selected anchor point, helping to immediately identify the start point of the VWAP calculation in the chosen context.

Customizable Bands (Up to Three on Each Side):

Add up to three Bands above and below the VWAP to identify areas of deviation and excursion from the average price. You have two calculation options:

Standard Deviation: Based on volatility and statistical distance from the VWAP.

Percentage: Defines fixed percentage-based bands from the VWAP.

Key Pre-Market Levels (Pre-Market High/Low):

Display the Pre-Market High and Low levels as separate lines on the chart. These lines often serve as important psychological support and resistance zones, allowing you to see how the VWAP behaves near them.

Full Customization and Precise Control:

VWAP Source Selection: Determine which price data type will be used for the VWAP calculation. The default is HLC3 (average of High, Low, and Close), but any other relevant data source available in TradingView can be selected.

Offset: Set an offset for the VWAP line, allowing you to shift it left or right on the time axis by a chosen number of bars.

Customizable Colors: Choose your preferred colors for each slope state, Pre-Market High/Low lines, and Bands.

Setting the "Steepness" Threshold (Per-mille Price Change Per Minute ‱/min with Auto-Adjustment): Determine the sensitivity for identifying a steep slope by setting the required change threshold in VWAP in terms of per-mille price change per minute (‱/min). The indicator performs smart adjustment for any timeframe you select on the chart (e.g., 30 seconds, 1 minute, 5 minutes, 10 minutes, etc.), ensuring that the "steepness" setting maintains consistency and relevance.

Examples for Setting the Steepness Threshold:

Suppose you set the steepness threshold to 0.3‱/min (per-mille price change per minute).

On a 30-second chart: The indicator will check if the VWAP changed by 0.15 ‱/min (half of the per-minute threshold) within a single bar. If so, the slope will be considered steep. Explanation: Since 30 seconds is half a minute, the indicator looks for a change that is half of the threshold set for a full minute.

On a 1-minute chart: The indicator will check if the VWAP changed by 0.3 ‱/min (the full per-minute threshold) within a single bar. If so, the slope will be considered steep. Explanation: Here, the bar represents a full minute, so we check the full threshold.

On a 5-minute chart: The indicator will check if the VWAP changed by 1.5 ‱/min (5 times the per-minute threshold) within a single bar. If so, the slope will be considered steep. Explanation: A 5-minute bar contains 5 minutes, so the cumulative change in VWAP needs to be 5 times greater to be considered "steep" on the same scale.

In summary, this setting allows you to precisely and uniformly control the sensitivity of steep slope detection across all timeframes, providing immense flexibility in analyzing the asset's momentum.

Advantages of Using Per-mille Price Change Per Minute (‱/min)

Using per-mille price change per minute (‱/min) offers several key advantages for your indicator:

Normalized and Objective Measurement: It provides a uniform scale for the VWAP's rate of change, regardless of the asset's price or nominal value. A 0.1 per-mille change per minute always carries the same relative significance.

Comparison Across Different Asset Prices: Using per-mille allows for direct comparison of VWAP movement strength between assets trading at very different prices (e.g., a $100 asset versus a $1 asset), enabling an understanding of true momentum without bias from the nominal price.

Smart Timeframe Agnostic Adjustment: This is a critical capability. The indicator automatically adjusts the per-mille per minute threshold you set to any chart timeframe (30 seconds, 1 minute, 5 minutes, etc.), maintaining consistency in "steepness" detection without manual recalibration.

Precise Momentum Identification: This measurement precisely identifies when the VWAP's rate of change becomes significant, and when momentum strengthens or weakens, contributing to more informed trading decisions.

In short, per-mille change per minute (‱/min) provides accuracy, consistency, and flexibility in identifying VWAP momentum changes, with smart adaptation across all timeframes.

Who is this Indicator For?

VWAP Dynamic Slope is a powerful tool for:

Intraday Traders: For quick identification of intraday trend directions and momentum across any timeframe, with specific consideration for Pre-Market, Regular Hours, or Post-Market VWAP, and incorporating key pre-market levels.

Swing Traders and Long-Term Investors: For analyzing longer-term trends based on periodic and event-driven VWAP anchors.

Beginner Traders: As an excellent visual aid for understanding the relationship between price, volume, and trend direction, and how different anchor points, pre-market levels, and data sources influence price behavior.

Experienced Traders: For integration with existing strategies, gaining additional confirmation for trend strength identification, and highly precise and flexible parameter calibration.

VWAP Dynamic Slope provides a rich, multi-dimensional layer of information about the VWAP, helping you make more informed trading decisions in real-time, within the context of your chosen asset.

A+ Trade CheckList with Comprehensive Relative StrengthThe indicator designed for traders who need real-time market assessment across multiple timeframes and benchmarks. This comprehensive tool combines traditional technical analysis with sophisticated relative strength measurements to provide a complete market picture in one convenient table display.

The indicator tracks essential trading levels including:

QQQ and SPY trend analysis using exponential moving averages

Previous day and week high/low levels for key support and resistance

Market open levels from the first 5 and 15 minutes of trading (9:30 AM ET)

VWAP positioning for institutional price reference

Short-term EMA positioning for momentum assessment

Advanced Relative Strength Analysis

The standout feature of this indicator is its comprehensive 8-metric relative strength scoring system that compares your current ticker against both QQQ (Nasdaq-100) and SPY (S&P 500) benchmarks.

The 4-Metric Relative Strength System Explained

Metric 1: Relative Strength Ratio (RSR)

Purpose: Measures whether your ticker is outperforming or underperforming relative to its historical relationship with the benchmarks.

How it works:

Calculates the ratio of your ticker's price to QQQ/SPY prices

Compares current ratio to a 20-period moving average of the ratio

Scores +1 if ratio is above average (relative strength), -1 if below (relative weakness)

Trading significance: Identifies when a stock is breaking out of its normal correlation pattern with major indices.

Metric 2: Percentage-Based Relative Performance

Purpose: Compares short-term percentage changes to identify immediate relative momentum.

How it works:

Calculates 5-day percentage change for your ticker and benchmarks

Subtracts benchmark performance from ticker performance

Scores +1 if outperforming by >1%, -1 if underperforming by >1%, 0 for neutral

Trading significance: Captures recent momentum shifts and identifies stocks moving independently of market direction.

