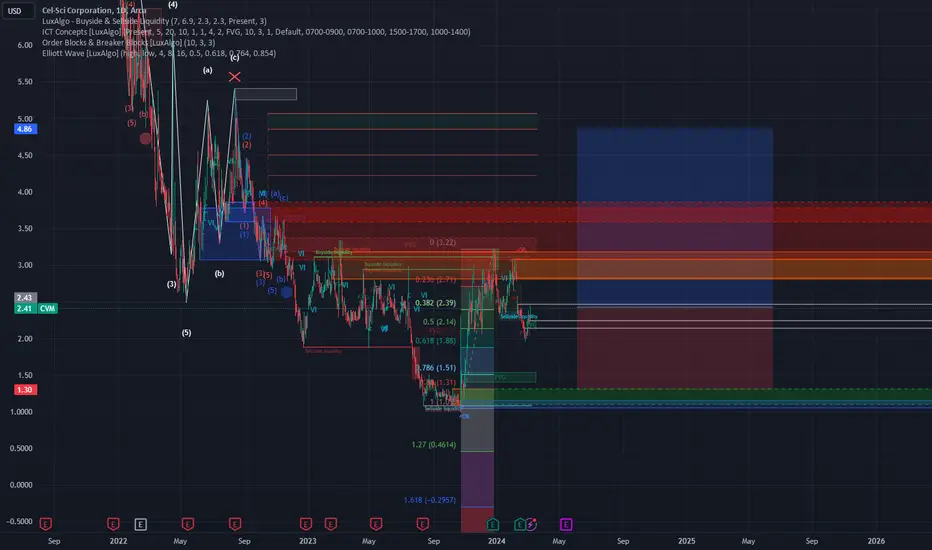

This Stock Has the Potencial to DoubleHere I present to you exclusively an undervalued share that few analysts have on their radar. The Cel-Sci share has recovered significantly from its lows reached in 2023 and formed a wave 1. There has been a correction, so we can expect big upward waves 3 and 5 soon. From an option sentiment perspective, the stock is overly bearish. However, an overly negative put-call ratio is a contra-indicator, so we are bullish on the stock. We expect Cel-Sci's share price to double in the coming months. About the company:

Cel-Sci Corporation, also known as CVM, is indeed an American biotechnology company specializing in the research and development of immunotherapy products for treating cancer, autoimmune diseases, and infectious diseases. The company is actively testing drugs in these areas of application.

Founded in Germany in 1983, Cel-Sci went public in the same year. Its shares are currently traded on the NYSE American and the Frankfurt Stock Exchange, among others.

CVM trade ideas

CVM1Y

RSI is trending down.

MFI is trending down.

-Both have reached a top.

5Y

RSI is trending up.

MFI is trending up.

-Both have bottomed.

ALL

RSI is reaching a bottom.

MFI is trending down.

There is a gap around $0.80 and $1.

Prediction: I think we will continue falling near the $0.80 and $1 range. Once RSI on the 1Y reaches a bottom it could be poised for an uptrend.

CVM; Trend Analysis with ASCO reviewDisclaimer

I am very invested in CVM, for a multitude of reasons, first as a scientist, second as an investor, third as my ego. I believe their recent clinical trial results are phenomenal, and illustrate it's potential as the pre-treatment for cancer in immuno-competent patients with appropriate genotypical and phenotypical screening. The clinical trial poster results as follows…

Safety results were not significantly different between treatment groups.

Leukocyte Interleukin, LI (MK) neoadjuvant immunotherapy did not add excess safety issues or TEAEs.

In the Randomized ITT population, early LI (MK) response decreases mortality and is prognostic/predictive of OS.

ITT Lower Risk LI (MK)+CIZ+SOC absolute OS advantage over SOC alone (Control) increased over time to 14.1% at 5-years; the 0.68 HR corresponds to a 47% prolongation of median survival, having a 46-month median OS advantage over SOC alone. The SCCHN population studied has been without any new therapy options in decades.

Much of this is a mix of science and legal speak, but my translations are as follows:

MK does not add safety issues

MK does not cause safety issues

MK response increases survival, and those that respond are more likely to survive longer

14.1% increased Survival at 5 years, this effect ramping up from 5% at 3 years, 9.5% at 4 years.

The big question that comes to mind after reading the poster is for an experiment: Identify the key oncogenic mutations and biomarkers for the individuals cancer, purify their antibodies before and after at various time points, prove that Multikine is specifically causing the increased survival long-term via immunological induction. This is a doable Phase 1b, proves Mechanism of action, and offers so much therapeutic profiling potential. Single-cell transcriptomics on the immune system profile before and after multikine at various time points would be the dream for future development, but it can only be done in humans because it is specifically confined to the limitations of species-homogenicity. Immune systems are so vast between person to person based on genetic SNPs, let alone species to species. The results wouldn't take years, ideally you'll see the specific changes early on and long-term survival is increased because of an immunological-booster versus greater initial tumour ablation - which the paper from the Phase 2 trial clearly shows a preference towards the former.

Still, there is data missing that I'd rather have to do more comparisons, and my general disdain for biostatisticians remains. There were a lot of ways to illustrate the study that would have made a better story, but I am guessing their FDA consultant favoured a narrow approach. As a Scientist, I have many questions at the molecular, genetic, and clinical level, but the results fit the initial hypothesis: Multikine is an immunotherapy that requires a working immune system, no surprises. Head and Neck cancer has been a therapeutic-resistant cancer, and a dive into some of the pathological and genetic traits of these tumours suggests why. If Multikine is enhancing the immune response, that would resound with the benefits in survival in lower-risk. I maintain that Cisplatin ruined half the study - i.e. the high-risk population, Cisplatin tears through everything, and immune cells are among the first to go as higher populating cells start suffering the most from poor DNA damage and checkpoint control pathways.

If I were an FDA investigator, I would be curious as to the patient drop-out rate, but I don't really know how much depth they would even get. I have spent countless hours going through the TCGA database as a researcher, I know how brutal Kaplan-Meier plots can be. Still, I want to know the full list of reasons for censoring data points. The key paragraph to read from the poster follows, with emphasis on key findings from the early response. As an FDA investigator, I would specifically look into this claim, and if it's true, I would get very excited.

In the as randomized ITT study population (n=923), the overall early response rate was 8.5% (45/529) for the combined LI (MK) treated groups ; the early response rates were 8.1% (32/395) for LI (MK)+CIZ+SOC and 9.7% (13/134) for LI (MK)+SOC. The early response rate was 0% (0/394) for SOC ; the difference between LI (MK) treated and SOC early response rate, for all patients as randomized, was highly significant (two-sided Fisher Exact test p=0.00000000001 ). The combined LI (MK) treated lower risk population had a 16% (34/212) early response rate and the LI (MK) treated higher risk population had an early response rate of 3.7% (10/269), while a 2.1% (1/48) response rate was noted in the LI (MK) treated subjects who had not been categorized to a risk group in the study. No early responses were observed in the SOC population irrespective of risk group .

