Volume Footprint Anomaly Scanner [PhenLabs]📊 PhenLabs - Volume Footprint Anomaly Scanner (VFAS)

Version: PineScript™ v6

📌 Description

The PhenLabs Volume Footprint Anomaly Scanner (VFAS) is an advanced Pine Script indicator designed to detect and highlight significant imbalances in buying and selling pressure within individual price bars. By analyzing a calculated "Delta" – the net difference between estimated buy and sell volume – and employing statistical Z-score analysis, VFAS pinpoints moments when buying or selling activity becomes unusually dominant. This script was created not in hopes of creating a "Buy and Sell" indicator but rather providing the user with a more in-depth insight into the intrabar volume delta and how it can fluctuate in unusual ways, leading to anomalies that can be capitalized on.

This indicator helps traders identify high-conviction points where strong market participants are active, signaling potential shifts in momentum or continuation of a trend. It aims to provide a clearer understanding of underlying market dynamics, allowing for more informed decision-making in various trading strategies, from identifying entry points to confirming trend strength.

🚀 Points of Innovation

● Z-Score for Delta Analysis : Utilizes statistical Z-scores to objectively identify statistically significant anomalies in buying/selling pressure, moving beyond simple, arbitrary thresholds.

● Dynamic Confidence Scoring : Assigns a multi-star confidence rating (1-4 stars) to each signal, factoring in high volume, trend alignment, and specific confirmation criteria, providing a nuanced view of signal strength.

● Integrated Trend Filtering : Offers an optional Exponential Moving Average (EMA)-based trend filter to ensure signals align with the broader market direction, reducing false positives in ranging markets.

● Strict Confirmation Logic : Implements specific confirmation criteria for higher-confidence signals, including price action and a time-based gap from previous signals, enhancing reliability.

● Intuitive Info Dashboard : Provides a real-time summary of market trend and the latest signal's direction and confidence directly on the chart, streamlining information access.

🔧 Core Components

● Core Delta Engine : Estimates the net buying/selling pressure (bar Delta) by analyzing price movement within each bar relative to volume. It also calculates average volume to identify bars with unusually high activity.

● Anomaly Detection (Z-Score) : Computes the Z-score for the current bar's Delta, indicating how many standard deviations it is from its recent average. This statistical measure is central to identifying significant anomalies.

● Trend Filter : Utilizes a dual Exponential Moving Average (EMA) cross-over system to define the prevailing market trend (uptrend, downtrend, or range), providing contextual awareness.

● Signal Processing & Confidence Algorithm : Evaluates anomaly conditions against trend filters and confirmation rules, then calculates a dynamic confidence score to produce actionable, contextualized signal information.

🔥 Key Features

● Advanced Delta Anomaly Detection : Pinpoints bars with exceptionally high buying or selling pressure, indicating potential institutional activity or strong market conviction.

● Multi-Factor Confidence Scoring : Each signal comes with a 1-4 star rating, clearly communicating its reliability based on high volume, trend alignment, and specific confirmation criteria.

● Optional Trend Alignment : Users can choose to filter signals, so only those aligned with the prevailing EMA-defined trend are displayed, enhancing signal quality.

● Interactive Signal Labels : Displays compact labels on the chart at anomaly points, offering detailed tooltips upon hover, including signal type, direction, confidence, and contextual information.

● Customizable Bar Colors : Visually highlights bars with Delta anomalies, providing an immediate visual cue for strong buying or selling activity.

● Real-time Info Dashboard : A clean, customizable dashboard shows the current market trend and details of the latest detected signal, keeping key information accessible at a glance.

● Configurable Alerts : Set up alerts for bullish or bearish Delta anomalies to receive real-time notifications when significant market pressure shifts occur.

🎨 Visualization

Signal Labels :

* Placed at the top/bottom of anomaly bars, showing a "📈" (bullish) or "📉" (bearish) icon.

* Tooltip: Hovering over a label reveals detailed information: Signal Type (e.g., "Delta Anomaly"), Direction, Confidence (e.g., "★★★☆"), and a descriptive explanation of the anomaly.

* Interpretation: Clearly marks actionable signals and provides deep insights without cluttering the chart, enabling quick assessment of signal strength and context.

● Info Dashboard :

* Located at the top-right of the chart, providing a clean summary.

* Displays: "PhenLabs - VFAS" header, "Market Trend" (Uptrend/Downtrend/Range with color-coded status), and "Direction | Conf." (showing the last signal's direction and star confidence).

* Optional "💡 Hover over signals for details" reminder.

* Interpretation: A concise, real-time summary of the market's pulse and the most recent high-conviction event, helping traders stay informed at a glance.

📖 Usage Guidelines

Setting Categories

⚙️ Core Delta & Volume Engine

● Minimum Volume Lookback (Bars)

○ Default: 9

○ Range: Integer (e.g., 5-50)

○ Description: Defines the number of preceding bars used to calculate the average volume and delta. Bars with volume below this average won't be considered for high-volume signals. A shorter lookback is more reactive to recent changes, while a longer one provides a smoother average.

📈 Anomaly Detection Settings

Delta Z-Score Anomaly Threshold

○ Default: 2.5

○ Range: Float (e.g., 1.0-5.0+)

○ Description: The number of standard deviations from the mean that a bar's delta must exceed to be considered a significant anomaly. A higher threshold means fewer, but potentially stronger, signals. A lower threshold will generate more signals, which might include less significant events. Experiment to find the optimal balance for your trading style.

🔬 Context Filters

Enable Trend Filter

○ Default: False

○ Range: Boolean (True/False)

○ Description: When enabled, signals will only be generated if they align with the current market trend as determined by the EMAs (e.g., only bullish signals in an uptrend, bearish in a downtrend). This helps to filter out counter-trend noise.

● Trend EMA Fast

○ Default: 50

○ Range: Integer (e.g., 10-100)

○ Description: The period for the faster Exponential Moving Average used in the trend filter. In combination with the slow EMA, it defines the trend direction.

● Trend EMA Slow

○ Default: 200

○ Range: Integer (e.g., 100-400)

○ Description: The period for the slower Exponential Moving Average used in the trend filter. The relationship between the fast and slow EMA determines if the market is in an uptrend (fast > slow) or downtrend (fast < slow).

🎨 Visual & UI Settings

● Show Info Dashboard

○ Default: True

○ Range: Boolean (True/False)

○ Description: Toggles the visibility of the dashboard on the chart, which provides a summary of market trend and the last detected signal.

● Show Dashboard Tooltip

○ Default: True

○ Range: Boolean (True/False)

○ Description: Toggles a reminder message in the dashboard to hover over signal labels for more detailed information.

● Show Delta Anomaly Bar Colors

○ Default: True

○ Range: Boolean (True/False)

○ Description: Enables or disables the coloring of bars based on their delta direction and whether they represent a significant anomaly.

● Show Signal Labels

○ Default: True

○ Range: Boolean (True/False)

○ Description: Controls the visibility of the “📈” or “📉” labels that appear on the chart when a delta anomaly signal is generated.

🔔 Alert Settings

Alert on Delta Anomaly

○ Default: True

○ Range: Boolean (True/False)

○ Description: When enabled, this setting allows you to set up alerts in TradingView that will trigger whenever a new bullish or bearish delta anomaly is detected.

✅ Best Use Cases

Early Trend Reversal / Continuation Detection: Identify strong surges of buying/selling pressure at key support/resistance levels that could indicate a reversal or the continuation of a strong move.

● Confirmation of Breakouts: Use high-confidence delta anomalies to confirm the validity of price breakouts, indicating strong conviction behind the move.

● Entry and Exit Points: Pinpoint precise entry opportunities when anomalies align with your trading strategy, or identify potential exhaustion signals for exiting trades.

● Scalping and Day Trading: The indicator’s sensitivity to intraday buying/selling imbalances makes it highly effective for short-term trading strategies.

● Market Sentiment Analysis: Gain a real-time understanding of underlying market sentiment by observing the prevalence and strength of bullish vs. bearish anomalies.

⚠️ Limitations

Estimated Delta: The script uses a simplified method to estimate delta based on bar close relative to its range, not actual order book or footprint data. While effective, it’s an approximation.

● Sensitivity to Z-Score Threshold: The effectiveness heavily relies on the `Delta Z-Score Anomaly Threshold`. Too low, and you’ll get many false positives; too high, and you might miss valid signals.

● Confirmation Criteria: The 4-star confidence level’s “confirmation” relies on specific subsequent bar conditions and previous confirmed signals, which might be too strict or specific for all contexts.

● Requires Context: While powerful, VFAS is best used in conjunction with other technical analysis tools and price action to form a comprehensive trading strategy. It is not a standalone “buy/sell” signal.

💡 What Makes This Unique

Statistical Rigor: The application of Z-score analysis to bar delta provides an objective, statistically-driven way to identify true anomalies, moving beyond arbitrary thresholds.

● Multi-Factor Confidence Scoring: The unique 1-4 star confidence system integrates multiple market dynamics (volume, trend alignment, specific follow-through) into a single, easy-to-interpret rating.