Metric 3: Beta-Adjusted Relative Strength (Alpha)

Purpose: Measures risk-adjusted performance by accounting for the ticker's natural volatility relationship with benchmarks.

How it works:

Calculates rolling beta (correlation and variance relationship)

Determines expected returns based on benchmark moves and beta

Measures alpha (excess returns above/below expectations)

Scores based on whether alpha is consistently positive or negative

Trading significance: Identifies stocks generating returns beyond what their risk profile would suggest, indicating fundamental strength or weakness.

Metric 4: Volume-Weighted Relative Strength

Purpose: Incorporates volume analysis to validate price-based relative strength signals.

How it works:

Compares VWAP-based percentage changes between ticker and benchmarks

Applies volume weighting factor based on relative volume strength

Enhances score when high relative volume confirms price movements

Trading significance: Distinguishes between genuine institutional-driven moves and low-volume price action that may not sustain.

Combined Scoring System

The indicator generates 8 individual scores (4 metrics × 2 benchmarks) that combine into a single strength assessment:

Score Interpretation

Strong (4-8 points): Ticker significantly outperforming both benchmarks across multiple methodologies

Moderate Strong (1-3 points): Ticker showing good relative strength with some mixed signals

Neutral (0 points): Balanced performance relative to benchmarks

Moderate Weak (-1 to -3 points): Ticker showing relative weakness with some mixed signals

Weak (-4 to -8 points): Ticker significantly underperforming both benchmarks

Display Format

The indicator shows results as: "Strong (6/8)" indicating the ticker scored 6 out of 8 possible points.

Rolling VWAP Channel [LuxAlgo]The Rolling VWAP Channel indicator creates a channel by analyzing a large number of Volume Weighted Average Prices (VWAPs) and determining a Channel based on percentile linear interpolation throughout the VWAPs.

🔶 USAGE

In this indicator, we have formed a Channel by first calculating multiple VWAPs, each with their respective anchor, then locating prices using "Percentile Linear Interpolation".

Note: Percentile Linear Interpolation locates the price point at which a specified percentage of VWAPs fall below it.

For example, a percentile of 50% would mean that 50% of the VWAP values fall below this price.

This method of analysis is important since the VWAPs are not often evenly distributed; therefore, we are able to draw importance to different levels by analyzing in percentiles.

When visualized, there is typically clustering of the VWAP values, which occurs at any given time, as seen below.

The channel can be tailored to each individual, with full control of each percentile represented in the channel. That being said, a general concept is that these clustered areas are clear results of sideways price action, which would lead us to believe that after interactions at these levels, we should expect to see a directional decision made by the market closely after.

🔶 DETAILS

The Rolling VWAP calculation calculates a user-specified number of VWAPs (up to 500), each anchored to a unique starting point in the chart based on the start of a new timeframe.

Each new timeframe that occurs causes a new VWAP to initialize. When the total number of desired VWAPs is reached, the oldest VWAP is removed and re-initialized, anchored to the current bar. Hence, the name " Rolling " VWAPs

This method allows us to automatically generate and manage large amounts of VWAPs without the need for user interaction.

After we have generated these VWAPs, we are able to run analyses on their returned values, such as the "Percentile Linear Interpolation" mentioned in the section above.

🔶 SETTINGS

Anchor Period: Choose which time period to use as the anchor point to initialize new VWAPs from.

VWAP Source: Choose the source for your VWAPs to calculate.

VWAP Amount: Sets the number of VWAPs to use. After this amount is on the chart, the oldest will be rolled.

🔹 Channel Lines

Toggle: Enable the associated VWAP Channel percentile line.

Percentile: Adjust each line's percentile independently for your needs.

Width: Adjust the width of the associated percentile line.

🔹 Calculation

Calculated Bars: Tells the indicator how many bars to calculate on, for faster calculations with less history, use a lower value. Setting this to 0 will remove the bar constraint.

VWAP %BVWAP %B - Volume Weighted Average Price Percent B

The VWAP %B indicator combines the reliability of VWAP (Volume Weighted Average Price) with the analytical power of %B oscillators, similar to Bollinger Bands %B but using volume-weighted statistics.

## How It Works

This indicator calculates where the current price sits relative to VWAP-based standard deviation bands, expressed as a percentage from 0 to 1:

• **VWAP Calculation**: Uses volume-weighted average price as the center line

• **Standard Deviation Bands**: Creates upper and lower bands using standard deviation around VWAP

• **%B Formula**: %B = (Price - Lower Band) / (Upper Band - Lower Band)

## Key Levels & Interpretation

• **Above 1.0**: Price is trading above the upper VWAP band (strong bullish momentum)

• **0.8 - 1.0**: Overbought territory, potential resistance

• **0.5**: Price exactly at VWAP (equilibrium)

• **0.2 - 0.0**: Oversold territory, potential support

• **Below 0.0**: Price is trading below the lower VWAP band (strong bearish momentum)

## Trading Applications

**Trend Following**: During strong trends, breaks above 1.0 or below 0.0 often signal continuation rather than reversal.

**Mean Reversion**: In ranging markets, extreme readings (>0.8 or <0.2) may indicate potential reversal points.

**Volume Context**: Unlike traditional %B, this incorporates volume weighting, making it more reliable during high-volume periods.

## Parameters

• **Length (20)**: Period for standard deviation calculation

• **Standard Deviation Multiplier (2.0)**: Controls band width

• **Source (close)**: Price input for calculations

## Visual Features

• Reference lines at key levels (0, 0.2, 0.5, 0.8, 1.0)

• Background highlighting for extreme breaks

• Real-time values table

• Clean oscillator format below price chart

Perfect for intraday traders and swing traders who want to combine volume analysis with momentum oscillators.