At this point, it is safe to assume everyone has read the amazing news from the Rectal cancer trial, with an astounding 100% remission rate in a small-scale trial. The benefits of a trial like this, are the clinicians can really cherry-pick their patients on the front-end, which illustrates their Mechanism of Action in action. These therapies will have a long road ahead of them, but they do not exist in a vacuum. IL-6 and IL-12 are the same class of cytokine, I am just unsure which specific member of the family Cel-Sci has in the Multikine mix vs the recent. Again, I maintain that Multikine is likely the in the first generation of true immunotherapies, but with a ton of space to build out and upon. Cancer is not a single target or pathway disease, and therapies that are able to safely interact and cooperate are going to be key to increasing cure rates.

The next big catalysts are the full paper publication and the FDA clinical trial meeting. I expect other biotech/pharma analysts are pouring over the clinical trial results from ASCO, communicating with their team and investors. The abstract publication definitely caused an increase in price movement and action. My general hypothesis has been that the company has to fight an uphill battle versus the initial reaction of that phase 3 result, but the strong backup from ASCO result's will get digested favourably. The biggest catalyst will be FDA approval or rejection, but base case has and maintains approval based on clear clinical need and effect. The longer term bull case remains to be a path similar to Keytruda, as the drug is able to be tested in other reasonable cancer pathologies. Reasonably speaking, I could see numerous combinatorial studies with other immune therapies and initial tumour ablation therapies, especially as personalized cancer treatment becomes a larger model.

Trend Analysis suggests a multitude of possibilities in the short to medium term, with severe Macroeconomic constraints. This analyst does predict a recession, with very sticky inflation still to come. Biotech's will continue to hurt as interest rates increase simply because they are capital vacuums, and runways will continue to be tested across the board. However, CVM isn't stuck in that position for long, and Forward Cash Flows go from $0 to $$$$$ very quickly after clinical approvals. The market will decide on how much that ultimately ends up as, but CVM remains overweight and undervalued on profit models by large amounts. There are still warrants for purchase of shares at a few price levels, these price levels will likely continue to serve as areas of resistance, and support. How exactly the rest of this turbulent period plays out has dramatic effects on future price movement. FDA approval will remain key to massive price increases, but as the FDA meeting comes closer and closer, volume will increase as investors levy their bets. I continue to contend that this data is superior to anything Keytruda, or any of the other PD-L1 and PD-1 therapies have put out, especially in the face of Bristol-Meyer Squibb's recent failure, and the recent issues of TIGIT, and several other key immunotherapy drugs. Multikine is a multi-component formulation, stimulating multiple pathways in the immune response, and fine tuning and complementation will be key towards increasing efficacy. Furthermore, finer genotypic and phenotypic tumour profiling will greatly predict drug efficacy. However, the FDA remains fluid in position and ideology, offering favouritism towards illogical paths at times. Recent behaviours suggest an organization improving, especially as more clinicians come to see the benefits of therapeutic strategies coming out of Dana Farber and Memorial Sloan Kettering.

Final DISCLAIMER

This is in no way, shape or form, fluid and function, an analytical, qualitative or intelligent compte rendu. The function of this essay is the maddening diatribe of a curious mind, and how this one manages micro- and macro-economic data for a critical investigation into the micro- and macro-economic world. This text is not suitable for direct consumption, and should never be used as a primary or secondary source. The contents of this text are often illogical and offensive, and great care should be given to the reader's personal qualifications and senses. This text is delivered on TradingView, where the userbase is expected to have a level of financial and investigative understanding that would enable them to query appropriate thoughts and abdicate nonsense to the void. May whatever sovereign and omnipotent being you believe in, guide you through this.

www.businesswire.com

aacrjournals.org

www.ncbi.nlm.nih.gov

www.ncbi.nlm.nih.gov

pubmed.ncbi.nlm.nih.gov

www.nature.com

www.frontiersin.org

CVM BullishPrice tested 4 fibonacci levels to close just under the .78 level. In addition the MACD just crossed on the daily.

Looks like $12.21 may act as resistance, in which case we may see a retracement to the $11.80-$11.22 level.

Target: $13.01 short term. $14.26-$16.71 possible if it starts to squeez.

CVM and Multikine; Rating and Confidence ReaffirmedDisclaimer

I am long $CVM to the tune of X0,000 shares (and growing). I genuinely believe, as a scientist, biochemist, and analyst, in Cel-Sci Corporation's Multikine. This article serves as the thesis that $CVM deserves that I have given to other stocks. As always buy shares, options are dangerous and are often used to manipulate the stock.

Now that we have gotten through that:

This is in no way, shape or form, fluid and function, an analytical, qualitative or intelligent compte rendu. There is absolutely no financial advice here because the only financial advice I can give is to research, research, and research. The purpose of this analysis is to serve as an example of an investigation into a company's background, fundamentals, and assets through various lenses to determine if it is a good potential investment for you. The function of this write up is to serve as an educational resource for investors looking to understand how to find good investments. So read and learn some things about a company that cured cancer, yeah, the big C.

Thesis

It is upon rare occasion that one must look towards the past for moving into the future. Then certainly we are led here, a company starting it's preclinical scientific journey in the 1980s. A relic of a flare in a field few thought held value, immunology. Now, it is one of the fastest growing fields in medicine and science, where immunotherapies are quickly becoming the next generation of cancer treatments. Where others have come, and shown promise, Multikine has been here, for decades, toiling in the dark, fighting off bankruptcy, manipulative media and share attacks, and snobby scientists and doctors. Cel Sci Corp stand on victory, their quest coming to an end, and the market coming to the beginning of their own: How much is a drug that safely cures cancer worth?

Keytruda, itself an inhibitor of the immunoblockade, brings in nearly $15 billion in revenue per year over the last 3, with some estimates that this is early rather than late. Keytruda's therapeutic effects limited to an average of 6 to 8 months of survival time depending on cancer, Immunotherapies quickly became the sensation despite "limited" clinical benefits. Molecularly speaking- that is under the hood- Keytruda's true glory served as a limited toxic drug. Standard chemotherapeutics rely on a simple principle: do as much damage to quickly dividing cells, as much so to cancerous cells. This damage is not specific to the cancer cells: normal, happy, healthy cells get damaged too, often leading to them dying. But sometimes they don't die, they carry that damage on and then become a cancer cell later on. Sometimes that which doesn't kill you, makes you stronger, and sometimes it makes something inside you stronger that then kills you. Cisplatin, itself a platinum based drug that binds to the DNA, RNA and proteins in a cell causing them to clump up, get degraded, fixed if possible, leading to massive chromosomal damage (the genetic code). Normal cells take up the Cisplatin to a similar degree to the cancer cells (in fact cancer cells can make more of a special drug pump, then pump all of the drug out of the cancer cell to be consumed by the healthy cells, thus helping it grow), except normal cells have special checkpoints in place to look out for damaged DNA to fix it, or if unfixable, destroy it. 99.9% of the time, the damage gets fixed, or the cell dies, and 99.9% of those times where the cell continues on and becomes cancerous, the immune system finds it and kills it as it identifies it shouldn't be there. Cisplatin has an extremely high rate of cancer reoccurrence, keeping patients alive through cancer round 1, but often failing in round 2 or 3, but also being the cause of round 2 and 3.