● User-Friendly Design: From the intuitive dashboard to the detailed signal tooltips, the indicator prioritizes clear and accessible information for traders of all experience levels.

🔬 How It Works

1. Bar Delta Calculation:

● The script first estimates the “buy volume” and “sell volume” for each bar. This is done by assuming that volume proportional to the distance from the low to the close represents buying, and volume proportional to the distance from the high to the close represents selling.

● How this contributes: This provides a proxy for the net buying or selling pressure (delta) within that specific price bar, even without access to actual footprint data.

2. Volume & Delta Z-Score Analysis:

● The average volume over a user-defined lookback period is calculated. Bars with volume less than twice this average are generally considered of lower interest.

● The Z-score for the calculated bar delta is computed. The Z-score measures how many standard deviations the current bar’s delta is from its average delta over the `Minimum Volume Lookback` period.

● How this contributes: A high positive Z-score indicates a bullish delta anomaly (significantly more buying than usual), while a high negative Z-score indicates a bearish delta anomaly (significantly more selling than usual). This identifies statistically unusual levels of pressure.

3. Trend Filtering (Optional):

● Two Exponential Moving Averages (Fast and Slow EMA) are used to determine the prevailing market trend. An uptrend is identified when the Fast EMA is above the Slow EMA, and a downtrend when the Fast EMA is below the Slow EMA.

● How this contributes: If enabled, the indicator will only display bullish delta anomalies during an uptrend and bearish delta anomalies during a downtrend, helping to confirm signals within the broader market context and avoid counter-trend signals.

4. Signal Generation & Confidence Scoring:

● When a delta Z-score exceeds the user-defined anomaly threshold, a signal is generated.

● This signal is then passed through a multi-factor confidence algorithm (`f_calculateConfidence`). It awards stars based on: high volume presence, alignment with the overall trend (if enabled), and a fourth star for very strong Z-scores (above 3.0) combined with specific follow-through candle patterns after a cooling-off period from a previous confirmed signal.

● How this contributes: Provides a qualitative rating (1-4 stars) for each anomaly, allowing traders to quickly assess the potential significance and reliability of the signal.

💡 Note:

The PhenLabs Volume Footprint Anomaly Scanner is a powerful analytical tool, but it’s crucial to understand that no indicator guarantees profit. Always backtest and forward-test the indicator settings on your chosen assets and timeframes. Consider integrating VFAS with your existing trading strategy, using its signals as confirmation for entries, exits, or trend bias. The Z-score threshold is highly customizable; lower values will yield more signals (including potential noise), while higher values will provide fewer but potentially higher-conviction signals. Adjust this parameter based on market volatility and your risk tolerance. Remember to combine statistical insights from VFAS with price action, support/resistance levels, and your overall market outlook for optimal results.

Zscore

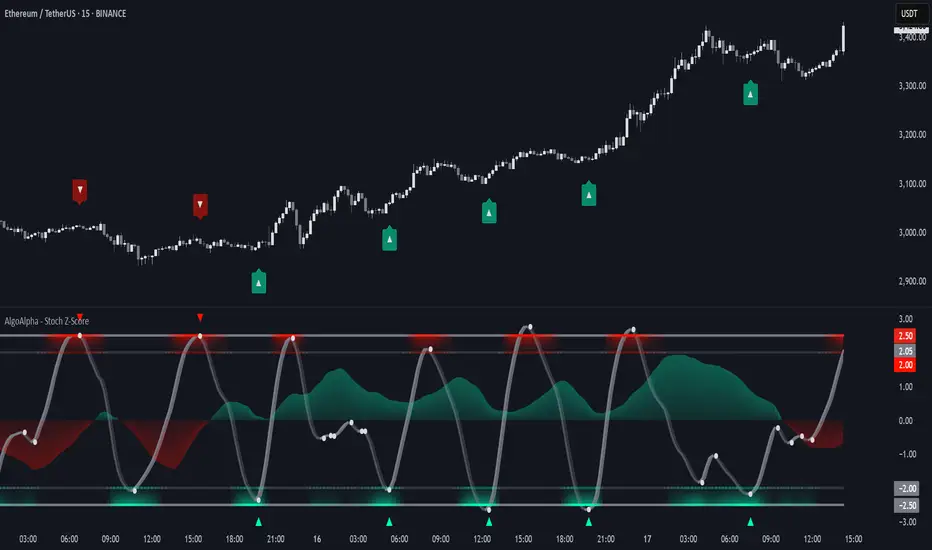

Stochastic Z-Score [AlgoAlpha]🟠 OVERVIEW

This indicator is a custom-built oscillator called the Stochastic Z-Score , which blends a volatility-normalized Z-Score with stochastic principles and smooths it using a Hull Moving Average (HMA). It transforms raw price deviations into a normalized momentum structure, then processes that through a stochastic function to better identify extreme moves. A secondary long-term momentum component is also included using an ALMA smoother. The result is a responsive oscillator that reacts to sharp imbalances while remaining stable in sideways conditions. Colored histograms, dynamic oscillator bands, and reversal labels help users visually assess shifts in momentum and identify potential turning points.

🟠 CONCEPTS

The Z-Score is calculated by comparing price to its mean and dividing by its standard deviation—this normalizes movement and highlights how far current price has stretched from typical values. This Z-Score is then passed through a stochastic function, which further refines the signal into a bounded range for easier interpretation. To reduce noise, a Hull Moving Average is applied. A separate long-term trend filter based on the ALMA of the Z-Score helps determine broader context, filtering out short-term traps. Zones are mapped with thresholds at ±2 and ±2.5 to distinguish regular momentum from extreme exhaustion. The tool is built to adapt across timeframes and assets.

🟠 FEATURES

Z-Score histogram with gradient color to visualize deviation intensity (optional toggle).

Primary oscillator line (smoothed stochastic Z-Score) with adaptive coloring based on momentum direction.

Dynamic bands at ±2 and ±2.5 to represent regular vs extreme momentum zones.

Long-term momentum line (ALMA) with contextual coloring to separate trend phases.

Automatic reversal markers when short-term crosses occur at extremes with supporting long-term momentum.

Built-in alerts for oscillator direction changes, zero-line crosses, overbought/oversold entries, and trend confirmation.

🟠 USAGE

Use this script to track momentum shifts and identify potential reversal areas. When the oscillator is rising and crosses above the previous value—especially from deeply negative zones (below -2)—and the ALMA is also above zero, this suggests bullish reversal conditions. The opposite holds for bearish setups. Reversal labels ("▲" and "▼") appear only when both short- and long-term conditions align. The ±2 and ±2.5 thresholds act as momentum warning zones; values inside are typical trends, while those beyond suggest exhaustion or extremes. Adjust the length input to match the asset’s volatility. Enable the histogram to explore underlying raw Z-Score movements. Alerts can be configured to notify key changes in momentum or zone entries.

Crowding model ║ BullVision🔬 Overview

The Crypto Crowding Model Pro is a sophisticated analytical tool designed to visualize and quantify market conditions across multiple cryptocurrencies. By leveraging Relative Strength Index (RSI) and Z-score calculations, this indicator provides traders with an intuitive and detailed snapshot of current crypto market dynamics, highlighting areas of extreme momentum, crowded trades, and potential reversal points.

⚙️ Key Concepts

📊 RSI and Z-Score Analysis

RSI (Relative Strength Index) evaluates the momentum and strength of each cryptocurrency, identifying overbought or oversold conditions.

Z-Score Normalization measures each asset's current price deviation relative to its historical average, identifying statistically significant extremes.

🎯 Crowding Analytics

An integrated analytics panel provides real-time crowding metrics, quantifying market sentiment into four distinct categories:

🔥 FOMO (Fear of Missing Out): High momentum, potential exhaustion.

❄️ Fear: Low momentum, potential reversal or consolidation.

📈 Recovery: Moderate upward momentum after a downward trend.

💪 Strength: Stable bullish conditions with sustained momentum.

🖥️ Visual Scatter Plot

Assets are plotted on a dynamic scatter plot, positioning each cryptocurrency according to its RSI and Z-score.

Color coding, symbol shapes, and sizes help quickly identify main market segments (BTC, ETH, TOTAL, OTHERS) and individual asset conditions.

🧩 Quadrant Classification

Assets are categorized into four quadrants based on their momentum and deviation:

Overbought Extended: High RSI and positive Z-score.

Recovery Phase: Low RSI but positive Z-score.

Oversold Compressed: Low RSI and negative Z-score.

Strong Consolidation: High RSI but negative Z-score.

🔧 User Customization

🎨 Visual Settings

Bar Scale: Adjust the scatter plot visual scale.

Asset Visibility: Optionally display key market benchmarks (TOTAL, BTC, ETH, OTHERS).

Gradient Background: Enhances visual interpretation of asset clusters.

Crowding Analytics Panel: Toggle the analytics panel on/off.

📊 Indicator Parameters

RSI Length: Defines the calculation period for RSI.

Z-score Lookback: Historical lookback period for normalization.

Crowding Alert Threshold: Sets alert sensitivity for crowded market conditions.