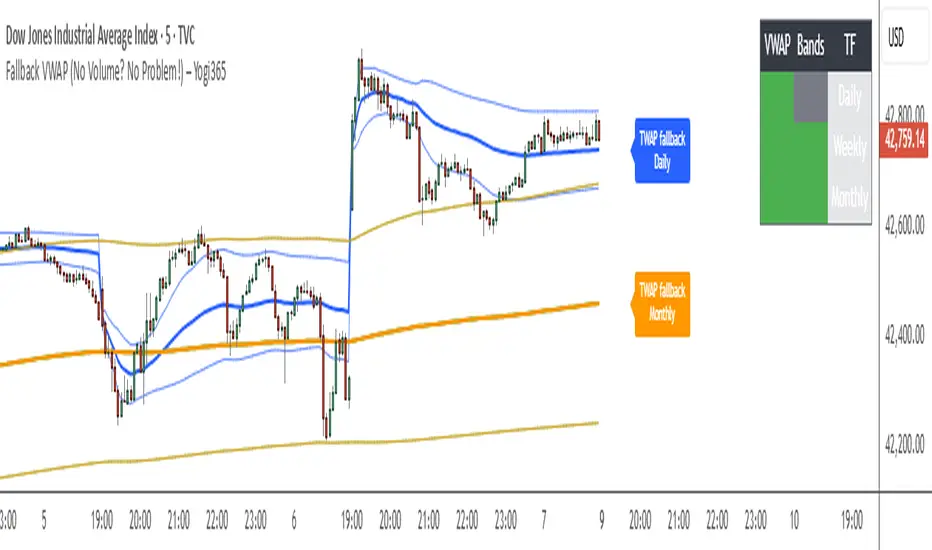

Fallback VWAP (No Volume? No Problem!) – Yogi365Fallback VWAP (No Volume? No Problem!) – Yogi365

This script plots Daily, Weekly, and Monthly VWAPs with ±1 Standard Deviation bands. When volume data is missing or zero (common in indices or illiquid assets), it automatically falls back to a TWAP-style calculation, ensuring that your VWAP levels always remain visible and accurate.

Features:

Daily, Weekly, and Monthly VWAPs with ±1 Std Dev bands.

Auto-detection of missing volume and seamless fallback.

Clean, color-coded trend table showing price vs VWAP/bands.

Uses hlc3 for VWAP source.

Labels indicate when fallback is used.

Best Used On:

Any asset or index where volume is unavailable.

Intraday and swing trading.

Works on all timeframes but optimized for overlay use.

How it Works:

If volume == 0, the script uses a constant fallback volume (1), turning the VWAP into a TWAP (Time-Weighted Average Price) — still useful for intraday or index-based analysis.

This ensures consistent plotting on instruments like indices (e.g., NIFTY, SENSEX,DJI etc.) which might not provide volume on TradingView.

David_FairPriceCandlestick_calculatedDescription:

This indicator displays the "Typical Price" for each candle as a visual marker (cross) directly on the chart. The Typical Price is calculated as the average of the High, Low, and Close values of each bar:

(High + Low + Close) / 3

The marker provides a quick visual reference to the fair or average price level within every single candle.

Unlike a Point of Control (POC) or volume-based indicators, this script works purely with price data and is independent of volume or order flow.

Use cases:

Identify where most trading activity may have been concentrated within the candle (for price-based strategies)

Support as a reference line for mean-reversion or fair value concepts

Works on all timeframes and instruments

Customization:

You can easily change the marker style (cross, dot, triangle, etc.) and color within the script.

Neural Adaptive VWAPNeural Adaptive VWAP with ML Features is an advanced trading indicator that enhances traditional Volume Weighted Average Price (VWAP) calculations through machine learning-inspired adaptive algorithms and predictive volume modeling.

🌟 Key Features:

🧠 Machine Learning-Inspired Adaptation

Dynamic weight adjustment system that learns from prediction errors

Multi-feature volume prediction using time-of-day patterns, price momentum, and volatility

Adaptive learning mechanism that improves accuracy over time

📊 Enhanced VWAP Calculation

Combines actual and predicted volume for forward-looking VWAP computation

Session-based reset with proper daily anchoring

Confidence bands based on rolling standard deviation for dynamic support/resistance

🎯 Advanced Signal Generation

Volume-confirmed crossover signals to reduce false entries

Color-coded candle visualization based on VWAP position

Multi-level strength indicators (strong/weak bullish/bearish zones)

⚙️ Intelligent Feature Engineering

Normalized volume analysis with statistical z-score

Time-series pattern recognition for intraday volume cycles

Price momentum and volatility integration

Sigmoid activation functions for realistic predictions

📈 How It Works:

The indicator employs a sophisticated feature engineering approach that extracts meaningful patterns from:

Volume Patterns: Normalized volume analysis and historical comparisons

Temporal Features: Time-of-day and minute-based cyclical patterns

Market Dynamics: Price momentum, volatility, and rate of change

Adaptive Learning: Error-based weight adjustment similar to neural network training

Unlike static VWAP indicators, this system continuously adapts its calculation methodology based on real-time market feedback, making it more responsive to changing market conditions while maintaining the reliability of traditional VWAP analysis.

🔧 Customizable Parameters:

VWAP Length (1-200 bars)

Volume Pattern Lookback (5-50 periods)

Learning Rate (0.001-0.1) for adaptation speed

Prediction Horizon (1-10 bars ahead)

Adaptation Period for weight updates

📊 Visual Elements:

Blue Line: Adaptive VWAP with predictive elements

Red/Green Bands: Dynamic confidence zones

Colored Candles: Position-based strength visualization

Signal Arrows: Volume-confirmed entry points

Info Table: Real-time performance metrics and weight distribution

🎯 Best Use Cases:

Intraday Trading: Enhanced execution timing with volume prediction

Institutional-Style Execution: Improved VWAP-based order placement

Trend Following: Adaptive trend identification with confidence zones

Support/Resistance Trading: Dynamic levels that adjust to market conditions

2-Day Volume Weighted Average Price (VWAP)This indicator extends TradingView’s built-in VWAP by calculating a volume-weighted average price over a continuous two-day window (yesterday + today), anchoring VWAP at the start of yesterday’s session and carrying it through to today’s close, but only plotting the segment that falls within the current trading session—yesterday’s data feeds into the calculation to ensure today’s VWAP reflects the prior session’s volume and price action, while the line drawn on your chart always begins at today’s session open.