Cel-Sci Corporation's Multikine, a mix of interleukins and cytokines used to communicate between the working immune system that an issue is there and needs to be addressed, showed excellent promise in Phase 1 and 2 clinical trials. However, clinical trials have been difficult and slow for a multitude of reasons; the immune system is extremely complex, and until recently there was no technology available to easily study the system in the true depth necessary. Pre-clinical research could not be done on standard laboratory animals as their immune systems are nearly completely defective. From there, a biochemical understanding of the nature of treatment itself impossible until recently, clinicians had little to no idea on what therapeutic response should look like, or what it could look like. Perhaps in some medieval notion, doctors might have considered activating the immune system to fight cancer would be similar to fighting a virus; shakes, shivers, fevers, sickness. When none of these effects, or even no side effects occurred, perhaps there was a considerable amount of white coats in large rooms shaking their heads assuming the project dead.

Through nearly 10 years of a Phase 3 in Head and Neck cancer, starting with a criminal and negligent CRO leading to a successful trial and large monetary recuperation, and ending with a stock-collapsing headline of " 14% increased 5 year survival over Surgery and Radiation alone, less than 10% increased 5 year survival over Surgery, Radiation and Cisplatin ". Perhaps in some small way, Cel-Sci Corporation never had a chance of an easy time, starting from the uphill battle through Ivy Tower elite scientists, ego-heavy medical doctors without a degree in immunology, manipulative short sellers and evil hedge funds reminiscent of the vile Michael Milken; through 3+ decades of pushing the entire medical field forward, paving the way through doctrine and dogma, leading to a breakthrough therapy with no significant side effects through hundreds of people, and an impressive long term survival rate in a cancer that has had no medical breakthroughs in just as long.

Previous articles by this author and others have suggested that the Cisplatin arm of head and neck cancer patients is likely at or below 62%, which is Multikine's 5 year survival topline result. However, the numbers drop from there, and the specifics of that population look even worse. Cisplatin has an extremely low disease free survival/cured rate (where cure is defined as 5 years without cancer), and high secondary tumour incidence. That isn't to say that if given a choice between death and Cisplatin by the oncologist, the patient should absolutely chose Cisplatin, but very soon, they won't have to. Oncologist's will be able to choose a treatment profile in waves, where the first wave is safe therapies, specifically those with low death/suffering rate, such as surgery, radiation, and perhaps a side effect free drug that activates the immune system leading to a long term immune response capable of suppressing the immuno-evasion of the tumour cells right through to 5+ years of healthy life. Patient's from the Phase 2 trial of Multikine had a significant shrinkage of tumour, composite loss of pain, regained freedom of movement in tongue, etc; the drug was an absolute success. In fact the muted response from the clinical results from the trial paper is astounding. While the world must wait for the Phase 3 results to be published in a peer-reviewed journal, a critical step in validating and diffusing the data, the door to the FDA is coming closer and closer. Within the next several weeks or months, a pre-BLA meeting is expected between the FDA and CVM, where they will discuss the next steps and review keynotes of the data organizing it for the final submission and drug review process through the hands of dozens of scientists and medical professionals. Here, the FDA will see as any scientific or medical eye will find, Multikine is a breakthrough drug that will revolutionize cancer treatments.

Emulating Keytruda's path from rich to uber-rich, Multikine will seek for, and gain, approval for Head and Neck cancer with an open label allowance for other indicated cancers. Keytruda went from seeking approval, to nearly complete market approval in a matter of 6 months. While Cel-Sci Corporation does not have the wealth and power to force such a keystone move on the FDA, following historical precedent and medical need, Multikine will be in cancer patients across the spectrum as long as they have a working immune system by the end of 2022, just as Keytruda was in the same position at the same time scale. There is nothing exclamatory or insane about this statement, it has been this way for every disease and every drug that has gone through the FDA; a standard of care exists, experimental drugs better than SOC come along, the new SOC is formed through years of main-stream drug use showing wide market agreement with the clinical trials. Even in Keytruda's own question, failure of all primary or secondary endpoints has not stopped it from getting added to the therapeutic regiment for nearly every cancer, and ultimate approval for said cancer by the FDA.

Multikine's lack of additional clinical response with Cisplatin was a scientific inevitability. Cisplatin damages fast growing cells, the immune system being one of the fastest. Cisplatin often leaves patient's immune system naïve, leading to a need for a geriatric round of childhood vaccines! However, the scientific team at Cel-Sci realized this pre-Phase 3, leading to the establishment of the clinical trial arm without Cisplatin. While bear's might call this part out as evidence of CVM's failure, it is specifically opposite. Cel-Sci Corporation's leadership strong-armed the FDA to allow this branch of the trial, and because of it, have illustrated multiple paramount issues;

Immunotherapies take a long time to work in cancer, but they do work.

Immunotherapies do not work with mainstream chemotherapeutics that have the potential to inhibit and mute their effects.

Cisplatin is a bad drug that kills people and is only used because sometimes it kills the cancer before killing the person.

In this thread, CVM's true long term worth comes in the clinical lessons learned, not just the lives saved. And Multikine does save lives. If only indicated for the current population, head and neck cancer without cisplatin treatment, an estimated 12,000 people a year will be saved by getting Multikine too. Financially speaking, that is a lot of dough. If given to all available patients in the 144,000 group and sitting at Keytruda costs per year of $150k, Multikine could see revenues of $21.6 billion within 3 years. Any deviation in patient population upwards, as is expected, could lead to the most economically impressive drug of all time, and a metric %&#@ of lives saved.

While the current price action is little more than the chaotic meandering of algorithms, market makers, and maleficent hedge funds trying to prevent a massive squeeze from decades of phantom shares being sold, the inevitable trajectory is upwards. This author will leave the curious investor's mind to wander through previous articles and historical acquisition deals of similar scope, but there has never been a drug with more active therapeutic potential than Multikine. When collective cancer research was losing it's mind over Keytruda/PD-L1/PD-1/CAR-T cells, etc, there was only pre-clinical evidence and all early clinical evidence was looking rough. Multikine is out of Phase 3s with a perfect safety record, a massive amount of therapeutic evidence showing a massive clinical benefit, 14% 5 year survival rate in Head and Neck cancer patients leading to a similar short term, and much better longer (>5yrs) term survival rates than Cisplatin. While the catalysts are in full scope for $CVM from today's $11, to a potential $X00, the most important element is this:

Fuck cancer.

