Yield Curve InversionThe Yield Curve Inversion indicator is a tool designed to help traders and analysts visualize and interpret the dynamics between the US 10-year and 2-year Treasury yields. This indicator is particularly useful for identifying yield curve inversions, often seen as a precursor to economic recessions.

Features and Interpretations

Display Modes: Choose between "Spread Mode" to visualize the yield spread indicating normal (green) or inverted (red) curves, or "Both Yields Mode" to view both yields.

Yield Spread: A plotted difference between 10-year and 2-year yields, with a zero line marking inversion. A negative spread suggests potential economic downturns.

Color Coding: Green for a normal yield curve (10Y > 2Y) and red for an inverted curve (2Y > 10Y).

Legend: Provides quick reference to yield curve states for easier interpretation.

This indicator is for educational and informational purposes only. It should not be considered financial advice or a recommendation to buy or sell any financial instruments. Users should conduct their own research and consult with a financial advisor before making investment decisions. The creator of this indicator is not responsible for any financial losses incurred through its use.

Yields

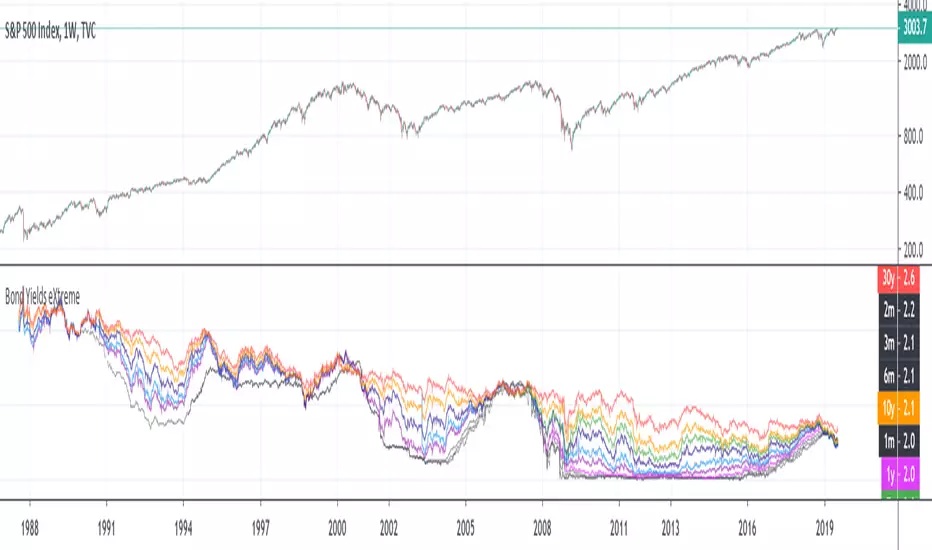

Yield Curve SpaghettiDisplays the difference in yield between multiple bond pairs for a given country.

Currently supports US, DE, and GB bonds

Global Yield SpreadThe Global Yield Spread is a simple indicator that can help to identify economic wellbeing and thus allows traders and investors alike to derive a rough estimation onto where the market is likely to go.

----------

Please note that things like Yield Spread generally influence the market only over longer time horizons of a couple weeks to many months.

Also be aware that the Yield Spread is only capable of measuring the Yields on Bonds and is thus limited to only changes that are reflected in the interest rates on the Bonds.

----------

The Normal Yield Spread is widely recognized for it's signal abilities for recessions or general economic well being...

However, since the rates have decreased drastically in the US something else has been proposed: The Global Yield Spread

As the normal US Yield Spread is loosing signal capacity because the US government can easily borrow money from overseas,

thus reducing the need to increase interest rates.

By monitoring and analyzing the Global Yield spread, traders and investors can gain insights into relative valuations, economic movements, market sentiment, and opportunities.

It can help inform their investment decisions and strategies, allowing them to allocate capital more effectively and potentially generate better returns.

You have options to visually represent a diversity of Countries and their according Yield Spreads.

Furthermore there are Global Yield Spreads for:

10Y-03MY

10Y-02Y

30Y-10Y

The Average Global Yield Spread encompasses the 3 options above to get an average reading.