Standard Deviation Bands: Optional ±1σ, ±2σ, and ±3σ envelopes, exactly as in the default VWAP, but based on the rolling two-day data.

Leslie's EMA Ribbon: 5/9/21 + VWAPEMA + VWAP Crossover Indicator with Alerts

This script blends three Exponential Moving Averages (5, 9, 21) with VWAP to identify momentum shifts and volume-confirmed trend signals. It’s optimized for the Daily timeframe, but also adaptable to shorter-term trading.

🔍 Why this combination?

EMAs provide fast and reliable trend signals:

- 5/9 EMA crossover → short-term shifts (more frequent)

- 9/21 EMA crossover → swing confirmation (less noise)

- VWAP adds volume context used by institutions for fair value tracking.

- 9EMA crossing VWAP confirms price action supported by volume.

Together, these tools offer a multi-layered view of market momentum — combining speed, confirmation, and conviction.

⚙️ Features:

Clean plots with dynamic labels on latest bar

Adjustable line weights for clarity

Alerts included for all crossovers:

- 5EMA / 9EMA

- 9EMA / 21EMA

- 9EMA / VWAP

✅ How to Use:

- Best on the Daily timeframe

- Use 5/9 as early signals, 9/21 for trend filtering, and 9/VWAP for volume-backed setups

- Turn on alerts to stay informed of key shifts without staring at charts

Adjustable Quad VWAPOverview

A powerful multi-timeframe VWAP indicator that displays four customizable rolling VWAPs with advanced features for comprehensive trend analysis and signal generation.

Key Features

🔧 Four Adjustable VWAPs

Fast VWAP: Default 7 days (1-365 adjustable)

Slow VWAP: Default 30 days (1-365 adjustable)

Medium VWAP: Default 90 days (1-365 adjustable)

Long VWAP: Default 365 days (1-365 adjustable)

VWAP Adaptive (RelVol-Adjusted)This indicator provides an Adaptive VWAP that adjusts volume weighting using RelVol (Relative Volume at Time), offering a more accurate and context-aware price reference during sessions with irregular volume behavior.

Classic VWAP calculates the average price weighted by raw volume, without considering the time of day. This becomes a serious limitation during major market events such as CPI releases, FOMC announcements, NFP, or large-cap earnings. These events often trigger massive volume spikes within one or two candles. As a result, the classic VWAP gets pulled toward those extreme prices and becomes permanently skewed for the rest of the session.

In such conditions, classic VWAP becomes unreliable. It no longer reflects fair value and often misleads traders relying on it for dynamic support, resistance, or reversion signals.

This Adaptive VWAP improves on that by using RelVol, which compares the current volume to the average volume seen at the same time over previous sessions. It gives more weight to price when volume is typical for that moment, and adjusts the influence when volume is statistically abnormal. This reduces the impact of isolated volume spikes and stabilizes the VWAP path, even in high-volatility environments.

For example, on SPY 1-minute or 5-minute charts during a CPI release, a massive spike in volume and price can occur within a single candle. Classic VWAP will immediately anchor itself to that spike. Adaptive VWAP using RelVol softens that effect and maintains a more realistic trajectory.

Key features:

- Adaptive VWAP weighted by time-adjusted Relative Volume (RelVol)

- Designed to maintain VWAP reliability during macroeconomic events

- Flexible anchoring: Session, Week, Month, Quarter, Earnings, etc.

- Optional display of Classic VWAP for comparison

- Up to 3 customizable deviation bands (standard deviation or percentage)

This tool is ideal for intraday traders who need a VWAP that remains usable and unbiased, even in volatile sessions. It adds robustness to VWAP-based strategies by incorporating time-sensitive volume normalization.

Retail Pain Index (RPIx) (RPIx) Retail Pain Index (DAFE)

See the Market’s Pain. Trade the Edge.

The Retail Pain Index (RPIx) is a next-generation volatility and sentiment tool designed to reveal the hidden moments when retail traders are most likely being squeezed, stopped out, or forced to capitulate. This is not just another oscillator—it’s a behavioral market scanner that quantifies “pain” as price rips away from the average entry zone, often marking the fuel for the next big move.

Why is RPIx so Unique?

Behavioral Volatility Engine:

RPIx doesn’t just track price or volume. It measures how far price is moving away from where the crowd has recently entered (using a rolling VWAP average), then normalizes this “distance” into a Z-score. The result? You see when the market is inflicting maximum pain on the most participants.

Dynamic, Intuitive Coloring:

The main RPIx line is purple in normal conditions, but instantly turns red when pain is extreme to the upside (+2.00 or higher) and green when pain is extreme to the downside (-2.00 or lower). This makes it visually obvious when the market is entering a “max pain” regime.

Threshold Lines for Clarity:

Dashed red and green lines at +2.00 and -2.00 Z-score levels make it easy to spot rare, high-pain events at a glance.

Signature Dashboard & Info Line:

Dashboard: A compact, toggleable panel in the top right of the indicator pane shows the current Z-score, threshold, and status—perfect for desktop users who want a quick read on market stress.

Info Line: For mobile or minimalist traders, a single-line info label gives you the essentials without cluttering your screen.

Inputs & Customization

Entry Cluster Lookback: Adjusts how many bars are used to calculate the “entry zone” (VWAP average). A higher value smooths the signal, a lower value makes it more responsive.

Pain Z-Score Threshold:

Sets the sensitivity for what counts as “extreme pain.” Default is ±2.00, but you can fine-tune this to match your asset’s volatility or your own risk appetite.

Show Dashboard / Show Compact Info Label:

Toggle these features on or off to fit your workflow and screen size.

How to utilize RPIx's awesomeness:

Extreme Readings = Opportunity:

When RPIx spikes above +2.00 (red) or below -2.00 (green), the market is likely running stops, liquidating weak hands, or forcing retail traders to capitulate. These moments often precede sharp reversals, trend accelerations, or volatility expansions.

Combine with Price Action:

Use RPIx as a confirmation tool for your existing strategy, or as a standalone alert for “pain points” where the crowd is most vulnerable.

Visual Edge:

The color-coded line and threshold levels make it easy to spot regime shifts and rare events—no more squinting at numbers or guessing when the market is about to snap.