Trading Beta

TradingView will enjoy my use of the term Beta with their new rock climbing theme.

The chart shows current price valuations across bear, bull and base case estimates.

From a basic standpoint, this author continues to buy shares, especially as the price continues to be pummeled by the banks and large hedge funds offloading their puts and getting in more calls. Ultimately, a short squeeze/retail interest/increased volume should yield a $50-75 bear price, where appropriate dissemination and understanding of the clinical data and therapeutic implications could lead to an initial bull run to $150-200 giving the company a market capitalization around $5-7 billion (a measly sum considering $OCGN's worth given vaccine uncertainty and $SAVA with pre-clinical data issues and a drug early on in a lengthy and competitive clinical process).

Reasonably speaking, the goal is to amass a large sum of shares, never sell, use leverage and margin to build up secondary positions as $CVM's long term success is guaranteed. Current and future short sellers will force smart moves, but appropriate risk management practices leave this as the primary goal.

Secondarily, amassing large quantities of shares and selling monthly covered calls at critical price points as a way to create sustaining, secondary income and a forward momentum/pressure on the stock promises some level of efficacy.

Tertiarily, options around impulse waves while keeping my own position stable and growing yields more favourable derivative outcomes. Cel-Sci Corporation no longer needs to be acquired to achieve maximum market capitalization, and in some ways, may best achieve shareholder value by utilizing their new manufacturing space to continue on their smaller scale, guaranteeing current investor access to a double digit billions in yearly revenue within 3-5 years.

Links to Previous articles

Links to other highly qualified articles

There are many more articles than this, I just tried to choose a few from the various mixed media sources. I absolutely encourage any investor to see what others have written on the matter, but do not, under any circumstance, believe any single person, including me, without doing your own research and confirming or denying any and every thing. It is absolutely imperative to double check, triple check any and everything.

www.cvmresearch.com

seekingalpha.com

www.sciencetimes.com

seekingalpha.com

finance.yahoo.com

biotechhealthx.com

Disclaimer

Thank you for reading, please review all links, articles, press briefings and scientific data. If ever any questions, please comment, message me, or find me on twitter.

Nice Long for CVM**SMALL ACCOUNT FRIENDLY PLAY**

Peep this insane chart!

**CVM**

Long above $12.50

Short below $11.22

$SPY $CVM

CVM; Breakout from bear pennant, prime for liftoffDisclaimer

General disclaimer here.

Short but sweet, we have sustained breakout from the bear pennant, we have a dwindling short pool (460k as of today borrowable from Fidelity, down from ~600k on Monday).

Less kick in the shorts, and they have until the 20th of this month to sustain the price channel and try to get it under 7.5.

Meanwhile, more and more groups are buying up shares in small amounts, likely on the back of bigger entities buying up, as State Street increased their position on the drop from $25.

We are only a few weeks away from a catalyst with the pre-BLA meeting, pushed by more and more FDA breakthrough news.

This is a great time to look for an entry on shares.

If you buy options, a good rule I use is 90-10. Only use 10% of funds on the options, that way if they go south, you are still likely to end up green on the overall trade.

With that said, we have no ceiling as the drop from 26 was abberative manipulation, we have a gamma squeeze lining up from $9 and into the $20s. Theoretical M&A prices are obscenely high, even conservative values at $5 billion would give this a x15 multiple.

Have fun y'all, always be safe, and please do your own research to verify. And always ask questions!

whalewisdom.com

CVM; Possible break of pennant into Gamma SqueezeDisclaimer

Not financial advice, blah blah blah.

Looking towards the end of current pennant into a gamma squeeze...

Options for 8/20 look like a massive gamma at 10 possible, with another big jump at 12.5 and 15. We could see a massive impulse up with intense gamma pressure from ~1.2 million shares in calls at 10, and another ~700-800k between now and 20.

All that with a massive short volume with a tiny float as is. State Street bought a ton more on the dive from $25, could be seeing institutional investors be buying up for the inevitable FDA approval into acquisition.

CVM; An Open Letter for a Large InvestorThis is an open letter to all large institutional investors with significant biotechnology/pharmaceutical experience.

The Company

Cel Sci Corp is a small, Immunology based biotech with a small pipeline outside of Multikine.

41 million shares outstanding with only State Street, BlackRock and Vanguard having ~5% stakes.

Extremely oversold with massive short shares outstanding and a significant presence keeping the price down, meaning they will short sell into a large ownership percent (as they already have done with State Street).

Theoretical end market capitalization of $15+ billion, possibility for setting record; No need to rely on acquisition, company can be shifted towards manufacturing and sales while keeping research pipeline in place as manufacturing facility already built and owned by company.

Multikine

Mix of cytokines and interleukins in a proprietary mix that is injected into primary and secondary tumour sites to activate the immune system, capable of activating through some form of immunoblockade, but plenty of room for advancement with existing and next wave immunoblockade inhibitors.

No adverse reactions with drug.

Given pre-surgery.

Nothing unique to Head and Neck Cancer, thus creating a possible market in all solid tumours; metastatic cancers unknown, but possible depending on immune cells activated, possible mechanism similar to "cancer vaccines", but with self-made antigens.

Massive market with possible repeat dosing, likely route to becoming SOC or routine additional medicine to all existing cancer therapeutic strategies.

Cures cancer and saves lives (increased survival >5 years over existing surgery+radiation, likely better effect over Cisplatin meaning less cisplatin use as frontline).

Best Theoretical Plan

Calls are dirt cheap, and all strike prices are going to be in the money post-catalyst (either FDA news or large scale investor, aka you).

Buy all the calls, buy batches of shares, 10k in size with time to cool between cycles as shorts will continue to try to suppress, thinking small scale investor is moving in. As price catalyzes, decrease share buying frequency to save money for the calls. Could easily end with >5% ownership, allowing more power in setting the future of CVM, either negotiating a higher acquisition price, or steering it towards becoming its own Pharmaceutical.

Why now?

Market is screwy, everyone is holding their breath waiting for this bomb, and the ending outcome is impossible to know 100%. Certain "safe" stocks are no longer safe, and the market is prone to a major shakeup everywhere. However, CVM is dirt cheap, but a safe bet. Cures for cancer are going to be at the head of hyperinflation, it is valuable forever. The drug cannot be outclassed by the "next wave" as the next wave of interleukin and cytokine therapies are pieces of Multikine, and any future medication that tears down the immunoblockade of tumours will only make Multikine work better.

This might just be the best inflation hedge right now, along with being sorely undervalued.

Disclaimer

I am not a financial anything, I am a biochemist/cancer researcher looking to live an easier life, and become an "activist investor".

This is a semi-anonymous sales pitch of a drug I am invested in, and believe will save a lot of lives from the horrors of cancer, and chemotherapy. I am available and willing to discuss this at any length in any details necessary, and have written several pieces on CVM.