🎯 Zone Settings

Quadrant Labels: Displays descriptive labels for each quadrant.

Danger Zones: Highlights extreme RSI levels indicative of heightened market risk.

📈 Visual Output

Dynamic Scatter Plot: Visualizes asset positioning clearly and intuitively.

Gradient and Grid: Professional gridlines and subtle gradient backgrounds assist visual assessment.

Danger Zone Highlights: Visually indicates RSI extremes to warn of potential market turning points.

Crowding Analytics Panel: Real-time summary of market sentiment and asset distribution.

🔍 Use Cases

This indicator is particularly beneficial for traders and analysts looking to:

Identify crowded trades and potential reversal points.

Quickly assess overall market sentiment and individual asset strength.

Integrate a robust momentum analysis into broader technical or fundamental strategies.

Enhance market timing and improve risk management decisions.

⚠️ Important Notes

This indicator does not provide explicit buy or sell signals.

It is intended solely for informational, analytical, and educational purposes.

Past performance and signals are not indicative of future market results.

Always combine with additional tools and analysis as part of comprehensive decision-making.

Z-scored ZLEMA | OquantZ-Scored ZLEMA | Oquant

This indicator combines the Zero-Lag Exponential Moving Average (ZLEMA) with Z-score normalization to present recent ZLEMA values relative to its mean. It helps users observe trend direction and momentum with reduced lag, while also highlighting potential overbought or oversold levels based on how far ZLEMA values deviate from their mean.

🧠 Concept Overview

📉 Zero Lag Exponential Moving Average (ZLEMA)

The EMA is a popular tool that calculates an average price, but unlike a simple moving average, it gives more weight to recent prices. This means the EMA reacts faster to new price changes and is less affected by older data. However, even with this weighting, the EMA still introduces some lag.

ZLEMA improves on the EMA by reducing this lag. It does this by adjusting how it accounts for previous prices, effectively "shifting" the data to better align the average with current market action. The result is an average that stays smooth but responds more quickly to real price changes—helping traders spot turning points or trend shifts earlier without being fooled by random noise.

📏 Z-score Normalization

Once ZLEMA is calculated, the indicator applies Z-score normalization to measure how far the current ZLEMA value is from its mean. The Z-score expresses this difference using standard deviations, providing a clear, standardized scale. This helps highlight when price moves are unusually strong—either upward or downward—beyond normal fluctuations.

🔍 How This Indicator Works

Smooth Price Data with ZLEMA

The indicator begins by applying the Zero-Lag Exponential Moving Average (ZLEMA) to the chosen price data. Unlike a regular moving average, ZLEMA reduces the typical delay by adjusting the input data before averaging. It does this by "shifting" the price series to remove the lag caused by older prices. This way, ZLEMA stays smooth but reacts more quickly to recent price changes—helping the indicator follow market moves faster without being too noisy.

Normalize ZLEMA values Using Z-score

Once ZLEMA is calculated, the indicator applies Z-score normalization to measure how far the current ZLEMA value is from its mean. The Z-score expresses this difference in terms of standard deviations, creating a clear, standardized scale. This helps highlight when price moves are unusually strong—either up or down—beyond normal fluctuations.

Set Signal Thresholds

Two threshold levels are set on the Z-score scale—crossing above the upper threshold is considered a long (buy) signal, indicating bullish momentum, while crossing below the lower threshold is considered a short (sell) signal, indicating bearish momentum.

Show Visual Signals on the Chart

The Z-score and bars are plotted with colors: green when Z-score is above the bullish threshold, purple when Z-score is below the bearish threshold.

⚙️ Customizable Inputs

Source: Choose the price source (close, open, etc.) for calculations.

ZLEMA Length: Adjust the ZLEMA length to control smoothness versus responsiveness.

Z-score period: Set the Z-score period to define how far back the indicator measures normal price behavior.

Thresholds: Adjust the upper and lower thresholds to control how sensitive the indicator is to strong momentum changes.

📈 Practical Use

This indicator helps identify trend directions and changes faster by combining ZLEMA with statistical analysis. It highlights when price moves are stronger than normal, making it easier to spot early signs of momentum shifts. Traders can use it to confirm trends or detect potential reversals with more timely signals.

🔔 Alert Support

This indicator includes optional built-in alert conditions that notify you when the Z-score crosses above the bullish threshold (long signal) or below the bearish threshold (short signal). You can enable these alerts to get timely updates on potential momentum shifts without constantly watching the chart.

⚠️ Disclaimer: This indicator is intended for educational and informational purposes only. Trading/investing involves risk, and past performance does not guarantee future results. Always test and evaluate indicators/strategies before applying them in live markets. Use at your own risk.

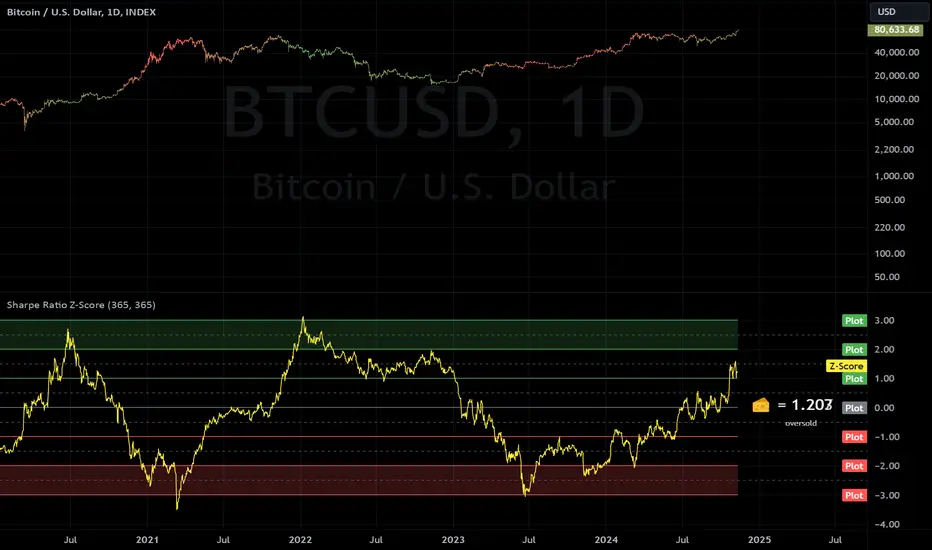

Uptrick: Universal Z-Score ValuationOverview

The Uptrick: Universal Z-Score Valuation is a tool designed to help traders spot when the market might be overreacting—whether that’s on the upside or the downside. It does this by combining the Z-scores of multiple key indicators into a single average, letting you see how far the current market conditions have stretched away from “normal.” This average is shown as a smooth line, supported by color-coded visuals, signal markers, optional background highlights, and a live breakdown table that shows the contribution of each indicator in real time. The focus here is on spotting potential reversals, not following trends. The indicator works well across all timeframes and asset classes, from fast intraday charts like the 1-minute and 5-minute, to higher timeframes such as the 4-hour, daily, or even weekly. Its universal design makes it suitable for any market — whether you're trading crypto, stocks, forex, or commodities.

Introduction

To understand what this indicator does, let’s start with the idea of a Z-score. In simple terms, a Z-score tells you how far a number is from the average of its recent history, measured in standard deviations. If the price of an asset is two standard deviations above its mean, that means it’s statistically “rare” or extended. That doesn’t guarantee a reversal—but it suggests the move is unusual enough to pay attention.

This concept isn’t new, but what this indicator does differently is apply the Z-score to a wide set of market signals—not just price. It looks at momentum, volatility, volume, risk-adjusted performance, and even institutional price baselines. Each of those indicators is normalized using Z-scores, and then they’re combined into one average. This gives you a single, easy-to-read line that summarizes whether the entire market is behaving abnormally. Instead of reacting to one indicator, you’re reacting to a statistically balanced blend.

Purpose

The goal of this script is to catch turning points—places where the market may be topping out or bottoming after becoming overstretched. It’s built for traders who want to fade sharp moves rather than follow trends. Think of moments when price explodes upward and starts pulling away from every moving average, volume spikes, volatility rises, and RSI shoots up. This tool is meant to spot those situations—not just when price is stretched, but when multiple different indicators agree that something is overdone.

Originality and Uniqueness

Most indicators that use Z-scores only apply them to one thing—price, RSI, or maybe Bollinger Bands. This one is different because it treats each indicator as a contributor to the full picture. You decide which ones to include, and the script averages them out. This makes the tool flexible but also deeply informative.

It doesn’t rely on complex or hidden math. It uses basic Z-score formulas, applies them to well-known indicators, and shows you the result. What makes it unique is the way it brings those signals together—statistically, visually, and interactively—so you can see what’s happening in the moment with full transparency. It’s not trying to be flashy or predictive. It’s just showing you when things have gone too far, too fast.

Inputs and Parameters

This indicator includes a wide range of configurable inputs, allowing users to customize which components are included in the Z-score average, how each indicator is calculated, and how results are displayed visually. Below is a detailed explanation of each input:

General Settings

Z-Score Lookback (default: 100): Number of bars used to calculate the mean and standard deviation for Z-score normalization. Larger values smooth the Z-scores; smaller values make them more reactive.