US Inversions & RecessionsUnderstand when the US yield curve inverted and when recessions took place. Select from Federal Funds Rate, 3 month yield, 2 year yield and 10 year yield.

Default ratio = Federal Funds Rate / 10 year yield

When line goes from white to red = inversion

When line goes from red to white = un-inversion

Yellow shading shows times when the rates are inverted.

Blue shading shows when recessions officially occurred.

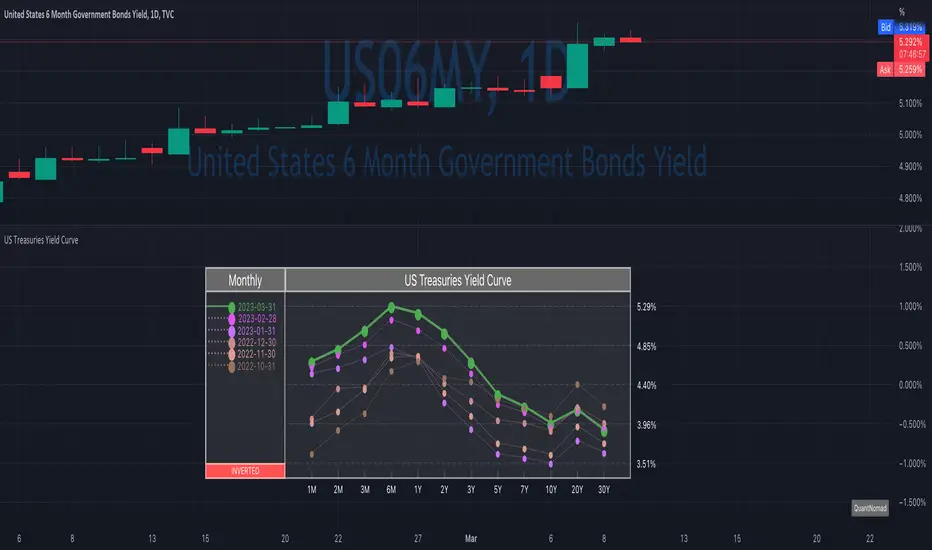

US Treasuries Yield CurveNews about the yield curve became pretty crucial for all the trades in the last year.

So in the team, we decided to implement a nice widget that will allow you to track the current yield curve in your chart directly.

It's possible to compare the current yield curve with past yield curves. You can choose to display the number of curves weeks, months, and years ago. So you can see the dynamics of the yield curve change.

When the Y2 > Y10 curve is considered invested, so you'll see an "Inverted" notification on the chart.

Thanks to @MUQWISHI for helping code it.

Disclaimer

Please remember that past performance may not indicate future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

10-Year Bond Yields (Interest Rate Differential)With this little script, I have attempted to incorporate fundamental data (in this case, 10-year bond yields) into technical analysis . When pairing two currencies, the one with a higher bond interest rate usually appreciates when the interest rate differential widens, or, to use a simple example: in a currency pair A vs. B, with A showing a higher bond yield than B, a widening interest rate gap is likely to help A and create a buying opportunity (shown as a blue square at the bottom of the chart), while the opposite is true when the gap tightens (sell signal, red square).

While long-term investors know about and make use of the importance of bond yield fluctuations, most short-term traders tend to dismiss the idea of using fundamental data, mostly for lack of quantifiability and limited impact in an intraday environment. After extensive backtesting on daily and intraday charts (6-12 hours), however, I realized this indicator still managed to produce useful results (less useful than on monthly and yearly charts, to be fair, but still useful enough), especially when paired with simple price-driven indicators, such as Heikin Ashi or linear regression .

My personal (and thus subjective) thoughts: worth a try. Buy and sell signals frequently contradicted both more popular indicators and my gut feeling and managed to take out losing trades that I had considered trades with a high winning probability. In other words, when the market lures traders into seemingly promising trading decisions, this indicator might give you an early warning, especially when you manage to adjust period and continuity parameters to your trading strategy.