Not financial advice, I don't know the future, and any interested party should perform their own due diligence before investing a single penny.

CVM; A brief breakdown and review of the crazy weekDisclaimer

Not financial advice, I literally wrote that gold is worthless if everyone just decides it to be so.

However, I put some effort into showing what I see what I look at the action. Everything is in the picture. TradingView fix your shit so I could have done this better.

Never think the shorts have to cover, Freddie Mac and Fannie Mae are proof of that, so if you enter into a fight, always be prepared to lose it.

Sometimes the most striking pattern is the one that shouldn't be there.

CVM; A Win for Medicine, a Death Sentence for Cancer and shortsDISCLAIMER

I am financially invested in this stock, I have 4200 shares, and a considerable amount of calls for an unspecified date and amount. So yes, I, in a very big way, am selling you. I financially benefit if you, the investigative reader, buy CVM shares or, very possibly, calls. That means that this is not financial advice, this is a sales pitch, so if you don't think you can separate pitch from information, avoid this article. I have been apprehensive on writing this article as I accept my bias, and while I will present the following analysis of the study results, and possible implications, I am extremely biased and my ability to make a rational decision could 100% be compromised. What I present is my best explanation of the trial results, what I believe to be occurring to the price, and some of the scenarios Multikine could play out.

Now that we have gotten through that; This is in no way, shape or form, fluid and function, an analytical, qualitative or intelligent compte rendu. There is absolutely no financial advice here because the only financial advice I can give is to research, research, and research. The purpose of this analysis is to serve as an example of an investigation into a company's background, fundamentals, and assets through various lenses to determine if it is a good potential investment for you. The function of this write up is to serve as an educational resource for investors looking to understand how to find good investments. So read and learn some things about a company that cured cancer, yeah, the big C.

Thesis -Clinical Analysis

www.businesswire.com

I made this very basic figure: twitter.com

Big question is which treatment would you ask for?

The hard line is a 14% increased 5 year survival in Head and Neck cancer patients with a solid tumour being treated with Multikine as opposed to the current standard of care(SOC). All without a single safety issue, meaning it wasn't making patients sick, and as it was given 3 weeks before surgery and radiation, there was plenty of time for the immune system to go into hyperdrive mode and present serious issues.

I know I write a metric $#%@ ton of words, but y'all, I try and always let the data do the work. This is as pretty as it gets in my shoes. At the end of the day, there are no sub-statistics that matter, because in every single patient population that got Multikine, there was an increase in survival. CIZ is a weird little multivitamin that has been found to boost a ton of drugs' effects in the clinic for completely unknown reasons, or at least they were unknown last time I checked, but it is more designed than developed, but it legitimately does some incredible things. My hypothesis is that the mix helps reduce oxidative stress, which isn't a major issue for normal people walking around, which is why it is never found to have an effect on its own in any clinical setting, but it does seem to help in these various trials. This is a little too scientific, but oxidative stress is turning out to be the number one pathway in disease and just general cellular maintenance. I actively work on this scientifically, so there is a lot of contentious hypothesizing, but I am finding that oxidative stress would have been a relatively simple evolutionary step to take early on in macro-cellular organisms, but humans have done everything except. One of the major issues that is rarely thought of in a scientific lab setting is the oxidative stress of the environment caused by the massive amount of cellular death from therapeutic death of cancer cells. Sometimes killing the cancer too fast can overload the bodies ability to dispose of the dead cells, and cause major systemic issues and death. Yeah, sometimes killing cancer can just kill the patient because they are too weak to handle getting rid of all the dead tissue in them. No, this is not an easy task, but damn if we don’t keep trying. Also oxidative stress and inflammation are very linked!

Cisplatin is a toxic drug, meaning it is bad for you. The only reason you take it is if there is something worse for you that it might kill first. This is one of those situations where my background as a biochemist and cancer research gives me a leg up on the average investor, I have personally used cisplatin in experiments on primary human cells testing cancer-genesis with various DNA damaging agents. While I can't give those results to you, I can summarize it as yeah Cisplatin is pretty freaking awful, and it should only ever be used if there is nothing else.

Enter the reasoning for going after Head and Neck cancer; 6% of all cancer diagnoses per year (meaning big bucks) + no new treatment approved in over 2 decades + orphan drug designation from FDA making it a little easier to file the paperwork. This point needs to be emphasized hard here, there is nothing unique to head and neck cancer that makes Multikine be specific to it. CVM don't intend on applying for FDA approval for a small subset of Head and Neck cancer patients and biting the bullet on a smaller population pool. CVM are going after FDA approval for that small pool with immediate open label use. I will testify before a court of law, I would formally request Multikine as treatment if I were diagnosed with cancer tomorrow. I am very, very, very excited for Multikine to get to the clinic, this is the game changer that we have been waiting for and it is killing me that we are not celebrating this one. Fuck the stock price, can we get a round of fucking beers for a god damn cure for cancer.

This is the only important line from the release:

In addition, as the OS results for the lower risk of recurrence patients (no chemotherapy) are significant (two-sided p=0.0236, HR=0.68) and the effect is robust, durable and increasing over time, CEL-SCI plans to seek FDA approval for Multikine cancer immunotherapy in this underserved patient population.

OS

-overall survival- overall survival benefit being increased percent of people who survived from Multikine- percent more living people thanks to Multikine

lower risk of recurrence patient

- patients with a tumour grade of Head and Neck cancer deemed to be low risk of metastasis and coming back post-therapy

significant two-sided p=0.0236

-essentially boils down to could only happen by chance once in 42.4 times, meaning the difference in survival in the Multikine population is in fact, not simple chance, but actual clinical correlation/causation.

HR=.68

-HR means Hazard Ratio, is a direct ratio of probably of death. A HR of .68 means that for every singular patient who dies from the Surgery+Radiation arm, only .68 people die from the Multikine+Surgery+Radiation arm. Lower the HR, better the outcome

The effect is robust, durable and increasing over time

-I wouldn't know what that meant without them explaining that the overall survival advantage increases past 5 years. Where cured of cancer is defined as 5 years without remittance, Multikine is curing cancer. Of course this is hearsay until we see the statistic results ourselves, but I would hesitate doubting a company that could be crushed if they didn't back that up with real numbers.

Now, the bigger picture of the trial:

twitter.com

To put it bluntly, Multikine and Cisplatin don't work well together. As of right now, we have no idea if Cisplatin + Multikine has an overall survival 5 year rate of 9.5%, or an overall survival 5 year rate of -100%. My personal theory is that Cisplatin is going to destroy any effect that Multikine had on the system. Multikine is injected into the primary and secondary tumour sites 3 weeks pre-surgery followed by cisplatin and radiation or just radiation. Multikine has 3 weeks to do its job before surgery comes in, followed by radiation and Cisplatin. If Multikine didn't complete its job in 3 weeks 100%, as in there was any considerable amount of cancerous tissue remaining, Cisplatin is going to come in and do it's job, like it or not.