Why RPIx?

Works on Any Asset, Any Timeframe:

Stocks, futures, crypto, forex—if there’s a crowd, there’s pain, and RPIx will find it.

Behavioral Alpha:

Most indicators lag. RPIx quantifies the psychological stress in the market, giving you a real-time edge over the herd.

Customizable, Clean, and Powerful:

Designed for both power users and mobile traders, with toggles for every workflow.

See the pain. Trade the edge.

Retail Pain Index: Because the market’s next move is written in the crowd’s discomfort.

For educational purposes only. Not financial advice. Always use proper risk management

Use with discipline. Trade your edge.

— Dskyz , for DAFE Trading Systems, for DAFE Trading Systems

Multi VWAPsMulti VWAPs Inspired by Biran Shannon and his book:

"MAXIMUM TRADING GAINS WITH ANCHORED VWAP . The Perfect Combination of Price, Time & Volume."

(ISBN 9798986868004)

A comprehensive VWAP (Volume Weighted Average Price) indicator that combines multiple timeframes and sessions in one view. Perfect for day trading and swing trading across different markets.

Features:

• Multiple VWAP Timeframes:

- Daily VWAP

- Weekly VWAP

- Monthly VWAP

- Quarterly VWAP

- Yearly VWAP

• Session-specific VWAPs:

- London Session (3:00 AM - 11:30 AM NY time)

- New York Session (9:30 AM - 4:00 PM NY time)

• Additional Indicators:

- Midnight Price Line (Previous day's closing price)

- 5-Day Moving Average

- 50-Day Moving Average

• Customization Options:

- Toggle individual VWAPs and indicators

- Customize colors for each component

- Adjustable label positioning

- MA smoothing settings

- Option to show/hide previous day's midnight price

• Smart Features:

- Auto-adjusting calculations based on timeframe

- Clear session boundaries

- Optimized for all chart timeframes

- Clean label system

Perfect for:

• Day traders tracking multiple timeframe momentum

• Swing traders using longer-term VWAPs

• Session traders focusing on London/NY hours

• Multi-timeframe analysis

• Price action trading with VWAP support/resistance

This indicator combines essential trading tools in one clean interface, helping you make informed decisions without cluttering your chart.

Money Flow Index + VWAP Trend FilterThis indicator combines the volume-weighted momentum analysis of the Money Flow Index (MFI) with the trend-filtering capabilities of the Volume Weighted Average Price (VWAP) to generate reliable buy and sell signals. By requiring MFI overbought/oversold conditions to align with the trend direction relative to VWAP, this indicator reduces false signals, making it ideal for trading on timeframes like 5-minute to 4-hour charts.

How It Works

The indicator uses two technical components to produce signals:

Money Flow Index (MFI) for Momentum Extremes:

The MFI, calculated over a default 14-period length, measures buying and selling pressure using price and volume data. A buy signal is triggered when MFI crosses above the oversold level (default: 20), indicating potential buying pressure, while a sell signal occurs when MFI crosses below the overbought level (default: 80), suggesting selling pressure.

Volume Weighted Average Price (VWAP) for Trend Direction:

The VWAP calculates the average price of an asset, weighted by volume, resetting at the start of each trading session (e.g., daily for stocks). It acts as a dynamic support/resistance level. A bullish trend is confirmed when the price is above the VWAP, and a bearish trend when the price is below the VWAP. This ensures MFI signals are filtered to align with the broader trend direction, plotted as a purple line on the chart.

Signal Generation

Signals are generated using the previous bar’s values to prevent repainting:

Buy Signal: The MFI crosses above the oversold level, and the price is above the VWAP (bullish trend). Displayed as a green upward triangle below the bar.

Sell Signal: The MFI crosses below the overbought level, and the price is below the VWAP (bearish trend). Displayed as a red downward triangle above the bar.

TLC sessionA Professional Intraday Session Tracker with VWAP and Economic Event Integration

Description

This indicator provides visual tracking of major trading sessions (Asian, London, New York) combined with VWAP calculations and macroeconomic event zones. It's designed for intraday traders who need to monitor session overlaps, liquidity periods, and high-impact news events.

The basic script of trading sessions was taken as a basis and refined for greater convenience.

Key Features:

Customizable Session Tracking: Visualize up to 3 trading sessions with adjustable time zones (supports IANA & GMT formats)

Dynamic VWAP Integration: Built-in Volume-Weighted Average Price calculation

Macro Event Zones: Highlights key economic announcement windows (adjustable for summer/winter time)

Price Action Visualization: Displays open/close prices, session ranges, and average price levels

Automatic DST Adjustment: Uses IANA timezone database for daylight savings awareness

How It Works

1. Trading Session Detection

Three fully configurable sessions (e.g., Asia, London, New York)

Each session displays:

Colored background zone

Opening price (dashed line)

Closing price (dashed line)

Average price (dotted line)

Optional label with session name

2. VWAP Calculation

Standard Volume-Weighted Average Price plotted as circled line

Helps identify fair value within each session

3. Macro Event Zones

Special highlighted period for economic news releases

Automatically adjusts for summer/winter time

Default set to 1000-1200 (summer) or 0900-1100 (winter) GMT-5 (US session open)

Why This Indicator is Unique

Multi-Session Awareness

Unlike simple session indicators, this tool:

Tracks price development within each session

Shows session overlaps (critical for volatility periods)

Maintains separate VWAP calculations across sessions

Professional-Grade Features

IANA timezone support (automatic DST handling)

Customizable visual elements (toggle labels, ranges, averages)

Object-based architecture (clean, efficient rendering)

News event integration (helps avoid trading during high-impact releases)

Usage Recommendations

Best Timeframes

1-minute to 1-hour charts (intraday focus)

Not recommended for daily+ timeframes

Trading Applications

1. Session Breakout Strategy: Trade breakouts when London/New York sessions open

2. VWAP Reversion: Fade moves that deviate too far from VWAP

3. News Avoidance: Reduce position sizing during macro event windows

Visual Example

Asian session (red)

London session (blue)

New York session (purple)

Macro event zone (white)

VWAP line (gold circles)

The basic script of trading sessions was taken as a basis and refined for greater convenience.