Currency pairs used in this script are all possible combinations of the eight majors. Each security has been assigned a name ("inst01" to "inst08" in the code) and a broker; if you make changes to the code, be sure not to mess with currency and broker names as this would render the entire script useless. Good luck trading, and feel free to suggest improvements!

US/CA Bond Yield CurveEasy Viewing of 4 different duration bond yields for US and Canada. Bond prices and bond yields are excellent indicators of the economy as a whole, and of inflation in particular. A bond's yield is the discount rate that can be used to make the present value of all of the bond's cash flows equal to its price. Good as part of a macro set.

10-2 Year Treasury Yield Spread by zdmreLong-term bond yield reflects inflation. Short-term bond yields are tools used to predict Fed's interest rate policy. Spread between the two represents four cycles of an economy.

1. Growth

Short-term yield rises as interest rates rise. Spread narrows.

2. Slow growth

Central bank raises interest rates faster and short-term yield exceeds long-term yield. Spread turns negative.

3. Recession

High interest rates lead to more defaults. Inflation caps consumption. Central bank lowers interest rate to stimulate the economy and short-term yield falls. Spread widens.

4. Recovery

Central bank continues easing. Spread remains wide and yield curve remains steep.

0 = Recession Risk

2.6 = Recovery Plan

DYOR

Recession IndicatorThis script attempts to predict recessions four quarters ahead.

According to the New York Fed, "The yield curve—specifically, the spread between the interest rates on the ten-year Treasury

note and the three-month Treasury bill—is a valuable forecasting tool. It is simple to use

and significantly outperforms other financial and macroeconomic indicators in predicting

recessions two to six quarters ahead."

The paper offers Estimated Recession Probabilities Using the Yield Curve Spread:

Four Quarters Ahead

Recession Probability Value of Spread

(Percent) (Percentage Points)

5 1.21

10 0.76

15 0.46

20 0.22

25 0.02

30 -0.17

40 -0.50

50 -0.82

60 -1.13

70 -1.46

80 -1.85

90 -2.40

"Note: The yield curve spread is defined as the spread between the

interest rates on the ten-year Treasury note and the three-month

Treasury bill."

You can choose at which Recession Probability (percent) you want to display the signal (default value is 25%), as well as choose if you want to only display the signal at inversion (default) or at all times when the yield curve is inverted.

To use, just select your current timeframe from the menu.

Includes an option for repainting -- default value is true, meaning the script will repaint the current bar.

False = Not Repainting = Value for the current bar is not repainted, but all past values are offset by 1 bar.

True = Repainting = Value for the current bar is repainted, but all past values are correct and not offset by 1 bar.

In both cases, all of the historical values are correct, it is just a matter of whether you prefer the current bar to be realistically painted and the historical bars offset by 1, or the current bar to be repainted and the historical data to match their respective price bars.

As explained by TradingView,`f_security()` is for coders who want to offer their users a repainting/no-repainting version of the HTF data.

Real Interest Rate DifferentialThe Real IRD is a simple indicator built for forex trades that need a long-term view and want to compare currencies in search of high yield. The indicated interest rate maturity is 2 years, since shorter maturities may not price central banks' monetary policy decisions.

Example:

- You need to do an analysis of the AUDUSD

- In the Interest Rate 1 field, we put the interest rate for the base currency, in this case the AUD

- In the Interest Rate 2 field, the interest rate of the other currency, in this case the USD

- In the CPI 1 field, inflation referring to base currency

- In the CPI 2 field, inflation for another currency

CPI Codes:

QUANDL:RATEINF/INFLATION_USA < USD

QUANDL:RATEINF/INFLATION_EUR < EUR

QUANDL:RATEINF/INFLATION_JPN < JPY

QUANDL:RATEINF/INFLATION_CHE < CHF

QUANDL:RATEINF/INFLATION_GBR < GBP

QUANDL:RATEINF/INFLATION_CAN < CAD

QUANDL:RATEINF/INFLATION_RUS < RUB

QUANDL:RATEINF/INFLATION_AUS < AUD

QUANDL:RATEINF/INFLATION_NZL < NZD