Cisplatin is like Chris Farley in a Little Coat to those tumour cells. To the few that manage to survive and make the EMT transition, or if the cancer stem cells survived (if those are even real, my guess is that this is a pool of cancer cells with an extremely fluid transcription profile that are kind of going back and forth between EMT-MET), cisplatin is ripping through their genome like a coffee bean grinder. I thought long and hard about the appropriate level of destruction I have seen from chromosomal spreads of cells on cisplatin, and coffee grinder feels pretty damn close sometimes. Cisplatin works by sticking to parts of the DNA in multiple places, making it impossible for the cell to make an exact replica of its genome, thus inducing mutations that could lead to death. Cisplatin causes more damage in quicker dividing cells; Cisplatin causes DNA damage, DNA damage that will be ignored and lead to fatal mitotic chromosomal splits/rearrangements, or DNA damage that will be addressed and fixed by healthy cells unless it is too great in which case they will choose to die rather than risk becoming cancerous later on.

Turns out some cells are just more selfish than others, they don't want to die. Cisplatin cancer reoccurrence is a very real thing that has been suppressed for a long time for a laundry list of reasons, namely being doctors and clinical scientists genuinely don't believe the patient is intelligent or informed enough to decide their own treatment course. That is putting it harshly, but essentially, Cisplatin was approved a long time ago and there are millions of people who have gotten millions of collective years on this planet thanks to Cisplatin. However, we are at the point where serious clinical work is being dragged down by Cisplatin because of the need to put every patient on it that can be on it regardless of theoretical alternatives. That and fighting with the FDA is pointless, they can just walk away and tell you go screw yourself. If CVM had any intention of having an arm from the get go of the total patient pool being only Multikine + Surgery + Radiation, I am 100% positive that 5 minutes talking with the most monotonous man in an off-white shirt with a terrible chemical structure tie, an FDA badge on a lanyard around their neck, sitting across from them as they awkwardly pull out their Worlds Best Federal Inspector of Medicine mug that they fill with their thermos with the Pfizer and AstraZeneca logo on it in the SHAPE OF A PILL, didn't just suck their will to live, he most certainly told them that every single cancer patient that can get the current SOC, will get SOC.

There is 1 silver lining element here that I would love to actually see datamined out (yes this is what datamining is); patients were not screened for fully functioning immune systems, meaning there were patients that could have been removed from the trial that were not as the drug would have had no way to cause a significant clinical effect. And that is where the real question begins with the Cisplatin + Multikine data. Was it because Cisplatin destroyed the immune system, thus stunting any long term immune response from Multikine, or is Multikine and Cisplatin not compatible on a more complex mechanistic teeter?

youtu.be

This is where I suggest CVM already knew Multikine wasn't going to work with Cisplatin. The way the trial was set up from the beginning illustrates they knew Cisplatin was never going to play nice.

I would like to point to Keytruda's first phase 3 results, and their FDA clearance history:

www.ncbi.nlm.nih.gov

Hint: Keytruda doesn't cure anyone. It just gives you more time, which is absolutely incredible and should not be taken from anyone. But it isn't a cure, it is a part of the cure .

www.drugs.com

June 30, 2014 - Keytruda is under regulatory review

September 4, 2014 - Keytruda is approved by the FDA

Keytruda gave people a few more months to live and it did it safely, without severe adverse effects. Keytruda was approved in 2 months.

Dispelling some of the fake newslines

The major reason this has taken over 30 years: THERE IS NO PRECLINICAL TEST TO TELL IF THIS THERAPY WORKS ASIDE FROM NON HUMAN PRIMAPES

It is invariably going to be tag line for short hedgefunds to stress "if it is so good, then why did it take 30+ years to get here". Unfortunately, the answer is the system. The system sucks, and the system has led to countless deaths because they are incredibly corrupt, inept and archaic. I am gifted by an interesting career in biotechs. I also have an interesting history in the financial markets. Part of this gives me insight into the crippling corruption in the CRO system, all the way to the approval system of the FDA, where countless lawsuits have proven correct that, yes, the FDA does accept bribes. CRO's are corrupt and disgusting monster corporations, anyone interested in a storied one could look no further than Parexel, which was getting bogged down with so many lawsuits and allegations that they had been abusing their position and purposefully not enrolling patients in small-scale biotech's clinical trials so their drugs never got through the long trials. There has been a number of interesting academic papers that have come out looking at the success/failure rate of drugs through clinical trials, and how prior to ~2012 something like 99% of drugs came out of large scale pharmaceutical companies. Unfortunately, as these papers are academic and the authors lacks a fundamental understanding and history of the system governing the clinical trial system, they fail to point out how many of these large scale pharmaceutical companies bribe CRO's, bribe the FDA, and work to spin extremely negative news in these clinical trials. Literally, these scumbags have gotten a hold of clinical study trial participant lists and called them all and fucking with the system by making them think they were going to die if they got the drug.

Want a sample study, look not further than our very own CVM: www.businesswire.com

There are no pre-clinical assays, especially not 30 years ago, that could give you the effects of a working immune system on a tumour. Mice do not have working immune systems, nor is there a guarantee any of the components in Multikine retain their appropriate pathway responses in any other species aside from humans. The major issue with a lot of diseases, like Alzheimer's, is the lack of a suitable test for drugs to know if they have an effect or not. It is not practical to screen drugs in patients (also not ethical), but the system has made it even more difficult to take drugs that work in human specific pre-clinical assays but do not have a suitable animal model to get into clinical trials. This has gotten better, but only very, very recently as the FDA has been slowly getting changed by a new wave of scientists and more-forward thinking government employees. Part of that leads us to the latest fiasco where an Alzheimer's drug without a clinical effect gets approved and cost ~$60k per year, which no way any nationally subsidized health insurance is going to pay. Part of that leads us to the countless fiascos of the countless drugs that have fallen through the cracks due to the system.

Fortunately, here we are, in 2021, with clinical trial results in hand and a much less suitable drug given the royal treatment as a role model.

cel-sci.com -page 6 for Head and neck cancer reasoning -pg 8 also good read

www.bloomberg.com -good discussion of Keytruda in this shareholders letter

Summary of Phase 3 FDA Trial

Multikine cures cancer in a specific subset of Head and Neck patients who did not get Cisplatin, which destroys the immune system, thus negating the effects of the drug.

Multikine had no negative medical events, meaning it was completely safe for EVERY SINGLE PATIENT WHO GOT IT.

Multikine activates the immune system against the tumour, similar to the way a vaccine allows your immune system to hunt down a virus or bacteria extra-well, but in a much more advanced way.

Theoretical Medical Relevancy

CVM's Multikine gets the immune system going red hot against solid tumours, but there is no study or data on how it would behave against a metastasized secondary tumour site, or against a metastatic cancer in general. I would not be surprised if Multikine is used in every single cancer given the patient has a working immune system. Furthermore, if Multikine is found to be safe in repeating doses, I can see maintenance Multikine being a serious clinical strategy.