Bar Color Mode (default: None): Determines how bars are visually colored. Options include: None: No candle coloring applied. - Heat: Smooth gradient based on the Z-score value. - Latest Signal: Applies a solid color based on the most recent buy or sell signal

Boolean - General

Plot Universal Valuation Line (default: true): If enabled, plots the average Z-score (zAvg) line in the separate pane.

Show Signals (default: true): Displays labels ("𝓤𝓹" for buy, "𝓓𝓸𝔀𝓷" for sell) when zAvg crosses above or below user-defined thresholds.

Show Z-Score Table (default: true): Displays a live table listing each enabled indicator's Z-score and the current average.

Select Indicators

These toggles enable or disable each indicator from contributing to the Z-score average:

Use VWAP Z-Score (default: true)

Use Sortino Z-Score (default: true)

Use ROC Z-Score (default: true)

Use Price Z-Score (default: true)

Use MACD Histogram Z-Score (default: false)

Use Bollinger %B Z-Score (default: false)

Use Stochastic K Z-Score (default: false)

Use Volume Z-Score (default: false)

Use ATR Z-Score (default: false)

Use RSI Z-Score (default: false)

Use Omega Z-Score (default: true)

Use Sharpe Z-Score (default: true)

Only enabled indicators are included in the average. This modular design allows traders to tailor the signal mix to their preferences.

Indicator Lengths

These inputs control how each individual indicator is calculated:

MACD Fast Length (default: 12)

MACD Slow Length (default: 26)

MACD Signal Length (default: 9)

Bollinger Basis Length (default: 20): Used to compute the Bollinger %B.

Bollinger Deviation Multiplier (default: 2.0): Standard deviation multiplier for the Bollinger Band calculation.

Stochastic Length (default: 14)

ATR Length (default: 14)

RSI Length (default: 14)

ROC Length (default: 10)

Zones

These thresholds define key signal levels for the Z-score average:

Neutral Line Level (default: 0): Baseline for the average Z-score.

Bullish Zone Level (default: -1): Optional intermediate zone suggesting early bullish conditions.

Bearish Zone Level (default: 1): Optional intermediate zone suggesting early bearish conditions.

Z = +2 Line Level (default: 2): Primary threshold for bearish signals.

Z = +3 Line Level (default: 3): Extreme bearish warning level.

Z = -2 Line Level (default: -2): Primary threshold for bullish signals.

Z = -3 Line Level (default: -3): Extreme bullish warning level.

These zone levels are used to generate signals, fill background shading, and draw horizontal lines for visual reference.

Why These Indicators Were Merged

Each indicator in this script was chosen for a specific reason. They all measure something different but complementary.

The VWAP Z-score helps you see when price has moved far from the volume-weighted average, often used by institutions.

Sortino Ratio Z-score focuses only on downside risk, which is often more relevant to traders than overall volatility.

ROC Z-score shows how fast price is changing—strong momentum may burn out quickly.

Price Z-score is the raw measure of how far current price has moved from its mean.

RSI Z-score shows whether momentum itself is stretched.

MACD Histogram Z-score captures shifts in trend strength and acceleration.

%B (Bollinger) Z-score indicates how close price is to the upper or lower volatility envelope.

Stochastic K Z-score gives a sense of how high or low price is relative to its recent range.

Volume Z-score shows when trading activity is unusually high or low.

ATR Z-score gives a read on volatility, showing if price movement is expanding or contracting.

Sharpe Z-score measures reward-to-risk performance, useful for evaluating trend quality.

Omega Z-score looks at the ratio of good returns to bad ones, offering a more nuanced view of efficiency.

By normalizing each of these using Z-scores and averaging only the ones you turn on, the script creates a flexible, balanced view of the market’s statistical stretch.

Calculations

The core formula is the standard Z-score:

Z = (current value - average) / standard deviation

Every indicator uses this formula after it’s calculated using your chosen settings. For example, RSI is first calculated as usual, then its Z-score is calculated over your selected lookback period. The script does this for every indicator you enable. Then it averages those Z-scores together to create a single value: zAvg. That value is plotted and used to generate visual cues, signals, table values, background color changes, and candle coloring.

Sequence

Each selected indicator is calculated using your custom input lengths.

The Z-score of each indicator is computed using the shared lookback period.

All active Z-scores are added up and averaged.

The resulting zAvg value is plotted as a line.

Signal conditions check if zAvg crosses user-defined thresholds (default: ±2).

If enabled, the script plots buy/sell signal labels at those crossover points.

The candle color is updated using your selected mode (heatmap or signal-based).

If extreme Z-scores are reached, background highlighting is applied.

A live table updates with each individual Z-score so you know what’s driving the signal.

Features

This script isn’t just about stats—it’s about making them usable in real time. Every feature has a clear reason to exist, and they’re all there to give you a better read on market conditions.

1. Universal Z-Score Line

This is your primary reference. It reflects the average Z-score across all selected indicators. The line updates live and is color-coded to show how far it is from neutral. The further it gets from 0, the brighter the color becomes—cyan for deeply oversold conditions, magenta for overbought. This gives you instant feedback on how statistically “hot” or “cold” the market is, without needing to read any numbers.

2. Signal Labels (“𝓤𝓹” and “𝓓𝓸𝔀𝓷”)

When the average Z-score drops below your lower bound, you’ll see a "𝓤𝓹" label below the bar, suggesting potential bullish reversal conditions. When it rises above the upper bound, a "𝓓𝓸𝔀𝓷" label is shown above the bar—indicating possible bearish exhaustion. These labels are visually clear and minimal so they don’t clutter your chart. They're based on clear crossover logic and do not repaint.

3. Real-Time Z-Score Table

The table shows each indicator's individual Z-score and the final average. It updates every bar, giving you a transparent breakdown of what’s happening under the hood. If the market is showing an extreme average score, this table helps you pinpoint which indicators are contributing the most—so you’re not just guessing where the pressure is coming from.

4. Bar Coloring Modes

You can choose from three modes:

None: Keeps your candles clean and untouched.

Heat: Applies a smooth gradient color based on Z-score intensity. As conditions become more extreme, candle color transitions from neutral to either cyan (bullish pressure) or magenta (bearish pressure).

Latest Signal: Applies hard coloring based on the most recent signal—greenish for a buy, purple for a sell. This mode is great for tracking market state at a glance without relying on a gradient.

Every part of the candle is colored—body, wick, and border—for full visibility.

5. Background Highlighting

When zAvg enters an extreme zone (typically above +2 or below -2), the background shifts color to reflect the market’s intensity. These changes aren’t overwhelming—they’re light fills that act as ambient warnings, helping you stay aware of when price might be reaching a tipping point.

6. Customizable Zone Lines and Fills

You can define what counts as neutral, overbought, and oversold using manual inputs. Horizontal lines show your thresholds, and shaded regions highlight the most extreme zones (+2 to +3 and -2 to -3). These lines give you visual structure to understand where price currently stands in relation to your personal reversal model.

7. Modular Indicator Control

You don’t have to use all the indicators. You can enable or disable any of the 12 with a simple checkbox. This means you can build your own “blend” of market context—maybe you only care about RSI, price, and volume. Or maybe you want everything on. The script adapts accordingly, only averaging what you select.

8. Fully Customizable Sensitivity and Lengths

You can adjust the Z-score lookback length globally (default 100), and tweak individual indicator lengths separately. This lets you tune the indicator’s responsiveness to suit your trading style—slower for longer swings, faster for scalping.

9. Clean Integration with Any Chart Layout

All visual elements are designed to be informative without taking over your chart. The coloring is soft but clear, the labels are readable without being huge, and you can turn off any feature you don’t need. The indicator can work as a full dashboard or as a simple line with a couple of alerts—it’s up to you.

10. Precise, Real-Time Signal Logic

The crossover logic for signals is exact and only fires when the Z-score moves across your defined boundary. No estimation, no delay. Everything is calculated based on current and previous bar data, and nothing repaints or back-adjusts.

Conclusion

The Universal Z-Score Valuation indicator is a tool for traders who want a clear, unbiased way to detect overextension. Instead of relying on a single signal, you get a composite of several market perspectives—momentum, volatility, volume, and more—all standardized into a single view. The script gives you the freedom to control the logic, the visuals, and the components. Whether you use it as a confirmation tool or a primary signal source, it’s designed to give you clarity when markets become chaotic.

Disclaimer

This indicator is for research and educational use only. It does not constitute financial advice or guarantees of performance. All trading involves risk, and users should test any strategy thoroughly before applying it to live markets. Use this tool at your own discretion.