Moving Volume-Weighted Avg Price, % Channel, BBsThis script includes:

- Moving Volume-Weighted Average Price line.

- User-defined % band above and below, very useful for "breakout" signals, and mentally adjusting to the magnitude of price swings when viewing an automatic scale on the price axis.

- Volume-Weighted Bollinger Bands, which are more sensitive to volume.

More detail:

- This is like TV's basic VWAP in concept, except the major flaw in that is that it has reset periods that you can't override, and the volume is cumulative until the next hard reset. The 'reset' is OK for securities trading, that resets every day anyway. But not for crypto - and not if/when securities trading goes 24/7. Also, the denominator accumulating over the entire period is also *not* OK, because then what is shown means something different as the day progresses - which kind of makes it useless. In other words, it starts out very sensitive to volume, and gets progressively more numb to it as they day progresses, and starts flattening out.

- This fixes both problems, by using a user-definable moving window for the average. Essentially combining SMA with volume-weighting.

- You may also find an invaluable trading aid, in the % bands above and below.

- What can optionally be shown is standard deviation bands, aka Bollinger bands. The advantage over regular BB is that it's volume-weighted. Since it is already calculated on a moving average, the period for the standard deviation has been shortened by default, and the magnitude increased, to better approximate regular Bollinger Bands - but it's still more responsive to volume.

Multi-VWAP System🚀 Multi-VWAP System — Anchored VWAP & Deviation Bands

Overview

The Multi-VWAP System provides traders with a professional-grade approach to anchored VWAP analysis. Inspired by Brian Shannon's pioneering work on Anchored VWAP, this indicator automatically calculates and plots:

Current Session VWAP

Previous Session VWAP (also known as "2-Day VWAP")

High-of-Day (HOD) Anchored VWAP

Each VWAP can also display optional Standard Deviation Bands to highlight statistically significant deviations from the volume-weighted average price.

🔍 Why Anchored VWAP Matters

Volume Weighted Average Price (VWAP) is among the most critical institutional indicators, as it represents the average price paid for a stock adjusted by trading volume. This makes VWAP crucial for identifying fair value and significant areas of institutional activity.

Institutions utilize VWAP extensively to guide their execution algorithms. For instance, if price dips below a 2-day anchored VWAP (anchored to the previous session's open), many institutions interpret this as a discounted entry, potentially triggering large-scale buy programs. Conversely, sustained movement above VWAP signals strong buying pressure and bullish sentiment.

📌 Why Multiple Anchors?

Traders commonly anchor VWAPs at critical reference points:

Current Session VWAP:

Essential for day traders as a reference for intraday sentiment. Price action above this line generally indicates bullish sentiment, while price below signals bearish sentiment.

Previous Session (2-Day) VWAP:

Heavily used by institutions and swing traders, it provides insight into multi-session sentiment. Institutions commonly activate buy or sell programs based on whether price is trading at a premium or discount relative to this VWAP.

High-of-Day (HOD) VWAP:

Frequently used by momentum traders, this anchor captures sentiment after the most recent intraday high. Price above the HOD VWAP suggests sustained bullish momentum, while price below might signal weakening momentum.

🌟 Standard Deviation Bands

Each anchored VWAP in this indicator includes optional Standard Deviation Bands, highlighting statistical extremes. Traders use these bands to:

Identify potentially overextended moves (beyond +2σ or +3σ).

Gauge momentum strength (holding above +1σ).

Spot mean-reversion setups when price returns to VWAP after extreme moves.

🎨 Dynamic Background and Momentum Colorization

To visually highlight strength or weakness in price action relative to VWAP:

Dynamic Background Fill between Current and Previous VWAPs:

Green background appears when the Current VWAP is above the Previous VWAP and the linear regression slope (adjustable length) is positive, indicating bullish sentiment.

Red background appears when the Current VWAP is below the Previous VWAP and the slope is negative, indicating bearish sentiment.

No fill when conditions are mixed or momentum is uncertain.

Gold Fill above HOD VWAP:

When price action is above the High-of-Day VWAP and momentum (linear regression slope) is positive, a subtle gold shading appears, quickly highlighting bullish momentum.

⚙ Fully Customizable Settings

Session Times: Adjust session start and end times to match your specific market hours.

Standard Deviation Bands: Enable or disable each VWAP’s deviation bands individually and select how many bands (1σ, 2σ, or 3σ) you'd like to display.

Momentum Slope Length: Adjustable lookback for linear regression slope calculation—giving you full control of trend sensitivity.

🎯 Who Should Use This Indicator?

This indicator is perfect for:

Day Traders who want quick insights into intraday sentiment shifts.

Swing Traders tracking institutional footprints and seeking optimal entry/exit points.

Momentum Traders who rely on clearly visible momentum signals from HOD anchored VWAPs.

Institutional Traders and Professionals seeking sophisticated, institutionally-inspired VWAP analysis without manual anchoring.

📈 Summary of Features

✅ Automatic VWAP Anchors (Current Session, Previous Session, High-of-Day)

✅ Optional Standard Deviation Bands for each VWAP anchor

✅ Dynamic Background Coloring based on price action and momentum conditions

✅ Gold Momentum Highlight for quick bullish momentum identification above HOD VWAP

✅ Fully Customizable Inputs for precise personalization and flexibility

📢 Conclusion

The Multi-VWAP System isn't just another VWAP indicator. It's an institutional-level, dynamic, multi-dimensional analysis tool inspired by the work of Brian Shannon and leading institutional traders. It takes the guesswork out of anchoring and analysis, leaving you free to focus on identifying and executing high-probability trade setups.

Enjoy trading smarter—not harder. Happy Trading! 🚀📊

Liquid Pulse Liquid Pulse by Dskyz (DAFE) Trading Systems

Liquid Pulse is a trading algo built by Dskyz (DAFE) Trading Systems for futures markets like NQ1!, designed to snag high-probability trades with tight risk control. it fuses a confluence system—VWAP, MACD, ADX, volume, and liquidity sweeps—with a trade scoring setup, daily limits, and VIX pauses to dodge wild volatility. visuals include simple signals, VWAP bands, and a dashboard with stats.