Furthermore, CVM has preclinical studies going on Multikine in COVID infection, likely investigating more chronic viral infections as well. If Multikine is able to blanket activate the immune system, causing it to be super thorough, there is no reason not to consider it in any and every single infection scenario, viral and bacterial. I absolutely can see Guillain-Barre syndrome in a much broader population study, or other various auto-immune system issues, but part of me wants to say that this can be removed with dosages, and part of me is curious if the multi-pronged interleukin pathway activation from Multikine doesn't offer some sort of critical auto-immune system inhibitor. This is a completely novel therapy, and the immune system *typically* tries not to destroy its host. An interesting read on guillain-barre here (pubmed.ncbi.nlm.nih.gov) shows that some anti-interleukin 17 agents are possible treatments for this, meaning if negative side effects do happen, the fact that the alternative is cancer killing the patient, it is doubtful this hinders the drug, and that medically therapeutic options exist. Truthfully, most GBS events and auto-immune events are scary but transient. Interestingly, the interleukin pathway is crazy, and really still not fully known. Some of the interleukins inhibit each others pathways, some of these in very specific ways to modify the effects. This is just going to be one of the things that has to pop up in large scale clinical trials, especially as Multikine is tested in countless other therapies where the native immune system can be leveraged to do its job (i.e. every single infection).

Multikine getting FDA approval is absolute, to what scope is less so. Multikine will get open label use for cancer, but whether any research hospital chooses to bend that for study in other biologically relevant illnesses is another. With the Immune system being the flavour of the decade, I can only imagine how deep clinicians reach in for this one. Theoretically, Multikine would be effective in wounds, especially gunshot/knife wounds where there is a clear point of entry for infection. Multikine could be used as an emergency treatment used as an adjuvant therapy while the patient is stabilizing and wound closed. I am scientifically and medically excited for the uses of this drug.

Personally, I would love to see liver cancer treatment with Multikine, specifically liver because liver exosomes are particularly easy to purify from Urine, meaning you could monitor biomarkers routinely through the treatment effect, given they were present in urine exosomes of course. It is a little unethical and cruel to do, but getting some tumour samples would be amazing during the treatment as well. Ideally, Multikine is activating the immune system in the tumour region where the immune system is gathering epitopes against the mutated proteins on the tumour, or to simplify it a little, the tumour starts looking foreign to the immune system as it makes errors here and there and "new" proteins. These are hypothesized to be present and if the immune system could be activated against these, they would be able to hunt down the tumour cells at the primary site, but would be primed against any re-establishment of the tumour should a cancer stem cell survive or a metastasized colony is present elsewhere, the immune system should now be able to hunt them down and kill them everywhere. It would be very cool if we could take the immune system population from a patient treated with Multikine, and see if they are specifically targeting that patient's tumour versus other primary tumour samples.

Thesis - Price Action/Manipulation Strategy

thc-lab.net

This article is absolutely worth while in reading. I am sorry that this is the way the world works, I truly am. I believe that we are close to real change, but I think it's more thanks to Bitcoin than anyone wants to admit.

Looking at the short ratio reported day in, June 28th the short volume is monstrous, the way it is 50-50 makes me think this is a bunch of phantom shorts that were sold short before borrowed, with a hypothesis that the resurgent volume spike on the 30th might have been short hedgefunds recycling their shorts on the T+2 cycle. The fact they haven't yet from the June 30th intrigues me greatly, could be they found the way to bury them matched call:puts as there was a massive spike in far out of the money puts and options on the second half of the week. Alternatively, we could see a volume increase on a T+3 cycle, as is common in those looking to take the longest time to cover their previous short sales, willing to take a small fine if they get one on abusing the T+2 date, but still way ahead of the T+6 antics of Penson Financial(now Apex), and still even way more ahead of the T+21/T+35 FTD cycles that we can see repeating in the volume spikes (and congruent price spikes) over the past few months since the initial impulse to 40. Either way, should be a fun week.

www.nakedshortreport.com

Thesis- Price Target and Discovery

Fact, M&A's are red hot right now. Also Fact, the markets are really wonky right now. There is no guarantee on a blockbuster acquisition being possible even if the drug really is all that, just because the banks don't know how to stop being greedy. However, you cannot take the value out of a drug that cures cancer, so while an M&A could take a while to precipitate, the price action should reflect the massive increase in value of CVM, especially given the way the market has been valuing M&A targets previously such as QuantumScape, Tilray/Aphria, and countless others (wow the M&A market really has been red hot).

I have hit some intrinsic form of word limit, so I will keep it short. I see a short term market capitalization anywhere from the $1.5-3 billion range, where we could see extreme impulse ranges in the $10-30 billion market capitalization (the short squeeze trend has made these massive volatility channels outrageously hard to predict but fantastically enjoyable as a long). Truthfully, I could see an M&A deal panning out extremely quickly in the $5-10 billion range should a company rush quick while CVM is still learning to count 0's, but I would rather them take the time to get the full value where we could see the biotech records being broken, because again, this drug cures cancers.

TA is nuts to do right now just because the rules got changed so hard, and the way the price is so obviously being manipulated with the rhythmic ladder attacks and buybacks and the insane drops timed with margin shuffles. I wouldn't try and read the lines too much here, looking to hop in and out of channels as they come and go. Set a price target, set a loss limit, always do your research.

Check out pharmaintelligence.informa.com

Disclaimer

Thank you for reading this analysis. The sole purpose of these are to serve as an educational resource for any one to gain an understanding of what to research when deciding to make an investment. If there is any material in this analysis that you feel could be explained better, or in more detail, or even if you have just a little question, let me know! As I develop this skill, my aim is to expand the reach of these articles to cover more topics to a wider audience. Feedback helps me grow, so I am happy to read the comments.

For legal and ethical reasons, this is not financial advice, I really really really cannot stress that enough. Furthermore, I do own 4200 shares at an average price of $14 per share. This information is given due to European financial regulations, not as financial guidance. This information is only accurate as of the date of publication, July 6th, 2021. The original, and only version published by me is on Tradingview.com.

CVM; The End is Nigh and the Reaper is coming to collect someoneAs always, I am not an analyst in any shape, form or capacity, except for shapes, forms and capacities. I am a complete stranger on the internet spewing absolute nonsense, please double check everything I post (I will add links when I have enough reputation).

Ok, with the formalities out of the way, let us get down to business. I am going to follow procedure by not following procedure and talk about the play first. The science is cool behind this, and I can talk about it in a fun way down below, but I happen to think the deal needs to be addressed at the top.