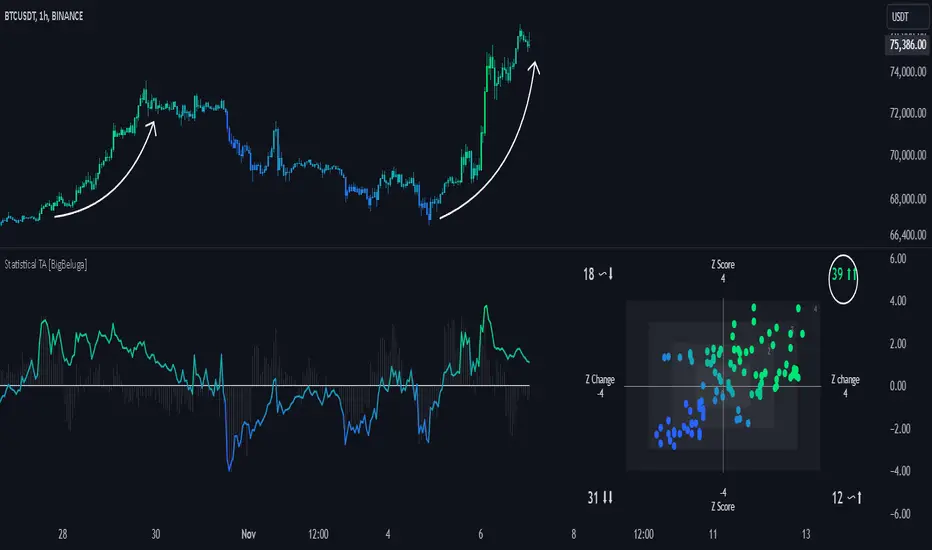

Z Score Overlay [BigBeluga]🔵 OVERVIEW

A clean and effective Z-score overlay that visually tracks how far price deviates from its moving average. By standardizing price movements, this tool helps traders understand when price is statistically extended or compressed—up to ±4 standard deviations. The built-in scale and real-time bin markers offer immediate context on where price stands in relation to its recent mean.

🔵 CONCEPTS

Z Score Calculation:

Z = (Close − SMA) ÷ Standard Deviation

This formula shows how many standard deviations the current price is from its mean.

Statistical Extremes:

• Z > +2 or Z < −2 suggests statistically significant deviation.

• Z near 0 implies price is close to its average.

Standardization of Price Behavior: Makes it easier to compare volatility and overextension across timeframes and assets.

🔵 FEATURES

Colored Z Line: Gradient coloring based on how far price deviates—

• Red = oversold (−4),

• Green = overbought (+4),

• Yellow = neutral (~0).

Deviation Scale Bar: A vertical scale from −4 to +4 standard deviations plotted to the right of price.

Active Z Score Bin: Highlights the current Z-score bin with a “◀” arrow

Context Labels: Clear numeric labels for each Z-level from −4 to +4 along the side.

Live Value Display: Shows exact Z-score on the active level.

Non-intrusive Overlay: Can be applied directly to price chart without changing scaling behavior.

🔵 HOW TO USE

Identify overbought/oversold areas based on +2 / −2 thresholds.

Spot potential mean reversion trades when Z returns from extreme levels.

Confirm strong trends when price remains consistently outside ±2.

Use in multi-timeframe setups to compare strength across contexts.

🔵 CONCLUSION

Z Score Overlay transforms raw price action into a normalized statistical view, allowing traders to easily assess deviation strength and mean-reversion potential. The intuitive scale and color-coded display make it ideal for traders seeking objective, volatility-aware entries and exits.

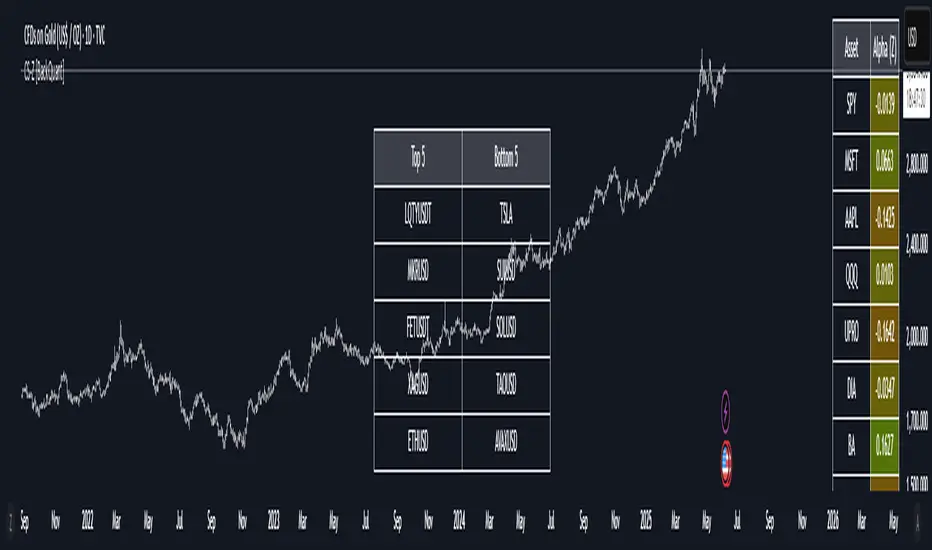

40 Ticker Cross-Sectional Z-Scores [BackQuant]40 Ticker Cross-Sectional Z-Scores

BackQuant’s 40 Ticker Cross-Sectional Z-Scores is a powerful portfolio management strategy that analyzes the relative performance of up to 40 different assets, comparing them on a cross-sectional basis to identify the top and bottom performers. This indicator computes Z-scores for each asset based on their log returns and evaluates them relative to the mean and standard deviation over a rolling window. The Z-scores represent how far an asset's return deviates from the average, and these values are used to rank the assets, allowing for dynamic asset allocation based on performance.

By focusing on the strongest-performing assets and avoiding the weakest, this strategy aims to enhance returns while managing risk. Additionally, by adjusting for standard deviations, the system offers a risk-adjusted method of ranking assets, making it suitable for traders who want to dynamically allocate capital based on performance metrics rather than just price movements.

Key Features

1. Cross-Sectional Z-Score Calculation:

The system calculates Z-scores for 40 different assets, evaluating their log returns against the mean and standard deviation over a rolling window. This enables users to assess the relative performance of each asset dynamically, highlighting which assets are performing better or worse compared to their historical norms. The Z-score is a useful statistical tool for identifying outliers in asset performance.

2. Asset Ranking and Allocation:

The system ranks assets based on their Z-scores and allocates capital to the top performers. It identifies the top and bottom assets, and traders can allocate capital to the top-performing assets, ensuring that their portfolio is aligned with the best performers. Conversely, the bottom assets are removed from the portfolio, reducing exposure to underperforming assets.

3. Rolling Window for Mean and Standard Deviation Calculations:

The Z-scores are calculated based on rolling means and standard deviations, making the system adaptive to changing market conditions. This rolling calculation window allows the strategy to adjust to recent performance trends and minimize the impact of outdated data.

4. Mean and Standard Deviation Visualization:

The script provides real-time visualizations of the mean (x̄) and standard deviation (σ) of asset returns, helping traders quickly identify trends and volatility in their portfolio. These visual indicators are useful for understanding the current market environment and making more informed allocation decisions.

5. Top & Bottom Performer Tables:

The system generates tables that display the top and bottom performers, ranked by their Z-scores. Traders can quickly see which assets are outperforming and underperforming. These tables provide clear and actionable insights, helping traders make informed decisions about which assets to include in their portfolio.

6. Customizable Parameters:

The strategy allows traders to customize several key parameters, including:

Rolling Calculation Window: Set the window size for the rolling mean and standard deviation calculations.

Top & Bottom Tickers: Choose how many of the top and bottom assets to display and allocate capital to.

Table Orientation: Select between vertical or horizontal table formats to suit the user’s preference.

7. Forward Test & Out-of-Sample Testing:

The system includes out-of-sample forward tests, ensuring that the strategy is evaluated based on real-time performance, not just historical data. This forward testing approach helps validate the robustness of the strategy in dynamic market conditions.

8. Visual Feedback and Alerts:

The system provides visual feedback on the current asset rankings and allocations, with dynamic labels and plots on the chart. Additionally, users receive alerts when allocations change, keeping them informed of important adjustments.

9. Risk Management via Z-Scores and Std Dev:

The system’s approach to asset selection is based on Z-scores, which normalize performance relative to the historical mean. By incorporating standard deviation, it accounts for the volatility and risk associated with each asset. This allows for more precise risk management and portfolio construction.

10. Note on Mean Reversion Strategy:

If you take the inverse of the signals provided by this indicator, the strategy can be used for mean-reversion rather than trend-following. This would involve buying the underperforming assets and selling the outperforming ones. However, it's important to note that this approach does not work well with highly correlated assets, as the relationship between the assets could result in the same directional movement, undermining the effectiveness of the mean-reversion strategy.

References

www.uts.edu.au

onlinelibrary.wiley.com

www.cmegroup.com

Final Thoughts

The 40 Ticker Cross-Sectional Z-Scores strategy offers a data-driven approach to portfolio management, dynamically allocating capital based on the relative performance of assets. By using Z-scores and standard deviations, this strategy ensures that capital is directed to the strongest performers while avoiding weaker assets, ultimately improving the risk-adjusted returns of the portfolio. Whether you’re focused on trend-following or looking to explore mean-reversion strategies, this flexible system can be tailored to suit your investment goals.