Core Components for Liquid Pulse

Volume Sensitivity (volumeSensitivity) controls how much volume spikes matter for entries. options: 'Low', 'Medium', 'High' default: 'High' (catches small spikes, good for active markets) tweak it: 'Low' for calm markets, 'High' for chaos.

MACD Speed (macdSpeed) sets the MACD’s pace for momentum. options: 'Fast', 'Medium', 'Slow' default: 'Medium' (solid balance) tweak it: 'Fast' for scalping, 'Slow' for swings.

Daily Trade Limit (dailyTradeLimit) caps trades per day to keep risk in check. range: 1 to 30 default: 20 tweak it: 5-10 for safety, 20-30 for action.

Number of Contracts (numContracts) sets position size. range: 1 to 20 default: 4 tweak it: up for big accounts, down for small.

VIX Pause Level (vixPauseLevel) stops trading if VIX gets too hot. range: 10 to 80 default: 39.0 tweak it: 30 to avoid volatility, 50 to ride it.

Min Confluence Conditions (minConditions) sets how many signals must align. range: 1 to 5 default: 2 tweak it: 3-4 for strict, 1-2 for more trades.

Min Trade Score (Longs/Shorts) (minTradeScoreLongs/minTradeScoreShorts) filters trade quality. longs range: 0 to 100 default: 73 shorts range: 0 to 100 default: 75 tweak it: 80-90 for quality, 60-70 for volume.

Liquidity Sweep Strength (sweepStrength) gauges breakouts. range: 0.1 to 1.0 default: 0.5 tweak it: 0.7-1.0 for strong moves, 0.3-0.5 for small.

ADX Trend Threshold (adxTrendThreshold) confirms trends. range: 10 to 100 default: 41 tweak it: 40-50 for trends, 30-35 for weak ones.

ADX Chop Threshold (adxChopThreshold) avoids chop. range: 5 to 50 default: 20 tweak it: 15-20 to dodge chop, 25-30 to loosen.

VWAP Timeframe (vwapTimeframe) sets VWAP period. options: '15', '30', '60', '240', 'D' default: '60' (1-hour) tweak it: 60 for day, 240 for swing, D for long.

Take Profit Ticks (Longs/Shorts) (takeProfitTicksLongs/takeProfitTicksShorts) sets profit targets. longs range: 5 to 100 default: 25.0 shorts range: 5 to 100 default: 20.0 tweak it: 30-50 for trends, 10-20 for chop.

Max Profit Ticks (maxProfitTicks) caps max gain. range: 10 to 200 default: 60.0 tweak it: 80-100 for big moves, 40-60 for tight.

Min Profit Ticks to Trail (minProfitTicksTrail) triggers trailing. range: 1 to 50 default: 7.0 tweak it: 10-15 for big gains, 5-7 for quick locks.

Trailing Stop Ticks (trailTicks) sets trail distance. range: 1 to 50 default: 5.0 tweak it: 8-10 for room, 3-5 for fast locks.

Trailing Offset Ticks (trailOffsetTicks) sets trail offset. range: 1 to 20 default: 2.0 tweak it: 1-2 for tight, 5-10 for loose.

ATR Period (atrPeriod) measures volatility. range: 5 to 50 default: 9 tweak it: 14-20 for smooth, 5-9 for reactive.

Hardcoded Settings volLookback: 30 ('Low'), 20 ('Medium'), 11 ('High') volThreshold: 1.5 ('Low'), 1.8 ('Medium'), 2 ('High') swingLen: 5

Execution Logic Overview trades trigger when confluence conditions align, entering long or short with set position sizes. exits use dynamic take-profits, trailing stops after a profit threshold, hard stops via ATR, and a time stop after 100 bars.

Features Multi-Signal Confluence: needs VWAP, MACD, volume, sweeps, and ADX to line up.

Risk Control: ATR-based stops (capped 15 ticks), take-profits (scaled by volatility), and trails.

Market Filters: VIX pause, ADX trend/chop checks, volatility gates. Dashboard: shows scores, VIX, ADX, P/L, win %, streak.

Visuals Simple signals (green up triangles for longs, red down for shorts) and VWAP bands with glow. info table (bottom right) with MACD momentum. dashboard (top right) with stats.

Chart and Backtest:

NQ1! futures, 5-minute chart. works best in trending, volatile conditions. tweak inputs for other markets—test thoroughly.

Backtesting: NQ1! Frame: Jan 19, 2025, 09:00 — May 02, 2025, 16:00 Slippage: 3 Commission: $4.60

Fee Typical Range (per side, per contract)

CME Exchange $1.14 – $1.20

Clearing $0.10 – $0.30

NFA Regulatory $0.02

Firm/Broker Commis. $0.25 – $0.80 (retail prop)

TOTAL $1.60 – $2.30 per side

Round Turn: (enter+exit) = $3.20 – $4.60 per contract

Disclaimer this is for education only. past results don’t predict future wins. trading’s risky—only use money you can lose. backtest and validate before going live. (expect moderators to nitpick some random chart symbol rule—i’ll fix and repost if they pull it.)

About the Author Dskyz (DAFE) Trading Systems crafts killer trading algos. Liquid Pulse is pure research and grit, built for smart, bold trading. Use it with discipline. Use it with clarity. Trade smarter. I’ll keep dropping badass strategies ‘til i build a brand or someone signs me up.

2025 Created by Dskyz, powered by DAFE Trading Systems. Trade smart, trade bold.

Volume-Weighted Pivot BandsThe Volume-Weighted Pivot Bands are meant to be a dynamic, rolling pivot system designed to provide traders with responsive support and resistance levels that adapt to both price volatility and volume participation. Unlike traditional daily pivot levels, this tool recalculates levels bar-by-bar using a rolling window of volume-weighted averages, making it highly relevant for intraday traders, scalpers, swing traders, and algorithmic systems alike.

-- What This Indicator Does --

This tool calculates a rolling VWAP-based pivot level, and surrounds that central pivot with up to five upper bands (R1–R5) and five lower bands (S1–S5). These act as dynamic zones of potential resistance (R) and support (S), adapting in real time to price and volume changes.

Rather than relying on static session or daily data, this indicator provides continually evolving levels, offering more relevant levels during sideways action, trending periods, and breakout conditions.