The Play

The play is this: CVM has been around for 33 years and has this one, singular drug. This drug just went through phase 3 clinical trials in the US after 9.5 years. If the drug succeeds, then it is possible this goes full vertical in multiple ways. If the drug fails, expect a bankruptcy announcement and your stock to become worthless instantly. Every single dollar you put into it is gone, poof, nada. You want to be rich, you put your savings in 20k, the play went the wrong way and now you have 0. If this scares you, good, that is what this bet is. I am not putting my life savings on this, as I don't think anyone should ever do.

Sometime very soon, official phase 3 results will be announced for Multikine, CVM's golden egg. As an independent contractor is performing the final data analysis, CVM nor anyone else knows what the end results are going to be. However, in the trial end conditions, they decided to wait for 298 deaths (just about a third of the total trial participants). They finished entering people into the trial in 2016, announced in may 2020 the final death. In the setup, they set the standard order of care at 55% for 3 year survival. Assuming 55% survival at 3 years, the control group would have 443 deaths. On top of that, this suggests Multikine has a 70%+ survival rate (some of the deaths will be removed from the trial such as car accident, stabbing, shooting, deaths absolutely having nothing to do with the drug). That is a homerun hit. Pulling some stats straight from cancerresearchuk.org & cancer.gov; 5 year survival % for all head and neck cancers is 27-30%, with 4% of all cancers being head and neck. If this drug does 70% @ 3 year, this becomes the standard of care, and the best part is, this is an additive. Multikine is pre- everything else, so no matter what other drugs get developed, it is likely Multikine will remain SoC.

Multikine has a huge short interest. Turns out Citadel and Susquehana went to town shorting this baby lately, with their shorts alone being more than what most institutional investors own, with a total 15% short interest. Sure, this isn't massive, but the low float combined with a sudden buying demand for a biotech-king to be or an acquisition by a bigger fish, there is a solid base for momentum upwards. Again, with that, its always possible Citadel and Susquehana know insider information and are going to make a lot of money off of this. Remember this is the definition of risky.

Everyone of those small biotechs with the potential breakout hit, most of them don't even make it this far into phase 3, let alone on the precipice. CVM is going to get the news soon, and it will be the catalyst for the moment we wait years for on these biotech gambles.

The Science

Multikine is a combination of human cytokines, which are the chemicals and proteins in your body that activate the immune system. Each one has it's own pathway, with it's own effects and results, so combining them like this is somewhat novel for me. I kinda like it. I believe that the recent failures of PD-L1 and other immune checkpoint blockade programs have been a great indicator on how 1-leg strategies targeting the cancer immune system is a waste of time. On top of that, Interleukins, which are cytokines and a component of this drug, have been tried for decades and decades in clinical trials for cancers. All of them have had weak results, always with the glimmer of hope, but somehow never panning out despite trial after trial. My personal hypothesis is that the trial setup has been all wrong on these for decades, combinatorial therapies should have been tested long ago. I have no idea if Multikine is what CVM says it is, I am not an immunologist and my basic understanding of this aspect of biology is weak and limited to RNA defense stuff. Summarily, I won't be surprised if this works.

Cancer and the immune system is the trillion dollar question right now. There have been some brilliant people investigating this for longer than I have been alive. There just may be brilliant people investigating this for longer than I will be alive. I can't answer specifics, especially specifics we don't know, but I can give you this: the way cancer uses and abuses the immune system varies over time, over need and over tissue type, the specifics are messy and will bog you down, all to boil down to this: the immune system has lost it's ability to identify or fight against a foreign and maligned organism (the cancer cell). By activating the immune system in every single way, the way Multikine hypothetically does, might just overload all the different defense mechanisms the cancer has to evade or trick the immune system.

One of the neat things about Interleukins and the research on them, is this stall effect they cause on cells that has been shown to lead to healthier and longer proliferation. The idea behind this being that the cell senses a problem, Interleukin is literally a red letter screaming problem across the cell, and the cell stops trying to proliferate, it does a check on everything. This has the possibility of causing a brief replication pause in the cancer cell, giving the immune system time to identify the cancer cell when it is unable to perform some of its tricks (a replication halt in G2/M phase should stop most transcriptome changes, some that might be very important in immune system evasion). Now the bad thing is sometimes cancer likes the pause, and depending on the length of time between a replication halt from a cytokine storm, and chemotherapies or radiation therapies; this has the potential to impact potential treatments in various cancer backgrounds.

Nothing in the science of Multikine is specific to head and neck cancers, so if CVM get this for head and neck, expect a massive push into other cancers, especially those without a reasonable standard of care.

The Company & The Financials

Don't even look here, it doesn't matter. The company is nothing without Multikine. They have a few preclinical programs, but if Multikine fails the game is over. Financials wise, it has 40M cash and nothing of interest.

I believe ownership % is important. The top institutional owners are Blackrock, Vanguard and State Street, all with just over 6 million shares combined. 30% institutional ownership, 38 million float, >15% short interest.

I cannot speak to the quality of the company and executives, but if you go to yahoo finance, key execs for CVM are mostly scientists. This is super bullish for me. Science should lead science, not business.

The History

I think it is important to note, and at the very least make you aware of the following:

A subreddit dedicated to CVM

Various communities with some strong opinions on shorts (google kill the shorts cvm)

With that said, I did not read through those locales, if you are interested in this stock, you might want to so you can be aware of what is going on in the periphery.

The End

As always, do your own due diligence and research. I know nothing. Please leave feedback, criticisms, suggestions. Thanks.

CVM Short Squeeze PossibleHigh short float

double top on price chart

tightening range of price

Ascending triangle

CVM F'n BullishShort term trend lines are crossing over as did the MACD. The RSI is still low considering the move up in the last week or so.

Yesterday's candle tested 3 fibonacci levels to close near the hod and above the .61 fib level. In addition the current price is still relatively close to the POC line (YTD)

I anticipating a strong move to the upside based on the chart and also in anticipation of data release.

Short term target: 27.86

**Disclosure: this is my favorite stock and I am long AF**

CVM Break OutCVM gapped up slightly at the open and managed to close above the descending trend line after testing the .382 fib level.

MACD cross is very bullish and the RSI is still on the cool side.

Break of 24.28 gets us to 25.79.

Short term targets $27.31, 29.48, 32.25 all likely before data imo.

Good Data sends this through the roof.

mid term +17,000%CEL-SCI Corporation engages in the research and development of immunotherapy for the treatment of cancer and infectious diseases.

BullishCVM closed at the .78 fibonacci level after briefly breaking higher. The MACD is positive and the RSI is still relatively cool at 62.

With a major catalyst due any day now this looks like it wants to run to prior highs.

Targeting $21.72, $26.56 in the short term.

CVM BULLISH AFSeveral reasons to be excited about this chart:

1. MACD cross imminent

2. Recent test of 200 sma and 13.85 level

3. 70% of vol YTD was traded at higher prices

4. Test of the .78 fib level

5. RSI still low

Short term targets: 18.74, 21.79 then 26,72

Likely considerably higher by 4/15/21

disclosure: Super long CVM. Its my favorite stock.