Price Statistical Strategy-Z Score V 1.01

Price Statistical Strategy – Z Score V 1.01

Overview

A technical breakdown of the logic and components of the “Price Statistical Strategy – Z Score V 1.01”.

This script implements a smoothed Z-Score crossover mechanism applied to the closing price to detect potential statistical deviations from local price mean. The strategy operates solely on price data (close) and includes signal spacing control and momentum-based candle filters. No volume-based or trend-detection components are included.

Core Methodology

The strategy is built on the statistical concept of Z-Score, which quantifies how far a value (closing price) is from its recent average, normalized by standard deviation. Two moving averages of the raw Z-Score are calculated: a short-term and a long-term smoothed version. The crossover between them generates long entries and exits.

Signal Conditions

Entry Condition:

A long position is opened when the short-term smoothed Z-Score crosses above the long-term smoothed Z-Score, and additional entry conditions are met.

Exit Condition:

The position is closed when the short-term Z-Score crosses below the long-term Z-Score, provided the exit conditions allow.

Signal Gapping:

A minimum number of bars (Bars gap between identical signals) must pass between repeated entry or exit signals to reduce noise.

Momentum Filter:

Entries are prevented during sequences of three or more consecutively bullish candles, and exits are prevented during three or more consecutively bearish candles.

Z-Score Function

The Z-Score is calculated as:

Z = (Close - SMA(Close, N)) / STDEV(Close, N)

Where N is the base period selected by the user.

Input Parameters

Enable Smoothed Z-Score Strategy

Enables or disables the Z-Score strategy logic. When disabled, no trades are executed.

Z-Score Base Period

Defines the number of bars used to calculate the simple moving average and standard deviation for the Z-Score. This value affects how responsive the raw Z-Score is to price changes.

Short-Term Smoothing

Sets the smoothing window for the short-term Z-Score. Higher values produce smoother short-term signals, reducing sensitivity to short-term volatility.

Long-Term Smoothing

Sets the smoothing window for the long-term Z-Score, which acts as the reference line in the crossover logic.

Bars gap between identical signals

Minimum number of bars that must pass before another signal of the same type (entry or exit) is allowed. This helps reduce redundant or overly frequent signals.

Trade Visualization Table

A table positioned at the bottom-right displays live PnL for open trades:

Entry Price

Unrealized PnL %

Text colors adapt based on whether unrealized profit is positive, negative, or neutral.

Technical Notes

This strategy uses only close prices — no trend indicators or volume components are applied.

All calculations are based on simple moving averages and standard deviation over user-defined windows.

Designed as a minimal, isolated Z-Score engine without confirmation filters or multi-factor triggers.

Uptrick: Dynamic Z-Score DeviationOverview

Uptrick: Dynamic Z‑Score Deviation is a trading indicator built in Pine Script that combines statistical filters and adaptive smoothing to highlight potential reversal points in price action. It combines a hybrid moving average, dual Z‑Score analysis on both price and RSI, and visual enhancements like slope‑based coloring, ATR‑based shadow bands, and dynamically scaled reversal signals.

Introduction

Statistical indicators like Z‑Scores measure how far a value deviates from its average relative to the typical variation (standard deviation). Standard deviation quantifies how dispersed a set of values is around its mean. A Z‑Score of +2 indicates a value two standard deviations above the mean, while -2 is two below. Traders use Z‑Scores to spot unusually high or low readings that may signal overbought or oversold conditions.

Moving averages smooth out price data to reveal trends. The Arnaud Legoux Moving Average (ALMA) reduces lag and noise through weighted averaging. A Zero‑Lag EMA (approximated here using a time‑shifted EMA) seeks to further minimize delay in following price. The RSI (Relative Strength Index) is a momentum oscillator that measures recent gains against losses over a set period.

ATR (Average True Range) gauges market volatility by averaging the range between high and low over a lookback period. Shadow bands built using ATR give a visual mood of volatility around a central trend line. Together, these tools inform a dynamic but statistically grounded view of market extremes.

Purpose

The main goal of this indicator is to help traders spot short‑term reversal opportunities on lower timeframes. By requiring both price and momentum (RSI) to exhibit statistically significant deviations from their norms, it filters out weak setups and focuses on higher‑probability mean‑reversion zones. Reversal signals appear when price deviates far enough from its hybrid moving average and RSI deviates similarly in the same direction. This makes it suitable for discretionary traders seeking clean entry cues in volatile environments.

Originality and Uniqueness

Uptrick: Dynamic Z‑Score Deviation distinguishes itself from standard reversal or mean‑reversion tools by combining several elements into a single framework:

A composite moving average (ALMA + Zero‑Lag EMA) for a smooth yet responsive baseline

Dual Z‑Score filters on price and RSI rather than relying on a single measure

Adaptive visual elements, including slope‑aware coloring, multi‑layer ATR shadows, and signal sizing based on combined Z‑Score magnitude

Most indicators focus on one aspect—price envelopes or RSI thresholds—whereas Uptrick: Dynamic Z‑Score Deviation requires both layers to align before signaling. Its visual design aids quick interpretation without overwhelming the chart.

Why these indicators were merged

Every component in Uptrick: Dynamic Z‑Score Deviation has a purpose:

• ALMA: provides a smooth moving average with reduced lag and fewer false crossovers than a simple SMA or EMA.

• Zero‑Lag EMA (ZLMA approximation): further reduces the delay relative to price by applying a time shift to EMA inputs. This keeps the composite MA closer to current price action.

• RSI and its EMA filter: RSI measures momentum. Applying an EMA filter on RSI smooths out false spikes and confirms genuine overbought or oversold momentum.

• Dual Z‑Scores: computing Z‑Scores on both the distance between price and the composite MA, and on smoothed RSI, ensures that signals only fire when both price and momentum are unusually stretched.

• ATR bands: using ATR‑based shadow layers visualizes volatility around the MA, guiding traders on potential support and resistance zones.

At the end, these pieces merge into a single indicator that detects statistically significant mean reversions while staying adaptive to real‑time volatility and momentum.

Calculations

1. Compute ALMA over the chosen MA length, offset, and sigma.

2. Approximate ZLMA by applying EMA to twice the price minus the price shifted by the MA length.

3. Calculate the composite moving average as the average of ALMA and ZLMA.

4. Compute raw RSI and smooth it with ALMA. Apply an EMA filter to raw RSI to reduce noise.

5. For both price and smoothed RSI, calculate the mean and standard deviation over the Z‑Score lookback period.

6. Compute Z‑Scores:

• z_price = (current price − composite MA mean) / standard deviation of price deviations

• z_rsi = (smoothed RSI − mean RSI) / standard deviation of RSI

7. Determine reversal conditions: both Z‑Scores exceed their thresholds in the same direction, RSI EMA is in oversold/overbought zones (below 40 or above 60), and price movement confirms directionality.

8. Compute signal strength as the sum of the absolute Z‑Scores, then classify into weak, medium, or strong.

9. Calculate ATR over the chosen period and multiply by layer multipliers to form shadow widths.

10.Derive slope over the chosen slope length and color the MA line and bars based on direction, optionally smoothing color transitions via EMA on RGB channels.

How this indicator actually works

1. The script begins by smoothing price data with ALMA and approximating a zero‑lag EMA, then averaging them for the main MA.

2. RSI is calculated, then smoothed and filtered.

3. Using a rolling window, the script computes statistical measures for both price deviations and RSI.

4. Z‑Scores tell how far current values lie from their recent norms.

5. When both Z‑Scores cross configured thresholds and momentum conditions align, reversal signals are flagged.

6. Signals are drawn with size and color reflecting strength.

7. The MA is plotted with dynamic coloring; ATR shadows are layered beneath to show volatility envelopes.

8. Bars can be colored to match MA slope, reinforcing trend context.

9. Alert conditions allow automated notifications when signals occur.

Inputs

Main Length: Main MA Length. Sets the period for ALMA and ZLMA.

RSI Length: RSI Length. Determines the lookback for momentum calculations.

Z-Score Lookback: Z‑Score Lookback. Window for mean and standard deviation computations.

Price Z-Score Threshold: Price Z‑Score Threshold. Minimum deviation required for price.

RSI Z-Score threshold: RSI Z‑Score Threshold. Minimum deviation required for momentum.

RSI EMA Filter Length: RSI EMA Filter Length. Smooths raw RSI readings.

ALMA Offset: Controls ALMA’s focal point in the window.

ALMA Sigma: Adjusts ALMA’s smoothing strength.

Show Reversal Signals : Toggle to display reversal signal markers.

Slope Sensitivity: Length for slope calculation. Higher values smooth slope changes.

Use Bar Coloring: Enables coloring of price bars based on MA slope.

Show MA Shadow: Toggle for ATR‑based shadow bands.

Shadow Layer Count: Number of shadow layers (1–4).

Base Shadow ATR Multiplier: Multiplier for ATR when sizing the first band.

Smooth Color Transitions (boolean): Smooths RGB transitions for line and shadows, if enabled.

ATR Length for Shadow: ATR Period for computing volatility bands.

Use Dynamic Signal Size: Toggles dynamic scaling of reversal symbols.