-- How the Bands Are Calculated --

Pivot (VWAP Pivot):

The core of this system is a rolling Volume-Weighted Average Price, calculated over a user-defined window (default 20 bars). This ensures that each bar’s price impact is weighted by its volume, giving a more accurate view of fair value during the selected lookback.

Volume-Weighted Range (VW Range):

The highest high and lowest low over the same window are used to calculate the volatility range — this acts as a spread factor.

Support & Resistance Bands (S1–S5, R1–R5):

The bands are offset above and below the pivot using multiples of the VW Range:

R1 = Pivot + (VW Range × multiplier)

R2 = R1 + (VW Range × multiplier)

R3 = R2 + (VW Range x multiplier)

...

S1 = Pivot − (VW Range × multiplier)

S2 = S1 − (VW Range × multiplier)

S3 = S2 - (VW Range x multiplier)

...

You can control the multiplier manually (default is 0.25), to widen or tighten band spacing.

Smoothing (Optional):

To prevent erratic movements, you can optionally toggle on/off a simple moving average to the pivot line (default length = 20), providing a smoother trend base for the bands.

-- How to Use It --

This indicator can be used for:

Support and resistance identification:

Price often reacts to R1/S1, and the outer bands (R4/R5 or S4/S5) act as overshoot zones or strong reversal areas.

Trend context:

If price is respecting upper bands (R2–R3), the trend is likely bullish. If price is pressing into S3 or lower, it may indicate sustained selling pressure or a breakdown.

Volatility framing:

The distance between bands adjusts based on price range over the rolling window. In tighter markets, the bands compress — in volatile moves, they expand. This makes the indicator self-adaptive.

Mean reversion trades:

A move into R4/R5 or S4/S5 without continuation can be a sign of exhaustion — potential for reversal toward the pivot.

Alerting:

Built-in alerts are available for crosses of all major bands (R1–R5, S1–S5), enabling trade automation or scalp alerts with ease.

-- Visual Features --

Fuchsia Lines: Mark all Resistance (R1–R5) levels.

Lime Lines: Mark all Support (S1–S5) levels.

Gray Circle Line: Marks the rolling pivot (VWAP-based).

-- Customizable Settings --

Rolling Length: Number of bars used to calculate VWAP and VW Range.

Multiplier: Controls how wide the bands are spaced.

Smooth Pivot: Toggle on/off to smooth the central pivot.

Pivot Smoothing Length: Controls how many bars to average when smoothing is enabled.

Offset: Visually shift all bands forward/backward in time.

-- Why Use This Over Standard Pivots? --

Traditional pivots are based on previous session data and remain fixed. That’s useful for static setups, but may become irrelevant as price action evolves. In contrast:

This system updates every bar, adjusting to current price behavior.

It includes volume — a key feature missing from most static pivots.

It shows multiple bands, giving a full view of compression, breakout potential, or trend exhaustion.

-- Who Is This For? --

This tool is ideal for:

Day traders & scalpers who need relevant intraday levels.

Swing traders looking for evolving areas of confluence.

Algorithmic/systematic traders who rely on quantifiable, volume-aware support/resistance.

Traders on all assets: works on crypto, stocks, futures, forex — any chart that has volume.

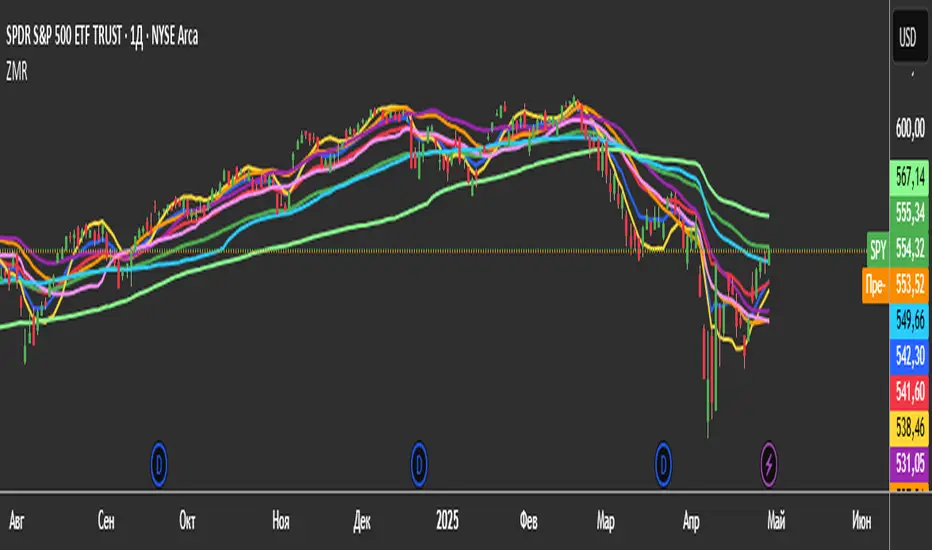

3 Zero Lag + 3 Moving Averages + 3 RVWAPThe "3 Zero Lag + 3 Moving Averages + 3 RVWAP" (ZMR) indicator combines three groups of tools for technical analysis.

1. Three Customizable Moving Averages (MAs):

Configuration for Each MA:

Choice of 7 types (SMA, EMA, WMA, HMA, VWMA, LSMA, SMMA).

Independent periods and price sources for each line.

Visualization:

MA1 (Blue), MA2 (Red), MA3 (Green).

2. Three Zero Lag EMAs (ZLEMA) with Individual Settings:

Lag Reduction: Corrects traditional EMA lag using:

Adjusted Price = 2 * Current Price - Price .

Flexibility:

Unique lengths (20, 50, 70) and individual price sources for each ZLEMA (HLC3, HL2, Close, etc.).

Colors:

ZLEMA1 (Yellow), ZLEMA2 (Orange), ZLEMA3 (Purple).

3. Three Rolling VWAPs with Custom Parameters:

Volume-Weighted Average Price (VWAP):

Calculated for three periods (20, 50, 100) with dedicated price sources for each VWAP.

Colors:

VWAP1 (Pink), VWAP2 (Light Blue), VWAP3 (Neon Green).