Features

Moving average smoothing: a hybrid of ALMA and Zero‑Lag EMA that balances responsiveness and noise reduction.

Slope coloring: MA line and optionally price bars change color based on trend direction; color transitions can be smoothed for visual continuity.

ATR shadow layers: translucent bands around the MA show volatility envelopes; up to four concentric layers help gauge distance from normal price swings.

Dual Z‑Score filters: price and momentum must both deviate beyond thresholds to trigger signals, reducing false positives.

Dynamic signal sizing: reversal markers scale in size based on the combined Z‑Score magnitude, making stronger signals more prominent.

Adaptive visuals: optional smoothing of color channels creates gradient effects on lines and fills for a polished look.

Alert conditions: built‑in buy and sell alerts notify traders when reversal setups emerge.

Conclusion

Uptrick: Dynamic Z‑Score Deviation delivers a structured way to identify short‑term reversal opportunities by fusing statistical rigor with adaptive smoothing and clear visual cues. It guides traders through multiple confirmation layers—hybrid moving average, dual Z‑Score analysis, momentum filtering, and volatility envelopes—while keeping the chart clean and informative.

Disclaimer

This indicator is provided for informational and educational purposes only and does not constitute financial advice. Trading carries risk and may not be suitable for all participants. Past performance is not indicative of future results. Always do your own analysis and risk management before making trading decisions.

Institutional MACD (Z-Score Edition) [VolumeVigilante]📈 Institutional MACD (Z-Score Edition) — Professional-Grade Momentum Signal

This is not your average MACD .

The Institutional MACD (Z-Score Edition) is a statistically enhanced momentum tool, purpose-built for serious traders and breakout hunters . By applying Z-Score normalization to the classic MACD structure, this indicator uncovers statistically significant momentum shifts , enabling cleaner reads on price extremes, trend continuation, and potential reversals.

💡 Why It Matters

The classic MACD is powerful — but raw momentum values can be noisy and relative , especially on volatile assets like BTC/USD . By transforming the MACD line, signal line, and histogram into Z-scores , we anchor these signals in statistical context . This makes the Institutional MACD:

✔️ Timeframe-agnostic and asset-normalized

✔️ Ideal for spotting true breakouts , not false flags

✔️ A reliable tool for detecting momentum divergence and exhaustion

🧪 Key Features

✅ Full Z-Score normalization (MACD, Signal, Histogram)

✅ Highlighted ±Z threshold bands for overbought/oversold zones

✅ Customizable histogram coloring for visual momentum shifts

✅ Built-in alerts for zero-crosses and Z-threshold breaks

✅ Clean overlay with optional display toggles

🔁 Strategy Tip: Mean Reversion Signals with Statistical Confidence

This indicator isn't just for spotting breakouts — it also shines as a mean reversion tool , thanks to its Z-Score normalization .

When the Z-Score histogram crosses beyond ±2, it marks a statistically significant deviation from the mean — often signaling that momentum is overstretched and the asset may be due for a pullback or reversal .

📌 How to use it:

Z > +2 → Price action is in overbought territory. Watch for exhaustion or short setups.

Z < -2 → Momentum is deeply oversold. Look for reversal confirmation or long opportunities.

These zones often precede snap-back moves , especially in range-bound or corrective markets .

🎯 Combine Z-Score extremes with:

Candlestick confirmation

Support/resistance zones

Volume or price divergence

Other mean reversion tools (e.g., RSI, Bollinger Bands)

Unlike the raw MACD, this version delivers statistical thresholds , not guesswork — helping traders make decisions rooted in probability, not emotion.

📢 Trade Smart. Trade Vigilantly.

Published by VolumeVigilante

Institutional Quantum Momentum Impulse [BullByte]## Overview

The Institutional Quantum Momentum Impulse (IQMI) is a sophisticated momentum oscillator designed to detect institutional-level trend strength, volatility conditions, and market regime shifts. It combines multiple advanced technical concepts, including:

- Quantum Momentum Engine (Hilbert Transform + MACD Divergence + Stochastic Energy)

- Fractal Volatility Scoring (GARCH + Keltner-based volatility)

- Dynamic Adaptive Bands (Self-adjusting thresholds based on efficiency)

- Market Phase Detection (Volume + Momentum alignment)

- Liquidity & Cumulative Delta Analysis

The indicator provides a Z-score normalized momentum reading, making it ideal for mean-reversion and trend-following strategies.

---

## Key Features

### 1. Quantum Momentum Core

- Combines Hilbert Transform, MACD divergence, and Stochastic Energy into a single composite momentum score.

- Normalized using a Z-score for statistical significance.

- Smoothed with EMA/WMA/HMA for cleaner signals.

### 2. Dynamic Adaptive Bands

- Upper/Lower bands adjust based on volatility and efficiency ratio .

- Acts as overbought/oversold zones when momentum reaches extremes.

### 3. Market Phase Detection

- Identifies bullish , bearish , or neutral phases using:

- Volume-Weighted MA alignment

- Fractal momentum extremes

### 4. Volatility & Liquidity Filters

- Fractal Volatility Score (0-100 scale) shows market instability.

- Liquidity Check ensures trades are taken in favorable spread conditions.

### 5. Dashboard & Visuals

- Real-time dashboard with key metrics:

- Momentum strength, volatility, efficiency, cumulative delta, and market regime.

- Gradient coloring for intuitive momentum visualization .

---

## Best Trade Setups

### 1. Trend-Following Entries

- Signal :

- QM crosses above zero + Market Phase = Bullish + ADX > 25

- Cumulative Delta rising (buying pressure)

- Confirmation :

- Efficiency > 0.5 (strong momentum quality)

- Liquidity = High (tight spreads)

### 2. Mean-Reversion Entries

- Signal :

- QM touches upper band + Volatility expanding

- Market Regime = Ranging (ADX < 25)

- Confirmation :

- Efficiency < 0.3 (weak momentum follow-through)

- Cumulative Delta divergence (price high but delta declining)

### 3. Breakout Confirmation

- Signal :

- QM holds above zero after a pullback

- Market Phase shifts to Bullish/Bearish

- Confirmation :

- Volatility rising (expansion phase)

- Liquidity remains high

---

## Recommended Timeframes

- Intraday (5M - 1H): Works well for scalping & swing trades.

- Swing Trading (4H - Daily): Best for trend-following setups.

- Position Trading (Weekly+): Useful for macro trend confirmation.

---

## Input Customization

- Resonance Factor (1.0 - 3.618 ): Adjusts MACD divergence sensitivity.

- Entropy Filter (0.382/0.50/0.618) : Controls stochastic damping.

- Smoothing Type (EMA/WMA/HMA) : Changes momentum responsiveness.

- Normalization Period : Adjusts Z-score lookback.

---

The IQMI is a professional-grade momentum indicator that combines institutional-level concepts into a single, easy-to-read oscillator. It works across all markets (stocks, forex, crypto) and is ideal for traders who want:

✅ Early trend detection

✅ Volatility-adjusted signals

✅ Institutional liquidity insights

✅ Clear dashboard for quick analysis

Try it on TradingView and enhance your trading edge! 🚀

Happy Trading!

- BullByte

Uptrick: Z-Score FlowOverview

Uptrick: Z-Score Flow is a technical indicator that integrates trend-sensitive momentum analysi s with mean-reversion logic derived from Z-Score calculations. Its primary objective is to identify market conditions where price has either stretched too far from its mean (overbought or oversold) or sits at a statistically “normal” range, and then cross-reference this observation with trend direction and RSI-based momentum signals. The result is a more contextual approach to trade entry and exit, emphasizing precision, clarity, and adaptability across varying market regimes.

Introduction

Financial instruments frequently transition between trending modes, where price extends strongly in one direction, and ranging modes, where price oscillates around a central value. A simple statistical measure like Z-Score can highlight price extremes by comparing the current price against its historical mean and standard deviation. However, such extremes alone can be misleading if the broader market structure is trending forcefully. Uptrick: Z-Score Flow aims to solve this gap by combining Z-Score with an exponential moving average (EMA) trend filter and a smoothed RSI momentum check, thus filtering out signals that contradict the prevailing market environment.

Purpose

The purpose of this script is to help traders pinpoint both mean-reversion opportunities and trend-based pullbacks in a way that is statistically grounded yet still mindful of overarching price action. By pairing Z-Score thresholds with supportive conditions, the script reduces the likelihood of acting on random price spikes or dips and instead focuses on movements that are significant within both historical and current contextual frameworks.

Originality and Uniquness

Layered Signal Verification: Signals require the fulfillment of multiple layers (Z-Score extreme, EMA trend bias, and RSI momentum posture) rather than merely breaching a statistical threshold.

RSI Zone Lockout: Once RSI enters an overbought/oversold zone and triggers a signal, the script locks out subsequent signals until RSI recovers above or below those zones, limiting back-to-back triggers.

Controlled Cooldown: A dedicated cooldown mechanic ensures that the script waits a specified number of bars before issuing a new signal in the opposite direction.

Gradient-Based Visualization: Distinct gradient fills between price and the Z-Mean line enhance readability, showing at a glance whether price is trading above or below its statistical average.

Comprehensive Metrics Panel: An optional on-chart table summarizes the Z-Score’s key metrics, streamlining the process of verifying current statistical extremes, mean levels, and momentum directions.

Why these indicators were merged

Z-Score measurements excel at identifying when price deviates from its mean, but they do not intrinsically reveal whether the market’s trajectory supports a reversion or if price might continue along its trend. The EMA, commonly used for spotting trend directions, offers valuable insight into whether price is predominantly ascending or descending. However, relying solely on a trend filter overlooks the intensity of price moves. RSI then adds a dedicated measure of momentum, helping confirm if the market’s energy aligns with a potential reversal (for example, price is statistically low but RSI suggests looming upward momentum). By uniting these three lenses—Z-Score for statistical context, EMA for trend direction, and RSI for momentum force—the script offers a more comprehensive and adaptable system, aiming to avoid false positives caused by focusing on just one aspect of price behavior.

Calculations

The core calculation begins with a simple moving average (SMA) of price over zLen bars, referred to as the basis. Next, the script computes the standard deviation of price over the same window. Dividing the difference between the current price and the basis by this standard deviation produces the Z-Score, indicating how many standard deviations the price is from its mean. A positive Z-Score reveals price is above its average; a negative reading indicates the opposite.

To detect overall market direction, the script calculates an exponential moving average (emaTrend) over emaTrendLen bars. If price is above this EMA, the script deems the market bullish; if below, it’s considered bearish. For momentum confirmation, the script computes a standard RSI over rsiLen bars, then applies a smoothing EMA over rsiEmaLen bars. This smoothed RSI (rsiEma) is monitored for both its absolute level (oversold or overbought) and its slope (the difference between the current and previous value). Finally, slopeIndex determines how many bars back the script compares the basis to check whether the Z-Mean line is generally rising, falling, or flat, which then informs the coloring scheme on the chart.

Calculations and Rational

Simple Moving Average for Baseline: An SMA is used for the core mean because it places equal weight on each bar in the lookback period. This helps maintain a straightforward interpretation of overbought or oversold conditions in the context of a uniform historical average.

Standard Deviation for Volatility: Standard deviation measures the variability of the data around the mean. By dividing price’s difference from the mean by this value, the Z-Score can highlight whether price is unusually stretched given typical volatility.

Exponential Moving Average for Trend: Unlike an SMA, an EMA places more emphasis on recent data, reacting quicker to new price developments. This quicker response helps the script promptly identify trend shifts, which can be crucial for filtering out signals that go against a strong directional move.

RSI for Momentum Confirmation: RSI is an oscillator that gauges price movement strength by comparing average gains to average losses over a set period. By further smoothing this RSI with another EMA, short-lived oscillations become less influential, making signals more robust.

SlopeIndex for Slope-Based Coloring: To clarify whether the market’s central tendency is rising or falling, the script compares the basis now to its level slopeIndex bars ago. A higher current reading indicates an upward slope; a lower reading, a downward slope; and similar readings, a flat slope. This is visually represented on the chart, providing an immediate sense of the directionality.

Inputs

zLen (Z-Score Period)

Specifies how many bars to include for computing the SMA and standard deviation that form the basis of the Z-Score calculation. Larger values produce smoother but slower signals; smaller values catch quick changes but may generate noise.

emaTrendLen (EMA Trend Filter)

Sets the length of the EMA used to detect the market’s primary direction. This is pivotal for distinguishing whether signals should be considered (price aligning with an uptrend or downtrend) or filtered out.

rsiLen (RSI Length)

Defines the window for the initial RSI calculation. This RSI, when combined with the subsequent smoothing EMA, forms the foundation for momentum-based signal confirmations.

rsiEmaLen (EMA of RSI Period)

Applies an exponential moving average over the RSI readings for additional smoothing. This step helps mitigate rapid RSI fluctuations that might otherwise produce whipsaw signals.

zBuyLevel (Z-Score Buy Threshold)

Determines how negative the Z-Score must be for the script to consider a potential oversold signal. If the Z-Score dives below this threshold (and other criteria are met), a buy signal is generated.

zSellLevel (Z-Score Sell Threshold)

Determines how positive the Z-Score must be for a potential overbought signal. If the Z-Score surpasses this threshold (and other checks are satisfied), a sell signal is generated.

cooldownBars (Cooldown (Bars))

Enforces a bar-based delay between opposite signals. Once a buy signal has fired, the script must wait the specified number of bars before registering a new sell signal, and vice versa.

slopeIndex (Slope Sensitivity (Bars))

Specifies how many bars back the script compares the current basis for slope coloration. A bigger slopeIndex highlights larger directional trends, while a smaller number emphasizes shorter-term shifts.

showMeanLine (Show Z-Score Mean Line)

Enables or disables the plotting of the Z-Mean and its slope-based coloring. Traders who prefer minimal chart clutter may turn this off while still retaining signals.

Features

Statistical Core (Z-Score Detection):

This feature computes the Z-Score by taking the difference between the current price and the basis (SMA) and dividing by the standard deviation. In effect, it translates price fluctuations into a standardized measure that reveals how significant a move is relative to the typical variation seen over the lookback. When the Z-Score crosses predefined thresholds (zBuyLevel for oversold and zSellLevel for overbought), it signals that price could be at an extreme.

How It Works: On each bar, the script updates the SMA and standard deviation. The Z-Score is then refreshed accordingly. Traders can interpret particularly large negative or positive Z-Score values as scenarios where price is abnormally low or high.

EMA Trend Filter:

An EMA over emaTrendLen bars is used to classify the market as bullish if the price is above it and bearish if the price is below it. This classification is applied to the Z-Score signals, accepting them only when they align with the broader price direction.

How It Works: If the script detects a Z-Score below zBuyLevel, it further checks if price is actually in a downtrend (below EMA) before issuing a buy signal. This might seem counterintuitive, but a “downtrend” environment plus an oversold reading often signals a potential bounce or a mean-reversion play. Conversely, for sell signals, the script checks if the market is in an uptrend first. If it is, an overbought reading aligns with potential profit-taking.

RSI Momentum Confirmation with Oversold/Overbought Lockout:

RSI is calculated over rsiLen, then smoothed by an EMA over rsiEmaLen. If this smoothed RSI dips below a certain threshold (for example, 30) and then begins to slope upward, the indicator treats it as a potential sign of recovering momentum. Similarly, if RSI climbs above a certain threshold (for instance, 70) and starts to slope downward, that suggests dwindling momentum. Additionally, once RSI is in these zones, the indicator locks out repetitive signals until RSI fully exits and re-enters those extreme territories.

How It Works: Each bar, the script measures whether RSI has dropped below the oversold threshold (like 30) and has a positive slope. If it does, the buy side is considered “unlocked.” For sell signals, RSI must exceed an overbought threshold (70) and slope downward. The combination of threshold and slope helps confirm that a reversal is genuinely in progress instead of issuing signals while momentum remains weak or stuck in extremes.

Cooldown Mechanism:

The script features a custom bar-based cooldown that prevents issuing new signals in the opposite direction immediately after one is triggered. This helps avoid whipsaw situations where the market quickly flips from oversold to overbought or vice versa.

How It Works: When a buy signal fires, the indicator notes the bar index. If the Z-Score and RSI conditions later suggest a sell, the script compares the current bar index to the last buy signal’s bar index. If the difference is within cooldownBars, the signal is disallowed. This ensures a predefined “quiet period” before switching signals.

Slope-Based Coloring (Z-Mean Line and Shadow):

The script compares the current basis value to its value slopeIndex bars ago. A higher reading now indicates a generally upward slope, while a lower reading indicates a downward slope. The script then shades the Z-Mean line in a corresponding bullish or bearish color, or remains neutral if little change is detected.

How It Works: This slope calculation is refreshingly straightforward: basis – basis . If the result is positive, the line is colored bullish; if negative, it is colored bearish; if approximately zero, it remains neutral. This provides a quick visual cue of the medium-term directional bias.

Gradient Overlays:

With gradient fills, the script highlights where price stands in relation to the Z-Mean. When price is above the basis, a purple-shaded region is painted, visually indicating a “bearish zone” for potential overbought conditions. When price is below, a teal-like overlay is used, suggesting a “bullish zone” for potential oversold conditions.

How It Works: Each bar, the script checks if price is above or below the basis. It then applies a fill between close and basis, using distinct colors to show whether the market is trading above or below its mean. This creates an immediate sense of how extended the market might be.

Buy and Sell Labels (with Alerts):

When a legitimate buy or sell condition passes every check (Z-Score threshold, EMA trend alignment, RSI gating, and cooldown clearance), the script plots a corresponding label directly on the chart. It also fires an alert (if alerts are set up), making it convenient for traders who want timely notifications.

How It Works: If rawBuy or rawSell conditions are met (refined by RSI, EMA trend, and cooldown constraints), the script calls the respective plot function to paint an arrow label on the chart. Alerts are triggered simultaneously, carrying easily recognizable messages.

Metrics Table: